Business Report: Analyzing The Dingleys' Children's Care Home Finances

VerifiedAdded on 2023/01/11

|13

|2677

|50

Report

AI Summary

This report provides a detailed financial analysis of a children's care home, examining key aspects such as profit and break-even points, fixed and variable costs, and sensitivity analysis to determine its impact on the business. It includes a comparative analysis of laundry options, offering insights into cost-effective choices. Furthermore, the report evaluates different accommodation options, comparing their potential profitability. The sensitivity analysis explores how changes in key variables, such as the number of children enrolled, affect the care home's break-even point and overall profitability. The report aims to guide financial decision-making for the care home's owners, the Dingleys, by providing data-driven recommendations based on the case study.

The Dingleys’

children’s care home

children’s care home

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1 Profit and Break-even analysis..........................................................................................4

I. Calculate the estimated annual profit and break-even point for the business, using the

number of care days that need to be sold.....................................................................................4

II. The running costs of the Care Home classified as fixed and variable....................................6

Task 2 – Laundry cost comparison and analysis.............................................................................8

I. Comparative analysis for each of the three laundry options....................................................8

Task 3 – Accommodation options...................................................................................................9

I. Advice the Dingleys on their space options.............................................................................9

Task 4 – Sensitivity analysis..........................................................................................................10

I. Sensitivity analysis to show how this could impact upon care homes break-even point and its

profitability................................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1 Profit and Break-even analysis..........................................................................................4

I. Calculate the estimated annual profit and break-even point for the business, using the

number of care days that need to be sold.....................................................................................4

II. The running costs of the Care Home classified as fixed and variable....................................6

Task 2 – Laundry cost comparison and analysis.............................................................................8

I. Comparative analysis for each of the three laundry options....................................................8

Task 3 – Accommodation options...................................................................................................9

I. Advice the Dingleys on their space options.............................................................................9

Task 4 – Sensitivity analysis..........................................................................................................10

I. Sensitivity analysis to show how this could impact upon care homes break-even point and its

profitability................................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Business accounting is systematic evidence gathering, review, evaluation and delivery.

Accounting may be carried out by one person in a small company or by multiple teams of big

businesses. Accounting is the way a corporation tracks its operations. Accounting is the

recording method for company-related financial transactions. In the accounting process, the

expenditure is called, evaluated and disclosed to supervisory authorities, regulators and tax

collectors. Basically, accounting is necessary for business entities in order to take corrective

actions such as making financial decisions and many more. The reports used are a short summary

of financial activities over an accounting cycle, which describes the functions, financial

condition, and cash flows of a business. The project report is based on a case study which is

related to running a children care home. The report covers detailed information about calculation

of profit, break even analysis, sensitivity analysis and many more.

Business accounting is systematic evidence gathering, review, evaluation and delivery.

Accounting may be carried out by one person in a small company or by multiple teams of big

businesses. Accounting is the way a corporation tracks its operations. Accounting is the

recording method for company-related financial transactions. In the accounting process, the

expenditure is called, evaluated and disclosed to supervisory authorities, regulators and tax

collectors. Basically, accounting is necessary for business entities in order to take corrective

actions such as making financial decisions and many more. The reports used are a short summary

of financial activities over an accounting cycle, which describes the functions, financial

condition, and cash flows of a business. The project report is based on a case study which is

related to running a children care home. The report covers detailed information about calculation

of profit, break even analysis, sensitivity analysis and many more.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1 Profit and Break-even analysis

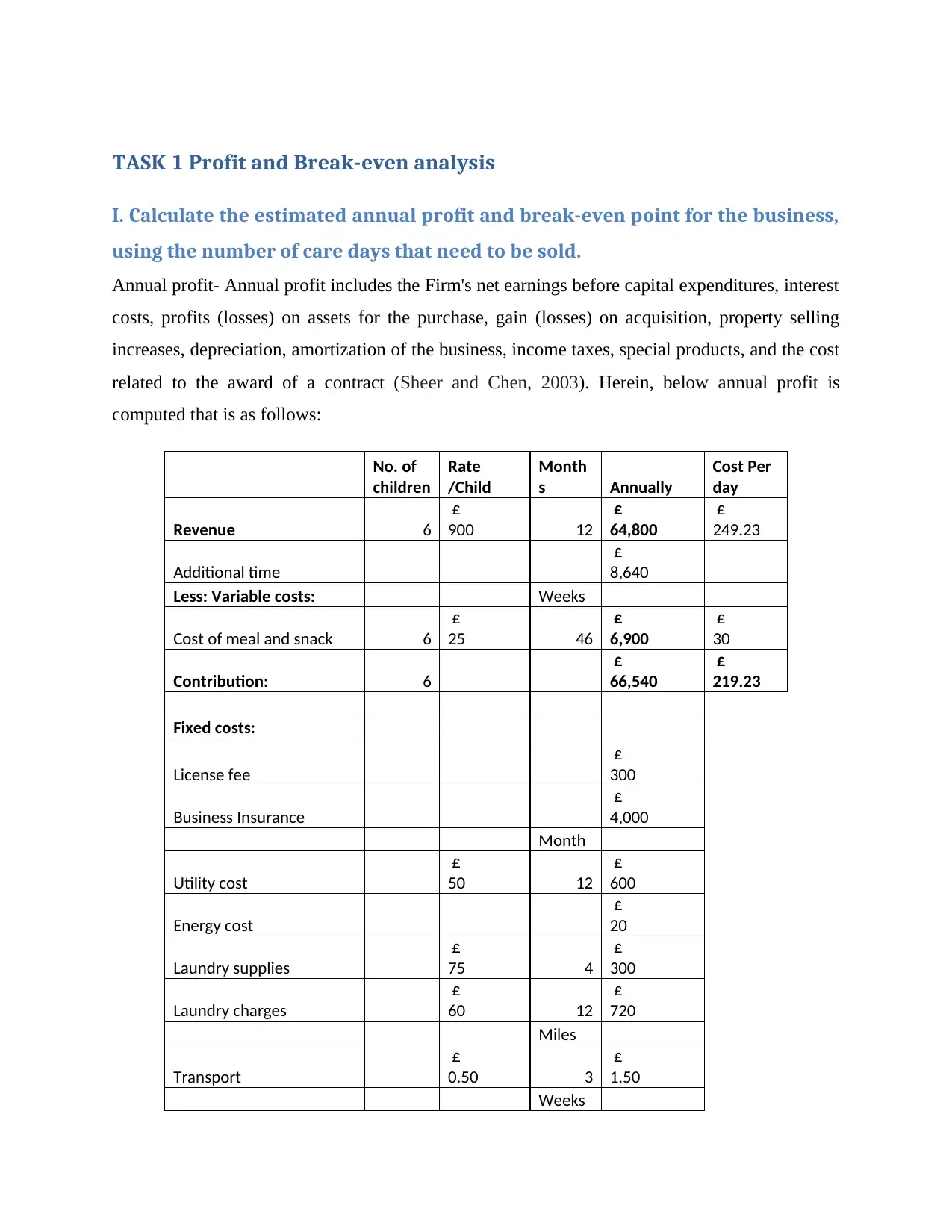

I. Calculate the estimated annual profit and break-even point for the business,

using the number of care days that need to be sold.

