University Tax Lodgement Analysis: BUS708 Statistics Report

VerifiedAdded on 2020/05/16

|13

|2166

|214

Report

AI Summary

This report analyzes tax lodgement preferences in Australia, drawing on data from the Australian Taxation Office (ATO) and a subset of 1000 individuals from the 2013-2014 dataset. The study investigates the proportion of people preferring tax agents over self-lodgement, examining factors such as age group, total income, and total deductions. The analysis includes both Australian residents and international students, employing statistical methods like confidence intervals, chi-square tests, and regression analysis. Key findings reveal a strong preference for tax agents across all age groups and income levels, with a significant association between age range and lodgement method. Furthermore, the report establishes a positive correlation between total income and total deduction amounts, providing insights into the financial aspects of tax lodgement. The report also provides insights into the preferences of international students. The report concludes by emphasizing the importance of tax agents and the factors influencing tax filing behavior.

Running Head: BUS708 STATISTICS AND DATA ANALYSIS

BUS708 Statistics and Data Analysis

Name of the Student

Name of the University

Author Note

BUS708 Statistics and Data Analysis

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUS708 STATISTICS AND DATA ANALYSIS

Table of Contents

Introduction.................................................................................................................................................2

Lodgement Method: Dataset 1....................................................................................................................2

Lodgement Method: Dataset 2....................................................................................................................3

Lodgement Method and Age Group............................................................................................................5

Lodgement Method and Total Income Amount..........................................................................................7

Total Income Amount and Total Deduction Amount...................................................................................9

Conclusion.................................................................................................................................................10

References.................................................................................................................................................11

Table of Contents

Introduction.................................................................................................................................................2

Lodgement Method: Dataset 1....................................................................................................................2

Lodgement Method: Dataset 2....................................................................................................................3

Lodgement Method and Age Group............................................................................................................5

Lodgement Method and Total Income Amount..........................................................................................7

Total Income Amount and Total Deduction Amount...................................................................................9

Conclusion.................................................................................................................................................10

References.................................................................................................................................................11

2BUS708 STATISTICS AND DATA ANALYSIS

Introduction

Lodgement of tax returns is an important thing that every individual belonging to any nation

must do. The same thing has to be done by the people in Australia. A lot of people fall under the income

range of taxable income and they have to lodge their tax returns. This can be in two different ways in

Australia. They can Lodge with the help of registered tax agents or can prepare their lodgements by

themselves. Previous studies showed that people prefer appointing tax agents for the lodgements

(Braithwaite 2017). The main aim of this study is to evaluate the proportion of people preferring tax

agents over themselves. This proportion will be tested on the basis of various factors such as age group,

Total income and total deduction.

To conduct this study, data has been collected from the Australian Taxation Office (ATO). A

subset of 1000 people from the dataset of 2013-2014 has been collected. This data is Secondary data as

it is collected from the website. The variables present in this dataset are given as follows:

Gender: Categorical Variable

Age Range: Categorical Variable

Lodgement Method: Categorical Variable

Total Income Amount:Quantitative Variable

Total Deduction Amount: Quantitative Variable

The first five cases of the dataset are attached in the following table 1

Table 1: First five cases of ATO Dataset

Along with evaluating the preference of the Australian people, the preference of the

international students also had to be evaluated. For this purpose, data has been collected from some

students about their preferences. Thus, this data is known as primary data as it is collected directly from

the students.

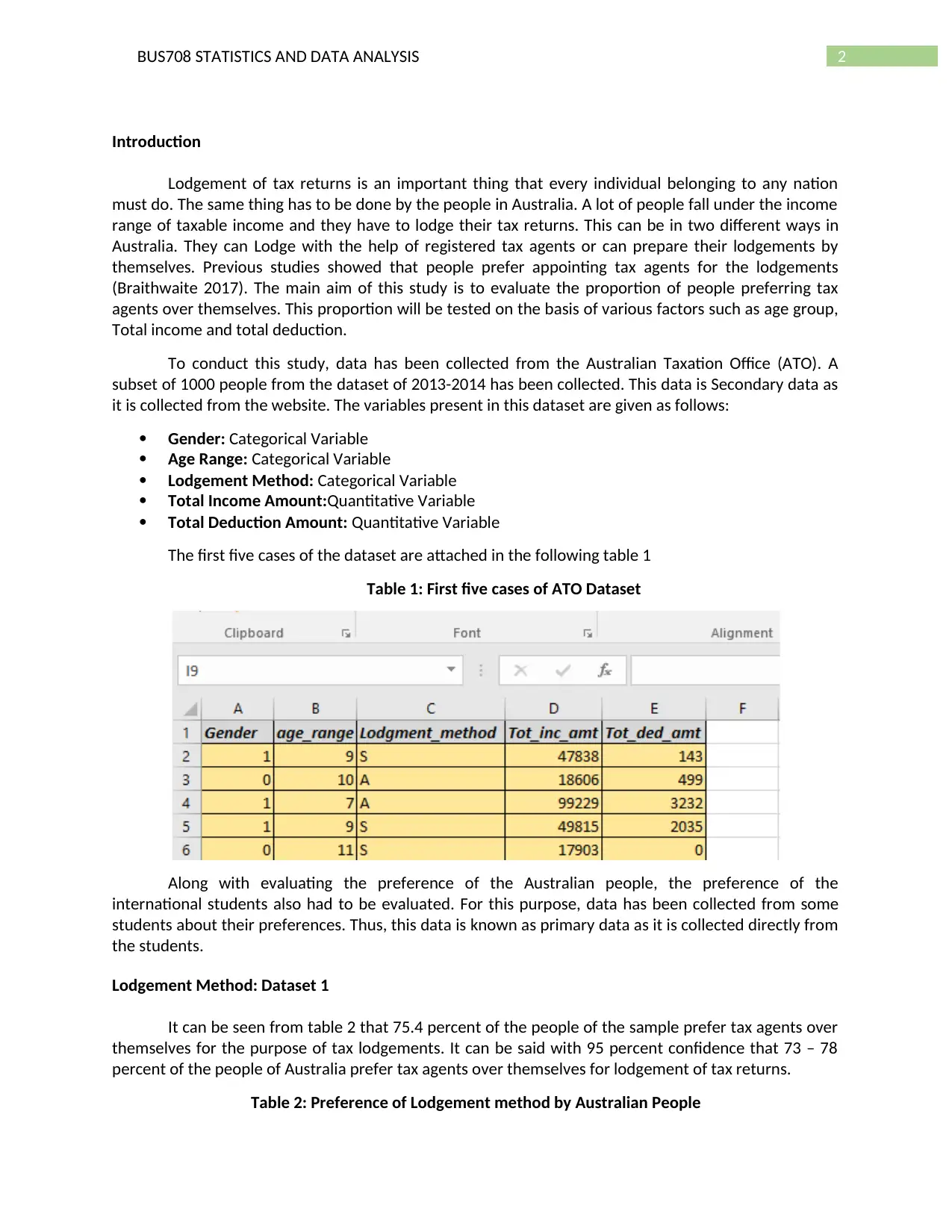

Lodgement Method: Dataset 1

It can be seen from table 2 that 75.4 percent of the people of the sample prefer tax agents over

themselves for the purpose of tax lodgements. It can be said with 95 percent confidence that 73 – 78

percent of the people of Australia prefer tax agents over themselves for lodgement of tax returns.

Table 2: Preference of Lodgement method by Australian People

Introduction

Lodgement of tax returns is an important thing that every individual belonging to any nation

must do. The same thing has to be done by the people in Australia. A lot of people fall under the income

range of taxable income and they have to lodge their tax returns. This can be in two different ways in

Australia. They can Lodge with the help of registered tax agents or can prepare their lodgements by

themselves. Previous studies showed that people prefer appointing tax agents for the lodgements

(Braithwaite 2017). The main aim of this study is to evaluate the proportion of people preferring tax

agents over themselves. This proportion will be tested on the basis of various factors such as age group,

Total income and total deduction.

