Business Analytics Report: Business Performance and Strategy Analysis

VerifiedAdded on 2022/11/24

|15

|4271

|386

Report

AI Summary

This business analytics report delves into various techniques crucial for informed business decision-making. It explores mathematical models, correlation analysis, and break-even analysis to assess the relationships between variables and their impact on profitability and growth. The report examines a case study involving a company's financial projections, cost behavior, and the effects of advertising expenditure on sales. It includes calculations for profit/loss, five-year projections, and break-even points. Furthermore, it analyzes the impact of different managerial strategies on the company's financial performance, providing insights into factors influencing business success and the application of marginal costing in business strategy formulation. The report concludes with a critical analysis of the benefits and limitations of these analytical tools, offering valuable insights for strategic decision-making.

MODULE: BUSINESS

ANALYTIC

ANALYTIC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

QUESTION- 1.................................................................................................................................1

a) Mathematical model................................................................................................................1

b) i) Calculation of the profit or loss............................................................................................2

ii) Five year projections...............................................................................................................2

c) Costing and the revenue behaviour..........................................................................................2

QUESTION- 2.................................................................................................................................3

a) Correlation coefficient of the advertising and sales in the company.......................................3

b) Scatter diagram of the data showing the relationship between the two variables...................4

c) Critical analysis of the impact of the advertising expenditure on the sales of the company...4

QUESTION- 3.................................................................................................................................5

a) Calculation of the break-even point and the margin of safety.................................................7

b) Reasons for the adoption of the original plan or amending it as per the Production and the

Marketing manager......................................................................................................................9

c) Other factors that should be considered by the management before committing the any

action for the business..................................................................................................................9

d) Benefits and limitation of the break-even model and its application in the marginal costing

and formulation of the business strategy...................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

QUESTION- 1.................................................................................................................................1

a) Mathematical model................................................................................................................1

b) i) Calculation of the profit or loss............................................................................................2

ii) Five year projections...............................................................................................................2

c) Costing and the revenue behaviour..........................................................................................2

QUESTION- 2.................................................................................................................................3

a) Correlation coefficient of the advertising and sales in the company.......................................3

b) Scatter diagram of the data showing the relationship between the two variables...................4

c) Critical analysis of the impact of the advertising expenditure on the sales of the company...4

QUESTION- 3.................................................................................................................................5

a) Calculation of the break-even point and the margin of safety.................................................7

b) Reasons for the adoption of the original plan or amending it as per the Production and the

Marketing manager......................................................................................................................9

c) Other factors that should be considered by the management before committing the any

action for the business..................................................................................................................9

d) Benefits and limitation of the break-even model and its application in the marginal costing

and formulation of the business strategy...................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

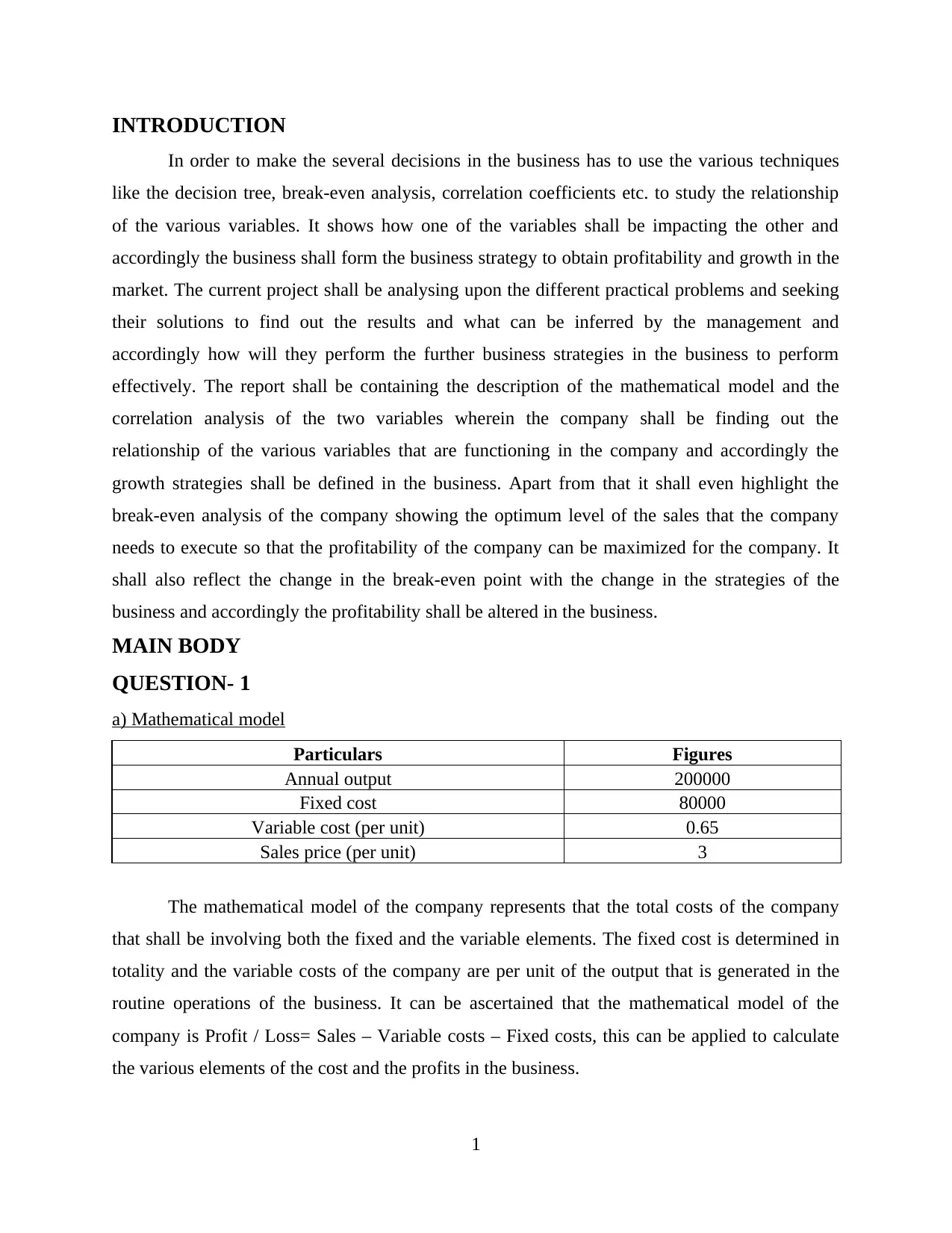

INTRODUCTION

In order to make the several decisions in the business has to use the various techniques

like the decision tree, break-even analysis, correlation coefficients etc. to study the relationship

of the various variables. It shows how one of the variables shall be impacting the other and

accordingly the business shall form the business strategy to obtain profitability and growth in the

market. The current project shall be analysing upon the different practical problems and seeking

their solutions to find out the results and what can be inferred by the management and

accordingly how will they perform the further business strategies in the business to perform

effectively. The report shall be containing the description of the mathematical model and the

correlation analysis of the two variables wherein the company shall be finding out the

relationship of the various variables that are functioning in the company and accordingly the

growth strategies shall be defined in the business. Apart from that it shall even highlight the

break-even analysis of the company showing the optimum level of the sales that the company

needs to execute so that the profitability of the company can be maximized for the company. It

shall also reflect the change in the break-even point with the change in the strategies of the

business and accordingly the profitability shall be altered in the business.

