Business Development: Management Accounting Report - Unit 5 Analysis

VerifiedAdded on 2020/06/04

|17

|4969

|110

Report

AI Summary

This report, focusing on Agmet Company, delves into the core principles of management accounting, emphasizing its crucial role in business growth and decision-making. It examines various management accounting methods, including price optimization, cost accounting, job costing, and inventory management, highlighting their practical applications within the organization. The report explores different reporting methods such as segmental reporting, performance reports, and inventory management reports, providing insights into how these tools aid in financial analysis and performance evaluation. Furthermore, it contrasts marginal and absorption costing, offering a clear understanding of their differences and implications for income statement management. The report also assesses the advantages and disadvantages of different planning tools and illustrates how a management accounting system adapts to address financial problems. Overall, the report provides a comprehensive overview of management accounting practices and their impact on business development and financial management within a global resource management company.

UNIT 5 MNG ACC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essentials requirement of management accounting in the

organisation............................................................................................................................1

P2 Methods of management accounting reporting in the company.......................................3

TASK 2............................................................................................................................................5

P3 Marginal and absorption costing and explaining differences............................................5

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different types of planning tools.................................8

P5 How management accounting system adapts to respond to financial problems.............11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essentials requirement of management accounting in the

organisation............................................................................................................................1

P2 Methods of management accounting reporting in the company.......................................3

TASK 2............................................................................................................................................5

P3 Marginal and absorption costing and explaining differences............................................5

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different types of planning tools.................................8

P5 How management accounting system adapts to respond to financial problems.............11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting plays a crucial role in as it assists the company in making

effective use of financial data and information for growth and development of business. The

report will evaluate the implementation of different management accounting system in Agmet

which is resource management business and it focused on establishing its global presence. The

firm deals in metals, edible oils, high temperature alloys etc., (Ramiah, Kuppusamy and

Gharleghi, 2018). Also, it will identify different methods of management accounting reporting

which helps in determining effective accounting management practices which are related with

growth and stakeholders of firm. Apart from this the report will outline difference between

Marginal and absorption costing which helps the enterprise in managing its income statement.

Thus, the report will identify management accounting tools which can helps Agmet in managing

financial problems such as, benchmarking, throughput accounting method etc.

TASK 1

P1 Management accounting and essentials requirement of management accounting in the

organisation

Management accounting is an important tool of managerial decision-making so that

organisation may be able to become internally strong so that customers may be provided quality

goods in the best possible way. Management accounting is an important branch of accounting

which summarises data obtained from financial accounting so that it may assess internal strength

of organisation in effective way (Zhang, Randhir and Zhang, 2018). The management is

benefited by such information as it is able to judge internal strength of the company and as such,

enhanced decisions are taken for the betterment of the organisation. Agmet Company which is

engaged in manufacturing sector provides chemical related products to customers. The company

also uses management accounting information in practice so that firm may perform well and

quality services to customers.

The main essence of such information is that managerial reports are prepared on timely

basis and as such, costs are ascertained quite easily. This provides clarity about the expenditures

incurred by the organisation to accomplish tasks. This help management to take measures to

reduce costs so that more production may be achieved with much ease. Financial information

provides management to take short-term as well as long term decisions in effectual way

1

Management accounting plays a crucial role in as it assists the company in making

effective use of financial data and information for growth and development of business. The

report will evaluate the implementation of different management accounting system in Agmet

which is resource management business and it focused on establishing its global presence. The

firm deals in metals, edible oils, high temperature alloys etc., (Ramiah, Kuppusamy and

Gharleghi, 2018). Also, it will identify different methods of management accounting reporting

which helps in determining effective accounting management practices which are related with

growth and stakeholders of firm. Apart from this the report will outline difference between

Marginal and absorption costing which helps the enterprise in managing its income statement.

Thus, the report will identify management accounting tools which can helps Agmet in managing

financial problems such as, benchmarking, throughput accounting method etc.

TASK 1

P1 Management accounting and essentials requirement of management accounting in the

organisation

Management accounting is an important tool of managerial decision-making so that

organisation may be able to become internally strong so that customers may be provided quality

goods in the best possible way. Management accounting is an important branch of accounting

which summarises data obtained from financial accounting so that it may assess internal strength

of organisation in effective way (Zhang, Randhir and Zhang, 2018). The management is

benefited by such information as it is able to judge internal strength of the company and as such,

enhanced decisions are taken for the betterment of the organisation. Agmet Company which is

engaged in manufacturing sector provides chemical related products to customers. The company

also uses management accounting information in practice so that firm may perform well and

quality services to customers.

