FHI Workbook Assignment - Financial Analysis and Budgeting

VerifiedAdded on 2023/04/23

|27

|5755

|132

Homework Assignment

AI Summary

This assignment is a comprehensive workbook exploring key concepts in business finance and accounting. It begins by examining internal and external sources of funding available to businesses, followed by an evaluation of various methods for generating income, including sales revenue, subletting, commissions, sponsorships, royalties, and capital gains, with a detailed breakdown of their contributions. The assignment then delves into cost analysis, differentiating between direct and indirect costs and providing examples. Further, it explores the characteristics of fixed, variable, and semi-variable costs, accompanied by diagrams, and evaluates methods of controlling stock, including the Just-in-Time order approach. The importance of accounting notes and budgetary control is discussed, and the process and purpose of budgetary control are explained. Finally, the assignment touches upon ratio analysis, emphasizing its role in interpreting business performance, and provides an overview of profitability and liquidity ratios.

FHI-WORKBOOK

This is the mandatory document to be submitted on STPMoodle

ASSIGNMENT SUBMISSION FORM

This sheet must be submitted with your assignment. Failure to complete, sign and submit

this form along with your work will result in a delay in marking your work. Marking can

only be proceed provided the evidence of your declaration of originality of your work

attached to your coursework.

Student Name

Student ID

Assessor Name

Qualification Title

Unit Number & Unit Title

Submission Deadline

Date of Submission

Learner Declaration

By submitting this form and signing below, I declare that:

I am the author of this assignment and that any assistance I received in its

preparation is fully disclosed and acknowledged in this assignment

I also certify that this assignment was prepared by me specifically for this course

I certify that I have taken all reasonable precautions to make sure that my work has

not been copied by other students

I confirm that I have understood the College’s regulations on plagiarism

I confirm that research resources are fully acknowledged

Signature: ……………………………………… Date: ………………………………

‘Plagiarism’ is presenting somebody else’s work as your own. It includes copying

information directly from the Web or books without referencing the material;

submitting joint coursework as an individual effort; copying another student’s

coursework; stealing coursework from another student and submitting it as your own

work.

This is the mandatory document to be submitted on STPMoodle

ASSIGNMENT SUBMISSION FORM

This sheet must be submitted with your assignment. Failure to complete, sign and submit

this form along with your work will result in a delay in marking your work. Marking can

only be proceed provided the evidence of your declaration of originality of your work

attached to your coursework.

Student Name

Student ID

Assessor Name

Qualification Title

Unit Number & Unit Title

Submission Deadline

Date of Submission

Learner Declaration

By submitting this form and signing below, I declare that:

I am the author of this assignment and that any assistance I received in its

preparation is fully disclosed and acknowledged in this assignment

I also certify that this assignment was prepared by me specifically for this course

I certify that I have taken all reasonable precautions to make sure that my work has

not been copied by other students

I confirm that I have understood the College’s regulations on plagiarism

I confirm that research resources are fully acknowledged

Signature: ……………………………………… Date: ………………………………

‘Plagiarism’ is presenting somebody else’s work as your own. It includes copying

information directly from the Web or books without referencing the material;

submitting joint coursework as an individual effort; copying another student’s

coursework; stealing coursework from another student and submitting it as your own

work.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

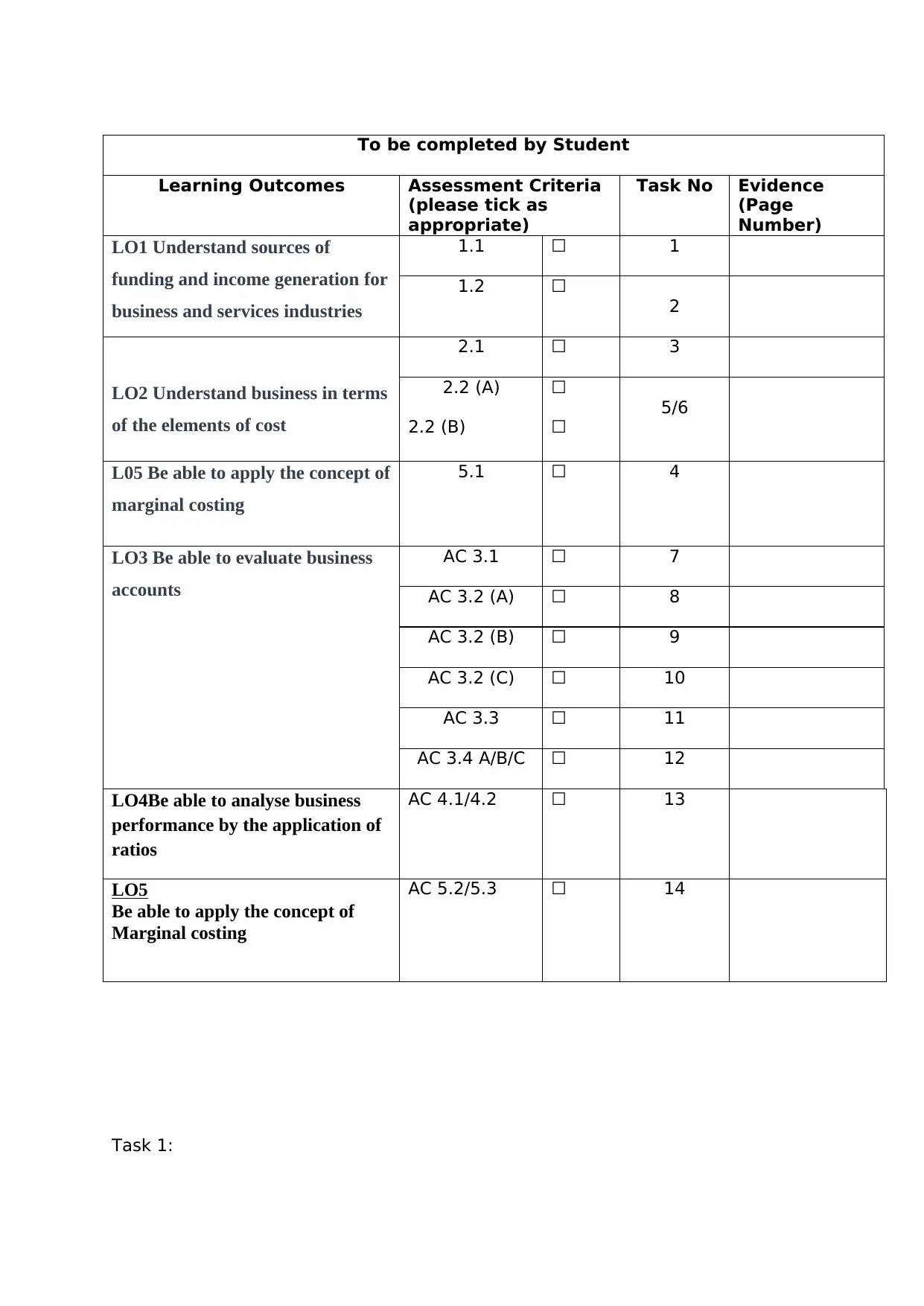

To be completed by Student

Learning Outcomes Assessment Criteria

(please tick as

appropriate)