MAIN BODY

QUESTION- 1

a) Mathematical model

Particulars Figures

Annual output 200000

Fixed cost 80000

Variable cost (per unit) 0.65

Sales price (per unit) 3

The mathematical model of the company represents that the total costs of the company

that shall be involving both the fixed and the variable elements. The fixed cost is determined in

totality and the variable costs of the company are per unit of the output that is generated in the

routine operations of the business. It can be ascertained that the mathematical model of the

company is Profit / Loss= Sales – Variable costs – Fixed costs, this can be applied to calculate

the various elements of the cost and the profits in the business.

1

In order to make the several decisions in the business has to use the various techniques

like the decision tree, break-even analysis, correlation coefficients etc. to study the relationship

of the various variables. It shows how one of the variables shall be impacting the other and

accordingly the business shall form the business strategy to obtain profitability and growth in the

market. The current project shall be analysing upon the different practical problems and seeking

their solutions to find out the results and what can be inferred by the management and

accordingly how will they perform the further business strategies in the business to perform

effectively. The report shall be containing the description of the mathematical model and the

correlation analysis of the two variables wherein the company shall be finding out the

relationship of the various variables that are functioning in the company and accordingly the

growth strategies shall be defined in the business. Apart from that it shall even highlight the

break-even analysis of the company showing the optimum level of the sales that the company

needs to execute so that the profitability of the company can be maximized for the company. It

shall also reflect the change in the break-even point with the change in the strategies of the

business and accordingly the profitability shall be altered in the business.

MAIN BODY

QUESTION- 1

a) Mathematical model

Particulars Figures

Annual output 200000

Fixed cost 80000

Variable cost (per unit) 0.65

Sales price (per unit) 3

The mathematical model of the company represents that the total costs of the company

that shall be involving both the fixed and the variable elements. The fixed cost is determined in

totality and the variable costs of the company are per unit of the output that is generated in the

routine operations of the business. It can be ascertained that the mathematical model of the

company is Profit / Loss= Sales – Variable costs – Fixed costs, this can be applied to calculate

the various elements of the cost and the profits in the business.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

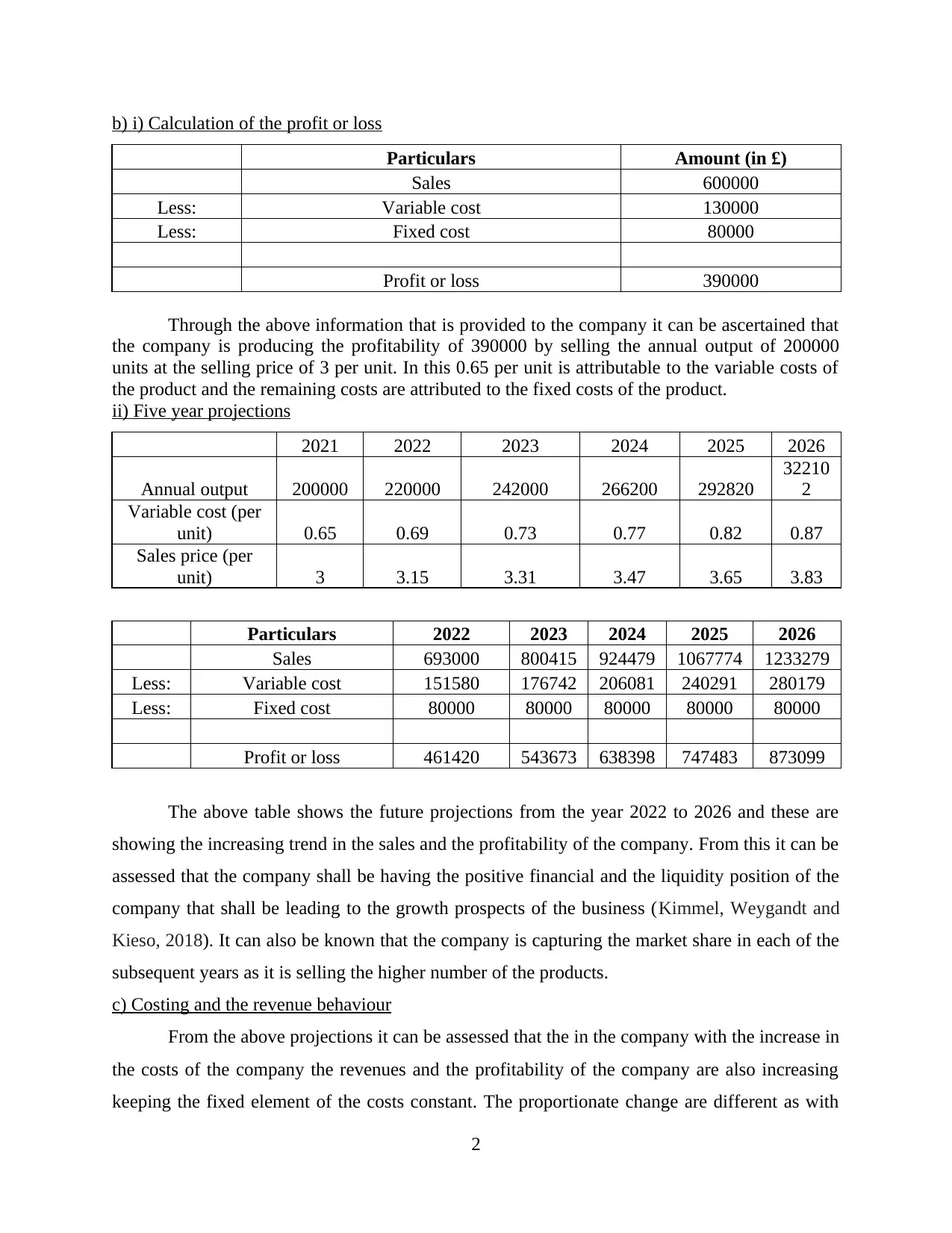

b) i) Calculation of the profit or loss

Particulars Amount (in £)

Sales 600000

Less: Variable cost 130000

Less: Fixed cost 80000

Profit or loss 390000

Through the above information that is provided to the company it can be ascertained that

the company is producing the profitability of 390000 by selling the annual output of 200000

units at the selling price of 3 per unit. In this 0.65 per unit is attributable to the variable costs of

the product and the remaining costs are attributed to the fixed costs of the product.

ii) Five year projections

2021 2022 2023 2024 2025 2026

Annual output 200000 220000 242000 266200 292820

32210

2

Variable cost (per

unit) 0.65 0.69 0.73 0.77 0.82 0.87

Sales price (per

unit) 3 3.15 3.31 3.47 3.65 3.83

Particulars 2022 2023 2024 2025 2026

Sales 693000 800415 924479 1067774 1233279

Less: Variable cost 151580 176742 206081 240291 280179

Less: Fixed cost 80000 80000 80000 80000 80000

Profit or loss 461420 543673 638398 747483 873099

The above table shows the future projections from the year 2022 to 2026 and these are

showing the increasing trend in the sales and the profitability of the company. From this it can be

assessed that the company shall be having the positive financial and the liquidity position of the

company that shall be leading to the growth prospects of the business (Kimmel, Weygandt and

