Report on Business Decision Analysis, Pricing and CVP Analysis

VerifiedAdded on 2023/06/05

|21

|5089

|397

Report

AI Summary

This report provides a comprehensive analysis of decision-making processes, incorporating utility functions, standard gamble assessments, and various decision criteria such as optimistic, pessimistic, and regret approaches. It delves into expected monetary value (EMV) calculations, including the expected value of perfect information (EVPI), and explores the value of information through conditional probabilities and Bayesian analysis. The report also covers Monte Carlo simulation for profit forecasting and includes a section on regression analysis to determine overhead costs based on machine hours and batch sizes. Furthermore, it examines cost-volume-profit (CVP) analysis to assess break-even points and profit targets under different pricing scenarios. The analysis is supported by calculations, decision trees, and tables to illustrate key concepts and findings.

Contents

Decision Analysis............................................................................................................................2

Q1a...............................................................................................................................................2

Q1b...............................................................................................................................................3

Q1b1.........................................................................................................................................3

Q1b2.........................................................................................................................................3

Q1b3.........................................................................................................................................4

Q1b4.........................................................................................................................................4

Q1b5.........................................................................................................................................5

Q1b6.........................................................................................................................................5

Value of information........................................................................................................................6

Q2a...............................................................................................................................................6

Q2b...............................................................................................................................................7

Q1c...............................................................................................................................................7

Q1d...............................................................................................................................................8

Monte Carlo Simulation................................................................................................................12

Q3a.............................................................................................................................................12

Q3b.............................................................................................................................................12

Q3c.............................................................................................................................................13

New Pricing Strategy - Report...............................................................................................13

Regression Analysis.......................................................................................................................15

Q4a.............................................................................................................................................15

Q4b.............................................................................................................................................15

1 – Overhead cost vs Machine Hours.................................................................................16

3 – Overhead VS Machine hours + Batches.......................................................................17

Q4c.............................................................................................................................................17

Q4d.............................................................................................................................................18

CVP Analysis.................................................................................................................................18

Q5a.............................................................................................................................................18

Q5b.............................................................................................................................................19

Q5c.............................................................................................................................................19

Q5d.............................................................................................................................................19

Decision Analysis............................................................................................................................2

Q1a...............................................................................................................................................2

Q1b...............................................................................................................................................3

Q1b1.........................................................................................................................................3

Q1b2.........................................................................................................................................3

Q1b3.........................................................................................................................................4

Q1b4.........................................................................................................................................4

Q1b5.........................................................................................................................................5

Q1b6.........................................................................................................................................5

Value of information........................................................................................................................6

Q2a...............................................................................................................................................6

Q2b...............................................................................................................................................7

Q1c...............................................................................................................................................7

Q1d...............................................................................................................................................8

Monte Carlo Simulation................................................................................................................12

Q3a.............................................................................................................................................12

Q3b.............................................................................................................................................12

Q3c.............................................................................................................................................13

New Pricing Strategy - Report...............................................................................................13

Regression Analysis.......................................................................................................................15

Q4a.............................................................................................................................................15

Q4b.............................................................................................................................................15

1 – Overhead cost vs Machine Hours.................................................................................16

3 – Overhead VS Machine hours + Batches.......................................................................17

Q4c.............................................................................................................................................17

Q4d.............................................................................................................................................18

CVP Analysis.................................................................................................................................18

Q5a.............................................................................................................................................18

Q5b.............................................................................................................................................19

Q5c.............................................................................................................................................19

Q5d.............................................................................................................................................19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Q5d1...........................................................................................................................................19

Q5d2...........................................................................................................................................19

References:....................................................................................................................................20

Q5d2...........................................................................................................................................19

References:....................................................................................................................................20

Decision Analysis

Q1a

Discuss how a utility function can be assessed. What is a standard gamble and how is it used

in determining utility values?

To assess a given Decision, the monetary value outcome of single decision choices made should

be normalized with the risk involved with the decision. In a decision choice after considering the

risk attached to it, the numeric representation is given by the Utility function.

