Business Finance Report: Analyzing Financial Performance and Cash Flow

VerifiedAdded on 2020/10/05

|12

|3434

|325

Report

AI Summary

This report provides an in-depth analysis of business finance, focusing on the concepts of profit, cash flow, and working capital. It explores the differences between profit and cash flow, the components of working capital (receivables, inventory, and payables), and how changes in working capital impact cash flow. The report uses Uber Tools (UTL) as a case study, examining how accounting concepts like accrual and full disclosure affect financial results. It further discusses strategies to improve cash flow through effective working capital management, including pricing strategies, leasing options, supplier relationships, credit checks, invoice management, electronic payment systems, and inventory optimization. The second part of the report delves into financial performance, defining key elements such as assets, liabilities, equity, expenses, and revenues. It also includes the calculation and interpretation of financial ratios like sales growth, gross profit margin, and operating income, offering recommendations for assessing the financial performance of a business. The report concludes by summarizing the key findings and recommendations for financial management.

Business

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

a. Meaning of profit and cash flow .............................................................................................1

b. Meaning of working capital, receivable, inventory and payables...........................................1

c. Changes in working capital that affect cash flow....................................................................2

2. Company may affect financial results .....................................................................................2

3. Improvement in cash flow through management of working capital......................................3

PART 2............................................................................................................................................4

1. (a) Elements of financial performance ....................................................................................4

b. Calculation of ratio for each year ............................................................................................5

c. Result to consider why ratio may change information ...........................................................6

2. Analyse and recommendation that helps to assess the financial performance of business.....7

CONCLUSION................................................................................................................................7

REFERENCE...................................................................................................................................9

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

a. Meaning of profit and cash flow .............................................................................................1

b. Meaning of working capital, receivable, inventory and payables...........................................1

c. Changes in working capital that affect cash flow....................................................................2

2. Company may affect financial results .....................................................................................2

3. Improvement in cash flow through management of working capital......................................3

PART 2............................................................................................................................................4

1. (a) Elements of financial performance ....................................................................................4

b. Calculation of ratio for each year ............................................................................................5

c. Result to consider why ratio may change information ...........................................................6

2. Analyse and recommendation that helps to assess the financial performance of business.....7

CONCLUSION................................................................................................................................7

REFERENCE...................................................................................................................................9

INTRODUCTION

Finance is first need of every organisation that helps to run a business effectively and

maintain profit margin. Business finance contains acquisition and utilization of funds so business

enterprise carry out their operation function efficiently. A businessman need to raise funds in

order to run growth of business (Belás and et.al., 2015). The main purpose of this report is to

understand the importance of business finance and how to increase it. To understand the concept

of business finance Uber tools has been taken that is UK based company and manufacture power

tools. This report will focus on different topics such as difference between profit and cash flow,

working capital, meaning of receivable, inventory and payables that will helps to show

profitability situation of UTL. Moreover, this report will define how working capital affect cash

flow if any changes arises, various ratio like sales growth, liquidity, gross profit, gearing, interest

coverage and return on equity that helps to describe financial performance of companies.

PART 1

1. (a) Meaning of profit and cash flow

Profit means net income that is calculate after ducting all expenses and taxes. Cash flow

means net amount that includes cash and cash equivalents amount which is transferred in to and

out of a business. In additional, cash flow is the gettable amount in a business at a certain period

of time as a result outflow and inflow of money that can be control by investing.

Profit contains net income after deducting interest and tax amount where as cash flow is

the collection of operating, investing and financing activity. In any organisation availability of

funds may make or break an enterprise and cash flow determines the viability.

(b). Meaning of working capital, receivable, inventory and payables

Working capital is required amount in any industry that is the difference between

company's current assets and current liabilities. Current assets means assets that can be converted

in cash within a year easily such as cash, debtor, bank, account receivable etc. and current

liabilities means need to pay within a year like as creditors or payables (Buckland and Davis,

2016).

Receivable is also known as account receivable, is balance of pending amount to a firm

or company for delivering goods and services but not receive payment through customers. Said

1

Finance is first need of every organisation that helps to run a business effectively and

maintain profit margin. Business finance contains acquisition and utilization of funds so business

enterprise carry out their operation function efficiently. A businessman need to raise funds in

order to run growth of business (Belás and et.al., 2015). The main purpose of this report is to

understand the importance of business finance and how to increase it. To understand the concept

of business finance Uber tools has been taken that is UK based company and manufacture power

tools. This report will focus on different topics such as difference between profit and cash flow,

working capital, meaning of receivable, inventory and payables that will helps to show

profitability situation of UTL. Moreover, this report will define how working capital affect cash

flow if any changes arises, various ratio like sales growth, liquidity, gross profit, gearing, interest

coverage and return on equity that helps to describe financial performance of companies.

