BM533: Demand-Supply Analysis and 21st Century Business Economics

VerifiedAdded on 2023/06/15

|12

|3062

|321

Report

AI Summary

This report provides a detailed analysis of demand and supply principles, including the law of demand, movement along the demand curve, and changes in the demand curve. It also explores the law of supply, movement along the supply curve, and changes in the supply curve. The report further evaluates and contrasts new ideas and concepts in 21st-century economics with those from previous centuries, linking them to current corporate practices. Neoliberal economics and its focus on wealth inequality are compared to traditional economic models. The document concludes by emphasizing the importance of maintaining economic equilibrium and leveraging investment for effective economic growth. This student-contributed assignment is available on Desklib, a platform offering a wide array of study tools and resources for students.

Contemporary business

economics

economics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

TASK 1........................................................................................................................................1

TASK 2........................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

TASK 1........................................................................................................................................1

TASK 2........................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Demand is an economics framework which explains the myriad of factors to be bought and

the amount each person is prepared to spend (Babic-Hodovic, Arslanagic-Kalajdzic and

Imsirpasic, 2017). The quantity of goods which a company must provide in addition to achieve

its profit is referred to as availability. Demand and supply principles are established in the

present questioning. Several charts would be used to illustrate changes in supplied or

consumption trends. Current macroeconomic models would also be examined in the foregoing

report.

MAIN BODY

TASK 1

Demand and supply are the two most important economics words. Companies can choose

how assets are employed and performing regular operations in such ecosystems.

Law of demand- The quantity demanded illustrates how customers' preferences change

when prices rise. If other factors consistently influence consumption and the cost of a product

rises, it leads to the decrease in item or service particular consumers. This is typical client desire

pattern. Because all other circumstances remain constant, the quantity sought by a product is

equal to the cost of a product, according to the quantity required. This implies that as costs

increase, interest falls. The law of consumption states that cost increases impact the number

purchased. This means that if firms charge greater costs for their activities and goods, consumers

might be less likely to acquire them, resulting in a fall in volume of goods. Decreased effective

usage is primarily to blame for this shift in demands (Cavicchioli, 2018). The consumption

criterion is crucial in economy growth policy. The efficient allocation of assets in an industry is

established using the availability principle, and the best cost and volume are discovered. The

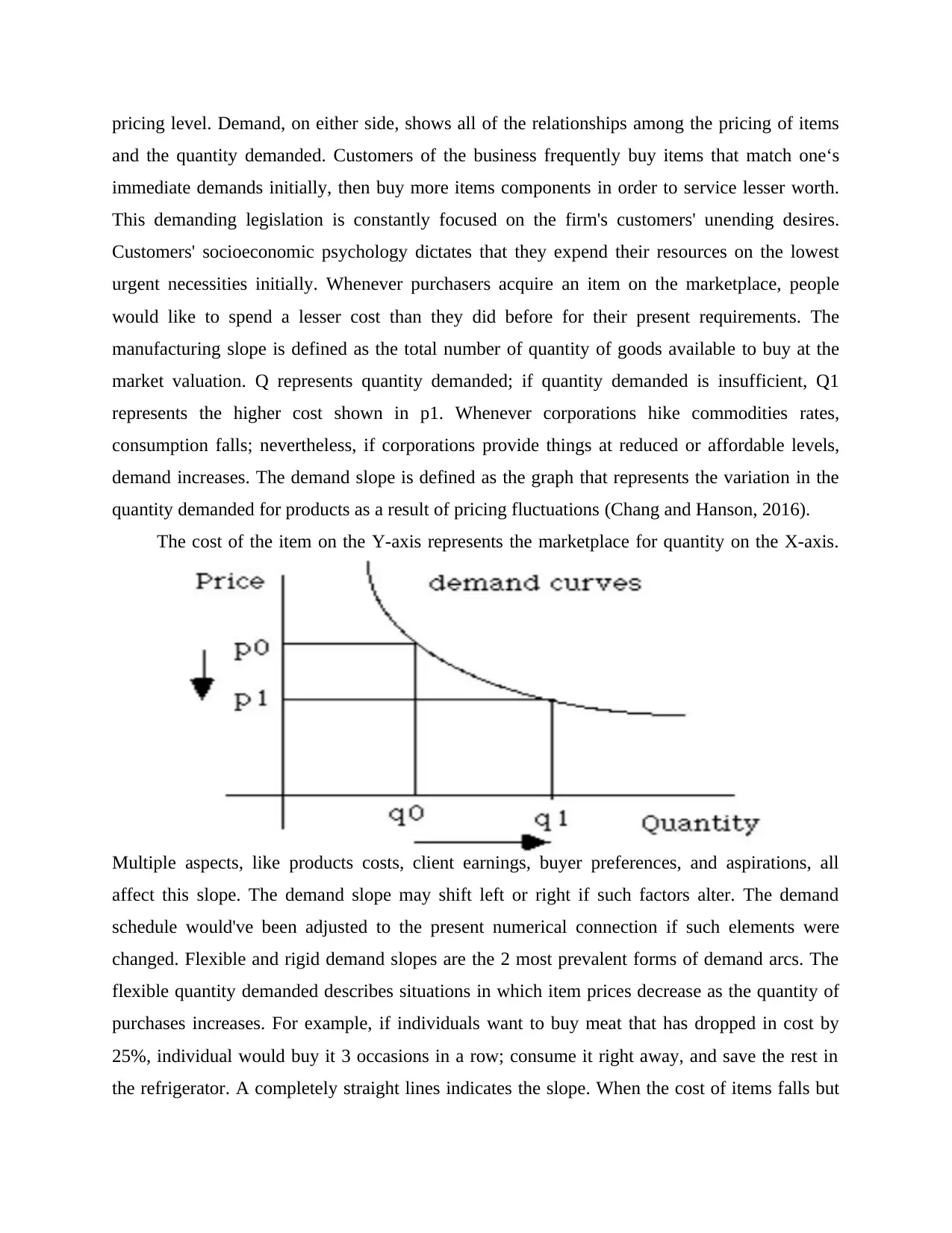

chart is a slope that shows the relationship among the amount demanded and the cost of a

product. The consumption slope's form varies depending on the item. The quantity demanded is

frequently curved in shape. In several economics books, however, a consumption slope has still

been depicted as a single direction. The x-axis represents the quantity required, while the y-axis

represents the cost. The explanation of the rule of consumption predicts a falling quantity

demanded. The difference among the volume requested and the volume necessary should be

identified. The required volume refers to the number of goods available to buy at a specific