To conduct this study, data has been collected from the Australian Taxation Office (ATO). A

subset of 1000 people from the dataset of 2013-2014 has been collected. This data is Secondary data as

it is collected from the website. The variables present in this dataset are given as follows:

Gender: Categorical Variable

Age Range: Categorical Variable

Lodgement Method: Categorical Variable

Total Income Amount:Quantitative Variable

Total Deduction Amount: Quantitative Variable

The first five cases of the dataset are attached in the following table 1

Table 1: First five cases of ATO Dataset

Along with evaluating the preference of the Australian people, the preference of the

international students also had to be evaluated. For this purpose, data has been collected from some

students about their preferences. Thus, this data is known as primary data as it is collected directly from

the students.

Lodgement Method: Dataset 1

It can be seen from table 2 that 75.4 percent of the people of the sample prefer tax agents over

themselves for the purpose of tax lodgements. It can be said with 95 percent confidence that 73 – 78

percent of the people of Australia prefer tax agents over themselves for lodgement of tax returns.

Table 2: Preference of Lodgement method by Australian People

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUS708 STATISTICS AND DATA ANALYSIS

Lodgement Method Frequency Percentage

A 754 75.40%

S 246 24.60%

Grand Total 1000 100%

75%

25%

Count of Lodgment_method

A

S

Figure 1: Pie Chart showing Preference of Lodgement methods by Australian People

Table 3: Confidence Interval for the proportion of Tax Agents preferred by Australian People

Sample Size 1000

Count of Successes 754

Confidence Level 95%

Sample Proportion 0.754

z Value 1.9600

Standard Error of the Proportion 0.013619251

Margin of Error 0.0267

Interval Lower Limit 72.73%

Interval Upper Limit 78.07%

Lodgement Method: Dataset 2

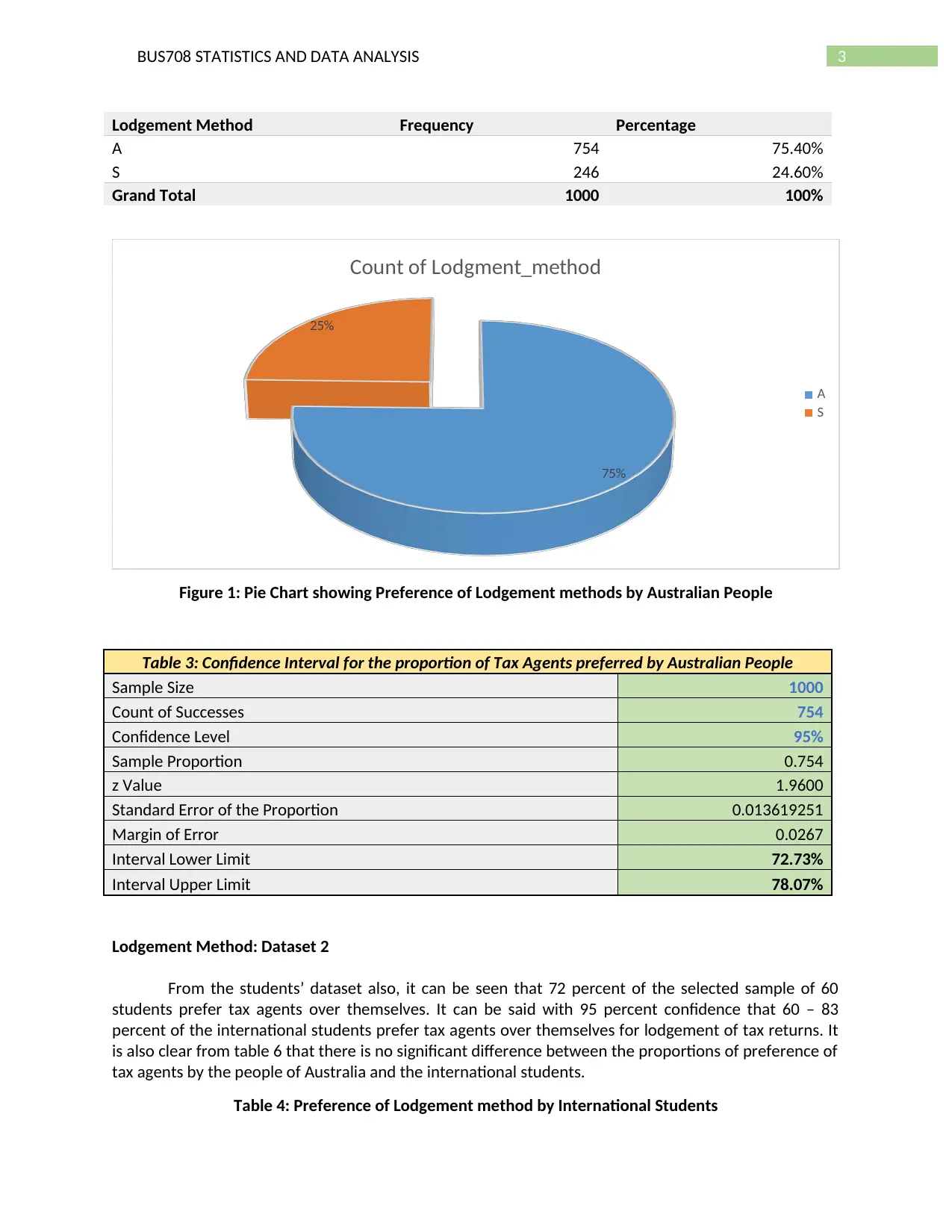

From the students’ dataset also, it can be seen that 72 percent of the selected sample of 60

students prefer tax agents over themselves. It can be said with 95 percent confidence that 60 – 83

percent of the international students prefer tax agents over themselves for lodgement of tax returns. It

is also clear from table 6 that there is no significant difference between the proportions of preference of

tax agents by the people of Australia and the international students.

Table 4: Preference of Lodgement method by International Students

Lodgement Method Frequency Percentage

A 754 75.40%

S 246 24.60%

Grand Total 1000 100%

75%

25%

Count of Lodgment_method

A

S

Figure 1: Pie Chart showing Preference of Lodgement methods by Australian People

Table 3: Confidence Interval for the proportion of Tax Agents preferred by Australian People

Sample Size 1000

Count of Successes 754

Confidence Level 95%

Sample Proportion 0.754

z Value 1.9600

Standard Error of the Proportion 0.013619251

Margin of Error 0.0267

Interval Lower Limit 72.73%

Interval Upper Limit 78.07%

Lodgement Method: Dataset 2

From the students’ dataset also, it can be seen that 72 percent of the selected sample of 60

students prefer tax agents over themselves. It can be said with 95 percent confidence that 60 – 83

percent of the international students prefer tax agents over themselves for lodgement of tax returns. It

is also clear from table 6 that there is no significant difference between the proportions of preference of

tax agents by the people of Australia and the international students.

