BA4008QA Business Decision Making: Financial Statement Analysis

VerifiedAdded on 2023/06/15

|12

|2686

|351

Report

AI Summary

This report provides a comprehensive financial analysis of London Ventures, focusing on business decision-making through the lens of financial statements. Task 1 involves the preparation of an income statement and statement of financial position based on the provided trial balance. Task 2 discusses the limitations of the income statement, such as ignoring non-revenue factors, not providing actual costs, and offering only confirmatory value. Task 3 explores the limitations of the balance sheet, including the use of historical costs, exclusion of non-monetary items, and the potential for window dressing. Finally, Task 4 calculates and suggests management strategies for inventory days, trade payable days, and trade receivable days. The report concludes with recommendations for effective management of these key financial metrics to improve London Ventures' overall financial health and decision-making processes. Desklib provides past papers and solved assignments for students.

BA4008QA BUSINESS

DECISION MAKING

DECISION MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1a..........................................................................................................................................3

(a) Preparation of Income Statement for London Ventures........................................................3

Task 1b.............................................................................................................................................4

Statement of financial position as at 31 March 2021 for London Ventures...............................4

TASK 2............................................................................................................................................6

Limitations of Income Statement................................................................................................6

Task 3...............................................................................................................................................7

Limitations of balance sheet or statement of financial position for London Ventures...............7

Task 4...............................................................................................................................................8

(a) Inventory Days......................................................................................................................9

b) Effective management of London Ventures trade payables...................................................9

c) Effective management of London Ventures Trade receivables............................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1a..........................................................................................................................................3

(a) Preparation of Income Statement for London Ventures........................................................3

Task 1b.............................................................................................................................................4

Statement of financial position as at 31 March 2021 for London Ventures...............................4

TASK 2............................................................................................................................................6

Limitations of Income Statement................................................................................................6

Task 3...............................................................................................................................................7

Limitations of balance sheet or statement of financial position for London Ventures...............7

Task 4...............................................................................................................................................8

(a) Inventory Days......................................................................................................................9

b) Effective management of London Ventures trade payables...................................................9

c) Effective management of London Ventures Trade receivables............................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

