Business Accounting Assignment: Detailed Solutions for Questions 1-10

VerifiedAdded on 2022/11/25

|14

|3109

|231

Homework Assignment

AI Summary

This document presents a comprehensive solution to a business accounting assignment, addressing ten key questions. The solution includes calculations and explanations for fundamental accounting concepts. It starts with basic accounting equations, followed by the preparation of T-accounts, and the creation of a trial balance. It also includes the preparation of profit and loss statements and balance sheets, capital and revenue expenditure identification, and the use of sales and purchase ledger control accounts. The assignment further covers ratio analysis, including gross profit percentage, net profit percentage, current ratio, and inventory turnover, as well as the calculation of payback periods and net present value. Finally, the document addresses the role of accountants, external auditors, and non-accountants in business decision-making, and the statutory obligations of management accountants. It also discusses the nature of accounting.

BUSINESS ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question: 1.......................................................................................................................................3

Question: 2.......................................................................................................................................4

Preparation of T-accounts............................................................................................................4

Question: 3.......................................................................................................................................6

Question: 4.......................................................................................................................................6

Question: 5.......................................................................................................................................7

Question: 6.......................................................................................................................................8

Question: 7.......................................................................................................................................8

Question: 8.....................................................................................................................................10

Question: 9.....................................................................................................................................10

Question: 10...................................................................................................................................11

REFERENCES..............................................................................................................................13

Question: 1.......................................................................................................................................3

Question: 2.......................................................................................................................................4

Preparation of T-accounts............................................................................................................4

Question: 3.......................................................................................................................................6

Question: 4.......................................................................................................................................6

Question: 5.......................................................................................................................................7

Question: 6.......................................................................................................................................8

Question: 7.......................................................................................................................................8

Question: 8.....................................................................................................................................10

Question: 9.....................................................................................................................................10

Question: 10...................................................................................................................................11

REFERENCES..............................................................................................................................13

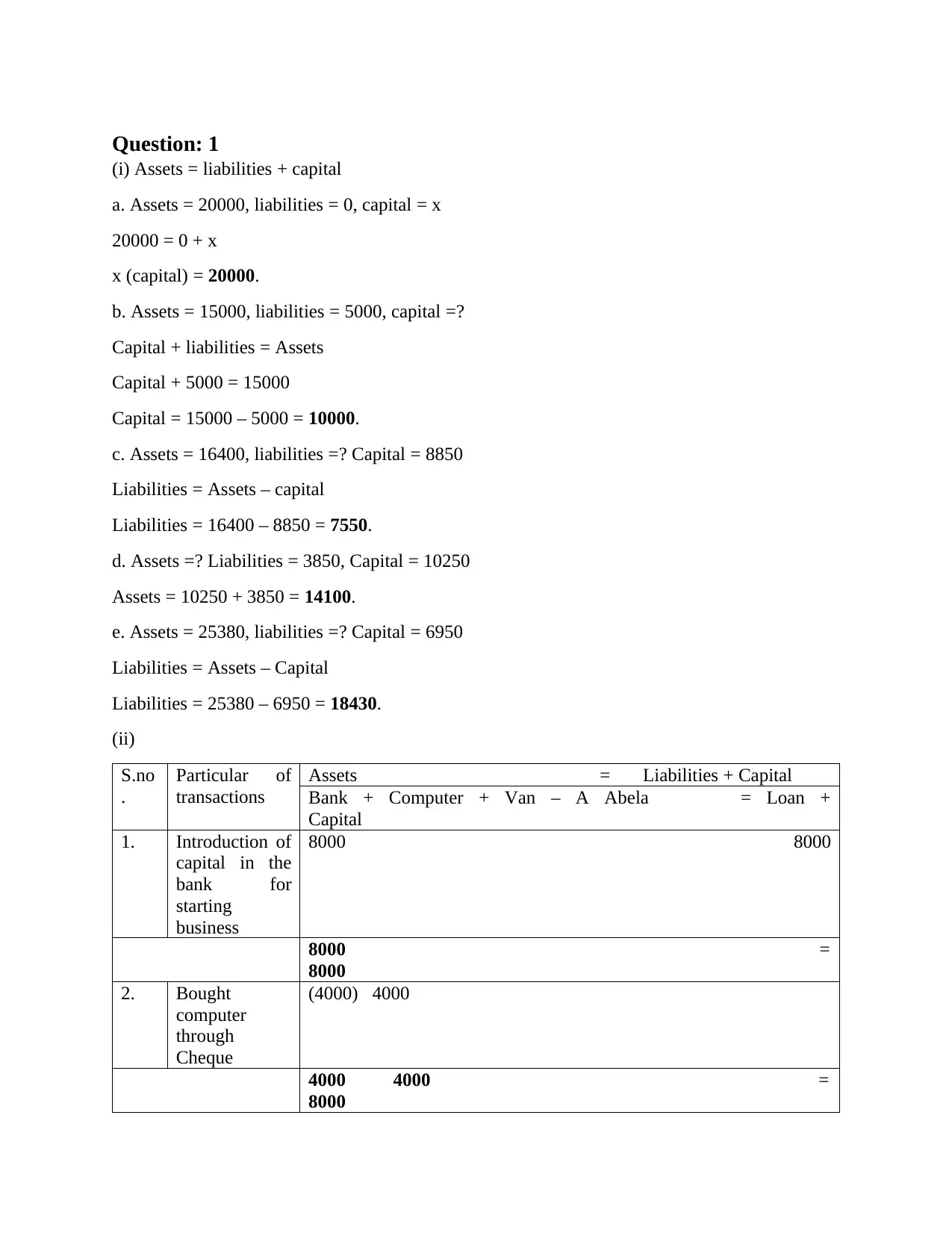

Question: 1

(i) Assets = liabilities + capital

a. Assets = 20000, liabilities = 0, capital = x

20000 = 0 + x

x (capital) = 20000.

b. Assets = 15000, liabilities = 5000, capital =?

Capital + liabilities = Assets

Capital + 5000 = 15000

Capital = 15000 – 5000 = 10000.

c. Assets = 16400, liabilities =? Capital = 8850

Liabilities = Assets – capital

Liabilities = 16400 – 8850 = 7550.

d. Assets =? Liabilities = 3850, Capital = 10250

Assets = 10250 + 3850 = 14100.

e. Assets = 25380, liabilities =? Capital = 6950

Liabilities = Assets – Capital

Liabilities = 25380 – 6950 = 18430.

(ii)

S.no

.

Particular of

transactions

Assets = Liabilities + Capital

Bank + Computer + Van – A Abela = Loan +

Capital

1. Introduction of

capital in the

bank for

starting

business

8000 8000

8000 =

8000

2. Bought

computer

through

Cheque

(4000) 4000

4000 4000 =

8000

(i) Assets = liabilities + capital

a. Assets = 20000, liabilities = 0, capital = x

20000 = 0 + x

x (capital) = 20000.

b. Assets = 15000, liabilities = 5000, capital =?

Capital + liabilities = Assets

Capital + 5000 = 15000

Capital = 15000 – 5000 = 10000.

c. Assets = 16400, liabilities =? Capital = 8850

Liabilities = Assets – capital

Liabilities = 16400 – 8850 = 7550.

d. Assets =? Liabilities = 3850, Capital = 10250

Assets = 10250 + 3850 = 14100.

e. Assets = 25380, liabilities =? Capital = 6950

Liabilities = Assets – Capital

Liabilities = 25380 – 6950 = 18430.

(ii)

S.no

.