Annual profit- Annual profit includes the Firm's net earnings before capital expenditures, interest

costs, profits (losses) on assets for the purchase, gain (losses) on acquisition, property selling

increases, depreciation, amortization of the business, income taxes, special products, and the cost

related to the award of a contract (Sheer and Chen, 2003). Herein, below annual profit is

computed that is as follows:

No. of

children

Rate

/Child

Month

s Annually

Cost Per

day

Revenue 6

£

900 12

£

64,800

£

249.23

Additional time

£

8,640

Less: Variable costs: Weeks

Cost of meal and snack 6

£

25 46

£

6,900

£

30

Contribution: 6

£

66,540

£

219.23

Fixed costs:

License fee

£

300

Business Insurance

£

4,000

Month

Utility cost

£

50 12

£

600

Energy cost

£

20

Laundry supplies

£

75 4

£

300

Laundry charges

£

60 12

£

720

Miles

Transport

£

0.50 3

£

1.50

Weeks

I. Calculate the estimated annual profit and break-even point for the business,

using the number of care days that need to be sold.

Annual profit- Annual profit includes the Firm's net earnings before capital expenditures, interest

costs, profits (losses) on assets for the purchase, gain (losses) on acquisition, property selling

increases, depreciation, amortization of the business, income taxes, special products, and the cost

related to the award of a contract (Sheer and Chen, 2003). Herein, below annual profit is

computed that is as follows:

No. of

children

Rate

/Child

Month

s Annually

Cost Per

day

Revenue 6

£

900 12

£

64,800

£

249.23

Additional time

£

8,640

Less: Variable costs: Weeks

Cost of meal and snack 6

£

25 46

£

6,900

£

30

Contribution: 6

£

66,540

£

219.23

Fixed costs:

License fee

£

300

Business Insurance

£

4,000

Month

Utility cost

£

50 12

£

600

Energy cost

£

20

Laundry supplies

£

75 4

£

300

Laundry charges

£

60 12

£

720

Miles

Transport

£

0.50 3

£

1.50

Weeks

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

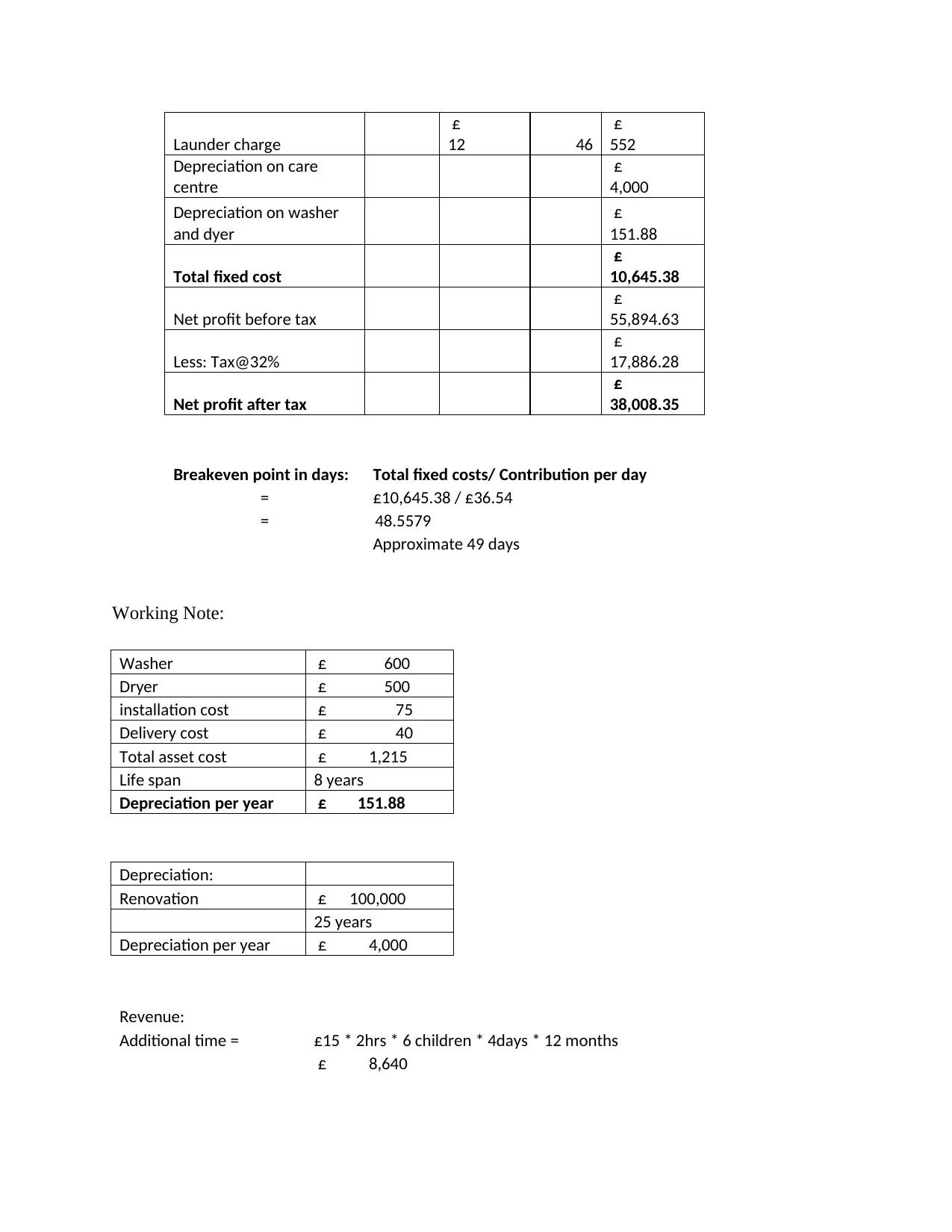

Launder charge

£

12 46

£

552

Depreciation on care

centre

£

4,000

Depreciation on washer

and dyer

£

151.88

Total fixed cost

£

10,645.38

Net profit before tax

£

55,894.63

Less: Tax@32%

£

17,886.28

Net profit after tax

£

38,008.35

Breakeven point in days: Total fixed costs/ Contribution per day

= £10,645.38 / £36.54

= 48.5579

Approximate 49 days

Working Note:

Washer £ 600

Dryer £ 500

installation cost £ 75

Delivery cost £ 40

Total asset cost £ 1,215

Life span 8 years

Depreciation per year £ 151.88

Depreciation:

Renovation £ 100,000

25 years

Depreciation per year £ 4,000

Revenue:

Additional time = £15 * 2hrs * 6 children * 4days * 12 months

£ 8,640

£

12 46

£

552

Depreciation on care

centre

£

4,000

Depreciation on washer

and dyer

£

151.88

Total fixed cost

£

10,645.38

Net profit before tax

£

55,894.63

Less: Tax@32%

£

17,886.28

Net profit after tax

£

38,008.35

Breakeven point in days: Total fixed costs/ Contribution per day

= £10,645.38 / £36.54

= 48.5579

Approximate 49 days

Working Note:

Washer £ 600

Dryer £ 500

installation cost £ 75

Delivery cost £ 40

Total asset cost £ 1,215

Life span 8 years

Depreciation per year £ 151.88

Depreciation:

Renovation £ 100,000

25 years

Depreciation per year £ 4,000

Revenue:

Additional time = £15 * 2hrs * 6 children * 4days * 12 months

£ 8,640

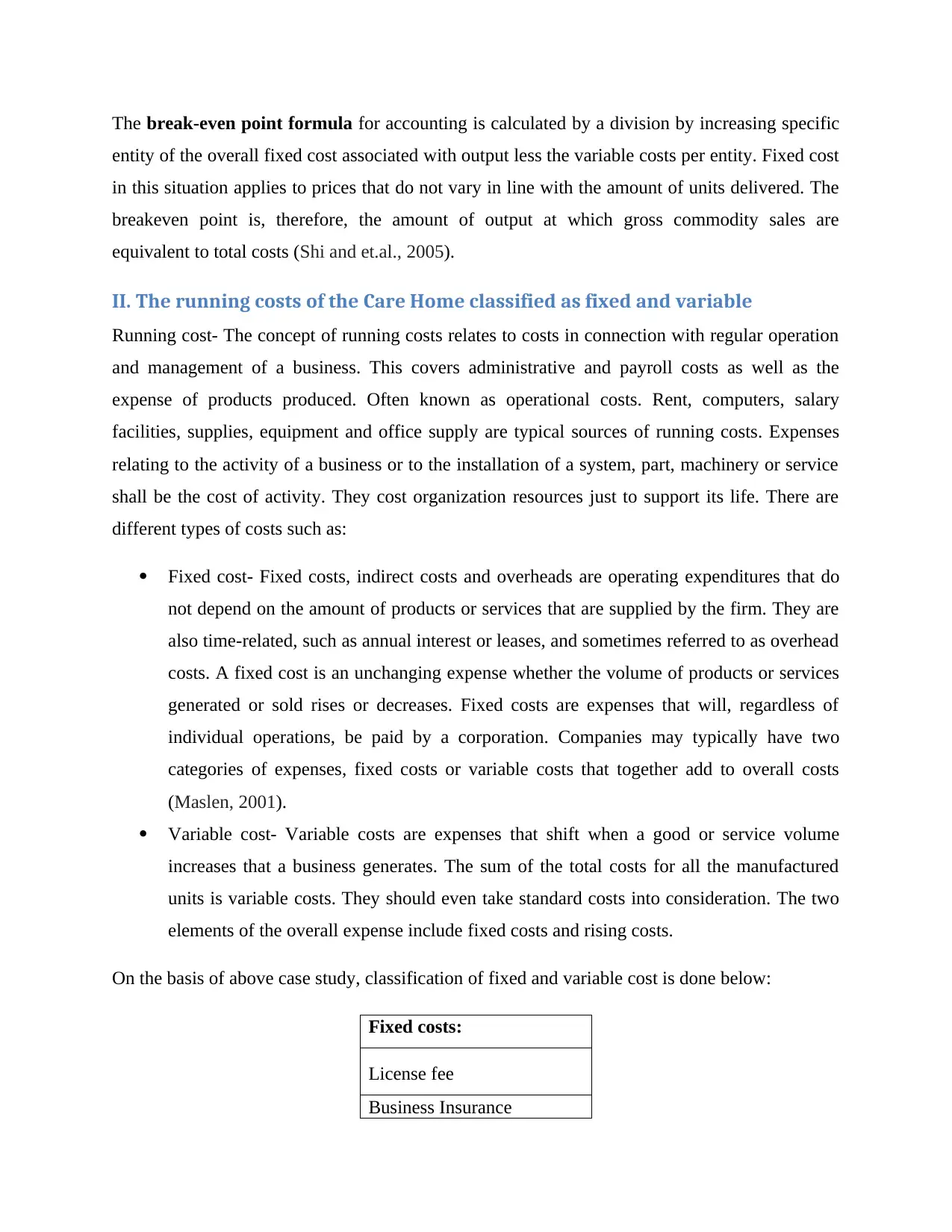

The break-even point formula for accounting is calculated by a division by increasing specific

entity of the overall fixed cost associated with output less the variable costs per entity. Fixed cost

in this situation applies to prices that do not vary in line with the amount of units delivered. The

breakeven point is, therefore, the amount of output at which gross commodity sales are

equivalent to total costs (Shi and et.al., 2005).

II. The running costs of the Care Home classified as fixed and variable

Running cost- The concept of running costs relates to costs in connection with regular operation

and management of a business. This covers administrative and payroll costs as well as the

expense of products produced. Often known as operational costs. Rent, computers, salary

facilities, supplies, equipment and office supply are typical sources of running costs. Expenses

relating to the activity of a business or to the installation of a system, part, machinery or service

shall be the cost of activity. They cost organization resources just to support its life. There are

different types of costs such as:

Fixed cost- Fixed costs, indirect costs and overheads are operating expenditures that do

not depend on the amount of products or services that are supplied by the firm. They are

also time-related, such as annual interest or leases, and sometimes referred to as overhead

costs. A fixed cost is an unchanging expense whether the volume of products or services

generated or sold rises or decreases. Fixed costs are expenses that will, regardless of

individual operations, be paid by a corporation. Companies may typically have two

categories of expenses, fixed costs or variable costs that together add to overall costs

(Maslen, 2001).

Variable cost- Variable costs are expenses that shift when a good or service volume

increases that a business generates. The sum of the total costs for all the manufactured

units is variable costs. They should even take standard costs into consideration. The two

elements of the overall expense include fixed costs and rising costs.

