BUS5ATE Semester 1: Statistical Replication & Stock Market Analysis

VerifiedAdded on 2023/06/13

|18

|3781

|325

Report

AI Summary

This report presents a statistical replication and analysis of research on the FIFA World Cup's effect on the U.S. stock market. The original study, by Kaplanski and Levi, suggests that investor sentiment, influenced by the outcomes of World Cup matches, affects stock market returns. Losing, in particular, has a negative impact. The replication employs ordinary least squares regression and ANOVA in R to analyze the relationship between stock returns and various factors, including event days and dummy variables. The analysis confirms a statistically significant relationship between world cup events and stock market returns, supporting the idea that major sports events can influence investor behavior. This website provides access to past papers and solved assignments for students seeking further insights.

1

RUNNING HEAD: Research Statistical Replication and Analysis

SUMMARY

There are many factors influencing the stock market, these include events as unimagined as

sports and even obvious ones such as war. Generally, there is a relationship between change in

stock prices and investor sentiment. This is as demonstrated by Guy Kaplanski and Levi in their

paper on “Exploitable Predictable Irrationality” taking into account the FIFA world cup event.

( Kaplanski & Levi. 2010. Pp 535-553)

In the paper, the writers argue that losing and winning often shift the investor sentiment, which

in the end affect their investment decisions. Naturally, there is only a single winner out of every

football match encounter and therefore after every game the stock market gets affected.

To investigate this hypothesis, an ideal neutral market is chosen, in this case the US stock

market. This is due to its versatility of global investors and therefore all the games played in the

world cup are likely to affect it. In their findings, a conclusion that losing affects the stock

market negatively whereas the effect of winning is negligible.

One of the main hypotheses is that losing instigates a negative effect by the fans whose countries

lose. To test this, three methods are employed, i.e.:

i. Theoretical, independent of match results

ii. Comparing average returns on the stock market, given that during the game period. On

about 30 teams lose.

iii. Technical analysis, through use of exact data to determine relationship in stock market

and sporting periods

RUNNING HEAD: Research Statistical Replication and Analysis

SUMMARY

There are many factors influencing the stock market, these include events as unimagined as

sports and even obvious ones such as war. Generally, there is a relationship between change in

stock prices and investor sentiment. This is as demonstrated by Guy Kaplanski and Levi in their

paper on “Exploitable Predictable Irrationality” taking into account the FIFA world cup event.

( Kaplanski & Levi. 2010. Pp 535-553)

In the paper, the writers argue that losing and winning often shift the investor sentiment, which

in the end affect their investment decisions. Naturally, there is only a single winner out of every

football match encounter and therefore after every game the stock market gets affected.

To investigate this hypothesis, an ideal neutral market is chosen, in this case the US stock

market. This is due to its versatility of global investors and therefore all the games played in the

world cup are likely to affect it. In their findings, a conclusion that losing affects the stock

market negatively whereas the effect of winning is negligible.

One of the main hypotheses is that losing instigates a negative effect by the fans whose countries

lose. To test this, three methods are employed, i.e.:

i. Theoretical, independent of match results

ii. Comparing average returns on the stock market, given that during the game period. On

about 30 teams lose.

iii. Technical analysis, through use of exact data to determine relationship in stock market

and sporting periods

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Research Statistical Replication and Analysis

In brief, the paper focuses on sentimental influence on the investment decisions made by

investors. Not only on local stock markets but also on international markets.

The major points drawn include:

i. US market has large number of investors compared to other markets

ii. Sentiments affect investor decisions, hence stock market. Hence there is a relationship

between stock market and investor sentiment

iii. Losing of country teams affects the stock market rather adversely

iv. Winning has a negligible positive effect

Research Statistical Replication and Analysis

In brief, the paper focuses on sentimental influence on the investment decisions made by

investors. Not only on local stock markets but also on international markets.

The major points drawn include:

i. US market has large number of investors compared to other markets

ii. Sentiments affect investor decisions, hence stock market. Hence there is a relationship

between stock market and investor sentiment

iii. Losing of country teams affects the stock market rather adversely

iv. Winning has a negligible positive effect

3

Research Statistical Replication and Analysis

CRITICAL EVALUATION

Several scholars have carried out research in order to answer the question of whether there is a

relationship between investor sentiment and investments. There have been a number of

researches conducted such as:

i. Investor sentiment and stock returns (Fisher & Meir. 2000)

ii. Sports sentiment and stock market returns (Sevil & Polat. 2015)

All these articles and many others seek to answer the same question as that rose in the research.

It is therefore important to determine the factors that influence the investor decision since it is

through this that the market may be modeled for prediction. Interestingly, games are among

instigators for sentiments, this is due to the loyalty attached to a particular team and even more

the spirit of nationalism. Therefore, the research question is important in contributing to the

learning of the mindset of the investor in relation to stock returns.

The research process is designed into six sections, each covering a specific aspect to consolidate

the whole research process, i.e.:

i. Introduction

ii. Background to the research motivation

iii. Methodology used in the research process

iv. Results and interpretations

v. Recommendations based on the results

vi. Conclusion

Research Statistical Replication and Analysis

CRITICAL EVALUATION

Several scholars have carried out research in order to answer the question of whether there is a

relationship between investor sentiment and investments. There have been a number of

researches conducted such as:

i. Investor sentiment and stock returns (Fisher & Meir. 2000)

ii. Sports sentiment and stock market returns (Sevil & Polat. 2015)

All these articles and many others seek to answer the same question as that rose in the research.