Assessing utility function scenario consider the Decision as a gamble and alternative 1 with only

2 possible outcome, 0 as utility for worst outcome stat 1 and 1 to best outcome state 2. p & q are

probabilities involved. Then, q = 1-p

Finding utility for any other scenario, we consider Alternative 2 with worst and best outcome.

When we equate Alternative 1 and alternative 2 outcomes, then;

Utility of Alternative1

p(1)+(1−p)(0)=p

Utility of Alternative 2=x

Utility of Alternative 2(x)=Utility of Alternative 1= p

x= p

We can therefore assign utility value of any other outcome using the summary below

Below Decision stump summarizes the Standard gamble.

.

Q1a

Discuss how a utility function can be assessed. What is a standard gamble and how is it used

in determining utility values?

To assess a given Decision, the monetary value outcome of single decision choices made should

be normalized with the risk involved with the decision. In a decision choice after considering the

risk attached to it, the numeric representation is given by the Utility function.

Assessing utility function scenario consider the Decision as a gamble and alternative 1 with only

2 possible outcome, 0 as utility for worst outcome stat 1 and 1 to best outcome state 2. p & q are

probabilities involved. Then, q = 1-p

Finding utility for any other scenario, we consider Alternative 2 with worst and best outcome.

When we equate Alternative 1 and alternative 2 outcomes, then;

Utility of Alternative1

p(1)+(1−p)(0)=p

Utility of Alternative 2=x

Utility of Alternative 2(x)=Utility of Alternative 1= p

x= p

We can therefore assign utility value of any other outcome using the summary below

Below Decision stump summarizes the Standard gamble.

.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Q1b

Below are details of Barnes, Decision outcomes.

Amount of Total Investment = 10000

Investment option1 – share Market

Good return = 14%

Fair return = 8%

Bad return = 0%

Investment option2 – Government bonds

Constant = 9%

Q1b1

The table below shows Decision Matrix of the the above values;

Decision matrix

Investment option

Share market Government bonds

Market

conditions

Good 1400 900

Fair 800 900

Bad 0 900

Q1b2

Which alternative would an optimist choose?

Optimist will go for maximum choice out of the maximum outcome on each of the market state.

Maximax-Optimist choice

Investment option Maximum

Share market Government bonds

Market

conditions

Good 1400 900 1400

Fair 800 900 900

Bad 0 900 900

Under optimistic criterion, the optimist choose, Share market as investment option.

Below are details of Barnes, Decision outcomes.

Amount of Total Investment = 10000

Investment option1 – share Market

Good return = 14%

Fair return = 8%

Bad return = 0%

Investment option2 – Government bonds

Constant = 9%

Q1b1

The table below shows Decision Matrix of the the above values;

Decision matrix

Investment option

Share market Government bonds

Market

conditions

Good 1400 900

Fair 800 900

Bad 0 900

Q1b2

Which alternative would an optimist choose?

Optimist will go for maximum choice out of the maximum outcome on each of the market state.

Maximax-Optimist choice

Investment option Maximum

Share market Government bonds

Market

conditions

Good 1400 900 1400

Fair 800 900 900

Bad 0 900 900

Under optimistic criterion, the optimist choose, Share market as investment option.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Q1b3

Which alternative would a pessimist choose?

Pessimist will go for minimum choice among the minimum outcome in each market state.

Minimini-pessimist choice

Investment option Minimum

Share market Government bonds

Market

conditions

Good 1400 900 900

Fair 800 900 800

Bad 0 900 0

Under Pessimistic criterion, the pessimist will choose, Share market as investment option, with 0

return.

Q1b4

Which alternative is indicated by the criterion of regret?

Regret Criterion is given by the minimax opportunity loss state, where Opportunity loss for a

given state is the different between the state outcome and maximum outcome of a market state.

Example: Opportunity Loss for Government bonds in Good market state is;

1400(maximum of outcome for good market ) – 900( outcome of Govt bonds∈Good market )

¿ 500

Criterion for regret is state where opportunity loss is minimum, which is investment in

government bonds in good market state.