Demand is an economics framework which explains the myriad of factors to be bought and

the amount each person is prepared to spend (Babic-Hodovic, Arslanagic-Kalajdzic and

Imsirpasic, 2017). The quantity of goods which a company must provide in addition to achieve

its profit is referred to as availability. Demand and supply principles are established in the

present questioning. Several charts would be used to illustrate changes in supplied or

consumption trends. Current macroeconomic models would also be examined in the foregoing

report.

MAIN BODY

TASK 1

Demand and supply are the two most important economics words. Companies can choose

how assets are employed and performing regular operations in such ecosystems.

Law of demand- The quantity demanded illustrates how customers' preferences change

when prices rise. If other factors consistently influence consumption and the cost of a product

rises, it leads to the decrease in item or service particular consumers. This is typical client desire

pattern. Because all other circumstances remain constant, the quantity sought by a product is

equal to the cost of a product, according to the quantity required. This implies that as costs

increase, interest falls. The law of consumption states that cost increases impact the number

purchased. This means that if firms charge greater costs for their activities and goods, consumers

might be less likely to acquire them, resulting in a fall in volume of goods. Decreased effective

usage is primarily to blame for this shift in demands (Cavicchioli, 2018). The consumption

criterion is crucial in economy growth policy. The efficient allocation of assets in an industry is

established using the availability principle, and the best cost and volume are discovered. The

chart is a slope that shows the relationship among the amount demanded and the cost of a

product. The consumption slope's form varies depending on the item. The quantity demanded is

frequently curved in shape. In several economics books, however, a consumption slope has still

been depicted as a single direction. The x-axis represents the quantity required, while the y-axis

represents the cost. The explanation of the rule of consumption predicts a falling quantity

demanded. The difference among the volume requested and the volume necessary should be

identified. The required volume refers to the number of goods available to buy at a specific

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

pricing level. Demand, on either side, shows all of the relationships among the pricing of items

and the quantity demanded. Customers of the business frequently buy items that match one‘s

immediate demands initially, then buy more items components in order to service lesser worth.

This demanding legislation is constantly focused on the firm's customers' unending desires.

Customers' socioeconomic psychology dictates that they expend their resources on the lowest

urgent necessities initially. Whenever purchasers acquire an item on the marketplace, people

would like to spend a lesser cost than they did before for their present requirements. The

manufacturing slope is defined as the total number of quantity of goods available to buy at the

market valuation. Q represents quantity demanded; if quantity demanded is insufficient, Q1

represents the higher cost shown in p1. Whenever corporations hike commodities rates,

consumption falls; nevertheless, if corporations provide things at reduced or affordable levels,

demand increases. The demand slope is defined as the graph that represents the variation in the

quantity demanded for products as a result of pricing fluctuations (Chang and Hanson, 2016).

The cost of the item on the Y-axis represents the marketplace for quantity on the X-axis.

Multiple aspects, like products costs, client earnings, buyer preferences, and aspirations, all

affect this slope. The demand slope may shift left or right if such factors alter. The demand

schedule would've been adjusted to the present numerical connection if such elements were

changed. Flexible and rigid demand slopes are the 2 most prevalent forms of demand arcs. The

flexible quantity demanded describes situations in which item prices decrease as the quantity of

purchases increases. For example, if individuals want to buy meat that has dropped in cost by

25%, individual would buy it 3 occasions in a row; consume it right away, and save the rest in

the refrigerator. A completely straight lines indicates the slope. When the cost of items falls but

and the quantity demanded. Customers of the business frequently buy items that match one‘s

immediate demands initially, then buy more items components in order to service lesser worth.

This demanding legislation is constantly focused on the firm's customers' unending desires.

Customers' socioeconomic psychology dictates that they expend their resources on the lowest

urgent necessities initially. Whenever purchasers acquire an item on the marketplace, people

would like to spend a lesser cost than they did before for their present requirements. The

manufacturing slope is defined as the total number of quantity of goods available to buy at the

market valuation. Q represents quantity demanded; if quantity demanded is insufficient, Q1

represents the higher cost shown in p1. Whenever corporations hike commodities rates,

consumption falls; nevertheless, if corporations provide things at reduced or affordable levels,

demand increases. The demand slope is defined as the graph that represents the variation in the

quantity demanded for products as a result of pricing fluctuations (Chang and Hanson, 2016).

The cost of the item on the Y-axis represents the marketplace for quantity on the X-axis.

Multiple aspects, like products costs, client earnings, buyer preferences, and aspirations, all

affect this slope. The demand slope may shift left or right if such factors alter. The demand

schedule would've been adjusted to the present numerical connection if such elements were

changed. Flexible and rigid demand slopes are the 2 most prevalent forms of demand arcs. The

flexible quantity demanded describes situations in which item prices decrease as the quantity of

purchases increases. For example, if individuals want to buy meat that has dropped in cost by

25%, individual would buy it 3 occasions in a row; consume it right away, and save the rest in

the refrigerator. A completely straight lines indicates the slope. When the cost of items falls but

the quantity purchased does not, the situation is called inelastic. If the individual decides to get

avocados, for instance, he would only get the limited goods since he understands that large

acquisitions would not meet the need. If avocado costs fall by 25%, people will only be able to

buy the amount of bananas they want. A steeply linear inelastic demand graph is presented.

