Business Management Accounting Report: Woodrock & Plaistead Analysis

VerifiedAdded on 2023/01/05

|17

|3663

|91

Report

AI Summary

This report delves into the core principles of business management accounting, offering a comprehensive analysis of various financial techniques. It begins with an introduction to management accounting and its significance, followed by a detailed examination of Woodrock Limited's cash position, including a cash budget analysis and recommendations for improvement. The report then explores Plaistead Plc, utilizing marginal costing techniques to identify the best business strategy, including break-even analysis, profit calculations, and the impact of different sales strategies. Finally, it covers standard costing variance calculations, providing a thorough understanding of budget preparation and variance analysis for Jayrod Plc. The report aims to provide a practical understanding of how management accounting tools can be used for effective decision-making and financial planning in business organizations.

Business Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Meaning of management accounting and its importance towards the organization...................1

QUESTION 1...................................................................................................................................2

Review on cash position of Woodrock Limited .............................................................................2

QUESTION 2...................................................................................................................................5

Analysis of best strategy for Plaistead Plc using marginal costing technique.............................5

QUESTION 4...................................................................................................................................8

Calculation of standard costing variance.....................................................................................8

CONCLUSION..............................................................................................................................12

REFRENCES.................................................................................................................................13

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Meaning of management accounting and its importance towards the organization...................1

QUESTION 1...................................................................................................................................2

Review on cash position of Woodrock Limited .............................................................................2

QUESTION 2...................................................................................................................................5

Analysis of best strategy for Plaistead Plc using marginal costing technique.............................5

QUESTION 4...................................................................................................................................8

Calculation of standard costing variance.....................................................................................8

CONCLUSION..............................................................................................................................12

REFRENCES.................................................................................................................................13

INTRODUCTION

Management accounting , this term is define systematic procedure of using and

representing accounting g information for internal user of the business organization. It is part of

accounting , which is generally applied by manager in their business corporation so they can

record all the transaction bin effective manner and reduce chances arise of errors. This report is

prepared to solve problem of different organization by applying technique of management

accounting. By making cash , flexible budget and computing variance as well as break even ,

margin safety and P/V ratio, in his report help in arising knowledge and understanding of

importance of managerial accounting in running business corporations. To control cost and arise

business profit by making attractive ,and reliable budget.

MAIN BODY

Meaning of management accounting and its importance towards the organization

Management accounting: Business strategy used for analysis, recording, computing and

presenting accounting information in effective way , which help in systematic decision making

process. It is part of management function. Accounting department by using this technique

accounting, record all the essential transaction in ethical way. This is essential tool which useful

in run business activity in effective way. Following are the role of management accounting :

Decision making: Manager apply tools of this accounting strategy which help in tasking

decision regarding which alternative is best .By applying marginal costing, and methods

of budgeting manager can easily recognize, which project useful in providing future

benefit for the organization (Alyousef, and Mickan, 2016).

Cutting cost: Business organizations by applying technique of computation of cost can

understand activities which become the reason of extra incurring of cost . This help in

making policies to cut cost of theses business activities. Which help in generating profit.

Optimum utilisation of resource: By identifying allocation of resource according to

business activity as well as cutting cost also useful in properly use scare resource special

finance resource of the business organization.

Making pricing strategy: Management accounting help in providing best pricing

strategy, through which organization take decision regarding selection of price for their

1

Management accounting , this term is define systematic procedure of using and

representing accounting g information for internal user of the business organization. It is part of

accounting , which is generally applied by manager in their business corporation so they can

record all the transaction bin effective manner and reduce chances arise of errors. This report is

prepared to solve problem of different organization by applying technique of management

accounting. By making cash , flexible budget and computing variance as well as break even ,

margin safety and P/V ratio, in his report help in arising knowledge and understanding of

importance of managerial accounting in running business corporations. To control cost and arise

business profit by making attractive ,and reliable budget.

MAIN BODY

Meaning of management accounting and its importance towards the organization

Management accounting: Business strategy used for analysis, recording, computing and

presenting accounting information in effective way , which help in systematic decision making

process. It is part of management function. Accounting department by using this technique

accounting, record all the essential transaction in ethical way. This is essential tool which useful

in run business activity in effective way. Following are the role of management accounting :

Decision making: Manager apply tools of this accounting strategy which help in tasking

decision regarding which alternative is best .By applying marginal costing, and methods

of budgeting manager can easily recognize, which project useful in providing future

benefit for the organization (Alyousef, and Mickan, 2016).

Cutting cost: Business organizations by applying technique of computation of cost can

understand activities which become the reason of extra incurring of cost . This help in

making policies to cut cost of theses business activities. Which help in generating profit.

Optimum utilisation of resource: By identifying allocation of resource according to

business activity as well as cutting cost also useful in properly use scare resource special

finance resource of the business organization.

Making pricing strategy: Management accounting help in providing best pricing

strategy, through which organization take decision regarding selection of price for their

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business organization. They choose price which satisfy customer as well as help in

gearing profit.

Help in environment scanning process: Marginal costing, standard costing and system

of management accounting useful in identifying effect of external as well as internal

department of production and distribution procedure .

Provide base for preparing budget: Planing tool of management accounting as well as

its system useful in given accurate information regarding formulating future as well as

current budget. This help manager to identifying future business opportunities.

Risk analysis: Management accounting useful in assessment of risk, by making budget,

organization able to identifying risk and on the basis of that they formulate future

policies to avoid theses risk.

