Corporate and Financial Accounting Report: Business Combination

VerifiedAdded on 2023/01/07

|12

|3879

|85

Report

AI Summary

This report provides a comprehensive analysis of corporate and financial accounting, with a specific focus on business combinations. Part A delves into the Australian Accounting Standards Board's role in global standard setting and the reasons IFRS is not compulsory for IASB members, along with the concepts of small and large proprietary companies and reporting entities. Part B examines business combinations through a comparative analysis of Baby Bunting Group Ltd and Accent Group Ltd, both Australian retail companies. The analysis includes the number of business combinations, fair value of consideration, components of acquisition costs, fair value of net identifiable assets, recognized and carrying values of assets and liabilities, goodwill, and intangible assets. The report also explores factors influencing goodwill recognition and provides a comparative analysis of the companies' disclosure practices. The report concludes by summarizing the key findings and insights gained from the analysis.

Corporate and

Financial Accounting

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

1. Explanation of the way in which Australian Accounting Standards Board take part in global

accounting standard setting process along with the reasons due to which IFRS are not

compulsory for the member countries of IASB...........................................................................1

2. Examination of the concept of small and large proprietary company and reporting entity

Along with the implication of being classified as either one of these types................................2

PART B............................................................................................................................................3

1. Total number of business combinations in the company report..............................................3

2. Fair value of consideration.......................................................................................................3

3. Components of acquisition costs.............................................................................................4

4. Fair value of all the net identifiable assets acquired................................................................4

5. Recognised value of each class of assets, liabilities and contingent liabilities........................5

6. Carrying value of each class of assets, liabilities and contingent liabilities............................5

7. The information regarding the value of goodwill or gain on bargain which is recorded in the

report............................................................................................................................................6

8. All the factors that are contributing in the recognition of the goodwill or gain on bargain

purchase.......................................................................................................................................7

9. The amount of goodwill as percentage of total consideration paid.........................................7

10. The amount of identifiable intangible assets as a percentage of total consideration paid.....8

11. Comparative analysis of the companies regarding disclosure of the business combination. 8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

1. Explanation of the way in which Australian Accounting Standards Board take part in global

accounting standard setting process along with the reasons due to which IFRS are not

compulsory for the member countries of IASB...........................................................................1

2. Examination of the concept of small and large proprietary company and reporting entity

Along with the implication of being classified as either one of these types................................2

PART B............................................................................................................................................3

1. Total number of business combinations in the company report..............................................3

2. Fair value of consideration.......................................................................................................3

3. Components of acquisition costs.............................................................................................4

4. Fair value of all the net identifiable assets acquired................................................................4

5. Recognised value of each class of assets, liabilities and contingent liabilities........................5

6. Carrying value of each class of assets, liabilities and contingent liabilities............................5

7. The information regarding the value of goodwill or gain on bargain which is recorded in the

report............................................................................................................................................6

8. All the factors that are contributing in the recognition of the goodwill or gain on bargain

purchase.......................................................................................................................................7

9. The amount of goodwill as percentage of total consideration paid.........................................7

10. The amount of identifiable intangible assets as a percentage of total consideration paid.....8

11. Comparative analysis of the companies regarding disclosure of the business combination. 8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Corporate and financial accounting are two different terms but both of them are required

to be focused by all the businesses as with the help of them companies can record all the

financial transactions as well as analyse the performance of business. If the organisation will not

be paying attention towards them then it may leave negative impact upon functionality of

business (Barker, 2019). Present report is having two different parts, Part A is focused with

accounting standard setting and reporting entity. Part B is related to the analysis of business

combination or acquisition assessment of the company. Two companies which are selected for

this part of the report are Baby Bunting Group Ltd and Accent Group Ltd. All the companies are

local entities of Australia. This assignment covers various topics such as role of Australian

Accounting Standard Board in setting global standard and concepts of small and large

proprietary and reporting entity. Additionally, detailed analysis of business communication of

two different companies is also covered in this report.

PART A

1. Explanation of the way in which Australian Accounting Standards Board take part in global

accounting standard setting process along with the reasons due to which IFRS are not

compulsory for the member countries of IASB

Australian Accounting Standards Board is responsible for taking part in the process of

global accounting standard setting process. All the accounting standards that are followed in

Australia are same as the standards of IFRS. When these standards are formulated by IASB then

AASB plays major role because all the standards that are followed in Australia are similar to

IFRS. The Australian Board take part in the global standard setting process effectively by

suggesting the IASB to make sure that all the IFRS are effectively formulated or not. Main

purpose of taking part in this process is to make sure that all the Australian Accounting standards

are issues, developed and maintained in systematic manner and amended with IFRS. AASB

consult with a range of stakeholders of companies of the Australia and analyses feedback from

them regarding IFRS. All the views of them are shared by AASB with IASB so that appropriate

changes could be made before setting a new standard (DAVALLOU and MAHMOODI, 2017).

If a country is a part of IASB then it does not required to follow IFRS because the

accounting process which will be followed by the will be formulated with the concept of

1

Corporate and financial accounting are two different terms but both of them are required

to be focused by all the businesses as with the help of them companies can record all the

financial transactions as well as analyse the performance of business. If the organisation will not

be paying attention towards them then it may leave negative impact upon functionality of

business (Barker, 2019). Present report is having two different parts, Part A is focused with

accounting standard setting and reporting entity. Part B is related to the analysis of business

combination or acquisition assessment of the company. Two companies which are selected for

this part of the report are Baby Bunting Group Ltd and Accent Group Ltd. All the companies are

local entities of Australia. This assignment covers various topics such as role of Australian

Accounting Standard Board in setting global standard and concepts of small and large

proprietary and reporting entity. Additionally, detailed analysis of business communication of

two different companies is also covered in this report.