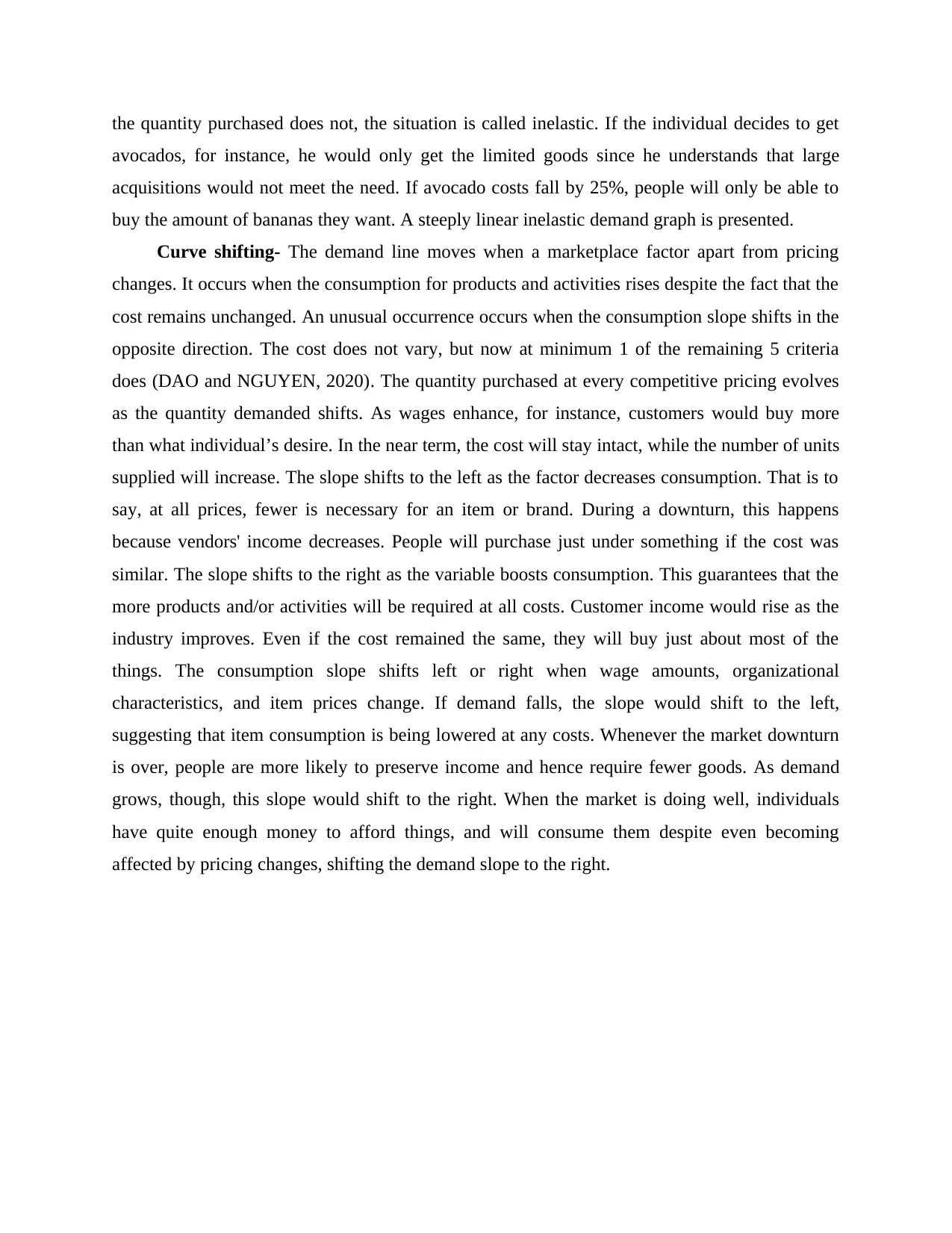

Curve shifting- The demand line moves when a marketplace factor apart from pricing

changes. It occurs when the consumption for products and activities rises despite the fact that the

cost remains unchanged. An unusual occurrence occurs when the consumption slope shifts in the

opposite direction. The cost does not vary, but now at minimum 1 of the remaining 5 criteria

does (DAO and NGUYEN, 2020). The quantity purchased at every competitive pricing evolves

as the quantity demanded shifts. As wages enhance, for instance, customers would buy more

than what individual’s desire. In the near term, the cost will stay intact, while the number of units

supplied will increase. The slope shifts to the left as the factor decreases consumption. That is to

say, at all prices, fewer is necessary for an item or brand. During a downturn, this happens

because vendors' income decreases. People will purchase just under something if the cost was

similar. The slope shifts to the right as the variable boosts consumption. This guarantees that the

more products and/or activities will be required at all costs. Customer income would rise as the

industry improves. Even if the cost remained the same, they will buy just about most of the

things. The consumption slope shifts left or right when wage amounts, organizational

characteristics, and item prices change. If demand falls, the slope would shift to the left,

suggesting that item consumption is being lowered at any costs. Whenever the market downturn

is over, people are more likely to preserve income and hence require fewer goods. As demand

grows, though, this slope would shift to the right. When the market is doing well, individuals

have quite enough money to afford things, and will consume them despite even becoming

affected by pricing changes, shifting the demand slope to the right.

avocados, for instance, he would only get the limited goods since he understands that large

acquisitions would not meet the need. If avocado costs fall by 25%, people will only be able to

buy the amount of bananas they want. A steeply linear inelastic demand graph is presented.