Table 4: Preference of Lodgement method by International Students

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUS708 STATISTICS AND DATA ANALYSIS

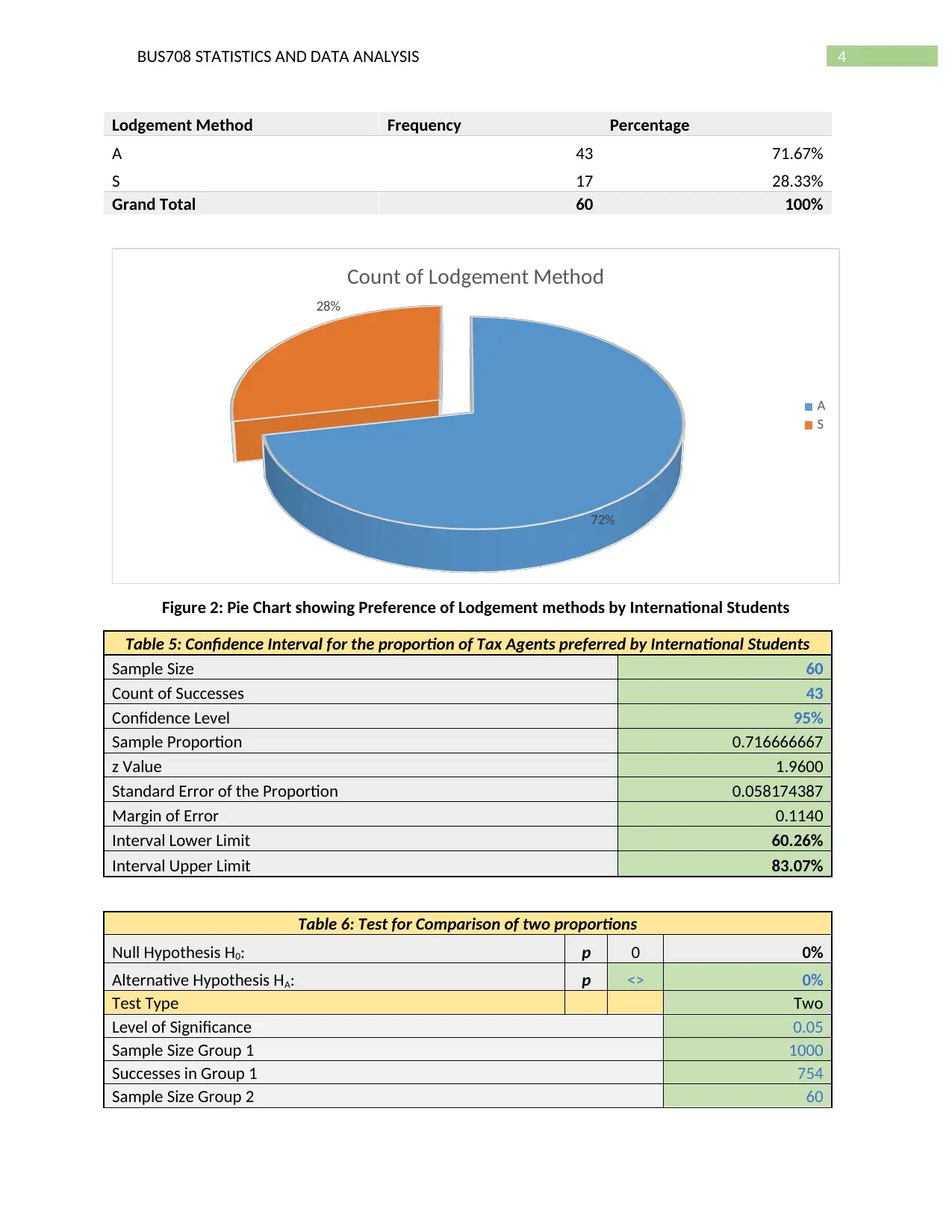

Lodgement Method Frequency Percentage

A 43 71.67%

S 17 28.33%

Grand Total 60 100%

72%

28%

Count of Lodgement Method

A

S

Figure 2: Pie Chart showing Preference of Lodgement methods by International Students

Table 5: Confidence Interval for the proportion of Tax Agents preferred by International Students

Sample Size 60

Count of Successes 43

Confidence Level 95%

Sample Proportion 0.716666667

z Value 1.9600

Standard Error of the Proportion 0.058174387

Margin of Error 0.1140

Interval Lower Limit 60.26%

Interval Upper Limit 83.07%

Table 6: Test for Comparison of two proportions

Null Hypothesis H0: p 0 0%

Alternative Hypothesis HA: p <> 0%

Test Type Two

Level of Significance 0.05

Sample Size Group 1 1000

Successes in Group 1 754

Sample Size Group 2 60

Lodgement Method Frequency Percentage

A 43 71.67%

S 17 28.33%

Grand Total 60 100%

72%

28%

Count of Lodgement Method

A

S

Figure 2: Pie Chart showing Preference of Lodgement methods by International Students

Table 5: Confidence Interval for the proportion of Tax Agents preferred by International Students