PART A

1. Explanation of the way in which Australian Accounting Standards Board take part in global

accounting standard setting process along with the reasons due to which IFRS are not

compulsory for the member countries of IASB

Australian Accounting Standards Board is responsible for taking part in the process of

global accounting standard setting process. All the accounting standards that are followed in

Australia are same as the standards of IFRS. When these standards are formulated by IASB then

AASB plays major role because all the standards that are followed in Australia are similar to

IFRS. The Australian Board take part in the global standard setting process effectively by

suggesting the IASB to make sure that all the IFRS are effectively formulated or not. Main

purpose of taking part in this process is to make sure that all the Australian Accounting standards

are issues, developed and maintained in systematic manner and amended with IFRS. AASB

consult with a range of stakeholders of companies of the Australia and analyses feedback from

them regarding IFRS. All the views of them are shared by AASB with IASB so that appropriate

changes could be made before setting a new standard (DAVALLOU and MAHMOODI, 2017).

If a country is a part of IASB then it does not required to follow IFRS because the

accounting process which will be followed by the will be formulated with the concept of

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

international reporting standards. For all the member countries of International Accounting

Standard Board it is not compulsory that they should follow the IFRS system because the rules,

regulation and principles for accounting which will be followed by them will have all the

amendments of IFRS.

2. Examination of the concept of small and large proprietary company and reporting entity Along

with the implication of being classified as either one of these types

In all the countries different companies operate business for different objectives. Some

types of businesses are described below:

Small proprietary company: A small business which is satisfying two of the following

criteria will be treated as small proprietary company:

The consolidated revenues for the year ending are less than 10 million dollars.

The total value of the consolidated assets at the end of accounting years is less than 5

million dollars.

The number of staff members working within the company is less than 50 at the end of

the accounting year.

If a business will comply with two of the above described points then it will be the small

proprietary company (Gilala, 2017).

Large proprietary company: An organisation which is complying with two of the

following criteria will be treated as large proprietary company:

The number of individuals working within the enterprise is more than 50.

The value of gross operating revenues is more than 10 million dollars for the accounting

year ending.

The value of gross assets for the year ending is more than 5 million dollars.

If a business entity is fulfilling two of the above criteria then it will be the large

proprietary company.

Reporting entity: A business in which all the stakeholders and other concerned persons

are interested in determining the business position and performance is known as reporting entity.

All of them use the information for the purpose of making future decisions so that all the goals

and objectives could be met. For a reporting entity it is very important to make sure that it is

complying with all the financial guidelines so that accurate and transparent final accounts could

be generated (Kowalewski, 2016).

2

Standard Board it is not compulsory that they should follow the IFRS system because the rules,

regulation and principles for accounting which will be followed by them will have all the

amendments of IFRS.

2. Examination of the concept of small and large proprietary company and reporting entity Along

with the implication of being classified as either one of these types

In all the countries different companies operate business for different objectives. Some

types of businesses are described below:

Small proprietary company: A small business which is satisfying two of the following

criteria will be treated as small proprietary company:

The consolidated revenues for the year ending are less than 10 million dollars.

The total value of the consolidated assets at the end of accounting years is less than 5

million dollars.

The number of staff members working within the company is less than 50 at the end of

the accounting year.

If a business will comply with two of the above described points then it will be the small

proprietary company (Gilala, 2017).

Large proprietary company: An organisation which is complying with two of the

following criteria will be treated as large proprietary company:

The number of individuals working within the enterprise is more than 50.

The value of gross operating revenues is more than 10 million dollars for the accounting

year ending.

The value of gross assets for the year ending is more than 5 million dollars.

If a business entity is fulfilling two of the above criteria then it will be the large

proprietary company.

Reporting entity: A business in which all the stakeholders and other concerned persons

are interested in determining the business position and performance is known as reporting entity.

All of them use the information for the purpose of making future decisions so that all the goals

and objectives could be met. For a reporting entity it is very important to make sure that it is

complying with all the financial guidelines so that accurate and transparent final accounts could

be generated (Kowalewski, 2016).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART B

1. Total number of business combinations in the company report

Baby Bunting Group Ltd is operating its business in Australia and it was founded in year

1979. Accent Group Limited is the another company which is also an Australian company which

is established in Melbourne, Australia and was founded in year 1981. Both the companies are

operating business under Retail industry. Business combination could be defined as the

transaction which is obtained by the company which is acquiring another entity. It is one of the

ways which are focused by the businesses for the purpose of growing their size by ignoring the

organic activities for the same purpose. From the annual report of baby Bunting Group Ltd it has

been analysed that no detailed information regarding business combination is mentioned in the

annual report. The main reason of it is that the enterprise has not acquired any business in year

2019. The company is having two subsidiaries which could be considered as its business

combinations. These entities are Baby Bunting Pty Ltd and Baby Bunting EST Pty Ltd. (Annual

Report of Baby Bunting Group Ltd, 2019)

On the other hand, from the annual report of Accent Group for year 2019 it has been

analysed that there are various business combinations in its report. During the June month of

year 2019 the enterprise acquired 30 TAF stores and it includes the New Zealand Master

Franchise License which are required by it. Apart from this, a sneaker and fashion boutique was

also acquired by the company from Zanerobe Global Holdings Pty Ltd. which was a subtype

business. By analysing detailed information of these acquisitions it has been analysed that there

were two different business combinations in the annual report of Accent Group.