Particular of

transactions

Assets = Liabilities + Capital

Bank + Computer + Van – A Abela = Loan +

Capital

1. Introduction of

capital in the

bank for

starting

business

8000 8000

8000 =

8000

2. Bought

computer

through

Cheque

(4000) 4000

4000 4000 =

8000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

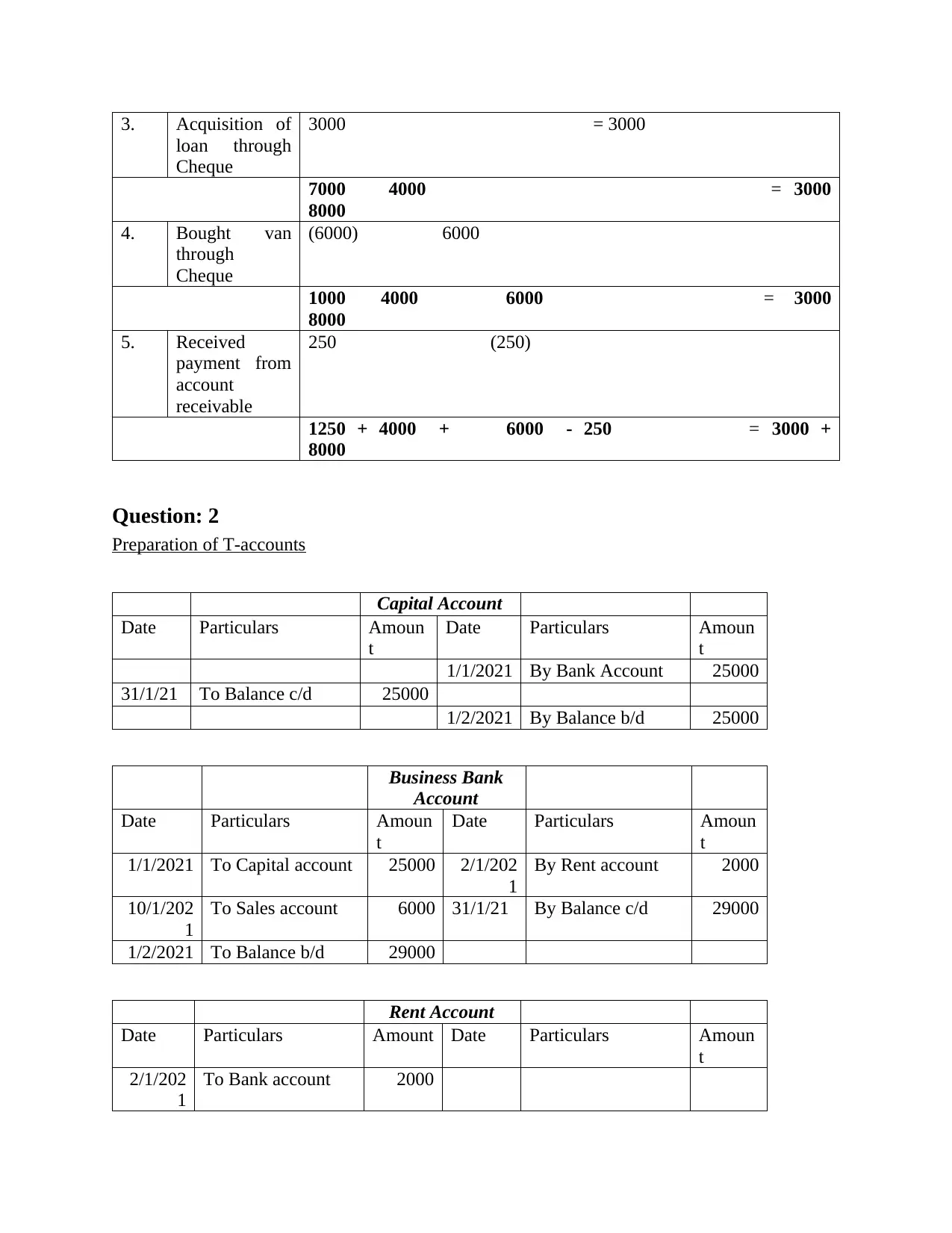

3. Acquisition of

loan through

Cheque

3000 = 3000

7000 4000 = 3000

8000

4. Bought van

through

Cheque

(6000) 6000

1000 4000 6000 = 3000

8000

5. Received

payment from

account

receivable

250 (250)

1250 + 4000 + 6000 - 250 = 3000 +

8000

Question: 2

Preparation of T-accounts

Capital Account

Date Particulars Amoun

t

Date Particulars Amoun

t

1/1/2021 By Bank Account 25000

31/1/21 To Balance c/d 25000

1/2/2021 By Balance b/d 25000

Business Bank

Account

Date Particulars Amoun

t

Date Particulars Amoun

t

1/1/2021 To Capital account 25000 2/1/202

1

By Rent account 2000

10/1/202

1

To Sales account 6000 31/1/21 By Balance c/d 29000

1/2/2021 To Balance b/d 29000

Rent Account

Date Particulars Amount Date Particulars Amoun

t

2/1/202

1

To Bank account 2000

loan through

Cheque

3000 = 3000

7000 4000 = 3000

8000

4. Bought van

through

Cheque

(6000) 6000

1000 4000 6000 = 3000

8000

5. Received

payment from

account

receivable

250 (250)