Curve shifting- The demand line moves when a marketplace factor apart from pricing

changes. It occurs when the consumption for products and activities rises despite the fact that the

cost remains unchanged. An unusual occurrence occurs when the consumption slope shifts in the

opposite direction. The cost does not vary, but now at minimum 1 of the remaining 5 criteria

does (DAO and NGUYEN, 2020). The quantity purchased at every competitive pricing evolves

as the quantity demanded shifts. As wages enhance, for instance, customers would buy more

than what individual’s desire. In the near term, the cost will stay intact, while the number of units

supplied will increase. The slope shifts to the left as the factor decreases consumption. That is to

say, at all prices, fewer is necessary for an item or brand. During a downturn, this happens

because vendors' income decreases. People will purchase just under something if the cost was

similar. The slope shifts to the right as the variable boosts consumption. This guarantees that the

more products and/or activities will be required at all costs. Customer income would rise as the

industry improves. Even if the cost remained the same, they will buy just about most of the

things. The consumption slope shifts left or right when wage amounts, organizational

characteristics, and item prices change. If demand falls, the slope would shift to the left,

suggesting that item consumption is being lowered at any costs. Whenever the market downturn

is over, people are more likely to preserve income and hence require fewer goods. As demand

grows, though, this slope would shift to the right. When the market is doing well, individuals

have quite enough money to afford things, and will consume them despite even becoming

affected by pricing changes, shifting the demand slope to the right.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

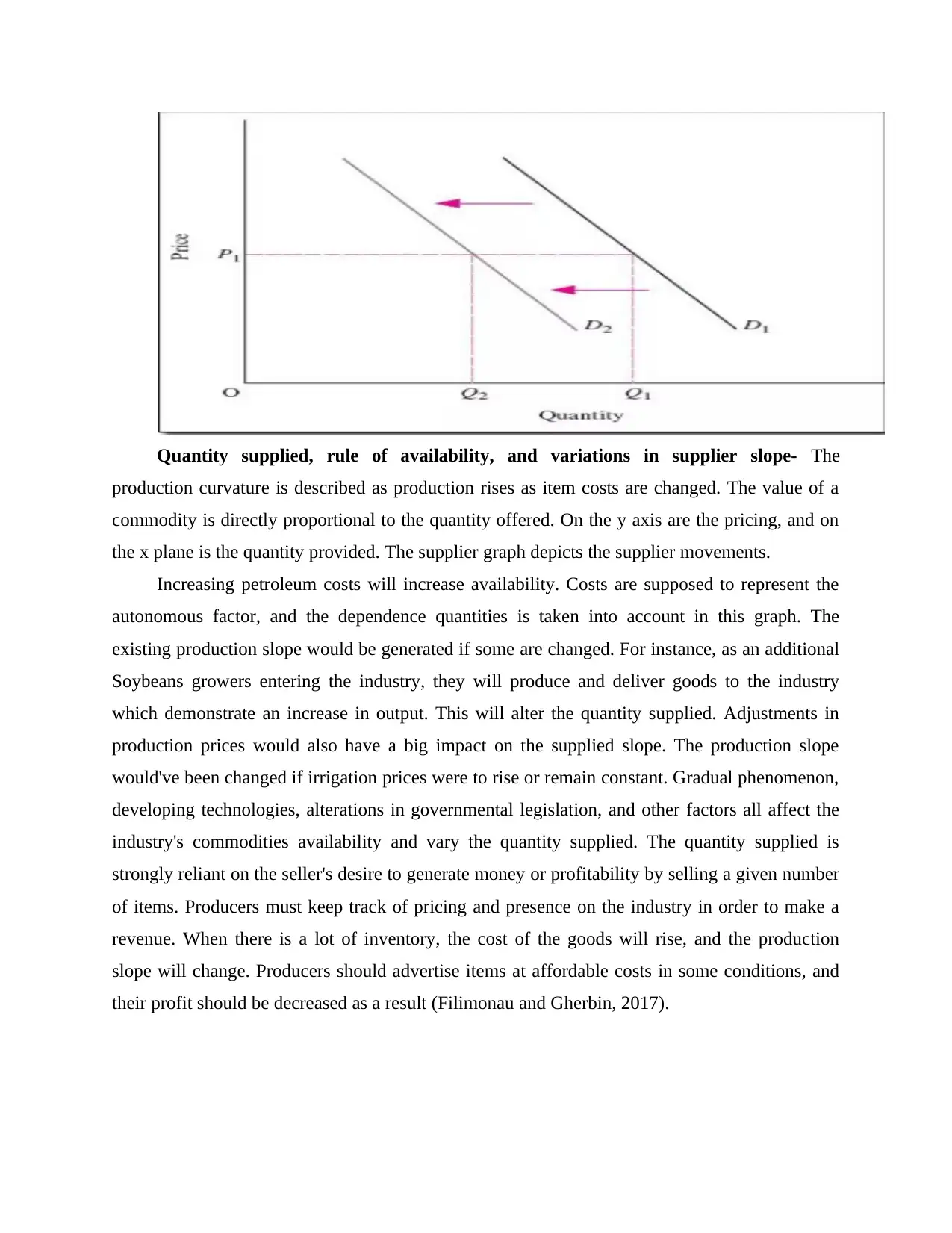

Quantity supplied, rule of availability, and variations in supplier slope- The

production curvature is described as production rises as item costs are changed. The value of a

commodity is directly proportional to the quantity offered. On the y axis are the pricing, and on

the x plane is the quantity provided. The supplier graph depicts the supplier movements.

Increasing petroleum costs will increase availability. Costs are supposed to represent the

autonomous factor, and the dependence quantities is taken into account in this graph. The

existing production slope would be generated if some are changed. For instance, as an additional

Soybeans growers entering the industry, they will produce and deliver goods to the industry

which demonstrate an increase in output. This will alter the quantity supplied. Adjustments in

production prices would also have a big impact on the supplied slope. The production slope

would've been changed if irrigation prices were to rise or remain constant. Gradual phenomenon,

developing technologies, alterations in governmental legislation, and other factors all affect the

industry's commodities availability and vary the quantity supplied. The quantity supplied is

strongly reliant on the seller's desire to generate money or profitability by selling a given number

of items. Producers must keep track of pricing and presence on the industry in order to make a

revenue. When there is a lot of inventory, the cost of the goods will rise, and the production

slope will change. Producers should advertise items at affordable costs in some conditions, and

their profit should be decreased as a result (Filimonau and Gherbin, 2017).

production curvature is described as production rises as item costs are changed. The value of a

commodity is directly proportional to the quantity offered. On the y axis are the pricing, and on

the x plane is the quantity provided. The supplier graph depicts the supplier movements.