Which alternative would a pessimist choose?

Pessimist will go for minimum choice among the minimum outcome in each market state.

Minimini-pessimist choice

Investment option Minimum

Share market Government bonds

Market

conditions

Good 1400 900 900

Fair 800 900 800

Bad 0 900 0

Under Pessimistic criterion, the pessimist will choose, Share market as investment option, with 0

return.

Q1b4

Which alternative is indicated by the criterion of regret?

Regret Criterion is given by the minimax opportunity loss state, where Opportunity loss for a

given state is the different between the state outcome and maximum outcome of a market state.

Example: Opportunity Loss for Government bonds in Good market state is;

1400(maximum of outcome for good market ) – 900( outcome of Govt bonds∈Good market )

¿ 500

Criterion for regret is state where opportunity loss is minimum, which is investment in

government bonds in good market state.

Investment option Max per state

Share market Government

bonds

State of market Good 1400 900 1400

Fair 800 900 900

Bad 0 900 900

Opportunity loss matrix

Share market Government

bond

Good 0 500

Fair 100 0

Bad 900 0

Maximum

opportunity loss

per option

900 500

Q1b5

Assuming probability of a good market = 0.4, a fair market = 0.4 and a bad market = 0.2, using

Expected monetary values what is the optimum action?

Probability per

market state

Investment option

Share market Government bond

Market

state

Good 0.4 1400 900

Fair 0.4 800 900

Bad 0.2 0 900

EMV =∑ total of Probability of market state∧outcomes attached .

EMV ( share market )=0.4 ×1400+0.4 × 800+0.2 ×0=880

EMV (Government bonds)=0.4 ×900+ 0.4 ×900+ 0.2× 900=900

Hence Optimum action would be investing in Government bonds.

Q1b6

What is the expected value of perfect information?

Expected Value with perfect Information is weighted average of maximum possible state of

available options and probability of occurrence of each state.

Thus;

EVwPI =0.4 × 1400+0.4 × 900+0.2 ×900=1100

Share market Government

bonds

State of market Good 1400 900 1400

Fair 800 900 900

Bad 0 900 900

Opportunity loss matrix

Share market Government

bond

Good 0 500

Fair 100 0

Bad 900 0

Maximum

opportunity loss

per option

900 500

Q1b5

Assuming probability of a good market = 0.4, a fair market = 0.4 and a bad market = 0.2, using

Expected monetary values what is the optimum action?

Probability per

market state

Investment option

Share market Government bond

Market

state

Good 0.4 1400 900

Fair 0.4 800 900

Bad 0.2 0 900

EMV =∑ total of Probability of market state∧outcomes attached .

EMV ( share market )=0.4 ×1400+0.4 × 800+0.2 ×0=880

EMV (Government bonds)=0.4 ×900+ 0.4 ×900+ 0.2× 900=900

Hence Optimum action would be investing in Government bonds.

Q1b6

What is the expected value of perfect information?

Expected Value with perfect Information is weighted average of maximum possible state of

available options and probability of occurrence of each state.

Thus;

EVwPI =0.4 × 1400+0.4 × 900+0.2 ×900=1100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Probability per

market state

Investment option Max in

state of

market

Share market Government

bond

Market state Good 0.4 1400 900 1400

Fair 0.4 800 900 900

Bad 0.2 0 900 900

Expected monetary value 1100

Expected value of Perfect Information is difference between the EVwPI and maximum of EVM

(900)

EVPI=1100 – 900=$ 200

Thus;

Expected value of Perfect Information is $200 for the given market state and investment options.