On the basis of above case study, classification of fixed and variable cost is done below:

Fixed costs:

License fee

Business Insurance

entity of the overall fixed cost associated with output less the variable costs per entity. Fixed cost

in this situation applies to prices that do not vary in line with the amount of units delivered. The

breakeven point is, therefore, the amount of output at which gross commodity sales are

equivalent to total costs (Shi and et.al., 2005).

II. The running costs of the Care Home classified as fixed and variable

Running cost- The concept of running costs relates to costs in connection with regular operation

and management of a business. This covers administrative and payroll costs as well as the

expense of products produced. Often known as operational costs. Rent, computers, salary

facilities, supplies, equipment and office supply are typical sources of running costs. Expenses

relating to the activity of a business or to the installation of a system, part, machinery or service

shall be the cost of activity. They cost organization resources just to support its life. There are

different types of costs such as:

Fixed cost- Fixed costs, indirect costs and overheads are operating expenditures that do

not depend on the amount of products or services that are supplied by the firm. They are

also time-related, such as annual interest or leases, and sometimes referred to as overhead

costs. A fixed cost is an unchanging expense whether the volume of products or services

generated or sold rises or decreases. Fixed costs are expenses that will, regardless of

individual operations, be paid by a corporation. Companies may typically have two

categories of expenses, fixed costs or variable costs that together add to overall costs

(Maslen, 2001).

Variable cost- Variable costs are expenses that shift when a good or service volume

increases that a business generates. The sum of the total costs for all the manufactured

units is variable costs. They should even take standard costs into consideration. The two

elements of the overall expense include fixed costs and rising costs.

On the basis of above case study, classification of fixed and variable cost is done below:

Fixed costs:

License fee

Business Insurance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

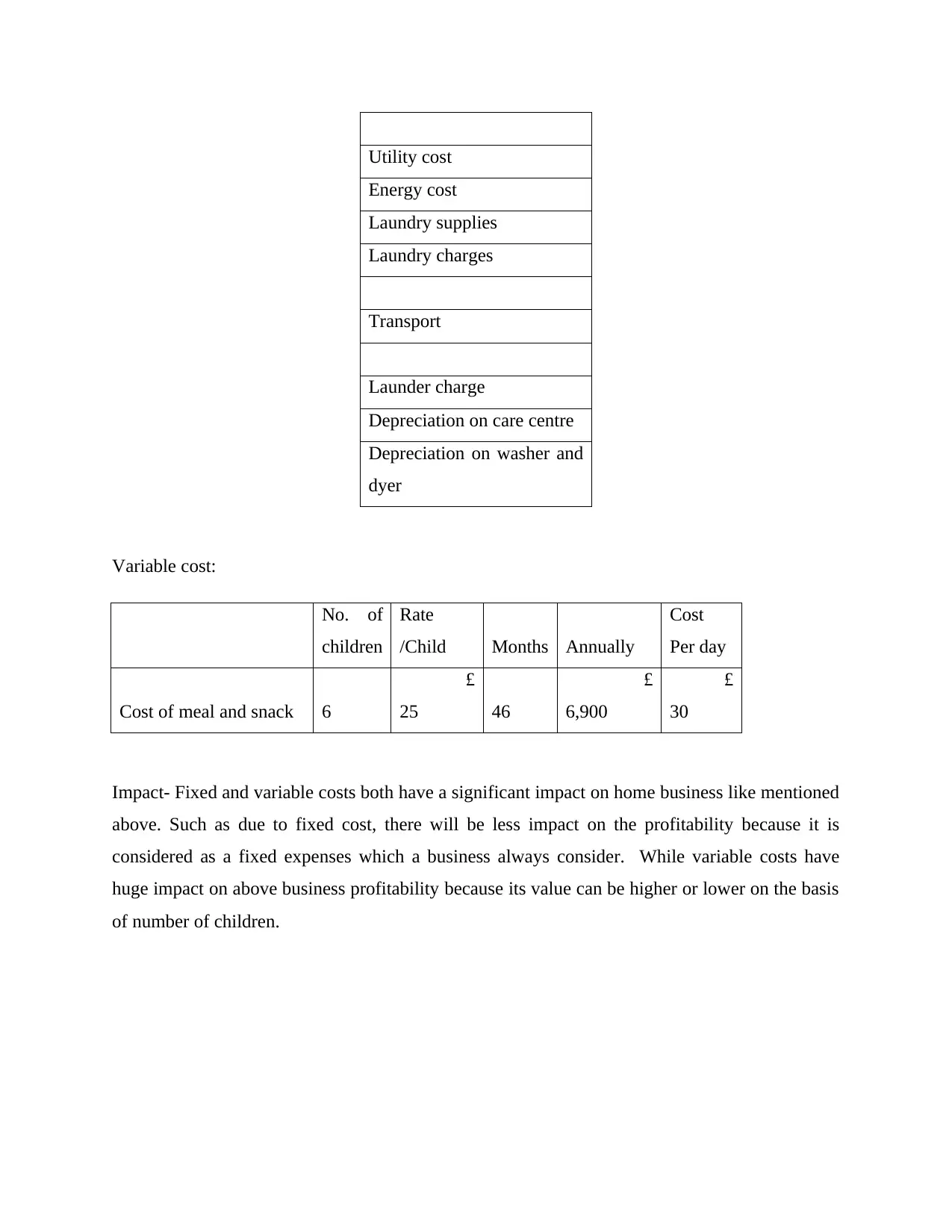

Utility cost

Energy cost

Laundry supplies

Laundry charges

Transport

Launder charge

Depreciation on care centre

Depreciation on washer and

dyer

Variable cost:

No. of

children

Rate

/Child Months Annually

Cost

Per day

Cost of meal and snack 6

£

25 46

£

6,900

£

30

Impact- Fixed and variable costs both have a significant impact on home business like mentioned

above. Such as due to fixed cost, there will be less impact on the profitability because it is

considered as a fixed expenses which a business always consider. While variable costs have

huge impact on above business profitability because its value can be higher or lower on the basis

of number of children.