1250 + 4000 + 6000 - 250 = 3000 +

8000

Question: 2

Preparation of T-accounts

Capital Account

Date Particulars Amoun

t

Date Particulars Amoun

t

1/1/2021 By Bank Account 25000

31/1/21 To Balance c/d 25000

1/2/2021 By Balance b/d 25000

Business Bank

Account

Date Particulars Amoun

t

Date Particulars Amoun

t

1/1/2021 To Capital account 25000 2/1/202

1

By Rent account 2000

10/1/202

1

To Sales account 6000 31/1/21 By Balance c/d 29000

1/2/2021 To Balance b/d 29000

Rent Account

Date Particulars Amount Date Particulars Amoun

t

2/1/202

1

To Bank account 2000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

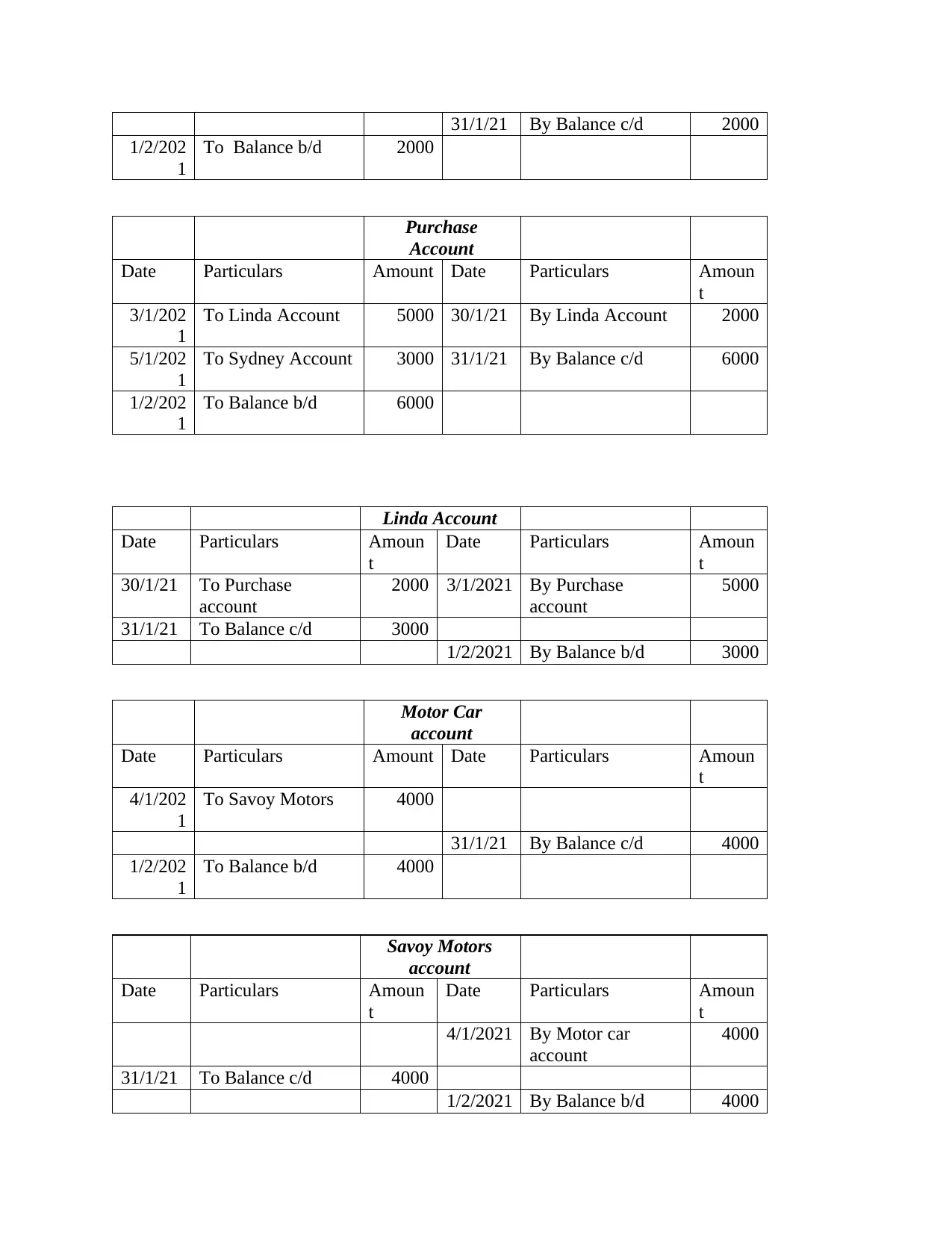

31/1/21 By Balance c/d 2000

1/2/202

1

To Balance b/d 2000

Purchase

Account

Date Particulars Amount Date Particulars Amoun

t

3/1/202

1

To Linda Account 5000 30/1/21 By Linda Account 2000

5/1/202

1

To Sydney Account 3000 31/1/21 By Balance c/d 6000

1/2/202

1

To Balance b/d 6000

Linda Account

Date Particulars Amoun

t

Date Particulars Amoun

t

30/1/21 To Purchase

account

2000 3/1/2021 By Purchase

account

5000

31/1/21 To Balance c/d 3000

1/2/2021 By Balance b/d 3000

Motor Car

account

Date Particulars Amount Date Particulars Amoun

t

4/1/202

1

To Savoy Motors 4000

31/1/21 By Balance c/d 4000

1/2/202

1

To Balance b/d 4000

Savoy Motors

account

Date Particulars Amoun

t

Date Particulars Amoun

t

4/1/2021 By Motor car

account

4000

31/1/21 To Balance c/d 4000

1/2/2021 By Balance b/d 4000

1/2/202

1

To Balance b/d 2000

Purchase

Account

Date Particulars Amount Date Particulars Amoun

t

3/1/202

1

To Linda Account 5000 30/1/21 By Linda Account 2000

5/1/202

1

To Sydney Account 3000 31/1/21 By Balance c/d 6000

1/2/202

1

To Balance b/d 6000

Linda Account

Date Particulars Amoun

t

Date Particulars Amoun

t

30/1/21 To Purchase

account

2000 3/1/2021 By Purchase

account

5000

31/1/21 To Balance c/d 3000

1/2/2021 By Balance b/d 3000

Motor Car

account

Date Particulars Amount Date Particulars Amoun

t

4/1/202

1

To Savoy Motors 4000

31/1/21 By Balance c/d 4000

1/2/202

1

To Balance b/d 4000

Savoy Motors

account

Date Particulars Amoun

t

Date Particulars Amoun

t

4/1/2021 By Motor car

account

4000

31/1/21 To Balance c/d 4000

1/2/2021 By Balance b/d 4000

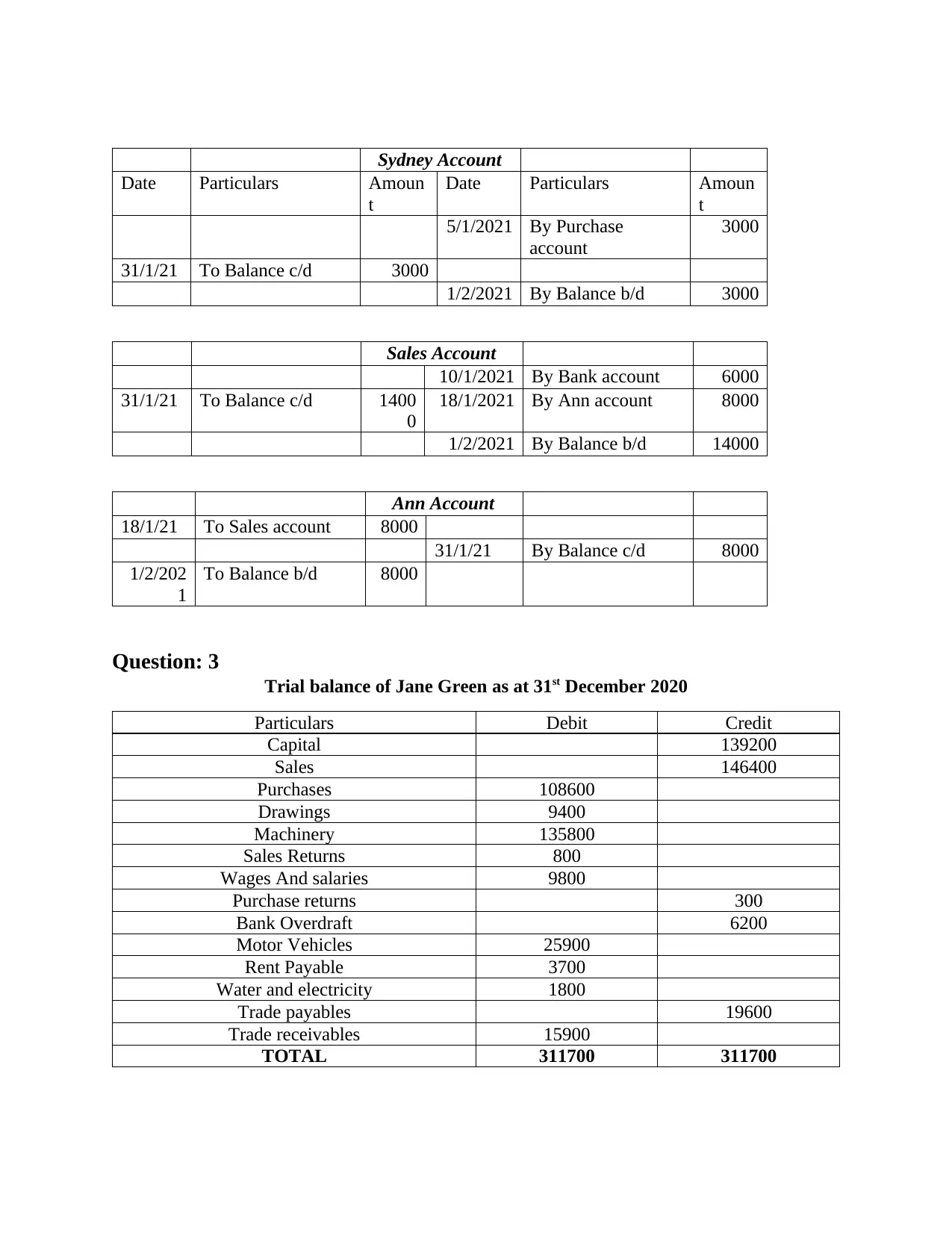

Sydney Account

Date Particulars Amoun

t

Date Particulars Amoun

t

5/1/2021 By Purchase

account

3000

31/1/21 To Balance c/d 3000

1/2/2021 By Balance b/d 3000

Sales Account

10/1/2021 By Bank account 6000

31/1/21 To Balance c/d 1400

0

18/1/2021 By Ann account 8000

1/2/2021 By Balance b/d 14000

Ann Account

18/1/21 To Sales account 8000

31/1/21 By Balance c/d 8000

1/2/202

1

To Balance b/d 8000

Question: 3

Trial balance of Jane Green as at 31st December 2020

Particulars Debit Credit

Capital 139200

Sales 146400

Purchases 108600

Drawings 9400

Machinery 135800

Sales Returns 800

Wages And salaries 9800

Purchase returns 300

Bank Overdraft 6200