Value of information

let P(FM) be the Probability for Market is Favorable.

let P(UM) be the Probability for Market is Unfavorable.

let P(FR|FM) be the probability for Research Favorable Given Market is Favorable.

let P(UR|FM) be the probability for Research Unfavorable Given Market is Favorable.

let P(UR|UM) be the probability for Research Unfavorable Given Market is Unfavorable.

let P(FR|UM) be the probability for Research Favorable Given Market is Unfavorable.

let P(FM|FR) be the Probability for Favorable Market given favorable Research

let P(UM|FR) be the Probability for Unfavorable Market given favorable Research

let P(FM|UR) be the Probability for favorable Market given Research Unfavorable.

let P(UM|UR) be the Probability for Unfavorable Market given Research Unfavorable.

let P(FR be the Probability for Favorable research

let P(UR) be the Probability for unfavorable research

For a Razor Factory, If the market were favorable return is of $100,000, but if the market were

unfavorable loss is $60,000. Jim estimates the probability of a favorable market is 0.5

So, P( FM )=0.5∧P(UM )=0.5∧R (FM )=100000∧R (UM )=−$ 60000

market state

Investment option Max in

state of

market

Share market Government

bond

Market state Good 0.4 1400 900 1400

Fair 0.4 800 900 900

Bad 0.2 0 900 900

Expected monetary value 1100

Expected value of Perfect Information is difference between the EVwPI and maximum of EVM

(900)

EVPI=1100 – 900=$ 200

Thus;

Expected value of Perfect Information is $200 for the given market state and investment options.

Value of information

let P(FM) be the Probability for Market is Favorable.

let P(UM) be the Probability for Market is Unfavorable.

let P(FR|FM) be the probability for Research Favorable Given Market is Favorable.

let P(UR|FM) be the probability for Research Unfavorable Given Market is Favorable.

let P(UR|UM) be the probability for Research Unfavorable Given Market is Unfavorable.

let P(FR|UM) be the probability for Research Favorable Given Market is Unfavorable.

let P(FM|FR) be the Probability for Favorable Market given favorable Research

let P(UM|FR) be the Probability for Unfavorable Market given favorable Research

let P(FM|UR) be the Probability for favorable Market given Research Unfavorable.

let P(UM|UR) be the Probability for Unfavorable Market given Research Unfavorable.

let P(FR be the Probability for Favorable research

let P(UR) be the Probability for unfavorable research

For a Razor Factory, If the market were favorable return is of $100,000, but if the market were

unfavorable loss is $60,000. Jim estimates the probability of a favorable market is 0.5

So, P( FM )=0.5∧P(UM )=0.5∧R (FM )=100000∧R (UM )=−$ 60000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Q2a

What should Jerry do? Show calculations

Jerry should calculate Estimated Monetary Value is either of the market conditions for either of

the 2 options, go for production or not go for production.

EMV is best of each condition weighted averaged against probability of occurrence for

condition.

EMV production={ R(FM )× P( FM )+ R( UM )× P (UM )}

EMV production=(0.5 ×100000+0.5 ×(−60000))

EMV production=20000

EMV no production={R(FM )× P( FM )+ R (UM )× P (UM )}

EMV no production=(0.5 × 0+0.5 ×0)

EMV no production=0

Option evaluation is best of EMV of either of 2 options. Which is corresponding to go for

production. Hence Jerry should go for Production.

Q2b

Revise the prior probabilities in light of his friend’s track record.

70% of friend’s past record is the time he would correctly provide a favorable market prediction

and 20% of the time he would incorrectly provide a favorable market prediction.

Prior Probabilities are prior probabilities for Favorable or unfavorable market conditions.

P( FM )=0.5

P(UM )=1 – P ( FM )=0.5

Q1c

What is the posterior probability of a good market given that his friend has provided an

unfavorable market prediction?

Posterior Probabilities, for Favorable Market given Favorable Research be P(FM|FR) and for

Unfavorable Market given Favorable Research be P(UM|FR).

To Calculate the Posterior Probabilities, Conditional Probabilities for P(FR|FM) and P(FR|UM)

is required.

As per friend’s track record.

P( FR∨FM )=0.7

What should Jerry do? Show calculations

Jerry should calculate Estimated Monetary Value is either of the market conditions for either of

the 2 options, go for production or not go for production.

EMV is best of each condition weighted averaged against probability of occurrence for

condition.