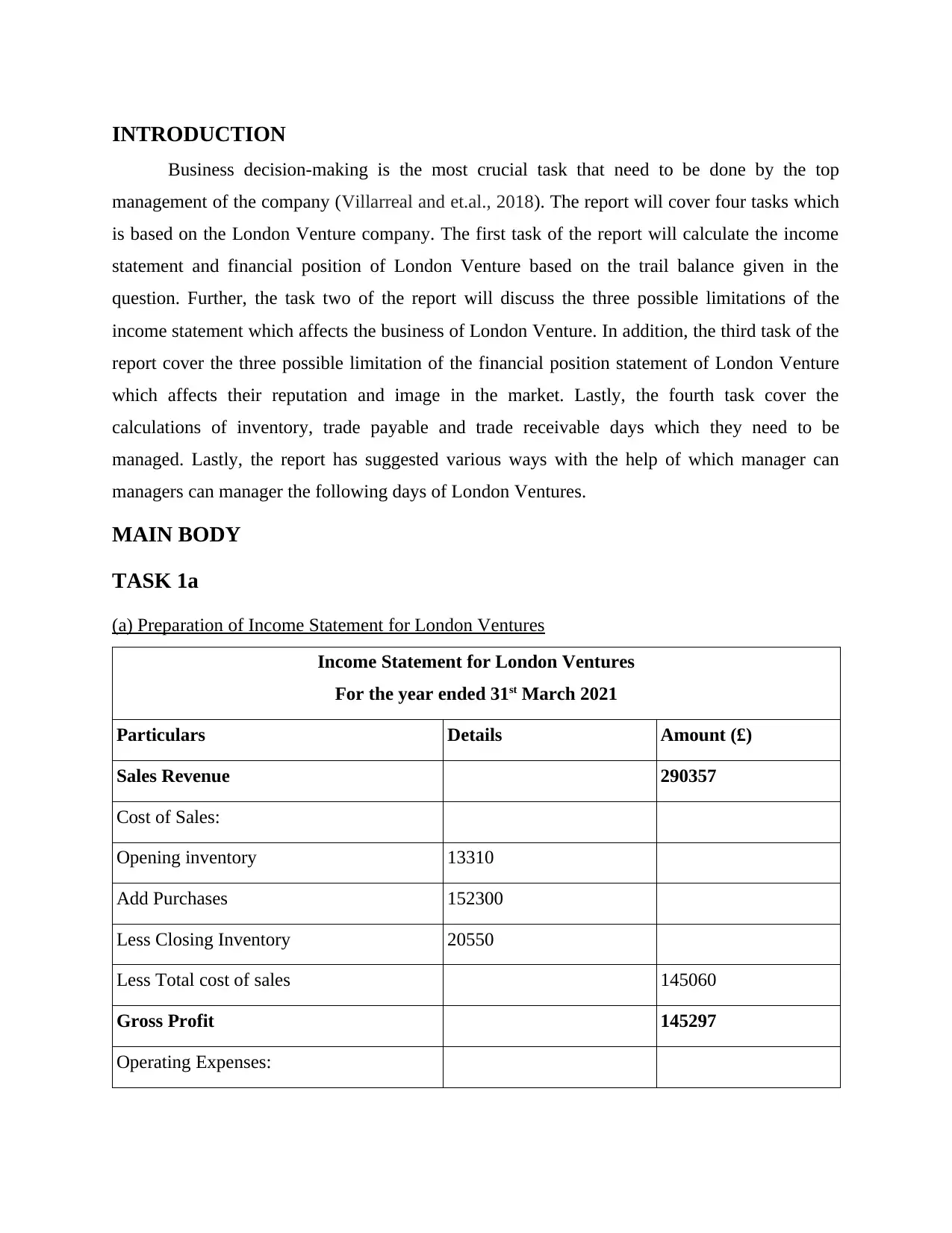

INTRODUCTION

Business decision-making is the most crucial task that need to be done by the top

management of the company (Villarreal and et.al., 2018). The report will cover four tasks which

is based on the London Venture company. The first task of the report will calculate the income

statement and financial position of London Venture based on the trail balance given in the

question. Further, the task two of the report will discuss the three possible limitations of the

income statement which affects the business of London Venture. In addition, the third task of the

report cover the three possible limitation of the financial position statement of London Venture

which affects their reputation and image in the market. Lastly, the fourth task cover the

calculations of inventory, trade payable and trade receivable days which they need to be

managed. Lastly, the report has suggested various ways with the help of which manager can

managers can manager the following days of London Ventures.

MAIN BODY

TASK 1a

(a) Preparation of Income Statement for London Ventures

Income Statement for London Ventures

For the year ended 31st March 2021

Particulars Details Amount (£)

Sales Revenue 290357

Cost of Sales:

Opening inventory 13310

Add Purchases 152300

Less Closing Inventory 20550

Less Total cost of sales 145060

Gross Profit 145297

Operating Expenses:

Business decision-making is the most crucial task that need to be done by the top

management of the company (Villarreal and et.al., 2018). The report will cover four tasks which

is based on the London Venture company. The first task of the report will calculate the income

statement and financial position of London Venture based on the trail balance given in the

question. Further, the task two of the report will discuss the three possible limitations of the

income statement which affects the business of London Venture. In addition, the third task of the

report cover the three possible limitation of the financial position statement of London Venture

which affects their reputation and image in the market. Lastly, the fourth task cover the

calculations of inventory, trade payable and trade receivable days which they need to be

managed. Lastly, the report has suggested various ways with the help of which manager can

managers can manager the following days of London Ventures.

MAIN BODY

TASK 1a

(a) Preparation of Income Statement for London Ventures

Income Statement for London Ventures

For the year ended 31st March 2021

Particulars Details Amount (£)

Sales Revenue 290357

Cost of Sales:

Opening inventory 13310

Add Purchases 152300

Less Closing Inventory 20550

Less Total cost of sales 145060

Gross Profit 145297

Operating Expenses:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

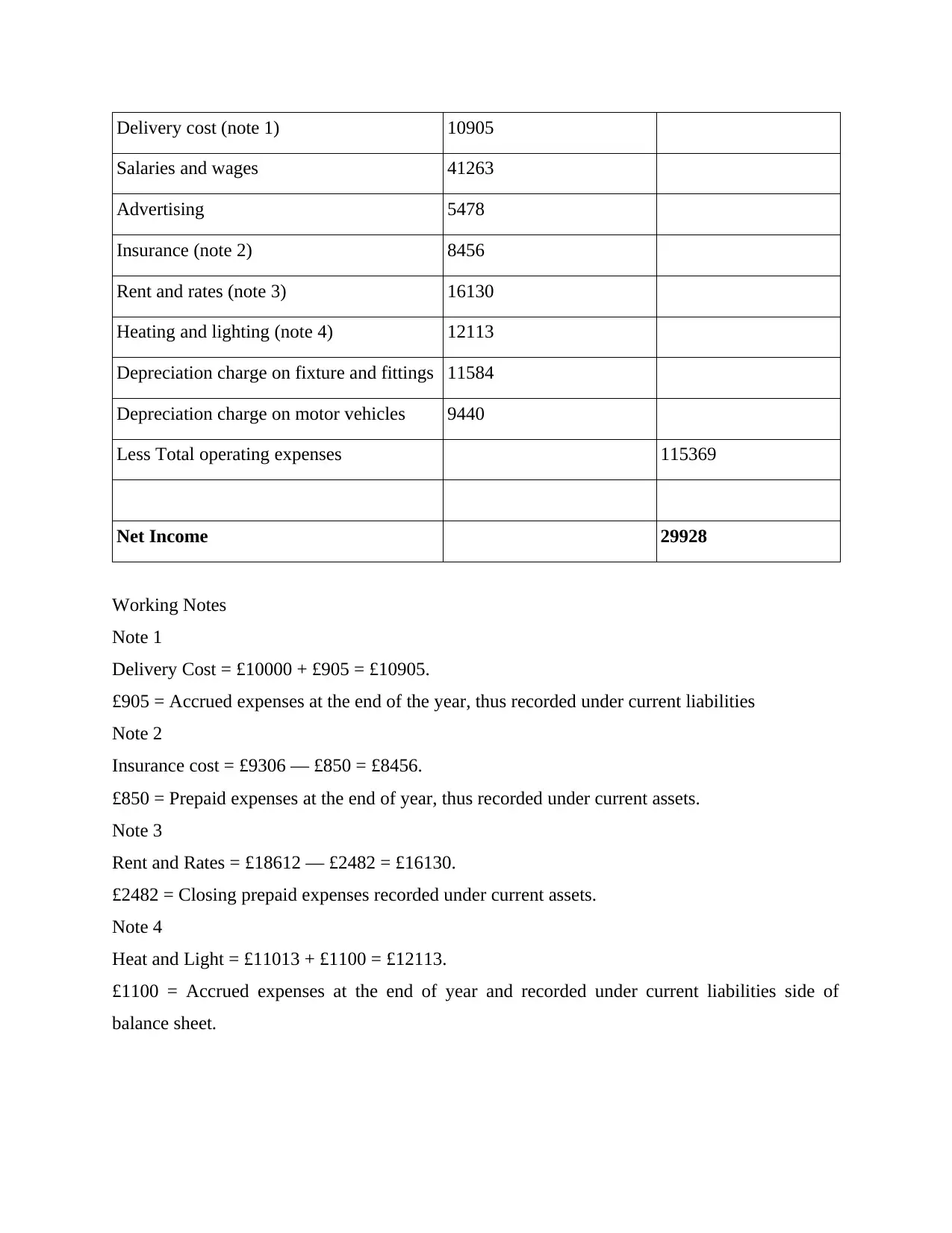

Delivery cost (note 1) 10905

Salaries and wages 41263

Advertising 5478

Insurance (note 2) 8456

Rent and rates (note 3) 16130

Heating and lighting (note 4) 12113

Depreciation charge on fixture and fittings 11584

Depreciation charge on motor vehicles 9440

Less Total operating expenses 115369

Net Income 29928

Working Notes

Note 1

Delivery Cost = £10000 + £905 = £10905.

£905 = Accrued expenses at the end of the year, thus recorded under current liabilities

Note 2

Insurance cost = £9306 — £850 = £8456.

£850 = Prepaid expenses at the end of year, thus recorded under current assets.

Note 3

Rent and Rates = £18612 — £2482 = £16130.

£2482 = Closing prepaid expenses recorded under current assets.

Note 4

Heat and Light = £11013 + £1100 = £12113.

£1100 = Accrued expenses at the end of year and recorded under current liabilities side of

balance sheet.

Salaries and wages 41263

Advertising 5478

Insurance (note 2) 8456

Rent and rates (note 3) 16130

Heating and lighting (note 4) 12113

Depreciation charge on fixture and fittings 11584

Depreciation charge on motor vehicles 9440

Less Total operating expenses 115369

Net Income 29928

Working Notes

Note 1

Delivery Cost = £10000 + £905 = £10905.

£905 = Accrued expenses at the end of the year, thus recorded under current liabilities

Note 2

Insurance cost = £9306 — £850 = £8456.

£850 = Prepaid expenses at the end of year, thus recorded under current assets.

Note 3

Rent and Rates = £18612 — £2482 = £16130.

£2482 = Closing prepaid expenses recorded under current assets.

Note 4

Heat and Light = £11013 + £1100 = £12113.

£1100 = Accrued expenses at the end of year and recorded under current liabilities side of