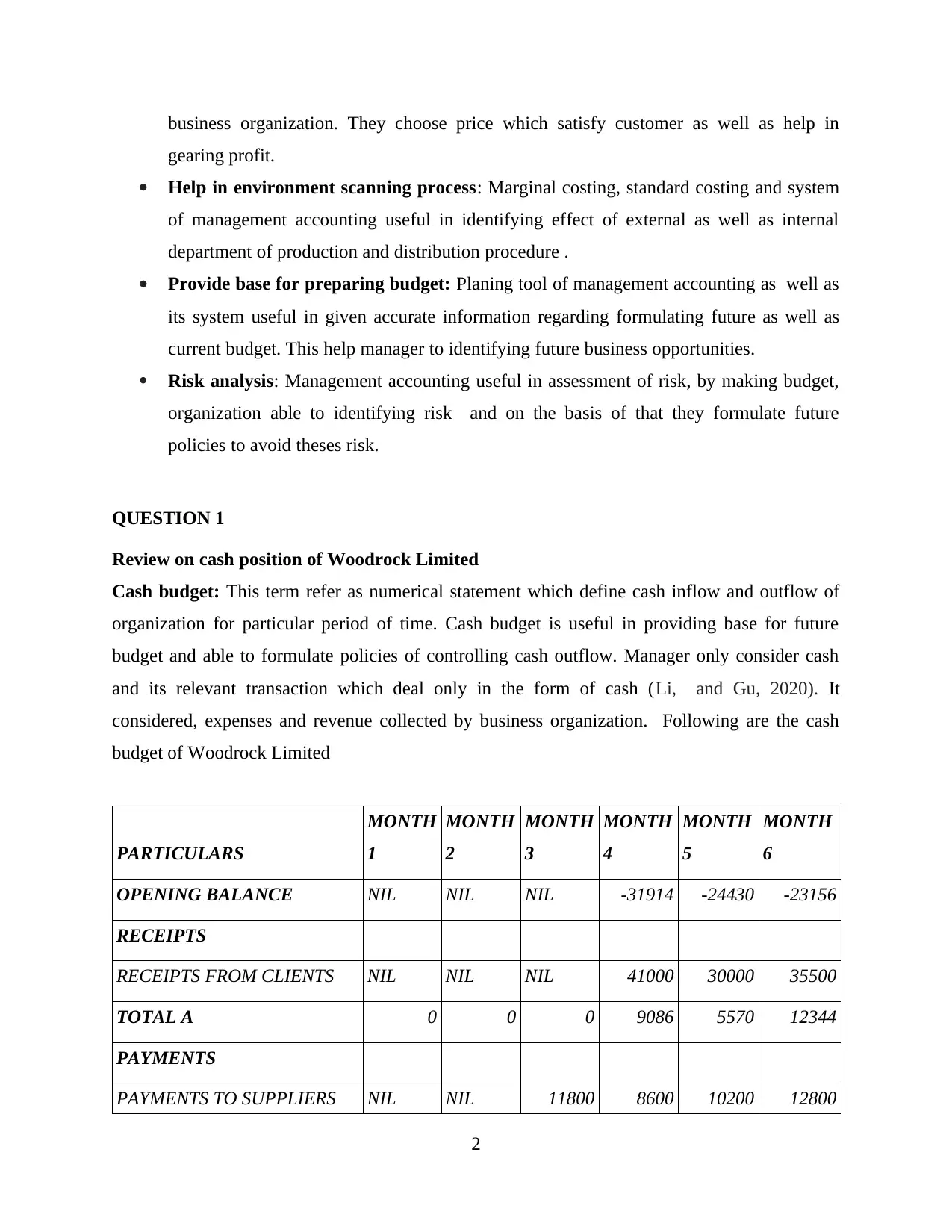

QUESTION 1

Review on cash position of Woodrock Limited

Cash budget: This term refer as numerical statement which define cash inflow and outflow of

organization for particular period of time. Cash budget is useful in providing base for future

budget and able to formulate policies of controlling cash outflow. Manager only consider cash

and its relevant transaction which deal only in the form of cash (Li, and Gu, 2020). It

considered, expenses and revenue collected by business organization. Following are the cash

budget of Woodrock Limited

PARTICULARS

MONTH

1

MONTH

2

MONTH

3

MONTH

4

MONTH

5

MONTH

6

OPENING BALANCE NIL NIL NIL -31914 -24430 -23156

RECEIPTS

RECEIPTS FROM CLIENTS NIL NIL NIL 41000 30000 35500

TOTAL A 0 0 0 9086 5570 12344

PAYMENTS

PAYMENTS TO SUPPLIERS NIL NIL 11800 8600 10200 12800

2

gearing profit.

Help in environment scanning process: Marginal costing, standard costing and system

of management accounting useful in identifying effect of external as well as internal

department of production and distribution procedure .

Provide base for preparing budget: Planing tool of management accounting as well as

its system useful in given accurate information regarding formulating future as well as

current budget. This help manager to identifying future business opportunities.

Risk analysis: Management accounting useful in assessment of risk, by making budget,

organization able to identifying risk and on the basis of that they formulate future

policies to avoid theses risk.

QUESTION 1

Review on cash position of Woodrock Limited

Cash budget: This term refer as numerical statement which define cash inflow and outflow of

organization for particular period of time. Cash budget is useful in providing base for future

budget and able to formulate policies of controlling cash outflow. Manager only consider cash

and its relevant transaction which deal only in the form of cash (Li, and Gu, 2020). It

considered, expenses and revenue collected by business organization. Following are the cash

