BACT105 Business Accounting: Depreciation Methods and Journal Entries

VerifiedAdded on 2023/06/12

|9

|898

|254

Report

AI Summary

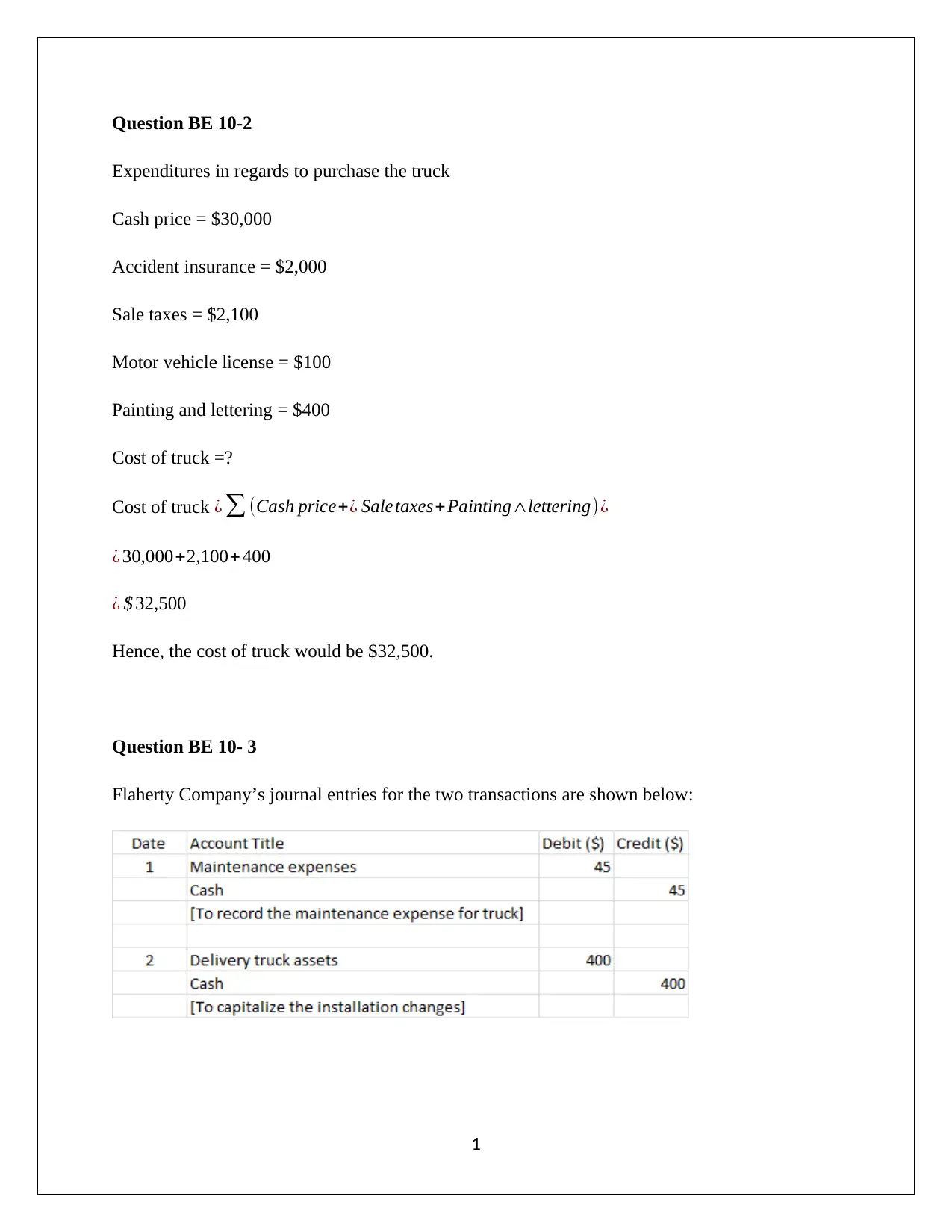