Kieso, 2018). It can also be known that the company is capturing the market share in each of the

subsequent years as it is selling the higher number of the products.

c) Costing and the revenue behaviour

From the above projections it can be assessed that the in the company with the increase in

the costs of the company the revenues and the profitability of the company are also increasing

keeping the fixed element of the costs constant. The proportionate change are different as with

2

Particulars Amount (in £)

Sales 600000

Less: Variable cost 130000

Less: Fixed cost 80000

Profit or loss 390000

Through the above information that is provided to the company it can be ascertained that

the company is producing the profitability of 390000 by selling the annual output of 200000

units at the selling price of 3 per unit. In this 0.65 per unit is attributable to the variable costs of

the product and the remaining costs are attributed to the fixed costs of the product.

ii) Five year projections

2021 2022 2023 2024 2025 2026

Annual output 200000 220000 242000 266200 292820

32210

2

Variable cost (per

unit) 0.65 0.69 0.73 0.77 0.82 0.87

Sales price (per

unit) 3 3.15 3.31 3.47 3.65 3.83

Particulars 2022 2023 2024 2025 2026

Sales 693000 800415 924479 1067774 1233279

Less: Variable cost 151580 176742 206081 240291 280179

Less: Fixed cost 80000 80000 80000 80000 80000

Profit or loss 461420 543673 638398 747483 873099

The above table shows the future projections from the year 2022 to 2026 and these are

showing the increasing trend in the sales and the profitability of the company. From this it can be

assessed that the company shall be having the positive financial and the liquidity position of the

company that shall be leading to the growth prospects of the business (Kimmel, Weygandt and

Kieso, 2018). It can also be known that the company is capturing the market share in each of the

subsequent years as it is selling the higher number of the products.

c) Costing and the revenue behaviour

From the above projections it can be assessed that the in the company with the increase in

the costs of the company the revenues and the profitability of the company are also increasing

keeping the fixed element of the costs constant. The proportionate change are different as with

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the increase of 6% in the variable costs only 5% are increased in the selling price of the

company, which means that the profitability proportion of the business is falling due to the lack

of the efficiency. It can also be observed that the fixed costs of the company are constant for the

long period of time for which the reason is that company is utilizing the lesser capacity in the

organization.

QUESTION- 2

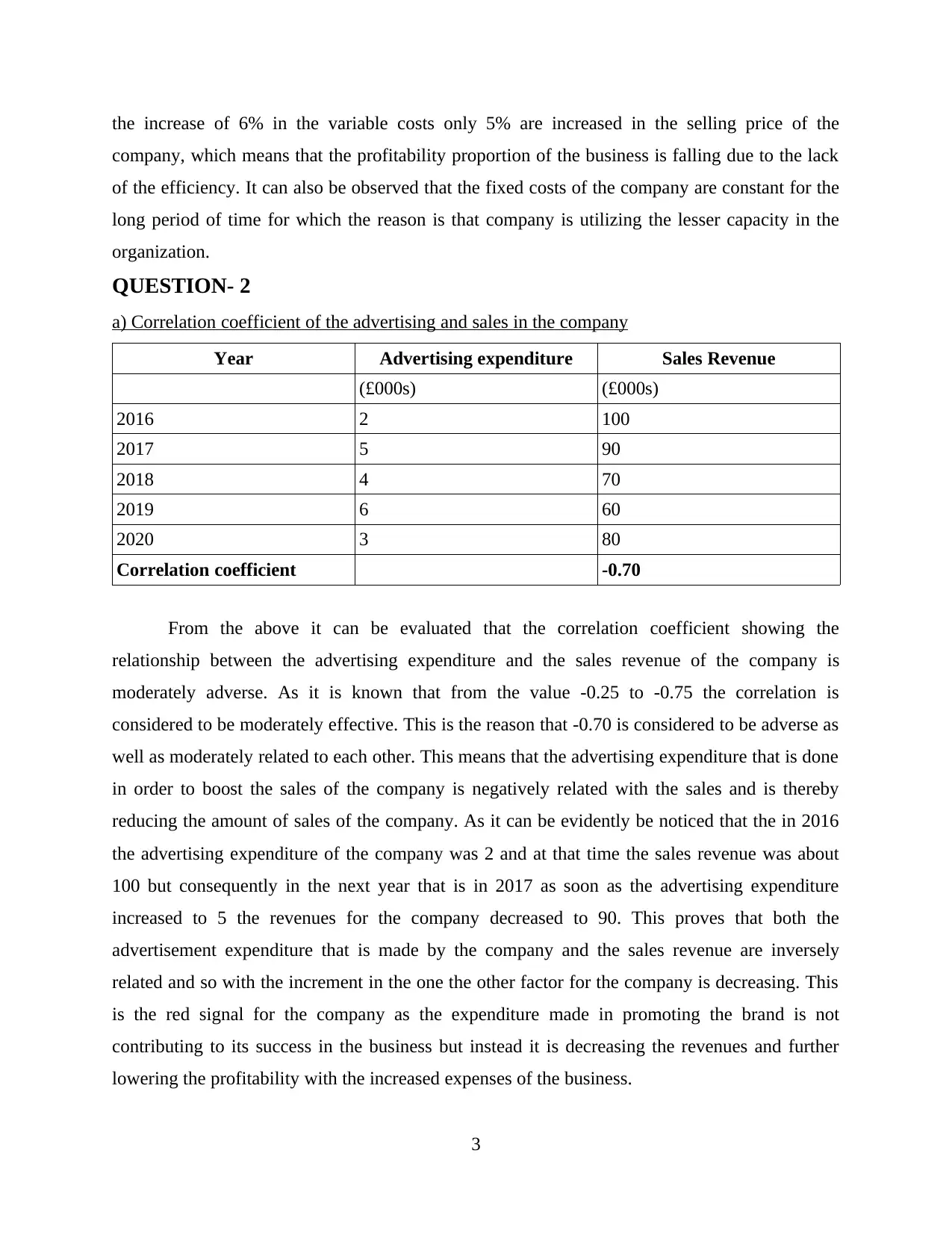

a) Correlation coefficient of the advertising and sales in the company

Year Advertising expenditure Sales Revenue

(£000s) (£000s)

2016 2 100

2017 5 90

2018 4 70

2019 6 60

2020 3 80

Correlation coefficient -0.70

From the above it can be evaluated that the correlation coefficient showing the

relationship between the advertising expenditure and the sales revenue of the company is

moderately adverse. As it is known that from the value -0.25 to -0.75 the correlation is

considered to be moderately effective. This is the reason that -0.70 is considered to be adverse as

well as moderately related to each other. This means that the advertising expenditure that is done

in order to boost the sales of the company is negatively related with the sales and is thereby

reducing the amount of sales of the company. As it can be evidently be noticed that the in 2016

the advertising expenditure of the company was 2 and at that time the sales revenue was about

100 but consequently in the next year that is in 2017 as soon as the advertising expenditure

increased to 5 the revenues for the company decreased to 90. This proves that both the

advertisement expenditure that is made by the company and the sales revenue are inversely

related and so with the increment in the one the other factor for the company is decreasing. This

is the red signal for the company as the expenditure made in promoting the brand is not

contributing to its success in the business but instead it is decreasing the revenues and further

lowering the profitability with the increased expenses of the business.