budget of Woodrock Limited

PARTICULARS

MONTH

1

MONTH

2

MONTH

3

MONTH

4

MONTH

5

MONTH

6

OPENING BALANCE NIL NIL NIL -31914 -24430 -23156

RECEIPTS

RECEIPTS FROM CLIENTS NIL NIL NIL 41000 30000 35500

TOTAL A 0 0 0 9086 5570 12344

PAYMENTS

PAYMENTS TO SUPPLIERS NIL NIL 11800 8600 10200 12800

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

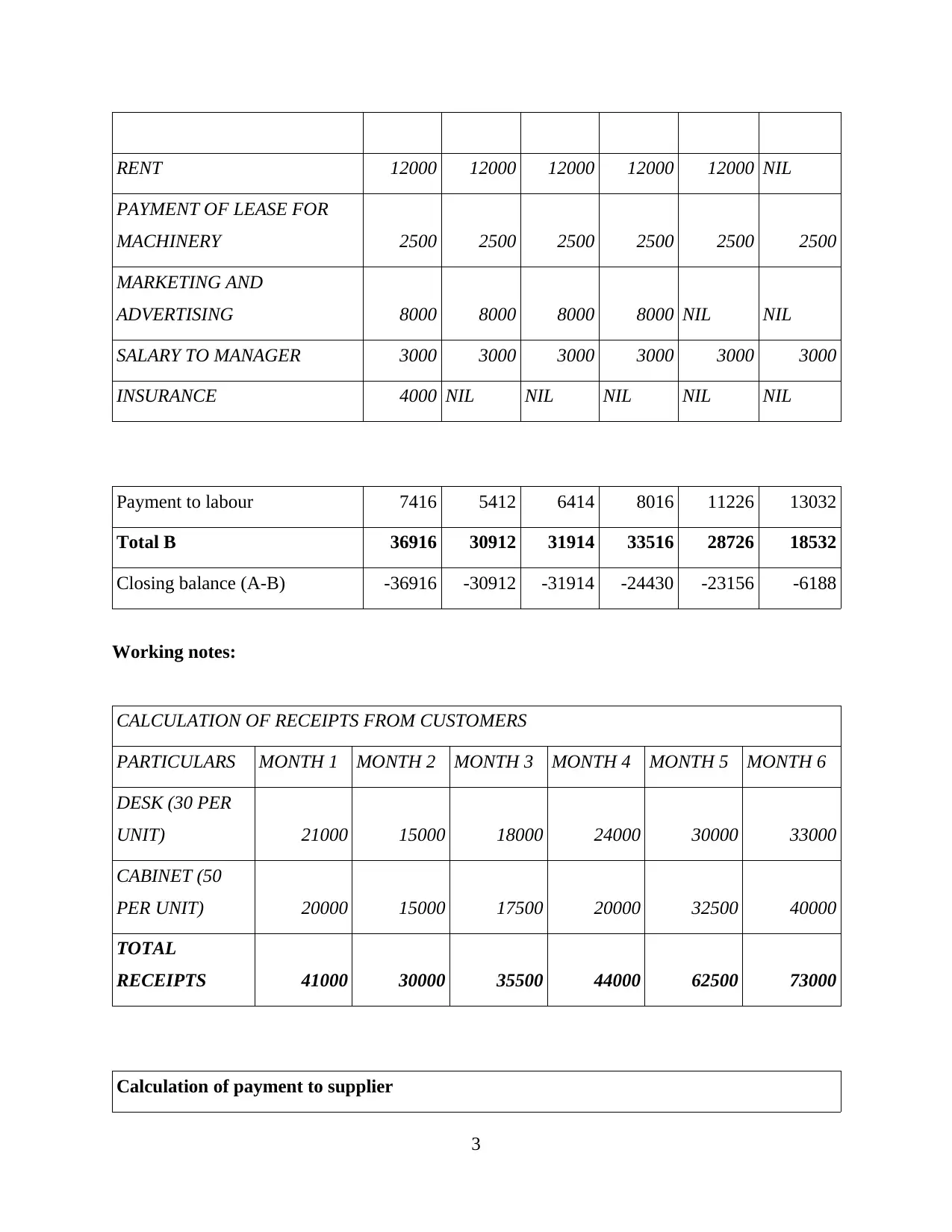

RENT 12000 12000 12000 12000 12000 NIL

PAYMENT OF LEASE FOR

MACHINERY 2500 2500 2500 2500 2500 2500

MARKETING AND

ADVERTISING 8000 8000 8000 8000 NIL NIL

SALARY TO MANAGER 3000 3000 3000 3000 3000 3000

INSURANCE 4000 NIL NIL NIL NIL NIL

Payment to labour 7416 5412 6414 8016 11226 13032

Total B 36916 30912 31914 33516 28726 18532

Closing balance (A-B) -36916 -30912 -31914 -24430 -23156 -6188

Working notes:

CALCULATION OF RECEIPTS FROM CUSTOMERS

PARTICULARS MONTH 1 MONTH 2 MONTH 3 MONTH 4 MONTH 5 MONTH 6

DESK (30 PER

UNIT) 21000 15000 18000 24000 30000 33000

CABINET (50

PER UNIT) 20000 15000 17500 20000 32500 40000

TOTAL

RECEIPTS 41000 30000 35500 44000 62500 73000

Calculation of payment to supplier

3

PAYMENT OF LEASE FOR

MACHINERY 2500 2500 2500 2500 2500 2500

MARKETING AND

ADVERTISING 8000 8000 8000 8000 NIL NIL

SALARY TO MANAGER 3000 3000 3000 3000 3000 3000

INSURANCE 4000 NIL NIL NIL NIL NIL

Payment to labour 7416 5412 6414 8016 11226 13032

Total B 36916 30912 31914 33516 28726 18532

Closing balance (A-B) -36916 -30912 -31914 -24430 -23156 -6188

Working notes:

CALCULATION OF RECEIPTS FROM CUSTOMERS

PARTICULARS MONTH 1 MONTH 2 MONTH 3 MONTH 4 MONTH 5 MONTH 6

DESK (30 PER

UNIT) 21000 15000 18000 24000 30000 33000

CABINET (50

PER UNIT) 20000 15000 17500 20000 32500 40000

TOTAL

RECEIPTS 41000 30000 35500 44000 62500 73000

Calculation of payment to supplier

3

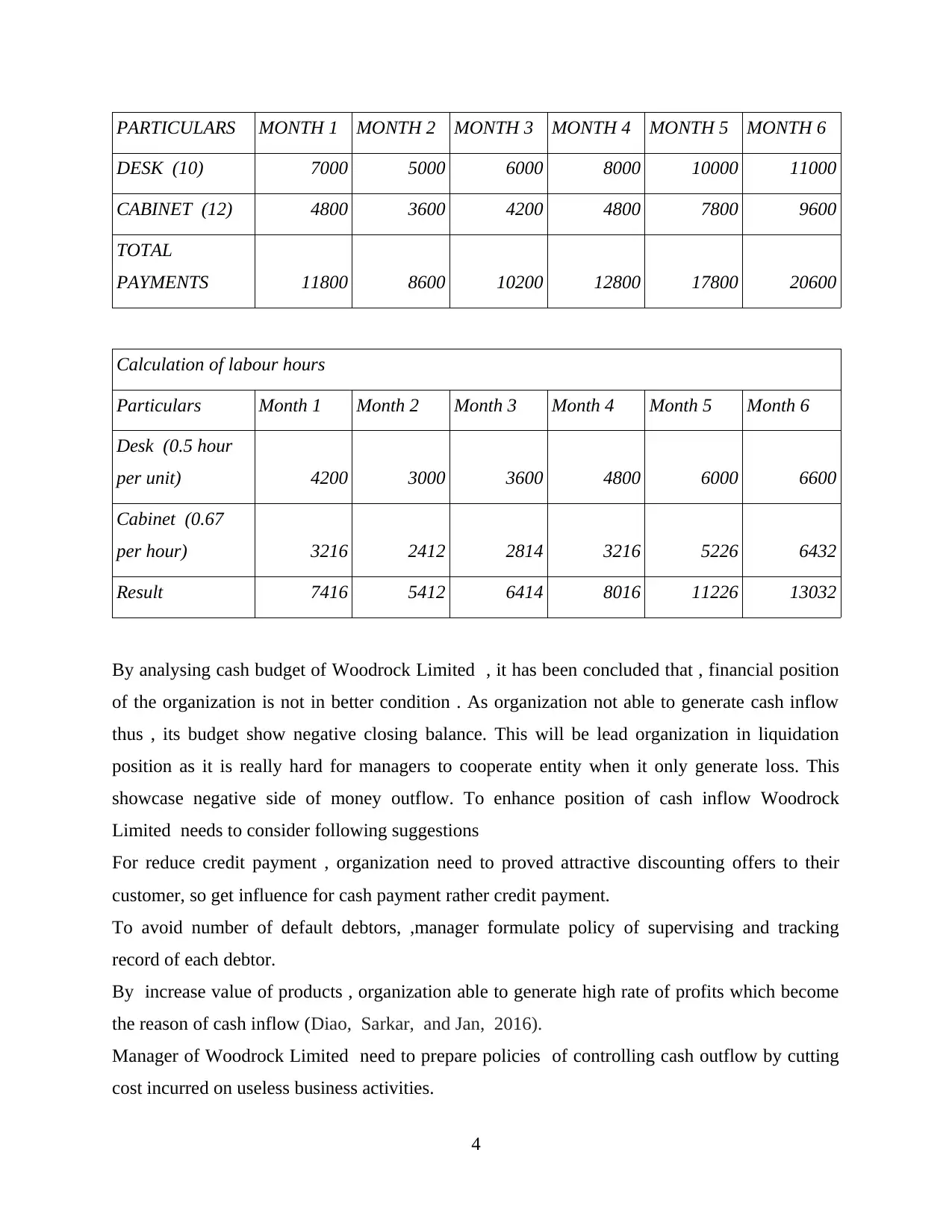

PARTICULARS MONTH 1 MONTH 2 MONTH 3 MONTH 4 MONTH 5 MONTH 6

DESK (10) 7000 5000 6000 8000 10000 11000

CABINET (12) 4800 3600 4200 4800 7800 9600

TOTAL

PAYMENTS 11800 8600 10200 12800 17800 20600

Calculation of labour hours

Particulars Month 1 Month 2 Month 3 Month 4 Month 5 Month 6

Desk (0.5 hour

per unit) 4200 3000 3600 4800 6000 6600

Cabinet (0.67

per hour) 3216 2412 2814 3216 5226 6432

Result 7416 5412 6414 8016 11226 13032

By analysing cash budget of Woodrock Limited , it has been concluded that , financial position

of the organization is not in better condition . As organization not able to generate cash inflow

thus , its budget show negative closing balance. This will be lead organization in liquidation

position as it is really hard for managers to cooperate entity when it only generate loss. This

showcase negative side of money outflow. To enhance position of cash inflow Woodrock

