Business Accounting Assignment: Trial Balance, Adjustments, KIA

VerifiedAdded on 2023/06/04

|10

|2403

|174

Homework Assignment

AI Summary

This business accounting assignment from Kent Institute of Australia (KIA) addresses key concepts such as trial balances, adjusting journal entries, and closing entries. It includes practical exercises like preparing journal entries for accrued interest and supplies, constructing an adjusted trial balance for Paul Services, and journalizing closing entries. The assignment also delves into the purpose of creating and adjusting trial balances, highlighting their role in error detection and financial statement preparation. Furthermore, it explains the differences between adjusting and closing entries, emphasizing their importance in maintaining accurate financial records. The document provides detailed explanations and numerical examples, offering a comprehensive overview of essential accounting principles. Find more solved assignments and study resources on Desklib.

BUSINESS

ACCOUNTING

ASSIGNMENT

ANKUR PATEL

K170960

KENT INSITUTE OF AUSTRALIA

ACCOUNTING

ASSIGNMENT

ANKUR PATEL

K170960

KENT INSITUTE OF AUSTRALIA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Question-1............................................................................................................................................................1

Question-2............................................................................................................................................................1

Question-3............................................................................................................................................................3

Question-4............................................................................................................................................................3

Question-5............................................................................................................................................................3

Question-6............................................................................................................................................................4

Trial balance....................................................................................................................................................4

Reason for Creation......................................................................................................................................4

Reason for recording...................................................................................................................................5

Purpose of writing an adjusted trial balance......................................................................................5

Difference between the adjustment entries and closing journal entries.................................6

References...........................................................................................................................................................7

Question-1............................................................................................................................................................1

Question-2............................................................................................................................................................1

Question-3............................................................................................................................................................3

Question-4............................................................................................................................................................3

Question-5............................................................................................................................................................3

Question-6............................................................................................................................................................4

Trial balance....................................................................................................................................................4

Reason for Creation......................................................................................................................................4

Reason for recording...................................................................................................................................5

Purpose of writing an adjusted trial balance......................................................................................5

Difference between the adjustment entries and closing journal entries.................................6

References...........................................................................................................................................................7

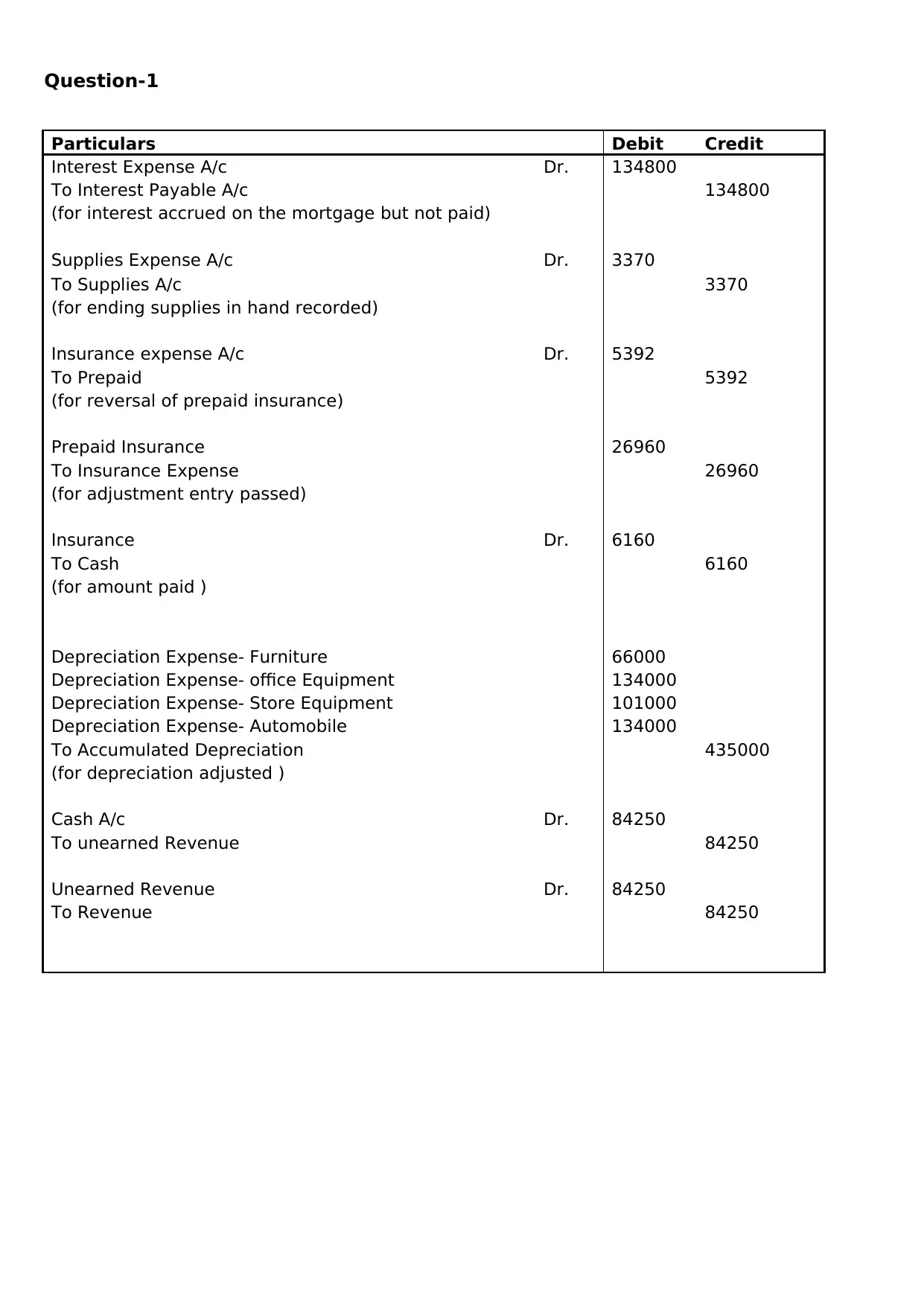

Question-1

Particulars Debit Credit

Interest Expense A/c Dr. 134800

To Interest Payable A/c 134800

(for interest accrued on the mortgage but not paid)