The main essence of such information is that managerial reports are prepared on timely

basis and as such, costs are ascertained quite easily. This provides clarity about the expenditures

incurred by the organisation to accomplish tasks. This help management to take measures to

reduce costs so that more production may be achieved with much ease. Financial information

provides management to take short-term as well as long term decisions in effectual way

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Ahadiat, 2013). Agmet Company is benefited as through management accounting various trend

charts, variances are carried out which provides clarity to management to assess progress of the

organisation in the best possible way. However, external stakeholders are not provided this

information as it belongs for making decisions solely by the management. Thus, company is

benefited by such information and enhanced decisions are made for achieving common targets.

In addition to this, various types of management accounting are described below-

Price optimisation:

Price optimisation is useful analysis which is quite useful for organisation to set price of

the products in effective way. In simple words, it is a mathematical analysis which is used to

assess the consumer behaviour when certain price is quoted by the company. This technique help

management to analyse that whether customers are ready to buy products at that price which is

quoted by it or should modify price in accordance to the wish of customers in the best possible

way (Chenhall and Smith, 2011). This help management to successfully set price of a particular

product with reference to wish of customers and as such, they achieve satisfaction quite easily.

Agmet Company also uses this management accounting method so that adequate prices may be

quoted so that customers may be delighted and they are not attracted to rivals.

Cost accounting:

Cost accounting is another useful for management to ascertain costs and initiate measures

to reduce costs. This is essentially required mainly in manufacturing sector which involves lot of

indirect expenses, direct, fixed, variable and semi-variable expenditures in accomplishing tasks.

This accounting technique analyses each and every costs and as such, steps are taken to minimise

expenses in effective manner (Van der Stede, 2011). Various costs are ascertained and actual and

planned output is compared so that management may be able to take better and effective

decisions in the best possible way. This help management to take enhanced decisions so that

costs may be reduced and overall production may be achieved with much ease. The

ascertainment of various costs such as operating costs are also important as business has to

perform daily operational tasks and which incurs expenditures. Thus, cost accounting is effective

branch of management accounting which reduces cost of the concern to accomplish enhanced

production.

2

charts, variances are carried out which provides clarity to management to assess progress of the

organisation in the best possible way. However, external stakeholders are not provided this

information as it belongs for making decisions solely by the management. Thus, company is

benefited by such information and enhanced decisions are made for achieving common targets.

In addition to this, various types of management accounting are described below-

Price optimisation:

Price optimisation is useful analysis which is quite useful for organisation to set price of

the products in effective way. In simple words, it is a mathematical analysis which is used to

assess the consumer behaviour when certain price is quoted by the company. This technique help

management to analyse that whether customers are ready to buy products at that price which is

quoted by it or should modify price in accordance to the wish of customers in the best possible

way (Chenhall and Smith, 2011). This help management to successfully set price of a particular

product with reference to wish of customers and as such, they achieve satisfaction quite easily.

Agmet Company also uses this management accounting method so that adequate prices may be

quoted so that customers may be delighted and they are not attracted to rivals.

Cost accounting:

Cost accounting is another useful for management to ascertain costs and initiate measures

to reduce costs. This is essentially required mainly in manufacturing sector which involves lot of

indirect expenses, direct, fixed, variable and semi-variable expenditures in accomplishing tasks.

This accounting technique analyses each and every costs and as such, steps are taken to minimise

expenses in effective manner (Van der Stede, 2011). Various costs are ascertained and actual and

planned output is compared so that management may be able to take better and effective

decisions in the best possible way. This help management to take enhanced decisions so that

costs may be reduced and overall production may be achieved with much ease. The

ascertainment of various costs such as operating costs are also important as business has to

perform daily operational tasks and which incurs expenditures. Thus, cost accounting is effective

branch of management accounting which reduces cost of the concern to accomplish enhanced

production.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing:

Job costing is useful method of management accounting and is essentially required in the

business. Agmet Company which is engaged in the manufacturing sector is highly benefited by

this technique as manufacturing costs are easily ascertained. Job costing is beneficial for the

organisation as it analyses costs incurred on various jobs which are engaged in accomplishing

required production and as such, this technique help management to analyse jobs which are

producing required output and also analyses inefficient jobs (Ward, 2012). Thus, expenditures on

various jobs are easily evaluated and company is able to take enhanced decisions with much ease

regarding minimising costs on unproductive jobs so that overall production may be achieved

quite effectually. This help management to analyse which job is achieving required production

and which is not generating desired production. This help to ascertain costs on jobs and as such,

desired production is generated with much ease.

Inventory management:

Inventory is required in the organisation so that it may be able to provide goods to

customers. Large number of orders are received on daily basis and as such, it is required that

company may provide their orders on timely basis. Production department requires inventory to

be achieve desired production. In this scenario, inventory is required to be managed quite

effectively so that production may be done and customers may be provided with goods within

stipulated time. This is required to be done by the management as resources are scarce and

company cannot waste the same. If inventory is ordered in more than required quantity, then it

will lead to unnecessary wastage of money as it has to be maintained in the warehouse which

will incur additional cost of handling. Thus, it is required that management should analyse needs

of production department and as such, inventory must be ordered.