PART 1

1. (a) Meaning of profit and cash flow

Profit means net income that is calculate after ducting all expenses and taxes. Cash flow

means net amount that includes cash and cash equivalents amount which is transferred in to and

out of a business. In additional, cash flow is the gettable amount in a business at a certain period

of time as a result outflow and inflow of money that can be control by investing.

Profit contains net income after deducting interest and tax amount where as cash flow is

the collection of operating, investing and financing activity. In any organisation availability of

funds may make or break an enterprise and cash flow determines the viability.

(b). Meaning of working capital, receivable, inventory and payables

Working capital is required amount in any industry that is the difference between

company's current assets and current liabilities. Current assets means assets that can be converted

in cash within a year easily such as cash, debtor, bank, account receivable etc. and current

liabilities means need to pay within a year like as creditors or payables (Buckland and Davis,

2016).

Receivable is also known as account receivable, is balance of pending amount to a firm

or company for delivering goods and services but not receive payment through customers. Said

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

other way, account receivable are sum of money owned by consumer to another entity for selling

goods and services on credit.

Inventory is an accounting term that means goods or stock are being get ready for selling

on an enterprise such as finished goods. It involves raw material ( used to manufacture goods),

work in progress (process being made) and finished good ( ready for sale).

Payables refers money owned to employees, creditors, government or lenders represent

as a liability in financial statement. If these liability are pending within twelve months, it will be

shown as short term liability.

(c). Changes in working capital that affect cash flow

Every organisation prepare financial statement and cash flow statement which shows

company's financial position by including inflow and outflow. Any business is depend on its

working capital that is variation between current assets and current liabilities which impact on

cash flow statement. Changes in working capital affect cash flow such as if firm increase amount

of current assets, cash flow from operation activity will decrease. If assets amount decrease or

reduce, cash flow from operating activity will decrease. For instance, if UTL purchase fixed

assets then current assets will increase and cash flow will also impact. If currents assets sold by

manager then currents assets will decrease but cash will increase and cash flow will be of same

amount (Cassar, Ittner and Cavalluzzo, 2015).

2. Company may affect financial results

Accounting concept are the important rules and regulation to that deals with monetary

value's items that can be attributed. In Uber tools manager follows accrual and full discloser,

matching and accrual concept that helps to run a business such as :

Accrual concept: This concept states expenses and revenues, that is not recorded yet in

company's balance sheet. According to accrual concept an enterprise should record all expenses

and incomes at the time of incurred which is not mentioned in financial statement. Manager of

UTL company prepare financial statement and shows revenues and expenses, based on accrual

accounting such as interest expenses, payables and account receivables.

Full discloser concept: This means a firm should disclose all information that relates to

business. UTL use this concept and prepare financial statements by disclosing all financial

information that helps to increase profits. Such as the operating profit of UTL was £ 36 million

in last year before interest and tax by using accounting concepts.

2

goods and services on credit.

Inventory is an accounting term that means goods or stock are being get ready for selling

on an enterprise such as finished goods. It involves raw material ( used to manufacture goods),

work in progress (process being made) and finished good ( ready for sale).

Payables refers money owned to employees, creditors, government or lenders represent

as a liability in financial statement. If these liability are pending within twelve months, it will be

shown as short term liability.

(c). Changes in working capital that affect cash flow

Every organisation prepare financial statement and cash flow statement which shows

company's financial position by including inflow and outflow. Any business is depend on its

working capital that is variation between current assets and current liabilities which impact on

cash flow statement. Changes in working capital affect cash flow such as if firm increase amount

of current assets, cash flow from operation activity will decrease. If assets amount decrease or

reduce, cash flow from operating activity will decrease. For instance, if UTL purchase fixed

assets then current assets will increase and cash flow will also impact. If currents assets sold by

manager then currents assets will decrease but cash will increase and cash flow will be of same

amount (Cassar, Ittner and Cavalluzzo, 2015).

2. Company may affect financial results

Accounting concept are the important rules and regulation to that deals with monetary

value's items that can be attributed. In Uber tools manager follows accrual and full discloser,

matching and accrual concept that helps to run a business such as :

Accrual concept: This concept states expenses and revenues, that is not recorded yet in

company's balance sheet. According to accrual concept an enterprise should record all expenses

and incomes at the time of incurred which is not mentioned in financial statement. Manager of

UTL company prepare financial statement and shows revenues and expenses, based on accrual

accounting such as interest expenses, payables and account receivables.

Full discloser concept: This means a firm should disclose all information that relates to

business. UTL use this concept and prepare financial statements by disclosing all financial

information that helps to increase profits. Such as the operating profit of UTL was £ 36 million

in last year before interest and tax by using accounting concepts.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Matching concept: This is a core concept of accounting that means expenses of any

enterprises should be matched with its income or revenue which incurred from expenses.

