Accounting for Business: Financial Ratio Analysis and Solutions

VerifiedAdded on 2023/06/04

|9

|890

|66

Homework Assignment

AI Summary

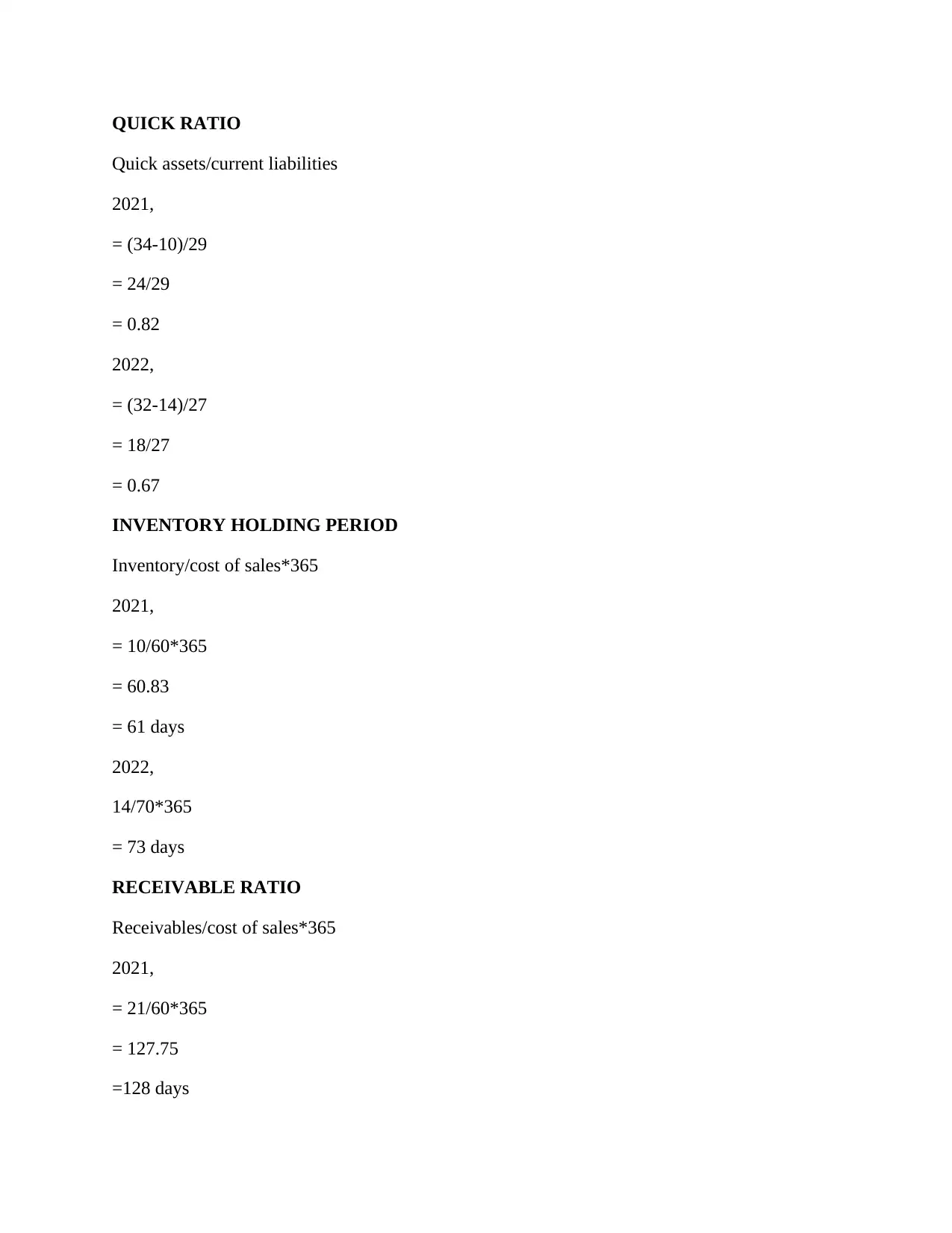

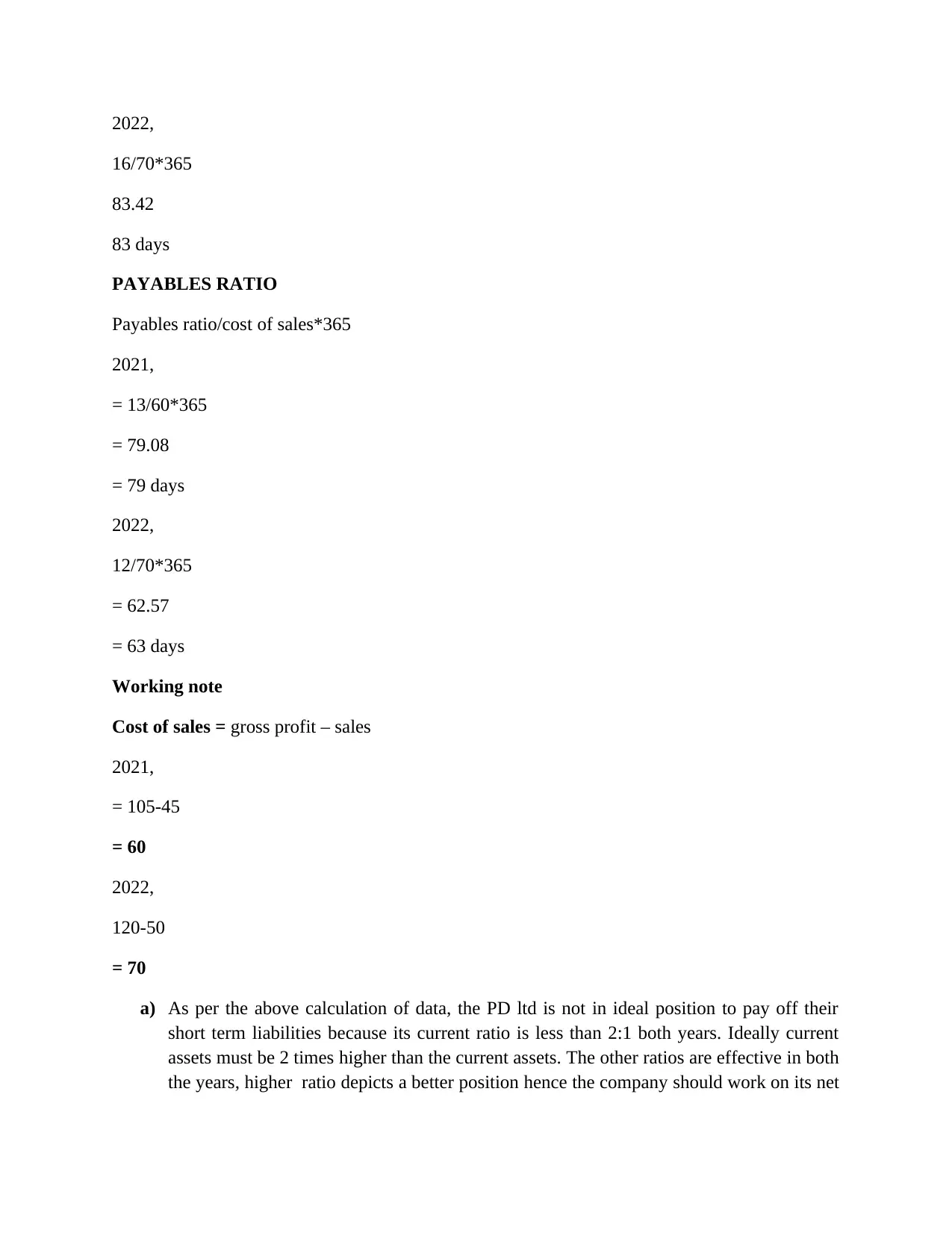

This document presents a comprehensive solution to an accounting assignment, focusing on financial analysis and break-even analysis. The assignment delves into calculating and interpreting various financial ratios, including gross profit ratio, net profit ratio, current ratio, quick ratio, inventory holding period, receivables ratio, and payables ratio. It also includes detailed calculations for break-even points, cost-volume-profit analysis, and margin of safety. The solution provides a step-by-step breakdown of the calculations and interpretations, offering insights into a company's financial performance and position. The document also includes an analysis of the limitations of the models used and provides a list of references. This assignment is a valuable resource for students studying business accounting, offering a clear understanding of key financial concepts and their practical application.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.