P2 Methods of management accounting reporting in the company

Segmental or departmental report:

Segment reporting is useful piece of information to management so that financial

condition of the company may be assessed. This report breaks financial data into various

segments or department of the company and the same information is listed into the financial

statements of firm (Management accounting, 2018). Top management is benefited by such

3

Job costing is useful method of management accounting and is essentially required in the

business. Agmet Company which is engaged in the manufacturing sector is highly benefited by

this technique as manufacturing costs are easily ascertained. Job costing is beneficial for the

organisation as it analyses costs incurred on various jobs which are engaged in accomplishing

required production and as such, this technique help management to analyse jobs which are

producing required output and also analyses inefficient jobs (Ward, 2012). Thus, expenditures on

various jobs are easily evaluated and company is able to take enhanced decisions with much ease

regarding minimising costs on unproductive jobs so that overall production may be achieved

quite effectually. This help management to analyse which job is achieving required production

and which is not generating desired production. This help to ascertain costs on jobs and as such,

desired production is generated with much ease.

Inventory management:

Inventory is required in the organisation so that it may be able to provide goods to

customers. Large number of orders are received on daily basis and as such, it is required that

company may provide their orders on timely basis. Production department requires inventory to

be achieve desired production. In this scenario, inventory is required to be managed quite

effectively so that production may be done and customers may be provided with goods within

stipulated time. This is required to be done by the management as resources are scarce and

company cannot waste the same. If inventory is ordered in more than required quantity, then it

will lead to unnecessary wastage of money as it has to be maintained in the warehouse which

will incur additional cost of handling. Thus, it is required that management should analyse needs

of production department and as such, inventory must be ordered.

P2 Methods of management accounting reporting in the company

Segmental or departmental report:

Segment reporting is useful piece of information to management so that financial

condition of the company may be assessed. This report breaks financial data into various

segments or department of the company and the same information is listed into the financial

statements of firm (Management accounting, 2018). Top management is benefited by such

3

information as it can easily evaluate income, expenditures and other aspect of various segments

so that profitability of each of segments may be easily evaluated. However, this report is required

for public companies and not the private ones.

Performance report:

Performance report is quite effective report which help management to assess

performance of something in the organisation. Mainly, these reports are prepared for assessing

the performance of employees so that overall efficiency may be evaluated in the best possible

way. This required so that management may analyse efficiency of employees so that in the event

of any deficient performances, measures may be taken effectively to accomplish desired

productivity in the best possible way (Vimpari, Kajander and Junnila, 2014). This help to

compare standard performance of employees with that of actual performance so that variances if

any can be easily ascertained and measures can be easily taken to remove the same. Weekly or

annual performance reports should be generated by Agmet Company so that deficiency may be

evaluated and performance may be enhanced to accomplish desired productivity.

Inventory management report:

Inventory management report is another essential report which is scrutinised by the

management to order desired inventory from suppliers. This is required so that adequate quantum

of inventory may be ordered so that production department may be able to achieve desired

production (Modell, 2010). Inventory management report is prepared by the production

department which is then forwarded to the management so that it may scrutinise the same and

order only required quantity of stock so that wastage may not occur and as such, production may

be easily achieved with adequate quantity of inventory which will lead to enhanced production

and that too with no spoilage of inventory.

Accounts receivables ageing report:

Customers are provided with facility to buy now and pay later. In simple words, they are

provided with credit facility so that they may pay for the purchased items afterwards. In order to

analyse, outstanding amount of payment from customers, a report known as accounts receivable

ageing report is prepared. This report is quite useful for Agmet Company so that it may be able

to analyse how much payment is pending from customers and as such, it can easily assess

4

so that profitability of each of segments may be easily evaluated. However, this report is required

for public companies and not the private ones.

Performance report:

Performance report is quite effective report which help management to assess

performance of something in the organisation. Mainly, these reports are prepared for assessing

the performance of employees so that overall efficiency may be evaluated in the best possible

way. This required so that management may analyse efficiency of employees so that in the event

of any deficient performances, measures may be taken effectively to accomplish desired

productivity in the best possible way (Vimpari, Kajander and Junnila, 2014). This help to

compare standard performance of employees with that of actual performance so that variances if

any can be easily ascertained and measures can be easily taken to remove the same. Weekly or

annual performance reports should be generated by Agmet Company so that deficiency may be

evaluated and performance may be enhanced to accomplish desired productivity.

