BUS707 - Accountants and Auditors Responsibilities in Governance

VerifiedAdded on 2022/09/26

|4

|1755

|21

Report

AI Summary

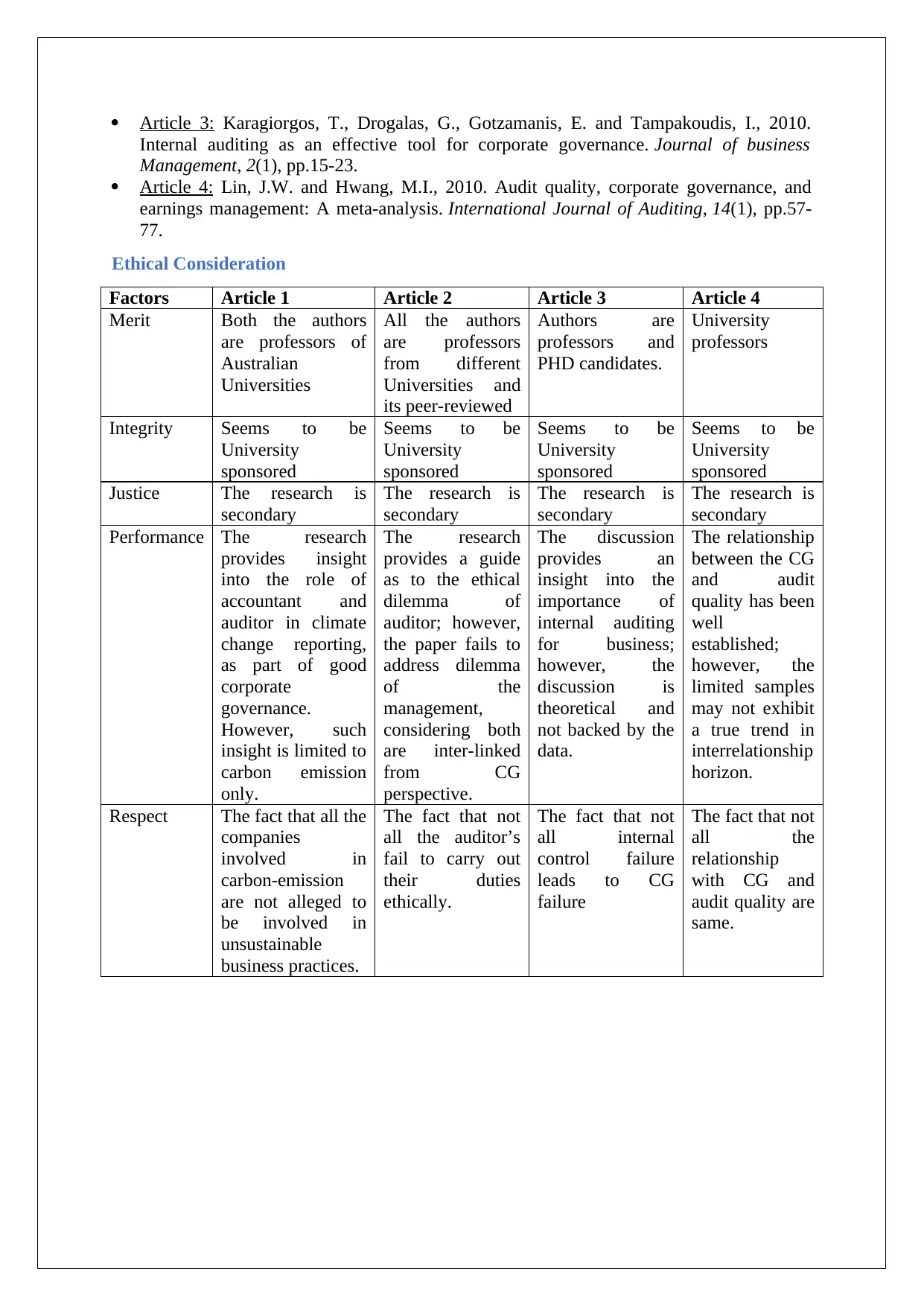

This research paper investigates the responsibilities and contributions of accountants and auditors towards corporate governance, focusing on their roles in ensuring efficient corporate reporting and sustainable business practices. It addresses the research question of how accountants and auditors contribute to corporate governance by identifying their individual roles and the interrelationship between them. The literature review highlights instances where failures in accounting and auditing have led to corporate collapses, emphasizing the importance of a strong corporate governance structure. The paper also discusses the ethical considerations involved in accounting and auditing, referencing key articles and their publication details. Ultimately, the report underscores the critical role of both accountants and auditors, along with effective leadership, in fostering a smooth accounting and auditing process within a well-designed corporate governance strategy.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.