It is therefore important to determine the factors that influence the investor decision since it is

through this that the market may be modeled for prediction. Interestingly, games are among

instigators for sentiments, this is due to the loyalty attached to a particular team and even more

the spirit of nationalism. Therefore, the research question is important in contributing to the

learning of the mindset of the investor in relation to stock returns.

The research process is designed into six sections, each covering a specific aspect to consolidate

the whole research process, i.e.:

i. Introduction

ii. Background to the research motivation

iii. Methodology used in the research process

iv. Results and interpretations

v. Recommendations based on the results

vi. Conclusion

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Research Statistical Replication and Analysis

The study design is a standard research procedure; therefore, it captures most of the research

aspects. However, inclusion of the areas into which the research features would improve the

relevancy to the readers. I.e. explanation of the study context, hence it is sensible

The method on data analysis involves regression to determine the relationship presented among

the data variables; which include:

Date of investigated events

Return on stock

Influential variables i.e. dummy variables

The research involves multiple regressions i.e. Ri= Yo+ βXi + £I where R is the daily stock

returns, Y correlation coefficient intercept and Xi are the independent variables robustness check

and visual graphing, which is adequate to investigate multiple relations between interest

variables and in carrying out data interpretation. This enables to establish the significant factors.

The process of data analysis and output processing was done using Eview software.

Interestingly, despite the indirect relation between football and stock in America, the research

pitches the economic specification to determine stock trends during world cup events. In the

American stock market, this is because, according to the authors the fact that approximately a

third of the companies quoted in the stock market are foreign and therefore the stock market is

most likely to be influenced by foreign investor decisions. Therefore

In application of mathematics and statistics to economics, the authors set up an economic model

used to show the effect of football sport during world cup events in a period after the Second

Research Statistical Replication and Analysis

The study design is a standard research procedure; therefore, it captures most of the research

aspects. However, inclusion of the areas into which the research features would improve the

relevancy to the readers. I.e. explanation of the study context, hence it is sensible

The method on data analysis involves regression to determine the relationship presented among

the data variables; which include:

Date of investigated events

Return on stock

Influential variables i.e. dummy variables

The research involves multiple regressions i.e. Ri= Yo+ βXi + £I where R is the daily stock

returns, Y correlation coefficient intercept and Xi are the independent variables robustness check

and visual graphing, which is adequate to investigate multiple relations between interest

variables and in carrying out data interpretation. This enables to establish the significant factors.

The process of data analysis and output processing was done using Eview software.

Interestingly, despite the indirect relation between football and stock in America, the research

pitches the economic specification to determine stock trends during world cup events. In the

American stock market, this is because, according to the authors the fact that approximately a

third of the companies quoted in the stock market are foreign and therefore the stock market is

most likely to be influenced by foreign investor decisions. Therefore

In application of mathematics and statistics to economics, the authors set up an economic model

used to show the effect of football sport during world cup events in a period after the Second

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Research Statistical Replication and Analysis

World War and 2006. The model specification includes outliers so as to be realistic and in line

with real life situation.

Model:

Ri= yo + ∑

1

2

y1iRi-1+ ∑

1

4

y2iDii+y3Hi + y4Ti + y5Pi+ y6Ei + ∑

1

2

y7iJii+ ɛi

Where ( Rt =daily return,Y0= regression intercept coefficient, Rt-1, Rt-2 =

1st and 2nd preceding day returns, Dit , [1,2,3,4], are dummy days of the week: Monday, Tuesday,

Wednesday, and Thursday,10 Ht is a dummy variable for days after a non-weekend holiday and

Tt is a dummy for first five days of taxation year, Pt is a dummy variable for the world cup

(June–July) event.) (Kaplanski & Levi, 2010. Pp 545).

The authors carry out a sensitivity analysis through:

i. Explaining the association between the inputted and outputted variables

ii. Simplifying the regression model to remove insignificant structure parts

iii. Lowering uncertainty by identifying the inputs

iv. Locating errors in the model

v. Testing model robustness

vi. Investigating key connections in the observations and forecasts

Therefore, the researchers carry out adequate sensitivity analysis.

After testing the null hypothesis, carrying out analysis and interpretation of the output, the

authors find a relationship between stock prices during the world cup events and the winning or

losing of teams. Therefore, they conclude that the world cup effect is:

Large

Research Statistical Replication and Analysis

World War and 2006. The model specification includes outliers so as to be realistic and in line

with real life situation.

Model:

Ri= yo + ∑

1

2

y1iRi-1+ ∑

1

4

y2iDii+y3Hi + y4Ti + y5Pi+ y6Ei + ∑

1

2

y7iJii+ ɛi

Where ( Rt =daily return,Y0= regression intercept coefficient, Rt-1, Rt-2 =

1st and 2nd preceding day returns, Dit , [1,2,3,4], are dummy days of the week: Monday, Tuesday,

Wednesday, and Thursday,10 Ht is a dummy variable for days after a non-weekend holiday and

Tt is a dummy for first five days of taxation year, Pt is a dummy variable for the world cup

(June–July) event.) (Kaplanski & Levi, 2010. Pp 545).

The authors carry out a sensitivity analysis through:

i. Explaining the association between the inputted and outputted variables

ii. Simplifying the regression model to remove insignificant structure parts

iii. Lowering uncertainty by identifying the inputs

iv. Locating errors in the model

v. Testing model robustness

vi. Investigating key connections in the observations and forecasts

Therefore, the researchers carry out adequate sensitivity analysis.

After testing the null hypothesis, carrying out analysis and interpretation of the output, the

authors find a relationship between stock prices during the world cup events and the winning or

losing of teams. Therefore, they conclude that the world cup effect is:

Large

6

Research Statistical Replication and Analysis

Highly significant

Long-lasting

Such that the average return during the event is -2.58%, compared to normal days on the same

period when returns average on +1.21%.