Limited needs to consider following suggestions

For reduce credit payment , organization need to proved attractive discounting offers to their

customer, so get influence for cash payment rather credit payment.

To avoid number of default debtors, ,manager formulate policy of supervising and tracking

record of each debtor.

By increase value of products , organization able to generate high rate of profits which become

the reason of cash inflow (Diao, Sarkar, and Jan, 2016).

Manager of Woodrock Limited need to prepare policies of controlling cash outflow by cutting

cost incurred on useless business activities.

4

DESK (10) 7000 5000 6000 8000 10000 11000

CABINET (12) 4800 3600 4200 4800 7800 9600

TOTAL

PAYMENTS 11800 8600 10200 12800 17800 20600

Calculation of labour hours

Particulars Month 1 Month 2 Month 3 Month 4 Month 5 Month 6

Desk (0.5 hour

per unit) 4200 3000 3600 4800 6000 6600

Cabinet (0.67

per hour) 3216 2412 2814 3216 5226 6432

Result 7416 5412 6414 8016 11226 13032

By analysing cash budget of Woodrock Limited , it has been concluded that , financial position

of the organization is not in better condition . As organization not able to generate cash inflow

thus , its budget show negative closing balance. This will be lead organization in liquidation

position as it is really hard for managers to cooperate entity when it only generate loss. This

showcase negative side of money outflow. To enhance position of cash inflow Woodrock

Limited needs to consider following suggestions

For reduce credit payment , organization need to proved attractive discounting offers to their

customer, so get influence for cash payment rather credit payment.

To avoid number of default debtors, ,manager formulate policy of supervising and tracking

record of each debtor.

By increase value of products , organization able to generate high rate of profits which become

the reason of cash inflow (Diao, Sarkar, and Jan, 2016).

Manager of Woodrock Limited need to prepare policies of controlling cash outflow by cutting

cost incurred on useless business activities.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Optimum lionization of inventory, help in reducing maintenance cost on storing inventory.

By spreading target market Woodrock Limited able to covert their adverse cash closing balance

into favourable balance.

Issue related with behavioural aspect which may causes of arsing problem within business

organization

Success of budget depend on qualities and expertise skills of manager , thus it is not necessary

formation of cash budget help in providing accurate and reliable future business information.

Budgeting is time consuming procedure as collection of record, analysing and researching

books , past records and on the basis of that preparing budget. All these steps require huge time.

It is not essential that particular budget technique useful in applying all the aspect of business

department.

QUESTION 2

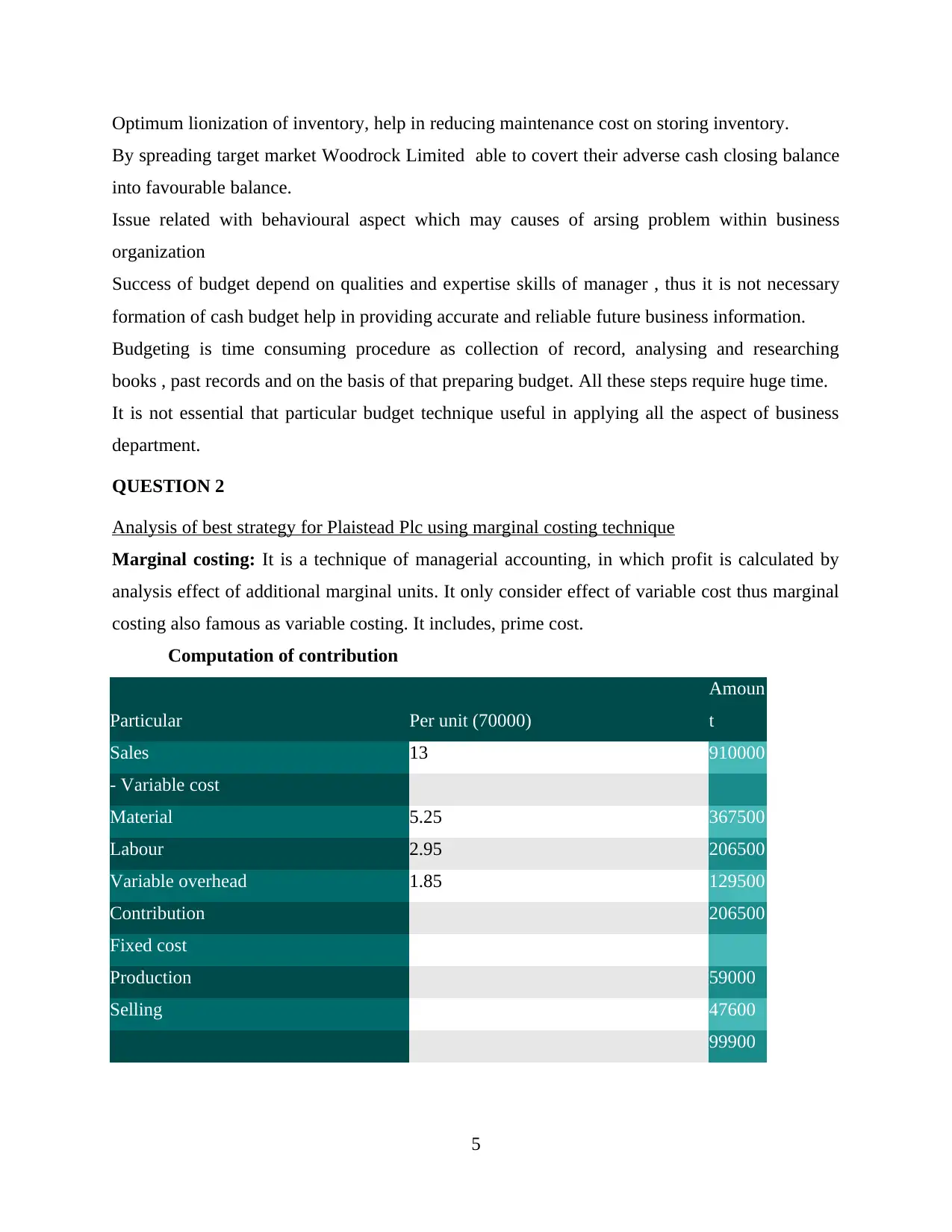

Analysis of best strategy for Plaistead Plc using marginal costing technique

Marginal costing: It is a technique of managerial accounting, in which profit is calculated by

analysis effect of additional marginal units. It only consider effect of variable cost thus marginal

costing also famous as variable costing. It includes, prime cost.