Task No Evidence

(Page

Number)

LO1 Understand sources of

funding and income generation for

business and services industries

1.1 ☐ 1

1.2 ☐

2

LO2 Understand business in terms

of the elements of cost

2.1 ☐ 3

2.2 (A)

2.2 (B)

☐

☐

5/6

L05 Be able to apply the concept of

marginal costing

5.1 ☐ 4

LO3 Be able to evaluate business

accounts

AC 3.1 ☐ 7

AC 3.2 (A) ☐ 8

AC 3.2 (B) ☐ 9

AC 3.2 (C) ☐ 10

AC 3.3 ☐ 11

AC 3.4 A/B/C ☐ 12

LO4Be able to analyse business

performance by the application of

ratios

AC 4.1/4.2 ☐ 13

LO5

Be able to apply the concept of

Marginal costing

AC 5.2/5.3 ☐ 14

Task 1:

Learning Outcomes Assessment Criteria

(please tick as

appropriate)

Task No Evidence

(Page

Number)

LO1 Understand sources of

funding and income generation for

business and services industries

1.1 ☐ 1

1.2 ☐

2

LO2 Understand business in terms

of the elements of cost

2.1 ☐ 3

2.2 (A)

2.2 (B)

☐

☐

5/6

L05 Be able to apply the concept of

marginal costing

5.1 ☐ 4

LO3 Be able to evaluate business

accounts

AC 3.1 ☐ 7

AC 3.2 (A) ☐ 8

AC 3.2 (B) ☐ 9

AC 3.2 (C) ☐ 10

AC 3.3 ☐ 11

AC 3.4 A/B/C ☐ 12

LO4Be able to analyse business

performance by the application of

ratios

AC 4.1/4.2 ☐ 13

LO5

Be able to apply the concept of

Marginal costing

AC 5.2/5.3 ☐ 14

Task 1:

AC1.1 review 4 sources (2 internal and 2 external sources) of

funding available to business and services industries.

(maximum word count – 350/ at least 1 reference required)

Internal source of funds are generated from the internal sources and

external sources of funds are generated from 3rd part or outside sources. 2

internal sources of funding those are available to the service industries or

businesses are –

Love money – love money or the money borrowed from spouse, family and friends is a

popular source of funding that is generally repaid once the business starts earning sufficient

profits. This arrangement can be cheaper and quicker and the terms of repayment may be

flexible as compared to bank loan. However, borrowing though love money may raise stress

for the entrepreneur, specifically if business does not perform well.

Personal investment – while starting-up a business the owner himself or herself can

contribute to the business fund through cash or through collateral of his or her asset. It is

the most cost effective and easiest way of raising fund while raising fund from bank is

comparatively difficult (Brown and Lee 2019).

2 external sources of funding those are available to the service industries

or businesses are –

Bank loan – it is widely used external source of fund for business and service industries. Bank

provides short term as well as long term loans to the business in exchange of interest

payment at specific rate to be paid on monthly or quarterly or annual basis. However, to

raise fund through bank loan the business shall have excellent credit score and sound track

records. Further, in case of start-up business the bank requires the personal guarantee or

collateral of asset from the entrepreneur.

Angels – generally, angels are the retired company executives or the wealthy individuals

those invest in the small firms of others directly. Generally they are the leaders in their own

sector and hence they contribute their network for the contact as well as their skills and

knowledge. However, in exchange, they supervise the management practices of the business

that is they hold a position in the board of directors of the company (Dastory, Schäfer and

Stephan 2018).

funding available to business and services industries.

(maximum word count – 350/ at least 1 reference required)

Internal source of funds are generated from the internal sources and

external sources of funds are generated from 3rd part or outside sources. 2

internal sources of funding those are available to the service industries or

businesses are –

Love money – love money or the money borrowed from spouse, family and friends is a

popular source of funding that is generally repaid once the business starts earning sufficient

profits. This arrangement can be cheaper and quicker and the terms of repayment may be

flexible as compared to bank loan. However, borrowing though love money may raise stress

for the entrepreneur, specifically if business does not perform well.

Personal investment – while starting-up a business the owner himself or herself can

contribute to the business fund through cash or through collateral of his or her asset. It is

the most cost effective and easiest way of raising fund while raising fund from bank is

comparatively difficult (Brown and Lee 2019).

2 external sources of funding those are available to the service industries

or businesses are –

Bank loan – it is widely used external source of fund for business and service industries. Bank

provides short term as well as long term loans to the business in exchange of interest

payment at specific rate to be paid on monthly or quarterly or annual basis. However, to

raise fund through bank loan the business shall have excellent credit score and sound track

records. Further, in case of start-up business the bank requires the personal guarantee or

collateral of asset from the entrepreneur.

Angels – generally, angels are the retired company executives or the wealthy individuals

those invest in the small firms of others directly. Generally they are the leaders in their own

sector and hence they contribute their network for the contact as well as their skills and

knowledge. However, in exchange, they supervise the management practices of the business

that is they hold a position in the board of directors of the company (Dastory, Schäfer and

Stephan 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 2:

AC1.2 evaluate the contribution made by a range of methods of

generating income within a given business and services

operation (maximum word count – 300 excluding calculation)

Different methods of generating the income help the business to generate

earnings from other sources if any particular source is not sufficient or stops

generating any further earnings. Various forms of generating the income from

service or business operation are as follows –

Sales income or revenues – sales revenues are realized by the business through selling of the

products or providing services to the customers. For any business sales revenue is generally

the major source of income. Sales revenues are parted into gross sales that is, the total sales

and the net sales that is the sales reduced by the sales discounts, sales returns and any other

allowances.