balance sheet.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

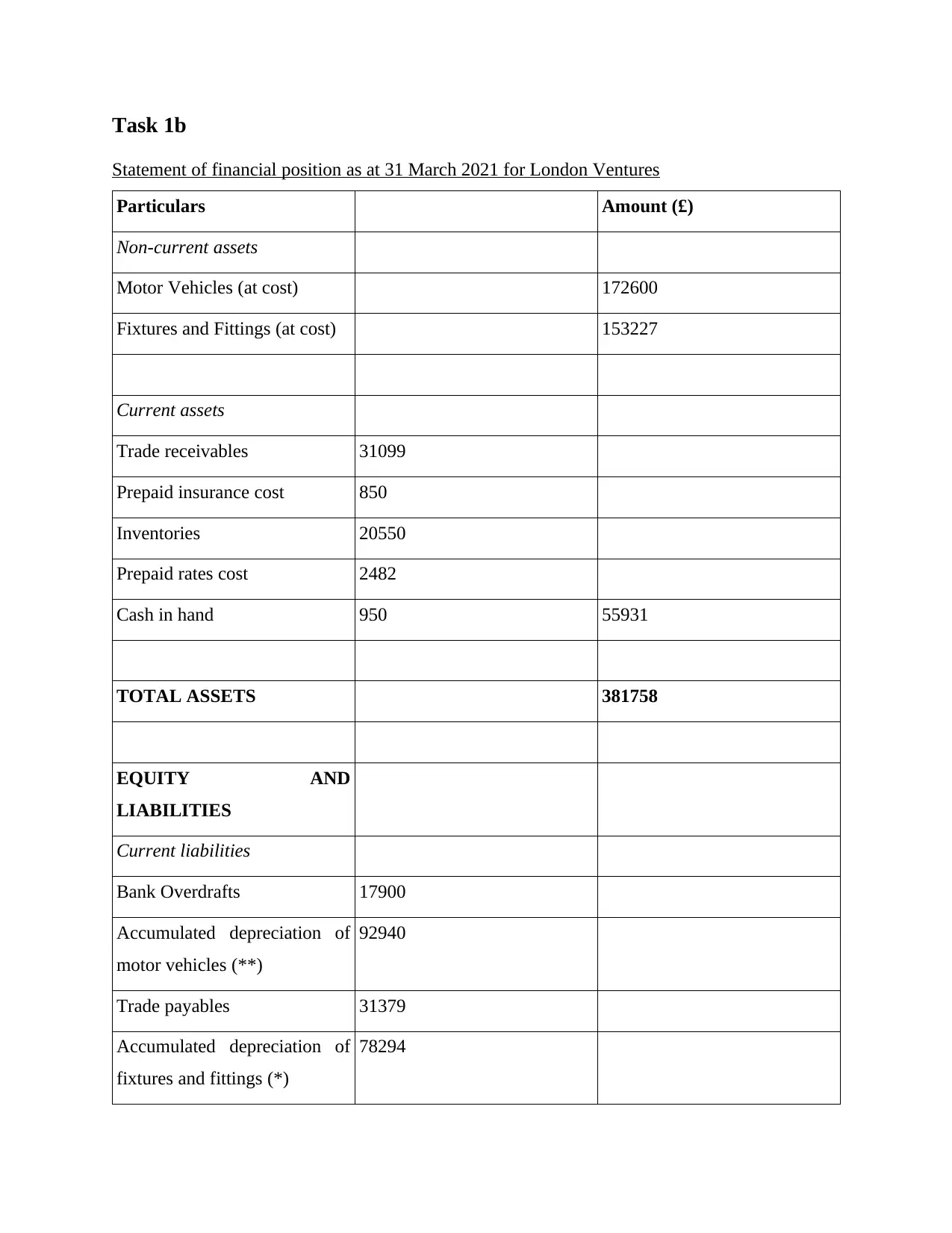

Task 1b

Statement of financial position as at 31 March 2021 for London Ventures

Particulars Amount (£)

Non-current assets

Motor Vehicles (at cost) 172600

Fixtures and Fittings (at cost) 153227

Current assets

Trade receivables 31099

Prepaid insurance cost 850

Inventories 20550

Prepaid rates cost 2482

Cash in hand 950 55931

TOTAL ASSETS 381758

EQUITY AND

LIABILITIES

Current liabilities

Bank Overdrafts 17900

Accumulated depreciation of

motor vehicles (**)

92940

Trade payables 31379

Accumulated depreciation of

fixtures and fittings (*)

78294

Statement of financial position as at 31 March 2021 for London Ventures

Particulars Amount (£)

Non-current assets

Motor Vehicles (at cost) 172600

Fixtures and Fittings (at cost) 153227

Current assets

Trade receivables 31099

Prepaid insurance cost 850

Inventories 20550

Prepaid rates cost 2482

Cash in hand 950 55931

TOTAL ASSETS 381758

EQUITY AND

LIABILITIES

Current liabilities

Bank Overdrafts 17900

Accumulated depreciation of

motor vehicles (**)

92940

Trade payables 31379

Accumulated depreciation of

fixtures and fittings (*)

