Business Economics: Supply, Demand, and Market Equilibrium Analysis

VerifiedAdded on 2023/04/21

|17

|2692

|429

Homework Assignment

AI Summary

This assignment solution delves into various aspects of business economics, starting with an analysis of how changes in oil prices affect the demand for related goods like automobiles, home insulation, coal, tires, and bicycles. It explains concepts such as external costs and benefits, highlighting their impact on resource allocation and market efficiency, and discusses the characteristics of public goods that prevent private markets from supplying them adequately. The solution further explores the concept of opportunity cost using the example of wood and the production possibility frontier, and clarifies why the 'free' car offered with chocolate purchases is not truly free due to hidden costs and opportunity costs. The assignment also examines income and cross-price elasticity of demand to determine the nature of goods and their relationships, and discusses the relevance of perfect competition in the real world. Finally, it explains short-run and long-run equilibrium conditions for firms under perfect competition and differentiates between fixed and variable inputs in production, using a coffee shop as an example.

Running head: BUSINESS ECONOMICS

Business Economics

Name of the Student

Name of the University

Course ID

Business Economics

Name of the Student

Name of the University

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUSINESS ECONOMICS

Table of Contents

Question 1........................................................................................................................................

Question a....................................................................................................................................

Question b....................................................................................................................................

Question c....................................................................................................................................

Question 2........................................................................................................................................

Question a....................................................................................................................................

Question b....................................................................................................................................

Question c....................................................................................................................................

Question 4........................................................................................................................................

Question a....................................................................................................................................

Question b....................................................................................................................................

Question c....................................................................................................................................

Question d....................................................................................................................................

Question 5........................................................................................................................................

Question a....................................................................................................................................

Question b..................................................................................................................................

Question c..................................................................................................................................

Question 6......................................................................................................................................

Question a..................................................................................................................................

Question b..................................................................................................................................

Question c..................................................................................................................................

References......................................................................................................................................

Table of Contents

Question 1........................................................................................................................................

Question a....................................................................................................................................

Question b....................................................................................................................................

Question c....................................................................................................................................

Question 2........................................................................................................................................

Question a....................................................................................................................................

Question b....................................................................................................................................

Question c....................................................................................................................................

Question 4........................................................................................................................................

Question a....................................................................................................................................

Question b....................................................................................................................................

Question c....................................................................................................................................

Question d....................................................................................................................................

Question 5........................................................................................................................................

Question a....................................................................................................................................

Question b..................................................................................................................................

Question c..................................................................................................................................

Question 6......................................................................................................................................

Question a..................................................................................................................................

Question b..................................................................................................................................

Question c..................................................................................................................................

References......................................................................................................................................