This conclusion is sensible and is important in determining when to buy and sell stocks as major

sports events happen, it also suggests balancing on stocks bought to avoid bad losses during

world cup event.

Research Statistical Replication and Analysis

Highly significant

Long-lasting

Such that the average return during the event is -2.58%, compared to normal days on the same

period when returns average on +1.21%.

This conclusion is sensible and is important in determining when to buy and sell stocks as major

sports events happen, it also suggests balancing on stocks bought to avoid bad losses during

world cup event.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

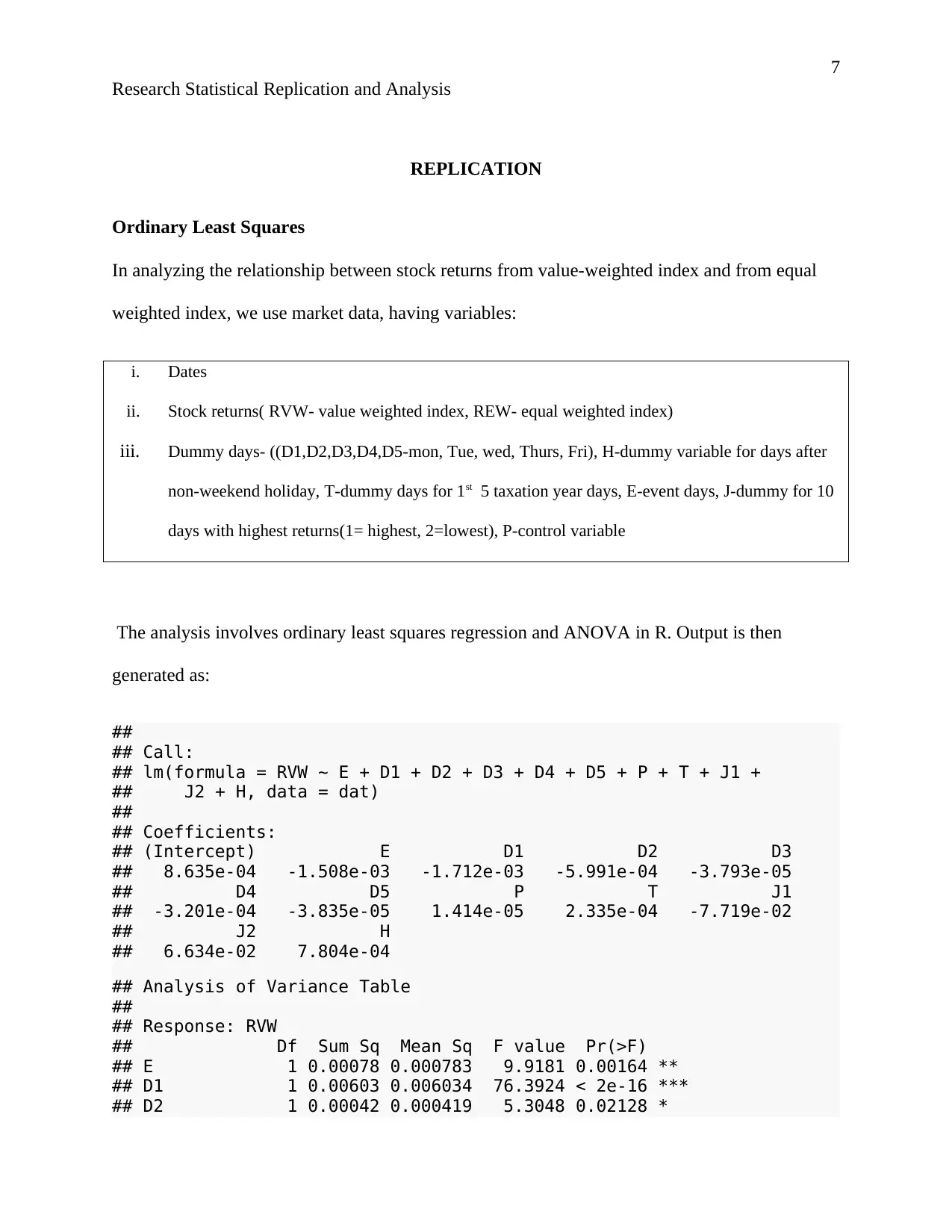

Research Statistical Replication and Analysis

REPLICATION

Ordinary Least Squares

In analyzing the relationship between stock returns from value-weighted index and from equal

weighted index, we use market data, having variables:

i. Dates

ii. Stock returns( RVW- value weighted index, REW- equal weighted index)

iii. Dummy days- ((D1,D2,D3,D4,D5-mon, Tue, wed, Thurs, Fri), H-dummy variable for days after

non-weekend holiday, T-dummy days for 1st 5 taxation year days, E-event days, J-dummy for 10

days with highest returns(1= highest, 2=lowest), P-control variable

The analysis involves ordinary least squares regression and ANOVA in R. Output is then

generated as:

##

## Call:

## lm(formula = RVW ~ E + D1 + D2 + D3 + D4 + D5 + P + T + J1 +

## J2 + H, data = dat)

##

## Coefficients:

## (Intercept) E D1 D2 D3

## 8.635e-04 -1.508e-03 -1.712e-03 -5.991e-04 -3.793e-05

## D4 D5 P T J1

## -3.201e-04 -3.835e-05 1.414e-05 2.335e-04 -7.719e-02

## J2 H

## 6.634e-02 7.804e-04

## Analysis of Variance Table

##

## Response: RVW

## Df Sum Sq Mean Sq F value Pr(>F)

## E 1 0.00078 0.000783 9.9181 0.00164 **

## D1 1 0.00603 0.006034 76.3924 < 2e-16 ***

## D2 1 0.00042 0.000419 5.3048 0.02128 *

Research Statistical Replication and Analysis

REPLICATION

Ordinary Least Squares

In analyzing the relationship between stock returns from value-weighted index and from equal

weighted index, we use market data, having variables:

i. Dates

ii. Stock returns( RVW- value weighted index, REW- equal weighted index)

iii. Dummy days- ((D1,D2,D3,D4,D5-mon, Tue, wed, Thurs, Fri), H-dummy variable for days after

non-weekend holiday, T-dummy days for 1st 5 taxation year days, E-event days, J-dummy for 10

days with highest returns(1= highest, 2=lowest), P-control variable

The analysis involves ordinary least squares regression and ANOVA in R. Output is then

generated as:

##

## Call:

## lm(formula = RVW ~ E + D1 + D2 + D3 + D4 + D5 + P + T + J1 +

## J2 + H, data = dat)

##

## Coefficients:

## (Intercept) E D1 D2 D3

## 8.635e-04 -1.508e-03 -1.712e-03 -5.991e-04 -3.793e-05

## D4 D5 P T J1

## -3.201e-04 -3.835e-05 1.414e-05 2.335e-04 -7.719e-02

## J2 H

## 6.634e-02 7.804e-04

## Analysis of Variance Table

##

## Response: RVW

## Df Sum Sq Mean Sq F value Pr(>F)

## E 1 0.00078 0.000783 9.9181 0.00164 **

## D1 1 0.00603 0.006034 76.3924 < 2e-16 ***

## D2 1 0.00042 0.000419 5.3048 0.02128 *

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Research Statistical Replication and Analysis

## D3 1 0.00006 0.000061 0.7744 0.37888

## D4 1 0.00017 0.000175 2.2154 0.13666

## D5 1 0.00000 0.000000 0.0033 0.95426

## P 1 0.00000 0.000000 0.0024 0.96086

## T 1 0.00004 0.000036 0.4554 0.49977

## J1 1 0.05964 0.059638 755.0297 < 2e-16 ***

## J2 1 0.04394 0.043944 556.3389 < 2e-16 ***

## H 1 0.00026 0.000256 3.2358 0.07206 .

## Residuals 16807 1.32754 0.000079

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

## 2.5 % 97.5 %

## (Intercept) -1.004847e-03 0.0027317483

## E -2.502098e-03 -0.0005129705

## D1 -3.606291e-03 0.0001821602

## D2 -2.491652e-03 0.0012933780

## D3 -1.930377e-03 0.0018545201

## D4 -2.213003e-03 0.0015727626

## D5 -1.931203e-03 0.0018545055

## P -3.661584e-04 0.0003944327

## T -7.349165e-04 0.0012018505

## J1 -8.270597e-02 -0.0716831654

## J2 6.082491e-02 0.0718473372

## H -6.996404e-05 0.0016306675

##

## Call:

## lm(formula = RVW ~ E + D1 + D2 + D3 + D4 + D5 + P + T + J1 +

## J2 + H, data = dat)

##

## Residuals:

## Min 1Q Median 3Q Max

## -0.093379 -0.004051 0.000258 0.004377 0.080933

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 8.634e-04 9.532e-04 0.906 0.36501

## E -1.508e-03 5.074e-04 -2.971 0.00297 **

## D1 -1.712e-03 9.664e-04 -1.772 0.07648 .

## D2 -5.991e-04 9.655e-04 -0.621 0.53491

## D3 -3.793e-05 9.655e-04 -0.039 0.96866

## D4 -3.201e-04 9.657e-04 -0.331 0.74028

## D5 -3.835e-05 9.657e-04 -0.040 0.96832

## P 1.414e-05 1.940e-04 0.073 0.94191

## T 2.335e-04 4.941e-04 0.473 0.63653

## J1 -7.719e-02 2.812e-03 -27.454 < 2e-16 ***

## J2 6.634e-02 2.812e-03 23.593 < 2e-16 ***

## H 7.803e-04 4.338e-04 1.799 0.07206 .

## ---

Research Statistical Replication and Analysis

## D3 1 0.00006 0.000061 0.7744 0.37888

## D4 1 0.00017 0.000175 2.2154 0.13666

## D5 1 0.00000 0.000000 0.0033 0.95426

## P 1 0.00000 0.000000 0.0024 0.96086

## T 1 0.00004 0.000036 0.4554 0.49977

## J1 1 0.05964 0.059638 755.0297 < 2e-16 ***

## J2 1 0.04394 0.043944 556.3389 < 2e-16 ***

## H 1 0.00026 0.000256 3.2358 0.07206 .

## Residuals 16807 1.32754 0.000079

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

## 2.5 % 97.5 %

## (Intercept) -1.004847e-03 0.0027317483

## E -2.502098e-03 -0.0005129705

## D1 -3.606291e-03 0.0001821602

## D2 -2.491652e-03 0.0012933780

## D3 -1.930377e-03 0.0018545201

## D4 -2.213003e-03 0.0015727626

## D5 -1.931203e-03 0.0018545055

## P -3.661584e-04 0.0003944327

## T -7.349165e-04 0.0012018505

## J1 -8.270597e-02 -0.0716831654

## J2 6.082491e-02 0.0718473372

## H -6.996404e-05 0.0016306675

##

## Call:

## lm(formula = RVW ~ E + D1 + D2 + D3 + D4 + D5 + P + T + J1 +

## J2 + H, data = dat)

##

## Residuals:

## Min 1Q Median 3Q Max

## -0.093379 -0.004051 0.000258 0.004377 0.080933

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 8.634e-04 9.532e-04 0.906 0.36501