78294

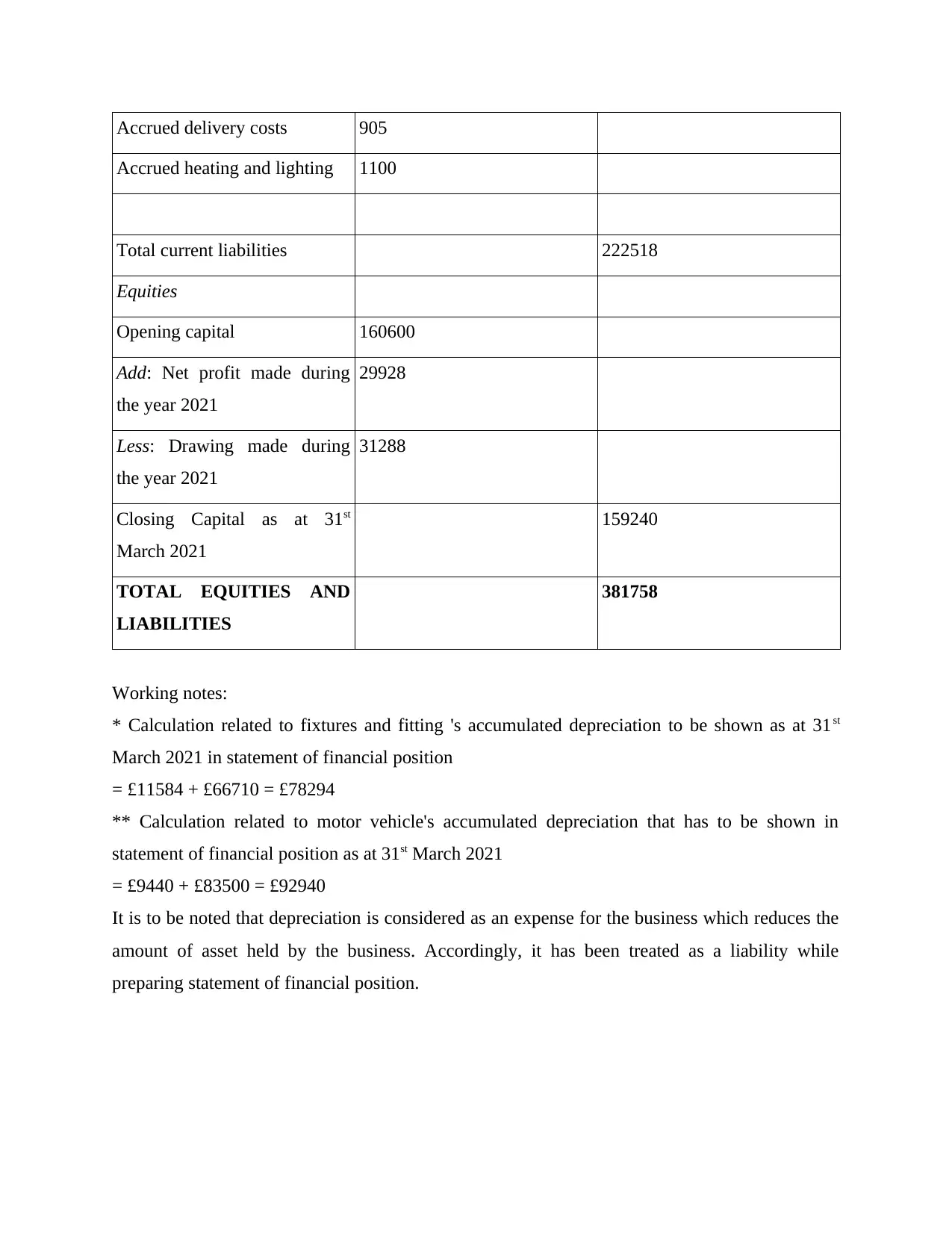

Accrued delivery costs 905

Accrued heating and lighting 1100

Total current liabilities 222518

Equities

Opening capital 160600

Add: Net profit made during

the year 2021

29928

Less: Drawing made during

the year 2021

31288

Closing Capital as at 31st

March 2021

159240

TOTAL EQUITIES AND

LIABILITIES

381758

Working notes:

* Calculation related to fixtures and fitting 's accumulated depreciation to be shown as at 31st

March 2021 in statement of financial position

= £11584 + £66710 = £78294

** Calculation related to motor vehicle's accumulated depreciation that has to be shown in

statement of financial position as at 31st March 2021

= £9440 + £83500 = £92940

It is to be noted that depreciation is considered as an expense for the business which reduces the

amount of asset held by the business. Accordingly, it has been treated as a liability while

preparing statement of financial position.

Accrued heating and lighting 1100

Total current liabilities 222518

Equities

Opening capital 160600

Add: Net profit made during

the year 2021

29928

Less: Drawing made during

the year 2021

31288

Closing Capital as at 31st

March 2021

159240

TOTAL EQUITIES AND

LIABILITIES

381758

Working notes:

* Calculation related to fixtures and fitting 's accumulated depreciation to be shown as at 31st

March 2021 in statement of financial position

= £11584 + £66710 = £78294

** Calculation related to motor vehicle's accumulated depreciation that has to be shown in

statement of financial position as at 31st March 2021

= £9440 + £83500 = £92940

It is to be noted that depreciation is considered as an expense for the business which reduces the

amount of asset held by the business. Accordingly, it has been treated as a liability while

preparing statement of financial position.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

Limitations of Income Statement

The three possible limitations of income statement that affects the business of London

Ventures are as follows: Ignores non-revenue factors: The one and most significant disadvantage of statement of

income is that it considers only those data which impact the revenue and wages. It means

it does not consider the qualitative factors which affects the data recorded in income

statement. For example, the income statement of London Ventures reflect the salaries and

wages paid to employees of the company but does not reflect the factors such as how

such wages are determined by the company. Beside this, the income statement also not

reflect the ways through which they earn the returns or profit from its customers despite

being declaring the sales revenue and profits. It is because this is not in the monetary

term (Aanestad and Szekely, 2021). Thus, this is one of the cons of income statement

which sometime cause difficulty for the manager of London venture to understand that

how such amount is determined by the accountant. It will also affect the business

decision-making process of financial managers. Does not Provide actual cost: Another disadvantage of the income statement is that it

will not provide the actual cost information. For example, London Ventures buys the

motor vehicles which is recorded in balance sheet but its depreciation expenses is

recorded in the income statement. In order to compute the depreciation expenses, the

company estimate the life of the assets in advance only. But in reality, the assets last for

longer than what is estimated by the company (Lee, 2021). So, it can be said that the

amount of depreciation expenses shown in the income statement of the London Venture

is not actual. In simple term, it means that the data represented by the income statement

of the company does not provide actual cost of the assets rather than it provides a fair

estimation of the expenses.