Sub-letting – rent received from the tenant under sublease is rental income from subletting

and it shall be reported as income. If tenant pays the expenses the receiver is obliged to pay

the same pursuant to lease and the payment from tenant is considered as income.

Commission – commission income is the fees earned by the agents and brojers in making the

sales or in closing any deal. It is primary revenue account for stock brokers; real estate

brokers and insurance agencies.

Sponsorship – sponsorship income received from a sponsor is popular way of income. It

refers to the support, whether in form of finance or in form of services and goods offered by

businesses or public members.

Royalties – royalty income is the payment received in consideration of usage and

exploitation of the literary or artistic works, mineral rights or patents. It is dependent upon

the type of the business carried upon by the entity. It is generally of 2 types – royalties

received for usage of patents, trademarks or copyrights and royalties received for usage of

minerals, gas or oil (Cooper et al. 2016).

Capital gains – capital gain is increase in value of any capital asset that provides it higher

value as compared to the asset’s purchase price. However, such gain is not reported until

asset is sold. Capital gain can be long-term as well as short term. It is a common practice for

many businesses to use the business profits for the purpose of investment. There always

exists a chance that the investment will earn profit in the form of capital gains. This generally

takes place in case when the entity buys and sells the stocks, invest in mutual funds or in real

estate. It can be considered as a big source for income and the applicable tax rate on capital

gain is different as compared to regular income (Sharma and Sharma 2017).

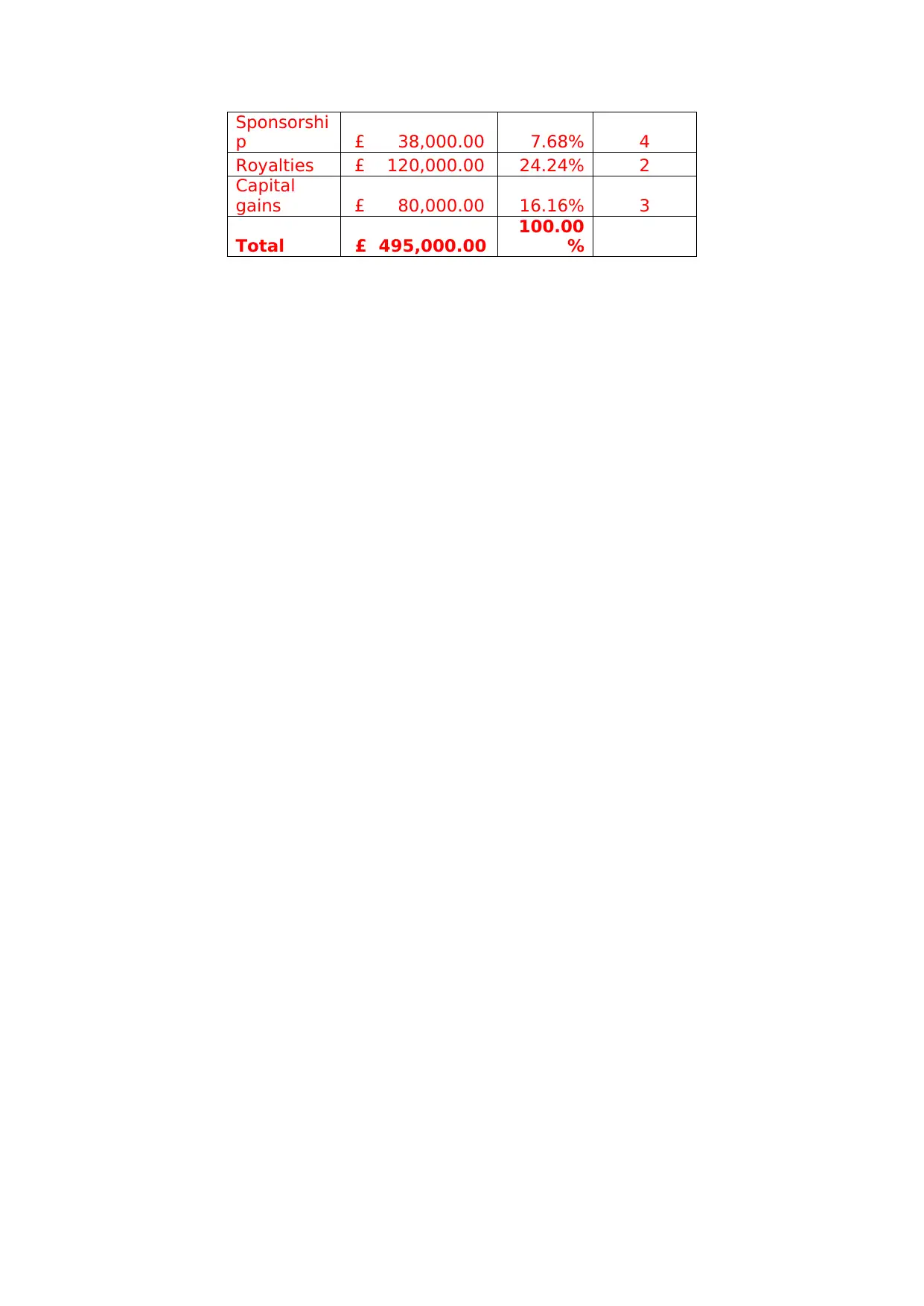

Contribution made by different methods for generating income –

Income Amount

Percent

age Ranking

Sales

revenue £ 200,000.00 40.40% 1

Subletting £ 35,000.00 7.07% 5

Commissio

n £ 22,000.00 4.44% 6

AC1.2 evaluate the contribution made by a range of methods of

generating income within a given business and services

operation (maximum word count – 300 excluding calculation)

Different methods of generating the income help the business to generate

earnings from other sources if any particular source is not sufficient or stops

generating any further earnings. Various forms of generating the income from

service or business operation are as follows –

Sales income or revenues – sales revenues are realized by the business through selling of the

products or providing services to the customers. For any business sales revenue is generally

the major source of income. Sales revenues are parted into gross sales that is, the total sales

and the net sales that is the sales reduced by the sales discounts, sales returns and any other

allowances.