Inventory management report:

Inventory management report is another essential report which is scrutinised by the

management to order desired inventory from suppliers. This is required so that adequate quantum

of inventory may be ordered so that production department may be able to achieve desired

production (Modell, 2010). Inventory management report is prepared by the production

department which is then forwarded to the management so that it may scrutinise the same and

order only required quantity of stock so that wastage may not occur and as such, production may

be easily achieved with adequate quantity of inventory which will lead to enhanced production

and that too with no spoilage of inventory.

Accounts receivables ageing report:

Customers are provided with facility to buy now and pay later. In simple words, they are

provided with credit facility so that they may pay for the purchased items afterwards. In order to

analyse, outstanding amount of payment from customers, a report known as accounts receivable

ageing report is prepared. This report is quite useful for Agmet Company so that it may be able

to analyse how much payment is pending from customers and as such, it can easily assess

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

amount of each of them and then contact them to pay outstanding amount (Bennett, Schaltegger

and Zvezdov, 2013). Thus, it is required that customers may make timely payments as

organisation requires amount for carrying out daily operational tasks with much ease. If there are

many customers from whom payment is pending, then well-structured strategies should be

implemented so that timely amount may be recovered from unpaid customer invoices.

Job cost report:

Job cost report is prepared to manage costs incurred on job so that expenditures on

various jobs may be analysed in effective way. This help management to allocate each job to

particular division code so that expenditures incurred on various jobs may be easily evaluated

(Christian, 2018). This report is much essential to company so that it may be able to check on

various costs and as such, measures are taken to reduce expenses so that adequate production

may be achieved with much ease. This help management to bifurcate productive and

unproductive jobs so that deficiency may be removed and overall productivity may be easily

accomplished. Thus, job cost report is quite essential for Agmet Company to extract better

results.

Operational budget report:

Operational budget report is prepared to estimate income and expenditures that will be

incurred by various departments in the company. This report help management to assess budget

requirement of departments so that they all may be able to carry out tasks in the best possible

way (Rizza and Ruggeri, 2018). This report includes sales, production, direct materials and other

components which play an important role in the company so that budget may be prepared quite

easily. Operational budget report provides clarity about how many expenses will be incurred and

how much profit will be earned by departments and as such, it is essential report for the

management.