Increasing petroleum costs will increase availability. Costs are supposed to represent the

autonomous factor, and the dependence quantities is taken into account in this graph. The

existing production slope would be generated if some are changed. For instance, as an additional

Soybeans growers entering the industry, they will produce and deliver goods to the industry

which demonstrate an increase in output. This will alter the quantity supplied. Adjustments in

production prices would also have a big impact on the supplied slope. The production slope

would've been changed if irrigation prices were to rise or remain constant. Gradual phenomenon,

developing technologies, alterations in governmental legislation, and other factors all affect the

industry's commodities availability and vary the quantity supplied. The quantity supplied is

strongly reliant on the seller's desire to generate money or profitability by selling a given number

of items. Producers must keep track of pricing and presence on the industry in order to make a

revenue. When there is a lot of inventory, the cost of the goods will rise, and the production

slope will change. Producers should advertise items at affordable costs in some conditions, and

their profit should be decreased as a result (Filimonau and Gherbin, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

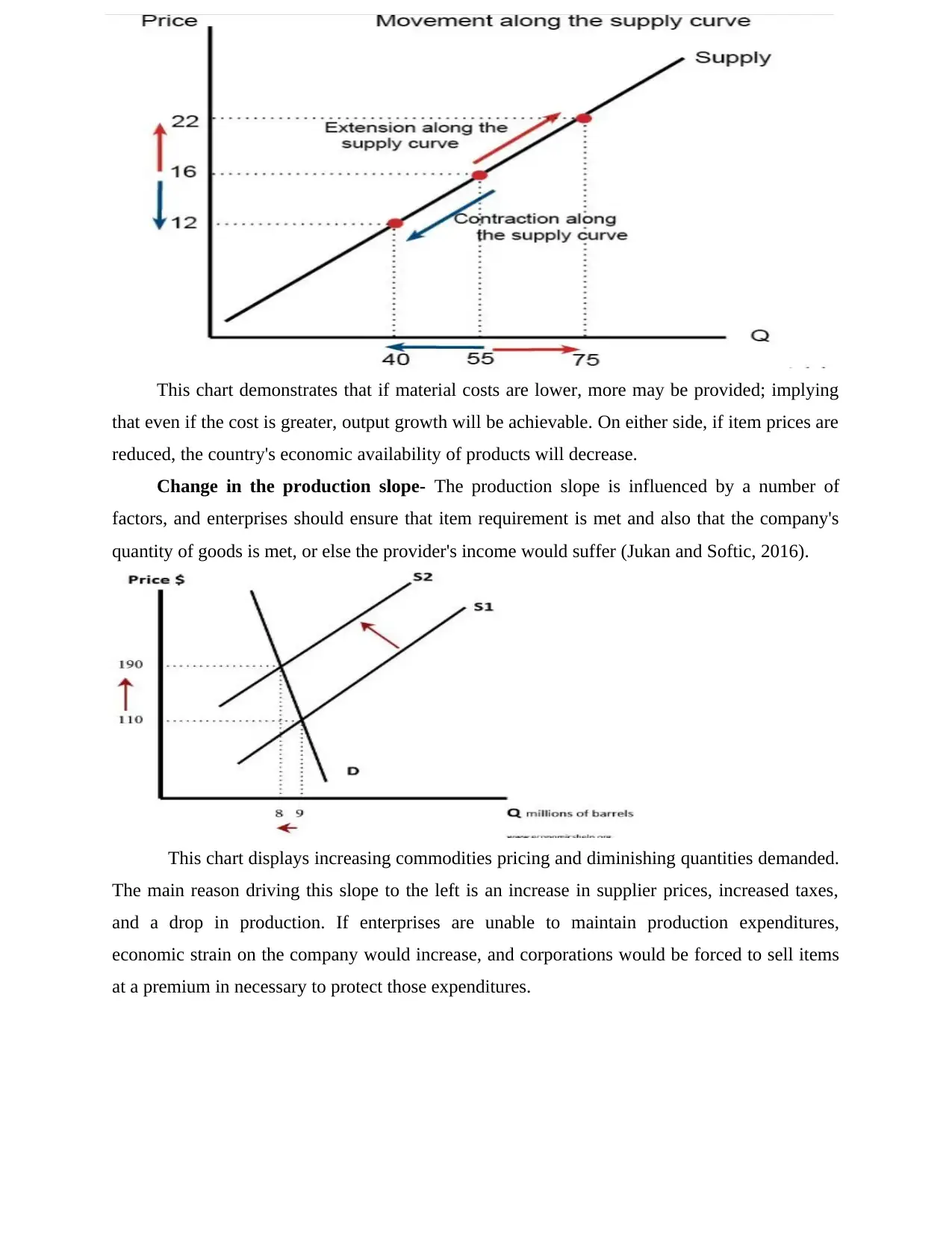

This chart demonstrates that if material costs are lower, more may be provided; implying

that even if the cost is greater, output growth will be achievable. On either side, if item prices are

reduced, the country's economic availability of products will decrease.

Change in the production slope- The production slope is influenced by a number of

factors, and enterprises should ensure that item requirement is met and also that the company's

quantity of goods is met, or else the provider's income would suffer (Jukan and Softic, 2016).

This chart displays increasing commodities pricing and diminishing quantities demanded.

The main reason driving this slope to the left is an increase in supplier prices, increased taxes,

and a drop in production. If enterprises are unable to maintain production expenditures,

economic strain on the company would increase, and corporations would be forced to sell items

at a premium in necessary to protect those expenditures.

that even if the cost is greater, output growth will be achievable. On either side, if item prices are

reduced, the country's economic availability of products will decrease.