Motor Vehicles 25900

Rent Payable 3700

Water and electricity 1800

Trade payables 19600

Trade receivables 15900

TOTAL 311700 311700

Date Particulars Amoun

t

Date Particulars Amoun

t

5/1/2021 By Purchase

account

3000

31/1/21 To Balance c/d 3000

1/2/2021 By Balance b/d 3000

Sales Account

10/1/2021 By Bank account 6000

31/1/21 To Balance c/d 1400

0

18/1/2021 By Ann account 8000

1/2/2021 By Balance b/d 14000

Ann Account

18/1/21 To Sales account 8000

31/1/21 By Balance c/d 8000

1/2/202

1

To Balance b/d 8000

Question: 3

Trial balance of Jane Green as at 31st December 2020

Particulars Debit Credit

Capital 139200

Sales 146400

Purchases 108600

Drawings 9400

Machinery 135800

Sales Returns 800

Wages And salaries 9800

Purchase returns 300

Bank Overdraft 6200

Motor Vehicles 25900

Rent Payable 3700

Water and electricity 1800

Trade payables 19600

Trade receivables 15900

TOTAL 311700 311700

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

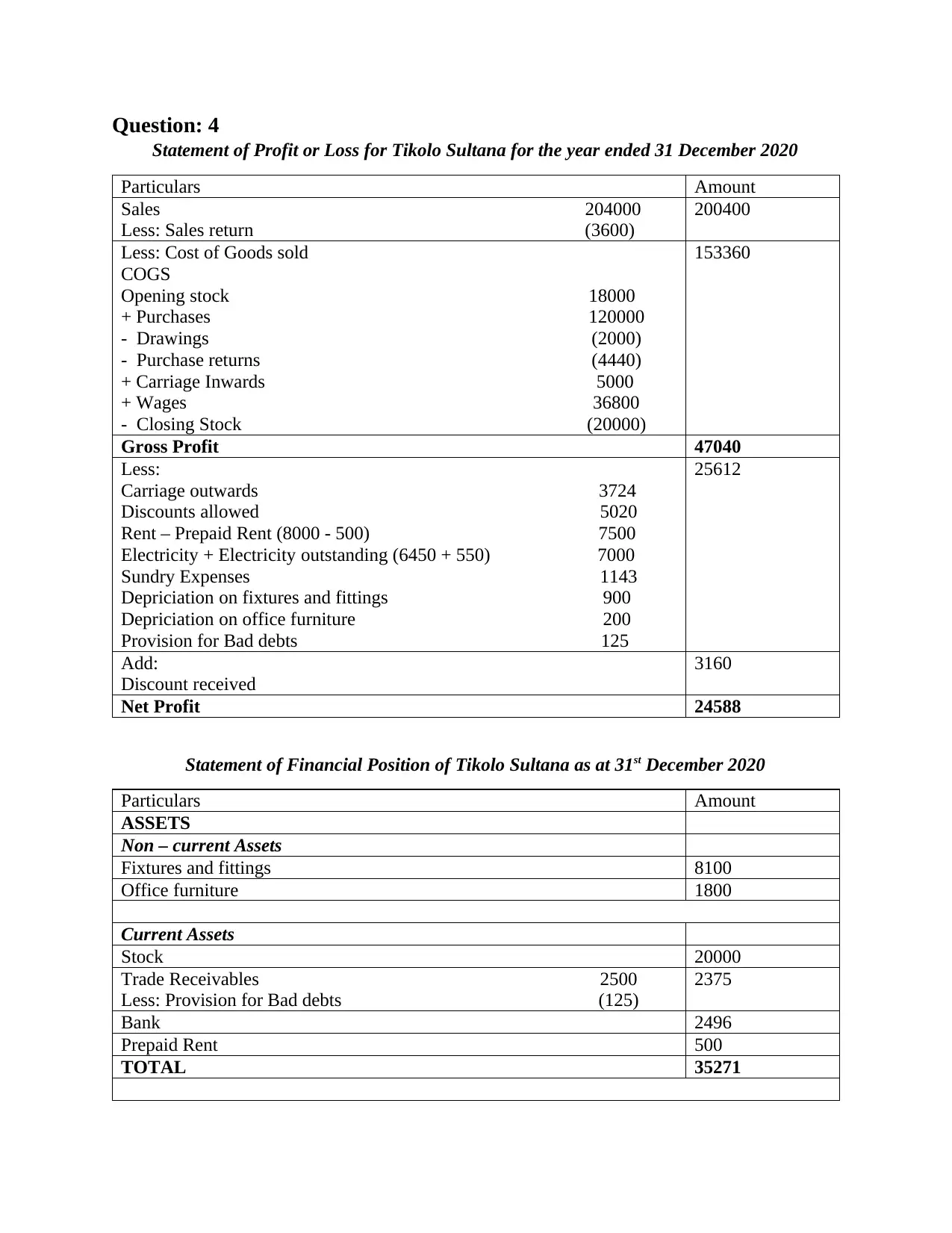

Question: 4

Statement of Profit or Loss for Tikolo Sultana for the year ended 31 December 2020

Particulars Amount

Sales 204000

Less: Sales return (3600)

200400

Less: Cost of Goods sold

COGS

Opening stock 18000

+ Purchases 120000

- Drawings (2000)

- Purchase returns (4440)

+ Carriage Inwards 5000

+ Wages 36800

- Closing Stock (20000)

153360

Gross Profit 47040

Less:

Carriage outwards 3724

Discounts allowed 5020

Rent – Prepaid Rent (8000 - 500) 7500

Electricity + Electricity outstanding (6450 + 550) 7000

Sundry Expenses 1143

Depriciation on fixtures and fittings 900

Depriciation on office furniture 200

Provision for Bad debts 125

25612

Add:

Discount received

3160

Net Profit 24588

Statement of Financial Position of Tikolo Sultana as at 31st December 2020

Particulars Amount

ASSETS

Non – current Assets

Fixtures and fittings 8100

Office furniture 1800

Current Assets

Stock 20000

Trade Receivables 2500

Less: Provision for Bad debts (125)

2375

Bank 2496

Prepaid Rent 500

TOTAL 35271

Statement of Profit or Loss for Tikolo Sultana for the year ended 31 December 2020

Particulars Amount

Sales 204000

Less: Sales return (3600)

200400

Less: Cost of Goods sold

COGS

Opening stock 18000

+ Purchases 120000

- Drawings (2000)

- Purchase returns (4440)

+ Carriage Inwards 5000

+ Wages 36800

- Closing Stock (20000)

153360

Gross Profit 47040

Less:

Carriage outwards 3724

Discounts allowed 5020

Rent – Prepaid Rent (8000 - 500) 7500

Electricity + Electricity outstanding (6450 + 550) 7000

Sundry Expenses 1143

Depriciation on fixtures and fittings 900

Depriciation on office furniture 200

Provision for Bad debts 125

25612

Add:

Discount received

3160

Net Profit 24588

Statement of Financial Position of Tikolo Sultana as at 31st December 2020

Particulars Amount

ASSETS

Non – current Assets

Fixtures and fittings 8100

Office furniture 1800

Current Assets

Stock 20000

Trade Receivables 2500

Less: Provision for Bad debts (125)

