Comprehensive Financial Report: Accounting for Business Decisions

VerifiedAdded on 2023/06/08

|13

|2110

|469

Report

AI Summary

This report provides a detailed analysis of accounting for business decisions, covering various aspects such as bank reconciliation, inventory management using the FIFO method, and depreciation calculations. It includes the preparation of a bank reconciliation statement for Energy Boost, journal entries for specific transactions, and the calculation of ending inventory and cost of sales using the FIFO costing method. The report also differentiates between perpetual and periodic inventory systems and addresses the recording of equipment purchases, accumulated depreciation using both straight-line and diminishing balance methods, and the sale of machinery. Furthermore, it presents adjusting entries at the end of the accounting period and discusses closing entries, contrasting the treatment in a sole proprietorship versus a company structure. This document is available on Desklib, which provides a platform for students to access solved assignments and past papers.

ACCOUNTING FOR

BUSINESS DECISIONS

BUSINESS DECISIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1........................................................................................................................................2

(a) Preparation of bank reconciliation statement for Energy Boost at 31st May 2022.................2

(b) Reason behind the preparation of bank reconciliation...........................................................3

QUESTION 2..................................................................................................................................3

Question 3........................................................................................................................................4

(a) Calculation of ending inventory and cost of sales for the month of May using the FIFO

costing method.............................................................................................................................4

(b) Difference between Perpetual and Periodic Inventory system..............................................6

QUESTION 4..................................................................................................................................7

Question 5........................................................................................................................................9

Preparation of adjusting entry at the end of the accounting period.............................................9

QUESTION 6..................................................................................................................................9

REFERENCES..............................................................................................................................11

1

Question 1........................................................................................................................................2

(a) Preparation of bank reconciliation statement for Energy Boost at 31st May 2022.................2

(b) Reason behind the preparation of bank reconciliation...........................................................3

QUESTION 2..................................................................................................................................3

Question 3........................................................................................................................................4

(a) Calculation of ending inventory and cost of sales for the month of May using the FIFO

costing method.............................................................................................................................4

(b) Difference between Perpetual and Periodic Inventory system..............................................6

QUESTION 4..................................................................................................................................7

Question 5........................................................................................................................................9

Preparation of adjusting entry at the end of the accounting period.............................................9

QUESTION 6..................................................................................................................................9

REFERENCES..............................................................................................................................11

1

Question 1

(a) Preparation of bank reconciliation statement for Energy Boost at 31st May 2022

Particulars Amount $ Amount $

Credit Balance as per bank

statement as at 31st May (A)

141624

Add:

Deposit not reflected on bank

statement

17556

Service charge on bank

statement but not recorded in

cash book

210

Dishonoured cheque not

recorded in cash book

5460

Total (B) 23226

Less:

Unpresented Cheques at 31st

May

52370

Interest earned on bank

account directly recorded in

bank statement

105

Cheques for insurance

expenses of $7520 incorrectly

recorded in books as $8275

755

Electronic transfer from

customer directly to bank

account

5410

Total (C) 58640

Debit Balance as per cash at

bank account in Energy boost

141624 + 26226 - 58640 106210

2

(a) Preparation of bank reconciliation statement for Energy Boost at 31st May 2022

Particulars Amount $ Amount $

Credit Balance as per bank

statement as at 31st May (A)

141624

Add:

Deposit not reflected on bank

statement

17556

Service charge on bank

statement but not recorded in

cash book

210

Dishonoured cheque not

recorded in cash book

5460

Total (B) 23226

Less:

Unpresented Cheques at 31st

May

52370

Interest earned on bank

account directly recorded in

bank statement

105

Cheques for insurance

expenses of $7520 incorrectly

recorded in books as $8275

755

Electronic transfer from

customer directly to bank

account

5410

Total (C) 58640

Debit Balance as per cash at

bank account in Energy boost

141624 + 26226 - 58640 106210

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as at 31st May (A) + (B) – (C)