Moreover, it states debit and credit side of accounts should be equal while maintaining accounts.

UTL apply this concept and record all transaction such as income and expenses of enterprise

(Cole and Sokolyk, 2016).

Accounting concepts are the essential part of any firm that helps to improve financial

results by maintaining proper records of accounts and transaction. Manager of UTL shows bad

debt that was increased £ 350 million from £ 250 million that year before that affect company's

financial results and position by using concepts.

3. Improvement in cash flow through management of working capital

The management of working capital assures that an organisation is able to make and

continue its operation function and it has ability to give satisfaction to both short term debt and

further incurring operational expenses. It considers managing stock, cash, account receivable and

payable. In UTL manager focuses on management of working capital that helps to increase in

cash flow by recording all current assets and liabilities.

Steps to improve cash flow and their recommendation

Increase price policy: Every enterprises can increase cash flow by selling number of

products at increasing price. Increasing prices will impact on UTL's profits and and financial

position because if price will be high then inflow will be generate (Cumming, Hou and Lee,

2016).

Lease, no need to buy: Since leasing is more costly than buying and there is need to pay

attention to bottom line that expenses are paid off or not, by maintaining incomes and expenses.

But by leasing there is a benefit that can pay in small instalment which helps to improve cash

flow. Manager of UTL also can use to establish new market of power tools at new place that will

help to increase the cash flow by investing in small increments.

From a buying cooperative: This means a company should use proper mind that will

help to increase cash flow such as need to purchase at low price with suppliers and maintain

relationship in order to getting discount (Moisseron, Moschetto and Teulon, 2015).

Conduct credit check on customers: This means an organisation should issue credit

check instead of cash payment if customer wants. For example, if customer has not sufficient

amount to pay then supplier should issue credit check that will help to receive payment on time

3

enterprises should be matched with its income or revenue which incurred from expenses.

Moreover, it states debit and credit side of accounts should be equal while maintaining accounts.

UTL apply this concept and record all transaction such as income and expenses of enterprise

(Cole and Sokolyk, 2016).

Accounting concepts are the essential part of any firm that helps to improve financial

results by maintaining proper records of accounts and transaction. Manager of UTL shows bad

debt that was increased £ 350 million from £ 250 million that year before that affect company's

financial results and position by using concepts.

3. Improvement in cash flow through management of working capital

The management of working capital assures that an organisation is able to make and

continue its operation function and it has ability to give satisfaction to both short term debt and

further incurring operational expenses. It considers managing stock, cash, account receivable and

payable. In UTL manager focuses on management of working capital that helps to increase in

cash flow by recording all current assets and liabilities.

Steps to improve cash flow and their recommendation

Increase price policy: Every enterprises can increase cash flow by selling number of

products at increasing price. Increasing prices will impact on UTL's profits and and financial

position because if price will be high then inflow will be generate (Cumming, Hou and Lee,

2016).

Lease, no need to buy: Since leasing is more costly than buying and there is need to pay

attention to bottom line that expenses are paid off or not, by maintaining incomes and expenses.

But by leasing there is a benefit that can pay in small instalment which helps to improve cash

flow. Manager of UTL also can use to establish new market of power tools at new place that will

help to increase the cash flow by investing in small increments.

From a buying cooperative: This means a company should use proper mind that will

help to increase cash flow such as need to purchase at low price with suppliers and maintain

relationship in order to getting discount (Moisseron, Moschetto and Teulon, 2015).

Conduct credit check on customers: This means an organisation should issue credit

check instead of cash payment if customer wants. For example, if customer has not sufficient

amount to pay then supplier should issue credit check that will help to receive payment on time

3

and increase customer loyalty. Manager of UTL can issue credit check as demand of customer

that will helps to increase inflow.

Send invoices out immediately: This means a supplier should send invoices at the time

of purchasing product and services that will helps to see receivables as soon as possible.

Follow electronic payment system: At present technologies are changing rapidly that

help to make profitable and product able organisation. By using new technique Manager of UTL

can increase cash flow through electronic payment system such as business credit card that give

a grace period as long as 21 day to pay.

Improve inventory: Every organisation should check stock time to time and should

focus what need to sell first instead of buying more material. For improving the inventory should

sell old stock which is in godown either discount or cost price. UTL should used FIFO method in

order to improve inventory that will be beneficial to improve cash flow (Djennas, 2016).

It has been recommended that if UTL adopt above mentioned all steps then can get

improvement in cash flow. It need to manage working capital in efficient manner and need to

keep records of all transaction such as increase and decrease in current assets or liabilities and

will helps to understand finance requirement and maintain cash flow.