3

company, which means that the profitability proportion of the business is falling due to the lack

of the efficiency. It can also be observed that the fixed costs of the company are constant for the

long period of time for which the reason is that company is utilizing the lesser capacity in the

organization.

QUESTION- 2

a) Correlation coefficient of the advertising and sales in the company

Year Advertising expenditure Sales Revenue

(£000s) (£000s)

2016 2 100

2017 5 90

2018 4 70

2019 6 60

2020 3 80

Correlation coefficient -0.70

From the above it can be evaluated that the correlation coefficient showing the

relationship between the advertising expenditure and the sales revenue of the company is

moderately adverse. As it is known that from the value -0.25 to -0.75 the correlation is

considered to be moderately effective. This is the reason that -0.70 is considered to be adverse as

well as moderately related to each other. This means that the advertising expenditure that is done

in order to boost the sales of the company is negatively related with the sales and is thereby

reducing the amount of sales of the company. As it can be evidently be noticed that the in 2016

the advertising expenditure of the company was 2 and at that time the sales revenue was about

100 but consequently in the next year that is in 2017 as soon as the advertising expenditure

increased to 5 the revenues for the company decreased to 90. This proves that both the

advertisement expenditure that is made by the company and the sales revenue are inversely

related and so with the increment in the one the other factor for the company is decreasing. This

is the red signal for the company as the expenditure made in promoting the brand is not

contributing to its success in the business but instead it is decreasing the revenues and further

lowering the profitability with the increased expenses of the business.

3

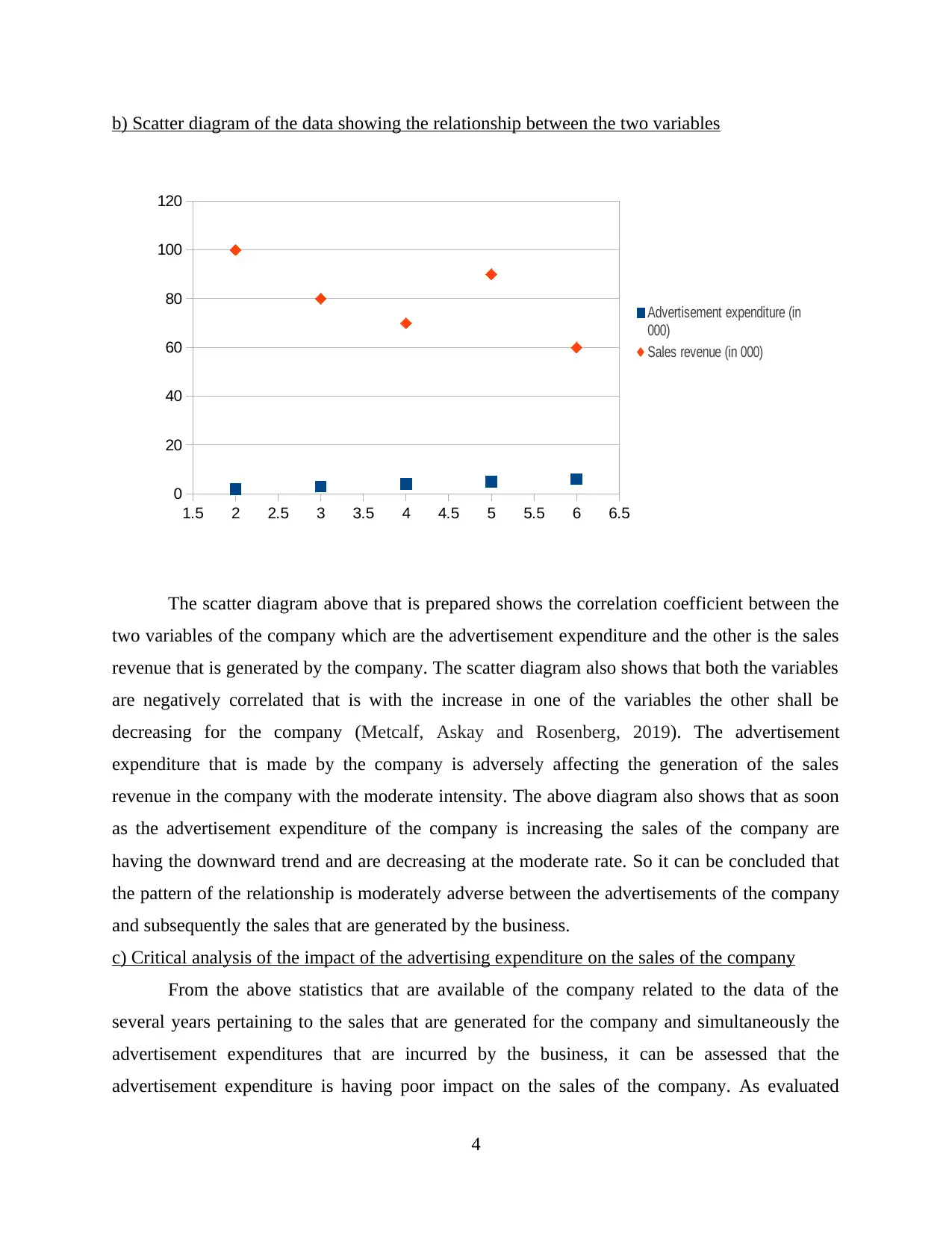

b) Scatter diagram of the data showing the relationship between the two variables

The scatter diagram above that is prepared shows the correlation coefficient between the

two variables of the company which are the advertisement expenditure and the other is the sales

revenue that is generated by the company. The scatter diagram also shows that both the variables

are negatively correlated that is with the increase in one of the variables the other shall be

decreasing for the company (Metcalf, Askay and Rosenberg, 2019). The advertisement

expenditure that is made by the company is adversely affecting the generation of the sales

revenue in the company with the moderate intensity. The above diagram also shows that as soon

as the advertisement expenditure of the company is increasing the sales of the company are

having the downward trend and are decreasing at the moderate rate. So it can be concluded that

the pattern of the relationship is moderately adverse between the advertisements of the company

and subsequently the sales that are generated by the business.

c) Critical analysis of the impact of the advertising expenditure on the sales of the company

From the above statistics that are available of the company related to the data of the

several years pertaining to the sales that are generated for the company and simultaneously the

advertisement expenditures that are incurred by the business, it can be assessed that the

advertisement expenditure is having poor impact on the sales of the company. As evaluated

4

1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 6.5

0

20

40

60

80

100

120

Advertisement expenditure (in

000)

Sales revenue (in 000)

The scatter diagram above that is prepared shows the correlation coefficient between the

two variables of the company which are the advertisement expenditure and the other is the sales

revenue that is generated by the company. The scatter diagram also shows that both the variables

are negatively correlated that is with the increase in one of the variables the other shall be

decreasing for the company (Metcalf, Askay and Rosenberg, 2019). The advertisement

expenditure that is made by the company is adversely affecting the generation of the sales

revenue in the company with the moderate intensity. The above diagram also shows that as soon

as the advertisement expenditure of the company is increasing the sales of the company are

having the downward trend and are decreasing at the moderate rate. So it can be concluded that

the pattern of the relationship is moderately adverse between the advertisements of the company

and subsequently the sales that are generated by the business.

c) Critical analysis of the impact of the advertising expenditure on the sales of the company

From the above statistics that are available of the company related to the data of the

several years pertaining to the sales that are generated for the company and simultaneously the

advertisement expenditures that are incurred by the business, it can be assessed that the

advertisement expenditure is having poor impact on the sales of the company. As evaluated

4

1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 6.5

0

20

40

60

80

100

120

Advertisement expenditure (in

000)

Sales revenue (in 000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

above both the variables are negatively related to one another and this is the reason that every

additional unit that is spend by the company on the advertisement expenditure it can be inferred

that the sales of the company are moderately effected, and they face the decreasing trend in the

company (Boughorbel, Jarray and El-Anbari, 2017). Therefore the marketing manager of the

company should know that the marketing and the promotions of the detergent business are not

being effectively undertaken and that is the reason they are not able to contribute that effectively

as they generally do to boost the sales of the company successfully for the company.