2. Fair value of consideration

From the annual report of Accent Group it has been analysed that the fair value for the

consideration which was paid at the acquisition was 435 as on 1st July 2018 and the same amount

for 30th June 2019 was 925 (Annual report of Accent Group, 2019). It was the opening and

closing balance for the enterprise. The actual fair value at the acquisition date for the

consideration transferred was around 12124. The key elements which were focused in the

calculation of it are cash paid to the vendor and outstanding debts. The total value of both of

them are 11813 and 311 respectively. The net cash which is used in the fair value was calculated

as follows:

3

1. Total number of business combinations in the company report

Baby Bunting Group Ltd is operating its business in Australia and it was founded in year

1979. Accent Group Limited is the another company which is also an Australian company which

is established in Melbourne, Australia and was founded in year 1981. Both the companies are

operating business under Retail industry. Business combination could be defined as the

transaction which is obtained by the company which is acquiring another entity. It is one of the

ways which are focused by the businesses for the purpose of growing their size by ignoring the

organic activities for the same purpose. From the annual report of baby Bunting Group Ltd it has

been analysed that no detailed information regarding business combination is mentioned in the

annual report. The main reason of it is that the enterprise has not acquired any business in year

2019. The company is having two subsidiaries which could be considered as its business

combinations. These entities are Baby Bunting Pty Ltd and Baby Bunting EST Pty Ltd. (Annual

Report of Baby Bunting Group Ltd, 2019)

On the other hand, from the annual report of Accent Group for year 2019 it has been

analysed that there are various business combinations in its report. During the June month of

year 2019 the enterprise acquired 30 TAF stores and it includes the New Zealand Master

Franchise License which are required by it. Apart from this, a sneaker and fashion boutique was

also acquired by the company from Zanerobe Global Holdings Pty Ltd. which was a subtype

business. By analysing detailed information of these acquisitions it has been analysed that there

were two different business combinations in the annual report of Accent Group.

2. Fair value of consideration

From the annual report of Accent Group it has been analysed that the fair value for the

consideration which was paid at the acquisition was 435 as on 1st July 2018 and the same amount

for 30th June 2019 was 925 (Annual report of Accent Group, 2019). It was the opening and

closing balance for the enterprise. The actual fair value at the acquisition date for the

consideration transferred was around 12124. The key elements which were focused in the

calculation of it are cash paid to the vendor and outstanding debts. The total value of both of

them are 11813 and 311 respectively. The net cash which is used in the fair value was calculated

as follows:

3

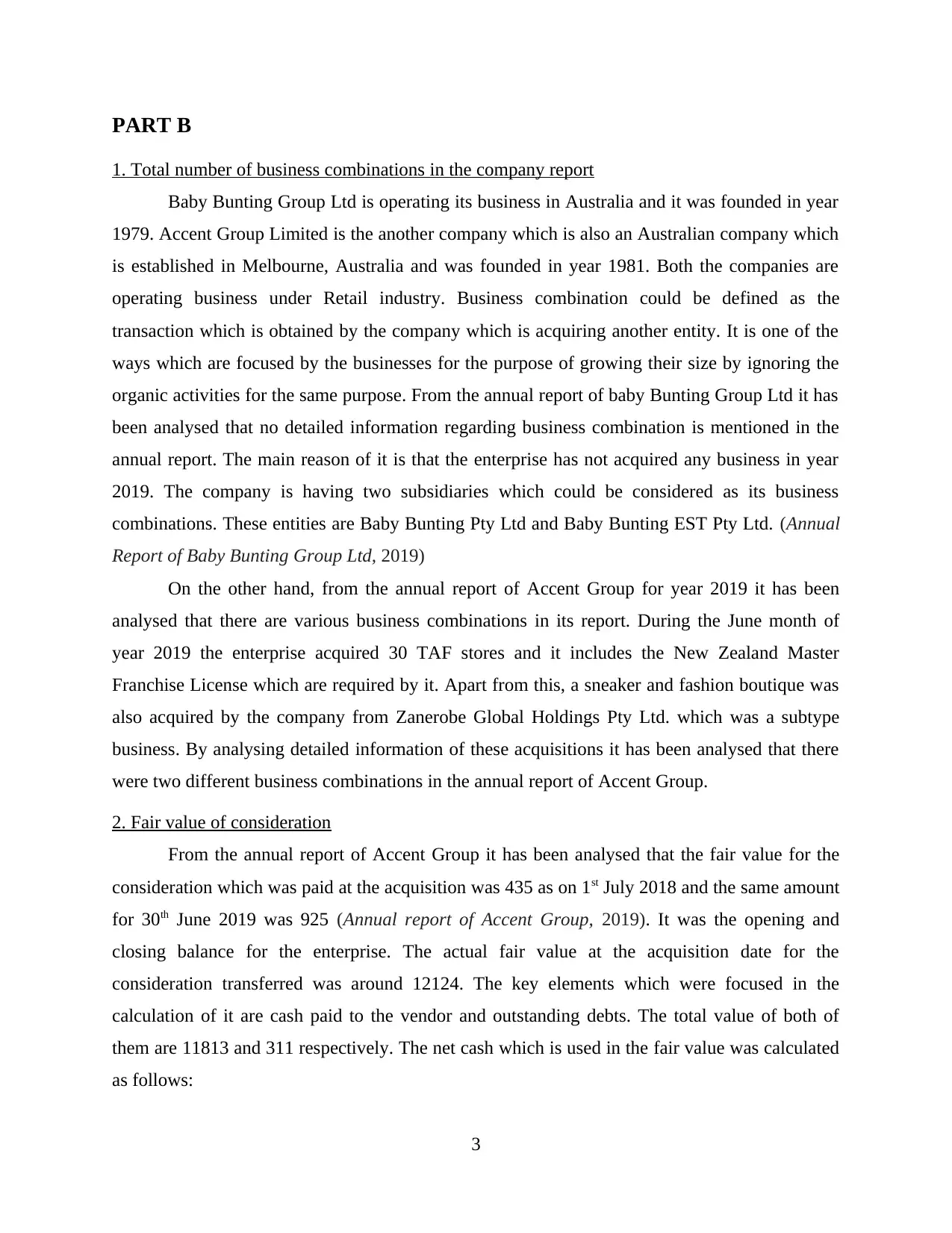

Particulars Amount

Cash used for acquiring business 12124

Less: Outstanding debts 311

Less: cash and cash equivalents 9

Net cash 11804

As Baby Bunting Group Ltd has not acquired any business during year 2019 so there will

be no fair value which would have been paid by the organisation for acquisition.

3. Components of acquisition costs

The amount which is faced by an organisation while acquiring the another business is

known as acquisition cost. From the annual report of Baby Bunting Group Ltd it has been

analysed that the company has not faced any acquisition cost because it has not acquired any

business during year 2019. On the other hand, the annual report of Accent Group is reflecting

that the total acquisition cost which was faced by the enterprise after acquiring 30 TAF stores

and Subtype Business was around 12124 dollars. The cash consideration in the total cost was

around 11813 and the non cash consideration of 311 was paid by the company to the owner of

the businesses which were acquired by it during 2019 (Kristanti and Herwany, 2017).

4. Fair value of all the net identifiable assets acquired

Net identifiable assets are such types of properties that are acquired by a business while

acquisition. The value of them could be measured within a specific time period with the future

benefit for the business. These are mainly used for the purpose of allocation of purchase price

and computation of goodwill during acquisition and merger. From the annual report of Baby

Bunting Group Ltd it has been analysed that there are no net identifiable assets that are acquired

by it as no acquisition was made by it during the year 2019. On the other hand, the value of net

identifiable assets in the annual report of Accent Group is around 2985. The elements that are

included in it are cash and cash equivalents, inventories, other current assets, property plant and

equipment, reacquired right, deferred tax asset etc. The values of all of them are around 9, 4146,

119, 256, 379 and 103 respectively. The elements that were deducted from the value of the assets

are lease liability, employee benefits, trade and other payables, other current liabilities etc. The

values of them are 674, 285, 21 and 1047 respectively (Nasr and Ntim, 2018).

4

Cash used for acquiring business 12124

Less: Outstanding debts 311

Less: cash and cash equivalents 9

Net cash 11804

As Baby Bunting Group Ltd has not acquired any business during year 2019 so there will

be no fair value which would have been paid by the organisation for acquisition.

3. Components of acquisition costs

The amount which is faced by an organisation while acquiring the another business is

known as acquisition cost. From the annual report of Baby Bunting Group Ltd it has been

analysed that the company has not faced any acquisition cost because it has not acquired any

business during year 2019. On the other hand, the annual report of Accent Group is reflecting

that the total acquisition cost which was faced by the enterprise after acquiring 30 TAF stores

and Subtype Business was around 12124 dollars. The cash consideration in the total cost was

around 11813 and the non cash consideration of 311 was paid by the company to the owner of

the businesses which were acquired by it during 2019 (Kristanti and Herwany, 2017).

4. Fair value of all the net identifiable assets acquired

Net identifiable assets are such types of properties that are acquired by a business while

acquisition. The value of them could be measured within a specific time period with the future

benefit for the business. These are mainly used for the purpose of allocation of purchase price

and computation of goodwill during acquisition and merger. From the annual report of Baby

Bunting Group Ltd it has been analysed that there are no net identifiable assets that are acquired

by it as no acquisition was made by it during the year 2019. On the other hand, the value of net

identifiable assets in the annual report of Accent Group is around 2985. The elements that are

included in it are cash and cash equivalents, inventories, other current assets, property plant and

equipment, reacquired right, deferred tax asset etc. The values of all of them are around 9, 4146,

119, 256, 379 and 103 respectively. The elements that were deducted from the value of the assets

are lease liability, employee benefits, trade and other payables, other current liabilities etc. The

values of them are 674, 285, 21 and 1047 respectively (Nasr and Ntim, 2018).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5. Recognised value of each class of assets, liabilities and contingent liabilities