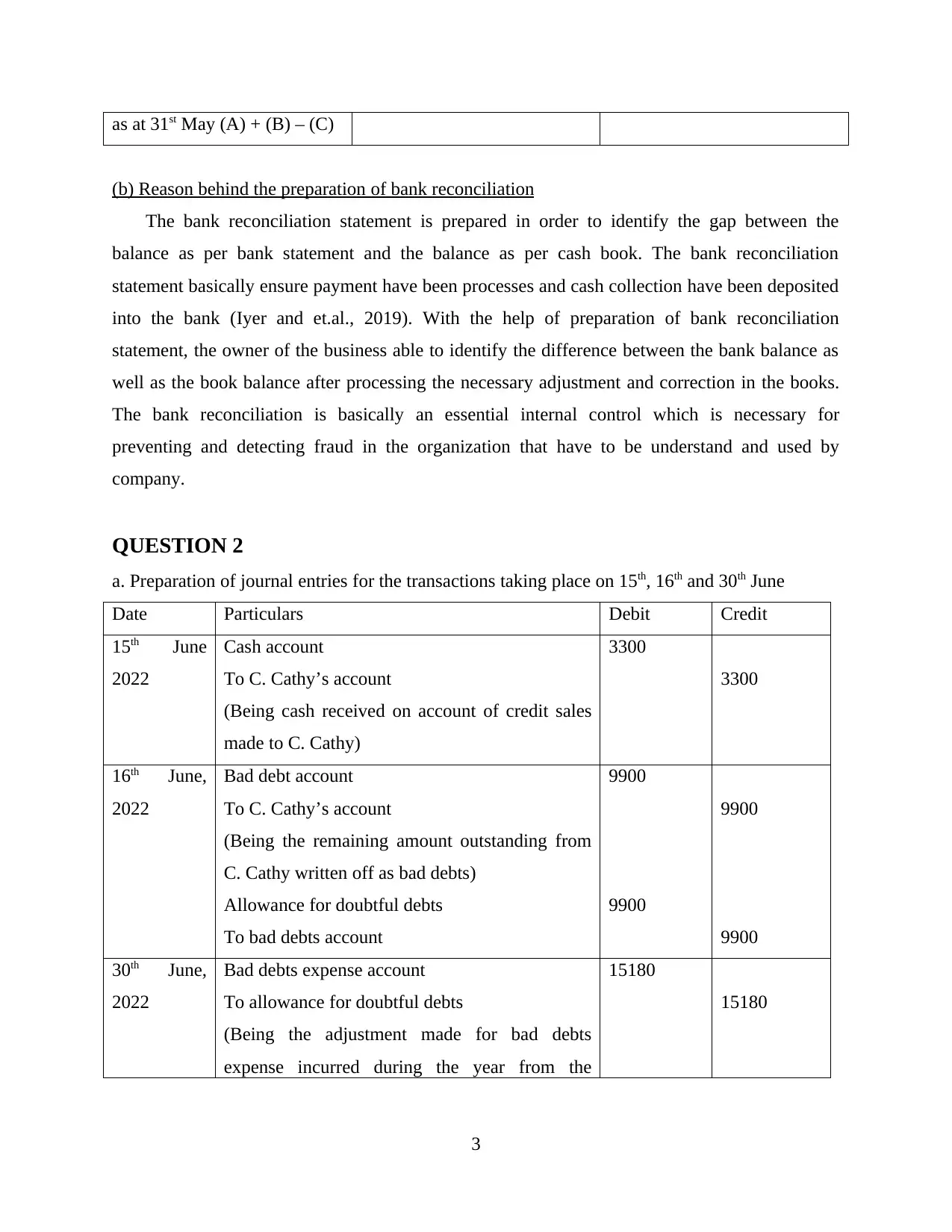

(b) Reason behind the preparation of bank reconciliation

The bank reconciliation statement is prepared in order to identify the gap between the

balance as per bank statement and the balance as per cash book. The bank reconciliation

statement basically ensure payment have been processes and cash collection have been deposited

into the bank (Iyer and et.al., 2019). With the help of preparation of bank reconciliation

statement, the owner of the business able to identify the difference between the bank balance as

well as the book balance after processing the necessary adjustment and correction in the books.

The bank reconciliation is basically an essential internal control which is necessary for

preventing and detecting fraud in the organization that have to be understand and used by

company.

QUESTION 2

a. Preparation of journal entries for the transactions taking place on 15th, 16th and 30th June

Date Particulars Debit Credit

15th June

2022

Cash account

To C. Cathy’s account

(Being cash received on account of credit sales

made to C. Cathy)

3300

3300

16th June,

2022

Bad debt account

To C. Cathy’s account

(Being the remaining amount outstanding from

C. Cathy written off as bad debts)

Allowance for doubtful debts

To bad debts account

9900

9900

9900

9900

30th June,

2022

Bad debts expense account

To allowance for doubtful debts

(Being the adjustment made for bad debts

expense incurred during the year from the

15180

15180

3

(b) Reason behind the preparation of bank reconciliation

The bank reconciliation statement is prepared in order to identify the gap between the

balance as per bank statement and the balance as per cash book. The bank reconciliation

statement basically ensure payment have been processes and cash collection have been deposited

into the bank (Iyer and et.al., 2019). With the help of preparation of bank reconciliation

statement, the owner of the business able to identify the difference between the bank balance as

well as the book balance after processing the necessary adjustment and correction in the books.

The bank reconciliation is basically an essential internal control which is necessary for

preventing and detecting fraud in the organization that have to be understand and used by

company.

QUESTION 2

a. Preparation of journal entries for the transactions taking place on 15th, 16th and 30th June

Date Particulars Debit Credit

15th June

2022

Cash account

To C. Cathy’s account

(Being cash received on account of credit sales

made to C. Cathy)