Provides Confirmatory value: Also, the income statement generally provides

confirmatory value which is disadvantage of it. This means that income statement is

basically prepared by the London Venture after the auditing of all the financial data

recorded by them. So, it is a limitation that the company can easily manipulate the

income statement which leads to wrong decision-making by the users of FS. The

Limitations of Income Statement

The three possible limitations of income statement that affects the business of London

Ventures are as follows: Ignores non-revenue factors: The one and most significant disadvantage of statement of

income is that it considers only those data which impact the revenue and wages. It means

it does not consider the qualitative factors which affects the data recorded in income

statement. For example, the income statement of London Ventures reflect the salaries and

wages paid to employees of the company but does not reflect the factors such as how

such wages are determined by the company. Beside this, the income statement also not

reflect the ways through which they earn the returns or profit from its customers despite

being declaring the sales revenue and profits. It is because this is not in the monetary

term (Aanestad and Szekely, 2021). Thus, this is one of the cons of income statement

which sometime cause difficulty for the manager of London venture to understand that

how such amount is determined by the accountant. It will also affect the business

decision-making process of financial managers. Does not Provide actual cost: Another disadvantage of the income statement is that it

will not provide the actual cost information. For example, London Ventures buys the

motor vehicles which is recorded in balance sheet but its depreciation expenses is

recorded in the income statement. In order to compute the depreciation expenses, the

company estimate the life of the assets in advance only. But in reality, the assets last for

longer than what is estimated by the company (Lee, 2021). So, it can be said that the

amount of depreciation expenses shown in the income statement of the London Venture

is not actual. In simple term, it means that the data represented by the income statement

of the company does not provide actual cost of the assets rather than it provides a fair

estimation of the expenses.

Provides Confirmatory value: Also, the income statement generally provides

confirmatory value which is disadvantage of it. This means that income statement is

basically prepared by the London Venture after the auditing of all the financial data

recorded by them. So, it is a limitation that the company can easily manipulate the

income statement which leads to wrong decision-making by the users of FS. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manipulation of data in the statement is done by the individuals with ill intentions which

affects the overall profitability and reputation of the business in the market (Ochoa-

Hernandez and et.al., 2020). At that time, it is the duty of the London Venture that they

should implement the proper internal control system within the business. The internal

control systems helps the company to identify the material misstatement in income

statement because of either fraud or error.

Task 3

Limitations of balance sheet or statement of financial position for London Ventures

Balance sheet or statement of financial position is helpful for both management and investors in

making financial decision and investment decision respectively as it indicates business financial

position at a particular date on which it has been prepared (Kahn and Baum, 2020). However,

there are certain limitations of statement of financial position as well due to which the financial

information provided it is not considered to be fruitful for decision – making. Some of these

limitations have been listed as follows:

Assets are shown on historical costs: In statement of financial position, the fixed assets of the

business are shown at historical costs after reducing the amount of depreciation for the period

and no consideration has been given to the current market value of assets. Thus, the statements

prepared on such basis are deemed as not indicating true asset's value. Due to this reason,

statement of financial position is being criticized on the ground that it doesn't reflect true value of

the business's assets (Robison and Barry, 2021). Also, valuation of current assets are done on the

basis of certain estimations which results in making this financial statement invalid to reflect

actual financial position of a concern. Furthermore, valuation of intangible assets is done on

imaginary basis which have no association with market value and indicates that business is quite

overvalued.

No inclusion of non – monetary items: Skills, honesty, loyalty and intelligence of company's

staff is being regarded as the biggest asset for any business. However, it cannot be measured in

terms of money and accordingly, it is the biggest limitation of statement of financial position that

it takes into consideration only those items which can be measured in terms of money. Therefore,

affects the overall profitability and reputation of the business in the market (Ochoa-

Hernandez and et.al., 2020). At that time, it is the duty of the London Venture that they

should implement the proper internal control system within the business. The internal

control systems helps the company to identify the material misstatement in income

statement because of either fraud or error.

Task 3

Limitations of balance sheet or statement of financial position for London Ventures

Balance sheet or statement of financial position is helpful for both management and investors in

making financial decision and investment decision respectively as it indicates business financial

position at a particular date on which it has been prepared (Kahn and Baum, 2020). However,

there are certain limitations of statement of financial position as well due to which the financial

information provided it is not considered to be fruitful for decision – making. Some of these

limitations have been listed as follows:

Assets are shown on historical costs: In statement of financial position, the fixed assets of the

business are shown at historical costs after reducing the amount of depreciation for the period

and no consideration has been given to the current market value of assets. Thus, the statements

prepared on such basis are deemed as not indicating true asset's value. Due to this reason,

statement of financial position is being criticized on the ground that it doesn't reflect true value of

the business's assets (Robison and Barry, 2021). Also, valuation of current assets are done on the

basis of certain estimations which results in making this financial statement invalid to reflect

actual financial position of a concern. Furthermore, valuation of intangible assets is done on

imaginary basis which have no association with market value and indicates that business is quite

overvalued.