Computation of contribution

Particular Per unit (70000)

Amoun

t

Sales 13 910000

- Variable cost

Material 5.25 367500

Labour 2.95 206500

Variable overhead 1.85 129500

Contribution 206500

Fixed cost

Production 59000

Selling 47600

99900

5

By spreading target market Woodrock Limited able to covert their adverse cash closing balance

into favourable balance.

Issue related with behavioural aspect which may causes of arsing problem within business

organization

Success of budget depend on qualities and expertise skills of manager , thus it is not necessary

formation of cash budget help in providing accurate and reliable future business information.

Budgeting is time consuming procedure as collection of record, analysing and researching

books , past records and on the basis of that preparing budget. All these steps require huge time.

It is not essential that particular budget technique useful in applying all the aspect of business

department.

QUESTION 2

Analysis of best strategy for Plaistead Plc using marginal costing technique

Marginal costing: It is a technique of managerial accounting, in which profit is calculated by

analysis effect of additional marginal units. It only consider effect of variable cost thus marginal

costing also famous as variable costing. It includes, prime cost.

Computation of contribution

Particular Per unit (70000)

Amoun

t

Sales 13 910000

- Variable cost

Material 5.25 367500

Labour 2.95 206500

Variable overhead 1.85 129500

Contribution 206500

Fixed cost

Production 59000

Selling 47600

99900

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

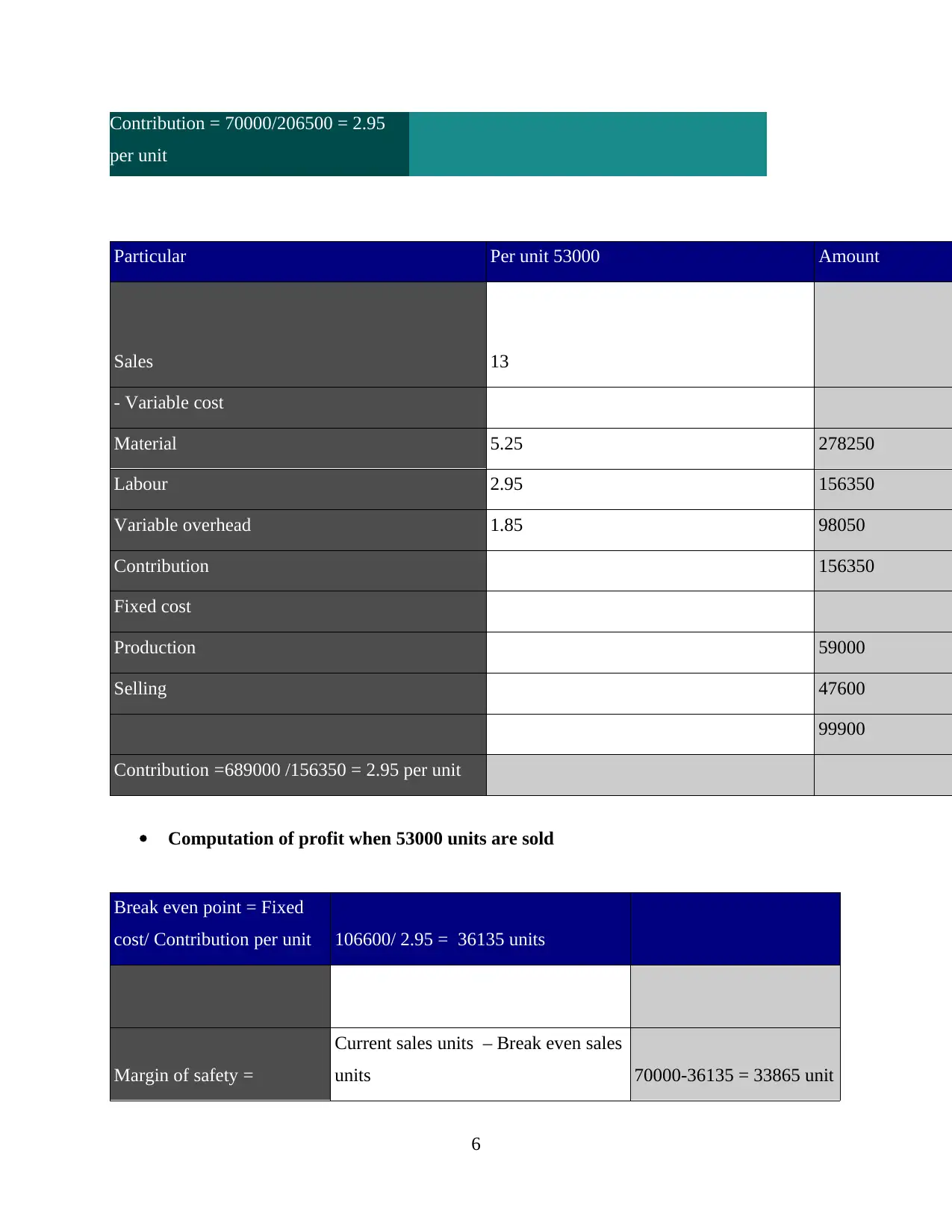

Contribution = 70000/206500 = 2.95

per unit

Particular Per unit 53000 Amount

Sales 13

- Variable cost

Material 5.25 278250

Labour 2.95 156350

Variable overhead 1.85 98050

Contribution 156350

Fixed cost

Production 59000

Selling 47600

99900

Contribution =689000 /156350 = 2.95 per unit

Computation of profit when 53000 units are sold