Sub-letting – rent received from the tenant under sublease is rental income from subletting

and it shall be reported as income. If tenant pays the expenses the receiver is obliged to pay

the same pursuant to lease and the payment from tenant is considered as income.

Commission – commission income is the fees earned by the agents and brojers in making the

sales or in closing any deal. It is primary revenue account for stock brokers; real estate

brokers and insurance agencies.

Sponsorship – sponsorship income received from a sponsor is popular way of income. It

refers to the support, whether in form of finance or in form of services and goods offered by

businesses or public members.

Royalties – royalty income is the payment received in consideration of usage and

exploitation of the literary or artistic works, mineral rights or patents. It is dependent upon

the type of the business carried upon by the entity. It is generally of 2 types – royalties

received for usage of patents, trademarks or copyrights and royalties received for usage of

minerals, gas or oil (Cooper et al. 2016).

Capital gains – capital gain is increase in value of any capital asset that provides it higher

value as compared to the asset’s purchase price. However, such gain is not reported until

asset is sold. Capital gain can be long-term as well as short term. It is a common practice for

many businesses to use the business profits for the purpose of investment. There always

exists a chance that the investment will earn profit in the form of capital gains. This generally

takes place in case when the entity buys and sells the stocks, invest in mutual funds or in real

estate. It can be considered as a big source for income and the applicable tax rate on capital

gain is different as compared to regular income (Sharma and Sharma 2017).

Contribution made by different methods for generating income –

Income Amount

Percent

age Ranking

Sales

revenue £ 200,000.00 40.40% 1

Subletting £ 35,000.00 7.07% 5

Commissio

n £ 22,000.00 4.44% 6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sponsorshi

p £ 38,000.00 7.68% 4

Royalties £ 120,000.00 24.24% 2

Capital

gains £ 80,000.00 16.16% 3

Total £ 495,000.00

100.00

%

p £ 38,000.00 7.68% 4

Royalties £ 120,000.00 24.24% 2

Capital

gains £ 80,000.00 16.16% 3

Total £ 495,000.00

100.00

%

Task 3:

AC 2.1-Discuss what is meant by direct costs and indirect costs.

List all your business costs and identify which are direct costs

and which are indirect costs. (maximum word count 250)

Direct cost – Direct costs are defined as the costs those can be traced accurately

with the cost object easily. Here the cost object can be product, department or

any project. Generally the direct cost benefits the single cost object and hence,

segregation of any cost as indirect or as direct shall be done through taking into

consideration the cost object. However, any particular cost can be the direct cost

for one object whereas the same can be indirect for any other object. Most of the

direct costs are variable in nature; however, it may not be the case always. For

instance, supervisor’s salary for a particular month who only supervised

construction of a particular building is direct fixed cost that is incurred for the

building (Costabile et al. 2017).

Indirect cost – costs those cannot be allocated to any specific cost object

accurately is known as indirect cost. Indirect cost generally benefits the multiple

cost objects and hence, it is practically not possible to trace them accurately to

any individual product, department or project. Indirect costs do not differ

substantially within certain volumes of production or activities and are therefore

generally the indirect costs are of fixed nature (Thompson et al. 2016).

All the business costs of The Restaurant Group Plc include cost of sales,

administrative costs and interest cost. Here, costs of sales are direct costs and

the administrative costs and interest expenses are indirect costs.

AC 2.1-Discuss what is meant by direct costs and indirect costs.

List all your business costs and identify which are direct costs

and which are indirect costs. (maximum word count 250)

Direct cost – Direct costs are defined as the costs those can be traced accurately

with the cost object easily. Here the cost object can be product, department or

any project. Generally the direct cost benefits the single cost object and hence,

segregation of any cost as indirect or as direct shall be done through taking into

consideration the cost object. However, any particular cost can be the direct cost

for one object whereas the same can be indirect for any other object. Most of the

direct costs are variable in nature; however, it may not be the case always. For

instance, supervisor’s salary for a particular month who only supervised

construction of a particular building is direct fixed cost that is incurred for the

building (Costabile et al. 2017).

Indirect cost – costs those cannot be allocated to any specific cost object

accurately is known as indirect cost. Indirect cost generally benefits the multiple

cost objects and hence, it is practically not possible to trace them accurately to

any individual product, department or project. Indirect costs do not differ

substantially within certain volumes of production or activities and are therefore

generally the indirect costs are of fixed nature (Thompson et al. 2016).

All the business costs of The Restaurant Group Plc include cost of sales,

administrative costs and interest cost. Here, costs of sales are direct costs and

the administrative costs and interest expenses are indirect costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