No inclusion of non – monetary items: Skills, honesty, loyalty and intelligence of company's

staff is being regarded as the biggest asset for any business. However, it cannot be measured in

terms of money and accordingly, it is the biggest limitation of statement of financial position that

it takes into consideration only those items which can be measured in terms of money. Therefore,

such biggest assets of the business remain unrecognised while preparing company's balance sheet

as these assets cannot be measured in monetary terms.

Window dressing may be possible: Financial statements are generally affected from window

dressing such as manipulation in sales amount, cash balances, etc. to indicate better financial

position among investors and creditors to secure additional capital amount easily (Bandiyono,

2020). This leads to misappropriation within statement of financial position and makes it uses

and application within all form of decision – making limited.

Task 4

as these assets cannot be measured in monetary terms.

Window dressing may be possible: Financial statements are generally affected from window

dressing such as manipulation in sales amount, cash balances, etc. to indicate better financial

position among investors and creditors to secure additional capital amount easily (Bandiyono,

2020). This leads to misappropriation within statement of financial position and makes it uses

and application within all form of decision – making limited.

Task 4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(a) Inventory Days

Formula = Total Inventory / Cost of goods sold * 365 days

= £20550 / 145060 × 365 days = 52 days

Management of inventory days

On the basis of above calculations it is analysed that London Venture holds its stocks for

longer span of time. This also denotes that the capability of the company to sold its stock in the

market is poor. In order to manage it and further improve it, the company need to focus on their

stocks purchasing and order. The company have to implement the economic order quantity

technique which involve the identification of optimal quantity of raw material which is required

at a single point of time, where both holding cost and ordering cost is equal to each other. Also,

effective marketing is also one of the best strategy which helps the company in managing its

inventory holding day because it is crucial for the company that they should manage it. If they

fail in doing so, then it may lead to spoilage of stock in the warehouse which further cause heavy

loss to the company (Aljaaidi and Bagais, 2020).

b) Effective management of London Ventures trade payables

Calculation of trade payables days

Trade payables days = Trade payables / Cost of sales * 365

= £31379 / £145060 * 365 = 78.95 days

From the result obtained for trade payables days, it can be seen that company is taking

approximately 79 days to make payment to its suppliers for the credit purchases made by it

which is considered to be long duration or credit period. This ratio can be improved in the

following ways:

Negotiation of better terms with creditors by developing good relationship with them

which is helpful in managing payments to them. This is done in the way where business

ask for such terms where they can make matching payments to their suppliers on

receiving of payment from their customers or debtors (Handoyo and Maulana, 2019).

Setting timely reminders for invoices on the basis of their becoming due which would

help London Ventures in making timely payment to their supplier without forgetting or

missing.

Formula = Total Inventory / Cost of goods sold * 365 days

= £20550 / 145060 × 365 days = 52 days

Management of inventory days

On the basis of above calculations it is analysed that London Venture holds its stocks for

longer span of time. This also denotes that the capability of the company to sold its stock in the

market is poor. In order to manage it and further improve it, the company need to focus on their

stocks purchasing and order. The company have to implement the economic order quantity

technique which involve the identification of optimal quantity of raw material which is required

at a single point of time, where both holding cost and ordering cost is equal to each other. Also,

effective marketing is also one of the best strategy which helps the company in managing its

inventory holding day because it is crucial for the company that they should manage it. If they

fail in doing so, then it may lead to spoilage of stock in the warehouse which further cause heavy

loss to the company (Aljaaidi and Bagais, 2020).

b) Effective management of London Ventures trade payables

Calculation of trade payables days

Trade payables days = Trade payables / Cost of sales * 365

= £31379 / £145060 * 365 = 78.95 days

From the result obtained for trade payables days, it can be seen that company is taking

approximately 79 days to make payment to its suppliers for the credit purchases made by it

which is considered to be long duration or credit period. This ratio can be improved in the

following ways:

Negotiation of better terms with creditors by developing good relationship with them

which is helpful in managing payments to them. This is done in the way where business

ask for such terms where they can make matching payments to their suppliers on

receiving of payment from their customers or debtors (Handoyo and Maulana, 2019).

Setting timely reminders for invoices on the basis of their becoming due which would

help London Ventures in making timely payment to their supplier without forgetting or

missing.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c) Effective management of London Ventures Trade receivables

Calculation of trade receivables days

Trade receivables days = Trade receivables / Revenue from sales * 365

= £31099 / £290357 * 365 = 39.09 days

From the above ratio indicating trade receivables days, it can be determined that

customers of London Ventures are taking approximately 39 days to make payment to them

which is less than the ideal trade receivables days indicates that company's short term liquidity

position would be quite good at it is getting timely payment from its customers. Alternatively, it

indicates that company will take 39 days to clear its trade receivables (Surachyati, Abubakar and

Daulay, 2019). There are different ways in which the company can manage its trade receivables

days effectively, such as the following:

Business must understand the payment history of their client before extending credit to

them, so that reasonability of credit extension can be determined easily.

Applying techniques for getting payments earlier from customers such as incentivize

customers with discounts and charging interest on outstanding amount.