EMV production={ R(FM )× P( FM )+ R( UM )× P (UM )}

EMV production=(0.5 ×100000+0.5 ×(−60000))

EMV production=20000

EMV no production={R(FM )× P( FM )+ R (UM )× P (UM )}

EMV no production=(0.5 × 0+0.5 ×0)

EMV no production=0

Option evaluation is best of EMV of either of 2 options. Which is corresponding to go for

production. Hence Jerry should go for Production.

Q2b

Revise the prior probabilities in light of his friend’s track record.

70% of friend’s past record is the time he would correctly provide a favorable market prediction

and 20% of the time he would incorrectly provide a favorable market prediction.

Prior Probabilities are prior probabilities for Favorable or unfavorable market conditions.

P( FM )=0.5

P(UM )=1 – P ( FM )=0.5

Q1c

What is the posterior probability of a good market given that his friend has provided an

unfavorable market prediction?

Posterior Probabilities, for Favorable Market given Favorable Research be P(FM|FR) and for

Unfavorable Market given Favorable Research be P(UM|FR).

To Calculate the Posterior Probabilities, Conditional Probabilities for P(FR|FM) and P(FR|UM)

is required.

As per friend’s track record.

P( FR∨FM )=0.7

P( FR∨UM )=0.2 .

Posterior probability Calculations for Favorable Research

State of

events

Prior Conditiona

l

probability

Joint Posterior

Favorable

market

P(FM)=0.5 P(FR|

FM)=0.7

P(FR ∩FM)= P(FR|FM)×P(FM)=0.35 0.78

Unfavorabl

e market

P(UM)=0.

5

P(FR|

UM)=0.2

P(FR ∩UM)= P(FR|UM)×P(FM)=0.10 0.22

Probability of favorable research

P(FR)=0.45

Joint Probability for Favorable market and Favorable Research P(FR∩FM) is product of P(FR|

FM) and P(FM) as calculated above = 0.35

While, Joint Probability for unfavorable market and Favorable Research P(FR∩UM) is product

of P(FR|UM) and P(UM) as calculated above =0.10

Taking sum of P(FR∩FM) and P(FR∩UM) gives the absolute probability for a favorable

research, which is P(FR) = 0.45.

The Bayes Theorem−P( A∨B)× P (B)=P (B∨ A)× P( A)

Hence ,

P( FM ∨FR)=P( FR∨FM ) × P( FM )/P(FR)=P (FR ∩ FM )/P(FR)=0.35 ÷ 0.45=0.78

P(UM ∨FR)=P(FR∨UM ) × P(UM )/ P( FR)=P(FR ∩ FM )/ P(FR)=0.10 ÷ 0.45=0.22

Q1d

What is the expected net gain or loss from engaging his friend to conduct the market

research? Should his friend be engaged? Why?

Expected Gain or loss for engaging the Friend for research can be calculated using a decision

tree.

Let P1 through P11 represent decision stumps in the Decision tree, while N1 to N9 represent the

outcome leaf nodes.

Let

Posterior probability Calculations for Favorable Research

State of

events

Prior Conditiona

l

probability

Joint Posterior

Favorable

market

P(FM)=0.5 P(FR|

FM)=0.7

P(FR ∩FM)= P(FR|FM)×P(FM)=0.35 0.78

Unfavorabl

e market

P(UM)=0.

5

P(FR|

UM)=0.2

P(FR ∩UM)= P(FR|UM)×P(FM)=0.10 0.22

Probability of favorable research

P(FR)=0.45

Joint Probability for Favorable market and Favorable Research P(FR∩FM) is product of P(FR|

FM) and P(FM) as calculated above = 0.35

While, Joint Probability for unfavorable market and Favorable Research P(FR∩UM) is product

of P(FR|UM) and P(UM) as calculated above =0.10

Taking sum of P(FR∩FM) and P(FR∩UM) gives the absolute probability for a favorable

research, which is P(FR) = 0.45.

