Comprehensive Finance Report: Business and Accounting Analysis

VerifiedAdded on 2020/02/23

|19

|2252

|61

Report

AI Summary

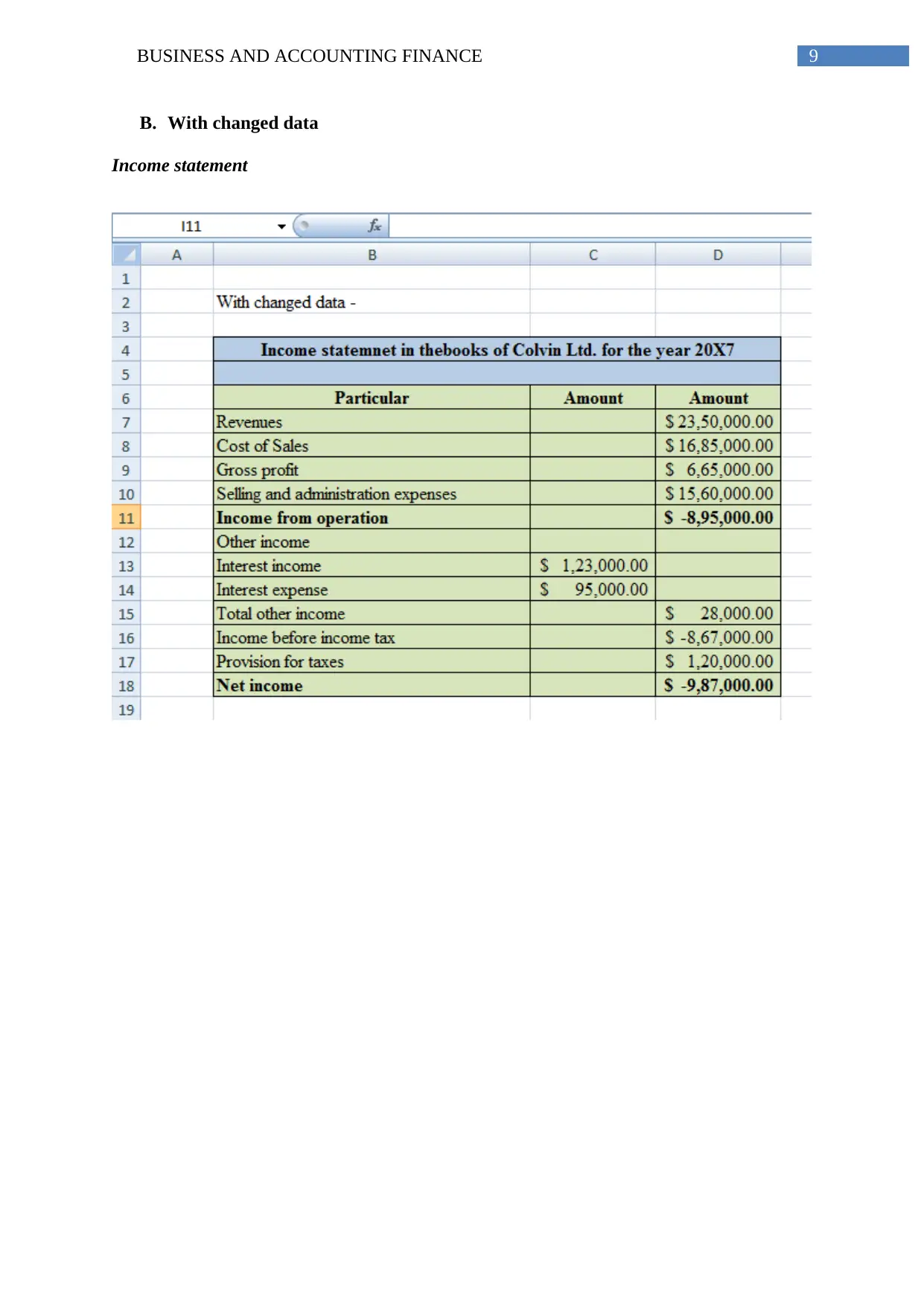

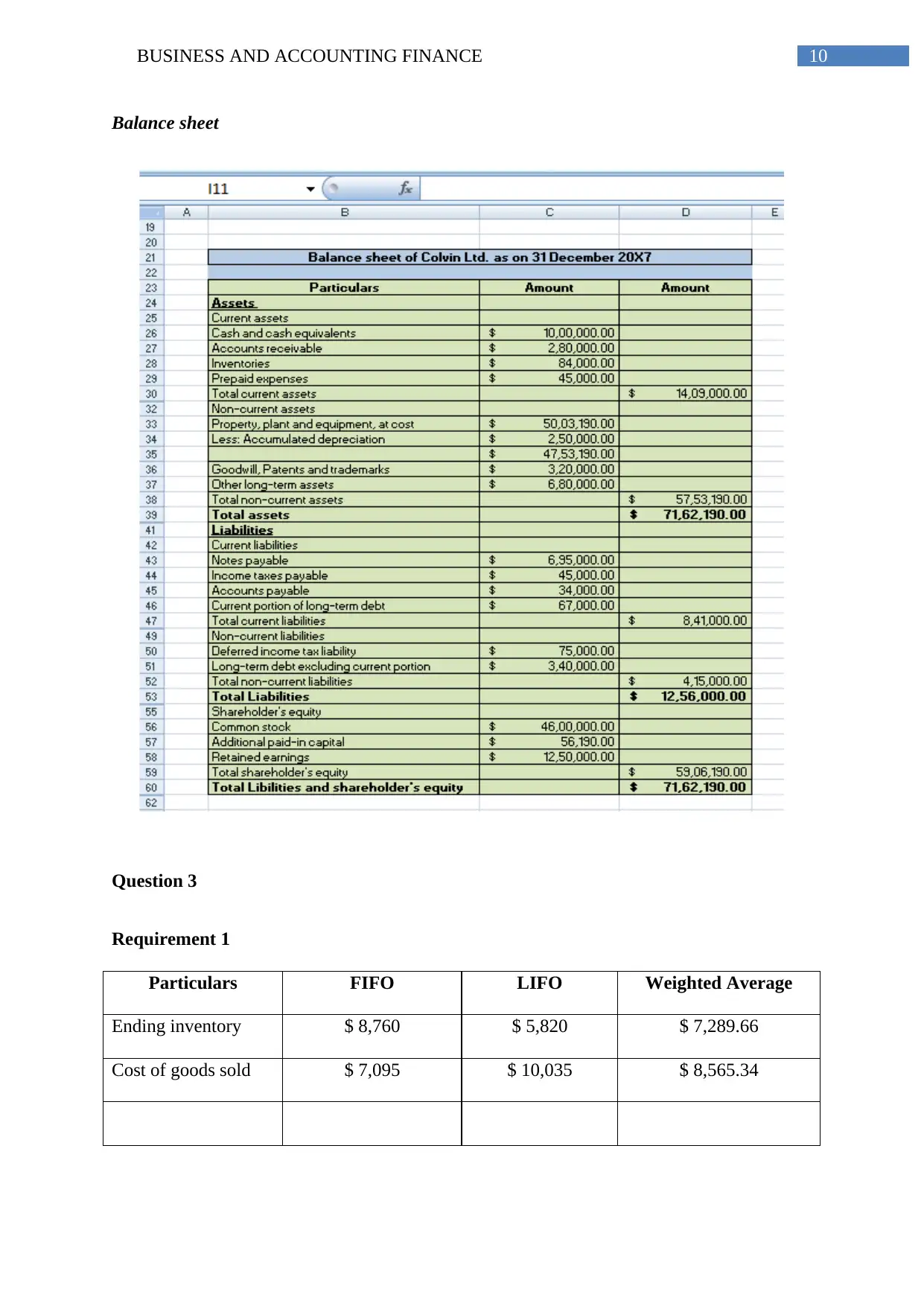

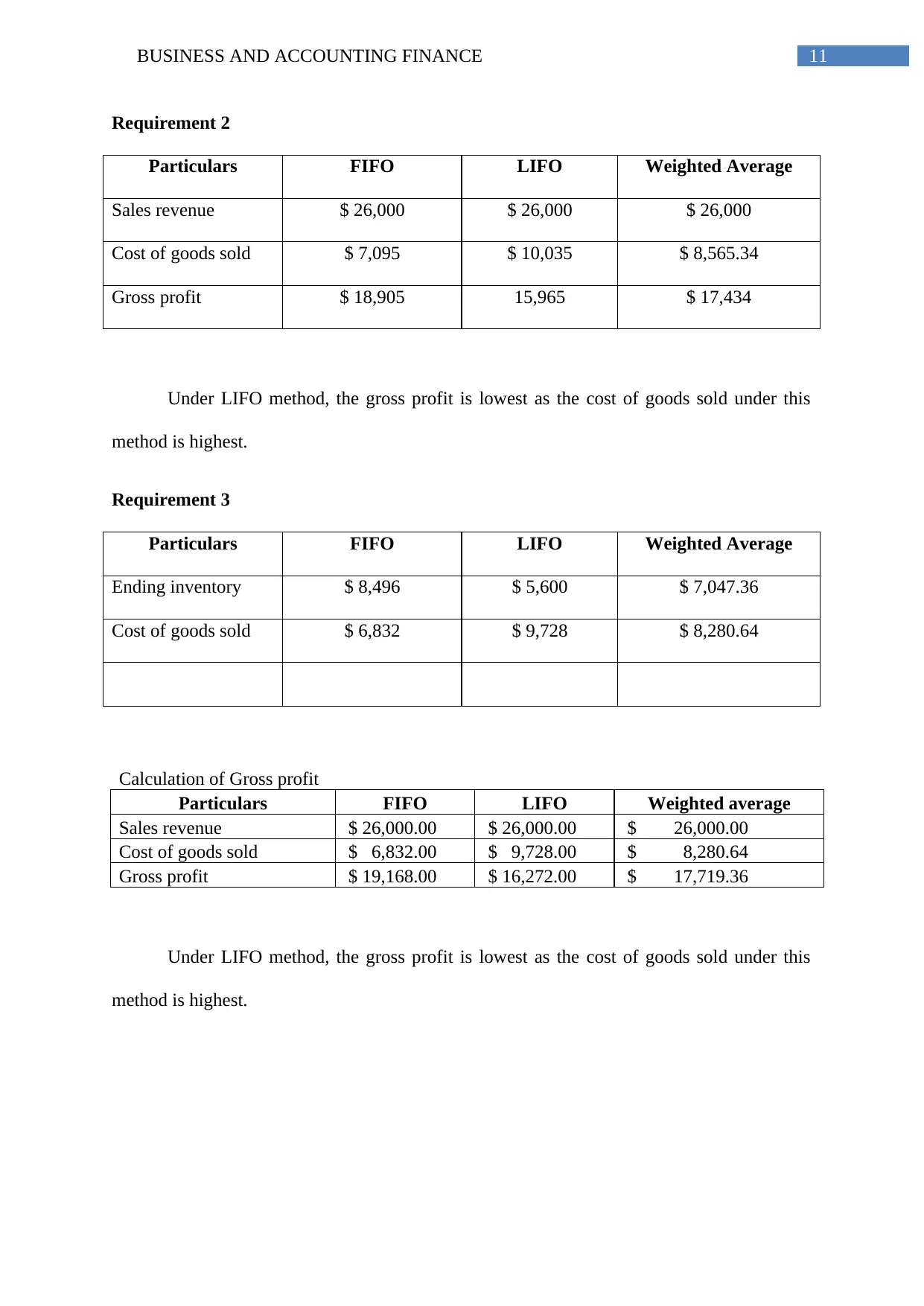

This report delves into the core concepts of business and accounting finance, presenting a comprehensive analysis of various financial aspects. It begins by defining key terms like accumulated depreciation and capitalization, followed by an exploration of inventory methods such as FIFO, LIFO, and weighted average, with illustrative examples. The report then analyzes financial statements including income statements and balance sheets, demonstrating the impact of different inventory methods on financial metrics. It further examines major financial reports and their purposes, emphasizing the importance of profits and cash flow, along with ethical considerations. Ratio analysis is conducted to compare financial performance, including rate of return and current ratio, using charts and calculations. The report concludes with business report elements for decision-making, touching upon digital dashboards and impression management in accounting, providing a well-rounded view of financial analysis and its practical applications.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.