Supplies Expense A/c Dr. 3370

To Supplies A/c 3370

(for ending supplies in hand recorded)

Insurance expense A/c Dr. 5392

To Prepaid 5392

(for reversal of prepaid insurance)

Prepaid Insurance 26960

To Insurance Expense 26960

(for adjustment entry passed)

Insurance Dr. 6160

To Cash 6160

(for amount paid )

Depreciation Expense- Furniture 66000

Depreciation Expense- office Equipment 134000

Depreciation Expense- Store Equipment 101000

Depreciation Expense- Automobile 134000

To Accumulated Depreciation 435000

(for depreciation adjusted )

Cash A/c Dr. 84250

To unearned Revenue 84250

Unearned Revenue Dr. 84250

To Revenue 84250

Particulars Debit Credit

Interest Expense A/c Dr. 134800

To Interest Payable A/c 134800

(for interest accrued on the mortgage but not paid)

Supplies Expense A/c Dr. 3370

To Supplies A/c 3370

(for ending supplies in hand recorded)

Insurance expense A/c Dr. 5392

To Prepaid 5392

(for reversal of prepaid insurance)

Prepaid Insurance 26960

To Insurance Expense 26960

(for adjustment entry passed)

Insurance Dr. 6160

To Cash 6160

(for amount paid )

Depreciation Expense- Furniture 66000

Depreciation Expense- office Equipment 134000

Depreciation Expense- Store Equipment 101000

Depreciation Expense- Automobile 134000

To Accumulated Depreciation 435000

(for depreciation adjusted )

Cash A/c Dr. 84250

To unearned Revenue 84250

Unearned Revenue Dr. 84250

To Revenue 84250

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

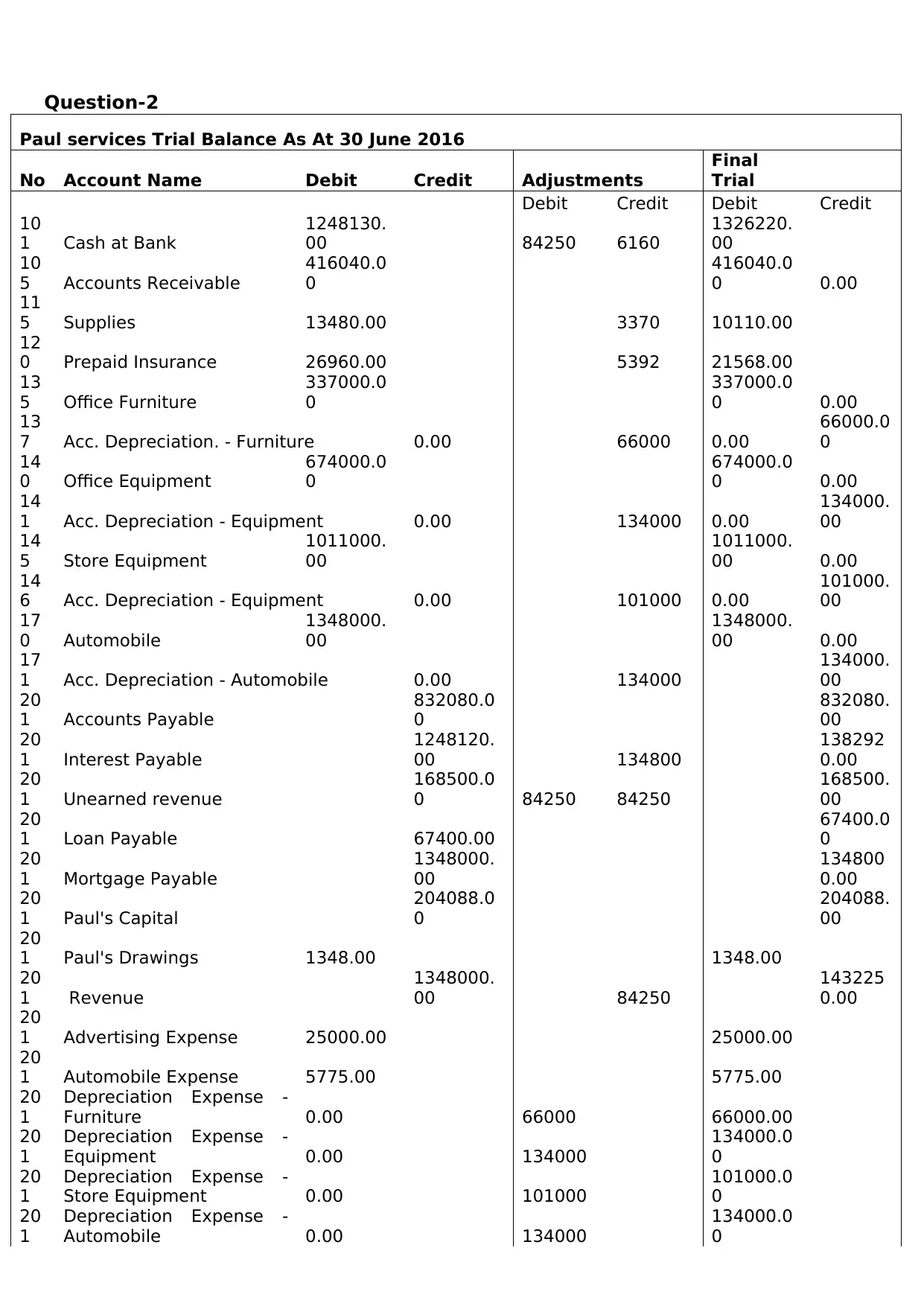

Question-2

Paul services Trial Balance As At 30 June 2016

No Account Name Debit Credit Adjustments

Final

Trial

Debit Credit Debit Credit

10

1 Cash at Bank

1248130.