PART 2

1. (a) Elements of financial performance

Financial performance is the ending result of any organisation that helps to measure how

well an enterprise could use assets in order to increase profits of company. Every firm prepares

financial statements end of the year with the help of financial information such as investors,

creditors that helps to analyse and evaluate financial performance (Gilje, 2017).In any

organisation manager make financial statement that shows financial position and future

expectation of company. It involves various elements to describe the financial performance like

as-

Assets: This involves wealth or legal right owned by business concern person at

monetary value to run a business. In another said, it is an item that is purchased by paying money

and expected to give benefits in future. It can be divide in to tangible, intangible, fixed and

current assets.

4

that will helps to increase inflow.

Send invoices out immediately: This means a supplier should send invoices at the time

of purchasing product and services that will helps to see receivables as soon as possible.

Follow electronic payment system: At present technologies are changing rapidly that

help to make profitable and product able organisation. By using new technique Manager of UTL

can increase cash flow through electronic payment system such as business credit card that give

a grace period as long as 21 day to pay.

Improve inventory: Every organisation should check stock time to time and should

focus what need to sell first instead of buying more material. For improving the inventory should

sell old stock which is in godown either discount or cost price. UTL should used FIFO method in

order to improve inventory that will be beneficial to improve cash flow (Djennas, 2016).

It has been recommended that if UTL adopt above mentioned all steps then can get

improvement in cash flow. It need to manage working capital in efficient manner and need to

keep records of all transaction such as increase and decrease in current assets or liabilities and

will helps to understand finance requirement and maintain cash flow.

PART 2

1. (a) Elements of financial performance

Financial performance is the ending result of any organisation that helps to measure how

well an enterprise could use assets in order to increase profits of company. Every firm prepares

financial statements end of the year with the help of financial information such as investors,

creditors that helps to analyse and evaluate financial performance (Gilje, 2017).In any

organisation manager make financial statement that shows financial position and future

expectation of company. It involves various elements to describe the financial performance like

as-

Assets: This involves wealth or legal right owned by business concern person at

monetary value to run a business. In another said, it is an item that is purchased by paying money

and expected to give benefits in future. It can be divide in to tangible, intangible, fixed and

current assets.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Liabilities: It is a obligation on any enterprise originated from past events that needs to

be pay as result outflow increases. Additional, liabilities are the amount paid by the businessman

to the creditors or outsiders. It can be classified in to current and non current liabilities.

Equity: This represent interest of owners in an organisation in form of stock or shares.

Basically equity is the differencing amount of value of assets and cost of liabilities. It is owned

by owner of the firm that helps to show the profit margin (Hanssens, Deloof and Vanacker,

2016).

Expenses: This is gross outflow which is arises by business corporation for generating

incomes and revenues. It shows in profit and loss account.

Revenues: It is gross inflow of assets that helps to increase owner's equity and maintain

profitability. For example, exchange of goods and services for money consideration that

maintains revenues.

Distribution to owners: This states decrease in equity that results from transfer to

business concern person. It defines the withdrawal amount through owners and reduce the

ownership interest. Such as cash dividend paid by a company to its shareholders (Julien, 2018).

Investments by owners: This means owner of any enterprise invest money in business in

order to get better returns. Moreover, it is contribution amount by owner to make profits and

growth of industry. For instance, issue of ownership shares of stock by a corporation for cash

amount.