The value which is determined the seller of business for all the assets, liabilities and other

elements that will be sold to the buyer is known as recognised value. There are various assets,

liabilities and contingent liabilities that were analysed while deciding the consideration of the

acquisition. It is very important for businesses to make sure that they are having detailed

information about all of them so that evaluation of business combination could be conducted in

systematic manner (Roychowdhury, Shroff and Verdi, 2019). The annual report of Baby Bunting

Group Ltd it has been analysed that there is no recognised value of each class of assets, liabilities

and contingent liabilities. Another company which is Accent Group acquired 30 TAF stores and

a fashion and sneaker boutique so there are various assets, liabilities and contingent liabilities

which were identified by the company. The recognised value of all the assets, liabilities an

contingent liabilities is as follows:

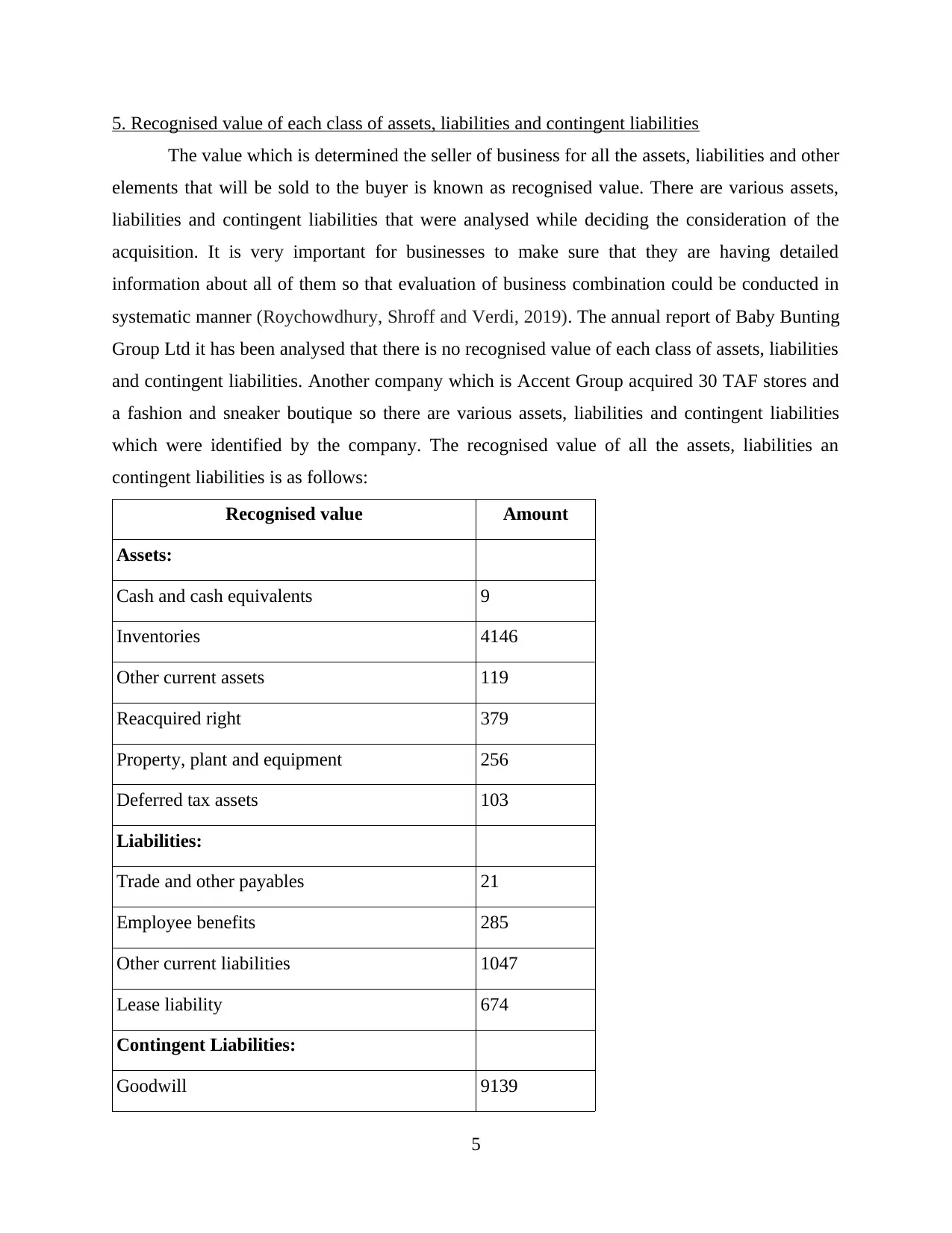

Recognised value Amount

Assets:

Cash and cash equivalents 9

Inventories 4146

Other current assets 119

Reacquired right 379

Property, plant and equipment 256

Deferred tax assets 103

Liabilities:

Trade and other payables 21

Employee benefits 285

Other current liabilities 1047

Lease liability 674

Contingent Liabilities:

Goodwill 9139

5

The value which is determined the seller of business for all the assets, liabilities and other

elements that will be sold to the buyer is known as recognised value. There are various assets,

liabilities and contingent liabilities that were analysed while deciding the consideration of the

acquisition. It is very important for businesses to make sure that they are having detailed

information about all of them so that evaluation of business combination could be conducted in

systematic manner (Roychowdhury, Shroff and Verdi, 2019). The annual report of Baby Bunting

