Business Accounting Exam - 119LON - Business Development Module

VerifiedAdded on 2023/01/07

|13

|2140

|55

Homework Assignment

AI Summary

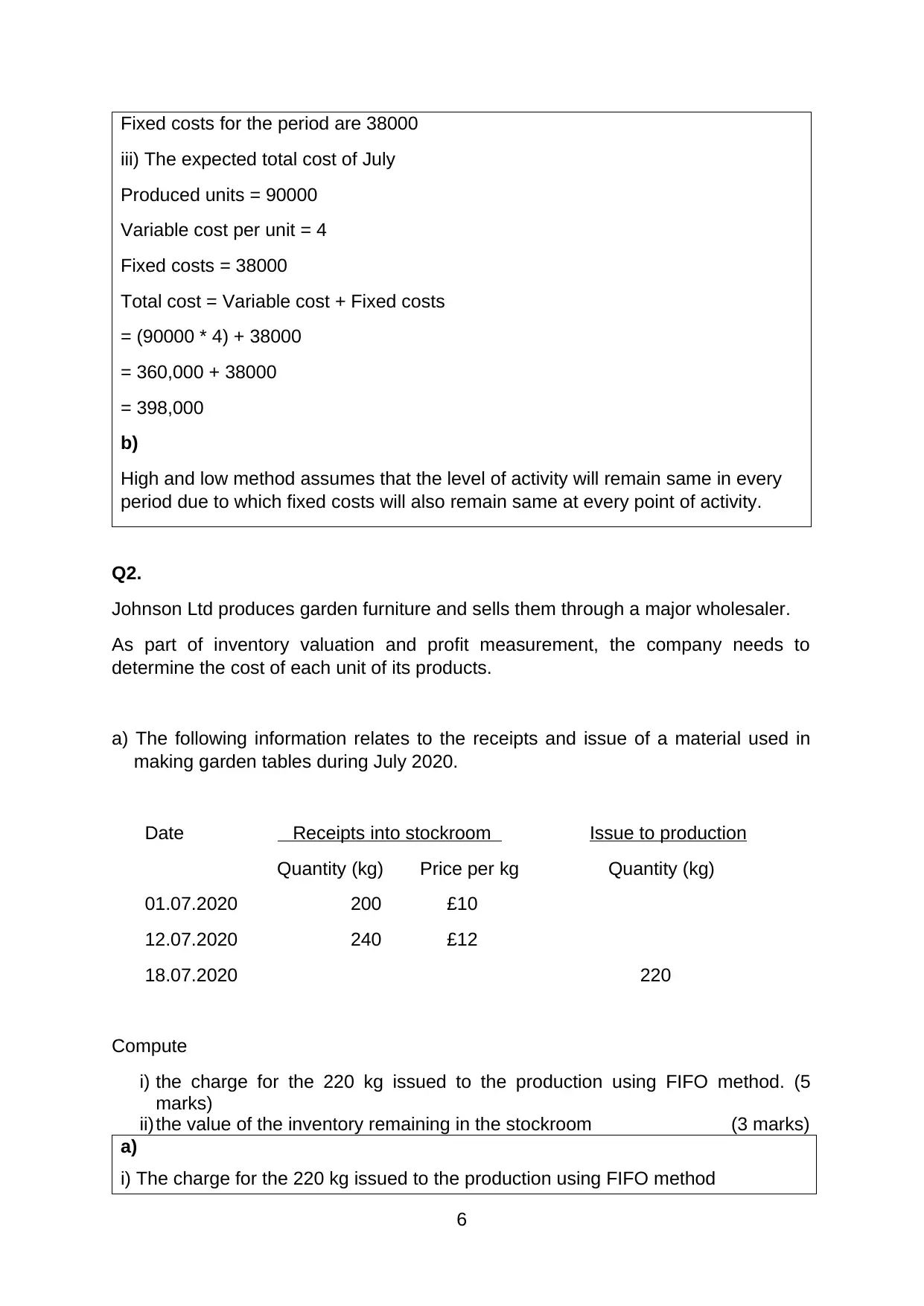