Energy cost

Laundry supplies

Laundry charges

Transport

Launder charge

Depreciation on care centre

Depreciation on washer and

dyer

Variable cost:

No. of

children

Rate

/Child Months Annually

Cost

Per day

Cost of meal and snack 6

£

25 46

£

6,900

£

30

Impact- Fixed and variable costs both have a significant impact on home business like mentioned

above. Such as due to fixed cost, there will be less impact on the profitability because it is

considered as a fixed expenses which a business always consider. While variable costs have

huge impact on above business profitability because its value can be higher or lower on the basis

of number of children.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

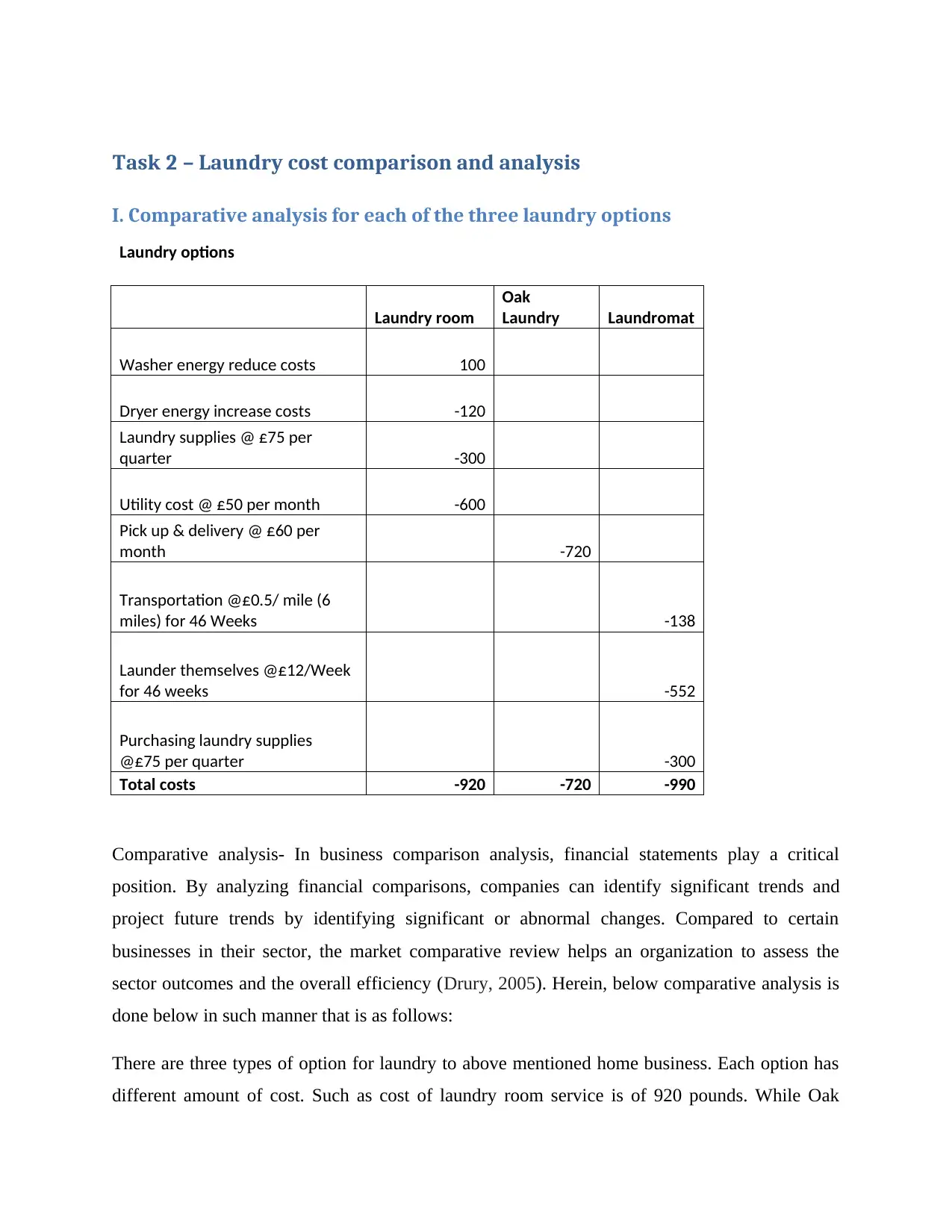

Task 2 – Laundry cost comparison and analysis

I. Comparative analysis for each of the three laundry options

Laundry options

Laundry room

Oak

Laundry Laundromat

Washer energy reduce costs 100

Dryer energy increase costs -120

Laundry supplies @ £75 per

quarter -300

Utility cost @ £50 per month -600

Pick up & delivery @ £60 per

month -720

Transportation @£0.5/ mile (6

miles) for 46 Weeks -138

Launder themselves @£12/Week

for 46 weeks -552

Purchasing laundry supplies

@£75 per quarter -300

Total costs -920 -720 -990

Comparative analysis- In business comparison analysis, financial statements play a critical

position. By analyzing financial comparisons, companies can identify significant trends and

project future trends by identifying significant or abnormal changes. Compared to certain

businesses in their sector, the market comparative review helps an organization to assess the

sector outcomes and the overall efficiency (Drury, 2005). Herein, below comparative analysis is

done below in such manner that is as follows:

There are three types of option for laundry to above mentioned home business. Each option has

different amount of cost. Such as cost of laundry room service is of 920 pounds. While Oak

I. Comparative analysis for each of the three laundry options

Laundry options

Laundry room

Oak

Laundry Laundromat

Washer energy reduce costs 100

Dryer energy increase costs -120

Laundry supplies @ £75 per

quarter -300

Utility cost @ £50 per month -600

Pick up & delivery @ £60 per

month -720

Transportation @£0.5/ mile (6

miles) for 46 Weeks -138

Launder themselves @£12/Week

for 46 weeks -552

Purchasing laundry supplies

@£75 per quarter -300

Total costs -920 -720 -990

Comparative analysis- In business comparison analysis, financial statements play a critical

position. By analyzing financial comparisons, companies can identify significant trends and

project future trends by identifying significant or abnormal changes. Compared to certain

businesses in their sector, the market comparative review helps an organization to assess the

sector outcomes and the overall efficiency (Drury, 2005). Herein, below comparative analysis is

done below in such manner that is as follows:

There are three types of option for laundry to above mentioned home business. Each option has

different amount of cost. Such as cost of laundry room service is of 920 pounds. While Oak

laundry’s cost is of 720 pounds. And the third option has cost of 990 pounds. This is indicating

that above business should focus on that option that is less expensive. So above business needs to

go with Oak laundry. If they will do so than it will be beneficial for them to gain higher benefit

with less cost. On the other hands, if they will focus to make invest on rest of other two laundry

option, then it will be risky for them to cover cost of different options. This is so because due to

higher cost of laundry, each child needs to pay more on laundry option which will lead to

negative option.