00 84250 6160

1326220.

00

10

5 Accounts Receivable

416040.0

0

416040.0

0 0.00

11

5 Supplies 13480.00 3370 10110.00

12

0 Prepaid Insurance 26960.00 5392 21568.00

13

5 Office Furniture

337000.0

0

337000.0

0 0.00

13

7 Acc. Depreciation. - Furniture 0.00 66000 0.00

66000.0

0

14

0 Office Equipment

674000.0

0

674000.0

0 0.00

14

1 Acc. Depreciation - Equipment 0.00 134000 0.00

134000.

00

14

5 Store Equipment

1011000.

00

1011000.

00 0.00

14

6 Acc. Depreciation - Equipment 0.00 101000 0.00

101000.

00

17

0 Automobile

1348000.

00

1348000.

00 0.00

17

1 Acc. Depreciation - Automobile 0.00 134000

134000.

00

20

1 Accounts Payable

832080.0

0

832080.

00

20

1 Interest Payable

1248120.

00 134800

138292

0.00

20

1 Unearned revenue

168500.0

0 84250 84250

168500.

00

20

1 Loan Payable 67400.00

67400.0

0

20

1 Mortgage Payable

1348000.

00

134800

0.00

20

1 Paul's Capital

204088.0

0

204088.

00

20

1 Paul's Drawings 1348.00 1348.00

20

1 Revenue

1348000.

00 84250

143225

0.00

20

1 Advertising Expense 25000.00 25000.00

20

1 Automobile Expense 5775.00 5775.00

20

1

Depreciation Expense -

Furniture 0.00 66000 66000.00

20

1

Depreciation Expense -

Equipment 0.00 134000

134000.0

0

20

1

Depreciation Expense -

Store Equipment 0.00 101000

101000.0

0

20

1

Depreciation Expense -

Automobile 0.00 134000

134000.0

0

Paul services Trial Balance As At 30 June 2016

No Account Name Debit Credit Adjustments

Final

Trial

Debit Credit Debit Credit

10

1 Cash at Bank

1248130.

00 84250 6160

1326220.

00

10

5 Accounts Receivable

416040.0

0

416040.0

0 0.00

11

5 Supplies 13480.00 3370 10110.00

12

0 Prepaid Insurance 26960.00 5392 21568.00

13

5 Office Furniture

337000.0

0

337000.0

0 0.00

13

7 Acc. Depreciation. - Furniture 0.00 66000 0.00

66000.0

0

14

0 Office Equipment

674000.0

0

674000.0

0 0.00

14

1 Acc. Depreciation - Equipment 0.00 134000 0.00

134000.

00

14

5 Store Equipment

1011000.

00

1011000.

00 0.00

14

6 Acc. Depreciation - Equipment 0.00 101000 0.00

101000.

00

17

0 Automobile

1348000.

00

1348000.

00 0.00

17

1 Acc. Depreciation - Automobile 0.00 134000

134000.

00

20

1 Accounts Payable

832080.0

0

832080.

00

20

1 Interest Payable

1248120.

00 134800

138292

0.00

20

1 Unearned revenue

168500.0

0 84250 84250

168500.

00

20

1 Loan Payable 67400.00

67400.0

0

20

1 Mortgage Payable

1348000.

00

134800

0.00

20

1 Paul's Capital

204088.0

0

204088.

00

20

1 Paul's Drawings 1348.00 1348.00

20

1 Revenue

1348000.