TASK 2

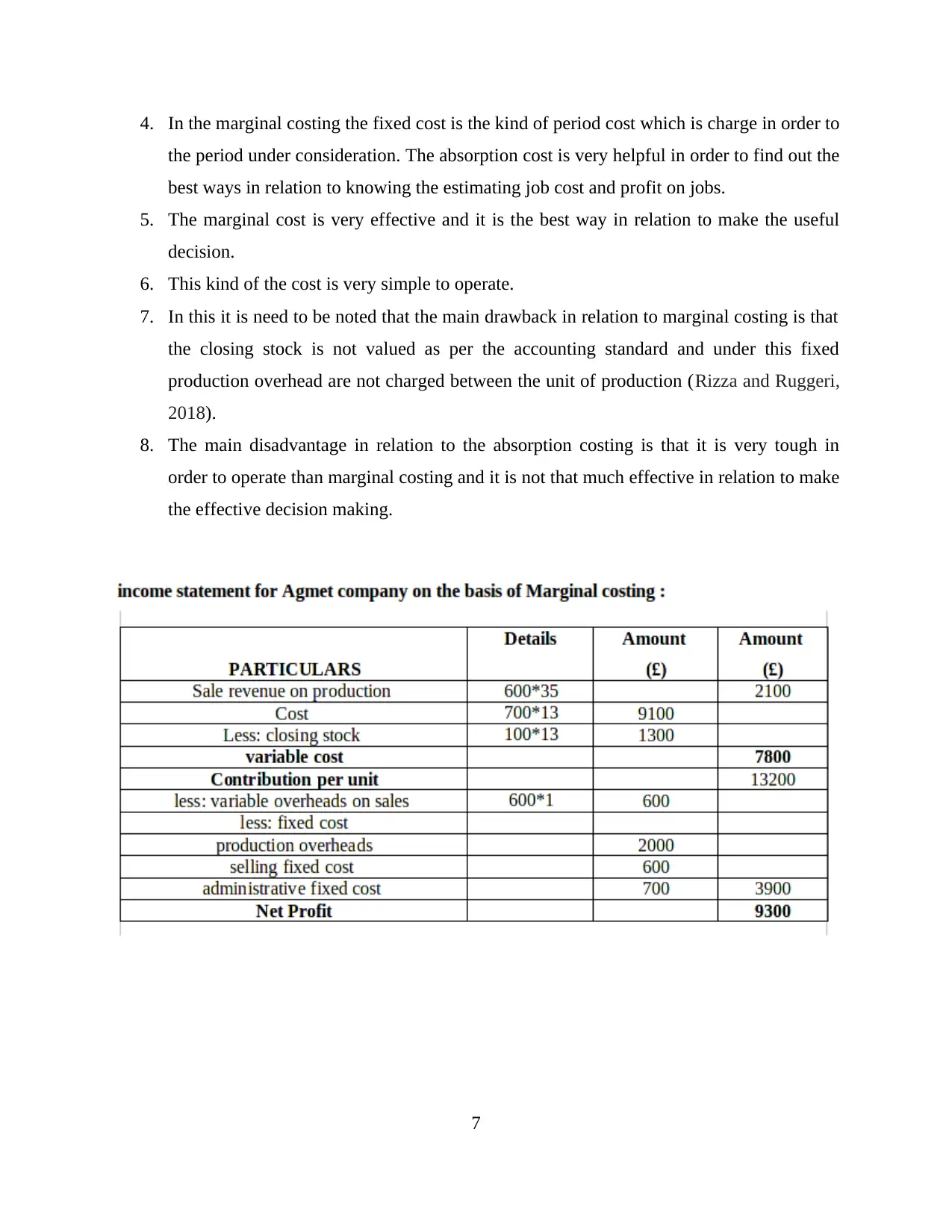

P3 Marginal and absorption costing and explaining differences

Marginal costing- The marginal cost is termed as the variable cost which is inclusive of

the various kind of the cost such are as labour, material and estimated portion of fixed cost. This

is inclusive of the overhead and selling expenses. This term mean increment or decrement in the

5

and Zvezdov, 2013). Thus, it is required that customers may make timely payments as

organisation requires amount for carrying out daily operational tasks with much ease. If there are

many customers from whom payment is pending, then well-structured strategies should be

implemented so that timely amount may be recovered from unpaid customer invoices.

Job cost report:

Job cost report is prepared to manage costs incurred on job so that expenditures on

various jobs may be analysed in effective way. This help management to allocate each job to

particular division code so that expenditures incurred on various jobs may be easily evaluated

(Christian, 2018). This report is much essential to company so that it may be able to check on

various costs and as such, measures are taken to reduce expenses so that adequate production

may be achieved with much ease. This help management to bifurcate productive and

unproductive jobs so that deficiency may be removed and overall productivity may be easily

accomplished. Thus, job cost report is quite essential for Agmet Company to extract better

results.

Operational budget report:

Operational budget report is prepared to estimate income and expenditures that will be

incurred by various departments in the company. This report help management to assess budget

requirement of departments so that they all may be able to carry out tasks in the best possible

way (Rizza and Ruggeri, 2018). This report includes sales, production, direct materials and other

components which play an important role in the company so that budget may be prepared quite

easily. Operational budget report provides clarity about how many expenses will be incurred and

how much profit will be earned by departments and as such, it is essential report for the

management.

TASK 2

P3 Marginal and absorption costing and explaining differences

Marginal costing- The marginal cost is termed as the variable cost which is inclusive of

the various kind of the cost such are as labour, material and estimated portion of fixed cost. This

is inclusive of the overhead and selling expenses. This term mean increment or decrement in the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

total cost of the production can be termed as the breakeven point (Gan and Chin 2018). In

marginal costing the variable cost changed as it added to the cost but fixed cost will remain the

same at the all stage. This is the kind of the principle technique in relation to make the all kind of

the effective decision. There are the various kinds of the marginal costing such are as-

1. The effective classification of fixed cost and variable cost.

2. The impressive determination of price.

3. Increment in profitability of firm.

4. The good valuation of stock.

The marginal contribution can be calculated in the following manner are as-

Sales price – variable price is equal to marginal costing.