## E -1.508e-03 5.074e-04 -2.971 0.00297 **

## D1 -1.712e-03 9.664e-04 -1.772 0.07648 .

## D2 -5.991e-04 9.655e-04 -0.621 0.53491

## D3 -3.793e-05 9.655e-04 -0.039 0.96866

## D4 -3.201e-04 9.657e-04 -0.331 0.74028

## D5 -3.835e-05 9.657e-04 -0.040 0.96832

## P 1.414e-05 1.940e-04 0.073 0.94191

## T 2.335e-04 4.941e-04 0.473 0.63653

## J1 -7.719e-02 2.812e-03 -27.454 < 2e-16 ***

## J2 6.634e-02 2.812e-03 23.593 < 2e-16 ***

## H 7.803e-04 4.338e-04 1.799 0.07206 .

## ---

9

Research Statistical Replication and Analysis

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 0.008887 on 16807 degrees of freedom

## Multiple R-squared: 0.07738, Adjusted R-squared: 0.07678

## F-statistic: 128.2 on 11 and 16807 DF, p-value: < 2.2e-16

##

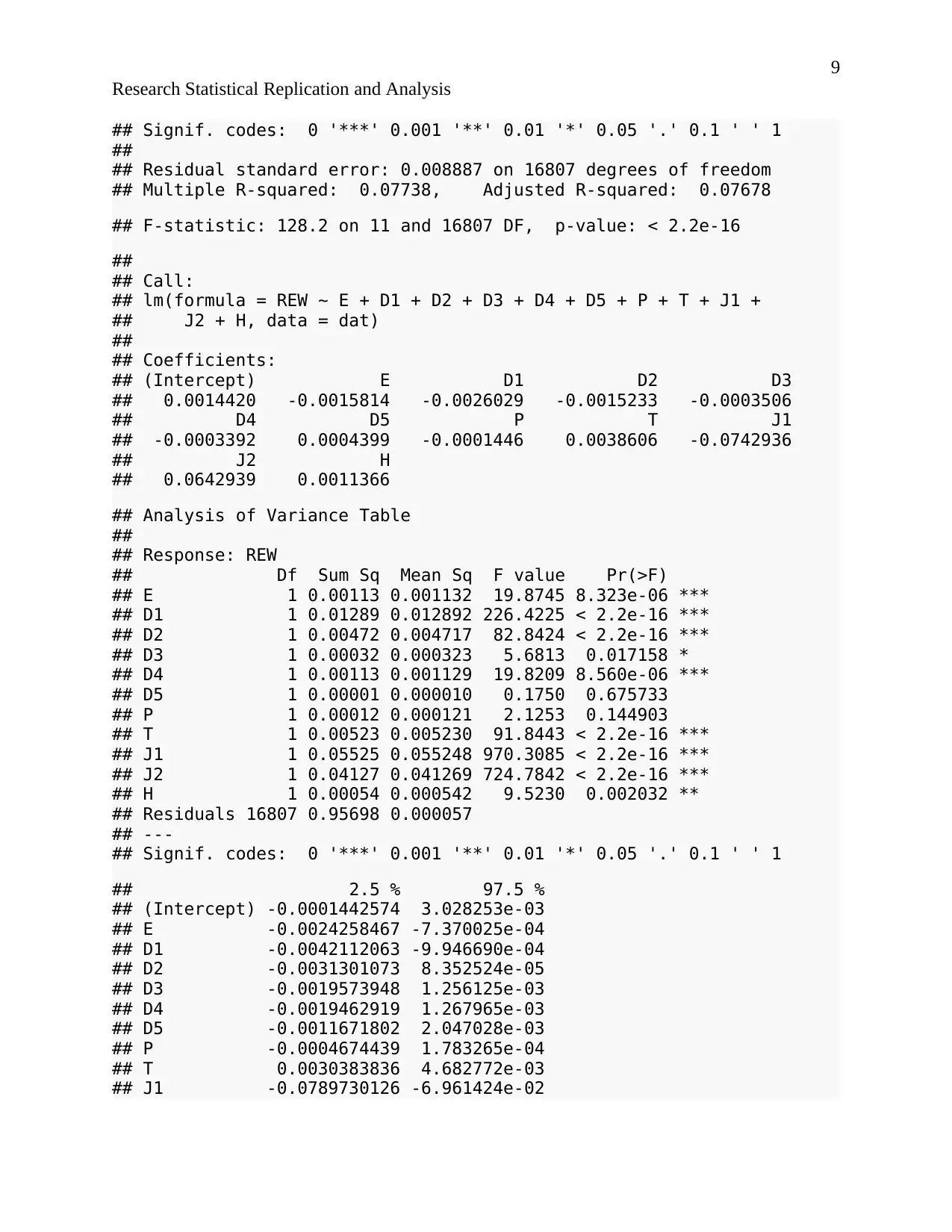

## Call:

## lm(formula = REW ~ E + D1 + D2 + D3 + D4 + D5 + P + T + J1 +

## J2 + H, data = dat)

##

## Coefficients:

## (Intercept) E D1 D2 D3

## 0.0014420 -0.0015814 -0.0026029 -0.0015233 -0.0003506

## D4 D5 P T J1

## -0.0003392 0.0004399 -0.0001446 0.0038606 -0.0742936

## J2 H

## 0.0642939 0.0011366

## Analysis of Variance Table

##

## Response: REW

## Df Sum Sq Mean Sq F value Pr(>F)

## E 1 0.00113 0.001132 19.8745 8.323e-06 ***

## D1 1 0.01289 0.012892 226.4225 < 2.2e-16 ***

## D2 1 0.00472 0.004717 82.8424 < 2.2e-16 ***

## D3 1 0.00032 0.000323 5.6813 0.017158 *

## D4 1 0.00113 0.001129 19.8209 8.560e-06 ***

## D5 1 0.00001 0.000010 0.1750 0.675733

## P 1 0.00012 0.000121 2.1253 0.144903

## T 1 0.00523 0.005230 91.8443 < 2.2e-16 ***

## J1 1 0.05525 0.055248 970.3085 < 2.2e-16 ***

## J2 1 0.04127 0.041269 724.7842 < 2.2e-16 ***

## H 1 0.00054 0.000542 9.5230 0.002032 **

## Residuals 16807 0.95698 0.000057

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

## 2.5 % 97.5 %

## (Intercept) -0.0001442574 3.028253e-03

## E -0.0024258467 -7.370025e-04

## D1 -0.0042112063 -9.946690e-04

## D2 -0.0031301073 8.352524e-05

## D3 -0.0019573948 1.256125e-03

## D4 -0.0019462919 1.267965e-03

## D5 -0.0011671802 2.047028e-03

## P -0.0004674439 1.783265e-04

## T 0.0030383836 4.682772e-03

## J1 -0.0789730126 -6.961424e-02

Research Statistical Replication and Analysis

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 0.008887 on 16807 degrees of freedom