Change in the production slope- The production slope is influenced by a number of

factors, and enterprises should ensure that item requirement is met and also that the company's

quantity of goods is met, or else the provider's income would suffer (Jukan and Softic, 2016).

This chart displays increasing commodities pricing and diminishing quantities demanded.

The main reason driving this slope to the left is an increase in supplier prices, increased taxes,

and a drop in production. If enterprises are unable to maintain production expenditures,

economic strain on the company would increase, and corporations would be forced to sell items

at a premium in necessary to protect those expenditures.

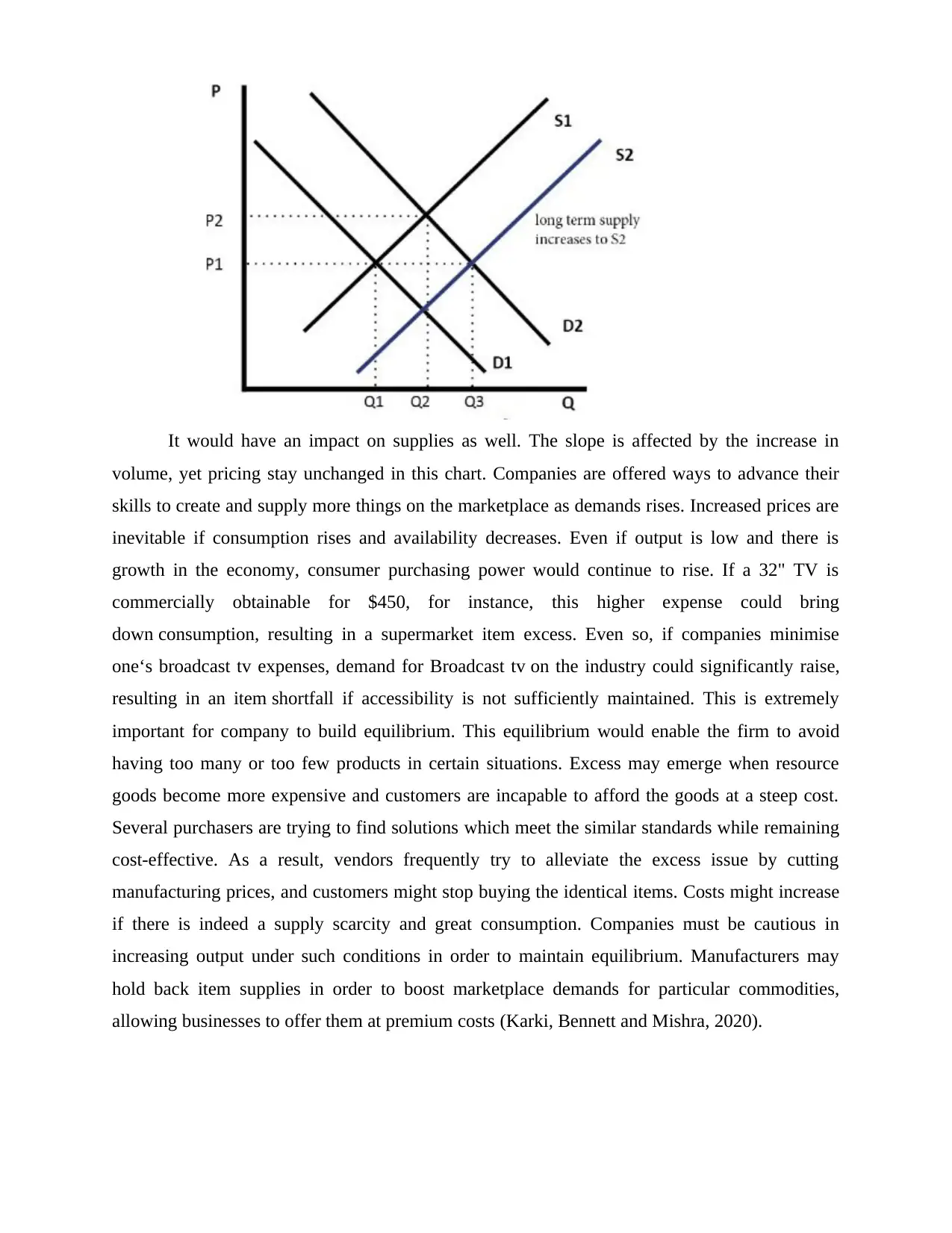

It would have an impact on supplies as well. The slope is affected by the increase in

volume, yet pricing stay unchanged in this chart. Companies are offered ways to advance their

skills to create and supply more things on the marketplace as demands rises. Increased prices are

inevitable if consumption rises and availability decreases. Even if output is low and there is

growth in the economy, consumer purchasing power would continue to rise. If a 32" TV is

commercially obtainable for $450, for instance, this higher expense could bring

down consumption, resulting in a supermarket item excess. Even so, if companies minimise

one‘s broadcast tv expenses, demand for Broadcast tv on the industry could significantly raise,

resulting in an item shortfall if accessibility is not sufficiently maintained. This is extremely

important for company to build equilibrium. This equilibrium would enable the firm to avoid

having too many or too few products in certain situations. Excess may emerge when resource

goods become more expensive and customers are incapable to afford the goods at a steep cost.

Several purchasers are trying to find solutions which meet the similar standards while remaining

cost-effective. As a result, vendors frequently try to alleviate the excess issue by cutting

manufacturing prices, and customers might stop buying the identical items. Costs might increase

if there is indeed a supply scarcity and great consumption. Companies must be cautious in

increasing output under such conditions in order to maintain equilibrium. Manufacturers may

hold back item supplies in order to boost marketplace demands for particular commodities,

allowing businesses to offer them at premium costs (Karki, Bennett and Mishra, 2020).

volume, yet pricing stay unchanged in this chart. Companies are offered ways to advance their

skills to create and supply more things on the marketplace as demands rises. Increased prices are

inevitable if consumption rises and availability decreases. Even if output is low and there is

growth in the economy, consumer purchasing power would continue to rise. If a 32" TV is

commercially obtainable for $450, for instance, this higher expense could bring

down consumption, resulting in a supermarket item excess. Even so, if companies minimise

one‘s broadcast tv expenses, demand for Broadcast tv on the industry could significantly raise,

resulting in an item shortfall if accessibility is not sufficiently maintained. This is extremely

important for company to build equilibrium. This equilibrium would enable the firm to avoid

having too many or too few products in certain situations. Excess may emerge when resource

goods become more expensive and customers are incapable to afford the goods at a steep cost.