Group Ltd it has been analysed that there is no recognised value of each class of assets, liabilities

and contingent liabilities. Another company which is Accent Group acquired 30 TAF stores and

a fashion and sneaker boutique so there are various assets, liabilities and contingent liabilities

which were identified by the company. The recognised value of all the assets, liabilities an

contingent liabilities is as follows:

Recognised value Amount

Assets:

Cash and cash equivalents 9

Inventories 4146

Other current assets 119

Reacquired right 379

Property, plant and equipment 256

Deferred tax assets 103

Liabilities:

Trade and other payables 21

Employee benefits 285

Other current liabilities 1047

Lease liability 674

Contingent Liabilities:

Goodwill 9139

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6. Carrying value of each class of assets, liabilities and contingent liabilities

Carrying value could be defined as an accounting measure which is based upon the value

represented in the balance sheet of the company. While recording information related to

acquisition the buyer business is required to have detailed information about it so that the

purchase consideration could be decided for the business. The annual report of Baby Bunting

Group Ltd it has been analysed that the company is not having any type of carrying value in the

annual report because no acquisition was made by it during the year 2019 (Sorensen and Miller,

2017). Apart from this, annual report of Accent Group is showing that the company acquired 30

stores and a subtype business so the details regarding the cost to the company is mentioned in the

report. There is no specific information is provided for the carrying cost so assets, liabilities and

contingent liabilities so the value of it will be same as the recognised cost. The detailed

assessment of all the elements for carrying value is as follows:

Carrying value Amount

Assets:

Inventories 4146

Reacquired right 379

Property, plant and equipment 256

Other current assets 119

Deferred tax assets 103

Cash and cash equivalents 9

Liabilities:

Other current liabilities 1047

Lease liability 674

Employee benefits 285

Trade and other payables 21

Contingent Liabilities:

Goodwill 9139

6

Carrying value could be defined as an accounting measure which is based upon the value

represented in the balance sheet of the company. While recording information related to

acquisition the buyer business is required to have detailed information about it so that the

purchase consideration could be decided for the business. The annual report of Baby Bunting

Group Ltd it has been analysed that the company is not having any type of carrying value in the

annual report because no acquisition was made by it during the year 2019 (Sorensen and Miller,

2017). Apart from this, annual report of Accent Group is showing that the company acquired 30

stores and a subtype business so the details regarding the cost to the company is mentioned in the

report. There is no specific information is provided for the carrying cost so assets, liabilities and

contingent liabilities so the value of it will be same as the recognised cost. The detailed

assessment of all the elements for carrying value is as follows:

Carrying value Amount

Assets:

Inventories 4146

Reacquired right 379

Property, plant and equipment 256

Other current assets 119

Deferred tax assets 103

Cash and cash equivalents 9

Liabilities:

Other current liabilities 1047

Lease liability 674

Employee benefits 285

Trade and other payables 21

Contingent Liabilities:

Goodwill 9139

6

7. The information regarding the value of goodwill or gain on bargain which is recorded in the

report

The annual report of Baby Bunting Group Ltd is showing 45321 as the value of goodwill

but it could not be considered as the element of acquisition or business combination because the

organisation has not acquired any business during the year 2019. On the other hand, the annual

report of Accent Group is showing 9139 as the goodwill in note 41 which is related to business

combination. It was the amount which was paid by the company to the owners of businesses

which were acquired by it during the year 2019. In the balance sheet of the company the opening

balance for goodwill was 295 and closing balance for the same is 304 (Thanh, 2016)

8. All the factors that are contributing in the recognition of the goodwill or gain on bargain

purchase

While buying a business it is very important for an organisation to make sure that

goodwill for the same is recognised because it can help to improve the market image. While

acquiring a new company the entities can pay attention towards different factors which are

location, time, nature of business, capital required, trend of profit and efficiency of management.

As Baby Bunting Group Ltd has not acquired any business during the year 2019 so there are no

factors which can contribute in the recognition of the goodwill. On the other hand, the annual

report of Accent Group it has been analysed that the company has acquired different stores and a

subtype business. While buying them the organisation paid attention towards different types of

factors. These are profits, nature of business and capital required. The profitability of all the

stores as well as the subtype business was very high so the entity focused it while recognising

goodwill. Apart from this, nature of business is also focused by the organisation for the purpose

of recognising the value of goodwill. As the stores that were acquired by it are operating

business under retail industry so it will help the entity to expand the business therefore the nature

of business was also focused by the entity while recognising goodwill of acquired entities

(Unerman, Bebbington and O’dwyer, 2018).

9. The amount of goodwill as percentage of total consideration paid

Baby Bunting Group Ltd has not acquired any business during the year 2019 so there will

be no amount of goodwill which would have been paid to the organisation which could have

acquired by it. On the other hand, Accent Group acquired 30 stores and a subtype business for

which the total consideration which was decided by the company was 12124. The amount of

7

report

The annual report of Baby Bunting Group Ltd is showing 45321 as the value of goodwill

but it could not be considered as the element of acquisition or business combination because the

organisation has not acquired any business during the year 2019. On the other hand, the annual

report of Accent Group is showing 9139 as the goodwill in note 41 which is related to business

combination. It was the amount which was paid by the company to the owners of businesses

which were acquired by it during the year 2019. In the balance sheet of the company the opening

balance for goodwill was 295 and closing balance for the same is 304 (Thanh, 2016)

8. All the factors that are contributing in the recognition of the goodwill or gain on bargain

purchase

While buying a business it is very important for an organisation to make sure that

goodwill for the same is recognised because it can help to improve the market image. While

acquiring a new company the entities can pay attention towards different factors which are

location, time, nature of business, capital required, trend of profit and efficiency of management.