Break even point = Fixed

cost/ Contribution per unit 106600/ 2.95 = 36135 units

Margin of safety =

Current sales units – Break even sales

units 70000-36135 = 33865 unit

6

per unit

Particular Per unit 53000 Amount

Sales 13

- Variable cost

Material 5.25 278250

Labour 2.95 156350

Variable overhead 1.85 98050

Contribution 156350

Fixed cost

Production 59000

Selling 47600

99900

Contribution =689000 /156350 = 2.95 per unit

Computation of profit when 53000 units are sold

Break even point = Fixed

cost/ Contribution per unit 106600/ 2.95 = 36135 units

Margin of safety =

Current sales units – Break even sales

units 70000-36135 = 33865 unit

6

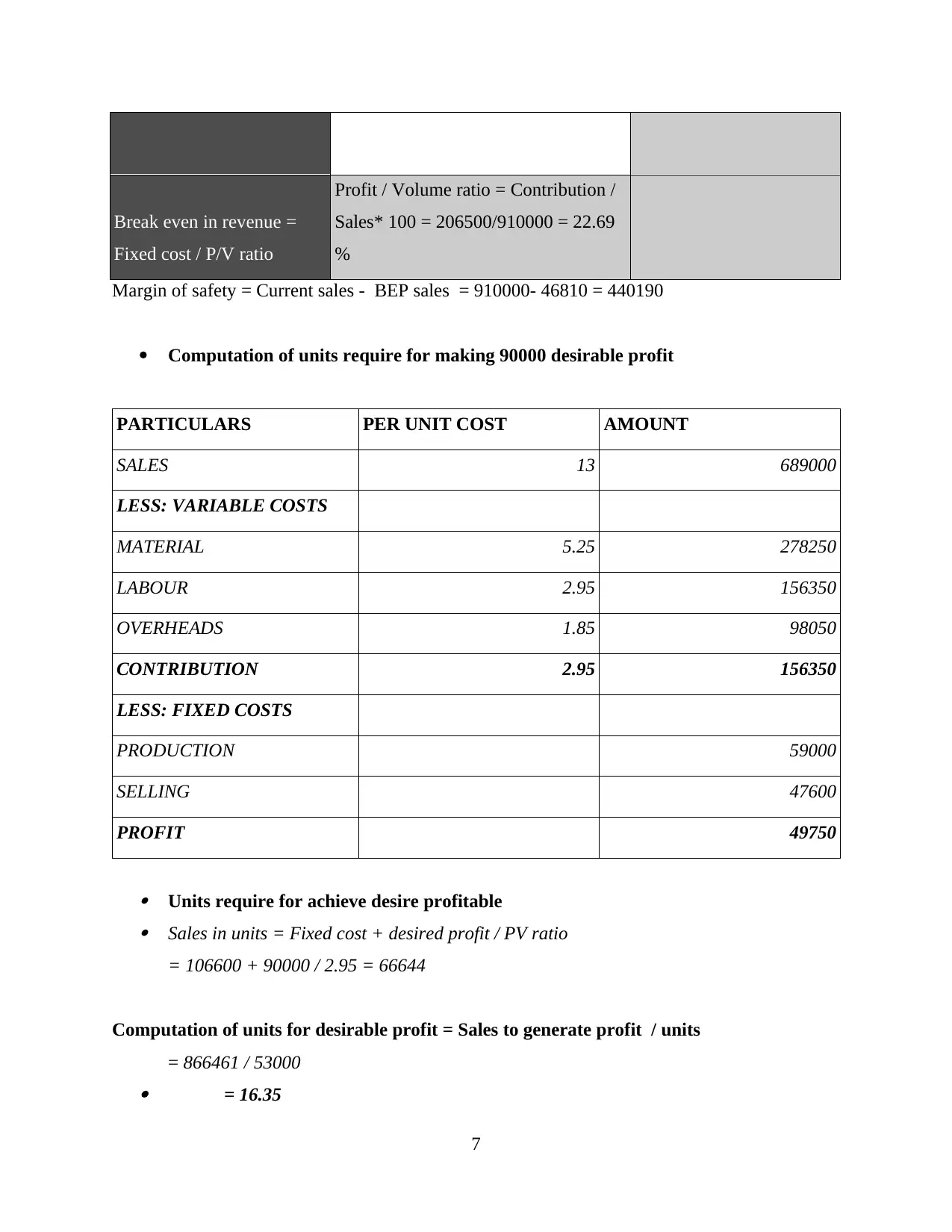

Break even in revenue =

Fixed cost / P/V ratio

Profit / Volume ratio = Contribution /

Sales* 100 = 206500/910000 = 22.69

%

Margin of safety = Current sales - BEP sales = 910000- 46810 = 440190

Computation of units require for making 90000 desirable profit

PARTICULARS PER UNIT COST AMOUNT

SALES 13 689000

LESS: VARIABLE COSTS

MATERIAL 5.25 278250

LABOUR 2.95 156350

OVERHEADS 1.85 98050

CONTRIBUTION 2.95 156350

LESS: FIXED COSTS

PRODUCTION 59000

SELLING 47600

PROFIT 49750

Units require for achieve desire profitable Sales in units = Fixed cost + desired profit / PV ratio

= 106600 + 90000 / 2.95 = 66644

Computation of units for desirable profit = Sales to generate profit / units

= 866461 / 53000 = 16.35

7

Fixed cost / P/V ratio

Profit / Volume ratio = Contribution /

Sales* 100 = 206500/910000 = 22.69

%

Margin of safety = Current sales - BEP sales = 910000- 46810 = 440190

Computation of units require for making 90000 desirable profit

PARTICULARS PER UNIT COST AMOUNT

SALES 13 689000

LESS: VARIABLE COSTS

MATERIAL 5.25 278250

LABOUR 2.95 156350

OVERHEADS 1.85 98050

CONTRIBUTION 2.95 156350

LESS: FIXED COSTS

PRODUCTION 59000

SELLING 47600

PROFIT 49750

Units require for achieve desire profitable Sales in units = Fixed cost + desired profit / PV ratio