Sample Size 60

Count of Successes 43

Confidence Level 95%

Sample Proportion 0.716666667

z Value 1.9600

Standard Error of the Proportion 0.058174387

Margin of Error 0.1140

Interval Lower Limit 60.26%

Interval Upper Limit 83.07%

Table 6: Test for Comparison of two proportions

Null Hypothesis H0: p 0 0%

Alternative Hypothesis HA: p <> 0%

Test Type Two

Level of Significance 0.05

Sample Size Group 1 1000

Successes in Group 1 754

Sample Size Group 2 60

5BUS708 STATISTICS AND DATA ANALYSIS

Successes in Group 2 43

Hypothesized Difference 0

Proportion Group 1 0.754

Proportion Group 2 0.716667

Average Proportion 0.751887

Difference in Two Proportions 0.037333

Z 0.650307

p-value 0.515494

Decision

Do not reject Ho

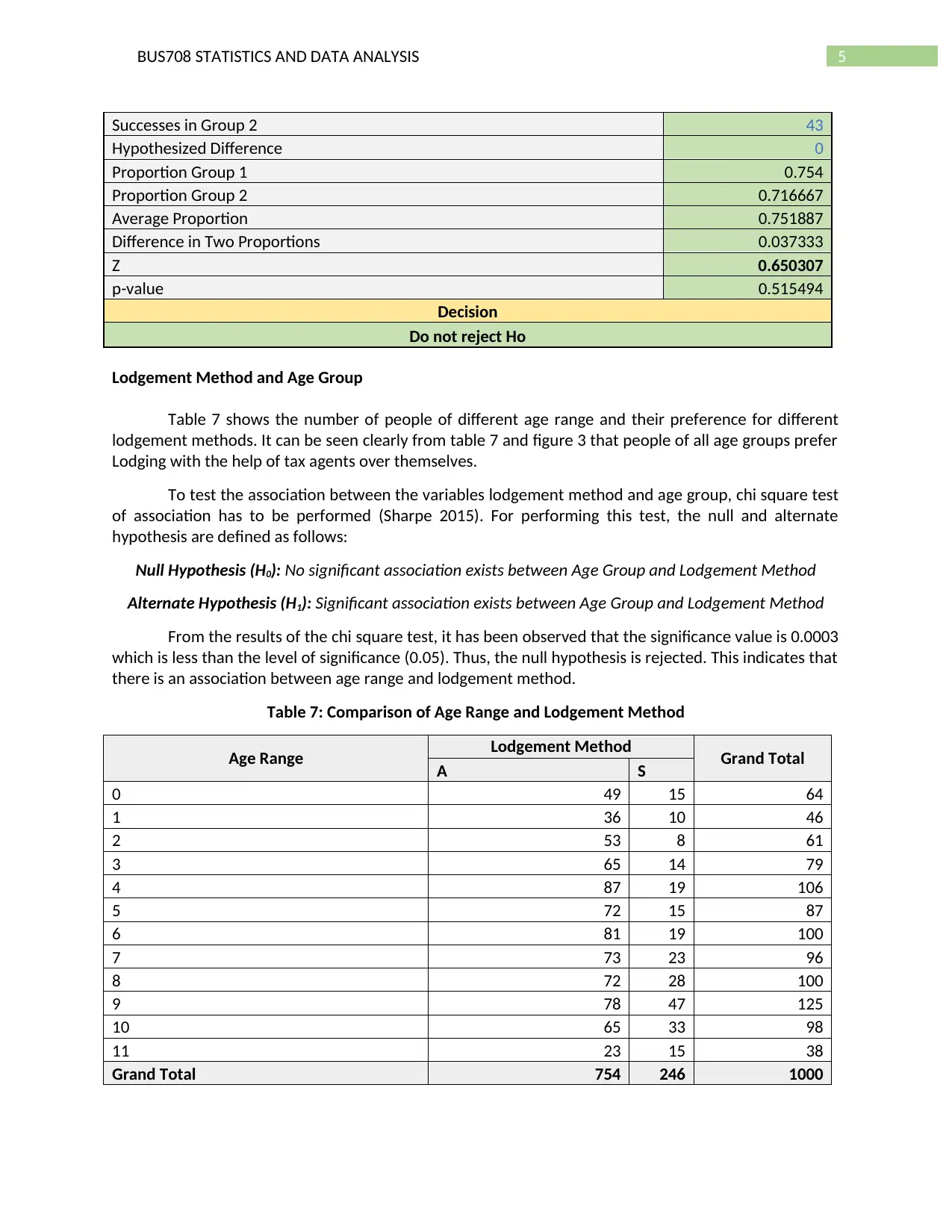

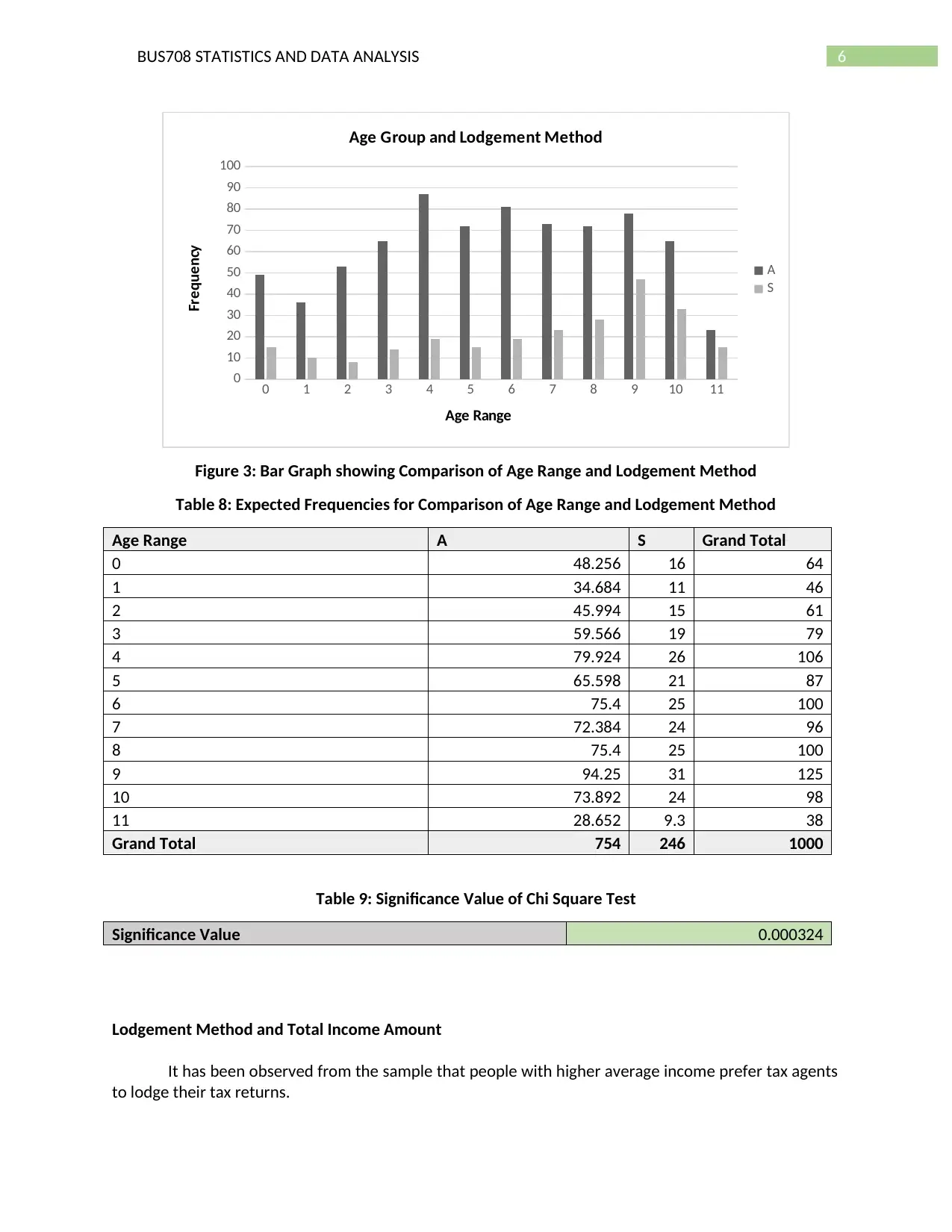

Lodgement Method and Age Group

Table 7 shows the number of people of different age range and their preference for different

lodgement methods. It can be seen clearly from table 7 and figure 3 that people of all age groups prefer

Lodging with the help of tax agents over themselves.

To test the association between the variables lodgement method and age group, chi square test

of association has to be performed (Sharpe 2015). For performing this test, the null and alternate

hypothesis are defined as follows:

Null Hypothesis (H0): No significant association exists between Age Group and Lodgement Method

Alternate Hypothesis (H1): Significant association exists between Age Group and Lodgement Method

From the results of the chi square test, it has been observed that the significance value is 0.0003

which is less than the level of significance (0.05). Thus, the null hypothesis is rejected. This indicates that

there is an association between age range and lodgement method.

Table 7: Comparison of Age Range and Lodgement Method

Age Range Lodgement Method Grand Total

A S

0 49 15 64

1 36 10 46

2 53 8 61

3 65 14 79

4 87 19 106

5 72 15 87

6 81 19 100

7 73 23 96

8 72 28 100

9 78 47 125

10 65 33 98

11 23 15 38

Grand Total 754 246 1000

Successes in Group 2 43

Hypothesized Difference 0

Proportion Group 1 0.754

Proportion Group 2 0.716667

Average Proportion 0.751887

Difference in Two Proportions 0.037333

Z 0.650307

p-value 0.515494

Decision

Do not reject Ho

Lodgement Method and Age Group

Table 7 shows the number of people of different age range and their preference for different

lodgement methods. It can be seen clearly from table 7 and figure 3 that people of all age groups prefer

Lodging with the help of tax agents over themselves.

To test the association between the variables lodgement method and age group, chi square test

of association has to be performed (Sharpe 2015). For performing this test, the null and alternate

hypothesis are defined as follows:

Null Hypothesis (H0): No significant association exists between Age Group and Lodgement Method

Alternate Hypothesis (H1): Significant association exists between Age Group and Lodgement Method

From the results of the chi square test, it has been observed that the significance value is 0.0003

which is less than the level of significance (0.05). Thus, the null hypothesis is rejected. This indicates that

there is an association between age range and lodgement method.

Table 7: Comparison of Age Range and Lodgement Method

Age Range Lodgement Method Grand Total

A S

0 49 15 64

1 36 10 46

2 53 8 61

3 65 14 79

4 87 19 106

5 72 15 87

6 81 19 100

7 73 23 96

8 72 28 100

9 78 47 125

10 65 33 98

11 23 15 38

Grand Total 754 246 1000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUS708 STATISTICS AND DATA ANALYSIS

0 1 2 3 4 5 6 7 8 9 10 11

0

10

20

30

40

50

60

70

80

90

100

Age Group and Lodgement Method

A

S

Age Range

Frequency

Figure 3: Bar Graph showing Comparison of Age Range and Lodgement Method

Table 8: Expected Frequencies for Comparison of Age Range and Lodgement Method

Age Range A S Grand Total

0 48.256 16 64

1 34.684 11 46

2 45.994 15 61

3 59.566 19 79

4 79.924 26 106

5 65.598 21 87

6 75.4 25 100

7 72.384 24 96

8 75.4 25 100

9 94.25 31 125

10 73.892 24 98

11 28.652 9.3 38

Grand Total 754 246 1000

Table 9: Significance Value of Chi Square Test

Significance Value 0.000324

Lodgement Method and Total Income Amount

It has been observed from the sample that people with higher average income prefer tax agents

to lodge their tax returns.

