Business Accounting Assignment: Trial Balance and Entries

VerifiedAdded on 2020/05/16

|14

|2159

|61

Homework Assignment

AI Summary

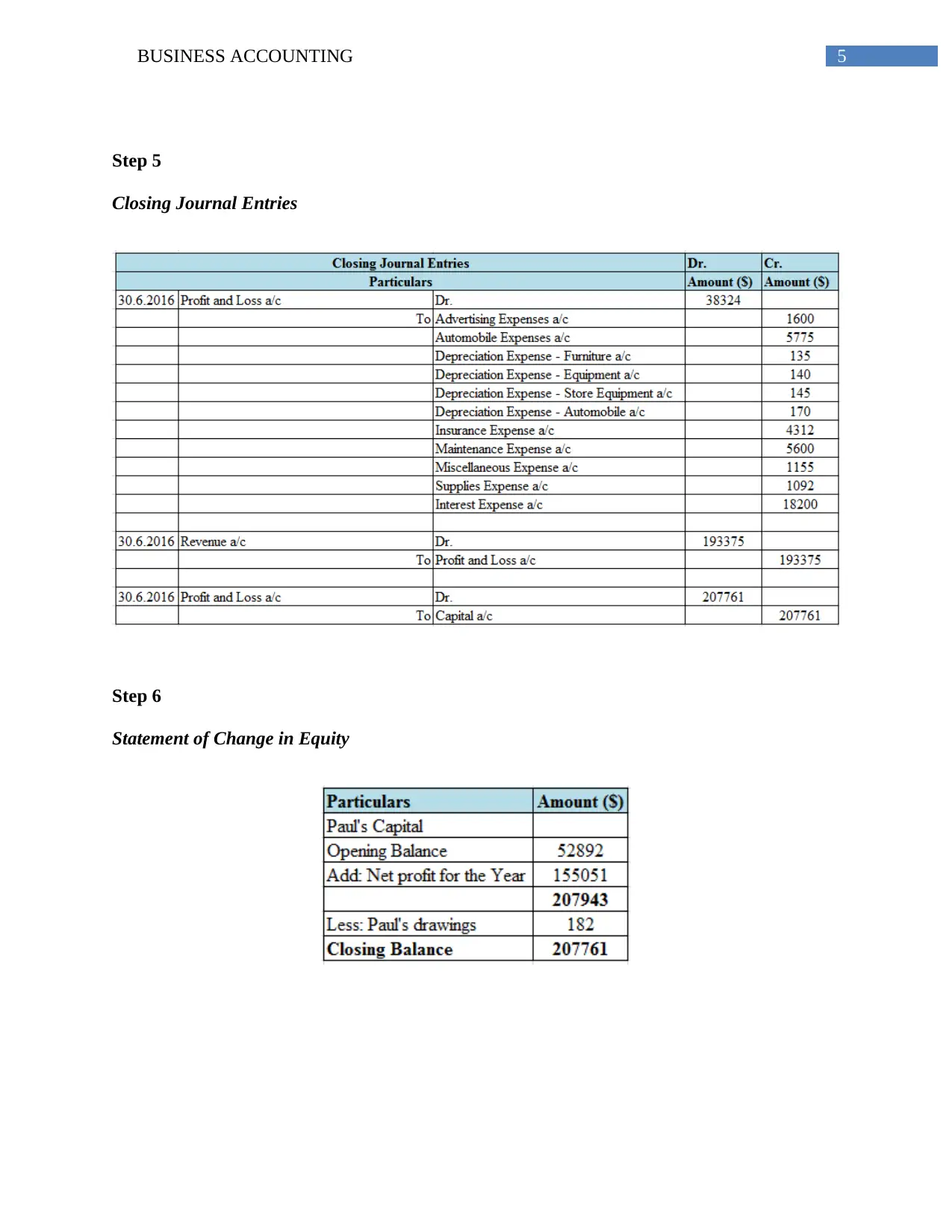

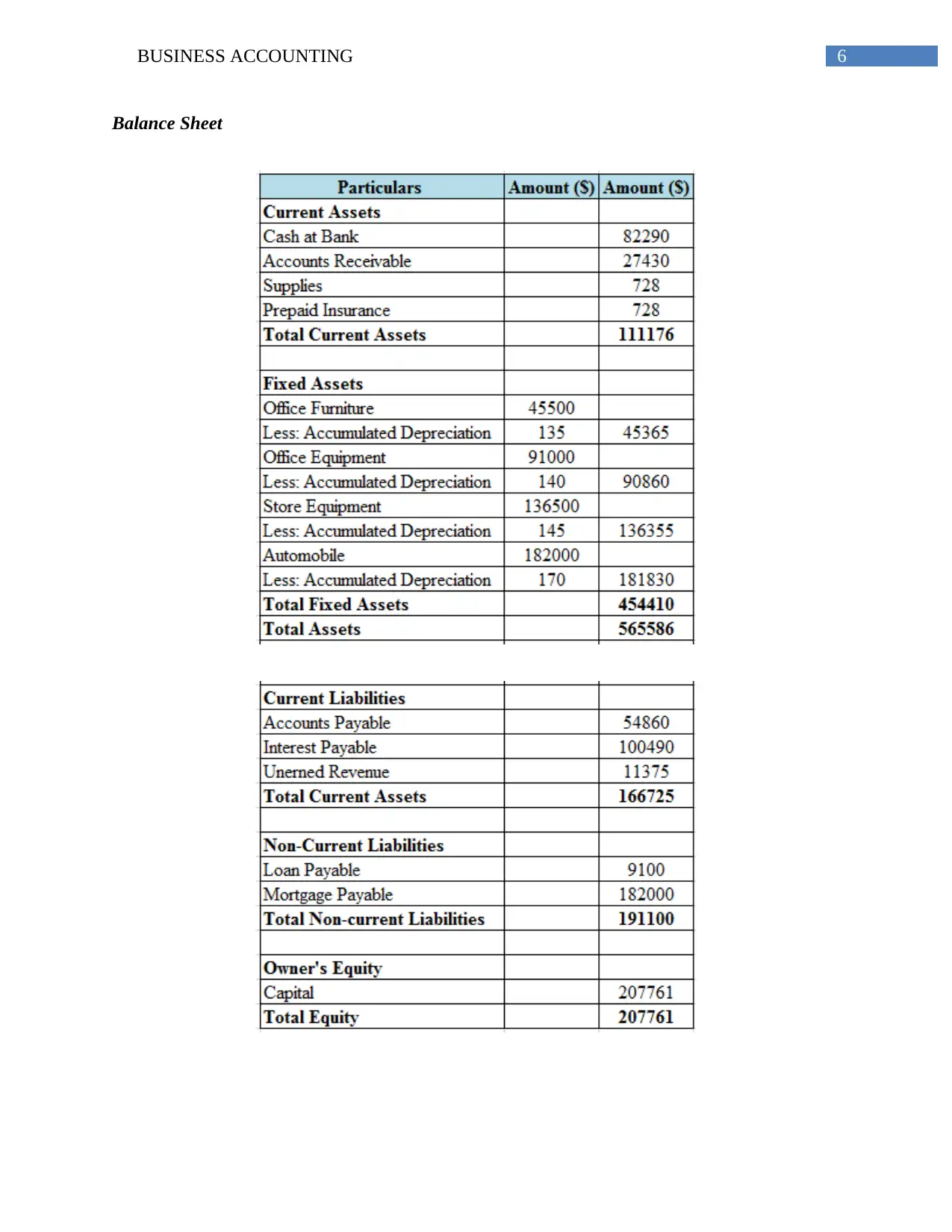

This document presents a comprehensive solution to a business accounting assignment, meticulously addressing key concepts such as trial balances, adjusting journal entries, and closing journal entries. The assignment delves into the significance of trial balances in detecting errors and ensuring the accuracy of financial records, highlighting their role in both manual and computerized accounting systems. It further explores the purpose and application of adjusting journal entries in aligning accounting records with the accrual basis of accounting, ensuring that revenues and expenses are accurately reflected in the correct accounting periods. The document also examines the adjusted trial balance, its function in correcting errors and preparing financial statements, and its role in facilitating the construction of essential financial reports like the balance sheet and statement of cash flows. Furthermore, the solution differentiates between adjusting and closing journal entries, emphasizing their distinct roles in the accounting cycle. References from various accounting textbooks and journals are included to support the analysis.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.