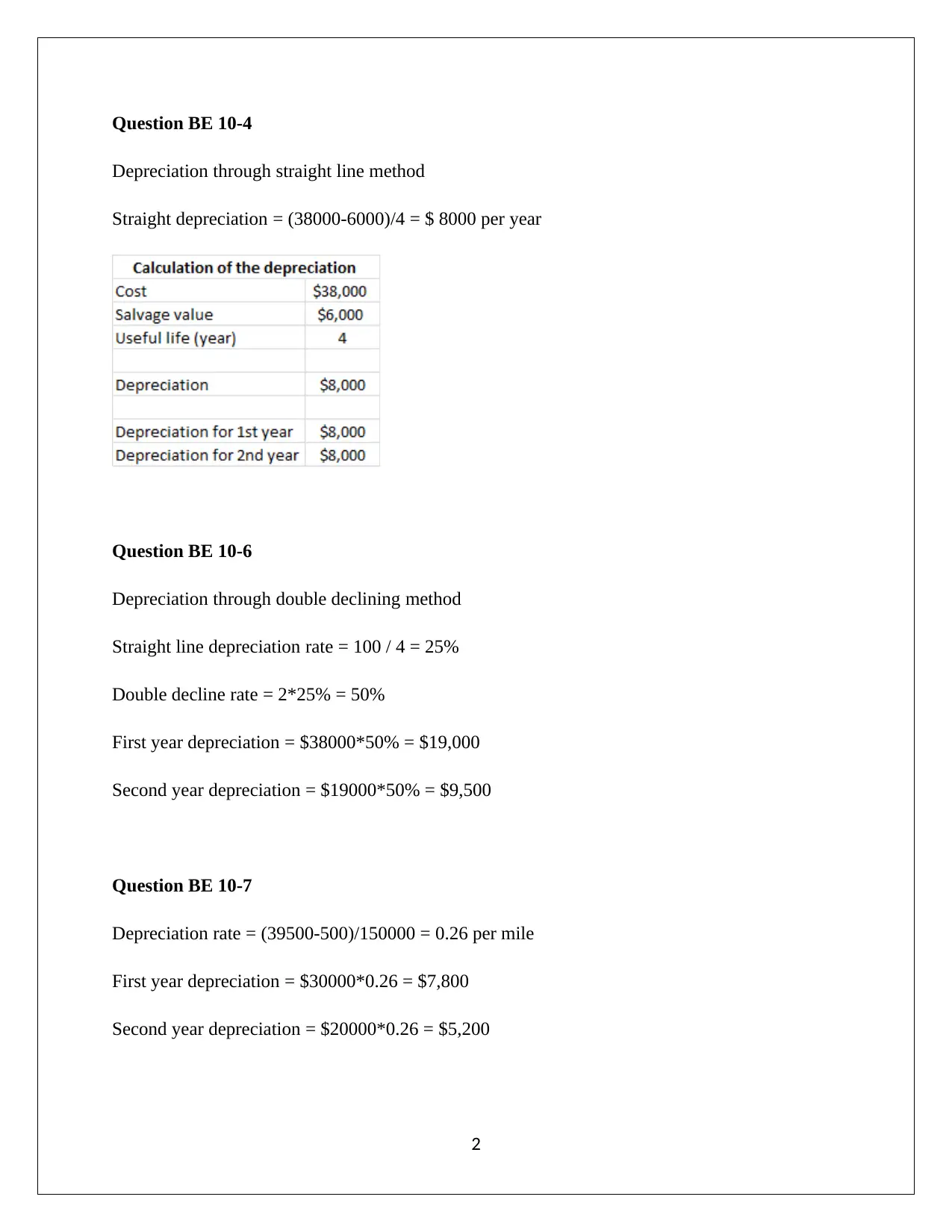

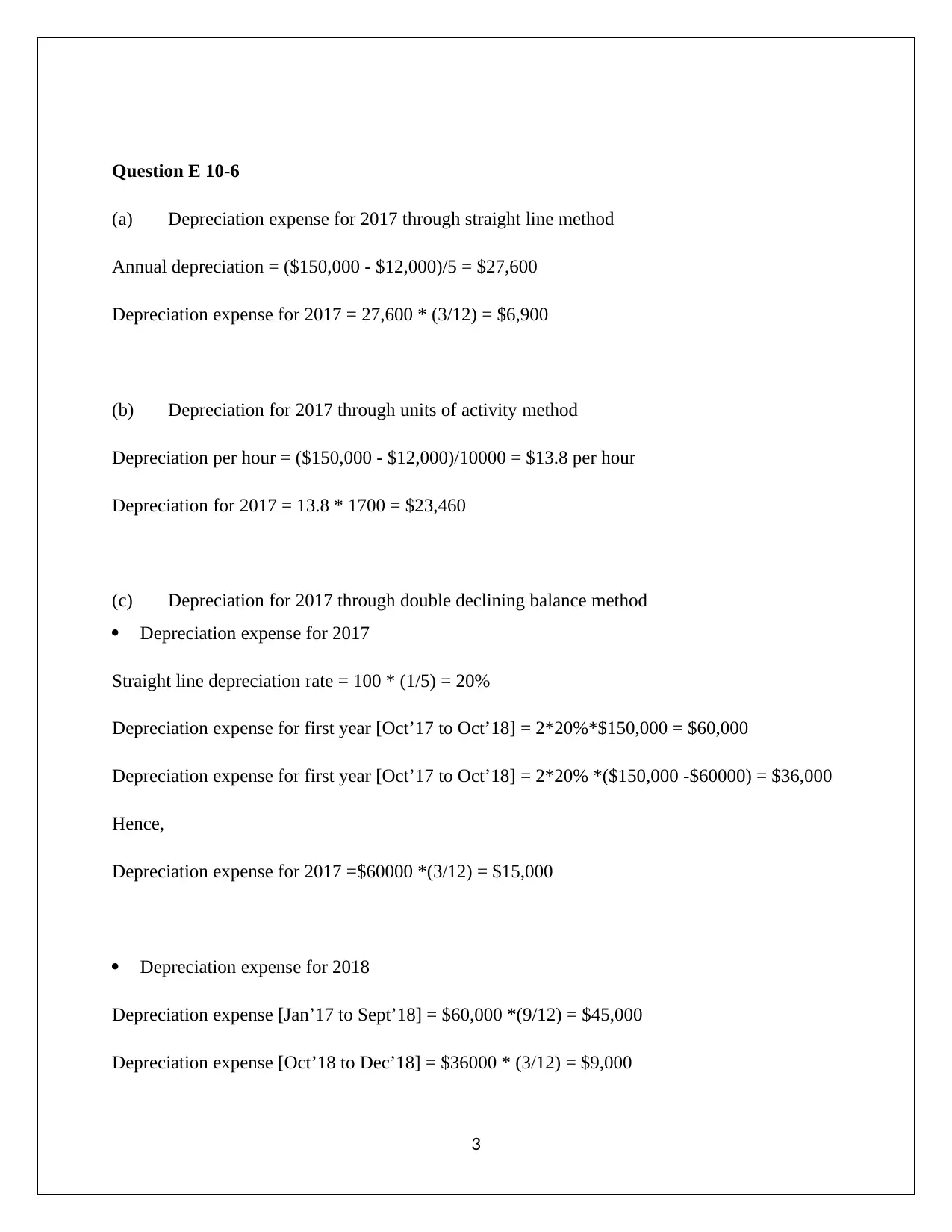

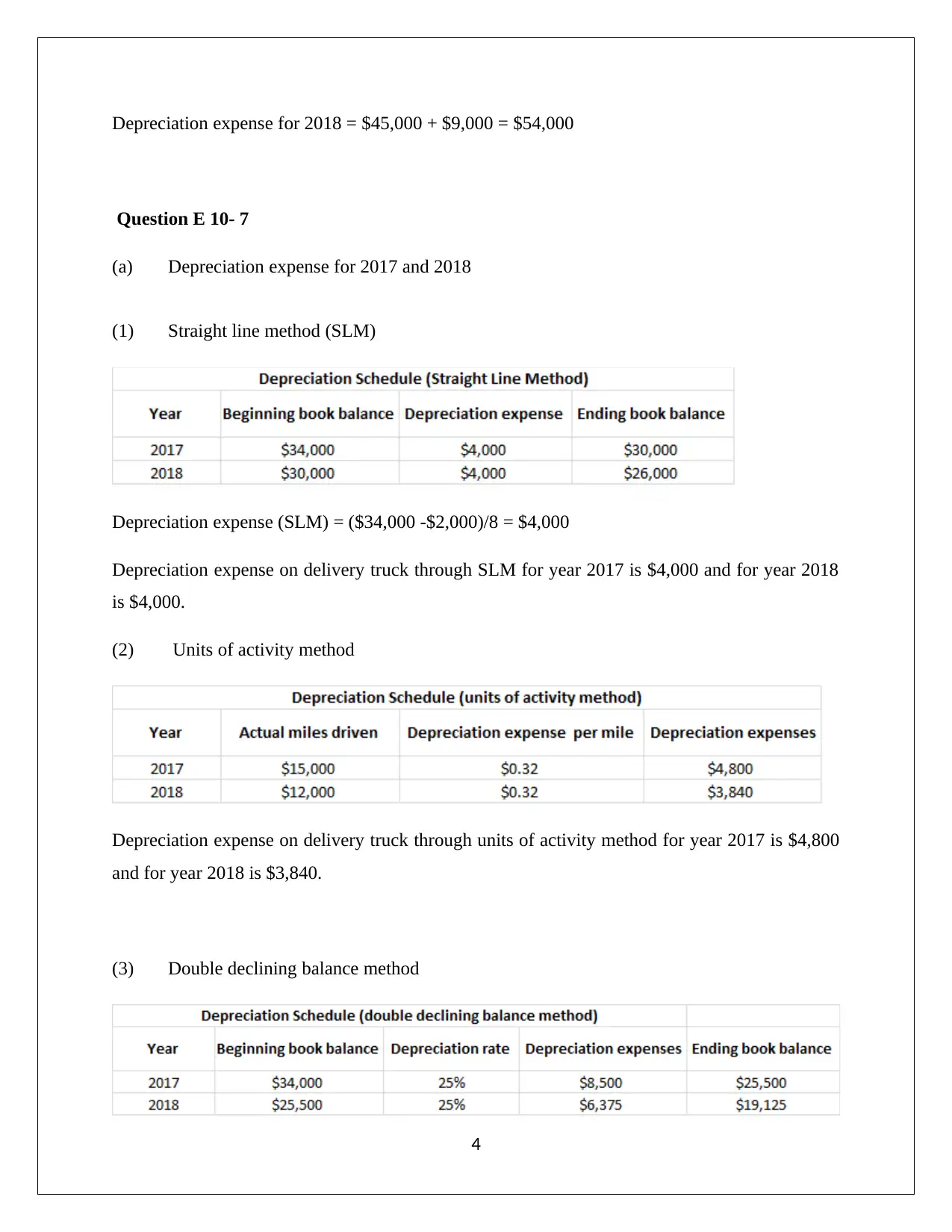

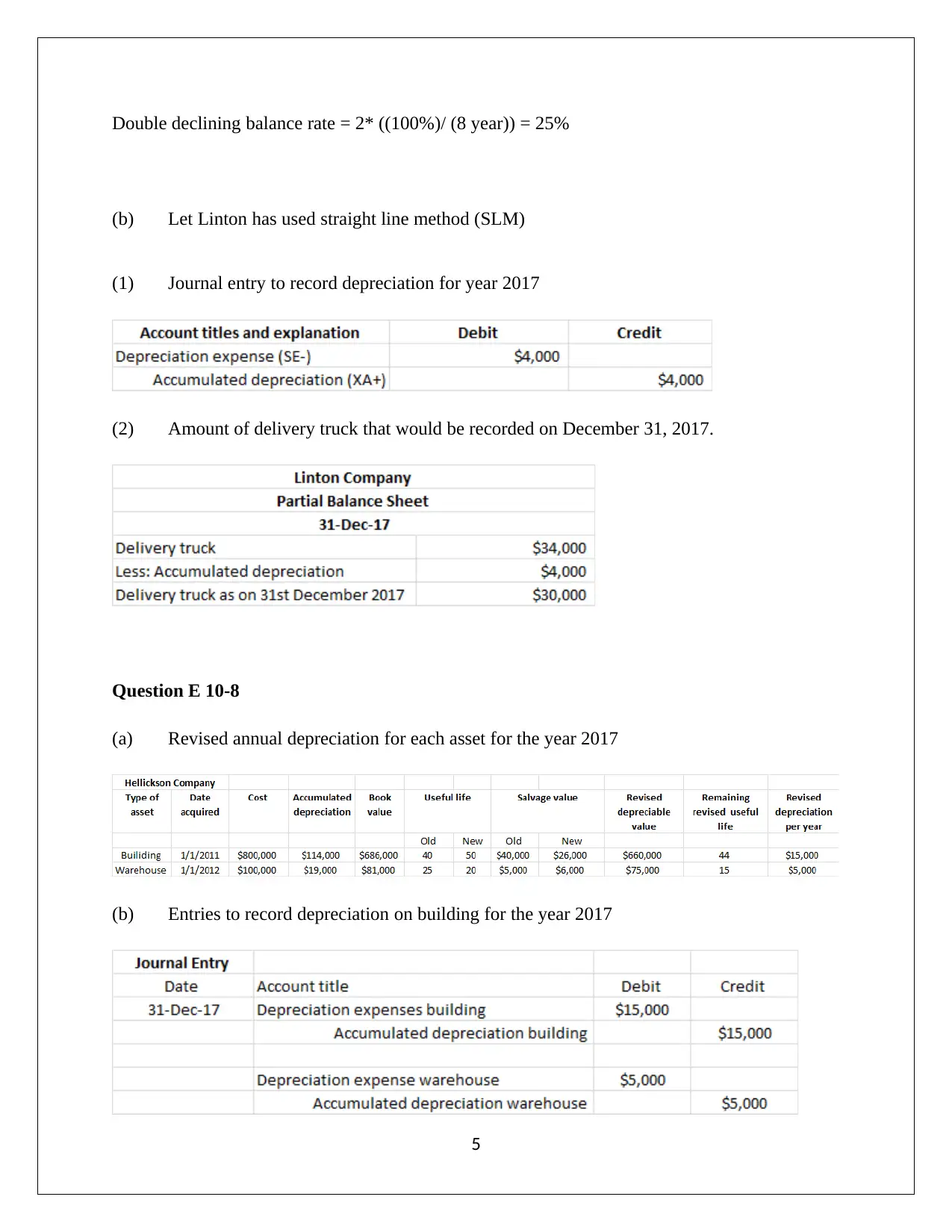

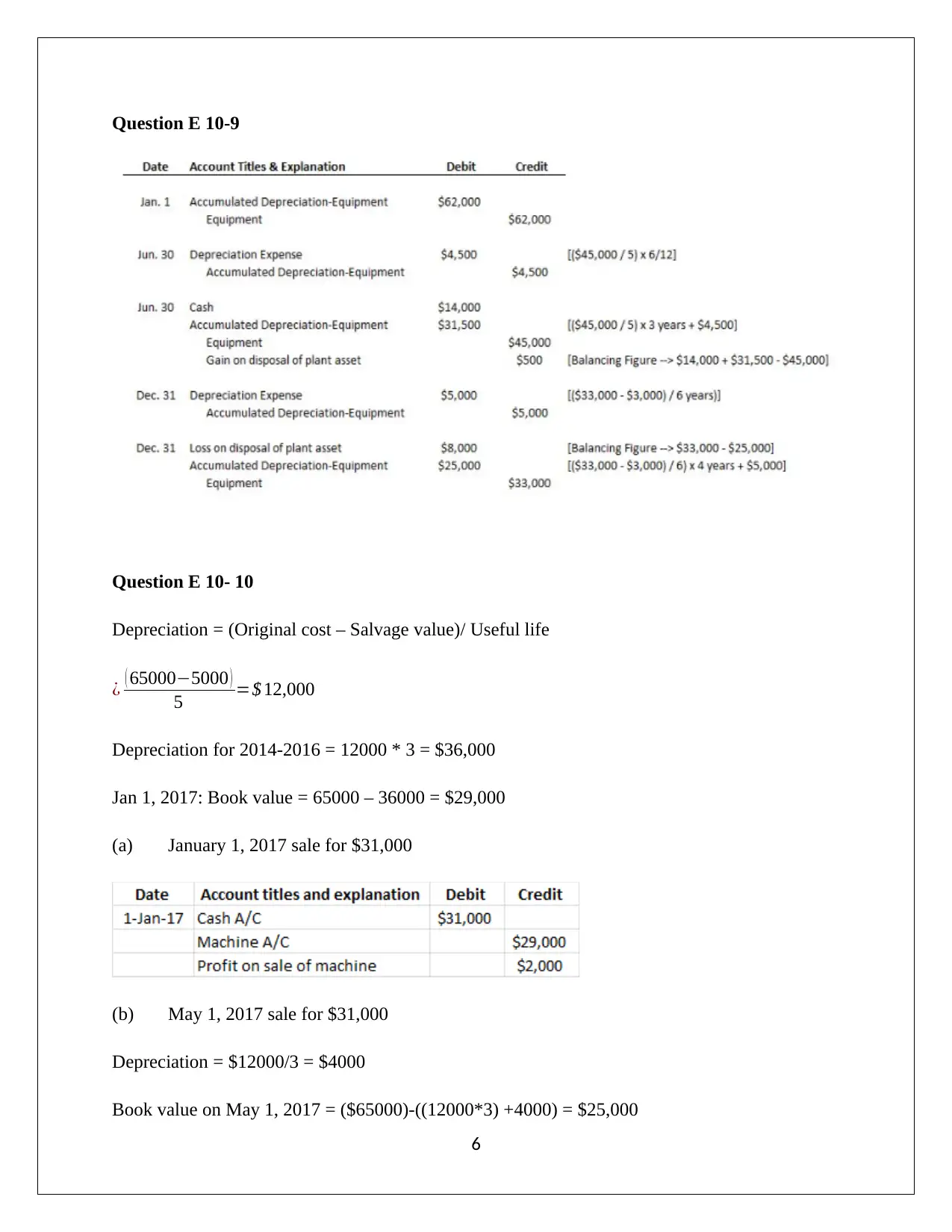