0 1 2 3 4 5 6 7 8 9 10 11

0

10

20

30

40

50

60

70

80

90

100

Age Group and Lodgement Method

A

S

Age Range

Frequency

Figure 3: Bar Graph showing Comparison of Age Range and Lodgement Method

Table 8: Expected Frequencies for Comparison of Age Range and Lodgement Method

Age Range A S Grand Total

0 48.256 16 64

1 34.684 11 46

2 45.994 15 61

3 59.566 19 79

4 79.924 26 106

5 65.598 21 87

6 75.4 25 100

7 72.384 24 96

8 75.4 25 100

9 94.25 31 125

10 73.892 24 98

11 28.652 9.3 38

Grand Total 754 246 1000

Table 9: Significance Value of Chi Square Test

Significance Value 0.000324

Lodgement Method and Total Income Amount

It has been observed from the sample that people with higher average income prefer tax agents

to lodge their tax returns.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUS708 STATISTICS AND DATA ANALYSIS

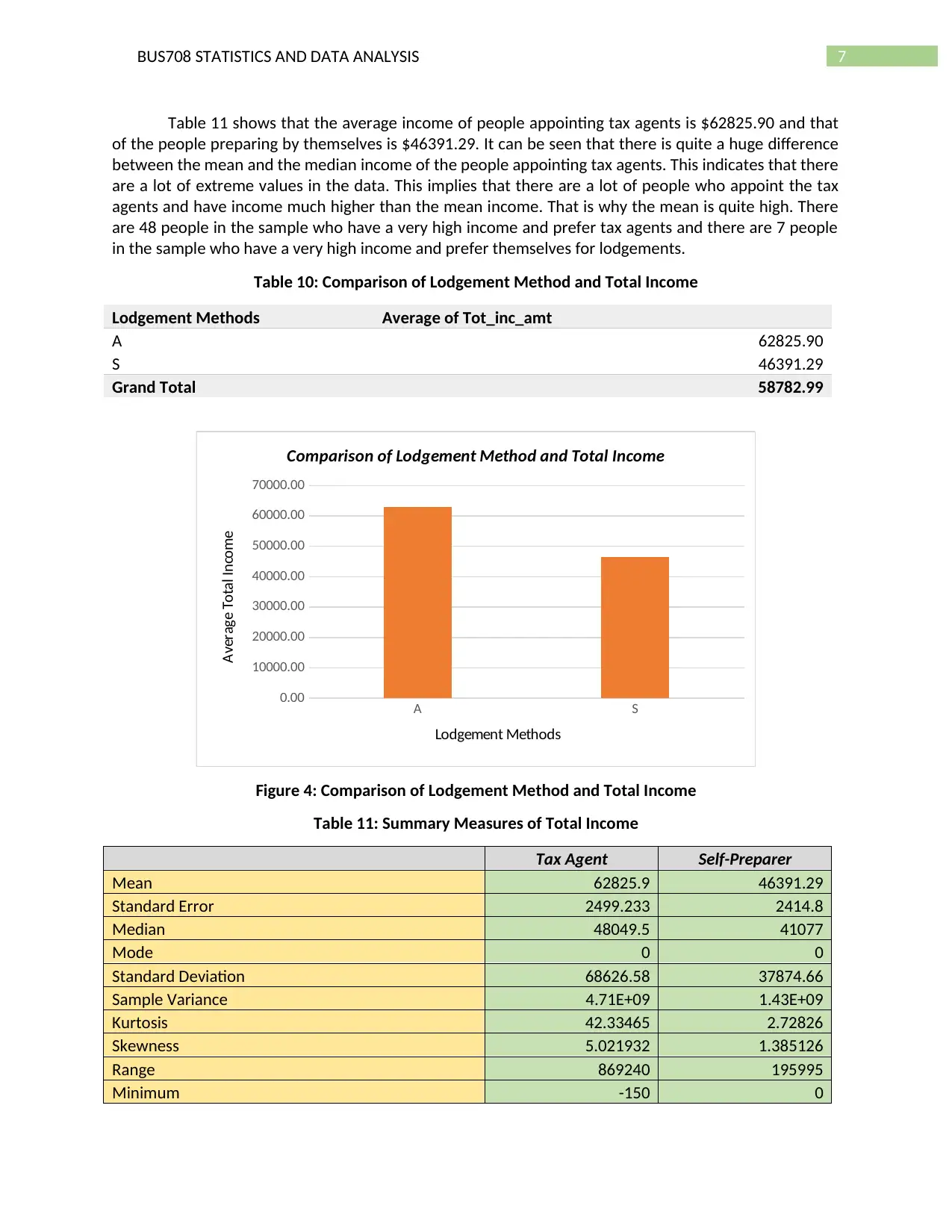

Table 11 shows that the average income of people appointing tax agents is $62825.90 and that

of the people preparing by themselves is $46391.29. It can be seen that there is quite a huge difference

between the mean and the median income of the people appointing tax agents. This indicates that there

are a lot of extreme values in the data. This implies that there are a lot of people who appoint the tax

agents and have income much higher than the mean income. That is why the mean is quite high. There

are 48 people in the sample who have a very high income and prefer tax agents and there are 7 people

in the sample who have a very high income and prefer themselves for lodgements.

Table 10: Comparison of Lodgement Method and Total Income

Lodgement Methods Average of Tot_inc_amt

A 62825.90

S 46391.29

Grand Total 58782.99

A S

0.00

10000.00

20000.00

30000.00

40000.00

50000.00

60000.00

70000.00

Comparison of Lodgement Method and Total Income

Lodgement Methods

Average Total Income

Figure 4: Comparison of Lodgement Method and Total Income

Table 11: Summary Measures of Total Income

Tax Agent Self-Preparer

Mean 62825.9 46391.29

Standard Error 2499.233 2414.8

Median 48049.5 41077

Mode 0 0

Standard Deviation 68626.58 37874.66

Sample Variance 4.71E+09 1.43E+09

Kurtosis 42.33465 2.72826

Skewness 5.021932 1.385126

Range 869240 195995

Minimum -150 0

Table 11 shows that the average income of people appointing tax agents is $62825.90 and that

of the people preparing by themselves is $46391.29. It can be seen that there is quite a huge difference

between the mean and the median income of the people appointing tax agents. This indicates that there

are a lot of extreme values in the data. This implies that there are a lot of people who appoint the tax

agents and have income much higher than the mean income. That is why the mean is quite high. There

are 48 people in the sample who have a very high income and prefer tax agents and there are 7 people

in the sample who have a very high income and prefer themselves for lodgements.