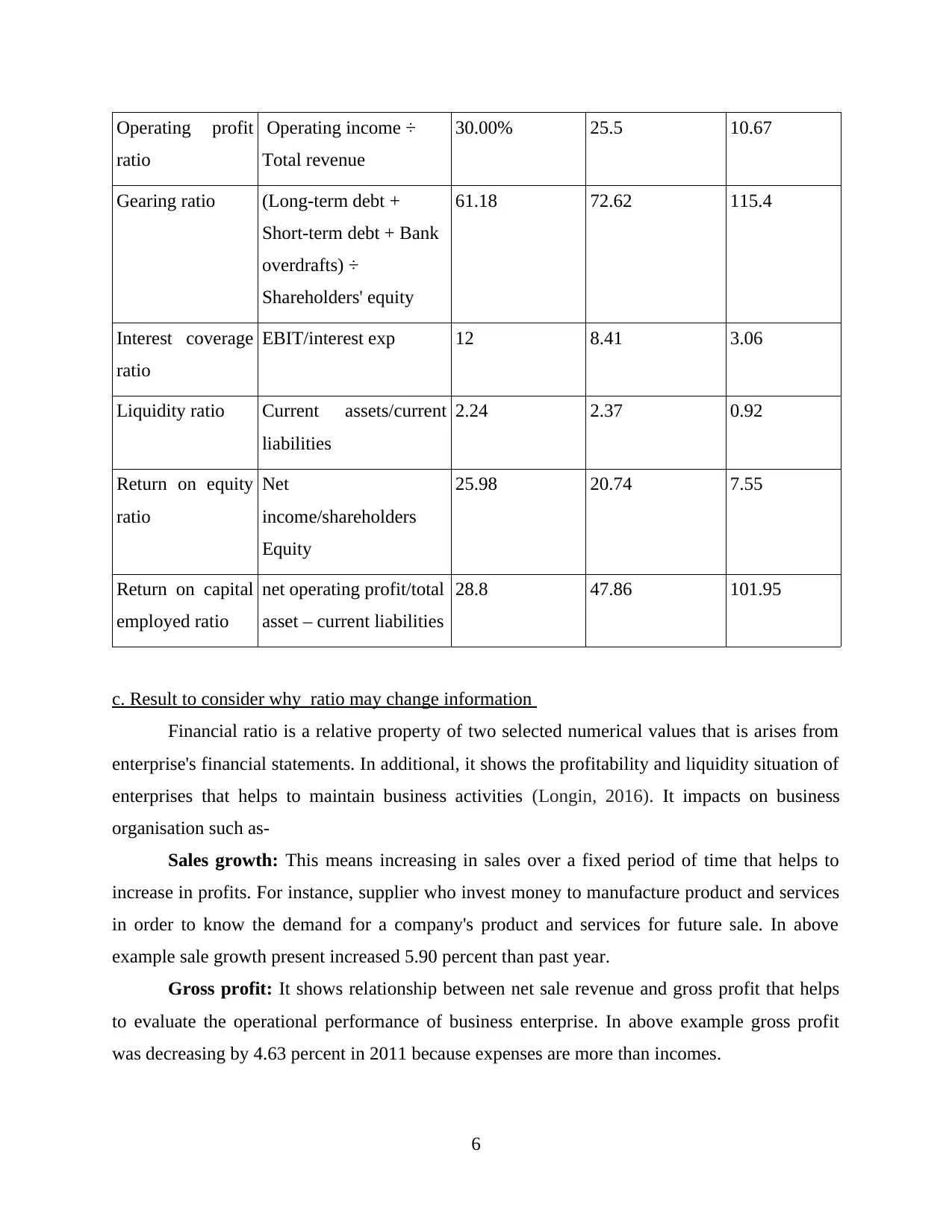

b. Calculation of ratio for each year

Ratio is the relation between two numbers or groups that helps to describe how much

bigger first is comparison to other number (Vismara and Benaroio, 2017). In additional, it is the

comparison between two numbers that shows liquidity, profitability, solvency and operational

efficiency ratio.

Ratio Formula 2009 2010 2011

Sales growth ratio Current year sale - last

year sale/last year

sale*100

- 10.00% 15.90%

Gross profit

margin ratio

Gross profit/total sales

revenue*100

63.88 63.63 59.25

5

be pay as result outflow increases. Additional, liabilities are the amount paid by the businessman

to the creditors or outsiders. It can be classified in to current and non current liabilities.

Equity: This represent interest of owners in an organisation in form of stock or shares.

Basically equity is the differencing amount of value of assets and cost of liabilities. It is owned

by owner of the firm that helps to show the profit margin (Hanssens, Deloof and Vanacker,

2016).

Expenses: This is gross outflow which is arises by business corporation for generating

incomes and revenues. It shows in profit and loss account.

Revenues: It is gross inflow of assets that helps to increase owner's equity and maintain

profitability. For example, exchange of goods and services for money consideration that

maintains revenues.

Distribution to owners: This states decrease in equity that results from transfer to

business concern person. It defines the withdrawal amount through owners and reduce the

ownership interest. Such as cash dividend paid by a company to its shareholders (Julien, 2018).

Investments by owners: This means owner of any enterprise invest money in business in

order to get better returns. Moreover, it is contribution amount by owner to make profits and

growth of industry. For instance, issue of ownership shares of stock by a corporation for cash

amount.

b. Calculation of ratio for each year

Ratio is the relation between two numbers or groups that helps to describe how much

bigger first is comparison to other number (Vismara and Benaroio, 2017). In additional, it is the

comparison between two numbers that shows liquidity, profitability, solvency and operational

efficiency ratio.