00 84250

143225

0.00

20

1 Advertising Expense 25000.00 25000.00

20

1 Automobile Expense 5775.00 5775.00

20

1

Depreciation Expense -

Furniture 0.00 66000 66000.00

20

1

Depreciation Expense -

Equipment 0.00 134000

134000.0

0

20

1

Depreciation Expense -

Store Equipment 0.00 101000

101000.0

0

20

1

Depreciation Expense -

Automobile 0.00 134000

134000.0

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

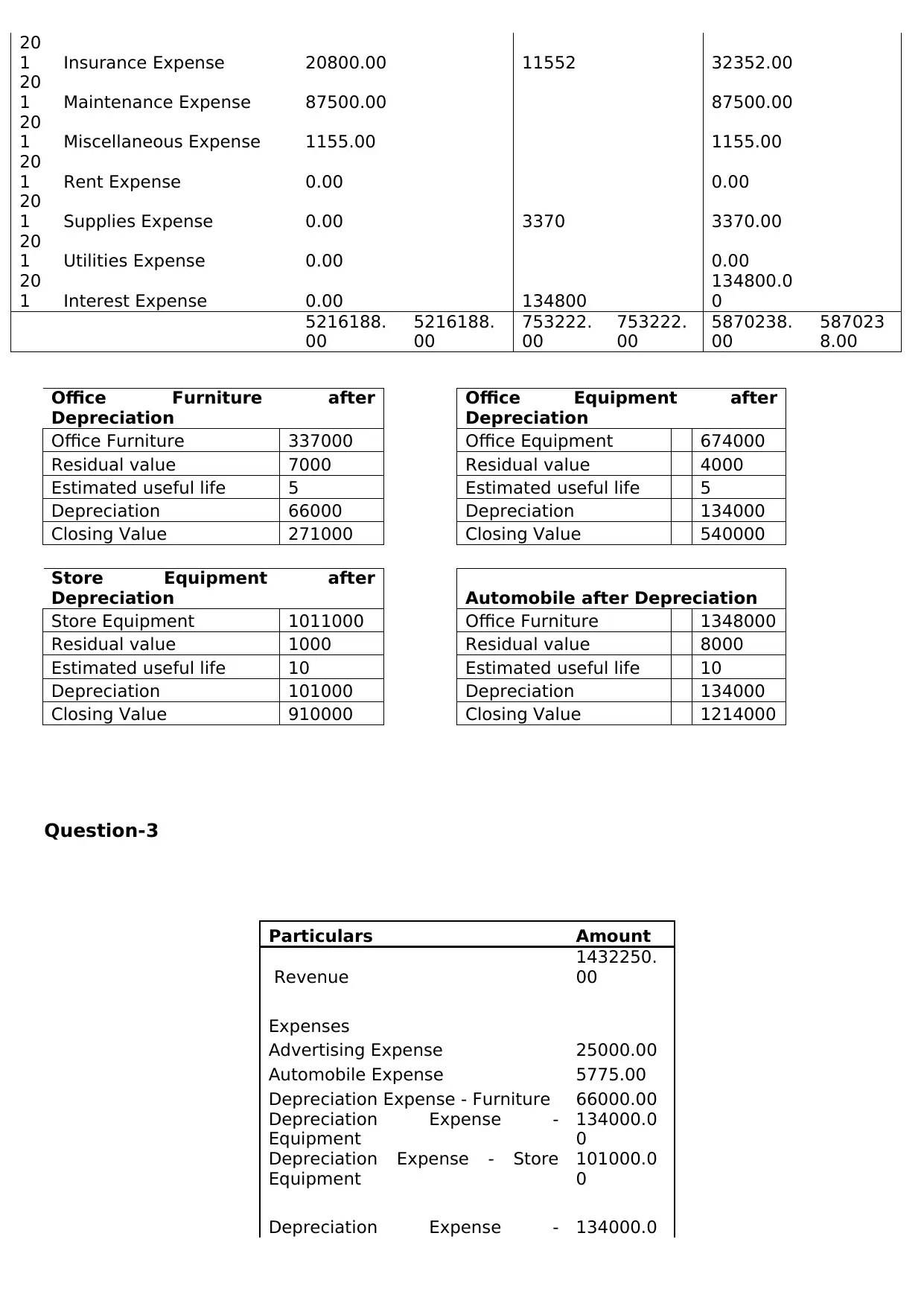

20

1 Insurance Expense 20800.00 11552 32352.00

20

1 Maintenance Expense 87500.00 87500.00

20

1 Miscellaneous Expense 1155.00 1155.00

20

1 Rent Expense 0.00 0.00

20

1 Supplies Expense 0.00 3370 3370.00

20

1 Utilities Expense 0.00 0.00

20

1 Interest Expense 0.00 134800

134800.0

0

5216188.

00

5216188.

00

753222.

00

753222.

00

5870238.

00

587023

8.00

Office Furniture after

Depreciation

Office Equipment after

Depreciation

Office Furniture 337000 Office Equipment 674000

Residual value 7000 Residual value 4000

Estimated useful life 5 Estimated useful life 5

Depreciation 66000 Depreciation 134000

Closing Value 271000 Closing Value 540000

Store Equipment after

Depreciation Automobile after Depreciation

Store Equipment 1011000 Office Furniture 1348000

Residual value 1000 Residual value 8000

Estimated useful life 10 Estimated useful life 10

Depreciation 101000 Depreciation 134000

Closing Value 910000 Closing Value 1214000

Question-3

Particulars Amount

Revenue

1432250.

00

Expenses

Advertising Expense 25000.00

Automobile Expense 5775.00

Depreciation Expense - Furniture 66000.00

Depreciation Expense -

Equipment

134000.0

0

Depreciation Expense - Store

Equipment

101000.0

0

Depreciation Expense - 134000.0

1 Insurance Expense 20800.00 11552 32352.00

20

1 Maintenance Expense 87500.00 87500.00

20

1 Miscellaneous Expense 1155.00 1155.00

20

1 Rent Expense 0.00 0.00

20

1 Supplies Expense 0.00 3370 3370.00

20

1 Utilities Expense 0.00 0.00

20

1 Interest Expense 0.00 134800

134800.0

0

5216188.

00

5216188.

00

753222.

00

753222.

00

5870238.

00

587023

8.00

Office Furniture after

Depreciation

Office Equipment after

Depreciation

Office Furniture 337000 Office Equipment 674000

Residual value 7000 Residual value 4000

Estimated useful life 5 Estimated useful life 5

Depreciation 66000 Depreciation 134000

Closing Value 271000 Closing Value 540000

Store Equipment after

Depreciation Automobile after Depreciation

Store Equipment 1011000 Office Furniture 1348000

Residual value 1000 Residual value 8000

Estimated useful life 10 Estimated useful life 10

Depreciation 101000 Depreciation 134000

Closing Value 910000 Closing Value 1214000

Question-3

Particulars Amount

Revenue

1432250.