It can be assessed that either the advertisements are being done for the products that are

already outdated, not using the latest technology, does not meet the tastes and preferences of the

customers and also may be using the wrong platforms to promote the products that are not

availing any benefits for the company. These are some reasons that the company might not be

able to benefit from the advertisement expenditures that they make for the sales and revenue

generation of the company.

The marketing manager in the company can gain the competitive advantage and generate

the better revenues and the profitability for the company through applying the right marketing

tactics and not doing any of the wasteful expenditures. Since currently it can be assessed that

digital platforms are being commonly applied for the promotional activities in the various

companies like the search engine optimization, optimized website of the company, internet ads

and the social media applications of the company. These have the wide reach in no real time and

that is the reason that the coverage of the company increases in terms of generating the revenues

for the company. Apart from that it can also be ascertained that may be the company requires

more funds in updating the existing technology or making the investments in the new investment

alternatives instead of the aggressive advertisement (Chicco and Jurman, 2020). So the manager

should build the strategy for the company effectively such that there is no gap in the company

and amount spend by the company contributes to its success and market growth.

So it can be assessed that the marketing manager of the company must review the

existing marketing strategy of making the aggressive advertisements. It should rather focus on

the several other proposals of making the expenditures in the company so that they can further

increase the sales and the efficiency of conducting the operations of the business.

QUESTION- 3

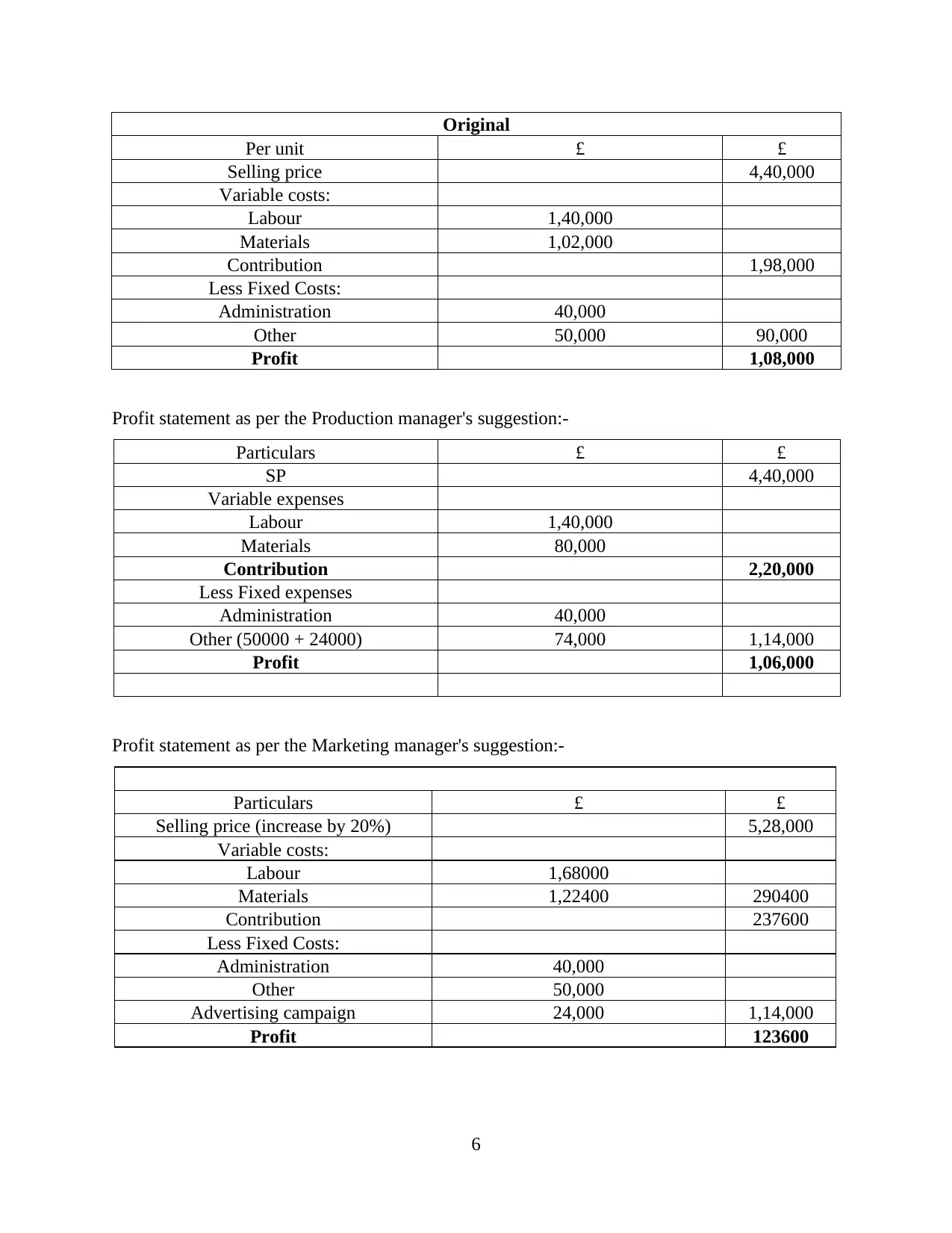

Profit statement as per the original estimates of the company:-

5

additional unit that is spend by the company on the advertisement expenditure it can be inferred

that the sales of the company are moderately effected, and they face the decreasing trend in the

company (Boughorbel, Jarray and El-Anbari, 2017). Therefore the marketing manager of the

company should know that the marketing and the promotions of the detergent business are not

being effectively undertaken and that is the reason they are not able to contribute that effectively

as they generally do to boost the sales of the company successfully for the company.

It can be assessed that either the advertisements are being done for the products that are

already outdated, not using the latest technology, does not meet the tastes and preferences of the

customers and also may be using the wrong platforms to promote the products that are not

availing any benefits for the company. These are some reasons that the company might not be

able to benefit from the advertisement expenditures that they make for the sales and revenue

generation of the company.

The marketing manager in the company can gain the competitive advantage and generate

the better revenues and the profitability for the company through applying the right marketing

tactics and not doing any of the wasteful expenditures. Since currently it can be assessed that

digital platforms are being commonly applied for the promotional activities in the various

companies like the search engine optimization, optimized website of the company, internet ads

and the social media applications of the company. These have the wide reach in no real time and

that is the reason that the coverage of the company increases in terms of generating the revenues

for the company. Apart from that it can also be ascertained that may be the company requires

more funds in updating the existing technology or making the investments in the new investment

alternatives instead of the aggressive advertisement (Chicco and Jurman, 2020). So the manager

should build the strategy for the company effectively such that there is no gap in the company

and amount spend by the company contributes to its success and market growth.