The Bayes Theorem−P( A∨B)× P (B)=P (B∨ A)× P( A)

Hence ,

P( FM ∨FR)=P( FR∨FM ) × P( FM )/P(FR)=P (FR ∩ FM )/P(FR)=0.35 ÷ 0.45=0.78

P(UM ∨FR)=P(FR∨UM ) × P(UM )/ P( FR)=P(FR ∩ FM )/ P(FR)=0.10 ÷ 0.45=0.22

Q1d

What is the expected net gain or loss from engaging his friend to conduct the market

research? Should his friend be engaged? Why?

Expected Gain or loss for engaging the Friend for research can be calculated using a decision

tree.

Let P1 through P11 represent decision stumps in the Decision tree, while N1 to N9 represent the

outcome leaf nodes.

Let

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P1 Represents decision node for Research∨do not conduct Research .

P2 Represents decision node for go for Production∨not go for Production .

P3 represents decision node for Research Favorable∨Unfavorable.

P4 represents decision node for Favorable Market ∨Unfavorable Market .

P5 isa dummy decision node for no production .

P6 represents decision node for go for Production∨not go for Production .

P7 represents decision node for go for Production∨not go for Production .

P8 represents decision node for Favorable Market∨Unfavorable Market .

P9 is a dummy decision node for no production .

P10 represents decision node for Favorable Market ∨Unfavorable Market

P11 is a dummy decision node for no production.

Let, N1 N4 and N7 represent the lead node for Favorable market, while N2 N5 and N8 represent

for Unfavorable Market condition, N3 N6 and N9 represent for no production. Monetary value

attached with each of the nodes are as follows.

eaf odesL N Monetary Value

N1 MF $1,00,000.00

N2 MU -$60,000.00

N3 o roducti onN P $0.00

N4 M Research costF - $95,000.00

N5 M Research costU - -$65,000.00

N6 Research cost -$5,000.00

N7 M Research costF - $95,000.00

N8 M Research costU - -$65,000.00

N9 Research cost -$5,000.00

¿ P(FM ∨UR)

¿ P(UR∨FM ) × P(FM )÷ ¿

¿ 0.3 ×0.5 ÷ ¿

¿ 0.3 ÷(0.3+ 0.8)

¿ 0.27

P(UM ∨UR)

¿ 1−P(FM ∨UR )

¿ 1 – 0.27

¿ 0.73

P(FM ∨FR)

P2 Represents decision node for go for Production∨not go for Production .

P3 represents decision node for Research Favorable∨Unfavorable.

P4 represents decision node for Favorable Market ∨Unfavorable Market .

P5 isa dummy decision node for no production .

P6 represents decision node for go for Production∨not go for Production .

P7 represents decision node for go for Production∨not go for Production .

P8 represents decision node for Favorable Market∨Unfavorable Market .

P9 is a dummy decision node for no production .

P10 represents decision node for Favorable Market ∨Unfavorable Market

P11 is a dummy decision node for no production.

Let, N1 N4 and N7 represent the lead node for Favorable market, while N2 N5 and N8 represent

for Unfavorable Market condition, N3 N6 and N9 represent for no production. Monetary value

attached with each of the nodes are as follows.

eaf odesL N Monetary Value

N1 MF $1,00,000.00

N2 MU -$60,000.00

N3 o roducti onN P $0.00

N4 M Research costF - $95,000.00

N5 M Research costU - -$65,000.00

N6 Research cost -$5,000.00

N7 M Research costF - $95,000.00

N8 M Research costU - -$65,000.00

N9 Research cost -$5,000.00

¿ P(FM ∨UR)

¿ P(UR∨FM ) × P(FM )÷ ¿

¿ 0.3 ×0.5 ÷ ¿

¿ 0.3 ÷(0.3+ 0.8)

¿ 0.27

P(UM ∨UR)

¿ 1−P(FM ∨UR )

¿ 1 – 0.27

¿ 0.73

P(FM ∨FR)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

¿ P( FR∨FM )× P(FM )/((P ( FR∨UM )× P(UM ))+( P( FR∨FM )∗P(FM )))

¿( 0.7 ×0.5)÷ (0.7 ×0.5+ 0.2× 0.5)