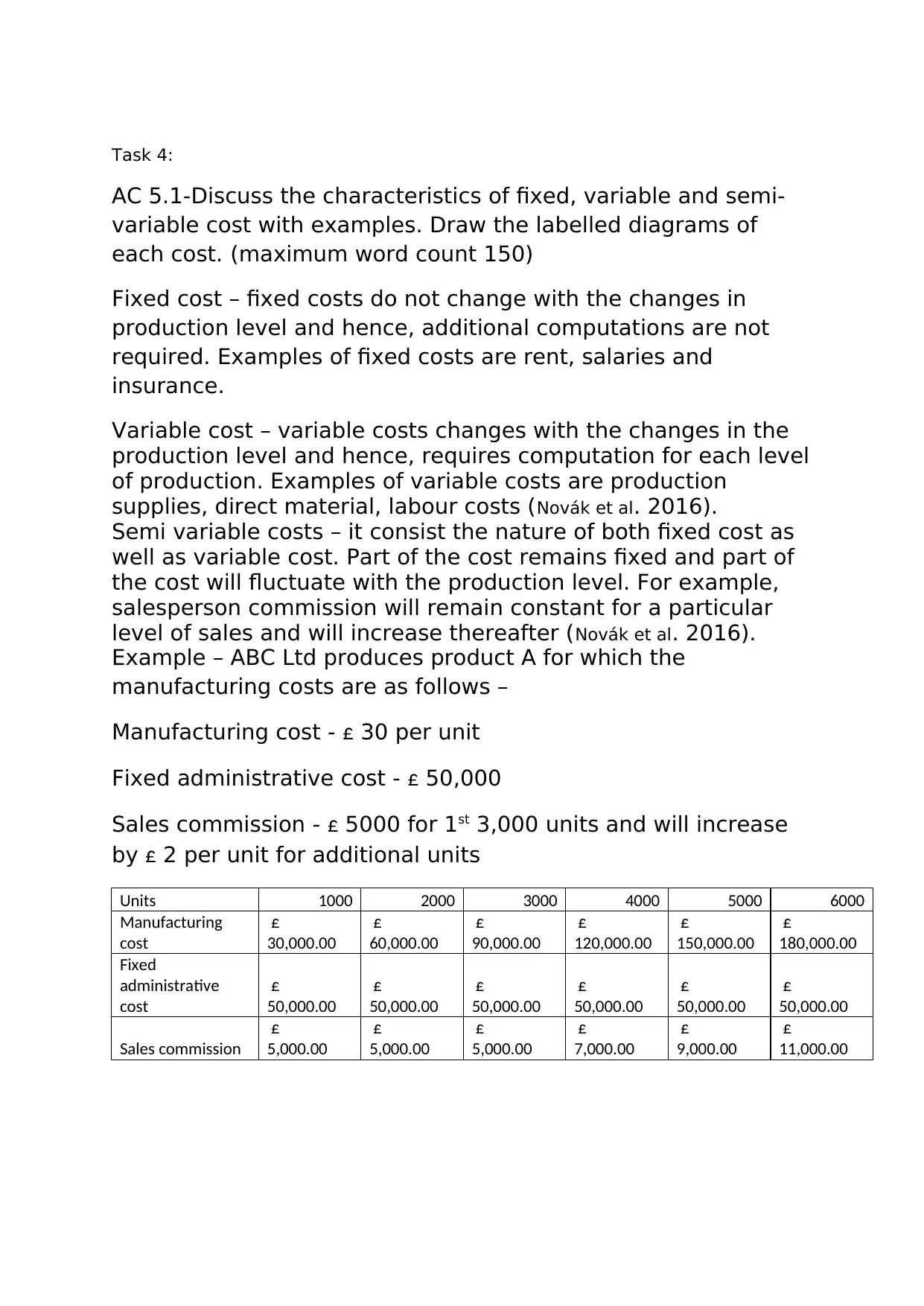

Task 4:

AC 5.1-Discuss the characteristics of fixed, variable and semi-

variable cost with examples. Draw the labelled diagrams of

each cost. (maximum word count 150)

Fixed cost – fixed costs do not change with the changes in

production level and hence, additional computations are not

required. Examples of fixed costs are rent, salaries and

insurance.

Variable cost – variable costs changes with the changes in the

production level and hence, requires computation for each level

of production. Examples of variable costs are production

supplies, direct material, labour costs (Novák et al. 2016).

Semi variable costs – it consist the nature of both fixed cost as

well as variable cost. Part of the cost remains fixed and part of

the cost will fluctuate with the production level. For example,

salesperson commission will remain constant for a particular

level of sales and will increase thereafter (Novák et al. 2016).

Example – ABC Ltd produces product A for which the

manufacturing costs are as follows –

Manufacturing cost - £ 30 per unit

Fixed administrative cost - £ 50,000

Sales commission - £ 5000 for 1st 3,000 units and will increase

by £ 2 per unit for additional units

Units 1000 2000 3000 4000 5000 6000

Manufacturing

cost

£

30,000.00

£

60,000.00

£

90,000.00

£

120,000.00

£

150,000.00

£

180,000.00

Fixed

administrative

cost

£

50,000.00

£

50,000.00

£

50,000.00

£

50,000.00

£

50,000.00

£

50,000.00

Sales commission

£

5,000.00

£

5,000.00

£

5,000.00

£

7,000.00

£

9,000.00

£

11,000.00

AC 5.1-Discuss the characteristics of fixed, variable and semi-

variable cost with examples. Draw the labelled diagrams of

each cost. (maximum word count 150)

Fixed cost – fixed costs do not change with the changes in

production level and hence, additional computations are not

required. Examples of fixed costs are rent, salaries and

insurance.

Variable cost – variable costs changes with the changes in the

production level and hence, requires computation for each level

of production. Examples of variable costs are production

supplies, direct material, labour costs (Novák et al. 2016).

Semi variable costs – it consist the nature of both fixed cost as

well as variable cost. Part of the cost remains fixed and part of

the cost will fluctuate with the production level. For example,

salesperson commission will remain constant for a particular

level of sales and will increase thereafter (Novák et al. 2016).

Example – ABC Ltd produces product A for which the

manufacturing costs are as follows –

Manufacturing cost - £ 30 per unit

Fixed administrative cost - £ 50,000

Sales commission - £ 5000 for 1st 3,000 units and will increase

by £ 2 per unit for additional units

Units 1000 2000 3000 4000 5000 6000

Manufacturing

cost

£

30,000.00

£

60,000.00

£

90,000.00

£

120,000.00

£

150,000.00

£

180,000.00

Fixed

administrative

cost

£

50,000.00

£

50,000.00

£

50,000.00

£

50,000.00

£

50,000.00

£

50,000.00

Sales commission

£

5,000.00

£

5,000.00

£

5,000.00

£

7,000.00

£

9,000.00

£

11,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1000 2000 3000 4000 5000 6000

£-

£20,000.00

£40,000.00

£60,000.00

£80,000.00

£100,000.00

£120,000.00

£140,000.00

£160,000.00

£180,000.00

£200,000.00

Manufacturing cost

Manufacturing cost

(Figure 1 - Diagram for variable cost)

(Source: Created by author)

1000 2000 3000 4000 5000 6000

£-

£10,000.00

£20,000.00

£30,000.00

£40,000.00

£50,000.00

£60,000.00

Administrative cost

Administrative cost

(Figure 2 - Diagram for fixed cost)

(Source: Created by author)

£-

£20,000.00

£40,000.00

£60,000.00

£80,000.00

£100,000.00

£120,000.00

£140,000.00

£160,000.00

£180,000.00

£200,000.00

Manufacturing cost

Manufacturing cost

(Figure 1 - Diagram for variable cost)

(Source: Created by author)

1000 2000 3000 4000 5000 6000

£-

£10,000.00

£20,000.00

£30,000.00

£40,000.00

£50,000.00

£60,000.00

Administrative cost

Administrative cost

(Figure 2 - Diagram for fixed cost)