3300

3300

16th June,

2022

Bad debt account

To C. Cathy’s account

(Being the remaining amount outstanding from

C. Cathy written off as bad debts)

Allowance for doubtful debts

To bad debts account

9900

9900

9900

9900

30th June,

2022

Bad debts expense account

To allowance for doubtful debts

(Being the adjustment made for bad debts

expense incurred during the year from the

15180

15180

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

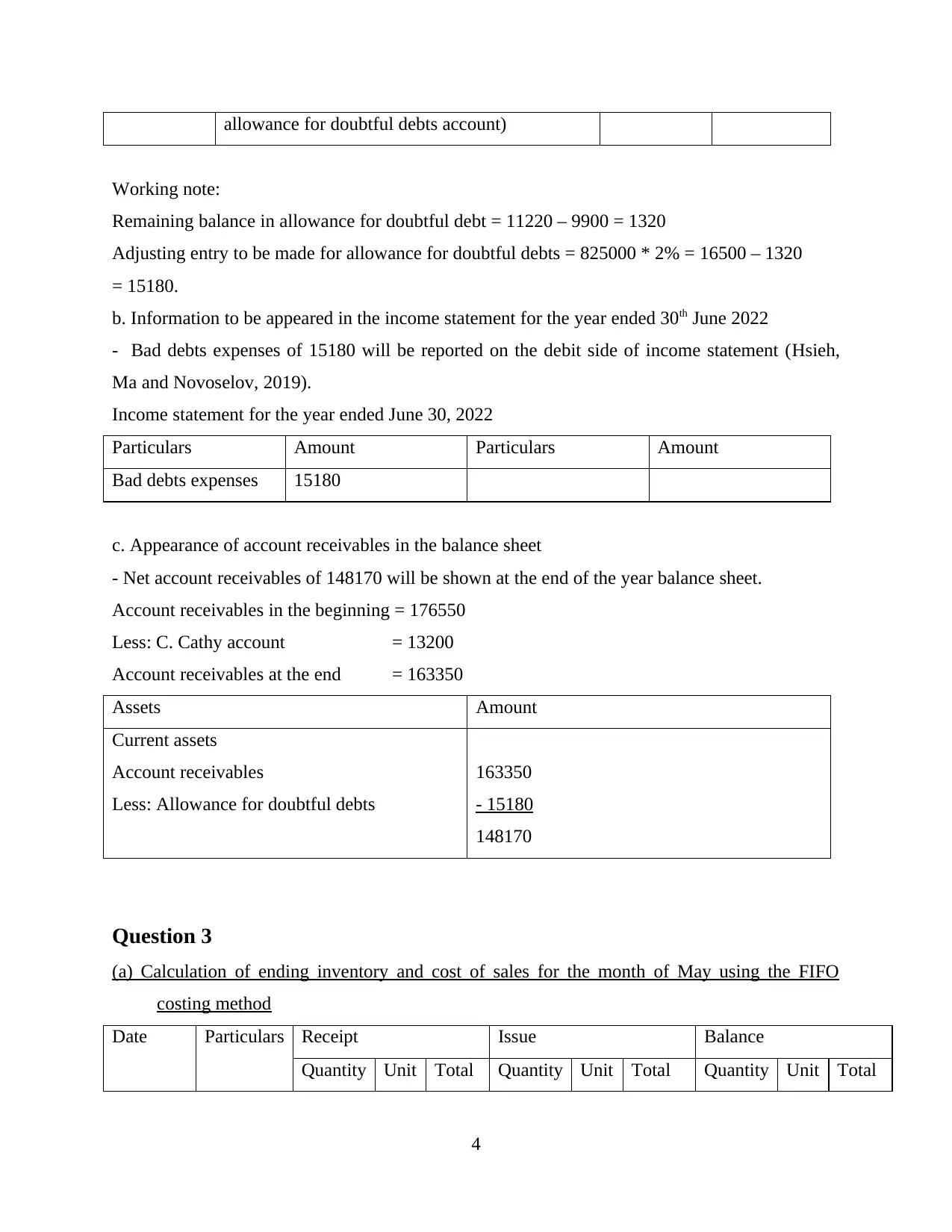

allowance for doubtful debts account)

Working note:

Remaining balance in allowance for doubtful debt = 11220 – 9900 = 1320

Adjusting entry to be made for allowance for doubtful debts = 825000 * 2% = 16500 – 1320

= 15180.

b. Information to be appeared in the income statement for the year ended 30th June 2022

- Bad debts expenses of 15180 will be reported on the debit side of income statement (Hsieh,

Ma and Novoselov, 2019).

Income statement for the year ended June 30, 2022

Particulars Amount Particulars Amount

Bad debts expenses 15180

c. Appearance of account receivables in the balance sheet

- Net account receivables of 148170 will be shown at the end of the year balance sheet.

Account receivables in the beginning = 176550

Less: C. Cathy account = 13200

Account receivables at the end = 163350

Assets Amount

Current assets

Account receivables

Less: Allowance for doubtful debts

163350

- 15180

148170

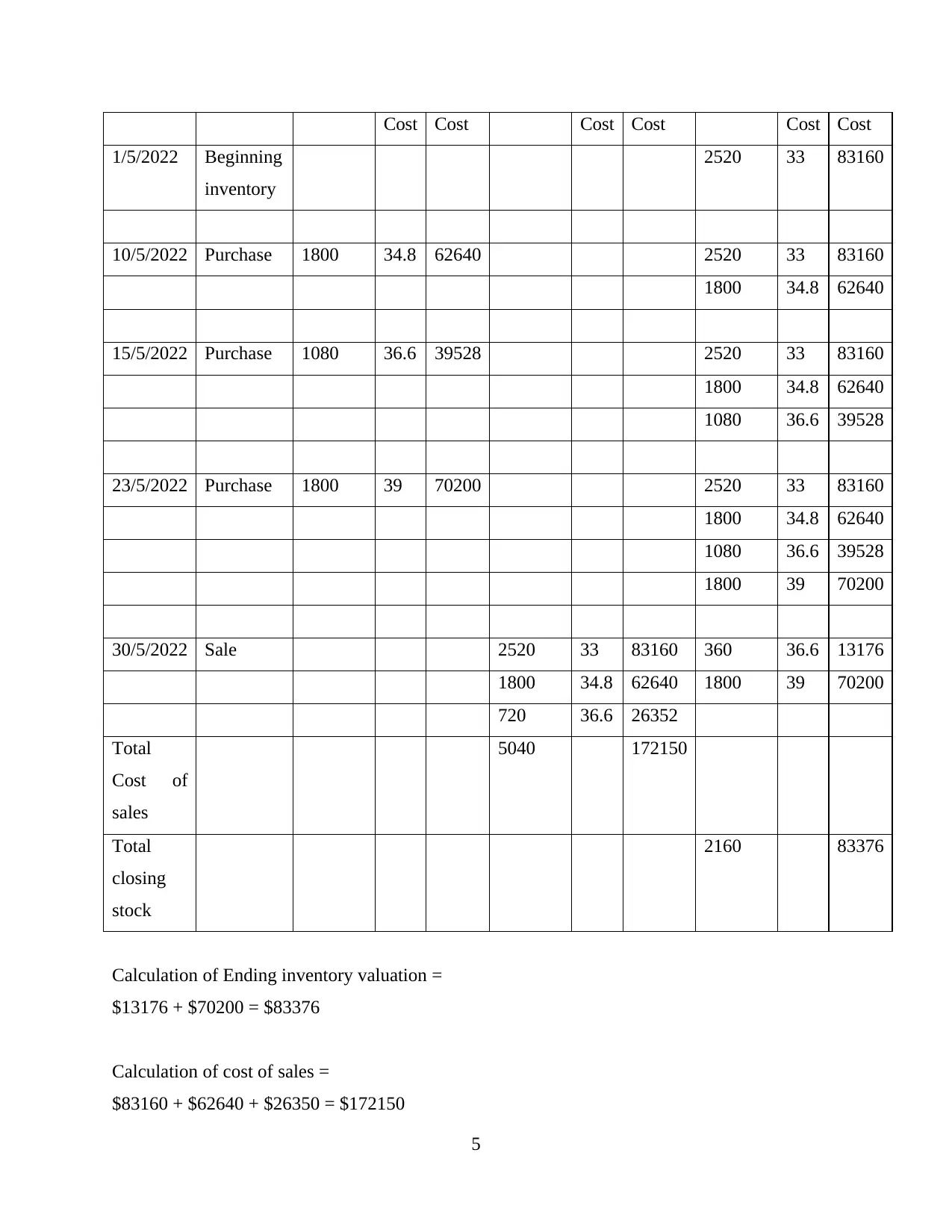

Question 3

(a) Calculation of ending inventory and cost of sales for the month of May using the FIFO

costing method

Date Particulars Receipt Issue Balance

Quantity Unit Total Quantity Unit Total Quantity Unit Total

4

Working note:

Remaining balance in allowance for doubtful debt = 11220 – 9900 = 1320

Adjusting entry to be made for allowance for doubtful debts = 825000 * 2% = 16500 – 1320

= 15180.

b. Information to be appeared in the income statement for the year ended 30th June 2022

- Bad debts expenses of 15180 will be reported on the debit side of income statement (Hsieh,

Ma and Novoselov, 2019).