00

Expenses

Advertising Expense 25000.00

Automobile Expense 5775.00

Depreciation Expense - Furniture 66000.00

Depreciation Expense -

Equipment

134000.0

0

Depreciation Expense - Store

Equipment

101000.0

0

Depreciation Expense - 134000.0

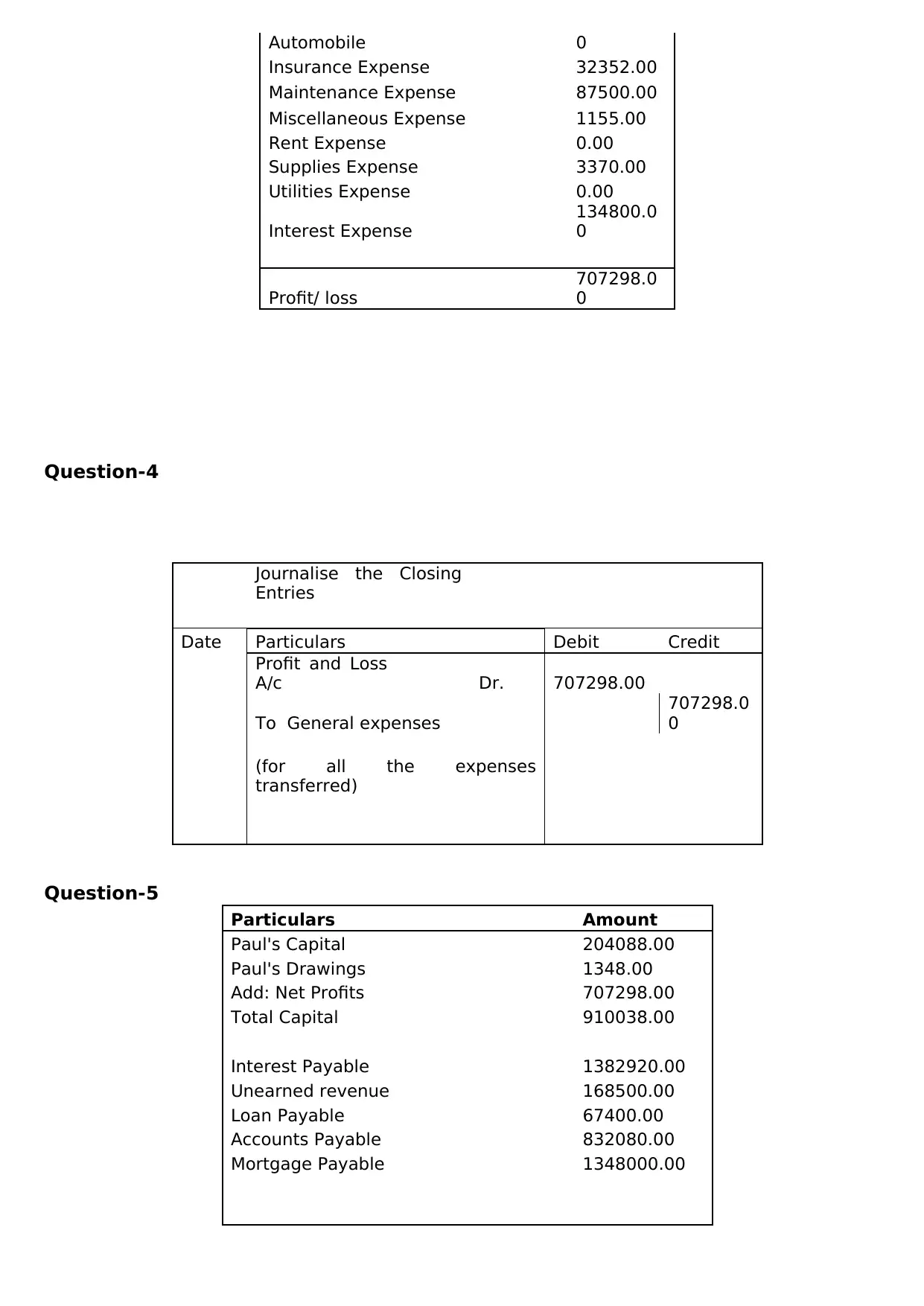

Automobile 0

Insurance Expense 32352.00

Maintenance Expense 87500.00

Miscellaneous Expense 1155.00

Rent Expense 0.00

Supplies Expense 3370.00

Utilities Expense 0.00

Interest Expense

134800.0

0

Profit/ loss

707298.0

0

Question-4

Journalise the Closing

Entries

Date Particulars Debit Credit

Profit and Loss

A/c Dr. 707298.00

To General expenses

707298.0

0

(for all the expenses

transferred)

Question-5

Particulars Amount

Paul's Capital 204088.00

Paul's Drawings 1348.00

Add: Net Profits 707298.00

Total Capital 910038.00

Interest Payable 1382920.00

Unearned revenue 168500.00

Loan Payable 67400.00

Accounts Payable 832080.00

Mortgage Payable 1348000.00

Insurance Expense 32352.00

Maintenance Expense 87500.00

Miscellaneous Expense 1155.00

Rent Expense 0.00

Supplies Expense 3370.00

Utilities Expense 0.00

Interest Expense

134800.0

0

Profit/ loss

707298.0

0

Question-4

Journalise the Closing

Entries

Date Particulars Debit Credit

Profit and Loss

A/c Dr. 707298.00

To General expenses

707298.0

0

(for all the expenses

transferred)