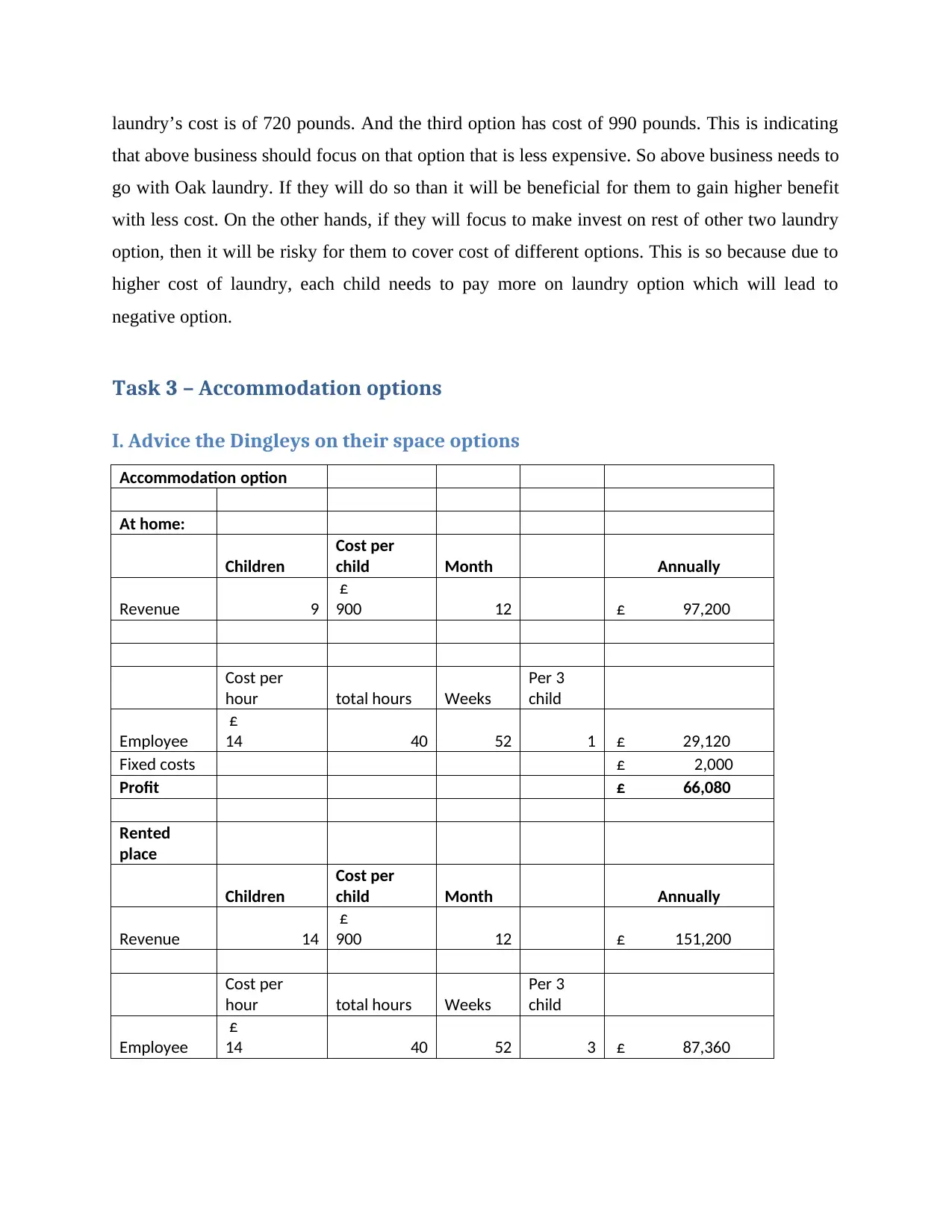

Task 3 – Accommodation options

I. Advice the Dingleys on their space options

Accommodation option

At home:

Children

Cost per

child Month Annually

Revenue 9

£

900 12 £ 97,200

Cost per

hour total hours Weeks

Per 3

child

Employee

£

14 40 52 1 £ 29,120

Fixed costs £ 2,000

Profit £ 66,080

Rented

place

Children

Cost per

child Month Annually

Revenue 14

£

900 12 £ 151,200

Cost per

hour total hours Weeks

Per 3

child

Employee

£

14 40 52 3 £ 87,360

that above business should focus on that option that is less expensive. So above business needs to

go with Oak laundry. If they will do so than it will be beneficial for them to gain higher benefit

with less cost. On the other hands, if they will focus to make invest on rest of other two laundry

option, then it will be risky for them to cover cost of different options. This is so because due to

higher cost of laundry, each child needs to pay more on laundry option which will lead to

negative option.

Task 3 – Accommodation options

I. Advice the Dingleys on their space options

Accommodation option

At home:

Children

Cost per

child Month Annually

Revenue 9

£

900 12 £ 97,200

Cost per

hour total hours Weeks

Per 3

child

Employee

£

14 40 52 1 £ 29,120

Fixed costs £ 2,000

Profit £ 66,080

Rented

place

Children

Cost per

child Month Annually

Revenue 14

£

900 12 £ 151,200

Cost per

hour total hours Weeks

Per 3

child

Employee

£

14 40 52 3 £ 87,360

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

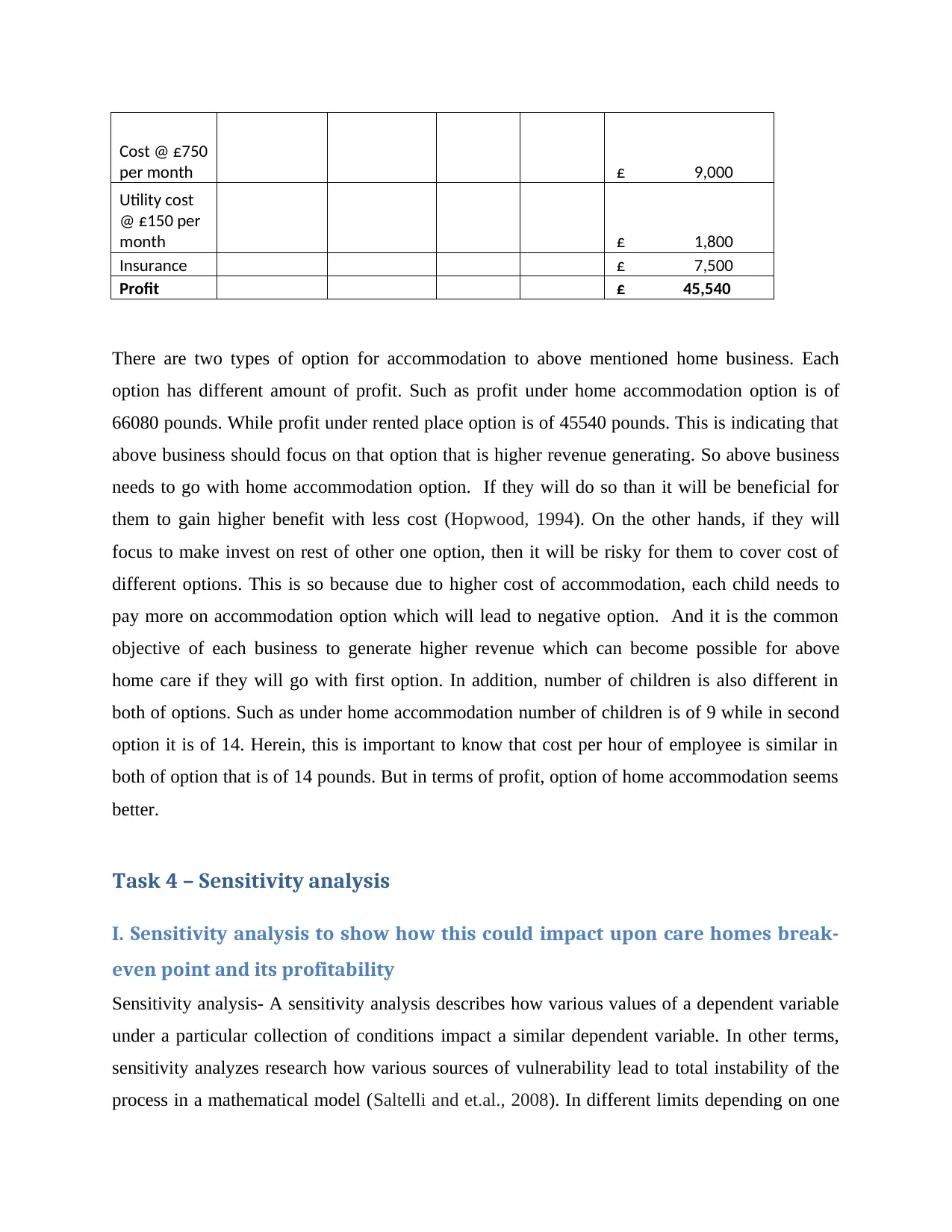

Cost @ £750

per month £ 9,000

Utility cost

@ £150 per

month £ 1,800

Insurance £ 7,500

Profit £ 45,540

There are two types of option for accommodation to above mentioned home business. Each

option has different amount of profit. Such as profit under home accommodation option is of

66080 pounds. While profit under rented place option is of 45540 pounds. This is indicating that

above business should focus on that option that is higher revenue generating. So above business

needs to go with home accommodation option. If they will do so than it will be beneficial for

them to gain higher benefit with less cost (Hopwood, 1994). On the other hands, if they will

focus to make invest on rest of other one option, then it will be risky for them to cover cost of

different options. This is so because due to higher cost of accommodation, each child needs to

pay more on accommodation option which will lead to negative option. And it is the common

objective of each business to generate higher revenue which can become possible for above

home care if they will go with first option. In addition, number of children is also different in

both of options. Such as under home accommodation number of children is of 9 while in second

option it is of 14. Herein, this is important to know that cost per hour of employee is similar in

both of option that is of 14 pounds. But in terms of profit, option of home accommodation seems

better.

Task 4 – Sensitivity analysis

I. Sensitivity analysis to show how this could impact upon care homes break-

even point and its profitability

Sensitivity analysis- A sensitivity analysis describes how various values of a dependent variable

under a particular collection of conditions impact a similar dependent variable. In other terms,

sensitivity analyzes research how various sources of vulnerability lead to total instability of the

process in a mathematical model (Saltelli and et.al., 2008). In different limits depending on one

per month £ 9,000

Utility cost

@ £150 per

month £ 1,800

Insurance £ 7,500

Profit £ 45,540

There are two types of option for accommodation to above mentioned home business. Each

option has different amount of profit. Such as profit under home accommodation option is of

66080 pounds. While profit under rented place option is of 45540 pounds. This is indicating that

above business should focus on that option that is higher revenue generating. So above business

needs to go with home accommodation option. If they will do so than it will be beneficial for

them to gain higher benefit with less cost (Hopwood, 1994). On the other hands, if they will

focus to make invest on rest of other one option, then it will be risky for them to cover cost of

different options. This is so because due to higher cost of accommodation, each child needs to

pay more on accommodation option which will lead to negative option. And it is the common

objective of each business to generate higher revenue which can become possible for above

home care if they will go with first option. In addition, number of children is also different in

both of options. Such as under home accommodation number of children is of 9 while in second

option it is of 14. Herein, this is important to know that cost per hour of employee is similar in

both of option that is of 14 pounds. But in terms of profit, option of home accommodation seems

better.

Task 4 – Sensitivity analysis

I. Sensitivity analysis to show how this could impact upon care homes break-

even point and its profitability

Sensitivity analysis- A sensitivity analysis describes how various values of a dependent variable

under a particular collection of conditions impact a similar dependent variable. In other terms,

sensitivity analyzes research how various sources of vulnerability lead to total instability of the

process in a mathematical model (Saltelli and et.al., 2008). In different limits depending on one

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

or more input variables, this approach is used. Sensitivity analysis is a technique which is used to

determine how different values of an independent variable will influence a particular dependent

variable under a given set of assumptions. This technique is used within specific limits that will

depend on one or more input variables, such as the effect that changes in interest rates will have

on the price of such a bond (Saltelli, and et.al., 2004).

Sensitivity analysis is related to the uncertainty inherent in mathematical models, where the

values of inputs used in the model may vary. It is the companion analytical tool for uncertainty

analysis, and the two are often used together. All models are formulated based on assumptions

regarding the validity of inputs used in calculations or studies conducted to draw conclusions for

policy decisions.