= 106600 + 90000 / 2.95 = 66644

Computation of units for desirable profit = Sales to generate profit / units

= 866461 / 53000 = 16.35

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

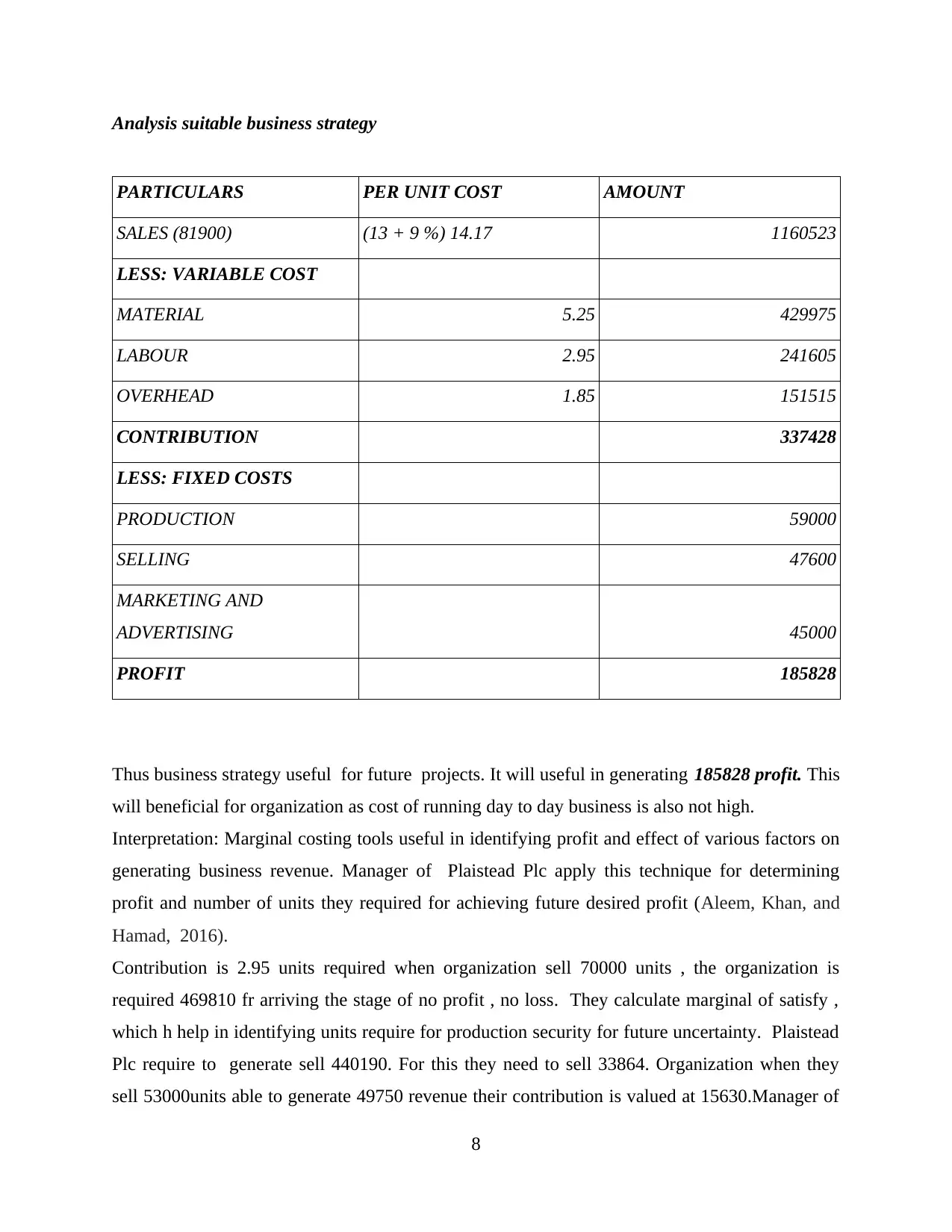

Analysis suitable business strategy

PARTICULARS PER UNIT COST AMOUNT

SALES (81900) (13 + 9 %) 14.17 1160523

LESS: VARIABLE COST

MATERIAL 5.25 429975

LABOUR 2.95 241605

OVERHEAD 1.85 151515

CONTRIBUTION 337428

LESS: FIXED COSTS

PRODUCTION 59000

SELLING 47600

MARKETING AND

ADVERTISING 45000

PROFIT 185828

Thus business strategy useful for future projects. It will useful in generating 185828 profit. This

will beneficial for organization as cost of running day to day business is also not high.

Interpretation: Marginal costing tools useful in identifying profit and effect of various factors on

generating business revenue. Manager of Plaistead Plc apply this technique for determining

profit and number of units they required for achieving future desired profit (Aleem, Khan, and

Hamad, 2016).

Contribution is 2.95 units required when organization sell 70000 units , the organization is

required 469810 fr arriving the stage of no profit , no loss. They calculate marginal of satisfy ,

which h help in identifying units require for production security for future uncertainty. Plaistead

Plc require to generate sell 440190. For this they need to sell 33864. Organization when they

sell 53000units able to generate 49750 revenue their contribution is valued at 15630.Manager of

8

PARTICULARS PER UNIT COST AMOUNT

SALES (81900) (13 + 9 %) 14.17 1160523

LESS: VARIABLE COST

MATERIAL 5.25 429975

LABOUR 2.95 241605

OVERHEAD 1.85 151515

CONTRIBUTION 337428

LESS: FIXED COSTS

PRODUCTION 59000

SELLING 47600

MARKETING AND

ADVERTISING 45000

PROFIT 185828

Thus business strategy useful for future projects. It will useful in generating 185828 profit. This

will beneficial for organization as cost of running day to day business is also not high.

Interpretation: Marginal costing tools useful in identifying profit and effect of various factors on

generating business revenue. Manager of Plaistead Plc apply this technique for determining

profit and number of units they required for achieving future desired profit (Aleem, Khan, and

Hamad, 2016).

Contribution is 2.95 units required when organization sell 70000 units , the organization is

required 469810 fr arriving the stage of no profit , no loss. They calculate marginal of satisfy ,

which h help in identifying units require for production security for future uncertainty. Plaistead

Plc require to generate sell 440190. For this they need to sell 33864. Organization when they

sell 53000units able to generate 49750 revenue their contribution is valued at 15630.Manager of

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

33864 require to attain their future profit target, 66644 units must be sale, only then they can

achieve their target.

Break even concept of marginal accounting is useful in determining the point where profit as

well as loss of the organization is equal. With the use of Break Even point, organization will be

able to recognize impact of launching new product. Manager can understand impact of additional

investment in organization. Main purpose of using this technique is to recognize best decision

which hep in gaining competitive business advantage. Effect of changing price on profit and

reducing or addition of new units. For calculating of Break even points manager require to work

according to following assumption

While calculating of BEP it is essential to focus or consider only fixed , and variable cost.

This concept is basically not consider fluctuation in files, thus price is treat as constant factor

while calculating BEP.

Volume of sales and level of product units also consider as equal level.

Manager consider, fixed price while calculating BEP it will useful in considering best alternative

Manager of business organization focus on generating profit. For Plaistead Plc it is essential to

determine theses effective break even point (Friedl, Küpper, and Pedell, 2005).

QUESTION 4

Calculation of standard costing variance

Budget: Numerical statement, through which manager can identify future position of

organization by understanding profit , loss and forecast expenses incurred in future period of

time. Preparing budget is really essential for organization wherever it was small, large or

medium size , every or4ganization need to formulate it . Thus will help in providing guideline

and future path. Procedure of preparing budget is define as budgeting their are various types of

budget is formulate and manager have option to apply different strategy through which they can

prepare budget. Following are the budget prepare by Jayrod Plc

Original budget: This is define as statement which show profit, loss, cash inflow and activities

through which organization can formulate their future business policies. It is considers as detail

budget, . They also showcase, debt and assets value of particular business organization. Original

budget is made for particular 2 years.

9

achieve their target.

Break even concept of marginal accounting is useful in determining the point where profit as

well as loss of the organization is equal. With the use of Break Even point, organization will be

able to recognize impact of launching new product. Manager can understand impact of additional

investment in organization. Main purpose of using this technique is to recognize best decision

which hep in gaining competitive business advantage. Effect of changing price on profit and

reducing or addition of new units. For calculating of Break even points manager require to work

according to following assumption

While calculating of BEP it is essential to focus or consider only fixed , and variable cost.

This concept is basically not consider fluctuation in files, thus price is treat as constant factor

while calculating BEP.

Volume of sales and level of product units also consider as equal level.

Manager consider, fixed price while calculating BEP it will useful in considering best alternative

Manager of business organization focus on generating profit. For Plaistead Plc it is essential to

determine theses effective break even point (Friedl, Küpper, and Pedell, 2005).

QUESTION 4

Calculation of standard costing variance

Budget: Numerical statement, through which manager can identify future position of

organization by understanding profit , loss and forecast expenses incurred in future period of

time. Preparing budget is really essential for organization wherever it was small, large or

medium size , every or4ganization need to formulate it . Thus will help in providing guideline

and future path. Procedure of preparing budget is define as budgeting their are various types of

budget is formulate and manager have option to apply different strategy through which they can

prepare budget. Following are the budget prepare by Jayrod Plc

Original budget: This is define as statement which show profit, loss, cash inflow and activities

through which organization can formulate their future business policies. It is considers as detail

budget, . They also showcase, debt and assets value of particular business organization. Original

budget is made for particular 2 years.