Question-5

Particulars Amount

Paul's Capital 204088.00

Paul's Drawings 1348.00

Add: Net Profits 707298.00

Total Capital 910038.00

Interest Payable 1382920.00

Unearned revenue 168500.00

Loan Payable 67400.00

Accounts Payable 832080.00

Mortgage Payable 1348000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

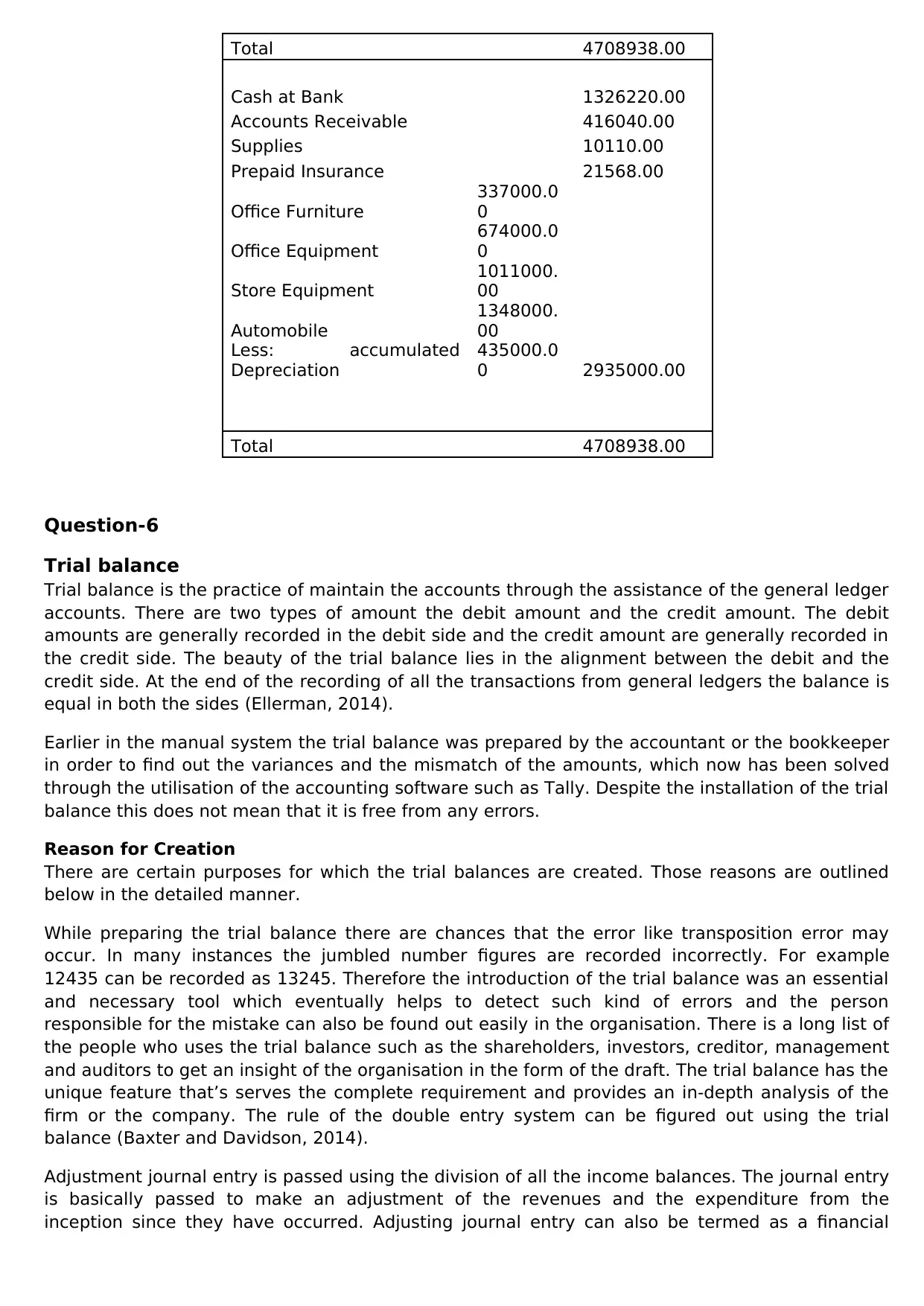

Total 4708938.00

Cash at Bank 1326220.00

Accounts Receivable 416040.00

Supplies 10110.00

Prepaid Insurance 21568.00

Office Furniture

337000.0

0

Office Equipment

674000.0

0

Store Equipment

1011000.

00

Automobile

1348000.

00

Less: accumulated

Depreciation

435000.0

0 2935000.00

Total 4708938.00

Question-6

Trial balance

Trial balance is the practice of maintain the accounts through the assistance of the general ledger

accounts. There are two types of amount the debit amount and the credit amount. The debit

amounts are generally recorded in the debit side and the credit amount are generally recorded in

the credit side. The beauty of the trial balance lies in the alignment between the debit and the

credit side. At the end of the recording of all the transactions from general ledgers the balance is

equal in both the sides (Ellerman, 2014).

Earlier in the manual system the trial balance was prepared by the accountant or the bookkeeper

in order to find out the variances and the mismatch of the amounts, which now has been solved

through the utilisation of the accounting software such as Tally. Despite the installation of the trial

balance this does not mean that it is free from any errors.

Reason for Creation

There are certain purposes for which the trial balances are created. Those reasons are outlined

below in the detailed manner.

While preparing the trial balance there are chances that the error like transposition error may

occur. In many instances the jumbled number figures are recorded incorrectly. For example

12435 can be recorded as 13245. Therefore the introduction of the trial balance was an essential

and necessary tool which eventually helps to detect such kind of errors and the person

responsible for the mistake can also be found out easily in the organisation. There is a long list of

the people who uses the trial balance such as the shareholders, investors, creditor, management

and auditors to get an insight of the organisation in the form of the draft. The trial balance has the

unique feature that’s serves the complete requirement and provides an in-depth analysis of the

firm or the company. The rule of the double entry system can be figured out using the trial

balance (Baxter and Davidson, 2014).

Adjustment journal entry is passed using the division of all the income balances. The journal entry

is basically passed to make an adjustment of the revenues and the expenditure from the

inception since they have occurred. Adjusting journal entry can also be termed as a financial

Cash at Bank 1326220.00

Accounts Receivable 416040.00

Supplies 10110.00

Prepaid Insurance 21568.00

Office Furniture

337000.0

0

Office Equipment

674000.0

0

Store Equipment

1011000.

00

Automobile

1348000.

00

Less: accumulated

Depreciation

435000.0

0 2935000.00

Total 4708938.00

Question-6

Trial balance

Trial balance is the practice of maintain the accounts through the assistance of the general ledger

accounts. There are two types of amount the debit amount and the credit amount. The debit

amounts are generally recorded in the debit side and the credit amount are generally recorded in

the credit side. The beauty of the trial balance lies in the alignment between the debit and the

credit side. At the end of the recording of all the transactions from general ledgers the balance is

equal in both the sides (Ellerman, 2014).

Earlier in the manual system the trial balance was prepared by the accountant or the bookkeeper

in order to find out the variances and the mismatch of the amounts, which now has been solved

through the utilisation of the accounting software such as Tally. Despite the installation of the trial

balance this does not mean that it is free from any errors.

Reason for Creation

There are certain purposes for which the trial balances are created. Those reasons are outlined

below in the detailed manner.