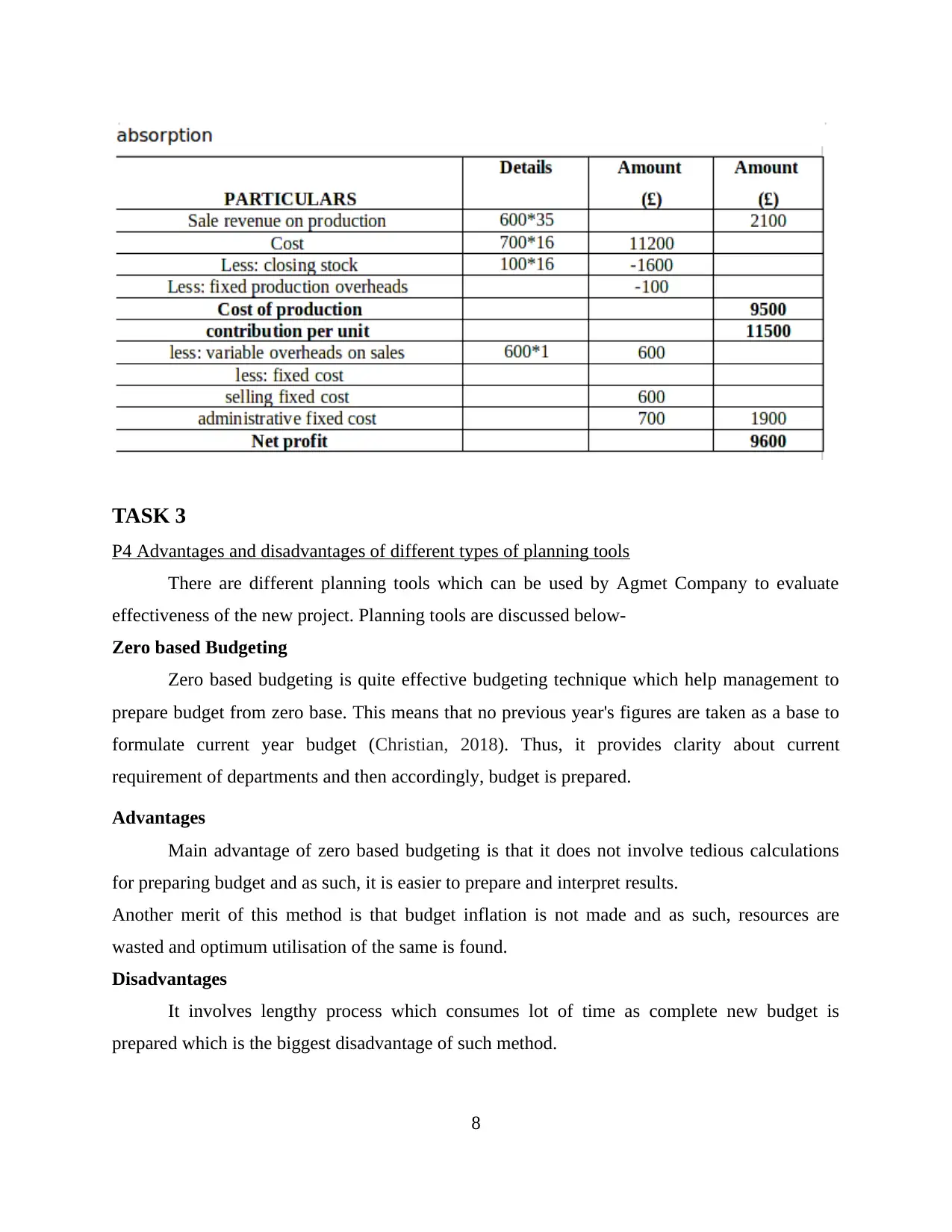

Absorption costing- In this the all manufacture cost is need to be absorbed as the unit

produced. This is inclusive of the all indirect expenses as well as direct expenses. This is related

to the income statement. This is one of the oldest and effective technique of calculating the

absorption cost (Richelle and et. al., 2018). The absorption costing can also be known as the full

costing method which will be helpful in order to do each thing in the effective and efficient

manner. In this kind of the technique the cost is made up of direct cost plus overhead costs. In

this there is no kind of inventory and overhead recovery date is available.

There are two differed methods in relation to find out method of absorption costing in the

following manner are as-

Inventory value

Unit cost.

This can be known with the help of it differentiation in the following manner are as-

1. The marginal cost is varying as per the change in the sales volume per unit due to this the

rate of profit also get fluctuated.

2. As per the SSAP 9 it has been stated that the Absorption cost is inclusive of the element

of fixed overheads I order to determining the inventory volume.

3. The over absorption is the one of the effective method in relation to identifying the

controlling cot of the organisation (Gan and Chin 2018). In the marginal costing there is

not any kind of under absorption overheads in the income statement.

6

marginal costing the variable cost changed as it added to the cost but fixed cost will remain the

same at the all stage. This is the kind of the principle technique in relation to make the all kind of

the effective decision. There are the various kinds of the marginal costing such are as-

1. The effective classification of fixed cost and variable cost.

2. The impressive determination of price.

3. Increment in profitability of firm.

4. The good valuation of stock.

The marginal contribution can be calculated in the following manner are as-

Sales price – variable price is equal to marginal costing.

Absorption costing- In this the all manufacture cost is need to be absorbed as the unit

produced. This is inclusive of the all indirect expenses as well as direct expenses. This is related

to the income statement. This is one of the oldest and effective technique of calculating the

absorption cost (Richelle and et. al., 2018). The absorption costing can also be known as the full

costing method which will be helpful in order to do each thing in the effective and efficient

manner. In this kind of the technique the cost is made up of direct cost plus overhead costs. In

this there is no kind of inventory and overhead recovery date is available.

There are two differed methods in relation to find out method of absorption costing in the

following manner are as-

Inventory value

Unit cost.

