Business Accounting Assignment: BABS Module 202104 - Semester 1

VerifiedAdded on 2022/11/24

|26

|1755

|440

Homework Assignment

AI Summary

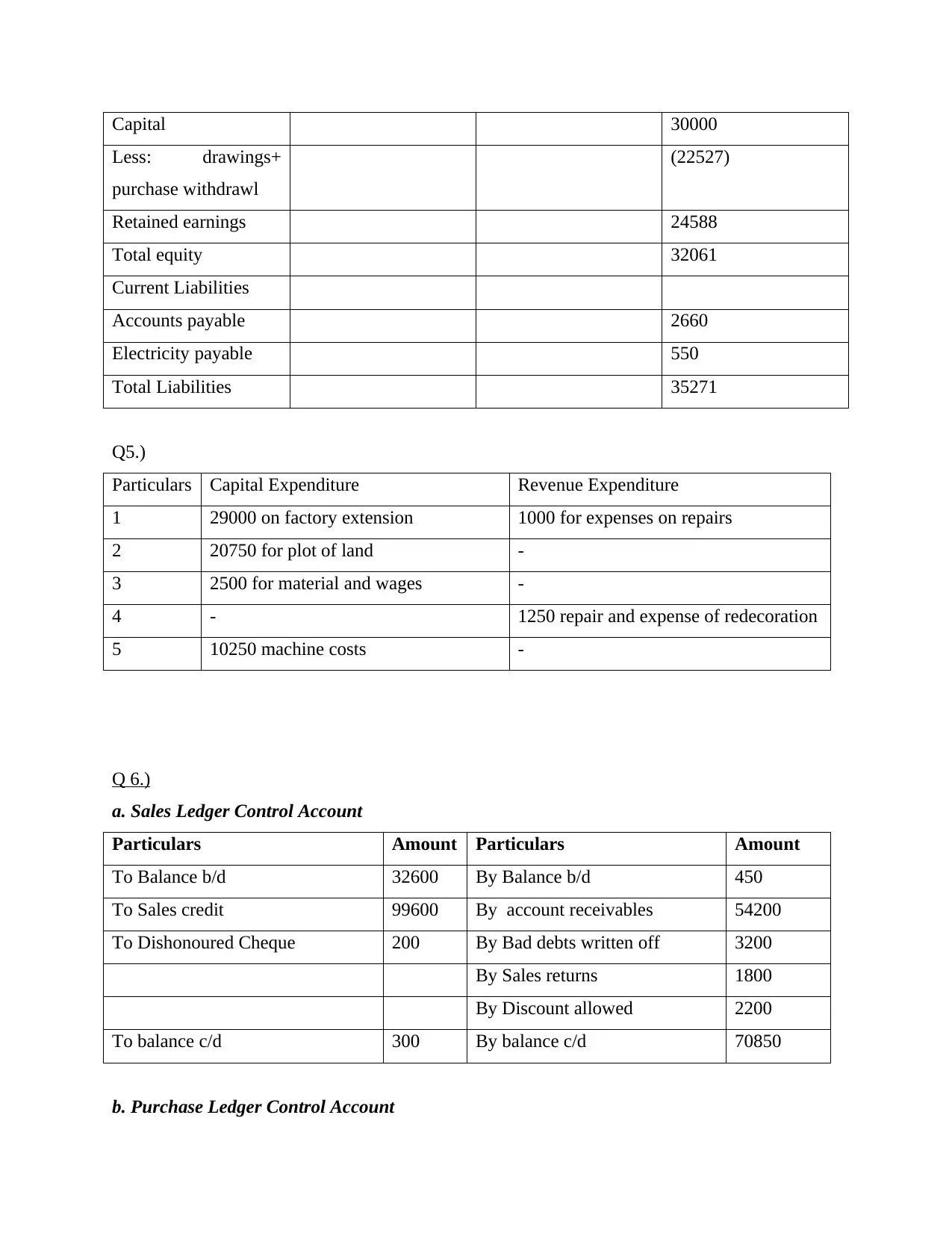

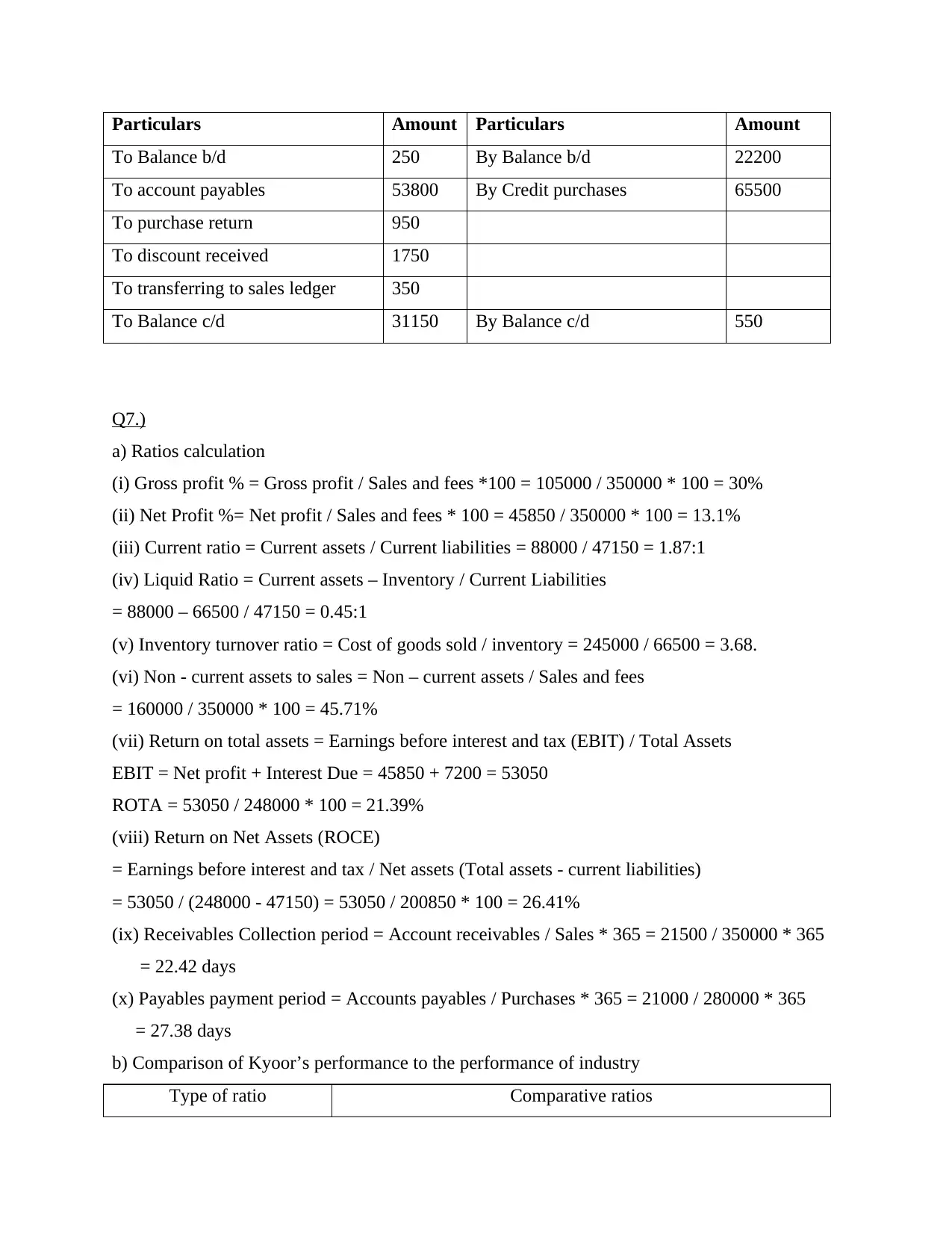

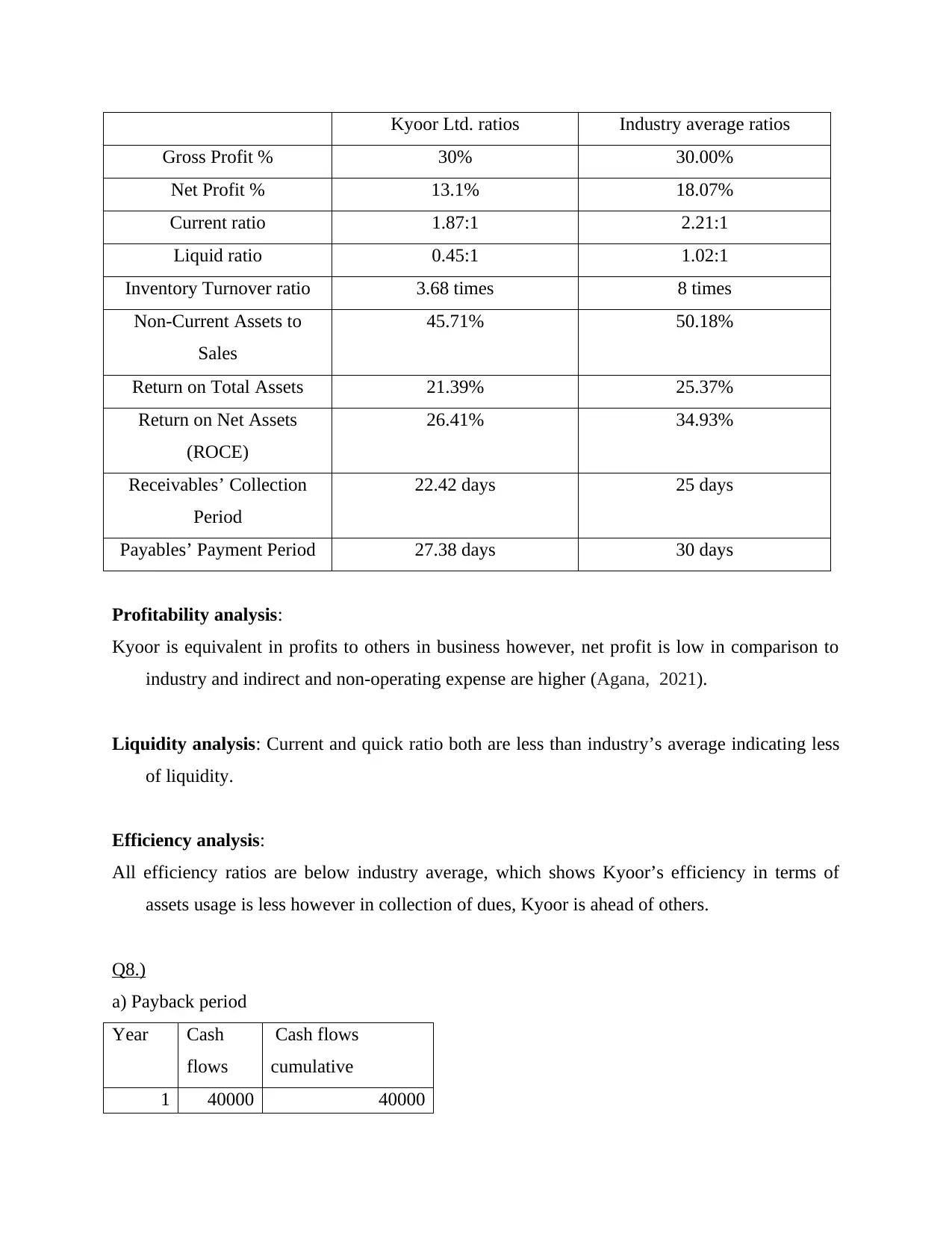

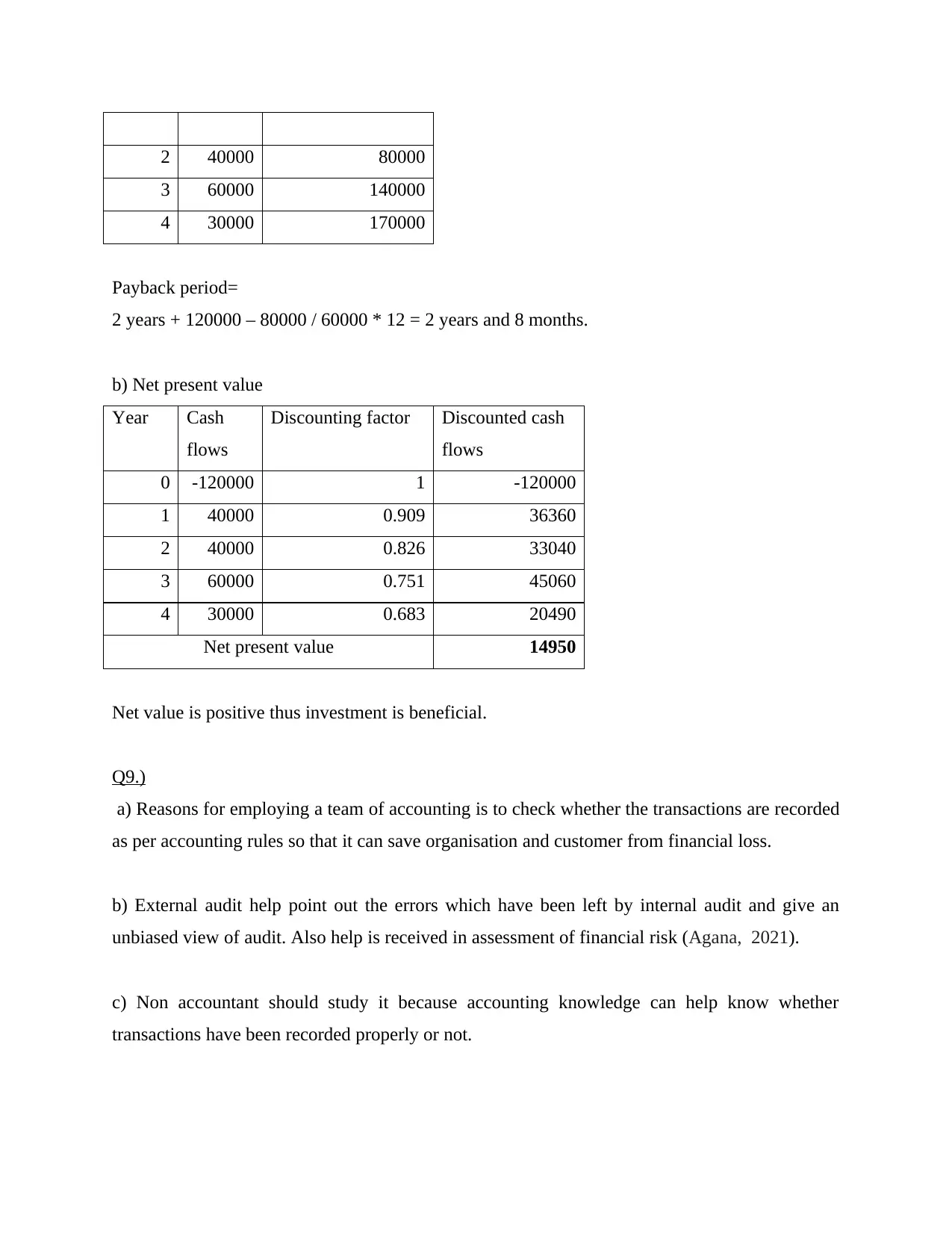

This document presents solutions to a comprehensive Business Accounting assignment, addressing ten key questions. The assignment covers a wide range of topics, including the fundamental accounting equation, journal entries, T-accounts, trial balance preparation, and the creation of financial statements like the statement of profit and loss and the statement of financial position. It explores control accounts, ratio analysis (gross profit, net profit, current, liquid, inventory turnover, and profitability ratios), and capital budgeting techniques such as the payback period and net present value. The assignment also delves into the roles of accounting teams and external audits, the importance of accounting knowledge, and the nature of accounting principles, including depreciation, bad debts, debentures, and share types. References to relevant accounting literature are also included.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.