While preparing the trial balance there are chances that the error like transposition error may

occur. In many instances the jumbled number figures are recorded incorrectly. For example

12435 can be recorded as 13245. Therefore the introduction of the trial balance was an essential

and necessary tool which eventually helps to detect such kind of errors and the person

responsible for the mistake can also be found out easily in the organisation. There is a long list of

the people who uses the trial balance such as the shareholders, investors, creditor, management

and auditors to get an insight of the organisation in the form of the draft. The trial balance has the

unique feature that’s serves the complete requirement and provides an in-depth analysis of the

firm or the company. The rule of the double entry system can be figured out using the trial

balance (Baxter and Davidson, 2014).

Adjustment journal entry is passed using the division of all the income balances. The journal entry

is basically passed to make an adjustment of the revenues and the expenditure from the

inception since they have occurred. Adjusting journal entry can also be termed as a financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reporting that corrects the mistake which have made in the previous years in the accounting

period. The adjusted journal entry is used to conform and make the balance with the accrual

concept. The adjusted journal entry is passed just before the preparation of the financial

statements to transfer the amount into the financial statements and reflect the clear and the

transparent picture. To manage the accounting cycles the adjusting journal entry is necessary and

a bigger picture is reflected in order to look at the economic changes of the firm (Horngren,

2012).

Reason for recording

Adjusting entries are the journal entries that are recorded at the end of the accounting period in

order to alter the ending balances of the general ledger. It is usually impossible to create the

financial statements that are fully in compliance with the accounting standards without the

adjusted journal entries being passed. Adjusting entries are recorded for the type of the

accounting transaction such as to record the depreciation and amortisation of the period, to

record a warranty reserve, when the sales reserve is created, or when any accrued expenses like

prepaid insurance or the expenses are recorded (Carey, Knowles and Towers-Clark, 2017) To

address the monthly revenue figure the adjusted entries are recorded so that the organisations

can get a clear picture of their books of accounts. The proper and the complete knowledge of the

adjustment journal entry help in knowing the future of the services. Therefore these journal

entries help in choosing the plans so business could pick up for the long term benefit. Altered

entries are by and large made up at each and every date of bookkeeping period that might be

either yearly or month to month. The report so prepared showcases the incomes that have been

earned and furthermore helps in knowing the costs that were acquired amid the bookkeeping

time frame (Warren and Jones, 2018)

Purpose of writing an adjusted trial balance

The adjusted trial balance is an internal document or a draft and not the financial statement;

rather it is used to make the financial statements of the company. The adjusted trial balance is

prepared when the listing of all the accounts and the balances are contained in the general ledger

and side by side the adjusting entries are also made. The basic purpose of the adjusted trial

balance is to have a verification of the debit and the credit balances, to verify that no adjusting

journal entry has been omitted (DWilliams, Haka,Bettner and Carcello, 2015).

Moreover in order to figure out whether the net income has been reported correctly or not and to

get an insight of the adjusting entries in the accounting duration. The primary objective of writing

the trial balance is to identify any variances among the debit and the credit balances all together.

Adjusted trial balances are introduced in the end of the bookkeeping cycle. Setting up a balanced

preliminary trial balance will help in building up the financial statements for a particular term and

before setting up balanced preliminary trial balances the yearly changes are required to be made.

The other explanation behind setting up the balanced preliminary TB is for guaranteeing

thatadjusting entries were recorded effectively (Weil, Schipper and Francis, 2013). According to

the last step through the financial statements the company performance is the major outlook in

the eyes of the creditors, investors, auditors and shareholders. If there is any variance in the

financial statements than it will not be accepted by the users of the statements (Kwok, 2017).

Difference between the adjustment entries and closing journal entries

The major variance between the adjusting journal entries and closing entries are that adjusting

entries are the time period of recording. In case of the adjusted journal entries, it is recorded at

the end of the financial year but before the preparation of the financial reports and these records

is maintained as a proof for the purpose of the organisation itself. Moreover the up to date

period. The adjusted journal entry is used to conform and make the balance with the accrual

concept. The adjusted journal entry is passed just before the preparation of the financial

statements to transfer the amount into the financial statements and reflect the clear and the

transparent picture. To manage the accounting cycles the adjusting journal entry is necessary and

a bigger picture is reflected in order to look at the economic changes of the firm (Horngren,

2012).

Reason for recording

Adjusting entries are the journal entries that are recorded at the end of the accounting period in

order to alter the ending balances of the general ledger. It is usually impossible to create the

financial statements that are fully in compliance with the accounting standards without the

adjusted journal entries being passed. Adjusting entries are recorded for the type of the

accounting transaction such as to record the depreciation and amortisation of the period, to

record a warranty reserve, when the sales reserve is created, or when any accrued expenses like

prepaid insurance or the expenses are recorded (Carey, Knowles and Towers-Clark, 2017) To

address the monthly revenue figure the adjusted entries are recorded so that the organisations

can get a clear picture of their books of accounts. The proper and the complete knowledge of the

adjustment journal entry help in knowing the future of the services. Therefore these journal

entries help in choosing the plans so business could pick up for the long term benefit. Altered

entries are by and large made up at each and every date of bookkeeping period that might be

either yearly or month to month. The report so prepared showcases the incomes that have been

earned and furthermore helps in knowing the costs that were acquired amid the bookkeeping

time frame (Warren and Jones, 2018)

Purpose of writing an adjusted trial balance

The adjusted trial balance is an internal document or a draft and not the financial statement;

rather it is used to make the financial statements of the company. The adjusted trial balance is

prepared when the listing of all the accounts and the balances are contained in the general ledger

and side by side the adjusting entries are also made. The basic purpose of the adjusted trial

balance is to have a verification of the debit and the credit balances, to verify that no adjusting

journal entry has been omitted (DWilliams, Haka,Bettner and Carcello, 2015).

