Business Accounting Assignment: Questions and Detailed Solutions

VerifiedAdded on 2022/11/30

|15

|2371

|78

Homework Assignment

AI Summary

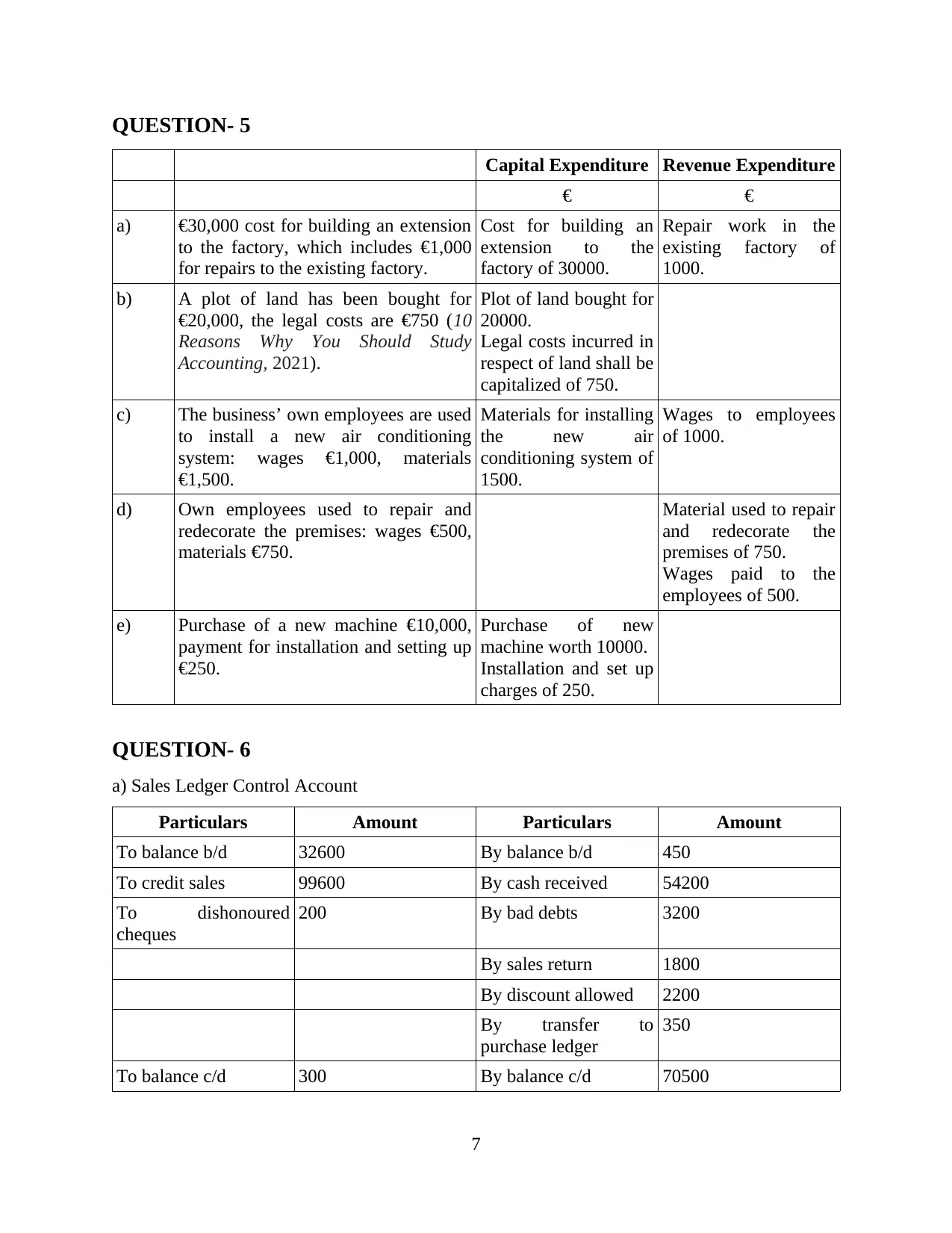

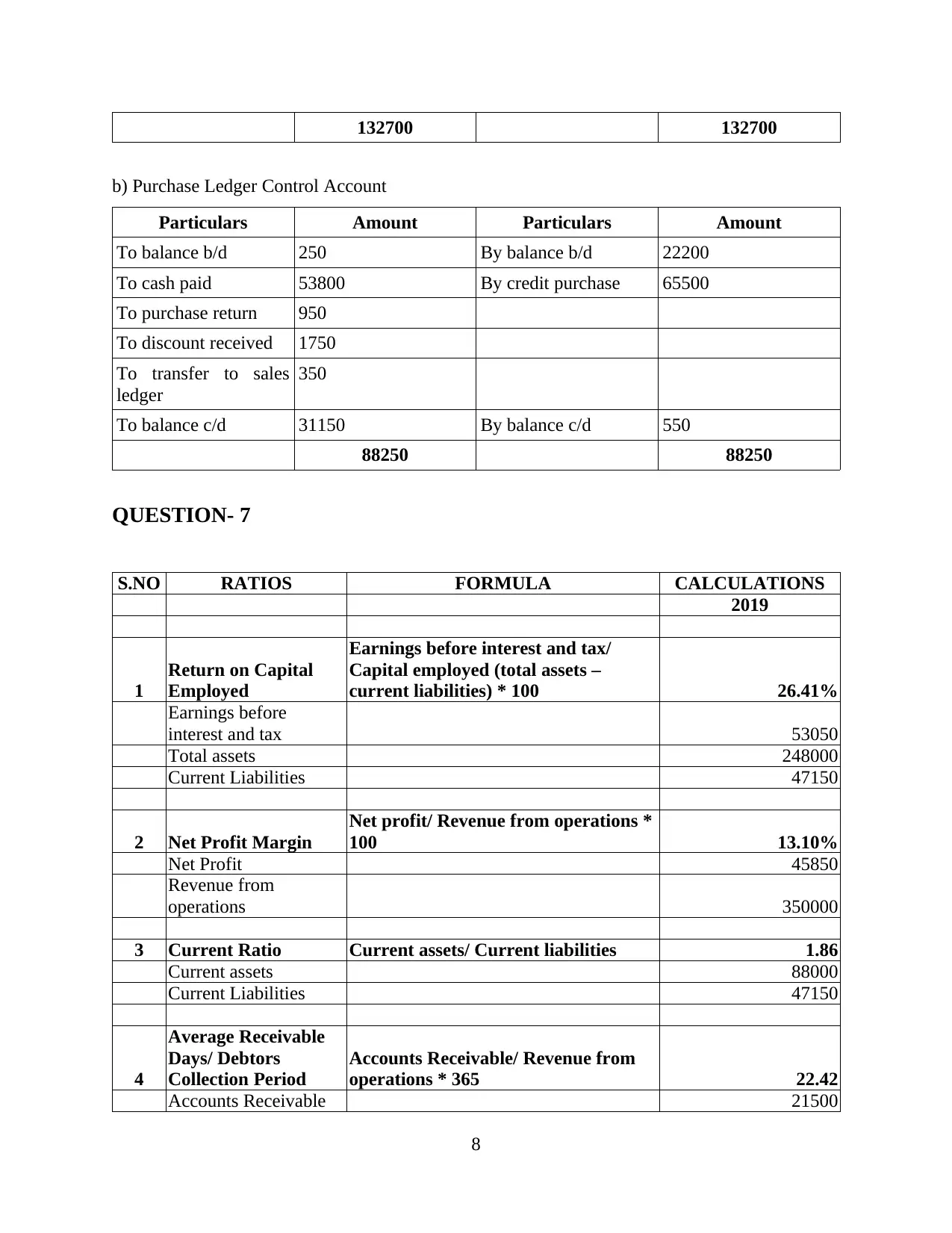

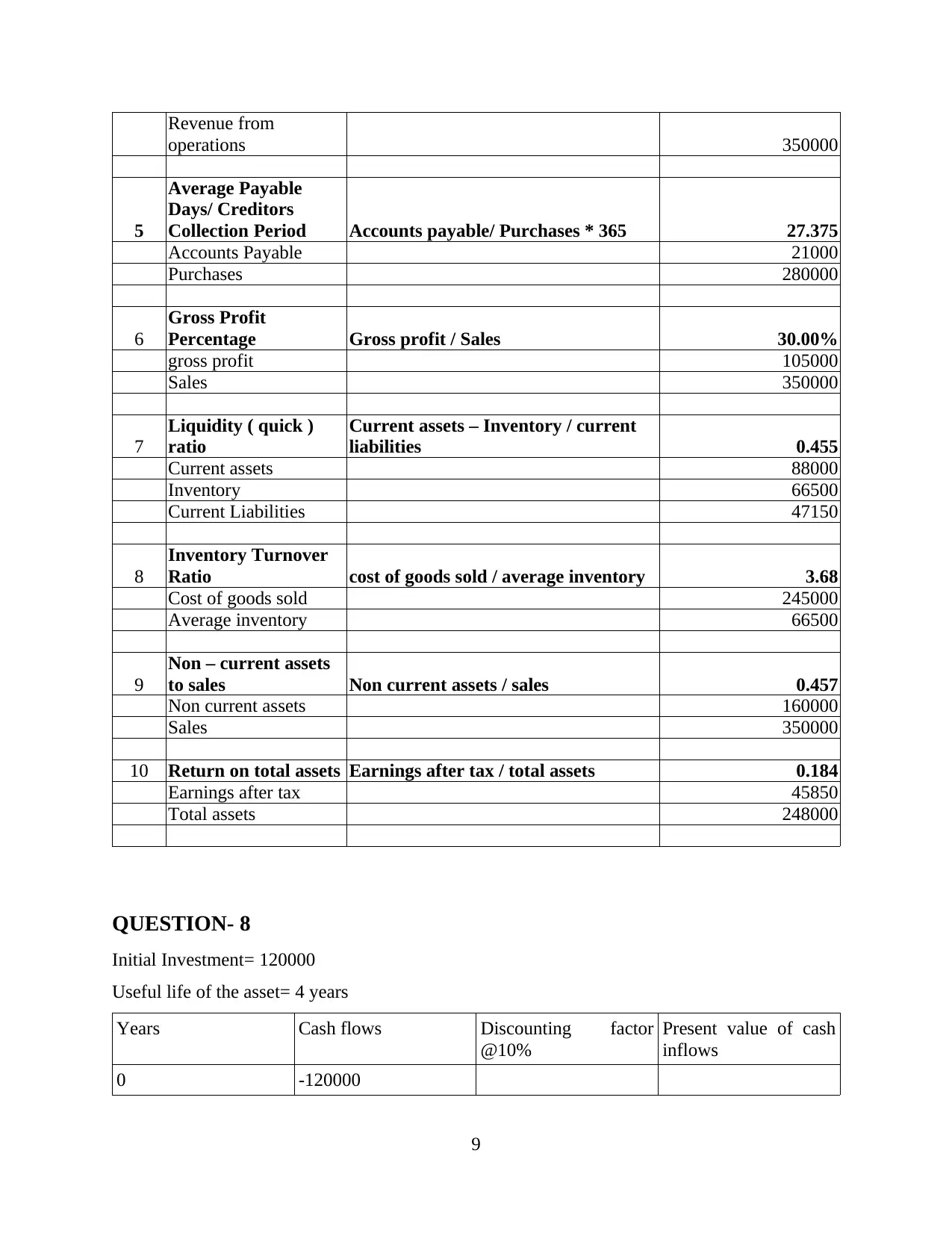

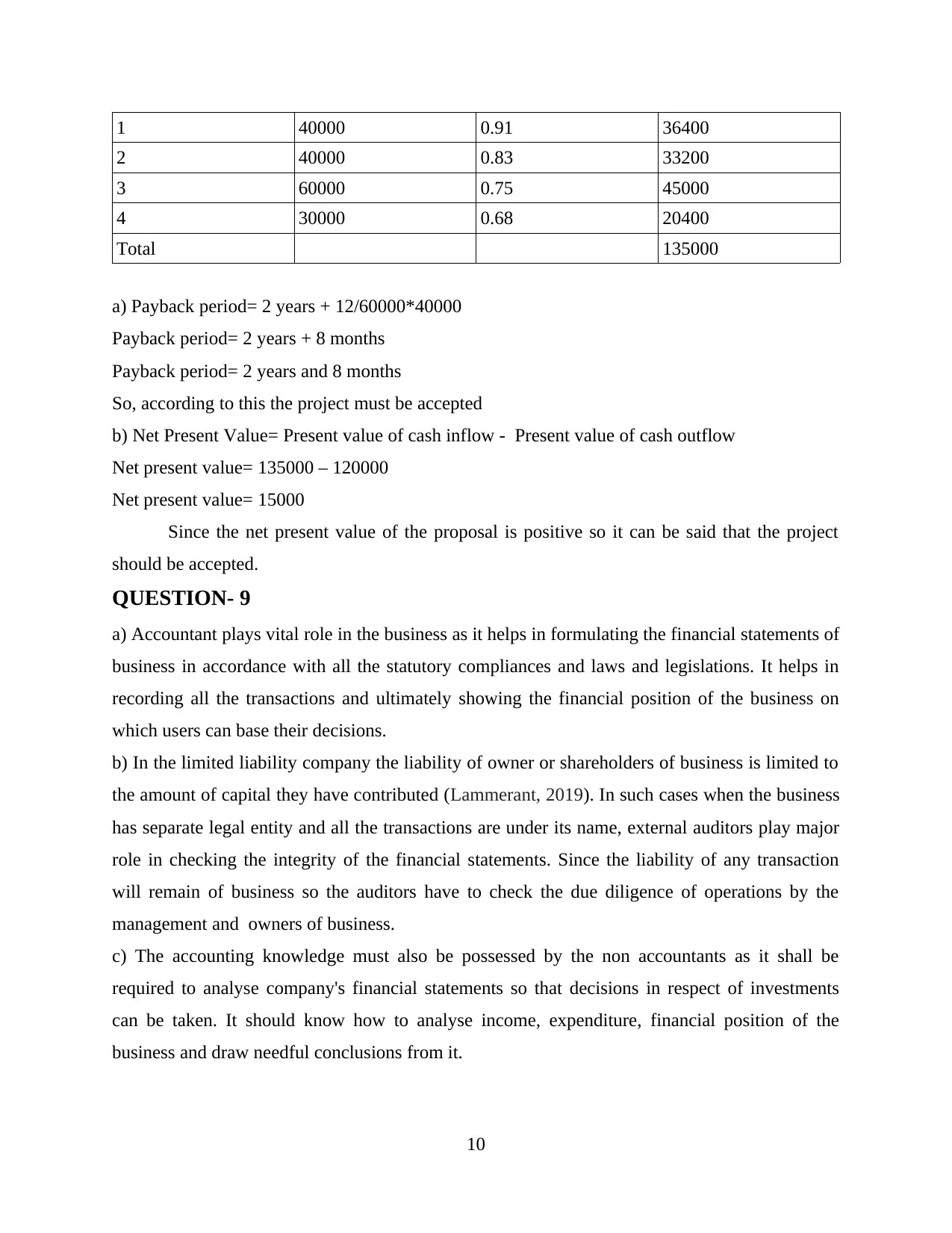

This comprehensive document provides detailed solutions to a variety of business accounting questions. It begins with basic double-entry bookkeeping, including the double-entry equation and the dual aspect of transactions. It then moves on to ledger accounts, trial balances, and the preparation of profit and loss statements and balance sheets. The assignment also covers capital versus revenue expenditure, control accounts, financial ratios, and investment appraisal techniques such as net present value and payback period. Furthermore, the document includes discussions on the role of accountants, the impact of limited liability, the importance of accounting knowledge for non-accountants, statutory requirements for management accounting, and the nature and purpose of accounting. Finally, it defines key accounting terms such as depreciation, allowance for bad debts, debentures, preference shares, and ordinary shares. This resource is designed to provide students with a thorough understanding of core accounting concepts and practical application.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.