2BUSINESS ECONOMICS

Question 1

Question a

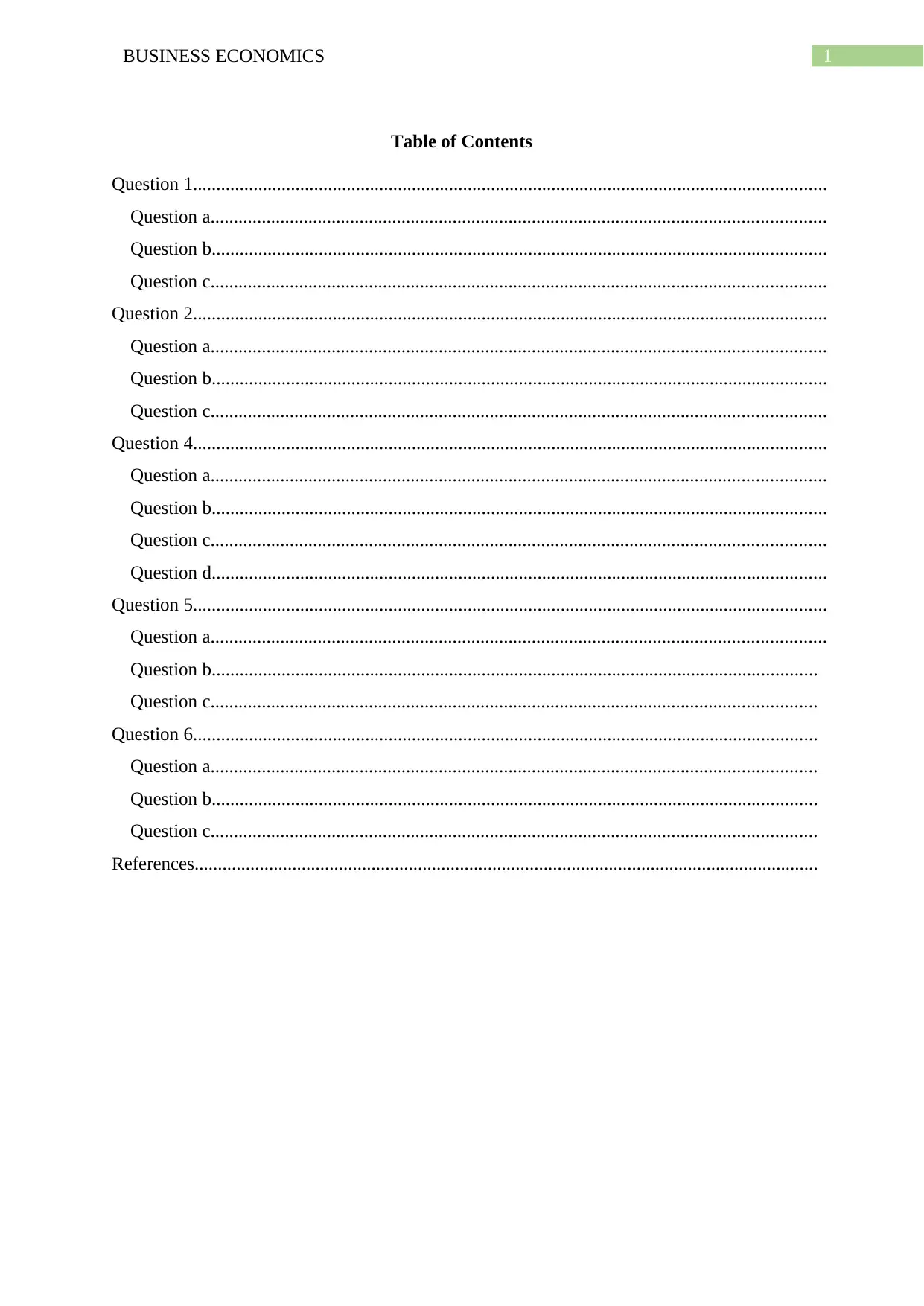

Figure 1: Effect of rise in oil price on automobile demand

A sharp rise in price of oil causes a fall in demand for automobile as automobile is a

complementary good of oil (Cowell, 2018) The decline in demand is shown by the leftward

shift of the automobile demand as shown in the above diagram

ii)

Figure 2: Effect of rise in oil price on home insulation demand

Question 1

Question a

Figure 1: Effect of rise in oil price on automobile demand

A sharp rise in price of oil causes a fall in demand for automobile as automobile is a

complementary good of oil (Cowell, 2018) The decline in demand is shown by the leftward

shift of the automobile demand as shown in the above diagram

ii)

Figure 2: Effect of rise in oil price on home insulation demand

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUSINESS ECONOMICS

When oil price rises, then people experience an increase in cost of energy. In such a

situation people attempts to take measures that reduce energy cost. Home insulation makes

efficient use of energy and reduces cost of heating and cooling appliances. This therefore will

lead to an increase in demand for home insulation. Accordingly, the demand curve shifts

outward.

iii)