Income statement for the year ended June 30, 2022

Particulars Amount Particulars Amount

Bad debts expenses 15180

c. Appearance of account receivables in the balance sheet

- Net account receivables of 148170 will be shown at the end of the year balance sheet.

Account receivables in the beginning = 176550

Less: C. Cathy account = 13200

Account receivables at the end = 163350

Assets Amount

Current assets

Account receivables

Less: Allowance for doubtful debts

163350

- 15180

148170

Question 3

(a) Calculation of ending inventory and cost of sales for the month of May using the FIFO

costing method

Date Particulars Receipt Issue Balance

Quantity Unit Total Quantity Unit Total Quantity Unit Total

4

Cost Cost Cost Cost Cost Cost

1/5/2022 Beginning

inventory

2520 33 83160

10/5/2022 Purchase 1800 34.8 62640 2520 33 83160

1800 34.8 62640

15/5/2022 Purchase 1080 36.6 39528 2520 33 83160

1800 34.8 62640

1080 36.6 39528

23/5/2022 Purchase 1800 39 70200 2520 33 83160

1800 34.8 62640

1080 36.6 39528

1800 39 70200

30/5/2022 Sale 2520 33 83160 360 36.6 13176

1800 34.8 62640 1800 39 70200

720 36.6 26352

Total

Cost of

sales

5040 172150

Total

closing

stock

2160 83376

Calculation of Ending inventory valuation =

$13176 + $70200 = $83376

Calculation of cost of sales =

$83160 + $62640 + $26350 = $172150

5

1/5/2022 Beginning

inventory

2520 33 83160

10/5/2022 Purchase 1800 34.8 62640 2520 33 83160

1800 34.8 62640

15/5/2022 Purchase 1080 36.6 39528 2520 33 83160

1800 34.8 62640

1080 36.6 39528

23/5/2022 Purchase 1800 39 70200 2520 33 83160

1800 34.8 62640

1080 36.6 39528

1800 39 70200

30/5/2022 Sale 2520 33 83160 360 36.6 13176

1800 34.8 62640 1800 39 70200

720 36.6 26352

Total

Cost of

sales

5040 172150

Total

closing

stock

2160 83376

Calculation of Ending inventory valuation =

$13176 + $70200 = $83376

Calculation of cost of sales =

$83160 + $62640 + $26350 = $172150

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

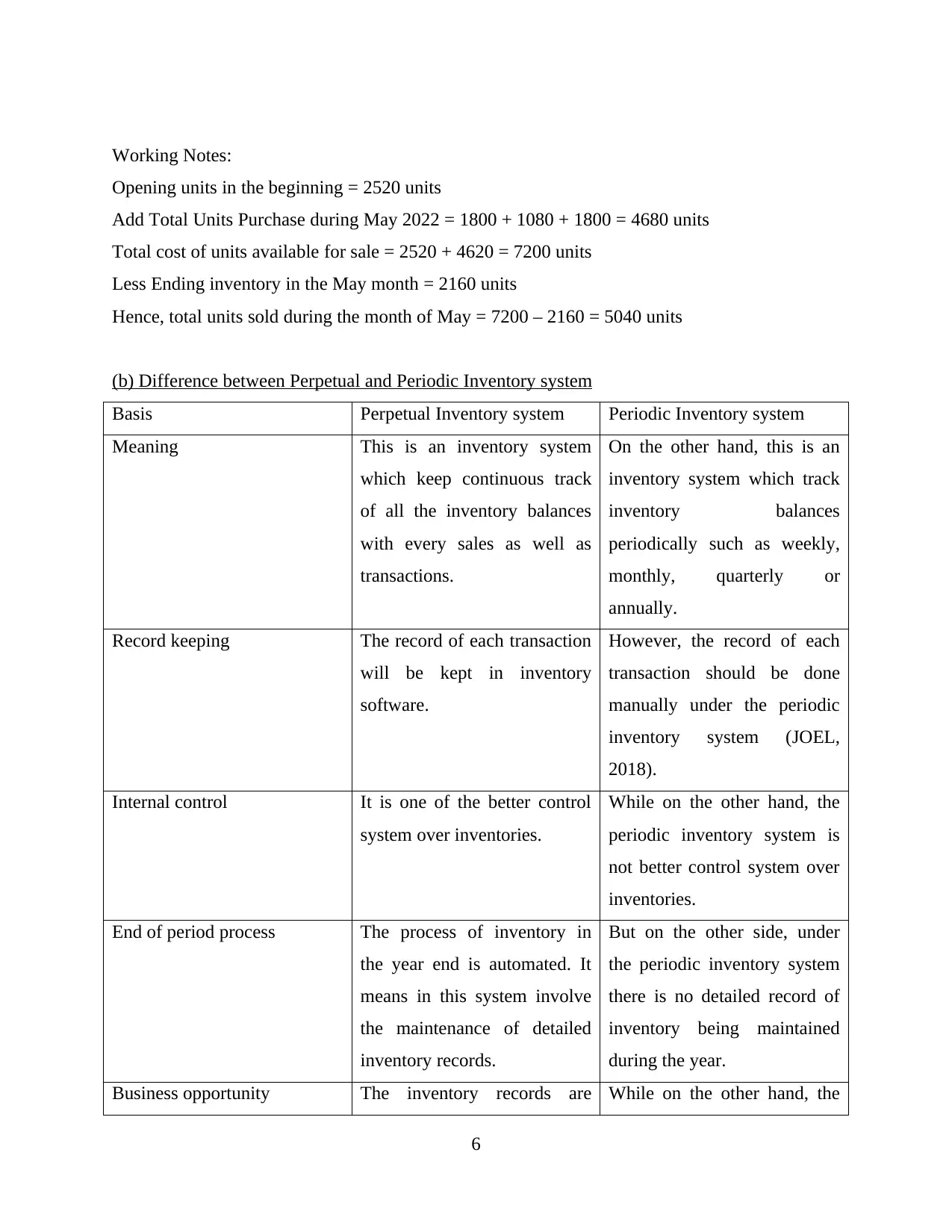

Working Notes:

Opening units in the beginning = 2520 units

Add Total Units Purchase during May 2022 = 1800 + 1080 + 1800 = 4680 units

Total cost of units available for sale = 2520 + 4620 = 7200 units

Less Ending inventory in the May month = 2160 units

Hence, total units sold during the month of May = 7200 – 2160 = 5040 units

(b) Difference between Perpetual and Periodic Inventory system

Basis Perpetual Inventory system Periodic Inventory system

Meaning This is an inventory system

which keep continuous track

of all the inventory balances

with every sales as well as

transactions.

On the other hand, this is an

inventory system which track

inventory balances

periodically such as weekly,

monthly, quarterly or

annually.

Record keeping The record of each transaction

will be kept in inventory

software.

However, the record of each

transaction should be done

manually under the periodic

inventory system (JOEL,

2018).

Internal control It is one of the better control

system over inventories.

While on the other hand, the

periodic inventory system is

not better control system over

inventories.

End of period process The process of inventory in

the year end is automated. It

means in this system involve

the maintenance of detailed

inventory records.

But on the other side, under

the periodic inventory system

there is no detailed record of

inventory being maintained

during the year.

Business opportunity The inventory records are While on the other hand, the

6

Opening units in the beginning = 2520 units

Add Total Units Purchase during May 2022 = 1800 + 1080 + 1800 = 4680 units

Total cost of units available for sale = 2520 + 4620 = 7200 units

Less Ending inventory in the May month = 2160 units

Hence, total units sold during the month of May = 7200 – 2160 = 5040 units

(b) Difference between Perpetual and Periodic Inventory system

Basis Perpetual Inventory system Periodic Inventory system

Meaning This is an inventory system

which keep continuous track

of all the inventory balances

with every sales as well as

transactions.

On the other hand, this is an

inventory system which track

inventory balances

periodically such as weekly,

monthly, quarterly or

annually.

Record keeping The record of each transaction

will be kept in inventory

software.

However, the record of each

transaction should be done

manually under the periodic

inventory system (JOEL,

2018).

Internal control It is one of the better control

system over inventories.

While on the other hand, the

periodic inventory system is

not better control system over

inventories.

End of period process The process of inventory in

the year end is automated. It

means in this system involve

the maintenance of detailed

inventory records.

But on the other side, under

the periodic inventory system

there is no detailed record of

inventory being maintained

during the year.

Business opportunity The inventory records are While on the other hand, the

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

easily maintained without

stopping the business

operation. The impact of

which there is no influence on

the business operation

(Rahardja and et.al., 2021).

This create further opportunity

to business in the form of high

sales, real profit etc.

business operation need to be

stop at the time when they

need to count the inventory or

during the valuation of

inventory at the end of the

year. This create issue for the

business opportunities the

impact of which company

unable to manage the work.

The sudden stop in business

production leads to delay in

supply and loss of earnings.