This can be known with the help of it differentiation in the following manner are as-

1. The marginal cost is varying as per the change in the sales volume per unit due to this the

rate of profit also get fluctuated.

2. As per the SSAP 9 it has been stated that the Absorption cost is inclusive of the element

of fixed overheads I order to determining the inventory volume.

3. The over absorption is the one of the effective method in relation to identifying the

controlling cot of the organisation (Gan and Chin 2018). In the marginal costing there is

not any kind of under absorption overheads in the income statement.

6

4. In the marginal costing the fixed cost is the kind of period cost which is charge in order to

the period under consideration. The absorption cost is very helpful in order to find out the

best ways in relation to knowing the estimating job cost and profit on jobs.

5. The marginal cost is very effective and it is the best way in relation to make the useful

decision.

6. This kind of the cost is very simple to operate.

7. In this it is need to be noted that the main drawback in relation to marginal costing is that

the closing stock is not valued as per the accounting standard and under this fixed

production overhead are not charged between the unit of production (Rizza and Ruggeri,

2018).

8. The main disadvantage in relation to the absorption costing is that it is very tough in

order to operate than marginal costing and it is not that much effective in relation to make

the effective decision making.

7

the period under consideration. The absorption cost is very helpful in order to find out the

best ways in relation to knowing the estimating job cost and profit on jobs.

5. The marginal cost is very effective and it is the best way in relation to make the useful

decision.

6. This kind of the cost is very simple to operate.

7. In this it is need to be noted that the main drawback in relation to marginal costing is that

the closing stock is not valued as per the accounting standard and under this fixed

production overhead are not charged between the unit of production (Rizza and Ruggeri,

2018).

8. The main disadvantage in relation to the absorption costing is that it is very tough in

order to operate than marginal costing and it is not that much effective in relation to make

the effective decision making.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

P4 Advantages and disadvantages of different types of planning tools

There are different planning tools which can be used by Agmet Company to evaluate

effectiveness of the new project. Planning tools are discussed below-

Zero based Budgeting

Zero based budgeting is quite effective budgeting technique which help management to

prepare budget from zero base. This means that no previous year's figures are taken as a base to

formulate current year budget (Christian, 2018). Thus, it provides clarity about current

requirement of departments and then accordingly, budget is prepared.

Advantages

Main advantage of zero based budgeting is that it does not involve tedious calculations

for preparing budget and as such, it is easier to prepare and interpret results.

Another merit of this method is that budget inflation is not made and as such, resources are

wasted and optimum utilisation of the same is found.

Disadvantages

It involves lengthy process which consumes lot of time as complete new budget is

prepared which is the biggest disadvantage of such method.

8

P4 Advantages and disadvantages of different types of planning tools

There are different planning tools which can be used by Agmet Company to evaluate

effectiveness of the new project. Planning tools are discussed below-

Zero based Budgeting

Zero based budgeting is quite effective budgeting technique which help management to

prepare budget from zero base. This means that no previous year's figures are taken as a base to

formulate current year budget (Christian, 2018). Thus, it provides clarity about current

requirement of departments and then accordingly, budget is prepared.

Advantages

Main advantage of zero based budgeting is that it does not involve tedious calculations

for preparing budget and as such, it is easier to prepare and interpret results.

Another merit of this method is that budget inflation is not made and as such, resources are

wasted and optimum utilisation of the same is found.

Disadvantages

It involves lengthy process which consumes lot of time as complete new budget is

prepared which is the biggest disadvantage of such method.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It requires more manpower and consumes enough time of employees and as such, daily activities

are not accomplished.

IRR (Internal Rate of Return)

IRR is effective technique which is used to evaluate attractiveness of new project. It

provides clarity about the rate of return that will be yield in the future by investing in same

(Bennett, Schaltegger and Zvezdov, 2013). This help management of Agmet Company whether

it should opt for investing in the project or not. More the rate of IRR, company should invest in

the project.

Advantages

Main advantage of IRR method is that it is easier to compute and does not involve

complex calculations which is helpful for interpreting results with much ease.

Another advantage of IRR method is that it considers time value of money and as such, it gives

effective results to opt for investing in the project or not.

Disadvantages

It is not effective planning tool for management as when two projects have different

durations, then results obtained are inaccurate.

Rate of return which is calculated is mere an estimate and as such, decisions made on this basis

may lead to poor results.

NPV (Net Present Value)

NPV is another effective way of evaluating effectiveness of new project in the best

possible way (Modell, 2010). The main essence of using this method as a planning tool is that

Agmet Company may assess profitability aspect of the project quite effectively. More the NPV,

company should invest in the project.

Advantages

NPV is a great planning tool as it considers time value of money while assessing effectiveness

and attractiveness of the project.