2375

Bank 2496

Prepaid Rent 500

TOTAL 35271

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

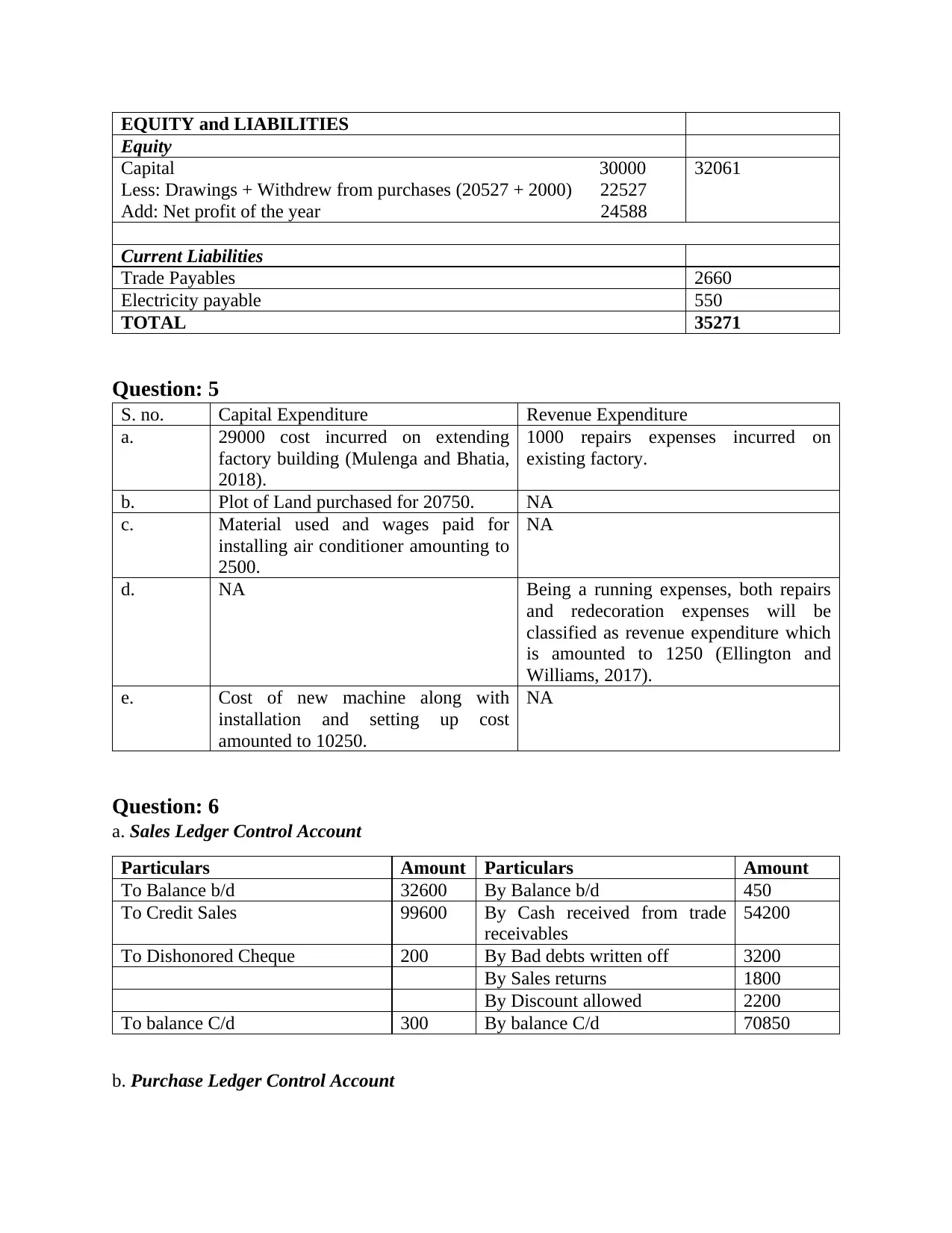

EQUITY and LIABILITIES

Equity

Capital 30000

Less: Drawings + Withdrew from purchases (20527 + 2000) 22527

Add: Net profit of the year 24588

32061

Current Liabilities

Trade Payables 2660

Electricity payable 550

TOTAL 35271

Question: 5

S. no. Capital Expenditure Revenue Expenditure

a. 29000 cost incurred on extending

factory building (Mulenga and Bhatia,

2018).

1000 repairs expenses incurred on

existing factory.

b. Plot of Land purchased for 20750. NA

c. Material used and wages paid for

installing air conditioner amounting to

2500.

NA

d. NA Being a running expenses, both repairs

and redecoration expenses will be

classified as revenue expenditure which

is amounted to 1250 (Ellington and

Williams, 2017).

e. Cost of new machine along with

installation and setting up cost

amounted to 10250.

NA

Question: 6

a. Sales Ledger Control Account

Particulars Amount Particulars Amount

To Balance b/d 32600 By Balance b/d 450

To Credit Sales 99600 By Cash received from trade

receivables

54200

To Dishonored Cheque 200 By Bad debts written off 3200

By Sales returns 1800

By Discount allowed 2200

To balance C/d 300 By balance C/d 70850

b. Purchase Ledger Control Account

Equity

Capital 30000

Less: Drawings + Withdrew from purchases (20527 + 2000) 22527

Add: Net profit of the year 24588

32061

Current Liabilities

Trade Payables 2660

Electricity payable 550

TOTAL 35271

Question: 5

S. no. Capital Expenditure Revenue Expenditure

a. 29000 cost incurred on extending

factory building (Mulenga and Bhatia,

2018).

1000 repairs expenses incurred on

existing factory.

b. Plot of Land purchased for 20750. NA

c. Material used and wages paid for

installing air conditioner amounting to

2500.

NA

d. NA Being a running expenses, both repairs

and redecoration expenses will be

classified as revenue expenditure which

is amounted to 1250 (Ellington and

Williams, 2017).

e. Cost of new machine along with

installation and setting up cost

amounted to 10250.