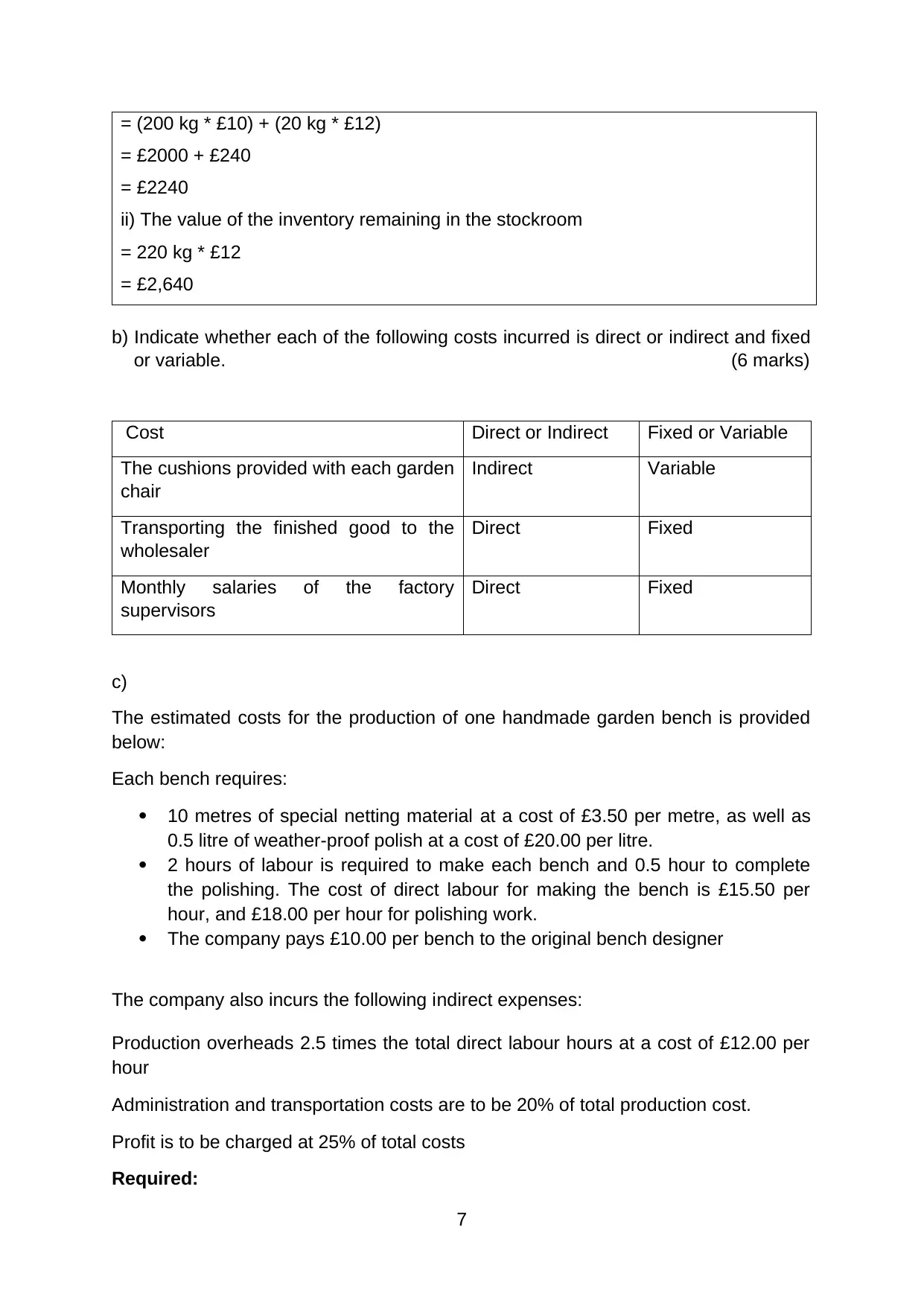

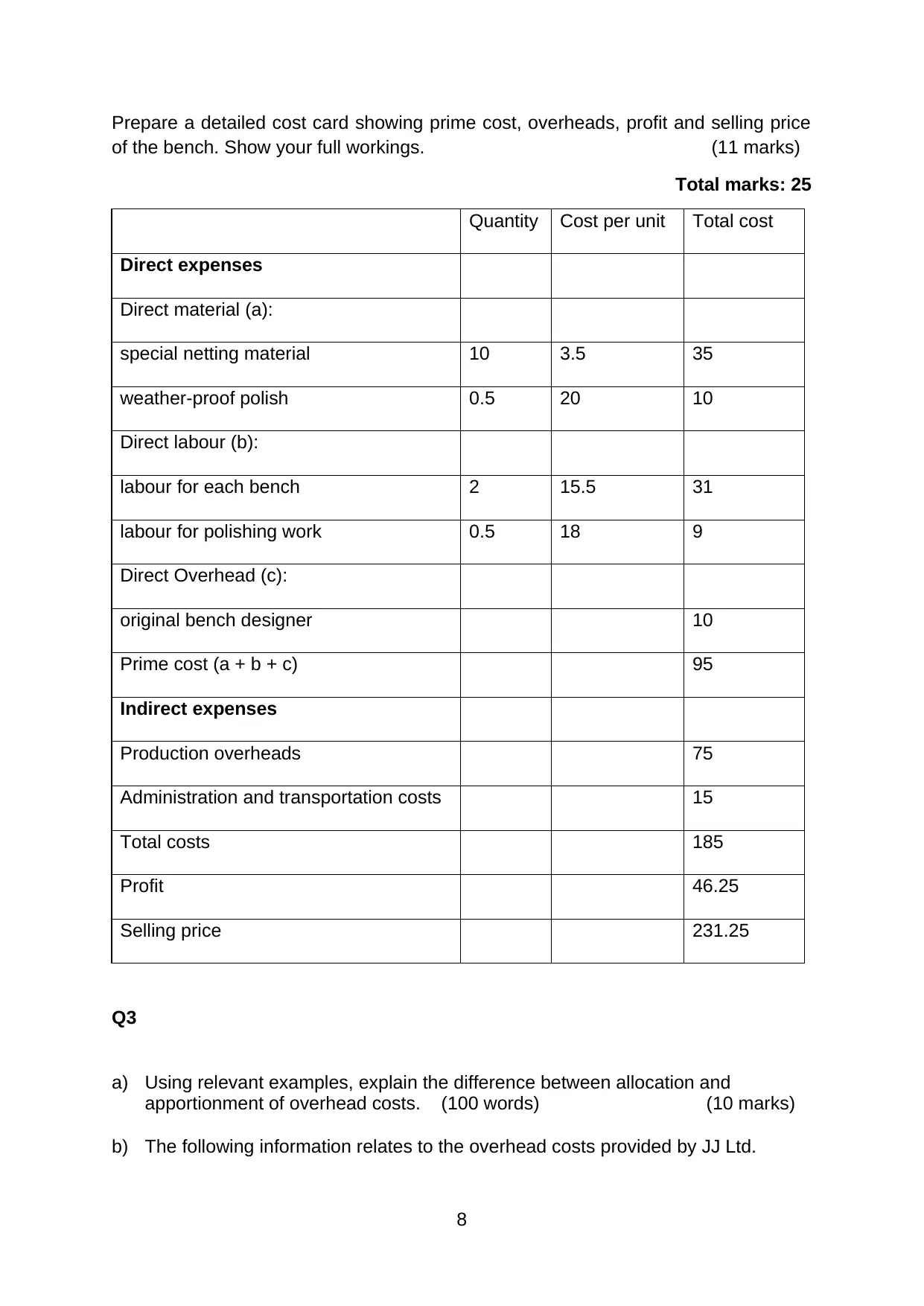

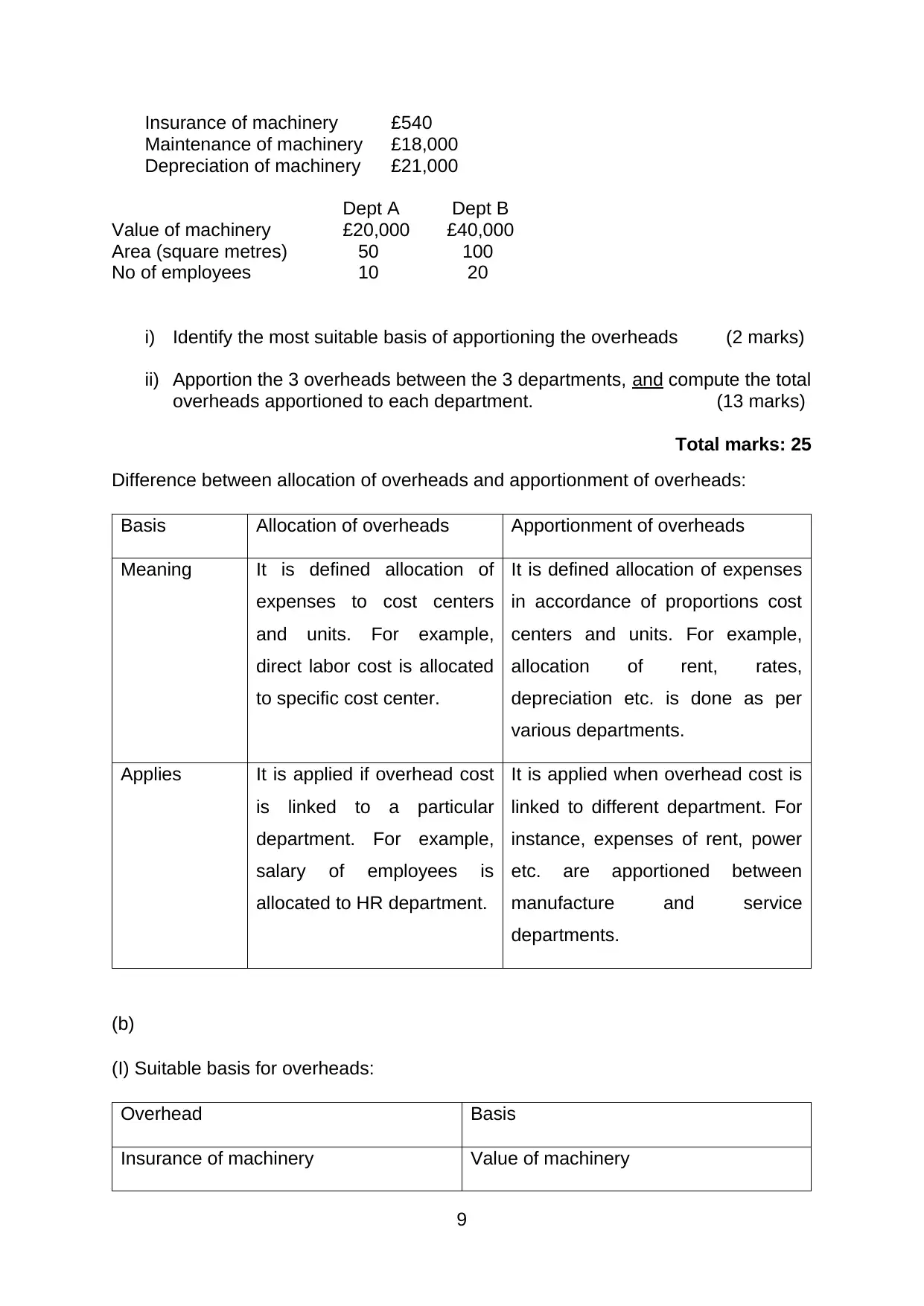

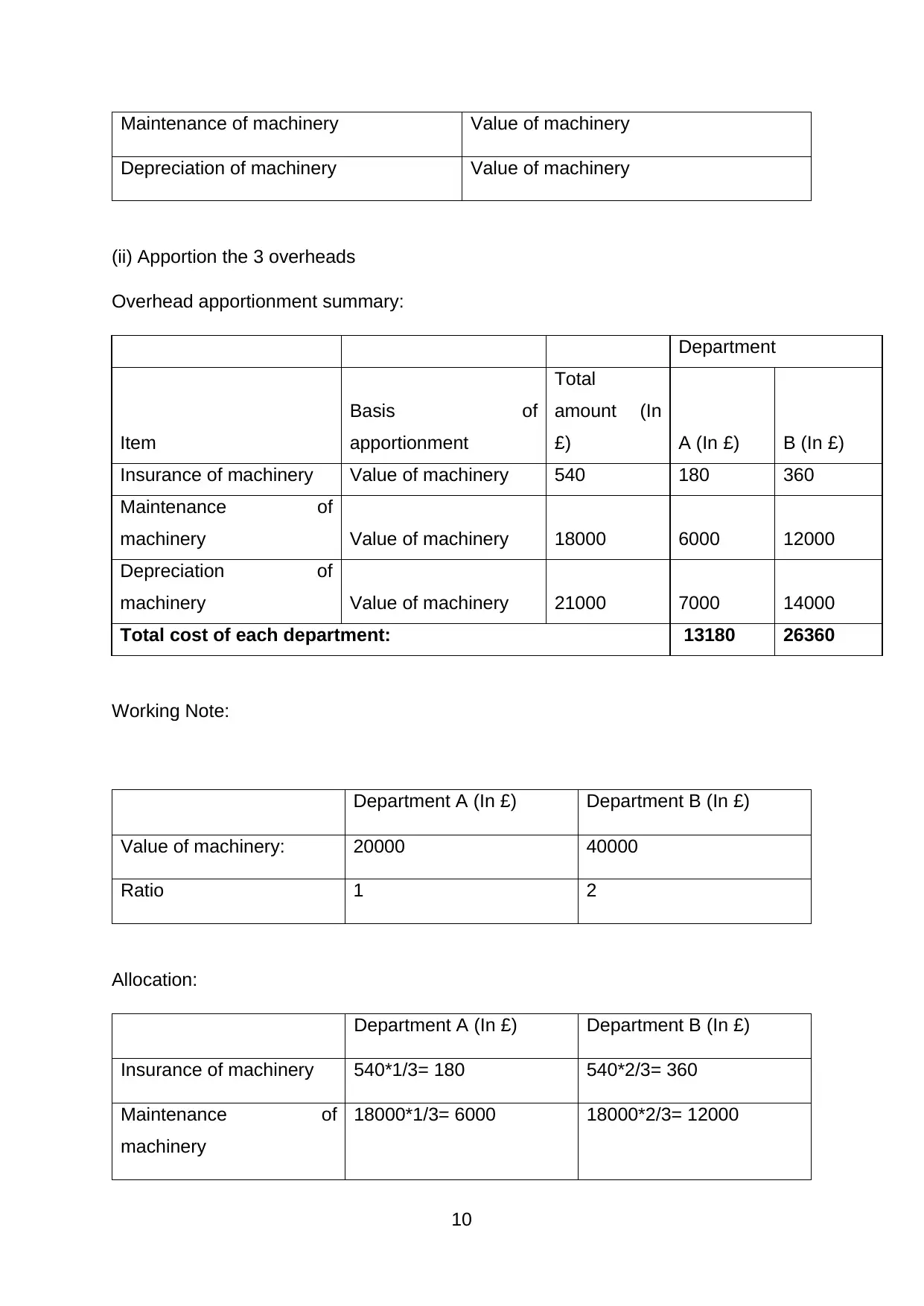