As Baby Bunting Group Ltd has not acquired any business during the year 2019 so there are no

factors which can contribute in the recognition of the goodwill. On the other hand, the annual

report of Accent Group it has been analysed that the company has acquired different stores and a

subtype business. While buying them the organisation paid attention towards different types of

factors. These are profits, nature of business and capital required. The profitability of all the

stores as well as the subtype business was very high so the entity focused it while recognising

goodwill. Apart from this, nature of business is also focused by the organisation for the purpose

of recognising the value of goodwill. As the stores that were acquired by it are operating

business under retail industry so it will help the entity to expand the business therefore the nature

of business was also focused by the entity while recognising goodwill of acquired entities

(Unerman, Bebbington and O’dwyer, 2018).

9. The amount of goodwill as percentage of total consideration paid

Baby Bunting Group Ltd has not acquired any business during the year 2019 so there will

be no amount of goodwill which would have been paid to the organisation which could have

acquired by it. On the other hand, Accent Group acquired 30 stores and a subtype business for

which the total consideration which was decided by the company was 12124. The amount of

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

goodwill in this value was around 9139 (Warren and Jones, 2018). The calculation of amount of

goodwill as percentage of total consideration paid is as follows:

Formula: Goodwill / total purchase consideration * 100

= 9139 / 12124 * 100

= 0.754 * 100

= 75.4%

The amount of goodwill as percentage of total consideration is 75.4% for the acquisition

which was made by Accent Group during year 2019.

10. The amount of identifiable intangible assets as a percentage of total consideration paid

The annual report of baby Bunting Group is demonstrating that the company has not

made any acquisition during 2019 so there is no value mentioned in the annual report regarding

identifiable intangible assets. On the other hand, Accent Group acquired different businesses in

2019 so the annual report is showing detailed regarding net identifiable intangible assets. In

order to calculate the amount of the assets as a percentage of total consideration paid the value of

intangible assets will be required to analysed (Velte, 2019). The calculation for the same is as

follows:

Intangible assets = Goodwill + deferred tax asset + reacquired right

= 9139 + 103 + 379

= 9621

Formula for percentage = Net identifiable intangible assets / total consideration * 100

= 9621 / 12124 * 100

= 0.7935 * 100

= 79.35%

11. Comparative analysis of the companies regarding disclosure of the business combination

From the annual report of Baby Bunting Group Ltd and Accent Group it has been

analysed that first company has not mentioned any information regarding business combination

in the report. On the other hand, second entity mentioned detailed information about business

combination in the annual report. Main reason for the same is that Baby Bunting has not

acquired any business during year 2019 but Accent Group acquired different businesses in the

year 2019 (Zhou, 2018). If both the companies will be compared then it could be said that second

8

goodwill as percentage of total consideration paid is as follows:

Formula: Goodwill / total purchase consideration * 100

= 9139 / 12124 * 100

= 0.754 * 100

= 75.4%

The amount of goodwill as percentage of total consideration is 75.4% for the acquisition

which was made by Accent Group during year 2019.

10. The amount of identifiable intangible assets as a percentage of total consideration paid

The annual report of baby Bunting Group is demonstrating that the company has not

made any acquisition during 2019 so there is no value mentioned in the annual report regarding

identifiable intangible assets. On the other hand, Accent Group acquired different businesses in

2019 so the annual report is showing detailed regarding net identifiable intangible assets. In

order to calculate the amount of the assets as a percentage of total consideration paid the value of

intangible assets will be required to analysed (Velte, 2019). The calculation for the same is as

follows:

Intangible assets = Goodwill + deferred tax asset + reacquired right

= 9139 + 103 + 379

= 9621

Formula for percentage = Net identifiable intangible assets / total consideration * 100

= 9621 / 12124 * 100

= 0.7935 * 100

= 79.35%

11. Comparative analysis of the companies regarding disclosure of the business combination

From the annual report of Baby Bunting Group Ltd and Accent Group it has been

analysed that first company has not mentioned any information regarding business combination

in the report. On the other hand, second entity mentioned detailed information about business

combination in the annual report. Main reason for the same is that Baby Bunting has not

acquired any business during year 2019 but Accent Group acquired different businesses in the

year 2019 (Zhou, 2018). If both the companies will be compared then it could be said that second

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

enterprise has mentioned the details of business combination properly but the first company has

not recorded any information.

CONCLUSION

From the above project report it has been concluded that financial accounting is the

process of recording information of finance related transactions and corporate accounting is a

technique which is used to evaluate financial performance of company on the basis of records.

AASB take part in the IFRS setting process so that effective amendments could be made in the

standards before introducing them in a country. There are various types of business that are

operating business in different nations. These are reporting entity, large and small proprietary.

When a company acquires another business and record information of it in the annual report then

it is known as business combination. The Australian Accounting Standard which is related to it is

AASB 3. All the companies that are acquiring a business during a year are required to make sure

that they have mentioned detailed information regarding various aspects. Some of them are

goodwill, purchase consideration, acquisition cost, net identifiable assets, liabilities and

contingent liabilities.