(Source: Created by author)

1000 2000 3000 4000 5000 6000

£-

£2,000.00

£4,000.00

£6,000.00

£8,000.00

£10,000.00

£12,000.00

Sales commission

Sales commission

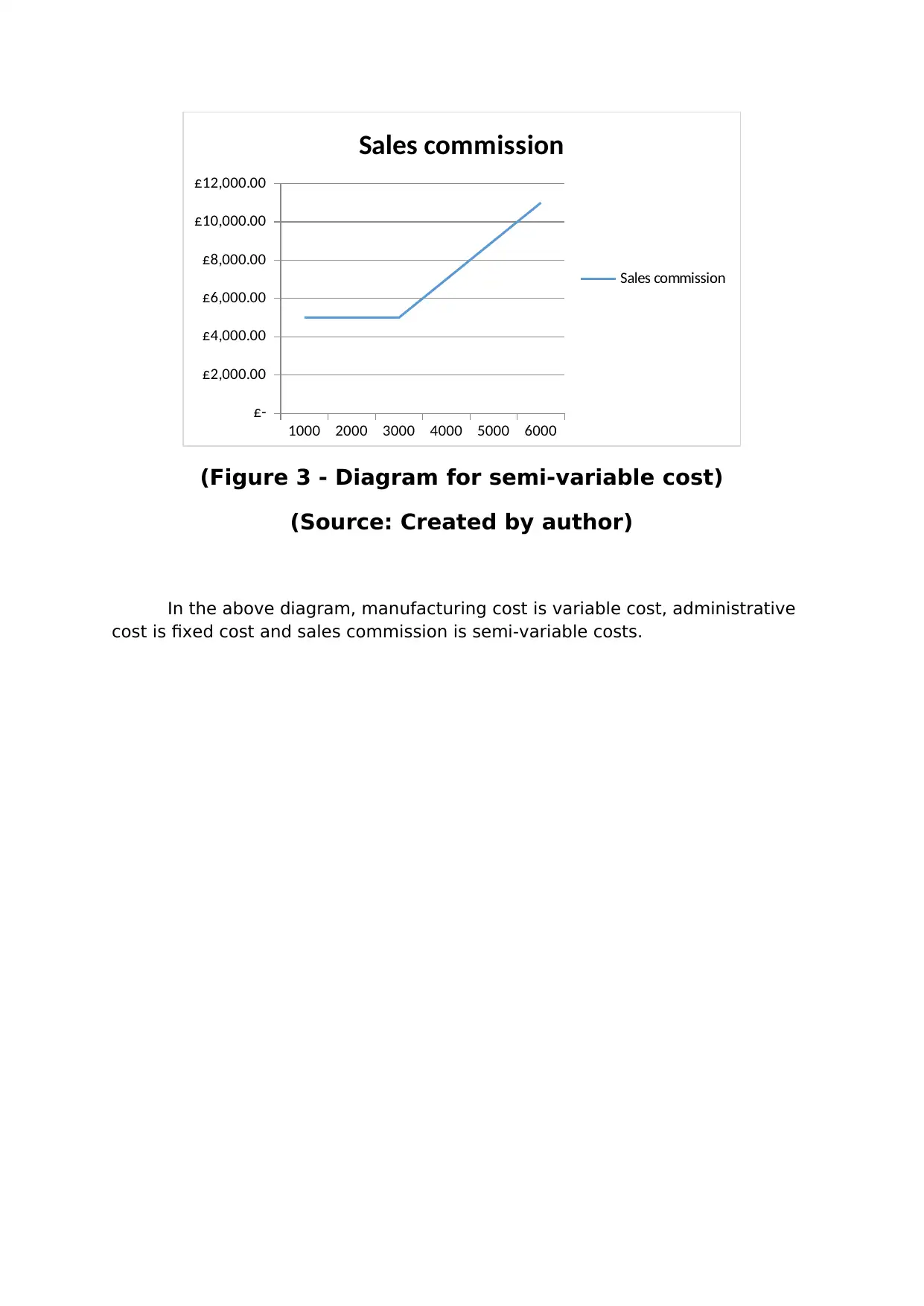

(Figure 3 - Diagram for semi-variable cost)

(Source: Created by author)