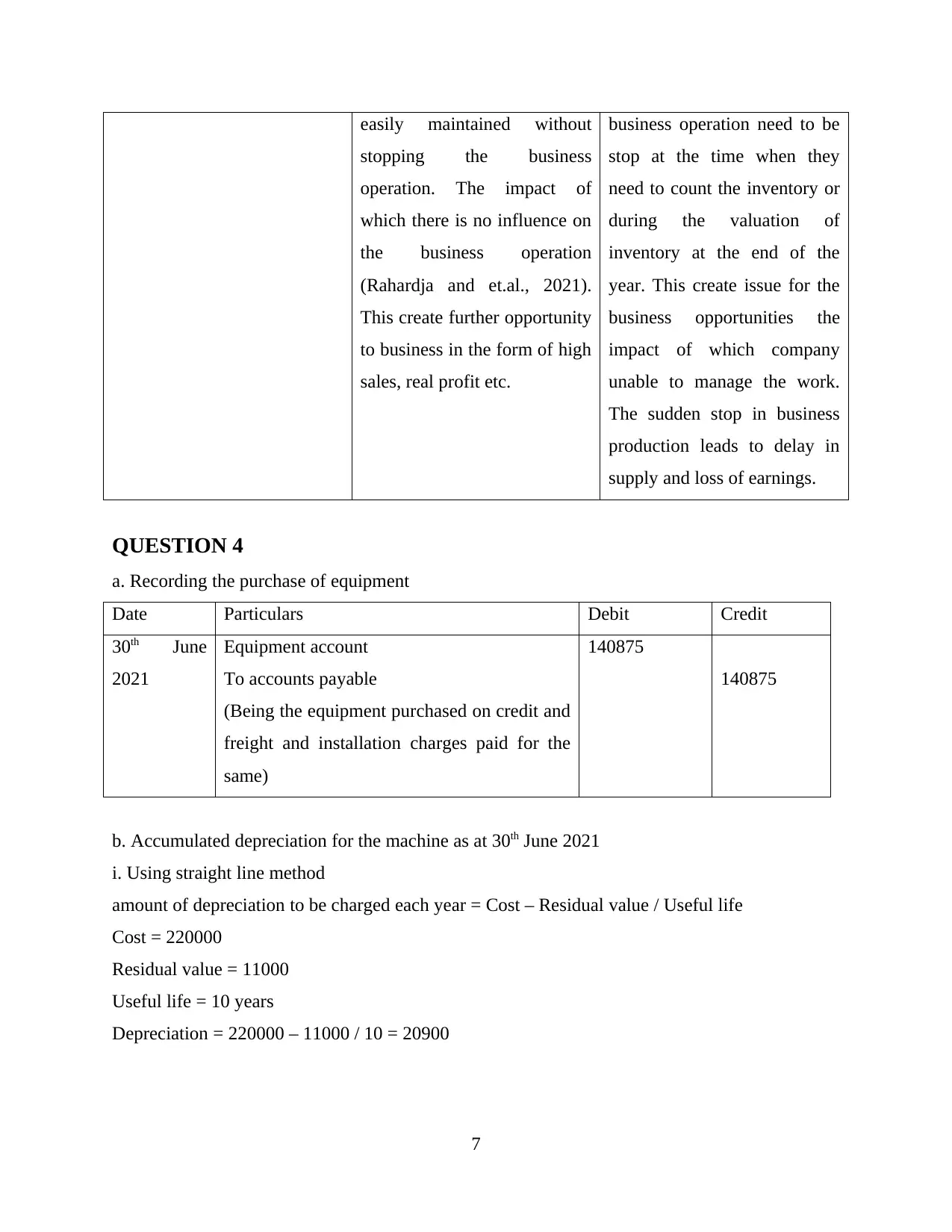

QUESTION 4

a. Recording the purchase of equipment

Date Particulars Debit Credit

30th June

2021

Equipment account

To accounts payable

(Being the equipment purchased on credit and

freight and installation charges paid for the

same)

140875

140875

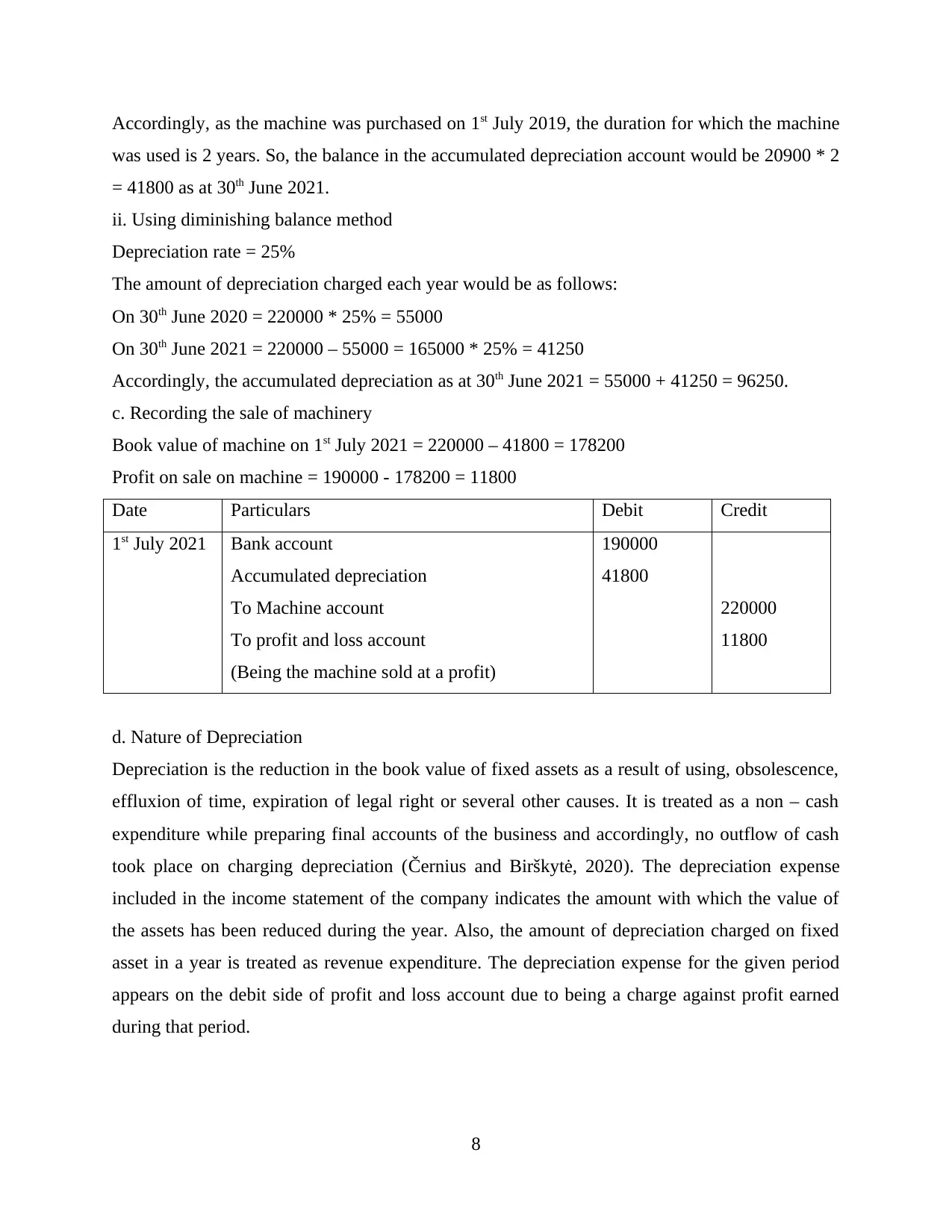

b. Accumulated depreciation for the machine as at 30th June 2021

i. Using straight line method

amount of depreciation to be charged each year = Cost – Residual value / Useful life

Cost = 220000

Residual value = 11000

Useful life = 10 years

Depreciation = 220000 – 11000 / 10 = 20900

7

stopping the business

operation. The impact of

which there is no influence on

the business operation

(Rahardja and et.al., 2021).

This create further opportunity

to business in the form of high

sales, real profit etc.

business operation need to be

stop at the time when they

need to count the inventory or

during the valuation of

inventory at the end of the

year. This create issue for the

business opportunities the

impact of which company

unable to manage the work.

The sudden stop in business

production leads to delay in

supply and loss of earnings.