It is useful tool as it analyses present value of cash inflows and outflows which provides clarity

about the effectiveness of new project.

Disadvantages

The main disadvantage of this method is that it takes into consideration discounting factor which

is difficult aspect to assess profitability of project.

9

are not accomplished.

IRR (Internal Rate of Return)

IRR is effective technique which is used to evaluate attractiveness of new project. It

provides clarity about the rate of return that will be yield in the future by investing in same

(Bennett, Schaltegger and Zvezdov, 2013). This help management of Agmet Company whether

it should opt for investing in the project or not. More the rate of IRR, company should invest in

the project.

Advantages

Main advantage of IRR method is that it is easier to compute and does not involve

complex calculations which is helpful for interpreting results with much ease.

Another advantage of IRR method is that it considers time value of money and as such, it gives

effective results to opt for investing in the project or not.

Disadvantages

It is not effective planning tool for management as when two projects have different

durations, then results obtained are inaccurate.

Rate of return which is calculated is mere an estimate and as such, decisions made on this basis

may lead to poor results.

NPV (Net Present Value)

NPV is another effective way of evaluating effectiveness of new project in the best

possible way (Modell, 2010). The main essence of using this method as a planning tool is that

Agmet Company may assess profitability aspect of the project quite effectively. More the NPV,

company should invest in the project.

Advantages

NPV is a great planning tool as it considers time value of money while assessing effectiveness

and attractiveness of the project.

It is useful tool as it analyses present value of cash inflows and outflows which provides clarity

about the effectiveness of new project.

Disadvantages

The main disadvantage of this method is that it takes into consideration discounting factor which

is difficult aspect to assess profitability of project.

9

NPV is not useful for making comparison between two mutually exclusive projects having

different sizes. This results into inaccurate results and wrong or poor investment decisions may

be made by the management.

Payback period

It is another useful tool for evaluating project. Agmet Company may be benefited by such

method as it provides clarity to management regarding project that how much time it will take to

yield better results. Less the time taken in order to have the higher amount of profitability on the

making of capital investment (Vimpari, Kajander and Junnila, 2014). The many kinds of the

enterprise are having the acceptable payback period and it is need to be consider in relation to

target the less number of years. The pay back method is totally depending on the time. The time

of money will be considered as the payback period and it is the time when money will be return.

This is one of the effective measurement in relation to identifying the risk of the investment.

Incremental Budgeting

It helps the Agmet in managing budget of company by comparing the current budget with

budget of past few years (Ramiah, Kuppusamy and Gharleghi, 2018). This helps in making

changes in present budget to managing incremental amount of present period.

Advantages

This method is beneficial as it is consistent and relevant. It helps in establishing

coordination between budgets of parts few years which is most common approach of managing

financial performance

Disadvantages

It leads to negligence of changes in present year.

Advantages

This is one of the popular method in relation to identifying the several reasons. In this the

first is the simplicity. The manager used this kind of the method in relation to have the effective

evaluation on the of the project in order to derive the small investment (Richelle and et.al.,

2018). This is inclusive with the group of employees in order to conduct the effective and

economic analysis.

Disadvantages

The payback period works in relation to ignore the time value of money. This is one of

the effective model which is helpful in relation to consider the cash flows. The pay back method

10

different sizes. This results into inaccurate results and wrong or poor investment decisions may

be made by the management.

Payback period

It is another useful tool for evaluating project. Agmet Company may be benefited by such

method as it provides clarity to management regarding project that how much time it will take to

yield better results. Less the time taken in order to have the higher amount of profitability on the

making of capital investment (Vimpari, Kajander and Junnila, 2014). The many kinds of the

enterprise are having the acceptable payback period and it is need to be consider in relation to

target the less number of years. The pay back method is totally depending on the time. The time

of money will be considered as the payback period and it is the time when money will be return.

This is one of the effective measurement in relation to identifying the risk of the investment.

Incremental Budgeting

It helps the Agmet in managing budget of company by comparing the current budget with

budget of past few years (Ramiah, Kuppusamy and Gharleghi, 2018). This helps in making

changes in present budget to managing incremental amount of present period.

Advantages

This method is beneficial as it is consistent and relevant. It helps in establishing

coordination between budgets of parts few years which is most common approach of managing

financial performance

Disadvantages

It leads to negligence of changes in present year.

Advantages

This is one of the popular method in relation to identifying the several reasons. In this the

first is the simplicity. The manager used this kind of the method in relation to have the effective

evaluation on the of the project in order to derive the small investment (Richelle and et.al.,

2018). This is inclusive with the group of employees in order to conduct the effective and

economic analysis.

Disadvantages

The payback period works in relation to ignore the time value of money. This is one of

the effective model which is helpful in relation to consider the cash flows. The pay back method

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.