Table 10: Comparison of Lodgement Method and Total Income

Lodgement Methods Average of Tot_inc_amt

A 62825.90

S 46391.29

Grand Total 58782.99

A S

0.00

10000.00

20000.00

30000.00

40000.00

50000.00

60000.00

70000.00

Comparison of Lodgement Method and Total Income

Lodgement Methods

Average Total Income

Figure 4: Comparison of Lodgement Method and Total Income

Table 11: Summary Measures of Total Income

Tax Agent Self-Preparer

Mean 62825.9 46391.29

Standard Error 2499.233 2414.8

Median 48049.5 41077

Mode 0 0

Standard Deviation 68626.58 37874.66

Sample Variance 4.71E+09 1.43E+09

Kurtosis 42.33465 2.72826

Skewness 5.021932 1.385126

Range 869240 195995

Minimum -150 0

8BUS708 STATISTICS AND DATA ANALYSIS

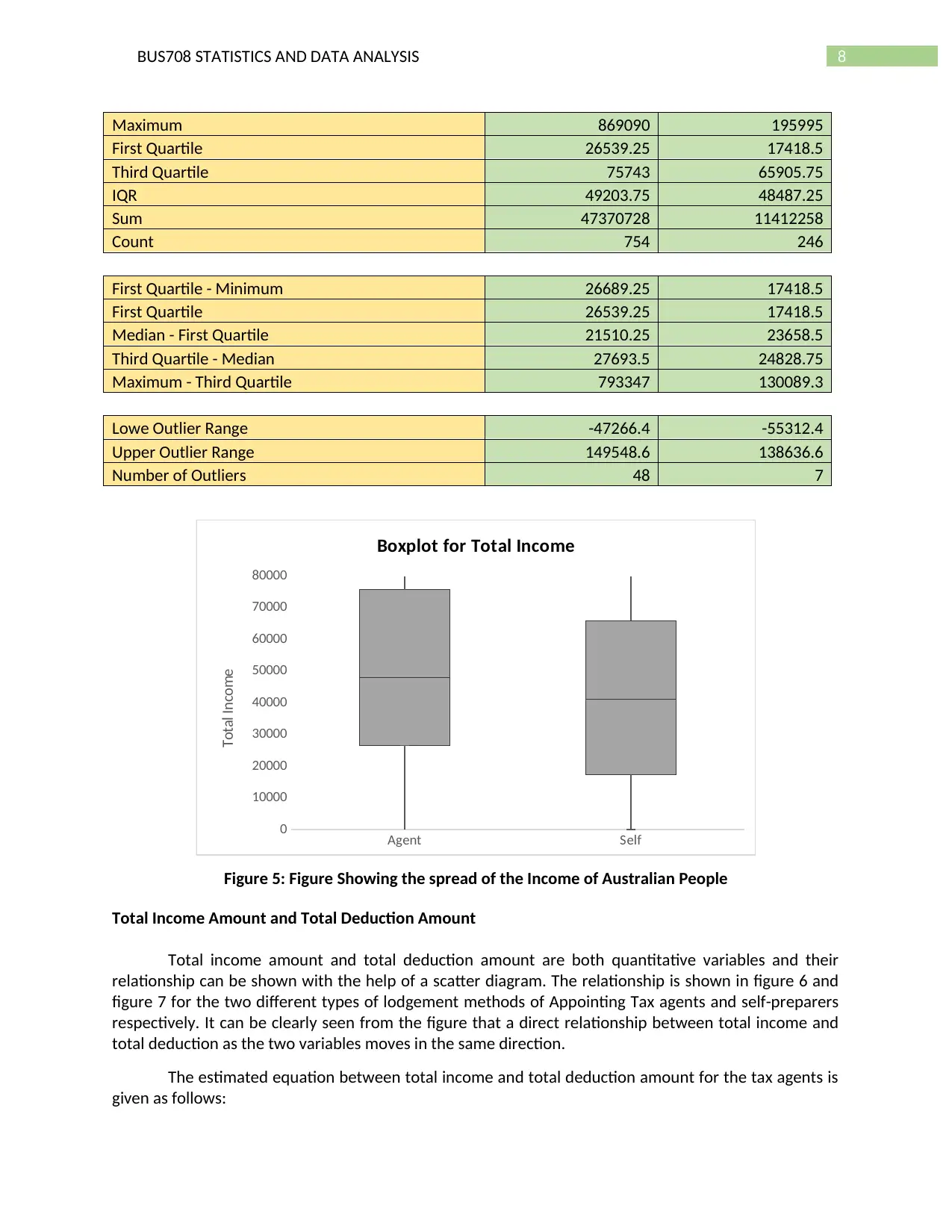

Maximum 869090 195995

First Quartile 26539.25 17418.5

Third Quartile 75743 65905.75

IQR 49203.75 48487.25

Sum 47370728 11412258

Count 754 246

First Quartile - Minimum 26689.25 17418.5

First Quartile 26539.25 17418.5

Median - First Quartile 21510.25 23658.5

Third Quartile - Median 27693.5 24828.75

Maximum - Third Quartile 793347 130089.3

Lowe Outlier Range -47266.4 -55312.4

Upper Outlier Range 149548.6 138636.6

Number of Outliers 48 7

Agent Self

0

10000

20000

30000

40000

50000

60000

70000

80000

Boxplot for Total Income

Total Income

Figure 5: Figure Showing the spread of the Income of Australian People

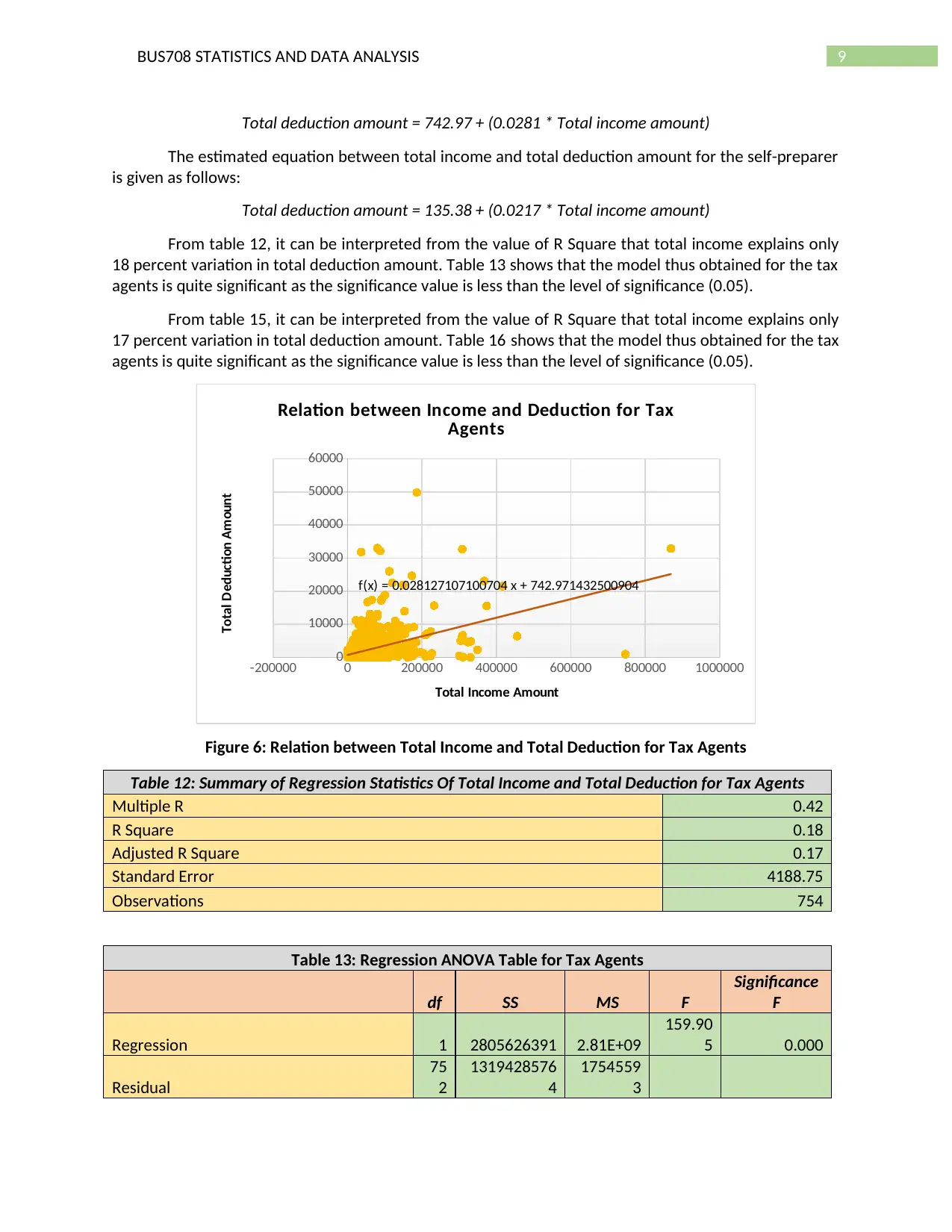

Total Income Amount and Total Deduction Amount

Total income amount and total deduction amount are both quantitative variables and their

relationship can be shown with the help of a scatter diagram. The relationship is shown in figure 6 and

figure 7 for the two different types of lodgement methods of Appointing Tax agents and self-preparers

respectively. It can be clearly seen from the figure that a direct relationship between total income and

total deduction as the two variables moves in the same direction.