NA

Question: 6

a. Sales Ledger Control Account

Particulars Amount Particulars Amount

To Balance b/d 32600 By Balance b/d 450

To Credit Sales 99600 By Cash received from trade

receivables

54200

To Dishonored Cheque 200 By Bad debts written off 3200

By Sales returns 1800

By Discount allowed 2200

To balance C/d 300 By balance C/d 70850

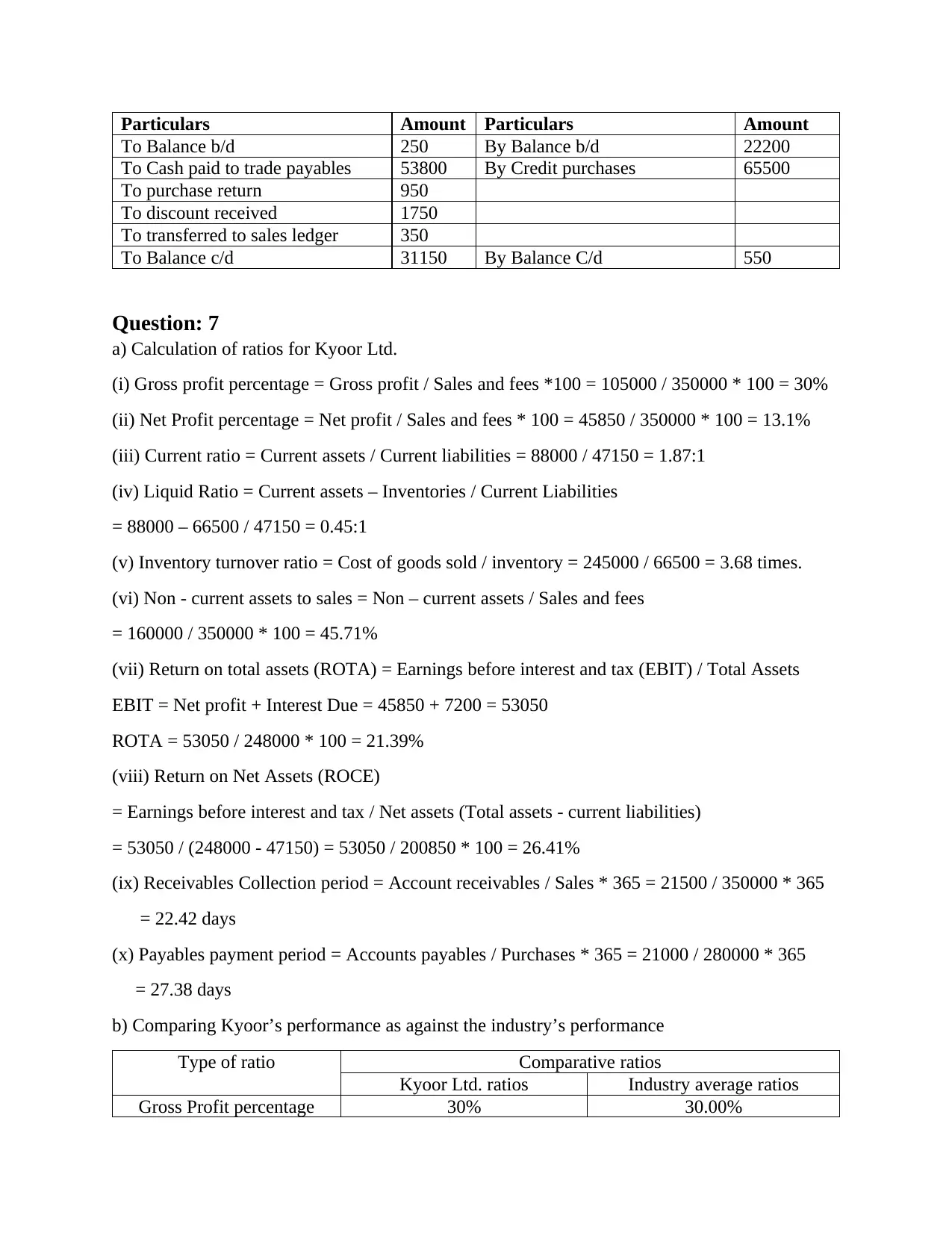

b. Purchase Ledger Control Account

Particulars Amount Particulars Amount

To Balance b/d 250 By Balance b/d 22200

To Cash paid to trade payables 53800 By Credit purchases 65500

To purchase return 950

To discount received 1750

To transferred to sales ledger 350

To Balance c/d 31150 By Balance C/d 550

Question: 7

a) Calculation of ratios for Kyoor Ltd.

(i) Gross profit percentage = Gross profit / Sales and fees *100 = 105000 / 350000 * 100 = 30%

(ii) Net Profit percentage = Net profit / Sales and fees * 100 = 45850 / 350000 * 100 = 13.1%

(iii) Current ratio = Current assets / Current liabilities = 88000 / 47150 = 1.87:1

(iv) Liquid Ratio = Current assets – Inventories / Current Liabilities

= 88000 – 66500 / 47150 = 0.45:1

(v) Inventory turnover ratio = Cost of goods sold / inventory = 245000 / 66500 = 3.68 times.

(vi) Non - current assets to sales = Non – current assets / Sales and fees

= 160000 / 350000 * 100 = 45.71%

(vii) Return on total assets (ROTA) = Earnings before interest and tax (EBIT) / Total Assets

EBIT = Net profit + Interest Due = 45850 + 7200 = 53050

ROTA = 53050 / 248000 * 100 = 21.39%

(viii) Return on Net Assets (ROCE)

= Earnings before interest and tax / Net assets (Total assets - current liabilities)

= 53050 / (248000 - 47150) = 53050 / 200850 * 100 = 26.41%

(ix) Receivables Collection period = Account receivables / Sales * 365 = 21500 / 350000 * 365

= 22.42 days

(x) Payables payment period = Accounts payables / Purchases * 365 = 21000 / 280000 * 365

= 27.38 days

b) Comparing Kyoor’s performance as against the industry’s performance

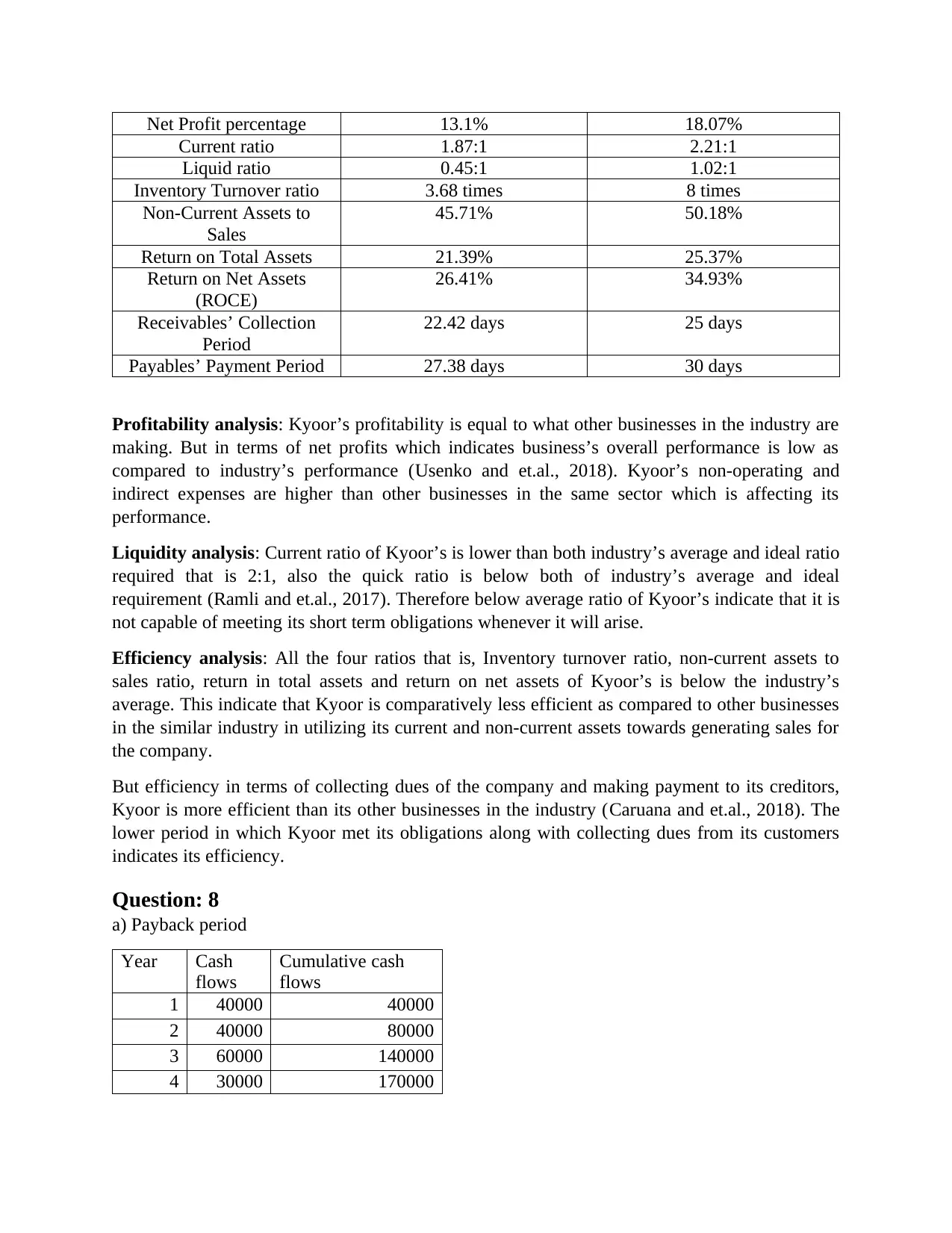

Type of ratio Comparative ratios

Kyoor Ltd. ratios Industry average ratios

Gross Profit percentage 30% 30.00%

To Balance b/d 250 By Balance b/d 22200

To Cash paid to trade payables 53800 By Credit purchases 65500

To purchase return 950

To discount received 1750

To transferred to sales ledger 350

To Balance c/d 31150 By Balance C/d 550

Question: 7

a) Calculation of ratios for Kyoor Ltd.

(i) Gross profit percentage = Gross profit / Sales and fees *100 = 105000 / 350000 * 100 = 30%

(ii) Net Profit percentage = Net profit / Sales and fees * 100 = 45850 / 350000 * 100 = 13.1%

(iii) Current ratio = Current assets / Current liabilities = 88000 / 47150 = 1.87:1

(iv) Liquid Ratio = Current assets – Inventories / Current Liabilities

= 88000 – 66500 / 47150 = 0.45:1

(v) Inventory turnover ratio = Cost of goods sold / inventory = 245000 / 66500 = 3.68 times.

