Business Economics: Elasticity, Market Structures and Efficiency

VerifiedAdded on 2023/06/07

|19

|2140

|315

Homework Assignment

AI Summary

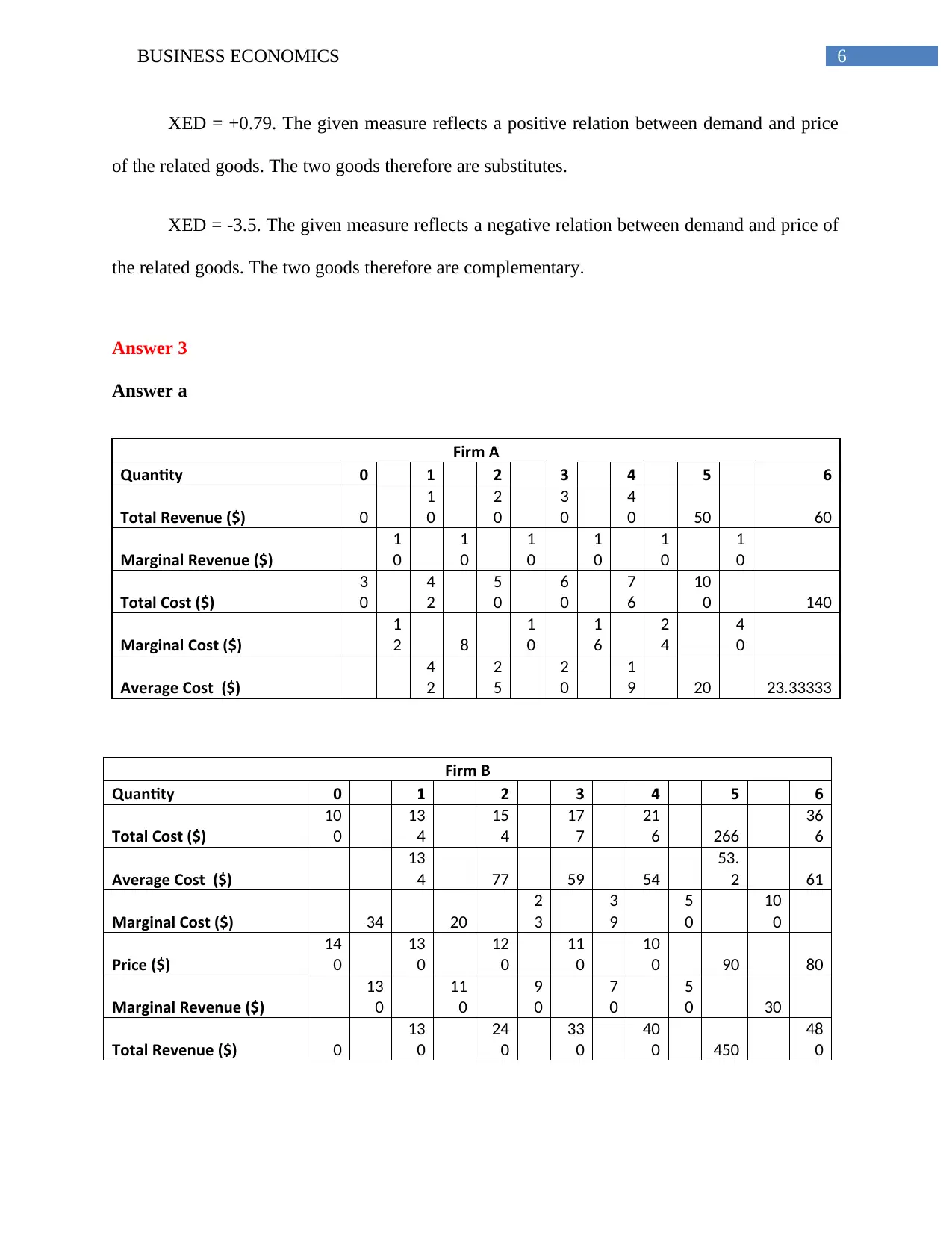

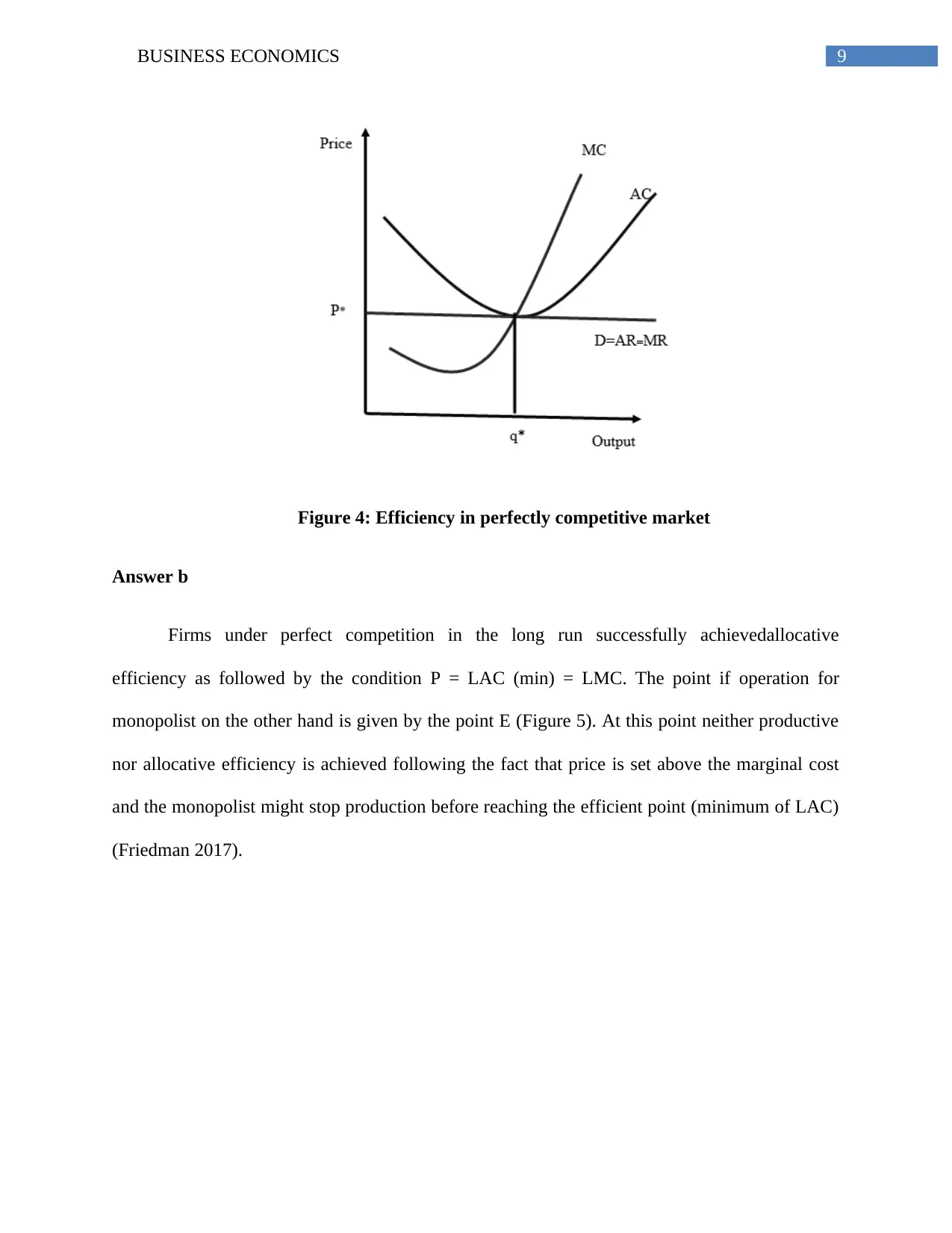

This business economics assignment delves into various aspects of microeconomics, including resource allocation, market efficiency, and elasticity analysis. It examines the impact of externalities on resource allocation, analyzes the characteristics of public and private goods, and explores market structures such as perfect competition and monopolistic competition. The assignment also evaluates the concepts of income and cross-price elasticity of demand, providing numerical examples and interpretations. Furthermore, it compares the efficiency of different market structures, including perfect competition and monopoly, and discusses short-run and long-run equilibrium conditions. The assignment concludes by analyzing the impact of a sharp rise in oil prices on the demand for related goods and services, illustrating the principles of supply and demand in various markets. Desklib provides a platform for students to access this and many other solved assignments and past papers.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.