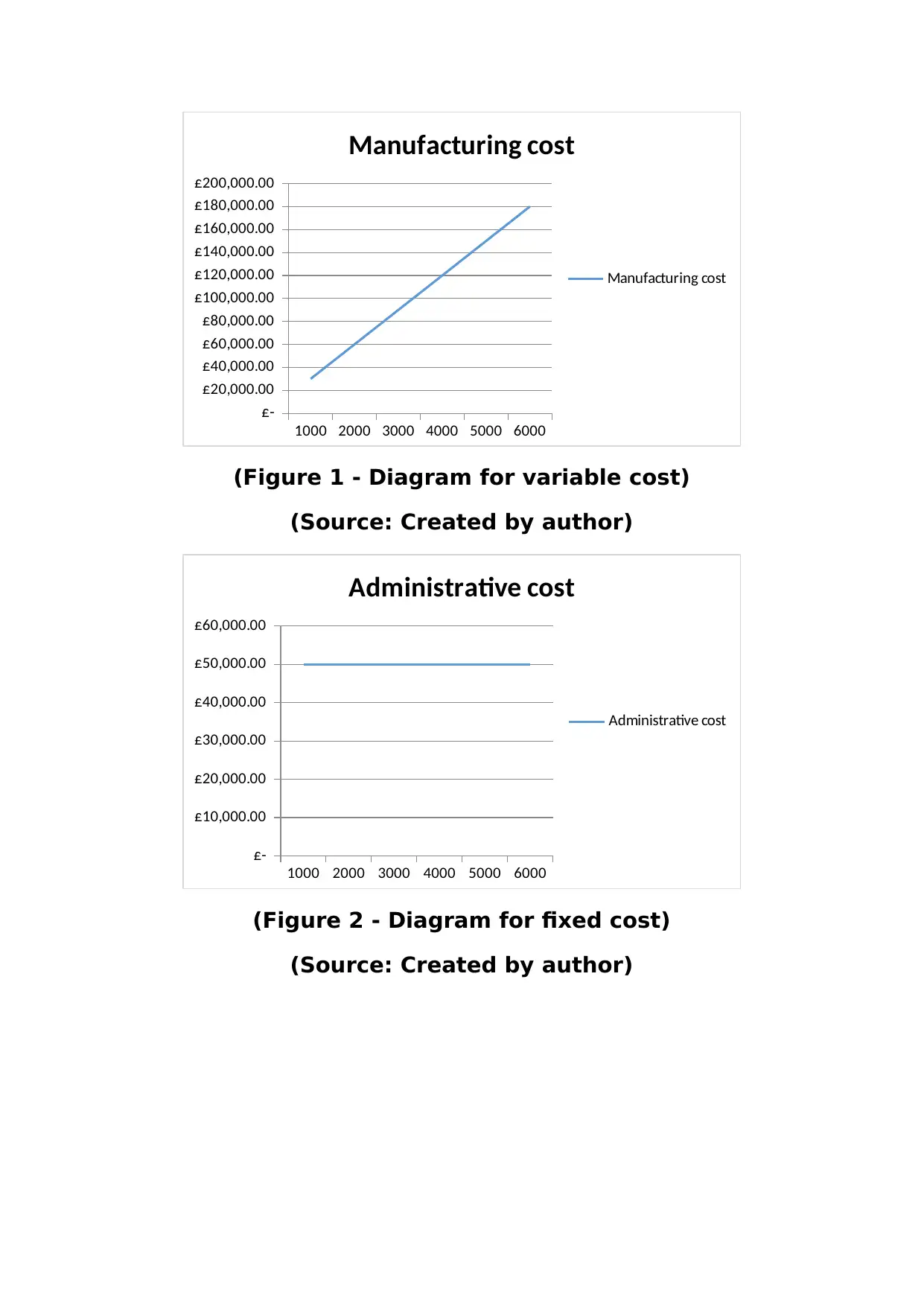

In the above diagram, manufacturing cost is variable cost, administrative

cost is fixed cost and sales commission is semi-variable costs.

£-

£2,000.00

£4,000.00

£6,000.00

£8,000.00

£10,000.00

£12,000.00

Sales commission

Sales commission

(Figure 3 - Diagram for semi-variable cost)

(Source: Created by author)

In the above diagram, manufacturing cost is variable cost, administrative

cost is fixed cost and sales commission is semi-variable costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 5:

AC 2.2 (A) Evaluate methods of controlling stock (maximum

word count 350/ at least 1 reference required)

Various methods are there for controlling the stock those are

designed for providing the efficient system to decide when,

what and how much order to be placed. Based on the type of

stock any of the following or mix of 2 or more methods can be

follows –

Just-in-time order – main objective of JIT is reducing the costs

through cutting the stock to minimum. Under this system the

items are delivered when they are actually required for

production and are immediately used upon receipt. However, it

includes the risk of running out of the stock and hence, the

purchaser shall be confident enough that the supplies will be

received on time. Various advantages of JIT system are – (i) it

leads to minimum amounts for inventory obsolescence as high

rate of inventory turnover keeps inventory as idle and in turn

will become obsolete (ii) low level of inventory will reduce the

holding costs (iii) as the required level of inventory is low, the

entity is required to invest less amount of cash for inventory (Lai

and Cheng 2016).

First – in – first – out – under this method goods purchased 1st or

the goods entered into stock 1st are used 1st for and the goods

entered last are used later. This system assures that the

perishable stocks of the company are efficiently used and it

does not get deteriorated. Stocks under this method are

recognised through the receipt date and moves through each

production stage following strict order (Muller 2019).

AC 2.2 (A) Evaluate methods of controlling stock (maximum

word count 350/ at least 1 reference required)

Various methods are there for controlling the stock those are

designed for providing the efficient system to decide when,

what and how much order to be placed. Based on the type of

stock any of the following or mix of 2 or more methods can be

follows –

Just-in-time order – main objective of JIT is reducing the costs

through cutting the stock to minimum. Under this system the

items are delivered when they are actually required for

production and are immediately used upon receipt. However, it

includes the risk of running out of the stock and hence, the

purchaser shall be confident enough that the supplies will be

received on time. Various advantages of JIT system are – (i) it

leads to minimum amounts for inventory obsolescence as high

rate of inventory turnover keeps inventory as idle and in turn

will become obsolete (ii) low level of inventory will reduce the

holding costs (iii) as the required level of inventory is low, the

entity is required to invest less amount of cash for inventory (Lai

and Cheng 2016).

First – in – first – out – under this method goods purchased 1st or

the goods entered into stock 1st are used 1st for and the goods

entered last are used later. This system assures that the

perishable stocks of the company are efficiently used and it

does not get deteriorated. Stocks under this method are

recognised through the receipt date and moves through each

production stage following strict order (Muller 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 6:

AC 2.2 (B) Evaluate methods of controlling cash (maximum

word count 250)

Various methods of controlling the cash flow are as follows –

Fast payment by the customers - For improving the cash

inflow, collection from the customers shall be fast and

prompt. It is possible through prompt billing and the

customers shall be informed promptly regarding the

payable amount and time by which the payment shall be

paid. Company may allow discount to the customers

making payment before due date. It will influence the

customers to make early payment (da Costa Moraes, Nagano

and Sobreiro 2015).

Decentralisation of collections – any big size firm that is

operating over the large geographical location can

enhance the cash flow through using the decentralised

system of collection. Different collection centres can be

opened under different locations rather than opening one

collection centre in one area. The idea behind this is

reducing mailing time from the customer’s despatch of the

cheques and its receipt in the company and further

reducing the collection time of cheques.

Fast conversion of the payment into cash – cash control

can be enhanced through improvement of the collection

procedure. Once a cheque is received from the customer it

shall be deposited immediately for collection. If the time

gap between collection of cheque and its collection is

reduced the cash control system will be improved (Cheung

2016).

AC 2.2 (B) Evaluate methods of controlling cash (maximum

word count 250)

Various methods of controlling the cash flow are as follows –

Fast payment by the customers - For improving the cash

inflow, collection from the customers shall be fast and

prompt. It is possible through prompt billing and the

customers shall be informed promptly regarding the

payable amount and time by which the payment shall be

paid. Company may allow discount to the customers

making payment before due date. It will influence the

customers to make early payment (da Costa Moraes, Nagano

and Sobreiro 2015).