Several purchasers are trying to find solutions which meet the similar standards while remaining

cost-effective. As a result, vendors frequently try to alleviate the excess issue by cutting

manufacturing prices, and customers might stop buying the identical items. Costs might increase

if there is indeed a supply scarcity and great consumption. Companies must be cautious in

increasing output under such conditions in order to maintain equilibrium. Manufacturers may

hold back item supplies in order to boost marketplace demands for particular commodities,

allowing businesses to offer them at premium costs (Karki, Bennett and Mishra, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

Evaluate and contrasting new ideas and concepts in 21st-century economy with

concepts from the previous centuries, and link them to current corporate practices

The twentieth-century neoliberal economics strategy was more concerned with goods and

income. The consumption and supplied slope identify various factors, which include items,

production, and wealth inequality. It is considered as a more comprehensive strategy that places

a higher focus on wealth inequality in perspective of commodity expenditure. Poor

competitiveness was brought to the industry at the same moment as a standard neoliberal

method. This indicates that profitable limited assets are efficiently managed. This will necessitate

a significant rise in cash and the expansion of item manufacturing in order to attain massive

economic achievement. This neoliberal concept combines with conventional manufacturing price

theoretical framework, demonstrating that increasing productivity is the goal. Traditional

economics concept states that production costs would determine product price, while neo-

classical macroeconomic concept places a greater emphasis on consumption. Several estimates

are taken in neoliberal economics theories; like that consumers would select a reasonable choice

among outcomes and goods. Companies are constantly searching to buy things that will benefit

themselves the most in effort to optimize their profits (Souza-Monteiro and Hooker, 2017).

People take utilization of industry information in their own way. This neoliberal economics

method demonstrates that long-term consumption growth encourages commodities supplier

extension. To effectively leveraged investment, the economic equilibrium must be preserved,

with the administration always striving to enhance it. This strategy discusses the items' utility

and marginalism. The usefulness of the items is highly dependent on client satisfaction with the

firm's specific items and offerings.

In the twentieth decade, economics dedicated more emphasis to sociological. In designed

to steer production, Keynesian macroeconomic philosophy of the twenty-first era argues that

consumption must rise. Consumers' desire to spend is considered as a key factor in the country's

economic improvement. As a result, economic incentive would be boosted by increased

government spending (Towse and Hernández, 2020). Consumers' earnings may rise, and items

might be purchased in greater numbers, in terms of raising governmental spending on major

building and transportation growth. This would help to meet requirements. According to this

hypothesis, inflexible capitalist would improve competitive marketplaces, allowing independent

Evaluate and contrasting new ideas and concepts in 21st-century economy with

concepts from the previous centuries, and link them to current corporate practices

The twentieth-century neoliberal economics strategy was more concerned with goods and

income. The consumption and supplied slope identify various factors, which include items,

production, and wealth inequality. It is considered as a more comprehensive strategy that places

a higher focus on wealth inequality in perspective of commodity expenditure. Poor

competitiveness was brought to the industry at the same moment as a standard neoliberal

method. This indicates that profitable limited assets are efficiently managed. This will necessitate

a significant rise in cash and the expansion of item manufacturing in order to attain massive

economic achievement. This neoliberal concept combines with conventional manufacturing price

theoretical framework, demonstrating that increasing productivity is the goal. Traditional

economics concept states that production costs would determine product price, while neo-

classical macroeconomic concept places a greater emphasis on consumption. Several estimates

are taken in neoliberal economics theories; like that consumers would select a reasonable choice

among outcomes and goods. Companies are constantly searching to buy things that will benefit

themselves the most in effort to optimize their profits (Souza-Monteiro and Hooker, 2017).

People take utilization of industry information in their own way. This neoliberal economics

method demonstrates that long-term consumption growth encourages commodities supplier

extension. To effectively leveraged investment, the economic equilibrium must be preserved,

with the administration always striving to enhance it. This strategy discusses the items' utility

and marginalism. The usefulness of the items is highly dependent on client satisfaction with the

firm's specific items and offerings.

In the twentieth decade, economics dedicated more emphasis to sociological. In designed

to steer production, Keynesian macroeconomic philosophy of the twenty-first era argues that

consumption must rise. Consumers' desire to spend is considered as a key factor in the country's

economic improvement. As a result, economic incentive would be boosted by increased

government spending (Towse and Hernández, 2020). Consumers' earnings may rise, and items

might be purchased in greater numbers, in terms of raising governmental spending on major

building and transportation growth. This would help to meet requirements. According to this

hypothesis, inflexible capitalist would improve competitive marketplaces, allowing independent

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

companies to emphasis mostly on increasing production. Products, environmental assets, and

employment are the emphasis of this philosophy. This idea can be used by individual firms to

increase their competitive desirability. Traditional macroeconomic thought places a greater

emphasis on regulatory constraints. This ensures that the budgeting and indebtedness are both in

good shape. Independent enterprises would increase their capital if the administration invests

greater than they do. Increasing employment prospects in the nation are aided by governmental

spending. Consumers would be available to acquire additional goods when there are enough

work possibilities, which would help to meet the industry's expanding need. Traditional

economics concept concentrates on increasing economical productivity in attempt to strengthen

the economics growth of the nation, whereas Keynesian financial concept concentrates on

governmental spending. Keynesian’s macroeconomic concept depicts the state helping in

employment development, whereas traditional philosophy suggests that the state's role must be

limited. The corporation might utilise such concepts to regulate pricing, demand, and supplies.