(vi) Non - current assets to sales = Non – current assets / Sales and fees

= 160000 / 350000 * 100 = 45.71%

(vii) Return on total assets (ROTA) = Earnings before interest and tax (EBIT) / Total Assets

EBIT = Net profit + Interest Due = 45850 + 7200 = 53050

ROTA = 53050 / 248000 * 100 = 21.39%

(viii) Return on Net Assets (ROCE)

= Earnings before interest and tax / Net assets (Total assets - current liabilities)

= 53050 / (248000 - 47150) = 53050 / 200850 * 100 = 26.41%

(ix) Receivables Collection period = Account receivables / Sales * 365 = 21500 / 350000 * 365

= 22.42 days

(x) Payables payment period = Accounts payables / Purchases * 365 = 21000 / 280000 * 365

= 27.38 days

b) Comparing Kyoor’s performance as against the industry’s performance

Type of ratio Comparative ratios

Kyoor Ltd. ratios Industry average ratios

Gross Profit percentage 30% 30.00%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net Profit percentage 13.1% 18.07%

Current ratio 1.87:1 2.21:1

Liquid ratio 0.45:1 1.02:1

Inventory Turnover ratio 3.68 times 8 times

Non-Current Assets to

Sales

45.71% 50.18%

Return on Total Assets 21.39% 25.37%

Return on Net Assets

(ROCE)

26.41% 34.93%

Receivables’ Collection

Period

22.42 days 25 days

Payables’ Payment Period 27.38 days 30 days

Profitability analysis: Kyoor’s profitability is equal to what other businesses in the industry are

making. But in terms of net profits which indicates business’s overall performance is low as

compared to industry’s performance (Usenko and et.al., 2018). Kyoor’s non-operating and

indirect expenses are higher than other businesses in the same sector which is affecting its

performance.

Liquidity analysis: Current ratio of Kyoor’s is lower than both industry’s average and ideal ratio

required that is 2:1, also the quick ratio is below both of industry’s average and ideal

requirement (Ramli and et.al., 2017). Therefore below average ratio of Kyoor’s indicate that it is

not capable of meeting its short term obligations whenever it will arise.

Efficiency analysis: All the four ratios that is, Inventory turnover ratio, non-current assets to

sales ratio, return in total assets and return on net assets of Kyoor’s is below the industry’s

average. This indicate that Kyoor is comparatively less efficient as compared to other businesses

in the similar industry in utilizing its current and non-current assets towards generating sales for

the company.

But efficiency in terms of collecting dues of the company and making payment to its creditors,

Kyoor is more efficient than its other businesses in the industry (Caruana and et.al., 2018). The

lower period in which Kyoor met its obligations along with collecting dues from its customers

indicates its efficiency.

Question: 8

a) Payback period

Year Cash

flows

Cumulative cash

flows

1 40000 40000

2 40000 80000

3 60000 140000

4 30000 170000

Current ratio 1.87:1 2.21:1

Liquid ratio 0.45:1 1.02:1

Inventory Turnover ratio 3.68 times 8 times

Non-Current Assets to

Sales

45.71% 50.18%

Return on Total Assets 21.39% 25.37%

Return on Net Assets

(ROCE)

26.41% 34.93%

Receivables’ Collection

Period

22.42 days 25 days

Payables’ Payment Period 27.38 days 30 days

Profitability analysis: Kyoor’s profitability is equal to what other businesses in the industry are

making. But in terms of net profits which indicates business’s overall performance is low as

compared to industry’s performance (Usenko and et.al., 2018). Kyoor’s non-operating and

indirect expenses are higher than other businesses in the same sector which is affecting its

performance.

Liquidity analysis: Current ratio of Kyoor’s is lower than both industry’s average and ideal ratio

required that is 2:1, also the quick ratio is below both of industry’s average and ideal

requirement (Ramli and et.al., 2017). Therefore below average ratio of Kyoor’s indicate that it is

not capable of meeting its short term obligations whenever it will arise.

Efficiency analysis: All the four ratios that is, Inventory turnover ratio, non-current assets to

sales ratio, return in total assets and return on net assets of Kyoor’s is below the industry’s

average. This indicate that Kyoor is comparatively less efficient as compared to other businesses

in the similar industry in utilizing its current and non-current assets towards generating sales for

the company.

But efficiency in terms of collecting dues of the company and making payment to its creditors,

Kyoor is more efficient than its other businesses in the industry (Caruana and et.al., 2018). The

lower period in which Kyoor met its obligations along with collecting dues from its customers

indicates its efficiency.

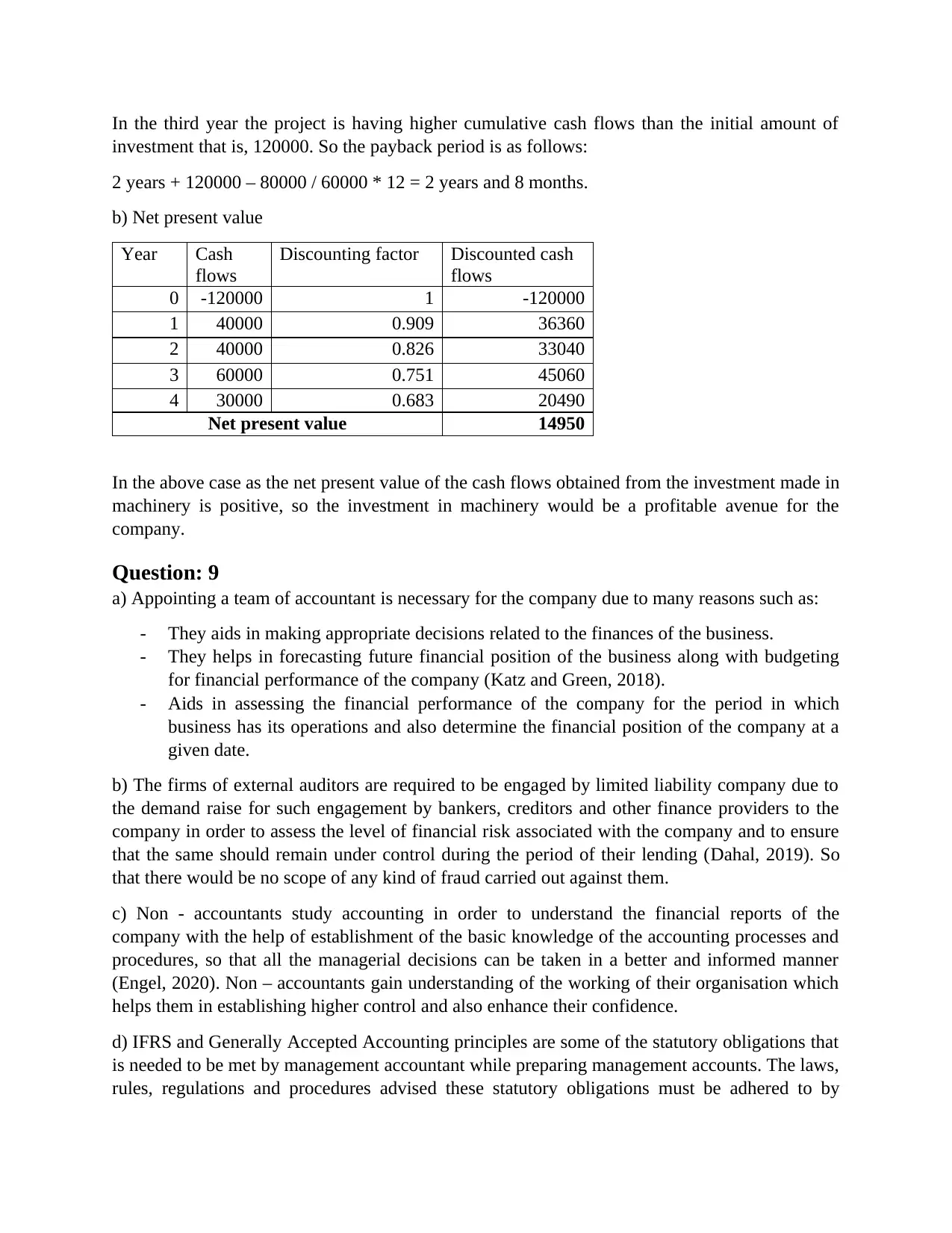

Question: 8

a) Payback period

Year Cash

flows

Cumulative cash

flows

1 40000 40000

2 40000 80000

3 60000 140000

4 30000 170000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In the third year the project is having higher cumulative cash flows than the initial amount of

investment that is, 120000. So the payback period is as follows:

2 years + 120000 – 80000 / 60000 * 12 = 2 years and 8 months.

b) Net present value

Year Cash

flows

Discounting factor Discounted cash

flows

0 -120000 1 -120000

1 40000 0.909 36360

2 40000 0.826 33040

3 60000 0.751 45060

4 30000 0.683 20490

Net present value 14950

In the above case as the net present value of the cash flows obtained from the investment made in

machinery is positive, so the investment in machinery would be a profitable avenue for the

company.