So it can be assessed that the marketing manager of the company must review the

existing marketing strategy of making the aggressive advertisements. It should rather focus on

the several other proposals of making the expenditures in the company so that they can further

increase the sales and the efficiency of conducting the operations of the business.

QUESTION- 3

Profit statement as per the original estimates of the company:-

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Original

Per unit £ £

Selling price 4,40,000

Variable costs:

Labour 1,40,000

Materials 1,02,000

Contribution 1,98,000

Less Fixed Costs:

Administration 40,000

Other 50,000 90,000

Profit 1,08,000

Profit statement as per the Production manager's suggestion:-

Particulars £ £

SP 4,40,000

Variable expenses

Labour 1,40,000

Materials 80,000

Contribution 2,20,000

Less Fixed expenses

Administration 40,000

Other (50000 + 24000) 74,000 1,14,000

Profit 1,06,000

Profit statement as per the Marketing manager's suggestion:-

Particulars £ £

Selling price (increase by 20%) 5,28,000

Variable costs:

Labour 1,68000

Materials 1,22400 290400

Contribution 237600

Less Fixed Costs:

Administration 40,000

Other 50,000

Advertising campaign 24,000 1,14,000

Profit 123600

6

Per unit £ £

Selling price 4,40,000

Variable costs:

Labour 1,40,000

Materials 1,02,000

Contribution 1,98,000

Less Fixed Costs:

Administration 40,000

Other 50,000 90,000

Profit 1,08,000

Profit statement as per the Production manager's suggestion:-

Particulars £ £

SP 4,40,000

Variable expenses

Labour 1,40,000

Materials 80,000

Contribution 2,20,000

Less Fixed expenses

Administration 40,000

Other (50000 + 24000) 74,000 1,14,000

Profit 1,06,000

Profit statement as per the Marketing manager's suggestion:-

Particulars £ £

Selling price (increase by 20%) 5,28,000

Variable costs:

Labour 1,68000

Materials 1,22400 290400

Contribution 237600

Less Fixed Costs:

Administration 40,000

Other 50,000

Advertising campaign 24,000 1,14,000

Profit 123600

6

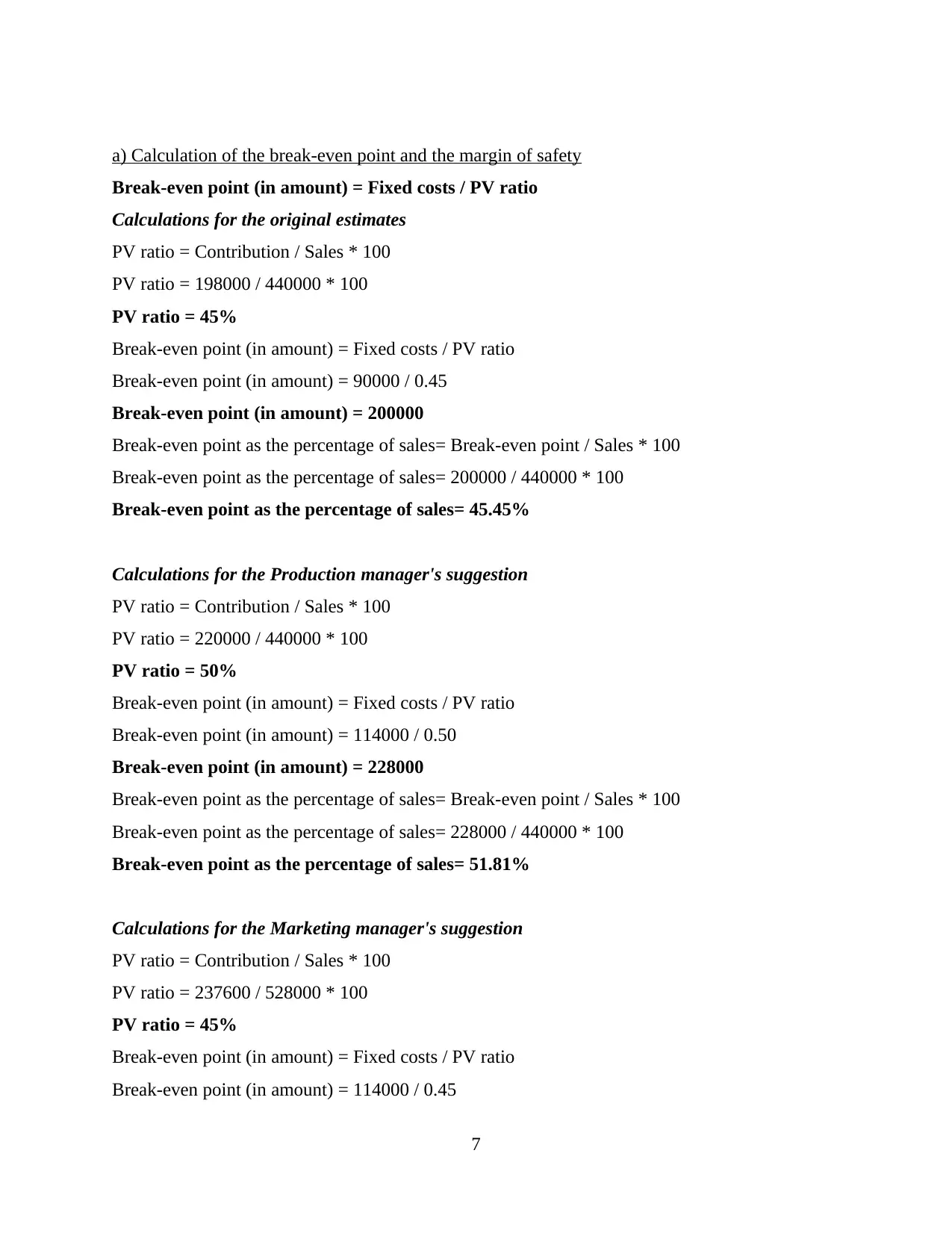

a) Calculation of the break-even point and the margin of safety

Break-even point (in amount) = Fixed costs / PV ratio

Calculations for the original estimates

PV ratio = Contribution / Sales * 100

PV ratio = 198000 / 440000 * 100

PV ratio = 45%

Break-even point (in amount) = Fixed costs / PV ratio

Break-even point (in amount) = 90000 / 0.45

Break-even point (in amount) = 200000

Break-even point as the percentage of sales= Break-even point / Sales * 100

Break-even point as the percentage of sales= 200000 / 440000 * 100

Break-even point as the percentage of sales= 45.45%

Calculations for the Production manager's suggestion

PV ratio = Contribution / Sales * 100

PV ratio = 220000 / 440000 * 100

PV ratio = 50%

Break-even point (in amount) = Fixed costs / PV ratio

Break-even point (in amount) = 114000 / 0.50

Break-even point (in amount) = 228000

Break-even point as the percentage of sales= Break-even point / Sales * 100

Break-even point as the percentage of sales= 228000 / 440000 * 100

Break-even point as the percentage of sales= 51.81%

Calculations for the Marketing manager's suggestion

PV ratio = Contribution / Sales * 100

PV ratio = 237600 / 528000 * 100

PV ratio = 45%

Break-even point (in amount) = Fixed costs / PV ratio

Break-even point (in amount) = 114000 / 0.45

7

Break-even point (in amount) = Fixed costs / PV ratio

Calculations for the original estimates

PV ratio = Contribution / Sales * 100

PV ratio = 198000 / 440000 * 100

PV ratio = 45%

Break-even point (in amount) = Fixed costs / PV ratio

Break-even point (in amount) = 90000 / 0.45

Break-even point (in amount) = 200000

Break-even point as the percentage of sales= Break-even point / Sales * 100

Break-even point as the percentage of sales= 200000 / 440000 * 100

Break-even point as the percentage of sales= 45.45%

Calculations for the Production manager's suggestion

PV ratio = Contribution / Sales * 100

PV ratio = 220000 / 440000 * 100

PV ratio = 50%

Break-even point (in amount) = Fixed costs / PV ratio

Break-even point (in amount) = 114000 / 0.50

Break-even point (in amount) = 228000

Break-even point as the percentage of sales= Break-even point / Sales * 100

Break-even point as the percentage of sales= 228000 / 440000 * 100

Break-even point as the percentage of sales= 51.81%

Calculations for the Marketing manager's suggestion

PV ratio = Contribution / Sales * 100

PV ratio = 237600 / 528000 * 100

PV ratio = 45%

Break-even point (in amount) = Fixed costs / PV ratio

Break-even point (in amount) = 114000 / 0.45

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

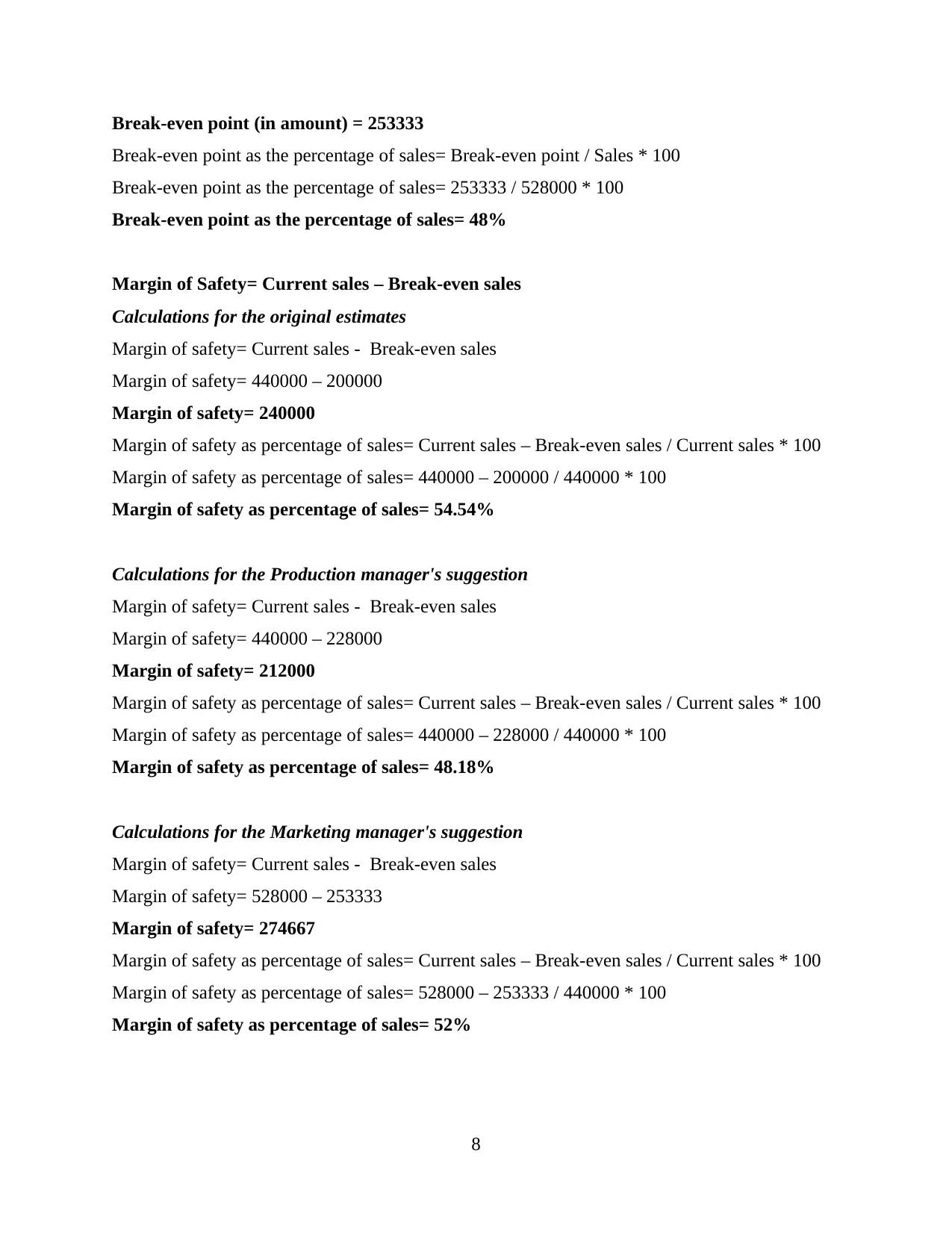

Break-even point (in amount) = 253333

Break-even point as the percentage of sales= Break-even point / Sales * 100

Break-even point as the percentage of sales= 253333 / 528000 * 100

Break-even point as the percentage of sales= 48%

Margin of Safety= Current sales – Break-even sales

Calculations for the original estimates

Margin of safety= Current sales - Break-even sales

Margin of safety= 440000 – 200000

Margin of safety= 240000

Margin of safety as percentage of sales= Current sales – Break-even sales / Current sales * 100

Margin of safety as percentage of sales= 440000 – 200000 / 440000 * 100

Margin of safety as percentage of sales= 54.54%

Calculations for the Production manager's suggestion

Margin of safety= Current sales - Break-even sales

Margin of safety= 440000 – 228000

Margin of safety= 212000

Margin of safety as percentage of sales= Current sales – Break-even sales / Current sales * 100

Margin of safety as percentage of sales= 440000 – 228000 / 440000 * 100

Margin of safety as percentage of sales= 48.18%

Calculations for the Marketing manager's suggestion

Margin of safety= Current sales - Break-even sales

Margin of safety= 528000 – 253333

Margin of safety= 274667

Margin of safety as percentage of sales= Current sales – Break-even sales / Current sales * 100

Margin of safety as percentage of sales= 528000 – 253333 / 440000 * 100

Margin of safety as percentage of sales= 52%

8

Break-even point as the percentage of sales= Break-even point / Sales * 100

Break-even point as the percentage of sales= 253333 / 528000 * 100

Break-even point as the percentage of sales= 48%

Margin of Safety= Current sales – Break-even sales

Calculations for the original estimates

Margin of safety= Current sales - Break-even sales

Margin of safety= 440000 – 200000

Margin of safety= 240000

Margin of safety as percentage of sales= Current sales – Break-even sales / Current sales * 100