Businesses can understand about customers' actual ability and develop a price-supply

equilibrium for performance measurement by applying such macroeconomic concepts (Yunus,

2017).

CONCLUSION

The preceding study demonstrates that consumption and supplies are two fundamental

socioeconomic concepts, and it is critical to maintain the firm's equilibrium in need to obtain

significant profitability. If costs fluctuate, this would affect consuming since purchasers would

not want to invest cash upon those costly goods; yet, if costs decrease, the demand or supplied

slope might alter since consumers' interests within those goods would rise.

employment are the emphasis of this philosophy. This idea can be used by individual firms to

increase their competitive desirability. Traditional macroeconomic thought places a greater

emphasis on regulatory constraints. This ensures that the budgeting and indebtedness are both in

good shape. Independent enterprises would increase their capital if the administration invests

greater than they do. Increasing employment prospects in the nation are aided by governmental

spending. Consumers would be available to acquire additional goods when there are enough

work possibilities, which would help to meet the industry's expanding need. Traditional

economics concept concentrates on increasing economical productivity in attempt to strengthen

the economics growth of the nation, whereas Keynesian financial concept concentrates on

governmental spending. Keynesian’s macroeconomic concept depicts the state helping in

employment development, whereas traditional philosophy suggests that the state's role must be

limited. The corporation might utilise such concepts to regulate pricing, demand, and supplies.

Businesses can understand about customers' actual ability and develop a price-supply

equilibrium for performance measurement by applying such macroeconomic concepts (Yunus,

2017).

CONCLUSION

The preceding study demonstrates that consumption and supplies are two fundamental

socioeconomic concepts, and it is critical to maintain the firm's equilibrium in need to obtain

significant profitability. If costs fluctuate, this would affect consuming since purchasers would

not want to invest cash upon those costly goods; yet, if costs decrease, the demand or supplied

slope might alter since consumers' interests within those goods would rise.

REFERENCES

Books and journals

Babic-Hodovic, V., Arslanagic-Kalajdzic, M. and Imsirpasic, A., 2017. Perceived quality and

corporate image in mobile services: the role of technical and functional quality. South

East European Journal of Economics and Business, 12(1), pp.114-125.

Cavicchioli, D., 2018. Detecting Market Power Along Food Supply Chains: Evidence and

Methodological Insights from the Fluid Milk Sector in Italy. Agriculture, 8(12), p.191.

Chang, A.C. and Hanson, T.J., 2016. The accuracy of forecasts prepared for the Federal Open

Market Committee. Journal of Economics and Business, 83, pp.23-43.

DAO, B.T.T. and NGUYEN, D.P., 2020. Determinants of profitability in commercial banks in

Vietnam, Malaysia and Thailand. The Journal of Asian Finance, Economics, and

Business, 7(4), pp.133-143.

Filimonau, V. and Gherbin, A., 2017. An exploratory study of food waste management practices

in the UK grocery retail sector. Journal of Cleaner Production, 167, pp.1184-1194.

Jukan, M.K. and Softic, A., 2016. Comparative analysis of financial inclusion in developing

regions around the world. Economic Review: Journal of Economics and Business, 14(2),

pp.56-65.

Karki, S.T., Bennett, A.C. and Mishra, J.L., 2020. Reducing food waste and food insecurity in

the UK: The architecture of surplus food distribution supply chain in addressing the

sustainable development goals (Goal 2 and Goal 12.3) at a city level. Industrial

Marketing Management.

Souza-Monteiro, D. and Hooker, N., 2017. Comparing UK food retailers corporate social

responsibility strategies. British Food Journal.

Towse, R. and Hernández, T.N. eds., 2020. Handbook of cultural economics. Edward Elgar

Publishing.

Yunus, M., 2017. A world of three zeros: the new economics of zero poverty, zero

unemployment, and zero net carbon emissions. Hachette UK.

Books and journals

Babic-Hodovic, V., Arslanagic-Kalajdzic, M. and Imsirpasic, A., 2017. Perceived quality and

corporate image in mobile services: the role of technical and functional quality. South

East European Journal of Economics and Business, 12(1), pp.114-125.

Cavicchioli, D., 2018. Detecting Market Power Along Food Supply Chains: Evidence and

Methodological Insights from the Fluid Milk Sector in Italy. Agriculture, 8(12), p.191.

Chang, A.C. and Hanson, T.J., 2016. The accuracy of forecasts prepared for the Federal Open

Market Committee. Journal of Economics and Business, 83, pp.23-43.

DAO, B.T.T. and NGUYEN, D.P., 2020. Determinants of profitability in commercial banks in

Vietnam, Malaysia and Thailand. The Journal of Asian Finance, Economics, and

Business, 7(4), pp.133-143.

Filimonau, V. and Gherbin, A., 2017. An exploratory study of food waste management practices

in the UK grocery retail sector. Journal of Cleaner Production, 167, pp.1184-1194.

Jukan, M.K. and Softic, A., 2016. Comparative analysis of financial inclusion in developing

regions around the world. Economic Review: Journal of Economics and Business, 14(2),

pp.56-65.

Karki, S.T., Bennett, A.C. and Mishra, J.L., 2020. Reducing food waste and food insecurity in

the UK: The architecture of surplus food distribution supply chain in addressing the

sustainable development goals (Goal 2 and Goal 12.3) at a city level. Industrial

Marketing Management.

Souza-Monteiro, D. and Hooker, N., 2017. Comparing UK food retailers corporate social

responsibility strategies. British Food Journal.

Towse, R. and Hernández, T.N. eds., 2020. Handbook of cultural economics. Edward Elgar

Publishing.

Yunus, M., 2017. A world of three zeros: the new economics of zero poverty, zero

unemployment, and zero net carbon emissions. Hachette UK.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.