Decentralisation of collections – any big size firm that is

operating over the large geographical location can

enhance the cash flow through using the decentralised

system of collection. Different collection centres can be

opened under different locations rather than opening one

collection centre in one area. The idea behind this is

reducing mailing time from the customer’s despatch of the

cheques and its receipt in the company and further

reducing the collection time of cheques.

Fast conversion of the payment into cash – cash control

can be enhanced through improvement of the collection

procedure. Once a cheque is received from the customer it

shall be deposited immediately for collection. If the time

gap between collection of cheque and its collection is

reduced the cash control system will be improved (Cheung

2016).

ASSIGNMENT 2

Task 7:

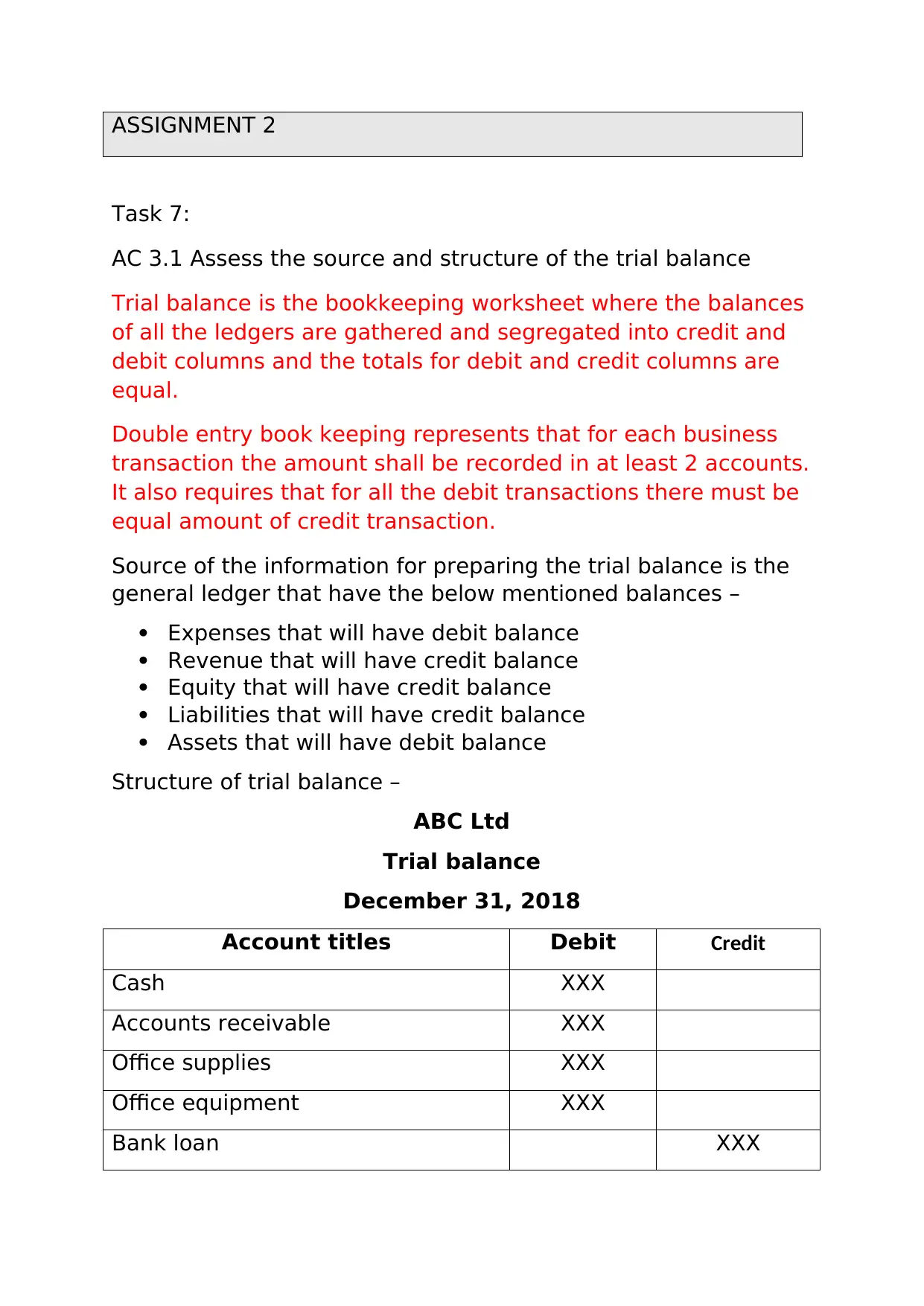

AC 3.1 Assess the source and structure of the trial balance

Trial balance is the bookkeeping worksheet where the balances

of all the ledgers are gathered and segregated into credit and

debit columns and the totals for debit and credit columns are

equal.

Double entry book keeping represents that for each business

transaction the amount shall be recorded in at least 2 accounts.

It also requires that for all the debit transactions there must be

equal amount of credit transaction.

Source of the information for preparing the trial balance is the

general ledger that have the below mentioned balances –

Expenses that will have debit balance

Revenue that will have credit balance

Equity that will have credit balance

Liabilities that will have credit balance

Assets that will have debit balance

Structure of trial balance –

ABC Ltd

Trial balance

December 31, 2018

Account titles Debit Credit

Cash XXX

Accounts receivable XXX

Office supplies XXX

Office equipment XXX

Bank loan XXX

Task 7:

AC 3.1 Assess the source and structure of the trial balance

Trial balance is the bookkeeping worksheet where the balances

of all the ledgers are gathered and segregated into credit and

debit columns and the totals for debit and credit columns are

equal.

Double entry book keeping represents that for each business

transaction the amount shall be recorded in at least 2 accounts.

It also requires that for all the debit transactions there must be

equal amount of credit transaction.

Source of the information for preparing the trial balance is the

general ledger that have the below mentioned balances –

Expenses that will have debit balance

Revenue that will have credit balance

Equity that will have credit balance

Liabilities that will have credit balance

Assets that will have debit balance

Structure of trial balance –

ABC Ltd

Trial balance

December 31, 2018

Account titles Debit Credit

Cash XXX

Accounts receivable XXX

Office supplies XXX

Office equipment XXX

Bank loan XXX

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.