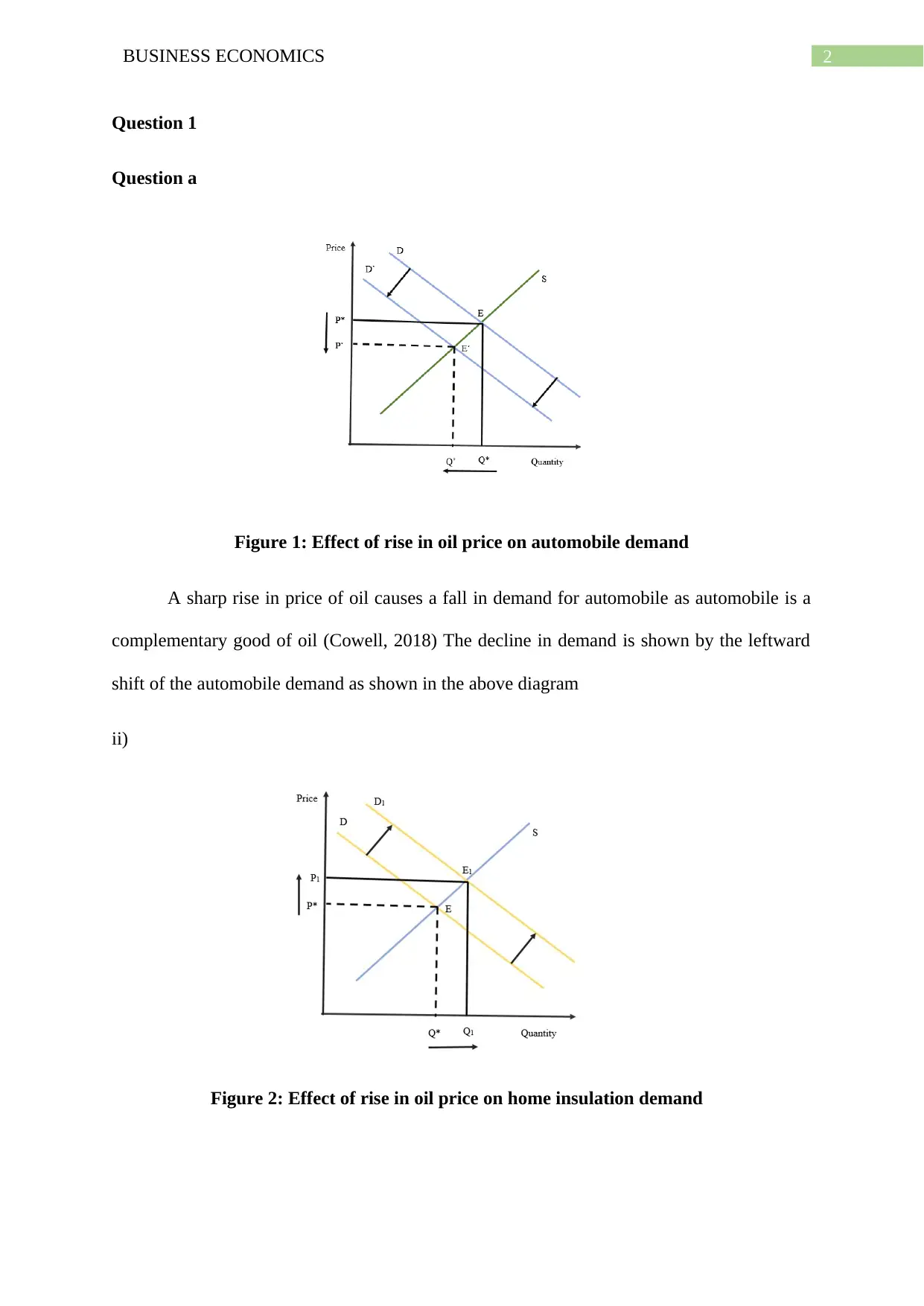

Figure 3: Effect of rise in oil price on coal demand

Coal is used as a substitute of oil. The increase on oil price thus encourages people to

increase demand for coal (Baumol & Blinder, 2015). The demand curve for coal therefore

shifts the demand curve to the right.

iv)

When oil price rises, then people experience an increase in cost of energy. In such a

situation people attempts to take measures that reduce energy cost. Home insulation makes

efficient use of energy and reduces cost of heating and cooling appliances. This therefore will

lead to an increase in demand for home insulation. Accordingly, the demand curve shifts

outward.

iii)

Figure 3: Effect of rise in oil price on coal demand

Coal is used as a substitute of oil. The increase on oil price thus encourages people to

increase demand for coal (Baumol & Blinder, 2015). The demand curve for coal therefore

shifts the demand curve to the right.