## Multiple R-squared: 0.07738, Adjusted R-squared: 0.07678

## F-statistic: 128.2 on 11 and 16807 DF, p-value: < 2.2e-16

##

## Call:

## lm(formula = REW ~ E + D1 + D2 + D3 + D4 + D5 + P + T + J1 +

## J2 + H, data = dat)

##

## Coefficients:

## (Intercept) E D1 D2 D3

## 0.0014420 -0.0015814 -0.0026029 -0.0015233 -0.0003506

## D4 D5 P T J1

## -0.0003392 0.0004399 -0.0001446 0.0038606 -0.0742936

## J2 H

## 0.0642939 0.0011366

## Analysis of Variance Table

##

## Response: REW

## Df Sum Sq Mean Sq F value Pr(>F)

## E 1 0.00113 0.001132 19.8745 8.323e-06 ***

## D1 1 0.01289 0.012892 226.4225 < 2.2e-16 ***

## D2 1 0.00472 0.004717 82.8424 < 2.2e-16 ***

## D3 1 0.00032 0.000323 5.6813 0.017158 *

## D4 1 0.00113 0.001129 19.8209 8.560e-06 ***

## D5 1 0.00001 0.000010 0.1750 0.675733

## P 1 0.00012 0.000121 2.1253 0.144903

## T 1 0.00523 0.005230 91.8443 < 2.2e-16 ***

## J1 1 0.05525 0.055248 970.3085 < 2.2e-16 ***

## J2 1 0.04127 0.041269 724.7842 < 2.2e-16 ***

## H 1 0.00054 0.000542 9.5230 0.002032 **

## Residuals 16807 0.95698 0.000057

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

## 2.5 % 97.5 %

## (Intercept) -0.0001442574 3.028253e-03

## E -0.0024258467 -7.370025e-04

## D1 -0.0042112063 -9.946690e-04

## D2 -0.0031301073 8.352524e-05

## D3 -0.0019573948 1.256125e-03

## D4 -0.0019462919 1.267965e-03

## D5 -0.0011671802 2.047028e-03

## P -0.0004674439 1.783265e-04

## T 0.0030383836 4.682772e-03

## J1 -0.0789730126 -6.961424e-02

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

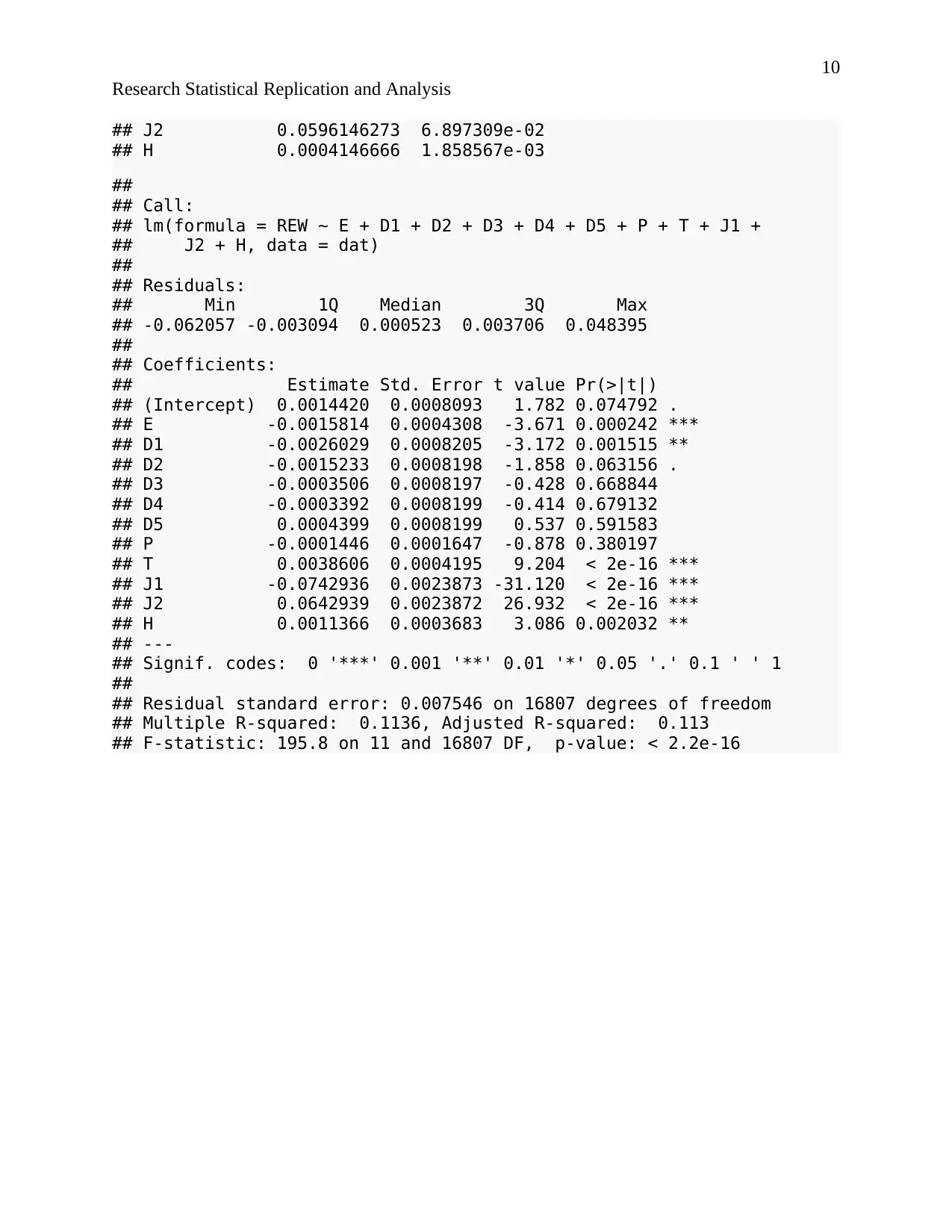

Research Statistical Replication and Analysis

## J2 0.0596146273 6.897309e-02

## H 0.0004146666 1.858567e-03

##

## Call:

## lm(formula = REW ~ E + D1 + D2 + D3 + D4 + D5 + P + T + J1 +

## J2 + H, data = dat)

##

## Residuals:

## Min 1Q Median 3Q Max

## -0.062057 -0.003094 0.000523 0.003706 0.048395

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 0.0014420 0.0008093 1.782 0.074792 .