Ratio Formula 2009 2010 2011

Sales growth ratio Current year sale - last

year sale/last year

sale*100

- 10.00% 15.90%

Gross profit

margin ratio

Gross profit/total sales

revenue*100

63.88 63.63 59.25

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

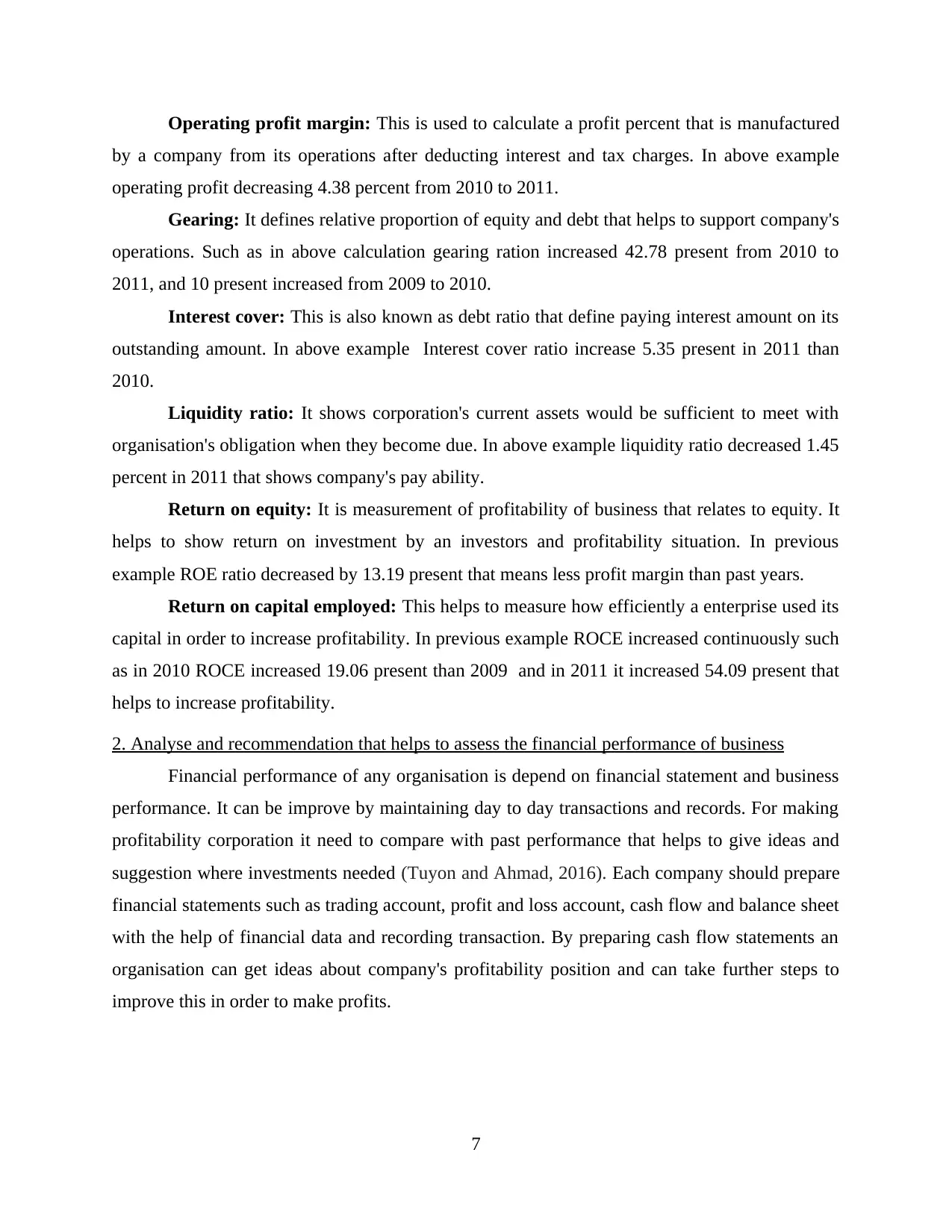

Operating profit

ratio

Operating income ÷

Total revenue

30.00% 25.5 10.67

Gearing ratio (Long-term debt +

Short-term debt + Bank

overdrafts) ÷

Shareholders' equity

61.18 72.62 115.4

Interest coverage

ratio

EBIT/interest exp 12 8.41 3.06

Liquidity ratio Current assets/current

liabilities

2.24 2.37 0.92

Return on equity

ratio

Net

income/shareholders

Equity

25.98 20.74 7.55

Return on capital

employed ratio

net operating profit/total

asset – current liabilities

28.8 47.86 101.95

c. Result to consider why ratio may change information

Financial ratio is a relative property of two selected numerical values that is arises from

enterprise's financial statements. In additional, it shows the profitability and liquidity situation of

enterprises that helps to maintain business activities (Longin, 2016). It impacts on business

organisation such as-

Sales growth: This means increasing in sales over a fixed period of time that helps to

increase in profits. For instance, supplier who invest money to manufacture product and services

in order to know the demand for a company's product and services for future sale. In above

example sale growth present increased 5.90 percent than past year.

Gross profit: It shows relationship between net sale revenue and gross profit that helps

to evaluate the operational performance of business enterprise. In above example gross profit

was decreasing by 4.63 percent in 2011 because expenses are more than incomes.