iv)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUSINESS ECONOMICS

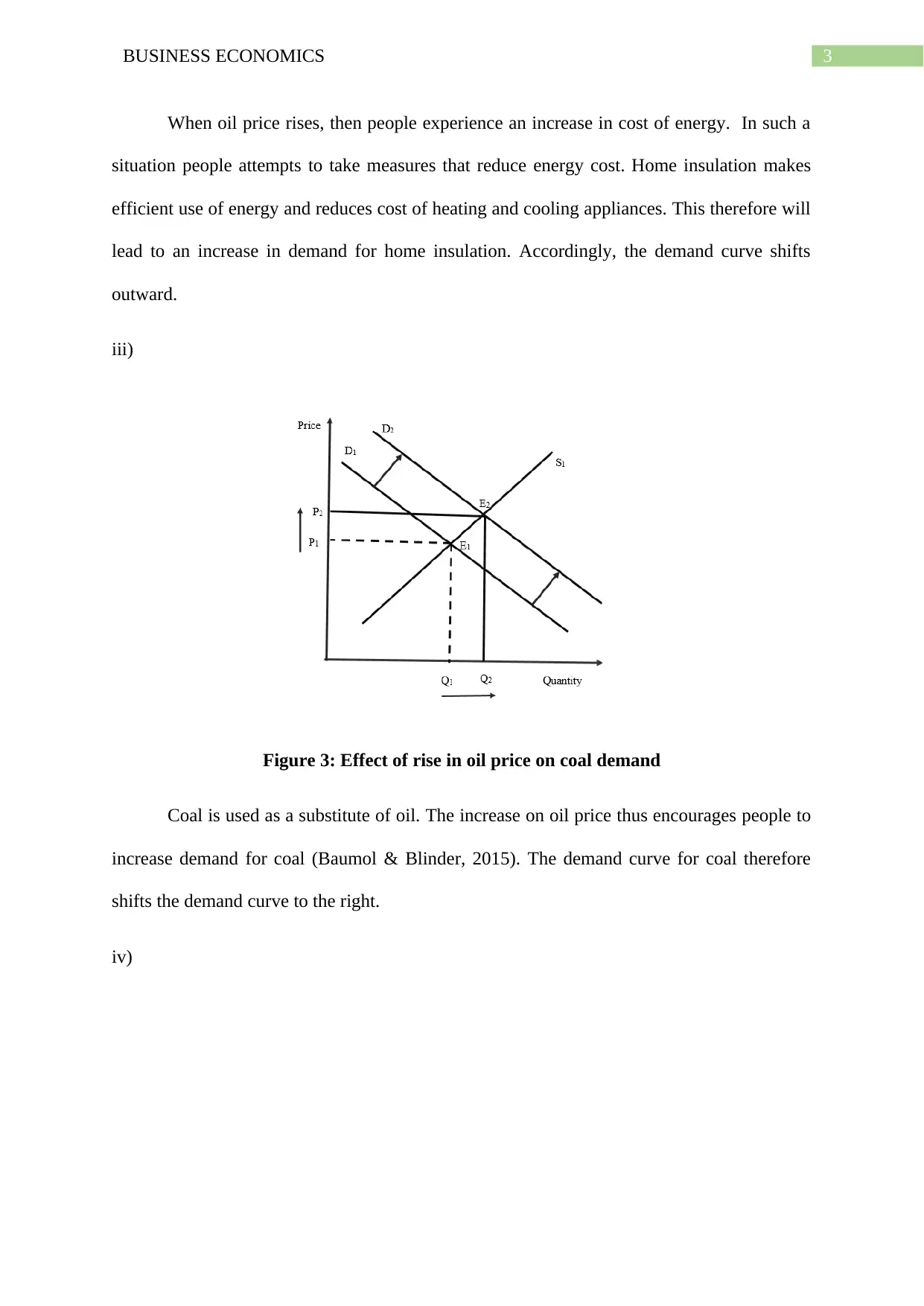

Figure 4: Effect of rise in oil price on tyres demand

The demand for tyres would decline following an increase in demand price of oil. In

reaction to increased oil price demand for automobiles decline. As automobile demand falls,

demand for tyres fall as well. This shown by the inward shift of the tyres demand curve in the

above figure.

v)

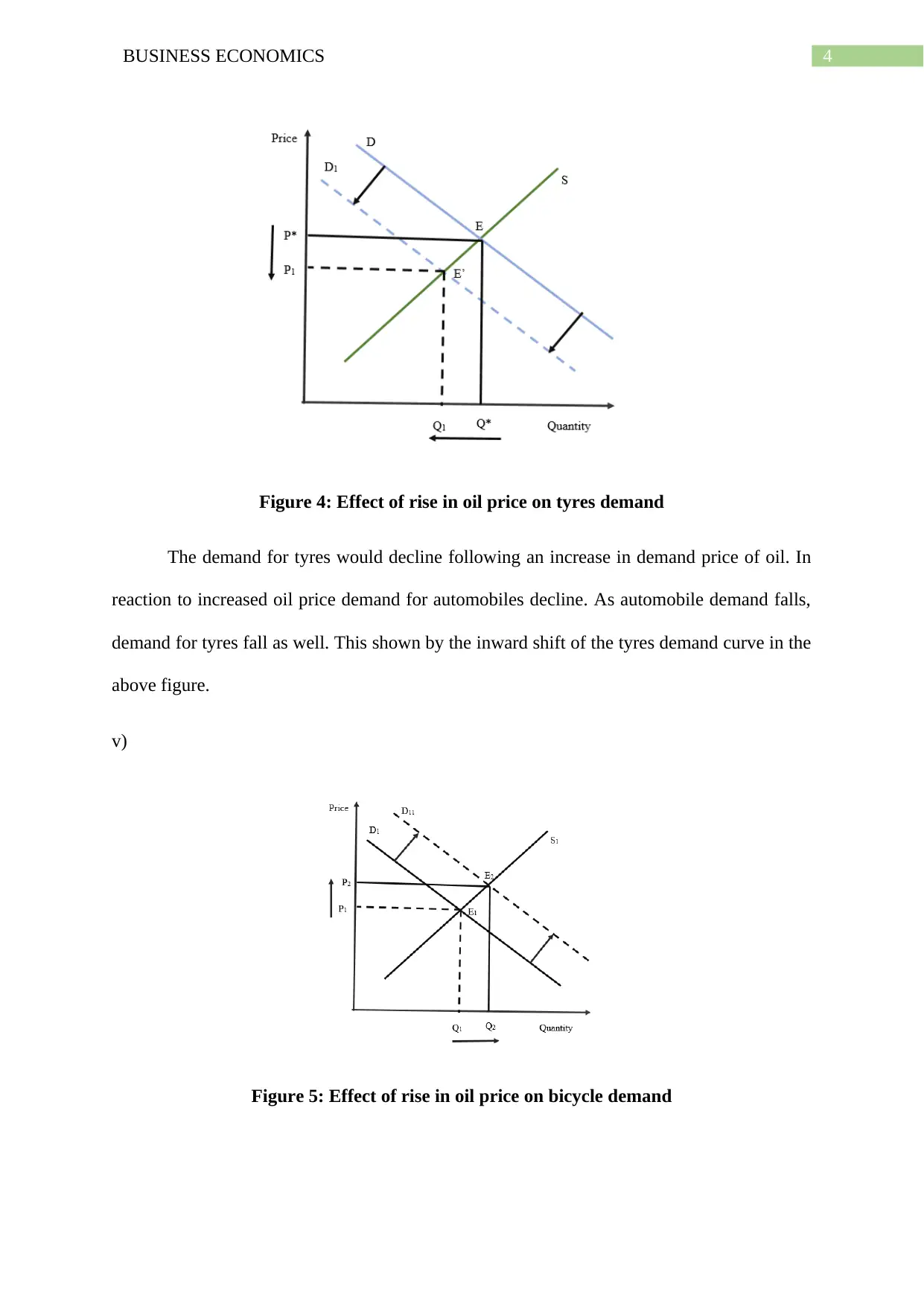

Figure 5: Effect of rise in oil price on bicycle demand

Figure 4: Effect of rise in oil price on tyres demand

The demand for tyres would decline following an increase in demand price of oil. In

reaction to increased oil price demand for automobiles decline. As automobile demand falls,

demand for tyres fall as well. This shown by the inward shift of the tyres demand curve in the

above figure.