Question: 9

a) Appointing a team of accountant is necessary for the company due to many reasons such as:

- They aids in making appropriate decisions related to the finances of the business.

- They helps in forecasting future financial position of the business along with budgeting

for financial performance of the company (Katz and Green, 2018).

- Aids in assessing the financial performance of the company for the period in which

business has its operations and also determine the financial position of the company at a

given date.

b) The firms of external auditors are required to be engaged by limited liability company due to

the demand raise for such engagement by bankers, creditors and other finance providers to the

company in order to assess the level of financial risk associated with the company and to ensure

that the same should remain under control during the period of their lending (Dahal, 2019). So

that there would be no scope of any kind of fraud carried out against them.

c) Non - accountants study accounting in order to understand the financial reports of the

company with the help of establishment of the basic knowledge of the accounting processes and

procedures, so that all the managerial decisions can be taken in a better and informed manner

(Engel, 2020). Non – accountants gain understanding of the working of their organisation which

helps them in establishing higher control and also enhance their confidence.

d) IFRS and Generally Accepted Accounting principles are some of the statutory obligations that

is needed to be met by management accountant while preparing management accounts. The laws,

rules, regulations and procedures advised these statutory obligations must be adhered to by

investment that is, 120000. So the payback period is as follows:

2 years + 120000 – 80000 / 60000 * 12 = 2 years and 8 months.

b) Net present value

Year Cash

flows

Discounting factor Discounted cash

flows

0 -120000 1 -120000

1 40000 0.909 36360

2 40000 0.826 33040

3 60000 0.751 45060

4 30000 0.683 20490

Net present value 14950

In the above case as the net present value of the cash flows obtained from the investment made in

machinery is positive, so the investment in machinery would be a profitable avenue for the

company.

Question: 9

a) Appointing a team of accountant is necessary for the company due to many reasons such as:

- They aids in making appropriate decisions related to the finances of the business.

- They helps in forecasting future financial position of the business along with budgeting

for financial performance of the company (Katz and Green, 2018).

- Aids in assessing the financial performance of the company for the period in which

business has its operations and also determine the financial position of the company at a

given date.

b) The firms of external auditors are required to be engaged by limited liability company due to

the demand raise for such engagement by bankers, creditors and other finance providers to the

company in order to assess the level of financial risk associated with the company and to ensure

that the same should remain under control during the period of their lending (Dahal, 2019). So

that there would be no scope of any kind of fraud carried out against them.

c) Non - accountants study accounting in order to understand the financial reports of the

company with the help of establishment of the basic knowledge of the accounting processes and

procedures, so that all the managerial decisions can be taken in a better and informed manner

(Engel, 2020). Non – accountants gain understanding of the working of their organisation which

helps them in establishing higher control and also enhance their confidence.

d) IFRS and Generally Accepted Accounting principles are some of the statutory obligations that

is needed to be met by management accountant while preparing management accounts. The laws,

rules, regulations and procedures advised these statutory obligations must be adhered to by

management accountant (Keong, Pengb and Lengc, 2019). It is required in order to assist

management in making wise decisions for the business, so that standards set during planning

stage can be easily fulfilled.

e) The nature of accounting can be understood in two ways that is, the first way is understanding

it from qualitative perspective which describes the characteristics of accounting information as

reliable, comparable, understandable, relevant and faithful representation (Ellington and

Williams, 2017). While the second way is understanding it from quantitative aspect which

describes the features of creation of accounting information as an art or science, concerned with

only financial transactions, records transactions in terms of money, classifies, summarize,

analyze, interpret and communicate the final results to the parties interested in the accounting

information associated with the company.

So, the very purpose of accounting is the accumulation of financial information of the company

in order to communicate the financial performance and financial position of the company

(Mulenga and Bhatia, 2018). It is also used for assessing the liquidity of the company which

helps in making decisions of the business in order to manage it efficiently and effectively.

Question: 10

a) Depriciation: Depriciation is the charge against the assets of the business in order to reduce

the value of the asset as per its utilization. So, at the time of disposal of the assets, its value can

be brought down to zero.

b) Allowance for bad and doubtful debts: It is the amount which is reduced as a certain

percentage of trade receivables of the business from whom the amount has become doubtful to

be recovered (Howcroft, 2017). It is a charge against profit of the business to provide for

probable losses in the future.

c) Debentures: Debentures are the source through which business used to borrow from external

sources. It forms part of the debt capital of the business (Schaltegger, Etxeberria and Ortas,

2017). It is an instrument which may secured or unsecured both. So, it is long term source of

financing for the company arranged through the issuance of debentures on which regular interest

has been paid the by the issuer.

d) Preference shares: It is an instrument through which finance can be sourced by the business

where small units known as shares are issued to the shareholders who got benefit of being paid

of dividend before equity shareholders of the company (Yurchenko, 2017). And because of this

preference, they are known as preference shareholders. They have no ownership and voting

rights in the company.

e) Ordinary shares: It consists of the equity capital of the company where shareholders got the

right to vote in the affairs of the company and also represents the ownership of the company to

the extent of their holding out of the total equity share capital of the company. They got paid of

the company’s profit in the form of dividend after all the other obligations due to the company

for that period are met out.

management in making wise decisions for the business, so that standards set during planning

stage can be easily fulfilled.

e) The nature of accounting can be understood in two ways that is, the first way is understanding

it from qualitative perspective which describes the characteristics of accounting information as

reliable, comparable, understandable, relevant and faithful representation (Ellington and

Williams, 2017). While the second way is understanding it from quantitative aspect which

describes the features of creation of accounting information as an art or science, concerned with

only financial transactions, records transactions in terms of money, classifies, summarize,

analyze, interpret and communicate the final results to the parties interested in the accounting

information associated with the company.

So, the very purpose of accounting is the accumulation of financial information of the company

in order to communicate the financial performance and financial position of the company

(Mulenga and Bhatia, 2018). It is also used for assessing the liquidity of the company which

helps in making decisions of the business in order to manage it efficiently and effectively.

Question: 10

a) Depriciation: Depriciation is the charge against the assets of the business in order to reduce

the value of the asset as per its utilization. So, at the time of disposal of the assets, its value can

be brought down to zero.

b) Allowance for bad and doubtful debts: It is the amount which is reduced as a certain

percentage of trade receivables of the business from whom the amount has become doubtful to

be recovered (Howcroft, 2017). It is a charge against profit of the business to provide for

probable losses in the future.

c) Debentures: Debentures are the source through which business used to borrow from external

sources. It forms part of the debt capital of the business (Schaltegger, Etxeberria and Ortas,

2017). It is an instrument which may secured or unsecured both. So, it is long term source of

financing for the company arranged through the issuance of debentures on which regular interest

has been paid the by the issuer.

d) Preference shares: It is an instrument through which finance can be sourced by the business

where small units known as shares are issued to the shareholders who got benefit of being paid

of dividend before equity shareholders of the company (Yurchenko, 2017). And because of this

preference, they are known as preference shareholders. They have no ownership and voting

rights in the company.

e) Ordinary shares: It consists of the equity capital of the company where shareholders got the

right to vote in the affairs of the company and also represents the ownership of the company to

the extent of their holding out of the total equity share capital of the company. They got paid of

the company’s profit in the form of dividend after all the other obligations due to the company

for that period are met out.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.