QUESTION 4

a. Recording the purchase of equipment

Date Particulars Debit Credit

30th June

2021

Equipment account

To accounts payable

(Being the equipment purchased on credit and

freight and installation charges paid for the

same)

140875

140875

b. Accumulated depreciation for the machine as at 30th June 2021

i. Using straight line method

amount of depreciation to be charged each year = Cost – Residual value / Useful life

Cost = 220000

Residual value = 11000

Useful life = 10 years

Depreciation = 220000 – 11000 / 10 = 20900

7

Accordingly, as the machine was purchased on 1st July 2019, the duration for which the machine

was used is 2 years. So, the balance in the accumulated depreciation account would be 20900 * 2

= 41800 as at 30th June 2021.

ii. Using diminishing balance method

Depreciation rate = 25%

The amount of depreciation charged each year would be as follows:

On 30th June 2020 = 220000 * 25% = 55000

On 30th June 2021 = 220000 – 55000 = 165000 * 25% = 41250

Accordingly, the accumulated depreciation as at 30th June 2021 = 55000 + 41250 = 96250.

c. Recording the sale of machinery

Book value of machine on 1st July 2021 = 220000 – 41800 = 178200

Profit on sale on machine = 190000 - 178200 = 11800

Date Particulars Debit Credit

1st July 2021 Bank account

Accumulated depreciation

To Machine account

To profit and loss account

(Being the machine sold at a profit)

190000

41800

220000

11800

d. Nature of Depreciation

Depreciation is the reduction in the book value of fixed assets as a result of using, obsolescence,

effluxion of time, expiration of legal right or several other causes. It is treated as a non – cash

expenditure while preparing final accounts of the business and accordingly, no outflow of cash

took place on charging depreciation (Černius and Birškytė, 2020). The depreciation expense

included in the income statement of the company indicates the amount with which the value of

the assets has been reduced during the year. Also, the amount of depreciation charged on fixed

asset in a year is treated as revenue expenditure. The depreciation expense for the given period

appears on the debit side of profit and loss account due to being a charge against profit earned

during that period.

8

was used is 2 years. So, the balance in the accumulated depreciation account would be 20900 * 2

= 41800 as at 30th June 2021.

ii. Using diminishing balance method

Depreciation rate = 25%

The amount of depreciation charged each year would be as follows:

On 30th June 2020 = 220000 * 25% = 55000

On 30th June 2021 = 220000 – 55000 = 165000 * 25% = 41250

Accordingly, the accumulated depreciation as at 30th June 2021 = 55000 + 41250 = 96250.

c. Recording the sale of machinery

Book value of machine on 1st July 2021 = 220000 – 41800 = 178200

Profit on sale on machine = 190000 - 178200 = 11800

Date Particulars Debit Credit

1st July 2021 Bank account

Accumulated depreciation

To Machine account

To profit and loss account

(Being the machine sold at a profit)

190000

41800

220000

11800

d. Nature of Depreciation

Depreciation is the reduction in the book value of fixed assets as a result of using, obsolescence,

effluxion of time, expiration of legal right or several other causes. It is treated as a non – cash

expenditure while preparing final accounts of the business and accordingly, no outflow of cash

took place on charging depreciation (Černius and Birškytė, 2020). The depreciation expense

included in the income statement of the company indicates the amount with which the value of

the assets has been reduced during the year. Also, the amount of depreciation charged on fixed

asset in a year is treated as revenue expenditure. The depreciation expense for the given period

appears on the debit side of profit and loss account due to being a charge against profit earned