## E -0.0015814 0.0004308 -3.671 0.000242 ***

## D1 -0.0026029 0.0008205 -3.172 0.001515 **

## D2 -0.0015233 0.0008198 -1.858 0.063156 .

## D3 -0.0003506 0.0008197 -0.428 0.668844

## D4 -0.0003392 0.0008199 -0.414 0.679132

## D5 0.0004399 0.0008199 0.537 0.591583

## P -0.0001446 0.0001647 -0.878 0.380197

## T 0.0038606 0.0004195 9.204 < 2e-16 ***

## J1 -0.0742936 0.0023873 -31.120 < 2e-16 ***

## J2 0.0642939 0.0023872 26.932 < 2e-16 ***

## H 0.0011366 0.0003683 3.086 0.002032 **

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 0.007546 on 16807 degrees of freedom

## Multiple R-squared: 0.1136, Adjusted R-squared: 0.113

## F-statistic: 195.8 on 11 and 16807 DF, p-value: < 2.2e-16

Research Statistical Replication and Analysis

## J2 0.0596146273 6.897309e-02

## H 0.0004146666 1.858567e-03

##

## Call:

## lm(formula = REW ~ E + D1 + D2 + D3 + D4 + D5 + P + T + J1 +

## J2 + H, data = dat)

##

## Residuals:

## Min 1Q Median 3Q Max

## -0.062057 -0.003094 0.000523 0.003706 0.048395

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 0.0014420 0.0008093 1.782 0.074792 .

## E -0.0015814 0.0004308 -3.671 0.000242 ***

## D1 -0.0026029 0.0008205 -3.172 0.001515 **

## D2 -0.0015233 0.0008198 -1.858 0.063156 .

## D3 -0.0003506 0.0008197 -0.428 0.668844

## D4 -0.0003392 0.0008199 -0.414 0.679132

## D5 0.0004399 0.0008199 0.537 0.591583

## P -0.0001446 0.0001647 -0.878 0.380197

## T 0.0038606 0.0004195 9.204 < 2e-16 ***

## J1 -0.0742936 0.0023873 -31.120 < 2e-16 ***

## J2 0.0642939 0.0023872 26.932 < 2e-16 ***

## H 0.0011366 0.0003683 3.086 0.002032 **

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 0.007546 on 16807 degrees of freedom

## Multiple R-squared: 0.1136, Adjusted R-squared: 0.113

## F-statistic: 195.8 on 11 and 16807 DF, p-value: < 2.2e-16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Research Statistical Replication and Analysis