¿ 0.7 ÷ 0.9

¿ 0.78

P(UM ∨FR)

¿ 1−P(FM ∨FR)

¿ 1 – 0.78

¿ 0.22

P(FR)

As per Bayes theorem for conditional probability explained above , we have−¿

P( FR∨FM )× P (FM )=P(FM ∨FR)× P ( FR)

¿ ¿

¿(0.7 ×0.5)÷ 0.78

¿ 0.45

P(UR )

¿ 1 – P(FR)

Conditional Probability values for different events summarized below are as follows.

robability ValuesP

MP(F ) 0.5

MP(U ) 0.5

R MP(F |F ) 0.7

R MP(U |F ) 0.3

R MP(U |U ) 0.8

R MP(F |U ) 0.2

M RP(F |F ) 0.78

M RP(U |F ) 0.22

M RP(F |U ) 0.27

M RP(U |U ) 0.72

RP(F ) 0.45

RP(U ) 0.55

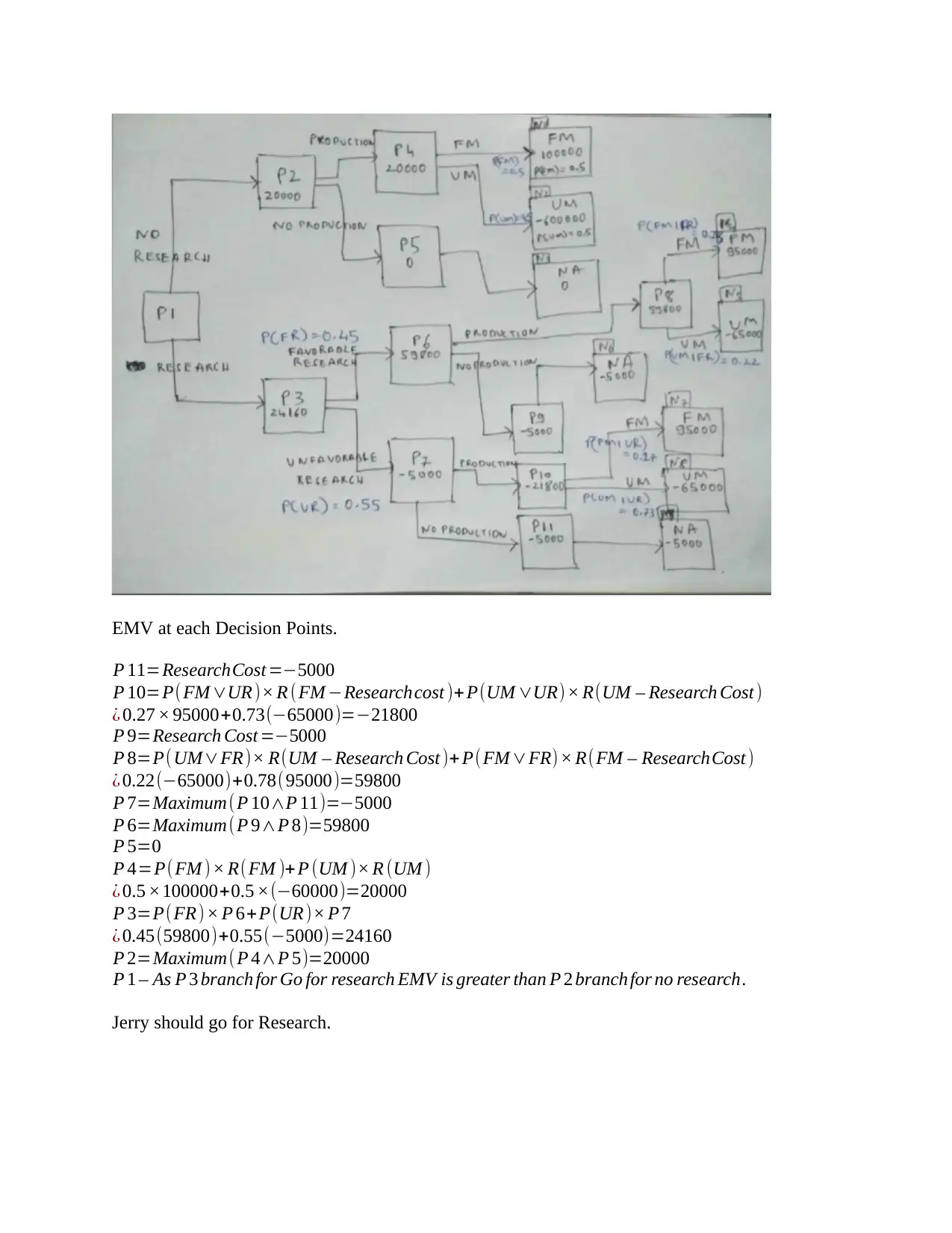

Plotting the above information on a decision tree, as per below diagram.

¿( 0.7 ×0.5)÷ (0.7 ×0.5+ 0.2× 0.5)

¿ 0.7 ÷ 0.9

¿ 0.78

P(UM ∨FR)

¿ 1−P(FM ∨FR)

¿ 1 – 0.78

¿ 0.22

P(FR)

As per Bayes theorem for conditional probability explained above , we have−¿

P( FR∨FM )× P (FM )=P(FM ∨FR)× P ( FR)

¿ ¿

¿(0.7 ×0.5)÷ 0.78

¿ 0.45

P(UR )

¿ 1 – P(FR)

Conditional Probability values for different events summarized below are as follows.

robability ValuesP

MP(F ) 0.5

MP(U ) 0.5

R MP(F |F ) 0.7

R MP(U |F ) 0.3

R MP(U |U ) 0.8

R MP(F |U ) 0.2

M RP(F |F ) 0.78

M RP(U |F ) 0.22

M RP(F |U ) 0.27

M RP(U |U ) 0.72

RP(F ) 0.45

RP(U ) 0.55

Plotting the above information on a decision tree, as per below diagram.