during that period.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

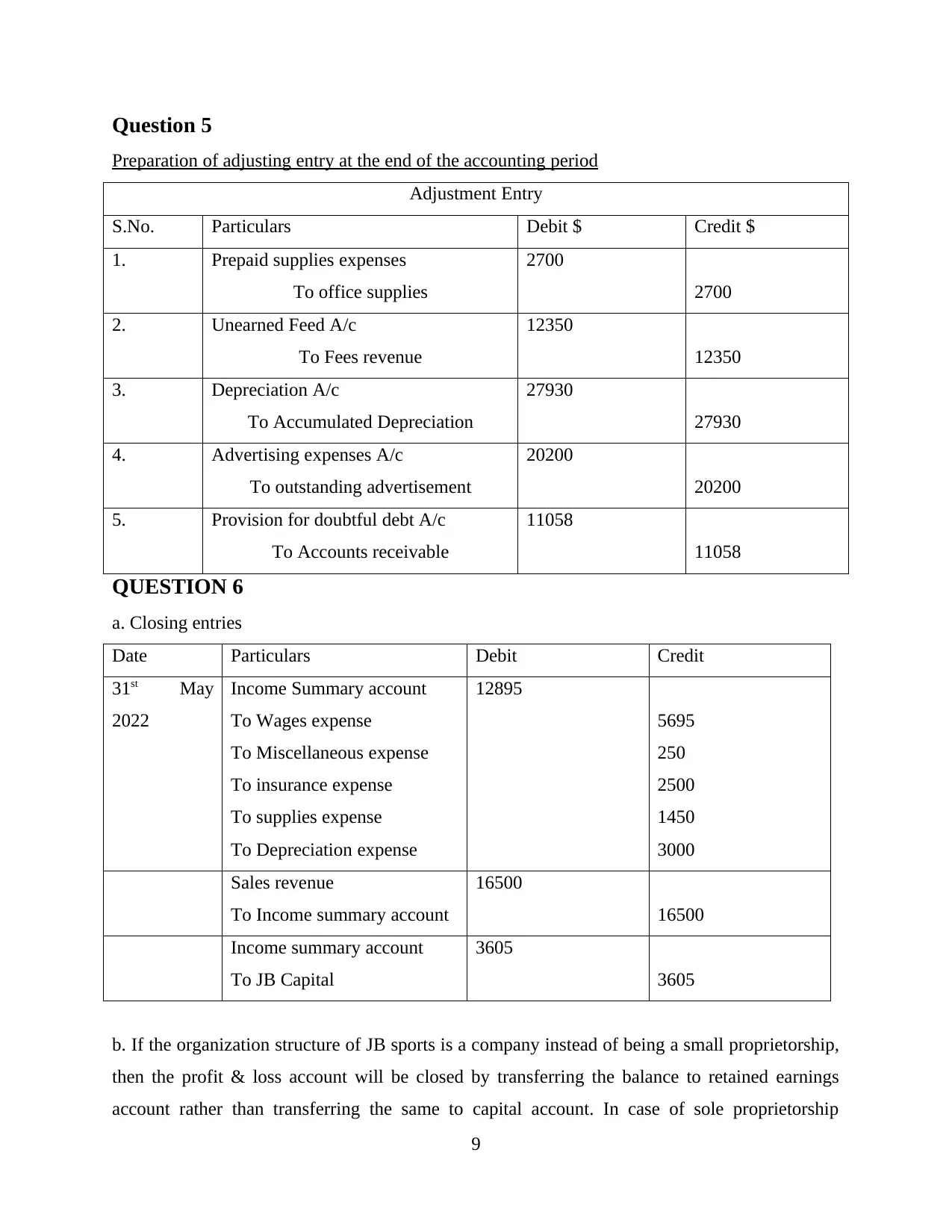

Question 5

Preparation of adjusting entry at the end of the accounting period

Adjustment Entry

S.No. Particulars Debit $ Credit $

1. Prepaid supplies expenses

To office supplies

2700

2700

2. Unearned Feed A/c

To Fees revenue

12350

12350

3. Depreciation A/c

To Accumulated Depreciation

27930

27930

4. Advertising expenses A/c

To outstanding advertisement

20200

20200

5. Provision for doubtful debt A/c

To Accounts receivable

11058

11058

QUESTION 6

a. Closing entries

Date Particulars Debit Credit

31st May

2022

Income Summary account

To Wages expense

To Miscellaneous expense

To insurance expense

To supplies expense

To Depreciation expense

12895

5695

250

2500

1450

3000

Sales revenue

To Income summary account

16500

16500

Income summary account

To JB Capital

3605

3605

b. If the organization structure of JB sports is a company instead of being a small proprietorship,

then the profit & loss account will be closed by transferring the balance to retained earnings

account rather than transferring the same to capital account. In case of sole proprietorship

9

Preparation of adjusting entry at the end of the accounting period

Adjustment Entry

S.No. Particulars Debit $ Credit $

1. Prepaid supplies expenses

To office supplies

2700

2700

2. Unearned Feed A/c

To Fees revenue

12350

12350

3. Depreciation A/c

To Accumulated Depreciation

27930

27930

4. Advertising expenses A/c

To outstanding advertisement

20200

20200

5. Provision for doubtful debt A/c

To Accounts receivable

11058

11058

QUESTION 6

a. Closing entries

Date Particulars Debit Credit

31st May

2022

Income Summary account

To Wages expense

To Miscellaneous expense

To insurance expense

To supplies expense

To Depreciation expense

12895

5695

250

2500

1450

3000

Sales revenue

To Income summary account

16500

16500

Income summary account

To JB Capital

3605

3605

b. If the organization structure of JB sports is a company instead of being a small proprietorship,

then the profit & loss account will be closed by transferring the balance to retained earnings

account rather than transferring the same to capital account. In case of sole proprietorship

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

structure, the sole owner is the only receiver of whatever profit the business has generated and

accordingly, the profit is transferred to his capital account only (Savova, 2021). However, in case

of company structure, the profits are either distributed as dividends or kept with the business for

further growth and expansion in a separate account known as retained earnings account.

Therefore, whatever the profits left after distributing the dividends are transferred to retained

earnings account in case of company structure.

10

accordingly, the profit is transferred to his capital account only (Savova, 2021). However, in case

of company structure, the profits are either distributed as dividends or kept with the business for

further growth and expansion in a separate account known as retained earnings account.

Therefore, whatever the profits left after distributing the dividends are transferred to retained

earnings account in case of company structure.

10

REFERENCES

Books and journals

Černius, G. and Birškytė, L., 2020. Financial information and management decisions: impact of

accounting policy on financial indicators of the firm.

Hsieh, C. C., Ma, Z. and Novoselov, K. E., 2019. Accounting conservatism, business strategy,

and ambiguity. Accounting, Organizations and Society, 74, pp.41-55.

Iyer, N. and et.al., 2019, April. Bank Reconciliation Bot. In 2nd International Conference on

Advances in Science & Technology (ICAST).

JOEL, N., 2018. COLLEGE OF EDUCATION AND EXTERNAL STUDIES (CEES)(SCHOOL

OF DISTANCE AND LIFELONG LEARNING) A REPORT ON FIELD

ATTACHMENT/FIELD ATTACHMENT AT AFRICAN LEADERSHIP AND

RECONCILIATION MINISTRIES (ALARM UGANDA) (Doctoral dissertation,

Makerere University Kampala).

Rahardja, U. and et.al., 2021. Financial management system integrated by web-based payment

cash link solution to invent smart reconciliation. In Proceedings of the international

conference on industrial engineering and operations management (pp. 4733-4743).

Savova, K., 2021. DIFFERENCES IN APPLICATION OF ACCOUNTING STANDARDS-

CURRENT ASPECTS. Ekonomicko-manazerske spektrum, 15(1), pp.111-122.

11

Books and journals

Černius, G. and Birškytė, L., 2020. Financial information and management decisions: impact of

accounting policy on financial indicators of the firm.

Hsieh, C. C., Ma, Z. and Novoselov, K. E., 2019. Accounting conservatism, business strategy,

and ambiguity. Accounting, Organizations and Society, 74, pp.41-55.

Iyer, N. and et.al., 2019, April. Bank Reconciliation Bot. In 2nd International Conference on

Advances in Science & Technology (ICAST).

JOEL, N., 2018. COLLEGE OF EDUCATION AND EXTERNAL STUDIES (CEES)(SCHOOL

OF DISTANCE AND LIFELONG LEARNING) A REPORT ON FIELD

ATTACHMENT/FIELD ATTACHMENT AT AFRICAN LEADERSHIP AND

RECONCILIATION MINISTRIES (ALARM UGANDA) (Doctoral dissertation,

Makerere University Kampala).

Rahardja, U. and et.al., 2021. Financial management system integrated by web-based payment

cash link solution to invent smart reconciliation. In Proceedings of the international

conference on industrial engineering and operations management (pp. 4733-4743).

Savova, K., 2021. DIFFERENCES IN APPLICATION OF ACCOUNTING STANDARDS-

CURRENT ASPECTS. Ekonomicko-manazerske spektrum, 15(1), pp.111-122.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.