Margin of safety as percentage of sales= 440000 – 200000 / 440000 * 100

Margin of safety as percentage of sales= 54.54%

Calculations for the Production manager's suggestion

Margin of safety= Current sales - Break-even sales

Margin of safety= 440000 – 228000

Margin of safety= 212000

Margin of safety as percentage of sales= Current sales – Break-even sales / Current sales * 100

Margin of safety as percentage of sales= 440000 – 228000 / 440000 * 100

Margin of safety as percentage of sales= 48.18%

Calculations for the Marketing manager's suggestion

Margin of safety= Current sales - Break-even sales

Margin of safety= 528000 – 253333

Margin of safety= 274667

Margin of safety as percentage of sales= Current sales – Break-even sales / Current sales * 100

Margin of safety as percentage of sales= 528000 – 253333 / 440000 * 100

Margin of safety as percentage of sales= 52%

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) Reasons for the adoption of the original plan or amending it as per the Production and the

Marketing manager

The plan that is to be executed in the company is the one which is highly profitable for

the company and that shall only be selected for the actual execution despite the various options

that are being presented. It can be assessed that in case of the break-even point as the percentage

of sales in the company the lowest is the most preferred as the quickest is the break-even point

there are higher margin for the profitability. In contrast to this it can be assessed that in the case

of the margin of safety as the percentage of sales the option that is generating the highest margin

of safety is considered to be the best as it shows the percentage till which the company is safe

from the negative returns. As per the above two parameters it can be evaluated that the option

that is satisfied by the above conditions is the original estimates that were affixed at the

beginning. This is because the break-even point is the minimum in this case and also apart from

that the margin of the safety for the option is the highest as compared to the other option that are

specified by the production and the marketing manager of the company.

c) Other factors that should be considered by the management before committing the any action

for the business

The break-even point in the company is one of the parameters that are considered when

the level of operational capacity is decided within the company helping it generate the maximum

profitability for the business. There are other factors also that needs to be considered by the

Mansleeep Plc's management before they commit to any sort of action by executing one of the

above options. Some major factors are:-

Human resource- The first and the foremost is the human resource element that needs to

be considered by the business as for any plan to be executed the required manpower is

necessary in the company (What Other Objectives, Besides Profit, Are Important to

Businesses? 2021). It needs to be ascertained that there are specific skills and talents in

the employees that are being recruited in the company and accordingly only the plans are

being selected by the management.

Technology- Technology is the other element that needs to be considered while

conducting the plan of the company. For the implementation of the particular plan in the

business the required level of the technology must be there in the business.

9

Marketing manager

The plan that is to be executed in the company is the one which is highly profitable for

the company and that shall only be selected for the actual execution despite the various options

that are being presented. It can be assessed that in case of the break-even point as the percentage

of sales in the company the lowest is the most preferred as the quickest is the break-even point

there are higher margin for the profitability. In contrast to this it can be assessed that in the case

of the margin of safety as the percentage of sales the option that is generating the highest margin

of safety is considered to be the best as it shows the percentage till which the company is safe

from the negative returns. As per the above two parameters it can be evaluated that the option

that is satisfied by the above conditions is the original estimates that were affixed at the

beginning. This is because the break-even point is the minimum in this case and also apart from

that the margin of the safety for the option is the highest as compared to the other option that are

specified by the production and the marketing manager of the company.

c) Other factors that should be considered by the management before committing the any action

for the business

The break-even point in the company is one of the parameters that are considered when

the level of operational capacity is decided within the company helping it generate the maximum

profitability for the business. There are other factors also that needs to be considered by the

Mansleeep Plc's management before they commit to any sort of action by executing one of the

above options. Some major factors are:-

Human resource- The first and the foremost is the human resource element that needs to

be considered by the business as for any plan to be executed the required manpower is

necessary in the company (What Other Objectives, Besides Profit, Are Important to

Businesses? 2021). It needs to be ascertained that there are specific skills and talents in

the employees that are being recruited in the company and accordingly only the plans are

being selected by the management.

Technology- Technology is the other element that needs to be considered while

conducting the plan of the company. For the implementation of the particular plan in the

business the required level of the technology must be there in the business.

9

Availability of the funds- This is the most significant concern for the business wherein

the funds needs to be available in the company so that the operations can be executed

smoothly in the company (Lee and et.al., 2018).

Customer satisfaction- Customer satisfaction is the other major goal of the enterprise

and the operations that are being conducted needs to ensure that the customers are

satisfied with it. It shall be providing the value of the money paid by them.

Sustainability of the operations- Whichever option is being selected and accordingly

processed in the entity must also focus on the major motives that is the fulfilment of the

corporate social responsibility through the sustainable development and environmental

protection.

Legal compliance- This is also an important concern of the business that the operations

being conducted does not violate the legal parameters and accordingly does not attract

any interference from the government.

d) Benefits and limitation of the break-even model and its application in the marginal costing and

formulation of the business strategy

Break-even model is applied to know the minimum level of the sales that needs to be

generated in the organization such that there are no profits but the revenues are sufficient to

cover the costs of the organization. It can be understood that this is the least which if not satisfied

then shall hamper the survival of the company. These are some major benefits and limitations

pertaining to the break-even model:-

Benefits of the break-even model

One of the most significant benefit of the break-even model is that it shall be assisting in

controlling the costs of the production (Tanco, Cat and Garat, 2019). As after analysing

the cost and relative profit it shall be evident that what are the optimum costs and

accordingly the measures shall be undertaken for reducing the costs of the company.

It shall also help in forming the make or buy decisions as it shall show the level of

profitability that is being generated. The operations will only be undertaken in the

organization that are generating sufficient profitability.

The production planning in the form of deciding on the optimum future capacity of the

operations in the company can be executed with the help of the break-even chart that is

formed by the company.

10

the funds needs to be available in the company so that the operations can be executed

smoothly in the company (Lee and et.al., 2018).

Customer satisfaction- Customer satisfaction is the other major goal of the enterprise

and the operations that are being conducted needs to ensure that the customers are

satisfied with it. It shall be providing the value of the money paid by them.

Sustainability of the operations- Whichever option is being selected and accordingly

processed in the entity must also focus on the major motives that is the fulfilment of the

corporate social responsibility through the sustainable development and environmental

protection.

Legal compliance- This is also an important concern of the business that the operations

being conducted does not violate the legal parameters and accordingly does not attract

any interference from the government.

d) Benefits and limitation of the break-even model and its application in the marginal costing and

formulation of the business strategy

Break-even model is applied to know the minimum level of the sales that needs to be

generated in the organization such that there are no profits but the revenues are sufficient to

cover the costs of the organization. It can be understood that this is the least which if not satisfied

then shall hamper the survival of the company. These are some major benefits and limitations

pertaining to the break-even model:-

Benefits of the break-even model

One of the most significant benefit of the break-even model is that it shall be assisting in

controlling the costs of the production (Tanco, Cat and Garat, 2019). As after analysing

the cost and relative profit it shall be evident that what are the optimum costs and

accordingly the measures shall be undertaken for reducing the costs of the company.

It shall also help in forming the make or buy decisions as it shall show the level of

profitability that is being generated. The operations will only be undertaken in the

organization that are generating sufficient profitability.

The production planning in the form of deciding on the optimum future capacity of the

operations in the company can be executed with the help of the break-even chart that is

formed by the company.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.