Business Accounting Report on Trial Balance, Adjustments, and Closing

VerifiedAdded on 2023/06/04

|13

|1830

|405

Report

AI Summary

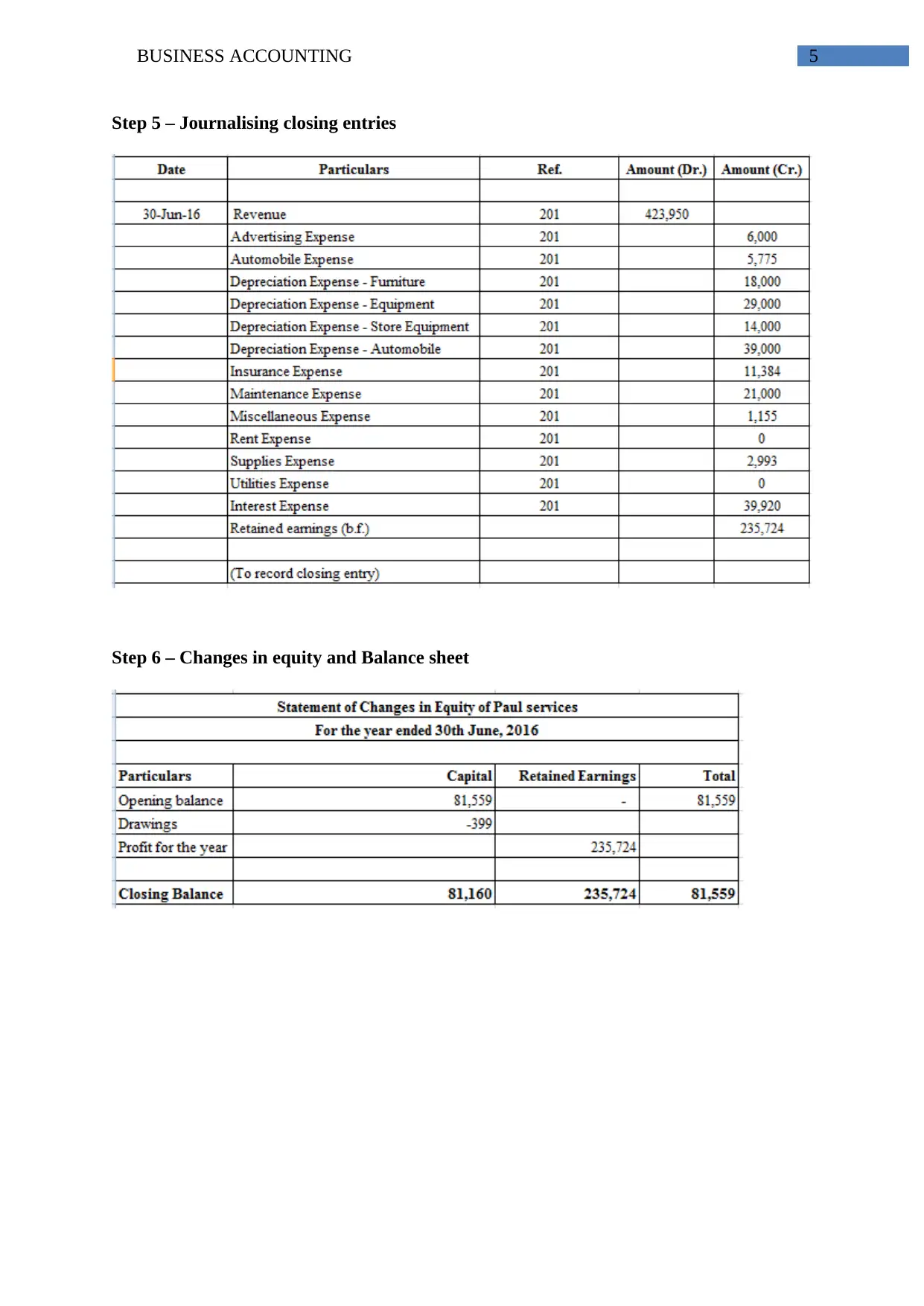

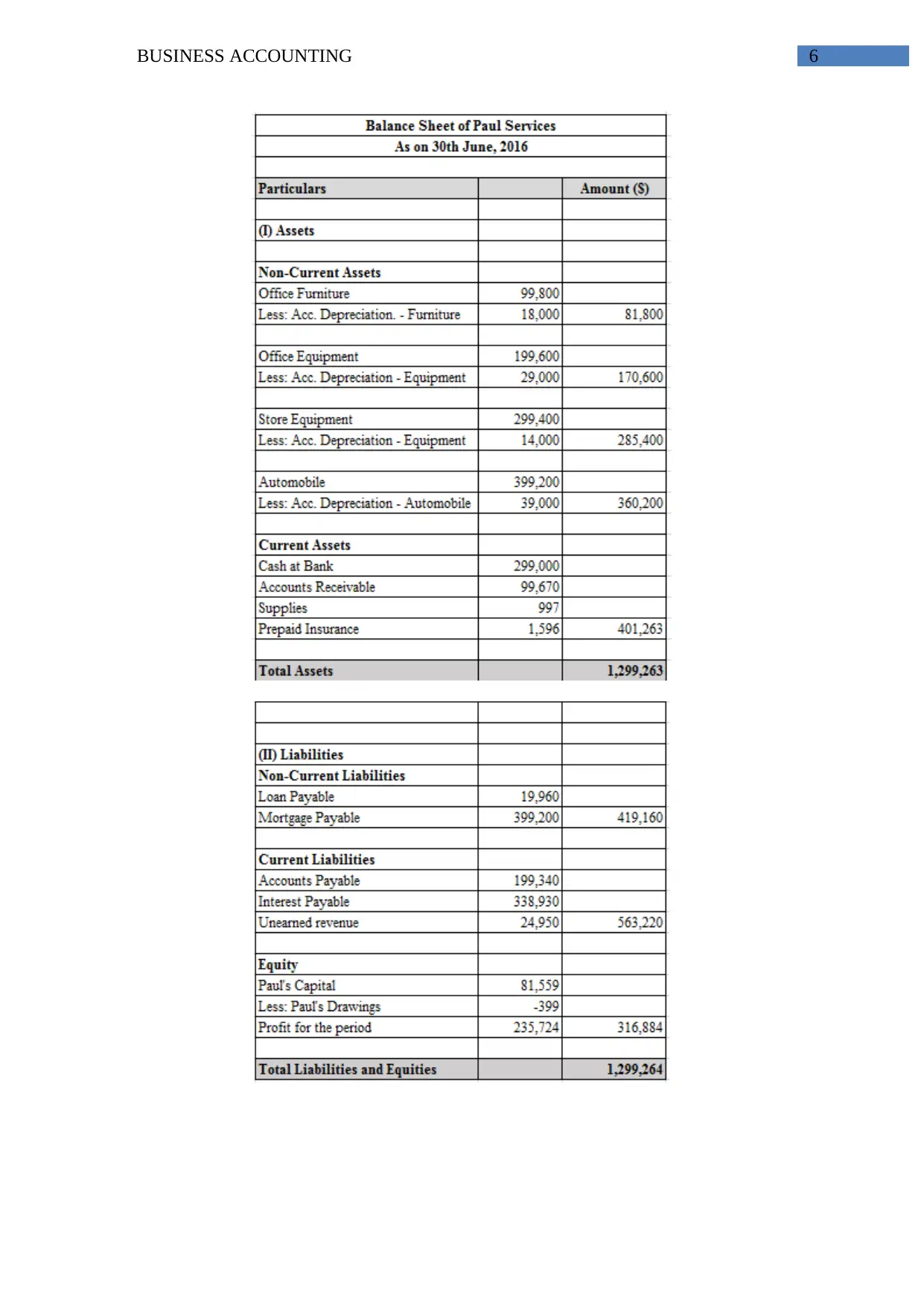

This business accounting report provides a comprehensive overview of key accounting concepts and procedures. It begins by defining the trial balance, explaining its purpose in ensuring the accuracy of general ledger entries, and highlighting its importance, particularly in manual accounting systems. The report then delves into adjustment journal entries, emphasizing their role in adhering to the accrual concept and matching principle, as well as correcting accounting errors. It discusses the different types of adjusting entries and their significance in updating accounts for accurate financial reporting. The report further examines the adjusted trial balance, outlining its function in verifying the accuracy of ledger entries after adjustments and its use in preparing financial statements. Finally, it contrasts adjusting and closing journal entries, detailing their distinct purposes and timing within the accounting cycle. The report concludes with a reference list of sources.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.