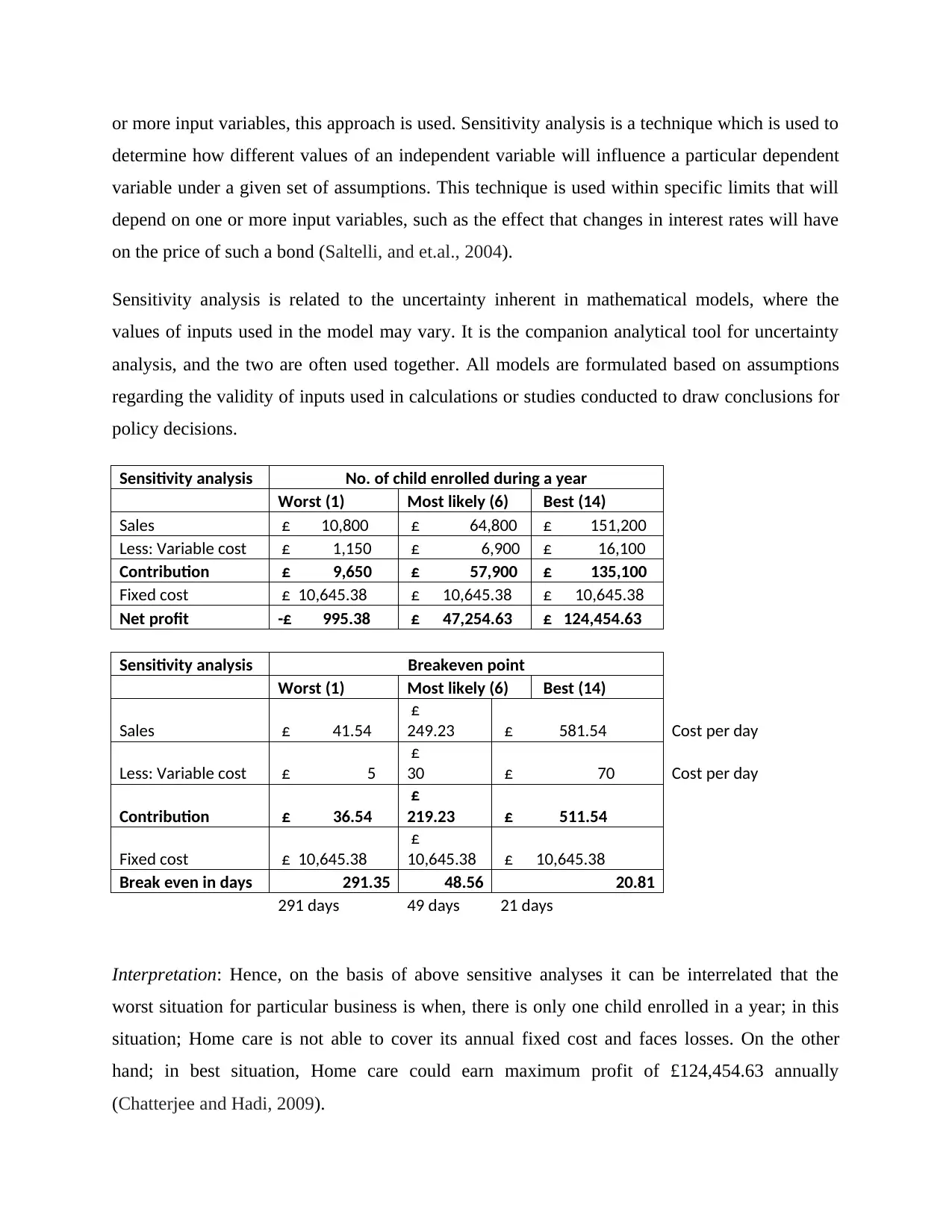

Sensitivity analysis No. of child enrolled during a year

Worst (1) Most likely (6) Best (14)

Sales £ 10,800 £ 64,800 £ 151,200

Less: Variable cost £ 1,150 £ 6,900 £ 16,100

Contribution £ 9,650 £ 57,900 £ 135,100

Fixed cost £ 10,645.38 £ 10,645.38 £ 10,645.38

Net profit -£ 995.38 £ 47,254.63 £ 124,454.63

Sensitivity analysis Breakeven point

Worst (1) Most likely (6) Best (14)

Sales £ 41.54

£

249.23 £ 581.54 Cost per day

Less: Variable cost £ 5

£

30 £ 70 Cost per day

Contribution £ 36.54

£

219.23 £ 511.54

Fixed cost £ 10,645.38

£

10,645.38 £ 10,645.38

Break even in days 291.35 48.56 20.81

291 days 49 days 21 days

Interpretation: Hence, on the basis of above sensitive analyses it can be interrelated that the

worst situation for particular business is when, there is only one child enrolled in a year; in this

situation; Home care is not able to cover its annual fixed cost and faces losses. On the other

hand; in best situation, Home care could earn maximum profit of £124,454.63 annually

(Chatterjee and Hadi, 2009).

determine how different values of an independent variable will influence a particular dependent

variable under a given set of assumptions. This technique is used within specific limits that will

depend on one or more input variables, such as the effect that changes in interest rates will have

on the price of such a bond (Saltelli, and et.al., 2004).

Sensitivity analysis is related to the uncertainty inherent in mathematical models, where the

values of inputs used in the model may vary. It is the companion analytical tool for uncertainty

analysis, and the two are often used together. All models are formulated based on assumptions

regarding the validity of inputs used in calculations or studies conducted to draw conclusions for

policy decisions.

Sensitivity analysis No. of child enrolled during a year

Worst (1) Most likely (6) Best (14)

Sales £ 10,800 £ 64,800 £ 151,200

Less: Variable cost £ 1,150 £ 6,900 £ 16,100

Contribution £ 9,650 £ 57,900 £ 135,100

Fixed cost £ 10,645.38 £ 10,645.38 £ 10,645.38

Net profit -£ 995.38 £ 47,254.63 £ 124,454.63

Sensitivity analysis Breakeven point

Worst (1) Most likely (6) Best (14)

Sales £ 41.54

£

249.23 £ 581.54 Cost per day

Less: Variable cost £ 5

£

30 £ 70 Cost per day

Contribution £ 36.54

£

219.23 £ 511.54

Fixed cost £ 10,645.38

£

10,645.38 £ 10,645.38

Break even in days 291.35 48.56 20.81

291 days 49 days 21 days

Interpretation: Hence, on the basis of above sensitive analyses it can be interrelated that the

worst situation for particular business is when, there is only one child enrolled in a year; in this

situation; Home care is not able to cover its annual fixed cost and faces losses. On the other

hand; in best situation, Home care could earn maximum profit of £124,454.63 annually

(Chatterjee and Hadi, 2009).

While talking about break-even point; in case of worst scenario, Home care is not able to cover

its fixed cost. This indicated by 291 days which exceeds 52 weeks in a year and in best scenario,

the minimum time taken by business to cover its fixed cost is 21 days.

CONCLUSION

Hence, after analyzing whole business report, it can be concluded that; Home care business has

more opportunity to grow its business through adopting best way fit to its business requirement

and legal actions. As, the whole report is just an assumption and estimation, other non-financial

factors like cultural gaps, moral issues and mental development should also considered and

prioritize for profit and generating sales revenues.

its fixed cost. This indicated by 291 days which exceeds 52 weeks in a year and in best scenario,

the minimum time taken by business to cover its fixed cost is 21 days.

CONCLUSION

Hence, after analyzing whole business report, it can be concluded that; Home care business has

more opportunity to grow its business through adopting best way fit to its business requirement

and legal actions. As, the whole report is just an assumption and estimation, other non-financial

factors like cultural gaps, moral issues and mental development should also considered and

prioritize for profit and generating sales revenues.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.