v)

Figure 5: Effect of rise in oil price on bicycle demand

5BUSINESS ECONOMICS

Bicycles are substitute of automobiles. The increase in cost of oil induces people to

substitute bicycles for automobiles (Nguyen & Wait, 2015) As a result, the demand for

bicycle increase shifting the bicycle demand curve to the right.

Question b

External costs indicate additional cost that is generated by private producers but is not

accounted by the direct agent of such activity. This has a negative effect on allocation of

resource and end with over allocation of resources. With external cost, private marginal cost

lies below the social marginal cost leading to overproduction of concerned goods in the free

market.

External benefits in contrast are the additional benefits generated from either private

production or consumption. As these benefits are not acknowledged by direct agents’

marginal social benefit exceeds that of private marginal benefit (McKenzie & Lee, 2016)

Goods are thus under produced in free market indicating inefficient allocation of resources.

Question c

The two characteristics of public goods that prevent private market to supply these

goods in sufficient quantity are non-rivalry and non-excludability. Non-rivalry means

consumption of particular units of good by one individual does not affect the benefits

incurred to others. This prevents individual from paying additional dollar for a good. Non-

excludability means people cannot be excluded from enjoying benefits of these goods. People

thus tend to become free riders and never reveal their preference for the particular good (Jain

& Ohri, 2015) The market demand curve fails to reflect willingness of consumers. Following

the incomplete information about cost and benefit private market fails in supplying public

goods in sufficient quantity.

Bicycles are substitute of automobiles. The increase in cost of oil induces people to

substitute bicycles for automobiles (Nguyen & Wait, 2015) As a result, the demand for

bicycle increase shifting the bicycle demand curve to the right.

Question b

External costs indicate additional cost that is generated by private producers but is not

accounted by the direct agent of such activity. This has a negative effect on allocation of

resource and end with over allocation of resources. With external cost, private marginal cost

lies below the social marginal cost leading to overproduction of concerned goods in the free

market.

External benefits in contrast are the additional benefits generated from either private

production or consumption. As these benefits are not acknowledged by direct agents’

marginal social benefit exceeds that of private marginal benefit (McKenzie & Lee, 2016)

Goods are thus under produced in free market indicating inefficient allocation of resources.

Question c

The two characteristics of public goods that prevent private market to supply these

goods in sufficient quantity are non-rivalry and non-excludability. Non-rivalry means

consumption of particular units of good by one individual does not affect the benefits

incurred to others. This prevents individual from paying additional dollar for a good. Non-

excludability means people cannot be excluded from enjoying benefits of these goods. People

thus tend to become free riders and never reveal their preference for the particular good (Jain

& Ohri, 2015) The market demand curve fails to reflect willingness of consumers. Following

the incomplete information about cost and benefit private market fails in supplying public

goods in sufficient quantity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUSINESS ECONOMICS