9

not recorded any information.

CONCLUSION

From the above project report it has been concluded that financial accounting is the

process of recording information of finance related transactions and corporate accounting is a

technique which is used to evaluate financial performance of company on the basis of records.

AASB take part in the IFRS setting process so that effective amendments could be made in the

standards before introducing them in a country. There are various types of business that are

operating business in different nations. These are reporting entity, large and small proprietary.

When a company acquires another business and record information of it in the annual report then

it is known as business combination. The Australian Accounting Standard which is related to it is

AASB 3. All the companies that are acquiring a business during a year are required to make sure

that they have mentioned detailed information regarding various aspects. Some of them are

goodwill, purchase consideration, acquisition cost, net identifiable assets, liabilities and

contingent liabilities.

9

REFERENCES

Books and Journals:

Barker, R., 2019. Corporate natural capital accounting. Oxford Review of Economic Policy.

35(1). pp.68-87.

DAVALLOU, M. and MAHMOODI, M., 2017. Working capital management, corporate

performance, and financial constraints.

Gilala, G., 2017. Financial Accounting in Maritime with SAP FI/CO: SAP Consultant, STEP 1

with Certificate.(Volume 1).

Kowalewski, O., 2016. Corporate governance and corporate performance: financial crisis (2008).

Management Research Review.

Kristanti, F. T. and Herwany, A., 2017. Corporate governance, financial ratios, political risk and

financial distress: A survival analysis. Accounting and Finance Review (AFR) Vol. 2(2).

Nasr, M. A. and Ntim, C. G., 2018. Corporate governance mechanisms and accounting

conservatism: evidence from Egypt. Corporate Governance: The International Journal

of Business in Society.

Roychowdhury, S., Shroff, N. and Verdi, R. S., 2019. The effects of financial reporting and

disclosure on corporate investment: A review. Journal of Accounting and

Economics.68(2-3). p.101246.

Sorensen, D. P. and Miller, S. E., 2017. Financial accounting scandals and the reform of

corporate governance in the United States and in Italy. Corporate Governance: The

International Journal of Business in Society.

Thanh, T. T., 2016. The role of Ethics and Corporate Governance in financial accounting

(Doctoral dissertation, Vietnamese-German University).

Unerman, J., Bebbington, J. and O’dwyer, B., 2018. Corporate reporting and accounting for

externalities. Accounting and business research. 48(5). pp.497-522.

Velte, P., 2019. What do we know about meta-analyses in accounting, auditing, and corporate

governance?. Meditari Accountancy Research.

Warren, C. S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Zhou, H. ed., 2018. The Routledge Companion to Accounting in China. Routledge.

Online

Annual report of Accent Group. 2019. [Online]. Available through:

<file:///home/user/Downloads/Accent%20Group%20Limited%20Annual%20Report

%202019.pdf>

Annual Report of Baby Bunting Group Ltd. 2019. [Online]. Available through:

<https://www.babybunting.com.au/media/wysiwyg/docs/Baby_Bunting_Annual_Report

_-_16_August_2019_-_FINAL.pdf>

10

Books and Journals:

Barker, R., 2019. Corporate natural capital accounting. Oxford Review of Economic Policy.

35(1). pp.68-87.

DAVALLOU, M. and MAHMOODI, M., 2017. Working capital management, corporate

performance, and financial constraints.

Gilala, G., 2017. Financial Accounting in Maritime with SAP FI/CO: SAP Consultant, STEP 1

with Certificate.(Volume 1).

Kowalewski, O., 2016. Corporate governance and corporate performance: financial crisis (2008).

Management Research Review.

Kristanti, F. T. and Herwany, A., 2017. Corporate governance, financial ratios, political risk and

financial distress: A survival analysis. Accounting and Finance Review (AFR) Vol. 2(2).

Nasr, M. A. and Ntim, C. G., 2018. Corporate governance mechanisms and accounting

conservatism: evidence from Egypt. Corporate Governance: The International Journal

of Business in Society.

Roychowdhury, S., Shroff, N. and Verdi, R. S., 2019. The effects of financial reporting and

disclosure on corporate investment: A review. Journal of Accounting and

Economics.68(2-3). p.101246.

Sorensen, D. P. and Miller, S. E., 2017. Financial accounting scandals and the reform of

corporate governance in the United States and in Italy. Corporate Governance: The

International Journal of Business in Society.

Thanh, T. T., 2016. The role of Ethics and Corporate Governance in financial accounting

(Doctoral dissertation, Vietnamese-German University).

Unerman, J., Bebbington, J. and O’dwyer, B., 2018. Corporate reporting and accounting for

externalities. Accounting and business research. 48(5). pp.497-522.

Velte, P., 2019. What do we know about meta-analyses in accounting, auditing, and corporate

governance?. Meditari Accountancy Research.

Warren, C. S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Zhou, H. ed., 2018. The Routledge Companion to Accounting in China. Routledge.

Online

Annual report of Accent Group. 2019. [Online]. Available through:

<file:///home/user/Downloads/Accent%20Group%20Limited%20Annual%20Report

%202019.pdf>

Annual Report of Baby Bunting Group Ltd. 2019. [Online]. Available through:

<https://www.babybunting.com.au/media/wysiwyg/docs/Baby_Bunting_Annual_Report

_-_16_August_2019_-_FINAL.pdf>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.