EMV at each Decision Points.

P 11=ResearchCost =−5000

P 10=P( FM ∨UR )× R ( FM −Researchcost )+ P(UM ∨UR)× R(UM – Research Cost )

¿ 0.27 × 95000+0.73(−65000)=−21800

P 9=Research Cost =−5000

P 8=P(UM∨FR)× R(UM – Research Cost )+ P(FM ∨FR)× R(FM – ResearchCost )

¿ 0.22(−65000)+0.78(95000)=59800

P 7=Maximum(P 10∧P 11)=−5000

P 6=Maximum(P 9∧P 8)=59800

P 5=0

P 4=P(FM )× R( FM )+P (UM )× R (UM )

¿ 0.5 ×100000+0.5 ×(−60000)=20000

P 3=P(FR)× P 6+ P(UR )× P 7

¿ 0.45(59800)+0.55(−5000)=24160

P 2=Maximum( P 4∧P 5)=20000

P 1 – As P 3 branch for Go for research EMV is greater than P 2 branch for no research.

Jerry should go for Research.

P 11=ResearchCost =−5000

P 10=P( FM ∨UR )× R ( FM −Researchcost )+ P(UM ∨UR)× R(UM – Research Cost )

¿ 0.27 × 95000+0.73(−65000)=−21800

P 9=Research Cost =−5000

P 8=P(UM∨FR)× R(UM – Research Cost )+ P(FM ∨FR)× R(FM – ResearchCost )

¿ 0.22(−65000)+0.78(95000)=59800

P 7=Maximum(P 10∧P 11)=−5000

P 6=Maximum(P 9∧P 8)=59800

P 5=0

P 4=P(FM )× R( FM )+P (UM )× R (UM )

¿ 0.5 ×100000+0.5 ×(−60000)=20000

P 3=P(FR)× P 6+ P(UR )× P 7

¿ 0.45(59800)+0.55(−5000)=24160

P 2=Maximum( P 4∧P 5)=20000

P 1 – As P 3 branch for Go for research EMV is greater than P 2 branch for no research.

Jerry should go for Research.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.