6

ratio

Operating income ÷

Total revenue

30.00% 25.5 10.67

Gearing ratio (Long-term debt +

Short-term debt + Bank

overdrafts) ÷

Shareholders' equity

61.18 72.62 115.4

Interest coverage

ratio

EBIT/interest exp 12 8.41 3.06

Liquidity ratio Current assets/current

liabilities

2.24 2.37 0.92

Return on equity

ratio

Net

income/shareholders

Equity

25.98 20.74 7.55

Return on capital

employed ratio

net operating profit/total

asset – current liabilities

28.8 47.86 101.95

c. Result to consider why ratio may change information

Financial ratio is a relative property of two selected numerical values that is arises from

enterprise's financial statements. In additional, it shows the profitability and liquidity situation of

enterprises that helps to maintain business activities (Longin, 2016). It impacts on business

organisation such as-

Sales growth: This means increasing in sales over a fixed period of time that helps to

increase in profits. For instance, supplier who invest money to manufacture product and services

in order to know the demand for a company's product and services for future sale. In above

example sale growth present increased 5.90 percent than past year.

Gross profit: It shows relationship between net sale revenue and gross profit that helps

to evaluate the operational performance of business enterprise. In above example gross profit

was decreasing by 4.63 percent in 2011 because expenses are more than incomes.

6

Operating profit margin: This is used to calculate a profit percent that is manufactured

by a company from its operations after deducting interest and tax charges. In above example

operating profit decreasing 4.38 percent from 2010 to 2011.

Gearing: It defines relative proportion of equity and debt that helps to support company's

operations. Such as in above calculation gearing ration increased 42.78 present from 2010 to

2011, and 10 present increased from 2009 to 2010.

Interest cover: This is also known as debt ratio that define paying interest amount on its

outstanding amount. In above example Interest cover ratio increase 5.35 present in 2011 than

2010.

Liquidity ratio: It shows corporation's current assets would be sufficient to meet with

organisation's obligation when they become due. In above example liquidity ratio decreased 1.45

percent in 2011 that shows company's pay ability.

Return on equity: It is measurement of profitability of business that relates to equity. It

helps to show return on investment by an investors and profitability situation. In previous

example ROE ratio decreased by 13.19 present that means less profit margin than past years.

Return on capital employed: This helps to measure how efficiently a enterprise used its

capital in order to increase profitability. In previous example ROCE increased continuously such

as in 2010 ROCE increased 19.06 present than 2009 and in 2011 it increased 54.09 present that

helps to increase profitability.

2. Analyse and recommendation that helps to assess the financial performance of business

Financial performance of any organisation is depend on financial statement and business

performance. It can be improve by maintaining day to day transactions and records. For making

profitability corporation it need to compare with past performance that helps to give ideas and

suggestion where investments needed (Tuyon and Ahmad, 2016). Each company should prepare

financial statements such as trading account, profit and loss account, cash flow and balance sheet

with the help of financial data and recording transaction. By preparing cash flow statements an

organisation can get ideas about company's profitability position and can take further steps to

improve this in order to make profits.

7

by a company from its operations after deducting interest and tax charges. In above example

operating profit decreasing 4.38 percent from 2010 to 2011.

Gearing: It defines relative proportion of equity and debt that helps to support company's

operations. Such as in above calculation gearing ration increased 42.78 present from 2010 to

2011, and 10 present increased from 2009 to 2010.

Interest cover: This is also known as debt ratio that define paying interest amount on its

outstanding amount. In above example Interest cover ratio increase 5.35 present in 2011 than

2010.

Liquidity ratio: It shows corporation's current assets would be sufficient to meet with

organisation's obligation when they become due. In above example liquidity ratio decreased 1.45

percent in 2011 that shows company's pay ability.

Return on equity: It is measurement of profitability of business that relates to equity. It

helps to show return on investment by an investors and profitability situation. In previous

example ROE ratio decreased by 13.19 present that means less profit margin than past years.

Return on capital employed: This helps to measure how efficiently a enterprise used its

capital in order to increase profitability. In previous example ROCE increased continuously such

as in 2010 ROCE increased 19.06 present than 2009 and in 2011 it increased 54.09 present that

helps to increase profitability.

2. Analyse and recommendation that helps to assess the financial performance of business

Financial performance of any organisation is depend on financial statement and business

performance. It can be improve by maintaining day to day transactions and records. For making

profitability corporation it need to compare with past performance that helps to give ideas and

suggestion where investments needed (Tuyon and Ahmad, 2016). Each company should prepare

financial statements such as trading account, profit and loss account, cash flow and balance sheet

with the help of financial data and recording transaction. By preparing cash flow statements an

organisation can get ideas about company's profitability position and can take further steps to

improve this in order to make profits.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION

Finance is the lifeblood of any organisation and business that helps to run a business at

market place by controlling cost and expenses. Moreover, Finance is the core of any business

and organisation that is used to grow a business activities by purchasing and selling product and

services. It make easy to understand need of business and take further steps to run an industry. It

is mandatory for each organisation to adopt accounting concept and principles that helps to take

effective business decision. This report covered various ratios that shows company's profitability

situation that helps to show financial performance.