The estimated equation between total income and total deduction amount for the tax agents is

given as follows:

Maximum 869090 195995

First Quartile 26539.25 17418.5

Third Quartile 75743 65905.75

IQR 49203.75 48487.25

Sum 47370728 11412258

Count 754 246

First Quartile - Minimum 26689.25 17418.5

First Quartile 26539.25 17418.5

Median - First Quartile 21510.25 23658.5

Third Quartile - Median 27693.5 24828.75

Maximum - Third Quartile 793347 130089.3

Lowe Outlier Range -47266.4 -55312.4

Upper Outlier Range 149548.6 138636.6

Number of Outliers 48 7

Agent Self

0

10000

20000

30000

40000

50000

60000

70000

80000

Boxplot for Total Income

Total Income

Figure 5: Figure Showing the spread of the Income of Australian People

Total Income Amount and Total Deduction Amount

Total income amount and total deduction amount are both quantitative variables and their

relationship can be shown with the help of a scatter diagram. The relationship is shown in figure 6 and

figure 7 for the two different types of lodgement methods of Appointing Tax agents and self-preparers

respectively. It can be clearly seen from the figure that a direct relationship between total income and

total deduction as the two variables moves in the same direction.

The estimated equation between total income and total deduction amount for the tax agents is

given as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUS708 STATISTICS AND DATA ANALYSIS

Total deduction amount = 742.97 + (0.0281 * Total income amount)

The estimated equation between total income and total deduction amount for the self-preparer

is given as follows:

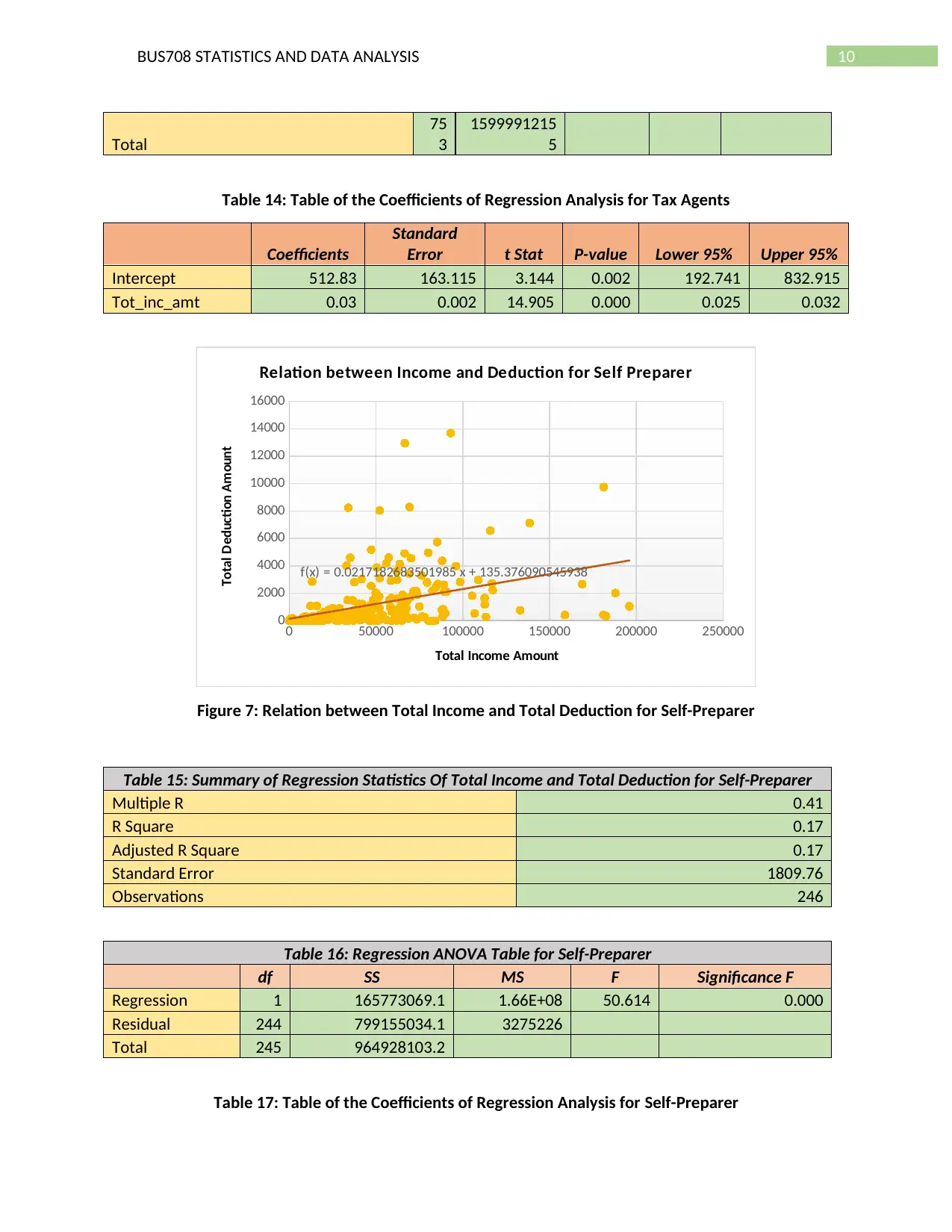

Total deduction amount = 135.38 + (0.0217 * Total income amount)

From table 12, it can be interpreted from the value of R Square that total income explains only

18 percent variation in total deduction amount. Table 13 shows that the model thus obtained for the tax

agents is quite significant as the significance value is less than the level of significance (0.05).

From table 15, it can be interpreted from the value of R Square that total income explains only

17 percent variation in total deduction amount. Table 16 shows that the model thus obtained for the tax

agents is quite significant as the significance value is less than the level of significance (0.05).

-200000 0 200000 400000 600000 800000 1000000

0

10000

20000

30000

40000

50000

60000

f(x) = 0.028127107100704 x + 742.971432500904

Relation between Income and Deduction for Tax

Agents

Total Income Amount

Total Deduction Amount

Figure 6: Relation between Total Income and Total Deduction for Tax Agents

Table 12: Summary of Regression Statistics Of Total Income and Total Deduction for Tax Agents

Multiple R 0.42

R Square 0.18

Adjusted R Square 0.17

Standard Error 4188.75

Observations 754

Table 13: Regression ANOVA Table for Tax Agents

df SS MS F

Significance

F

Regression 1 2805626391 2.81E+09

159.90

5 0.000

Residual

75

2

1319428576

4

1754559

3

Total deduction amount = 742.97 + (0.0281 * Total income amount)

The estimated equation between total income and total deduction amount for the self-preparer

is given as follows:

Total deduction amount = 135.38 + (0.0217 * Total income amount)

From table 12, it can be interpreted from the value of R Square that total income explains only

18 percent variation in total deduction amount. Table 13 shows that the model thus obtained for the tax

agents is quite significant as the significance value is less than the level of significance (0.05).

From table 15, it can be interpreted from the value of R Square that total income explains only

17 percent variation in total deduction amount. Table 16 shows that the model thus obtained for the tax

agents is quite significant as the significance value is less than the level of significance (0.05).