Question 2

Question a

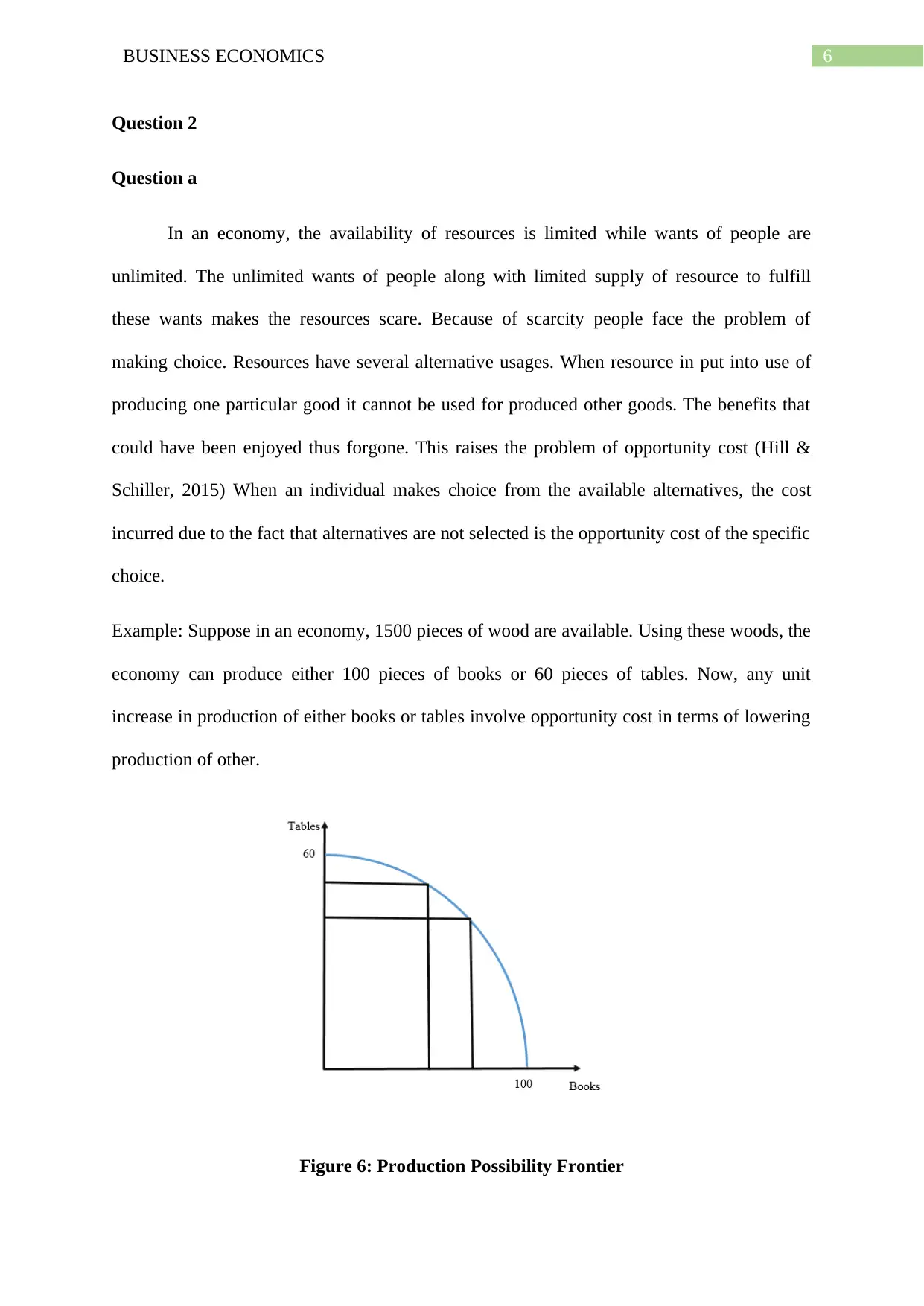

In an economy, the availability of resources is limited while wants of people are

unlimited. The unlimited wants of people along with limited supply of resource to fulfill

these wants makes the resources scare. Because of scarcity people face the problem of

making choice. Resources have several alternative usages. When resource in put into use of

producing one particular good it cannot be used for produced other goods. The benefits that

could have been enjoyed thus forgone. This raises the problem of opportunity cost (Hill &

Schiller, 2015) When an individual makes choice from the available alternatives, the cost

incurred due to the fact that alternatives are not selected is the opportunity cost of the specific

choice.

Example: Suppose in an economy, 1500 pieces of wood are available. Using these woods, the

economy can produce either 100 pieces of books or 60 pieces of tables. Now, any unit

increase in production of either books or tables involve opportunity cost in terms of lowering

production of other.

Figure 6: Production Possibility Frontier

Question 2

Question a

In an economy, the availability of resources is limited while wants of people are

unlimited. The unlimited wants of people along with limited supply of resource to fulfill

these wants makes the resources scare. Because of scarcity people face the problem of

making choice. Resources have several alternative usages. When resource in put into use of

producing one particular good it cannot be used for produced other goods. The benefits that

could have been enjoyed thus forgone. This raises the problem of opportunity cost (Hill &

Schiller, 2015) When an individual makes choice from the available alternatives, the cost

incurred due to the fact that alternatives are not selected is the opportunity cost of the specific

choice.

Example: Suppose in an economy, 1500 pieces of wood are available. Using these woods, the

economy can produce either 100 pieces of books or 60 pieces of tables. Now, any unit

increase in production of either books or tables involve opportunity cost in terms of lowering

production of other.