8

Finance is the lifeblood of any organisation and business that helps to run a business at

market place by controlling cost and expenses. Moreover, Finance is the core of any business

and organisation that is used to grow a business activities by purchasing and selling product and

services. It make easy to understand need of business and take further steps to run an industry. It

is mandatory for each organisation to adopt accounting concept and principles that helps to take

effective business decision. This report covered various ratios that shows company's profitability

situation that helps to show financial performance.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

REFERENCE

Books and Journal

Belás, J., and et.al., 2015. The business environment of small and medium-sized enterprises in

selected regions of the Czech Republic and Slovakia. E+ M Ekonomie a Management.

Buckland, R. and Davis, E. W., 2016. Finance for growing enterprises. Routledge.

Cassar, G., Ittner, C. D. and Cavalluzzo, K. S., 2015. Alternative information sources and

information asymmetry reduction: Evidence from small business debt. Journal of

Accounting and Economics. 59(2-3). pp.242-263.

Cole, R. and Sokolyk, T., 2016. Who needs credit and who gets credit? Evidence from the

surveys of small business finances. Journal of Financial Stability. 24. pp.40-60.

Cumming, D., Hou, W. and Lee, E., 2016. Business ethics and finance in greater China:

Synthesis and future directions in sustainability, CSR, and fraud. Journal of business

ethics. 138(4). pp.601-626.

Djennas, M., 2016. Business cycle volatility, growth and financial openness: Does Islamic

finance make any difference?. Borsa Istanbul Review. 16(3). pp.121-145.

Gilje, E.P., 2017. Does local access to finance matter? Evidence from US oil and natural gas

shale booms. Management Science.

Hanssens, J., Deloof, M. and Vanacker, T., 2016. The evolution of debt policies: New evidence

from business startups. Journal of Banking & Finance. 65. pp.120-133.

Julien, P.A., 2018. The state of the art in small business and entrepreneurship. Routledge.

Longin, F. ed., 2016. Extreme events in finance: A handbook of extreme value theory and its

applications. John Wiley & Sons.

Moisseron, J. Y., Moschetto, B. L. and Teulon, F., 2015. Islamic finance: a review of the

literature. The International Business & Economics Research Journal (Online). 14(5).

p.745.

Tuyon, J. and Ahmad, Z., 2016. Behavioural finance perspectives on Malaysian stock market

efficiency. Borsa Istanbul Review. 16(1). pp.43-61.

Vismara, S. and Benaroio, D., 2017. 11. Gender in entrepreneurial finance: matching investors

and entrepreneurs in equity. Gender and entrepreneurial activity. 271.

10

Books and Journal

Belás, J., and et.al., 2015. The business environment of small and medium-sized enterprises in

selected regions of the Czech Republic and Slovakia. E+ M Ekonomie a Management.

Buckland, R. and Davis, E. W., 2016. Finance for growing enterprises. Routledge.

Cassar, G., Ittner, C. D. and Cavalluzzo, K. S., 2015. Alternative information sources and

information asymmetry reduction: Evidence from small business debt. Journal of

Accounting and Economics. 59(2-3). pp.242-263.

Cole, R. and Sokolyk, T., 2016. Who needs credit and who gets credit? Evidence from the

surveys of small business finances. Journal of Financial Stability. 24. pp.40-60.

Cumming, D., Hou, W. and Lee, E., 2016. Business ethics and finance in greater China:

Synthesis and future directions in sustainability, CSR, and fraud. Journal of business

ethics. 138(4). pp.601-626.

Djennas, M., 2016. Business cycle volatility, growth and financial openness: Does Islamic

finance make any difference?. Borsa Istanbul Review. 16(3). pp.121-145.

Gilje, E.P., 2017. Does local access to finance matter? Evidence from US oil and natural gas

shale booms. Management Science.

Hanssens, J., Deloof, M. and Vanacker, T., 2016. The evolution of debt policies: New evidence

from business startups. Journal of Banking & Finance. 65. pp.120-133.

Julien, P.A., 2018. The state of the art in small business and entrepreneurship. Routledge.

Longin, F. ed., 2016. Extreme events in finance: A handbook of extreme value theory and its

applications. John Wiley & Sons.

Moisseron, J. Y., Moschetto, B. L. and Teulon, F., 2015. Islamic finance: a review of the

literature. The International Business & Economics Research Journal (Online). 14(5).

p.745.

Tuyon, J. and Ahmad, Z., 2016. Behavioural finance perspectives on Malaysian stock market

efficiency. Borsa Istanbul Review. 16(1). pp.43-61.

Vismara, S. and Benaroio, D., 2017. 11. Gender in entrepreneurial finance: matching investors

and entrepreneurs in equity. Gender and entrepreneurial activity. 271.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.