-200000 0 200000 400000 600000 800000 1000000

0

10000

20000

30000

40000

50000

60000

f(x) = 0.028127107100704 x + 742.971432500904

Relation between Income and Deduction for Tax

Agents

Total Income Amount

Total Deduction Amount

Figure 6: Relation between Total Income and Total Deduction for Tax Agents

Table 12: Summary of Regression Statistics Of Total Income and Total Deduction for Tax Agents

Multiple R 0.42

R Square 0.18

Adjusted R Square 0.17

Standard Error 4188.75

Observations 754

Table 13: Regression ANOVA Table for Tax Agents

df SS MS F

Significance

F

Regression 1 2805626391 2.81E+09

159.90

5 0.000

Residual

75

2

1319428576

4

1754559

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUS708 STATISTICS AND DATA ANALYSIS

Total

75

3

1599991215

5

Table 14: Table of the Coefficients of Regression Analysis for Tax Agents

Coefficients

Standard

Error t Stat P-value Lower 95% Upper 95%

Intercept 512.83 163.115 3.144 0.002 192.741 832.915

Tot_inc_amt 0.03 0.002 14.905 0.000 0.025 0.032

0 50000 100000 150000 200000 250000

0

2000

4000

6000

8000

10000

12000

14000

16000

f(x) = 0.0217182683501985 x + 135.376090545938

Relation between Income and Deduction for Self Preparer

Total Income Amount

Total Deduction Amount

Figure 7: Relation between Total Income and Total Deduction for Self-Preparer

Table 15: Summary of Regression Statistics Of Total Income and Total Deduction for Self-Preparer

Multiple R 0.41

R Square 0.17

Adjusted R Square 0.17

Standard Error 1809.76

Observations 246

Table 16: Regression ANOVA Table for Self-Preparer

df SS MS F Significance F

Regression 1 165773069.1 1.66E+08 50.614 0.000

Residual 244 799155034.1 3275226

Total 245 964928103.2

Table 17: Table of the Coefficients of Regression Analysis for Self-Preparer

Total

75

3

1599991215

5

Table 14: Table of the Coefficients of Regression Analysis for Tax Agents

Coefficients

Standard

Error t Stat P-value Lower 95% Upper 95%

Intercept 512.83 163.115 3.144 0.002 192.741 832.915

Tot_inc_amt 0.03 0.002 14.905 0.000 0.025 0.032

0 50000 100000 150000 200000 250000

0

2000

4000

6000

8000

10000

12000

14000

16000

f(x) = 0.0217182683501985 x + 135.376090545938

Relation between Income and Deduction for Self Preparer

Total Income Amount

Total Deduction Amount

Figure 7: Relation between Total Income and Total Deduction for Self-Preparer

Table 15: Summary of Regression Statistics Of Total Income and Total Deduction for Self-Preparer

Multiple R 0.41

R Square 0.17

Adjusted R Square 0.17

Standard Error 1809.76

Observations 246

Table 16: Regression ANOVA Table for Self-Preparer

df SS MS F Significance F

Regression 1 165773069.1 1.66E+08 50.614 0.000

Residual 244 799155034.1 3275226

Total 245 964928103.2

Table 17: Table of the Coefficients of Regression Analysis for Self-Preparer

11BUS708 STATISTICS AND DATA ANALYSIS

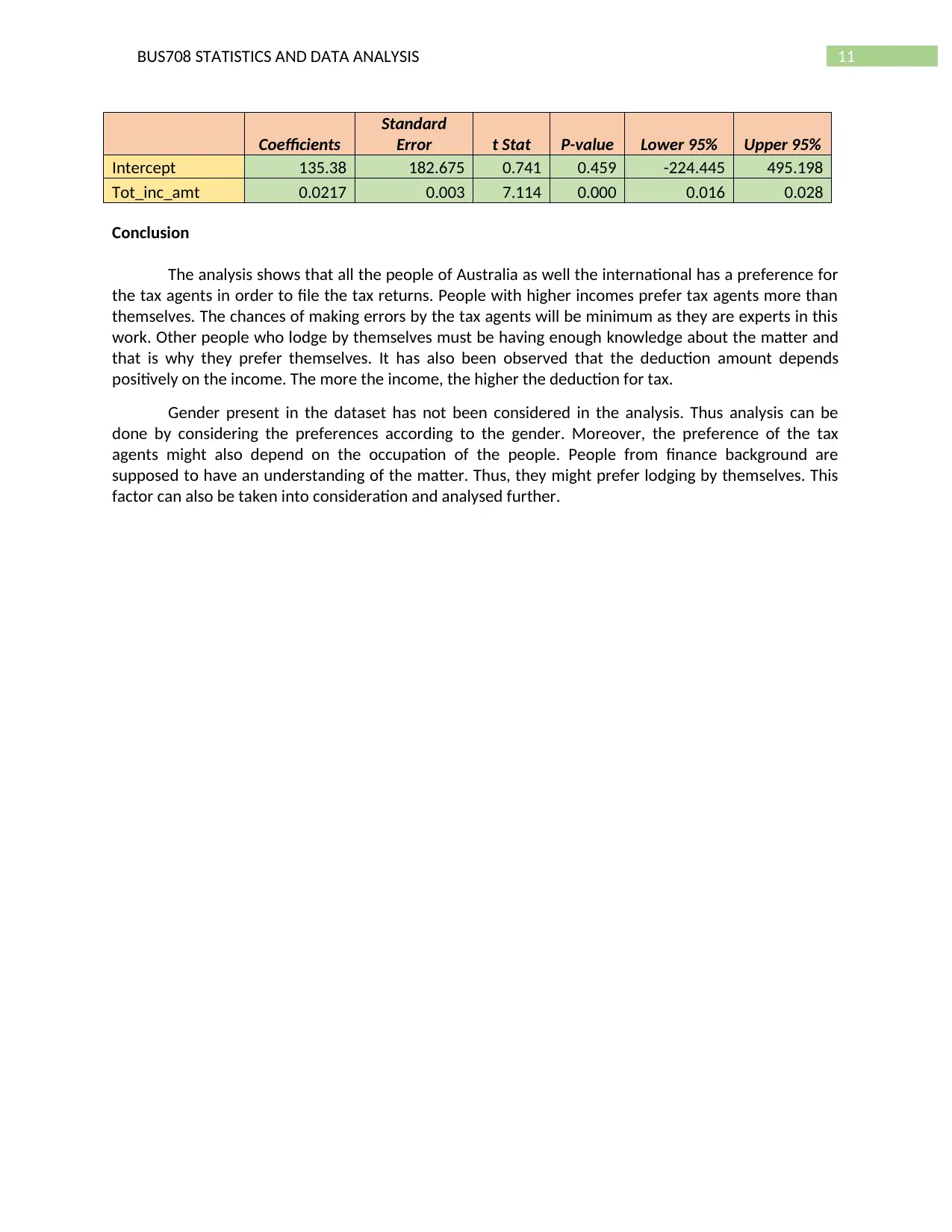

Coefficients

Standard

Error t Stat P-value Lower 95% Upper 95%

Intercept 135.38 182.675 0.741 0.459 -224.445 495.198

Tot_inc_amt 0.0217 0.003 7.114 0.000 0.016 0.028

Conclusion

The analysis shows that all the people of Australia as well the international has a preference for

the tax agents in order to file the tax returns. People with higher incomes prefer tax agents more than

themselves. The chances of making errors by the tax agents will be minimum as they are experts in this

work. Other people who lodge by themselves must be having enough knowledge about the matter and

that is why they prefer themselves. It has also been observed that the deduction amount depends

positively on the income. The more the income, the higher the deduction for tax.

Gender present in the dataset has not been considered in the analysis. Thus analysis can be

done by considering the preferences according to the gender. Moreover, the preference of the tax

agents might also depend on the occupation of the people. People from finance background are

supposed to have an understanding of the matter. Thus, they might prefer lodging by themselves. This

factor can also be taken into consideration and analysed further.

Coefficients

Standard

Error t Stat P-value Lower 95% Upper 95%

Intercept 135.38 182.675 0.741 0.459 -224.445 495.198

Tot_inc_amt 0.0217 0.003 7.114 0.000 0.016 0.028

Conclusion

The analysis shows that all the people of Australia as well the international has a preference for

the tax agents in order to file the tax returns. People with higher incomes prefer tax agents more than

themselves. The chances of making errors by the tax agents will be minimum as they are experts in this

work. Other people who lodge by themselves must be having enough knowledge about the matter and

that is why they prefer themselves. It has also been observed that the deduction amount depends

positively on the income. The more the income, the higher the deduction for tax.

Gender present in the dataset has not been considered in the analysis. Thus analysis can be

done by considering the preferences according to the gender. Moreover, the preference of the tax

agents might also depend on the occupation of the people. People from finance background are

supposed to have an understanding of the matter. Thus, they might prefer lodging by themselves. This

factor can also be taken into consideration and analysed further.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.