Figure 6: Production Possibility Frontier

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS ECONOMICS

8BUSINESS ECONOMICS

Question b

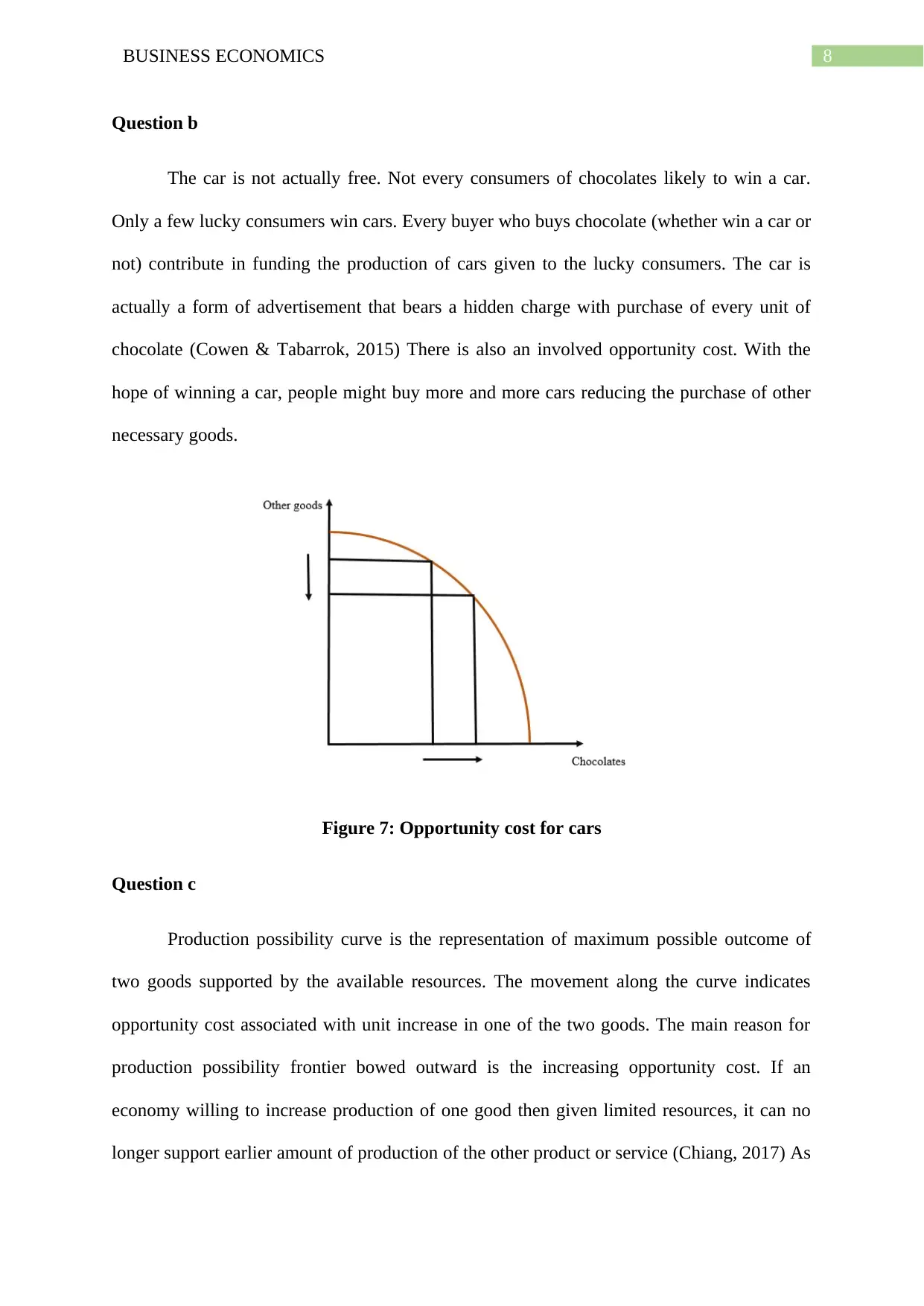

The car is not actually free. Not every consumers of chocolates likely to win a car.

Only a few lucky consumers win cars. Every buyer who buys chocolate (whether win a car or

not) contribute in funding the production of cars given to the lucky consumers. The car is

actually a form of advertisement that bears a hidden charge with purchase of every unit of

chocolate (Cowen & Tabarrok, 2015) There is also an involved opportunity cost. With the

hope of winning a car, people might buy more and more cars reducing the purchase of other

necessary goods.

Figure 7: Opportunity cost for cars

Question c

Production possibility curve is the representation of maximum possible outcome of

two goods supported by the available resources. The movement along the curve indicates

opportunity cost associated with unit increase in one of the two goods. The main reason for

production possibility frontier bowed outward is the increasing opportunity cost. If an

economy willing to increase production of one good then given limited resources, it can no

longer support earlier amount of production of the other product or service (Chiang, 2017) As

Question b

The car is not actually free. Not every consumers of chocolates likely to win a car.

Only a few lucky consumers win cars. Every buyer who buys chocolate (whether win a car or

not) contribute in funding the production of cars given to the lucky consumers. The car is

actually a form of advertisement that bears a hidden charge with purchase of every unit of

chocolate (Cowen & Tabarrok, 2015) There is also an involved opportunity cost. With the

hope of winning a car, people might buy more and more cars reducing the purchase of other

necessary goods.

Figure 7: Opportunity cost for cars

Question c

Production possibility curve is the representation of maximum possible outcome of

two goods supported by the available resources. The movement along the curve indicates

opportunity cost associated with unit increase in one of the two goods. The main reason for

production possibility frontier bowed outward is the increasing opportunity cost. If an

economy willing to increase production of one good then given limited resources, it can no

longer support earlier amount of production of the other product or service (Chiang, 2017) As

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUSINESS ECONOMICS

more and more of one good is produced, economy needs to sacrifice more and more of other

cost and hence opportunity cost increases. This increases gradient of PPF and makes it

concave.