Moreover in order to figure out whether the net income has been reported correctly or not and to

get an insight of the adjusting entries in the accounting duration. The primary objective of writing

the trial balance is to identify any variances among the debit and the credit balances all together.

Adjusted trial balances are introduced in the end of the bookkeeping cycle. Setting up a balanced

preliminary trial balance will help in building up the financial statements for a particular term and

before setting up balanced preliminary trial balances the yearly changes are required to be made.

The other explanation behind setting up the balanced preliminary TB is for guaranteeing

thatadjusting entries were recorded effectively (Weil, Schipper and Francis, 2013). According to

the last step through the financial statements the company performance is the major outlook in

the eyes of the creditors, investors, auditors and shareholders. If there is any variance in the

financial statements than it will not be accepted by the users of the statements (Kwok, 2017).

Difference between the adjustment entries and closing journal entries

The major variance between the adjusting journal entries and closing entries are that adjusting

entries are the time period of recording. In case of the adjusted journal entries, it is recorded at

the end of the financial year but before the preparation of the financial reports and these records

is maintained as a proof for the purpose of the organisation itself. Moreover the up to date

financial statements will be helpful for the company and the users of the same. The example of

accrual expenses is a good example to determine the adjustment entries treatment. The incomes

that are not yet received such as the interest accrued on the loan and not yet paid will be

adjusted with the help of an entry. Assuming the interest rate on $30,000 note payable is 9%

accruing the interest for one month (Laitinen, 2015).

Interest

Expense

150

Interest

Payable

15

0

The other entries posted involve the amounts for which the amounts have been already

transferred to the respective expense account already.

Closing entries on the other hand are posted on the last day of the accounting period and are

posted in the records but they are posted in the records once the financial statements are ready

(Taleb, Gibson and Hovey, 2015).

Most of the time,reports are inclusive of closing entries. The closing entries are also expected to

bring the difference to zero between the revenues and the expenses. This also means that the

revenue and expense accounts will start New Year with nothing in the accounts. This allows the

business entity to report the New Year profits and expenses that to with an ease.

accrual expenses is a good example to determine the adjustment entries treatment. The incomes

that are not yet received such as the interest accrued on the loan and not yet paid will be

adjusted with the help of an entry. Assuming the interest rate on $30,000 note payable is 9%

accruing the interest for one month (Laitinen, 2015).

Interest

Expense

150

Interest

Payable

15

0

The other entries posted involve the amounts for which the amounts have been already

transferred to the respective expense account already.

Closing entries on the other hand are posted on the last day of the accounting period and are

posted in the records but they are posted in the records once the financial statements are ready

(Taleb, Gibson and Hovey, 2015).

Most of the time,reports are inclusive of closing entries. The closing entries are also expected to

bring the difference to zero between the revenues and the expenses. This also means that the

revenue and expense accounts will start New Year with nothing in the accounts. This allows the

business entity to report the New Year profits and expenses that to with an ease.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Baxter, W.T. and Davidson, S. eds. (2014) Studies in accounting (Vol. 4). California: Routledge.

Carey, M., Knowles, C. and Towers-Clark, J. (2017) Accounting: a smart approach. London: Oxford

University Press.

DWilliams, J.R., Haka, S.F., Bettner, M.S. and Carcello, J.V., (2015) Financial and managerial

accounting.China: China Machine Press.

Ellerman, D., (2014) On double-entry bookkeeping: The mathematical treatment. Accounting

Education, 23(5), pp.483-501.

Horngren, C., Harrison, W., Oliver, S., Best, P., Fraser, D. and Tan, R., (2012) Financial

accounting.London: Pearson Higher Education AU.

Kwok, B.K. (2017) Accounting irregularities in financial statements: A definitive guide for litigators,

auditors and fraud investigators. California: Routledge.

Laitinen, E.K., (2015) Traditional versus operating cash flow in failure prediction. Journal of

Business Finance & Accounting, 21(2), pp.195-217.

Taleb, M.A., Gibson, B. and Hovey, M. (2015) Fifty years of Sustainability Accounting: does

accounting for income in business sustainability really exist?.International Journal of Accounting

and Financial Reporting, 5(1), pp.36-47.

Warren, C.S. and Jones, J. (2018) Corporate financial accounting. Boston: Cengage Learning.

Weil, R.L., Schipper, K. and Francis, J., (2013) Financial accounting: an introduction to concepts,

methods and uses.Boston: Cengage Learning.

Baxter, W.T. and Davidson, S. eds. (2014) Studies in accounting (Vol. 4). California: Routledge.

Carey, M., Knowles, C. and Towers-Clark, J. (2017) Accounting: a smart approach. London: Oxford

University Press.

DWilliams, J.R., Haka, S.F., Bettner, M.S. and Carcello, J.V., (2015) Financial and managerial

accounting.China: China Machine Press.

Ellerman, D., (2014) On double-entry bookkeeping: The mathematical treatment. Accounting

Education, 23(5), pp.483-501.

Horngren, C., Harrison, W., Oliver, S., Best, P., Fraser, D. and Tan, R., (2012) Financial

accounting.London: Pearson Higher Education AU.

Kwok, B.K. (2017) Accounting irregularities in financial statements: A definitive guide for litigators,

auditors and fraud investigators. California: Routledge.

Laitinen, E.K., (2015) Traditional versus operating cash flow in failure prediction. Journal of

Business Finance & Accounting, 21(2), pp.195-217.

Taleb, M.A., Gibson, B. and Hovey, M. (2015) Fifty years of Sustainability Accounting: does

accounting for income in business sustainability really exist?.International Journal of Accounting

and Financial Reporting, 5(1), pp.36-47.

Warren, C.S. and Jones, J. (2018) Corporate financial accounting. Boston: Cengage Learning.

Weil, R.L., Schipper, K. and Francis, J., (2013) Financial accounting: an introduction to concepts,

methods and uses.Boston: Cengage Learning.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.