CONCLUSION

From the above report it has been concluded that financial statements play a very

important role in making decisions related to financing, investment and appropriation of profits.

In this report, it has been evaluation that despite of various benefits there are certain limitations

of these financial statements due assumptions and estimations made while preparing it. At last,

various ways in which business can manage its trade payables, receivables and inventory has

been discussed.

Calculation of trade receivables days

Trade receivables days = Trade receivables / Revenue from sales * 365

= £31099 / £290357 * 365 = 39.09 days

From the above ratio indicating trade receivables days, it can be determined that

customers of London Ventures are taking approximately 39 days to make payment to them

which is less than the ideal trade receivables days indicates that company's short term liquidity

position would be quite good at it is getting timely payment from its customers. Alternatively, it

indicates that company will take 39 days to clear its trade receivables (Surachyati, Abubakar and

Daulay, 2019). There are different ways in which the company can manage its trade receivables

days effectively, such as the following:

Business must understand the payment history of their client before extending credit to

them, so that reasonability of credit extension can be determined easily.

Applying techniques for getting payments earlier from customers such as incentivize

customers with discounts and charging interest on outstanding amount.

CONCLUSION

From the above report it has been concluded that financial statements play a very

important role in making decisions related to financing, investment and appropriation of profits.

In this report, it has been evaluation that despite of various benefits there are certain limitations

of these financial statements due assumptions and estimations made while preparing it. At last,

various ways in which business can manage its trade payables, receivables and inventory has

been discussed.

REFERENCES

Aanestad, H. and Szekely, N., 2021. Understanding the Norwegian additive manufacturing

market: Its attractive aspects, limitations, potential and future opportunities within a

circular framework (Master's thesis, uis).

Aljaaidi, K. and Bagais, O., 2020. Days inventory outstanding and firm performance: Empirical

investigation from manufacturers. Accounting. 6(6). pp.1111-1116.

Bandiyono, A., 2020. Budget Participation and Internal Control for Better Quality Financial

Statements. Jurnal Akuntansi, 24(2), pp.313-327.

Handoyo, S. and Maulana, E. D., 2019. Determinants of Audit Report Lag of Financial

Statements in Banking Sector. Jurnal Manajemen, Strategi Bisnis dan Kewirausahaan.

Doi, 10.

Kahn, M. J. and Baum, N., 2020. Basic accounting and interpretation of financial statements.

In The Business Basics of Building and Managing a Healthcare Practice (pp. 13-18).

Springer, Cham.

Lee, H., 2021. Limitations of Insurance as a Risk Financing Tool. In Risk Management (pp. 105-

117). Springer, Singapore.

Ochoa-Hernandez and et.al., 2020. Emergent groin hernia repair at a County Hospital in

Guatemala: patient-related issues vs. health care system limitations. Hernia. 24(3). pp.625-

632.

Robison, L. J. and Barry, P. J., 2021. Coordinated financial statements: what-is, what-if and how-

much questions. Agricultural Finance Review.

Surachyati, E., Abubakar, E. and Daulay, M., 2019. Analysis of Factors That Affect the

Timeliness of Submission of the Financial Statements on Transportation Companies in

Indonesia Stock Exchange. International Journal of Research and Review, 6(1), pp.190-

201.

Villarreal, B. and et.al., 2018. Reduce slow moving inventory of convenience stores: A case

study. management.

Aanestad, H. and Szekely, N., 2021. Understanding the Norwegian additive manufacturing

market: Its attractive aspects, limitations, potential and future opportunities within a

circular framework (Master's thesis, uis).

Aljaaidi, K. and Bagais, O., 2020. Days inventory outstanding and firm performance: Empirical

investigation from manufacturers. Accounting. 6(6). pp.1111-1116.

Bandiyono, A., 2020. Budget Participation and Internal Control for Better Quality Financial

Statements. Jurnal Akuntansi, 24(2), pp.313-327.

Handoyo, S. and Maulana, E. D., 2019. Determinants of Audit Report Lag of Financial

Statements in Banking Sector. Jurnal Manajemen, Strategi Bisnis dan Kewirausahaan.

Doi, 10.

Kahn, M. J. and Baum, N., 2020. Basic accounting and interpretation of financial statements.

In The Business Basics of Building and Managing a Healthcare Practice (pp. 13-18).

Springer, Cham.

Lee, H., 2021. Limitations of Insurance as a Risk Financing Tool. In Risk Management (pp. 105-

117). Springer, Singapore.

Ochoa-Hernandez and et.al., 2020. Emergent groin hernia repair at a County Hospital in

Guatemala: patient-related issues vs. health care system limitations. Hernia. 24(3). pp.625-

632.

Robison, L. J. and Barry, P. J., 2021. Coordinated financial statements: what-is, what-if and how-

much questions. Agricultural Finance Review.

Surachyati, E., Abubakar, E. and Daulay, M., 2019. Analysis of Factors That Affect the

Timeliness of Submission of the Financial Statements on Transportation Companies in

Indonesia Stock Exchange. International Journal of Research and Review, 6(1), pp.190-

201.

Villarreal, B. and et.al., 2018. Reduce slow moving inventory of convenience stores: A case

study. management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.