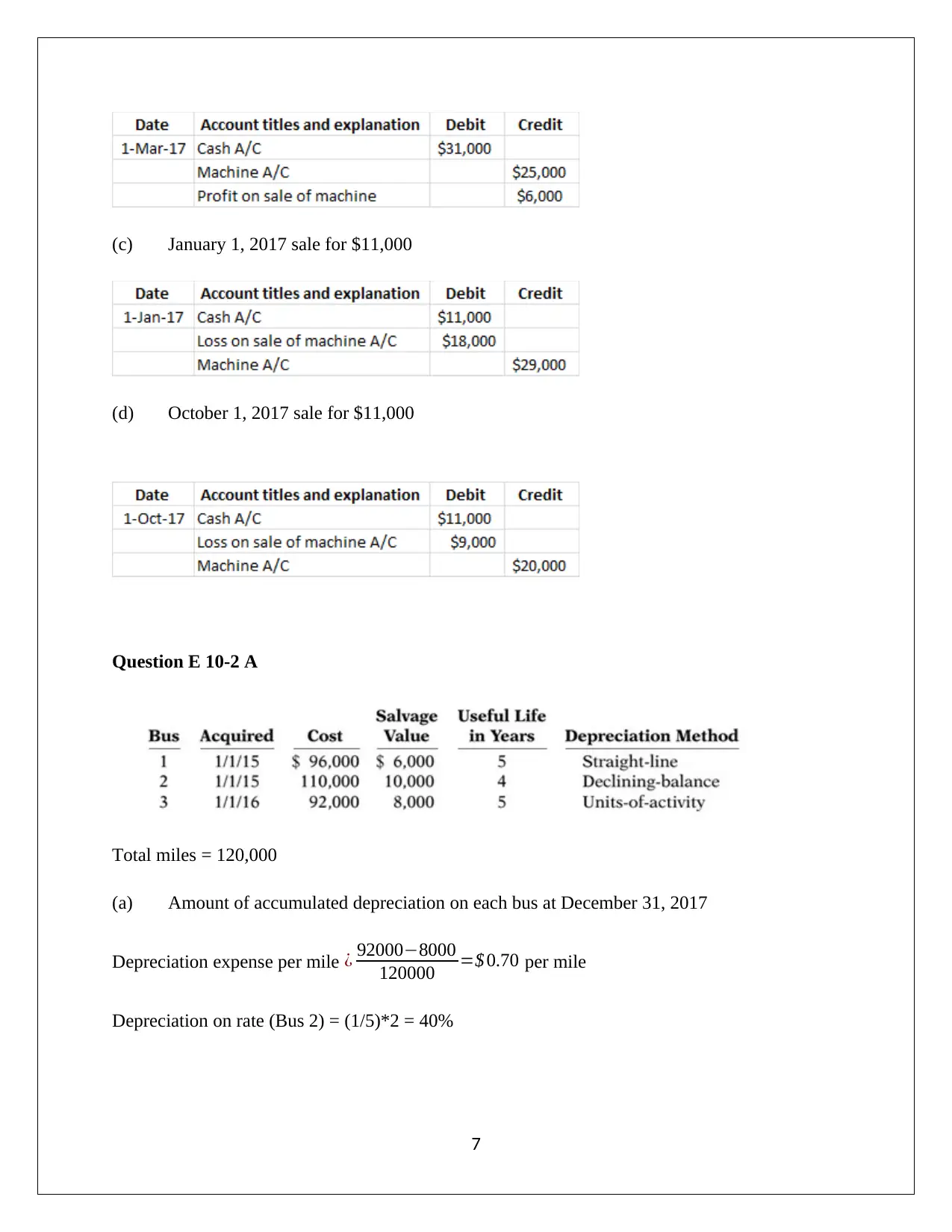

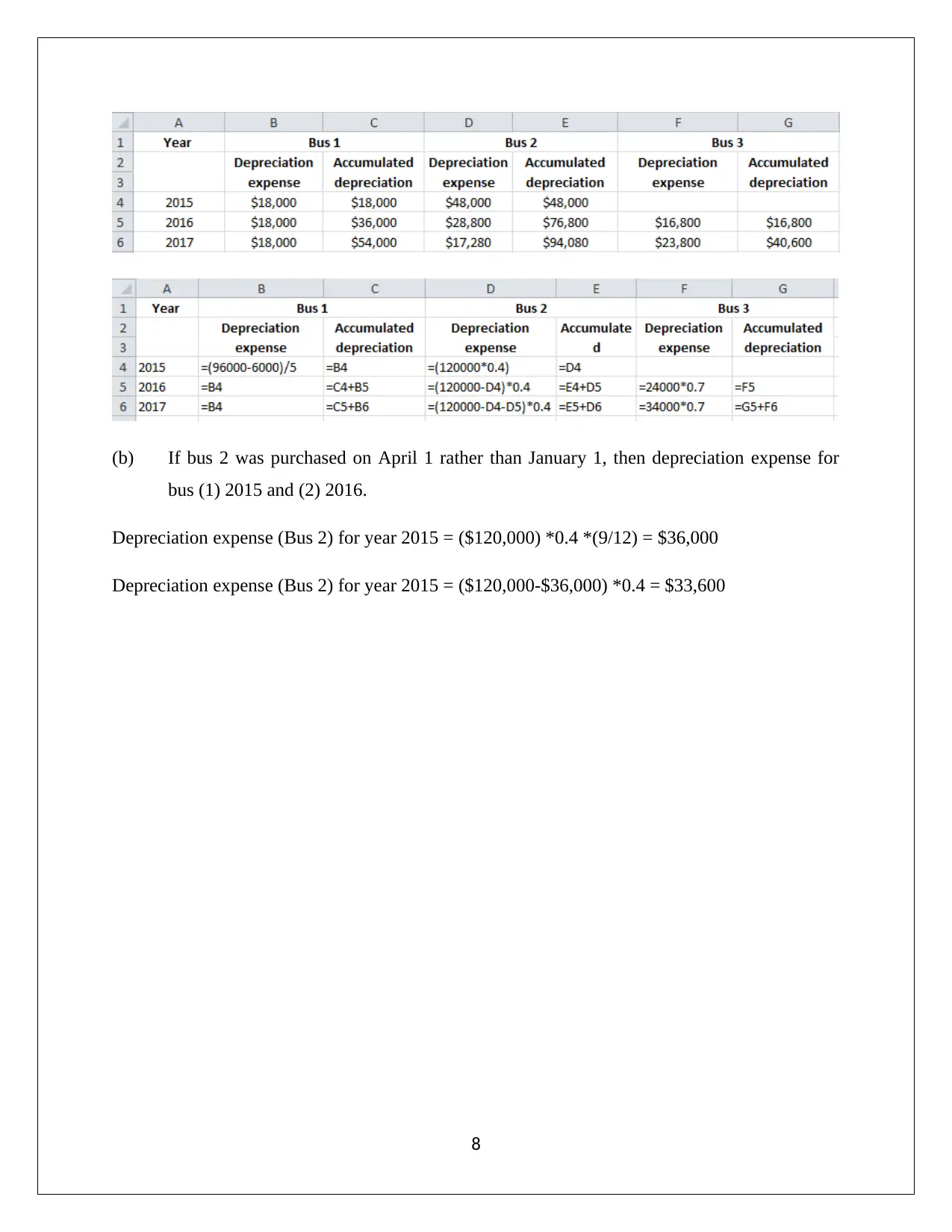

This business accounting report provides detailed solutions to problems related to depreciation methods, including straight-line, units of activity, and double-declining balance methods. It includes calculations for depreciation expense under different scenarios, such as changes in estimates and partial-year depreciation. Journal entries are provided to record depreciation and the sale of assets. The report also addresses the impact of different depreciation methods on financial statements and book value. It covers examples related to truck purchases, asset sales, and bus depreciation, offering a comprehensive overview of depreciation accounting principles. Desklib is a platform where students can find similar solved assignments and past papers to aid their studies.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.