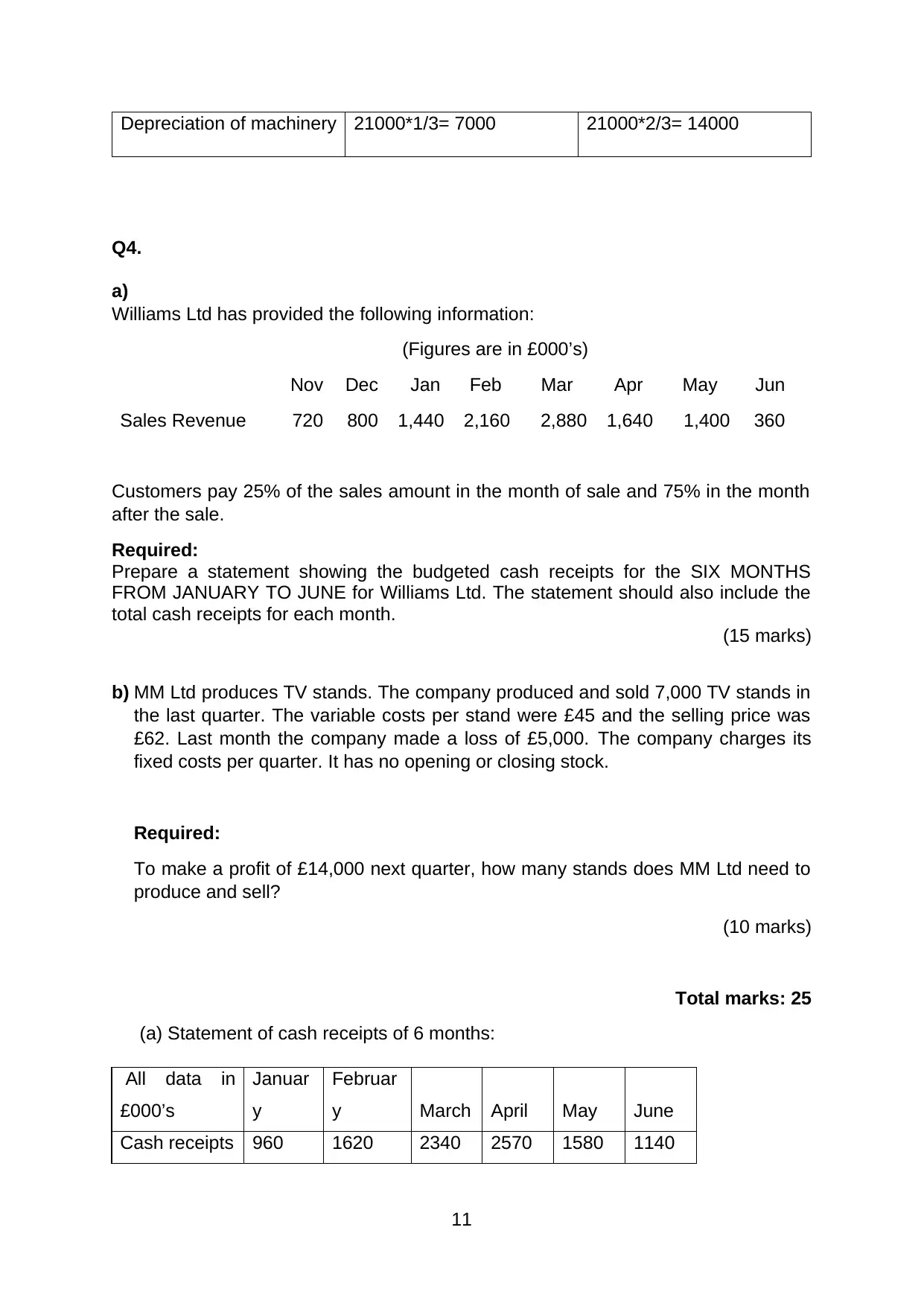

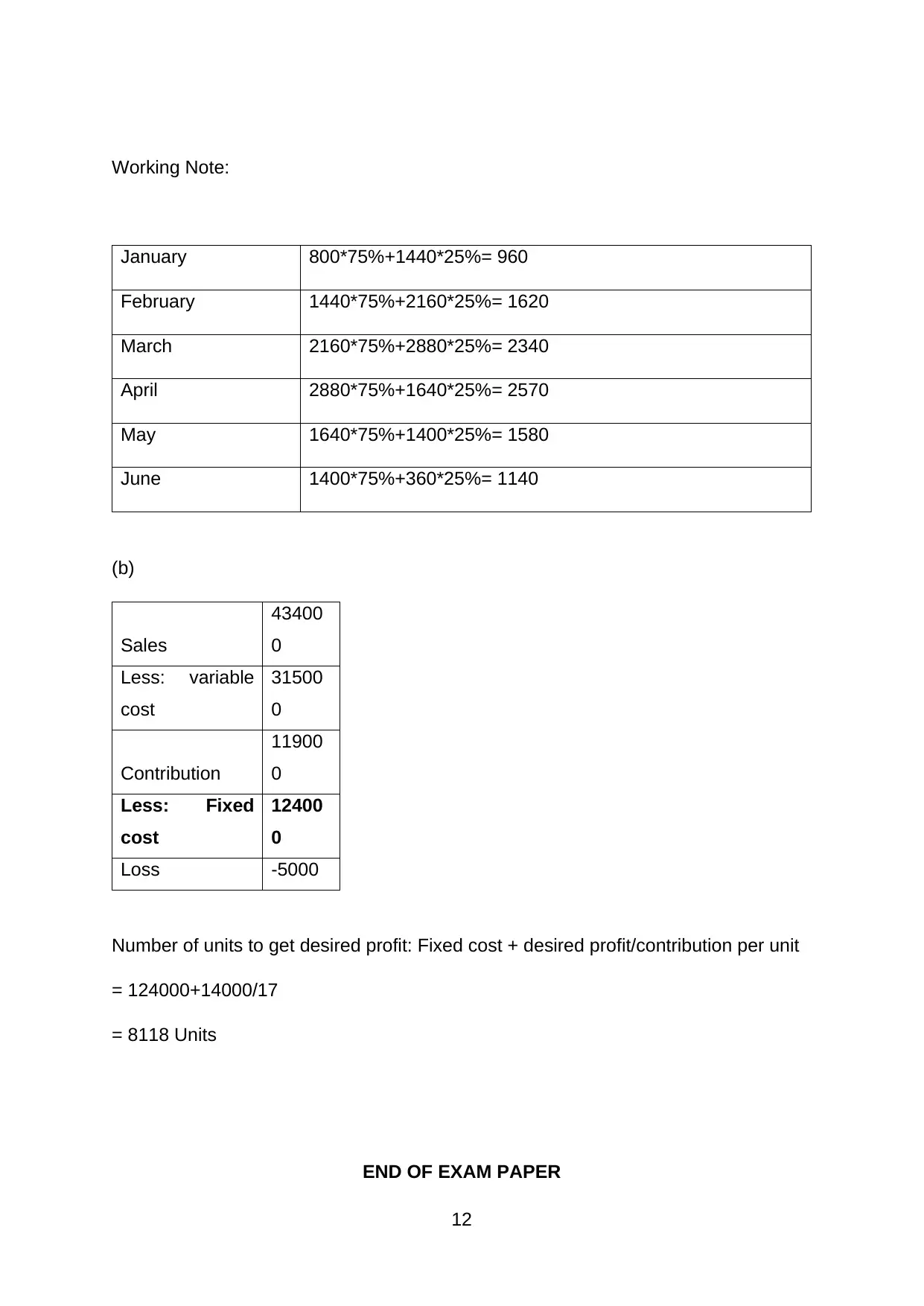

This document presents a detailed solution to a Business Accounting exam, comprising two sections, A and B. Section A encompasses multiple-choice questions covering fundamental accounting concepts like prime cost, marginal costing, and overheads. Section B delves into problem-solving, including cost analysis using the high-low method, inventory valuation with FIFO, and the allocation of overhead costs. The solution also addresses cash receipts forecasting and profit calculations, providing step-by-step workings and explanations for each question. The exam assesses the candidate's understanding of cost accounting, financial analysis, and the application of accounting principles in a business context.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.