9

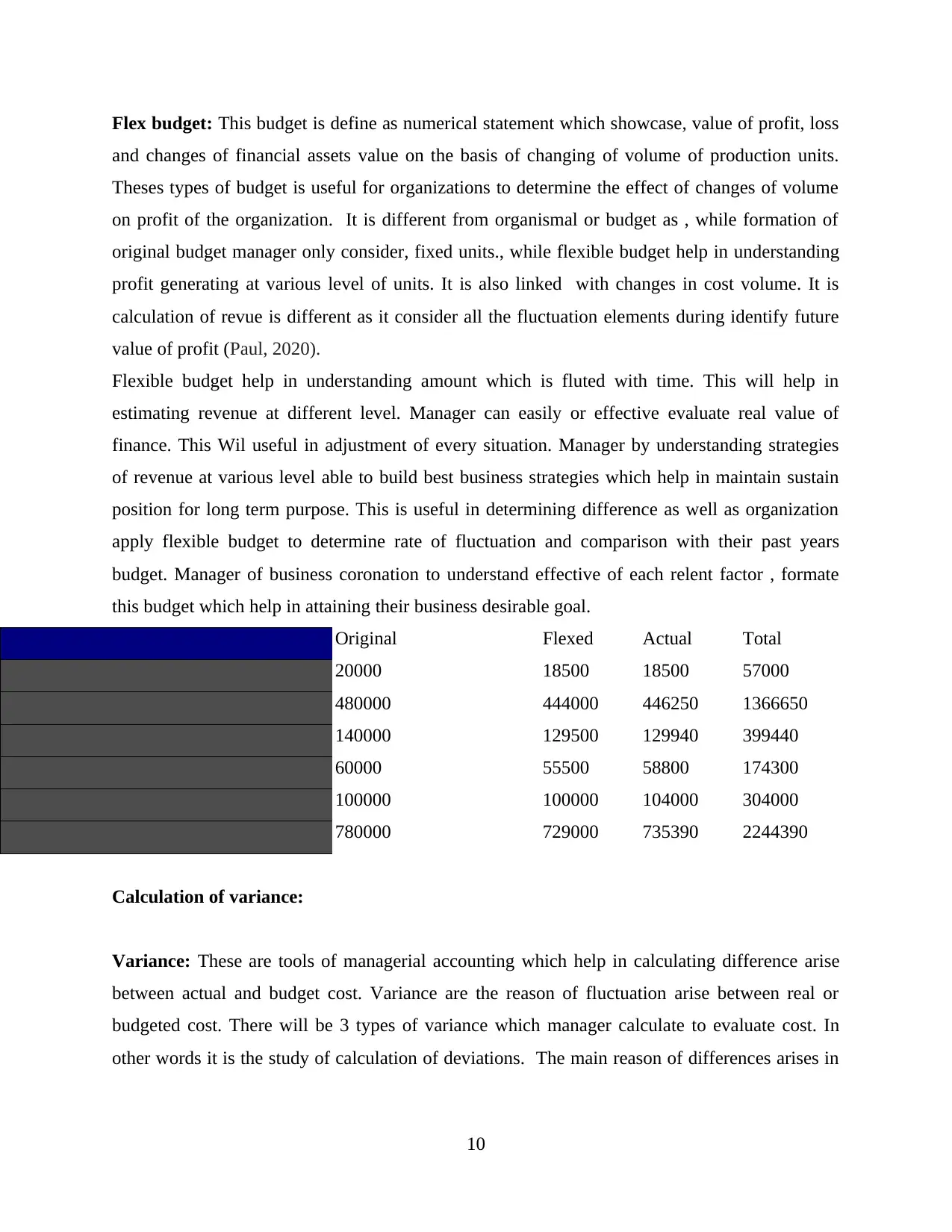

Flex budget: This budget is define as numerical statement which showcase, value of profit, loss

and changes of financial assets value on the basis of changing of volume of production units.

Theses types of budget is useful for organizations to determine the effect of changes of volume

on profit of the organization. It is different from organismal or budget as , while formation of

original budget manager only consider, fixed units., while flexible budget help in understanding

profit generating at various level of units. It is also linked with changes in cost volume. It is

calculation of revue is different as it consider all the fluctuation elements during identify future

value of profit (Paul, 2020).

Flexible budget help in understanding amount which is fluted with time. This will help in

estimating revenue at different level. Manager can easily or effective evaluate real value of

finance. This Wil useful in adjustment of every situation. Manager by understanding strategies

of revenue at various level able to build best business strategies which help in maintain sustain

position for long term purpose. This is useful in determining difference as well as organization

apply flexible budget to determine rate of fluctuation and comparison with their past years

budget. Manager of business coronation to understand effective of each relent factor , formate

this budget which help in attaining their business desirable goal.

Original Flexed Actual Total

20000 18500 18500 57000

480000 444000 446250 1366650

140000 129500 129940 399440

60000 55500 58800 174300

100000 100000 104000 304000

780000 729000 735390 2244390

Calculation of variance:

Variance: These are tools of managerial accounting which help in calculating difference arise

between actual and budget cost. Variance are the reason of fluctuation arise between real or

budgeted cost. There will be 3 types of variance which manager calculate to evaluate cost. In

other words it is the study of calculation of deviations. The main reason of differences arises in

10

and changes of financial assets value on the basis of changing of volume of production units.

Theses types of budget is useful for organizations to determine the effect of changes of volume

on profit of the organization. It is different from organismal or budget as , while formation of

original budget manager only consider, fixed units., while flexible budget help in understanding

profit generating at various level of units. It is also linked with changes in cost volume. It is

calculation of revue is different as it consider all the fluctuation elements during identify future

value of profit (Paul, 2020).

Flexible budget help in understanding amount which is fluted with time. This will help in

estimating revenue at different level. Manager can easily or effective evaluate real value of

finance. This Wil useful in adjustment of every situation. Manager by understanding strategies

of revenue at various level able to build best business strategies which help in maintain sustain

position for long term purpose. This is useful in determining difference as well as organization

apply flexible budget to determine rate of fluctuation and comparison with their past years

budget. Manager of business coronation to understand effective of each relent factor , formate

this budget which help in attaining their business desirable goal.

Original Flexed Actual Total

20000 18500 18500 57000

480000 444000 446250 1366650

140000 129500 129940 399440

60000 55500 58800 174300

100000 100000 104000 304000

780000 729000 735390 2244390

Calculation of variance:

Variance: These are tools of managerial accounting which help in calculating difference arise

between actual and budget cost. Variance are the reason of fluctuation arise between real or

budgeted cost. There will be 3 types of variance which manager calculate to evaluate cost. In

other words it is the study of calculation of deviations. The main reason of differences arises in

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.