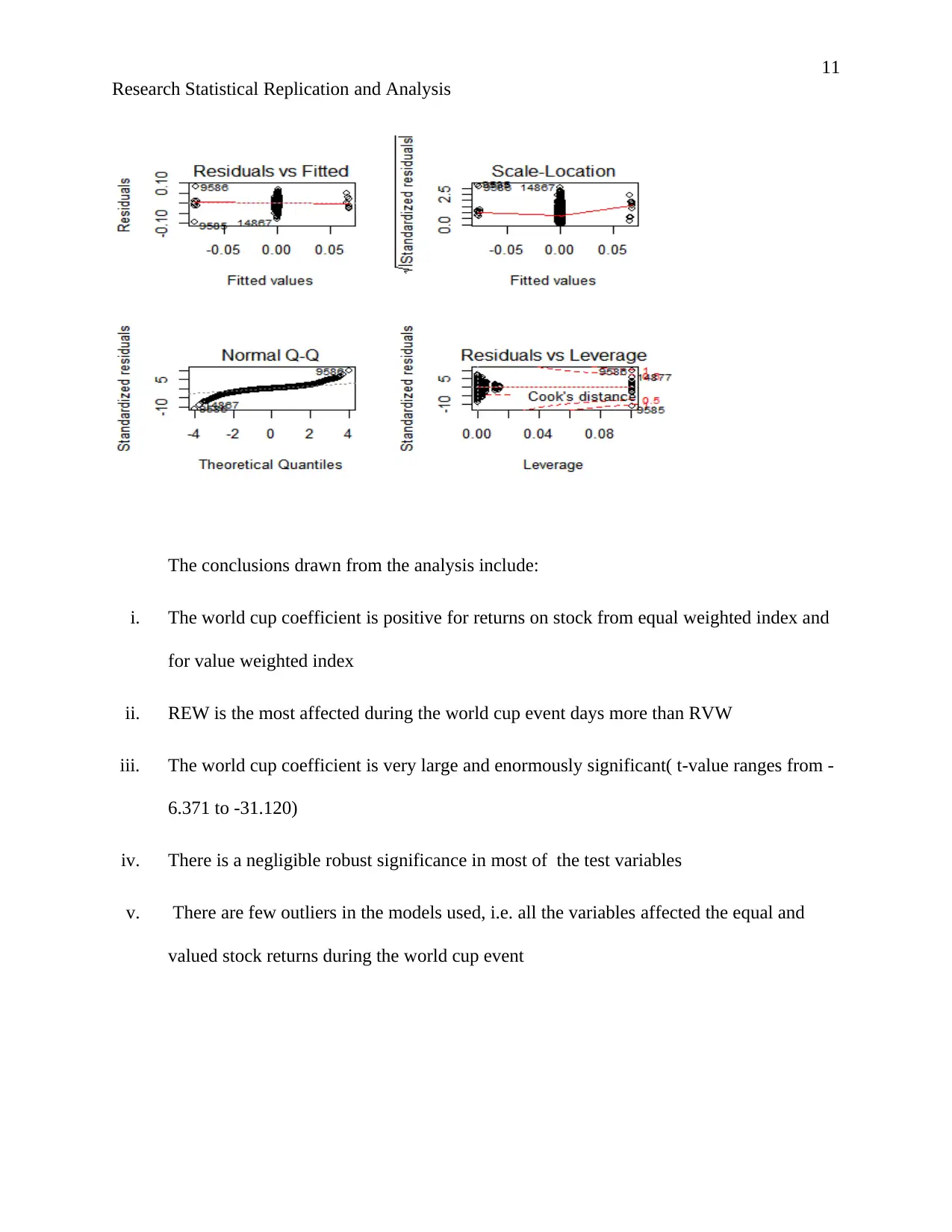

The conclusions drawn from the analysis include:

i. The world cup coefficient is positive for returns on stock from equal weighted index and

for value weighted index

ii. REW is the most affected during the world cup event days more than RVW

iii. The world cup coefficient is very large and enormously significant( t-value ranges from -

6.371 to -31.120)

iv. There is a negligible robust significance in most of the test variables

v. There are few outliers in the models used, i.e. all the variables affected the equal and

valued stock returns during the world cup event

Research Statistical Replication and Analysis

The conclusions drawn from the analysis include:

i. The world cup coefficient is positive for returns on stock from equal weighted index and

for value weighted index

ii. REW is the most affected during the world cup event days more than RVW

iii. The world cup coefficient is very large and enormously significant( t-value ranges from -

6.371 to -31.120)

iv. There is a negligible robust significance in most of the test variables

v. There are few outliers in the models used, i.e. all the variables affected the equal and

valued stock returns during the world cup event

12

Research Statistical Replication and Analysis

FURTHER ANALYSIS

Do Olympic Games affect market returns

Economic theorists often argue that major multiregional boost local economies of the host

countries, this includes:

i. International games such as world cup and Olympics

ii. Trade conventions

iii. Democratic national conventions

This is suggested to be due to a gush in the economic activities connected to the event. (Ross.

2018) . Previous research shows that when a country wins an Olympic medal, national stock

activity decreases (Jessica & Markellos, 2018).

The suggested reasons infer that games distract both the public and investors alike. The main

hypothesis is that Olympic games affect the stock market of the host country and the

international markets of other countries participating in the event. Our null hypothesis is that

Olympic Games do not affect the stock market and that stock markets are independent of

investor swayed sentiments.

Research Statistical Replication and Analysis

FURTHER ANALYSIS

Do Olympic Games affect market returns

Economic theorists often argue that major multiregional boost local economies of the host

countries, this includes:

i. International games such as world cup and Olympics

ii. Trade conventions

iii. Democratic national conventions

This is suggested to be due to a gush in the economic activities connected to the event. (Ross.

2018) . Previous research shows that when a country wins an Olympic medal, national stock

activity decreases (Jessica & Markellos, 2018).

The suggested reasons infer that games distract both the public and investors alike. The main

hypothesis is that Olympic games affect the stock market of the host country and the

international markets of other countries participating in the event. Our null hypothesis is that

Olympic Games do not affect the stock market and that stock markets are independent of

investor swayed sentiments.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.