Question 4

Question a

The income elasticity of demand captures proportionate change in demand for a

corresponding proportionate change in income (Baumol & Blinder, 2015) Due to recession

demand of consumers reduces by 10 percent. Given the income elasticity of pre-recorded

music compact is +7, the 10 percent decline in consumers’ income reduces demand for pre-

recorded compact disc by (10*7) = 70 percent. for cabinet maker’s work, the income

elasticity of demand is given as +0.7. That means a decline in income by 10 percent reduces

demand for cabinet maker’s work by (0.7*10) = 7 percent. Due to a higher income elasticity

of demand for pre-recorded compact disc, the recession has a higher impact on compact disc

than that of cabinet maker’s work

Question b

With accomplish the purpose of determining whether MP3 music players and pre-

recorded music compacts discs are in competition with each other the cross price elasticity of

demand needs to be determined. If cross price elasticity is negative, then this means goods

are complementary and hence, there would be no competition between goods (Jain & Ohri,

2015) The positive value of cross price elasticity implies two goods are substitute. In this

case, there are intense rivalry between the two goods as they compete against each other.

more and more of one good is produced, economy needs to sacrifice more and more of other

cost and hence opportunity cost increases. This increases gradient of PPF and makes it

concave.

Question 4

Question a

The income elasticity of demand captures proportionate change in demand for a

corresponding proportionate change in income (Baumol & Blinder, 2015) Due to recession

demand of consumers reduces by 10 percent. Given the income elasticity of pre-recorded

music compact is +7, the 10 percent decline in consumers’ income reduces demand for pre-

recorded compact disc by (10*7) = 70 percent. for cabinet maker’s work, the income

elasticity of demand is given as +0.7. That means a decline in income by 10 percent reduces

demand for cabinet maker’s work by (0.7*10) = 7 percent. Due to a higher income elasticity

of demand for pre-recorded compact disc, the recession has a higher impact on compact disc

than that of cabinet maker’s work

Question b

With accomplish the purpose of determining whether MP3 music players and pre-

recorded music compacts discs are in competition with each other the cross price elasticity of

demand needs to be determined. If cross price elasticity is negative, then this means goods

are complementary and hence, there would be no competition between goods (Jain & Ohri,

2015) The positive value of cross price elasticity implies two goods are substitute. In this

case, there are intense rivalry between the two goods as they compete against each other.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUSINESS ECONOMICS

Question c

YED = +0.8. The value of income elasticity indicates that as income increase by 1 percent

demand for the particular good increases by 0.8 percent. As demand increase with increase in

income the good is a normal good.

YED = -2.4. The value of income elasticity indicates that as income increase by 1 percent

demand for the particular good decreases by 2.4 percent. As demand decreases with increase

in income the good is inferior good.

Question d

XED = + 0.85. The specific value of cross price elasticity implies as price one good increases

by 1 percent, demand for the related good increases by 0.85 percent. The positive relation

between price and demand of the related good implies the two goods are substitute goods

(Hill & Schiller, 2015)

XED = - 0.85. The specific value of cross price elasticity implies as price one good increases

by 1 percent, demand for the related good lowers by 4.5 percent. The negative relation

between price and demand of the related good implies the two goods are complementary

goods.

Question 5

Question a

Economists rarely believe perfect competition to exist in real world. The main

characteristics of perfectly competitive markets include firms sell homogenous products,

forms are price takers, individual firm has a very small market share, buyers have perfect

knowledge about the market and there is free entry or exit of firms. In real world, these five

characteristics are rarely found together in one industry. Most of the products sold today

Question c

YED = +0.8. The value of income elasticity indicates that as income increase by 1 percent

demand for the particular good increases by 0.8 percent. As demand increase with increase in

income the good is a normal good.

YED = -2.4. The value of income elasticity indicates that as income increase by 1 percent

demand for the particular good decreases by 2.4 percent. As demand decreases with increase

in income the good is inferior good.

Question d

XED = + 0.85. The specific value of cross price elasticity implies as price one good increases

by 1 percent, demand for the related good increases by 0.85 percent. The positive relation

between price and demand of the related good implies the two goods are substitute goods

(Hill & Schiller, 2015)

XED = - 0.85. The specific value of cross price elasticity implies as price one good increases

by 1 percent, demand for the related good lowers by 4.5 percent. The negative relation

between price and demand of the related good implies the two goods are complementary

goods.

Question 5

Question a

Economists rarely believe perfect competition to exist in real world. The main

characteristics of perfectly competitive markets include firms sell homogenous products,

forms are price takers, individual firm has a very small market share, buyers have perfect

knowledge about the market and there is free entry or exit of firms. In real world, these five

characteristics are rarely found together in one industry. Most of the products sold today

11BUSINESS ECONOMICS

show some degree of differentiation. Products differ in terms of quality, size of the product,

brand identity and other parameters. Imperfectly competitive markets are more relevant form

of market structure (Cowen & Tabarrok, 2015) Perfectly competitive market thus though has

huge theoretical implication and used as benchmark of analyzing other markets, the concept

has little practical value.

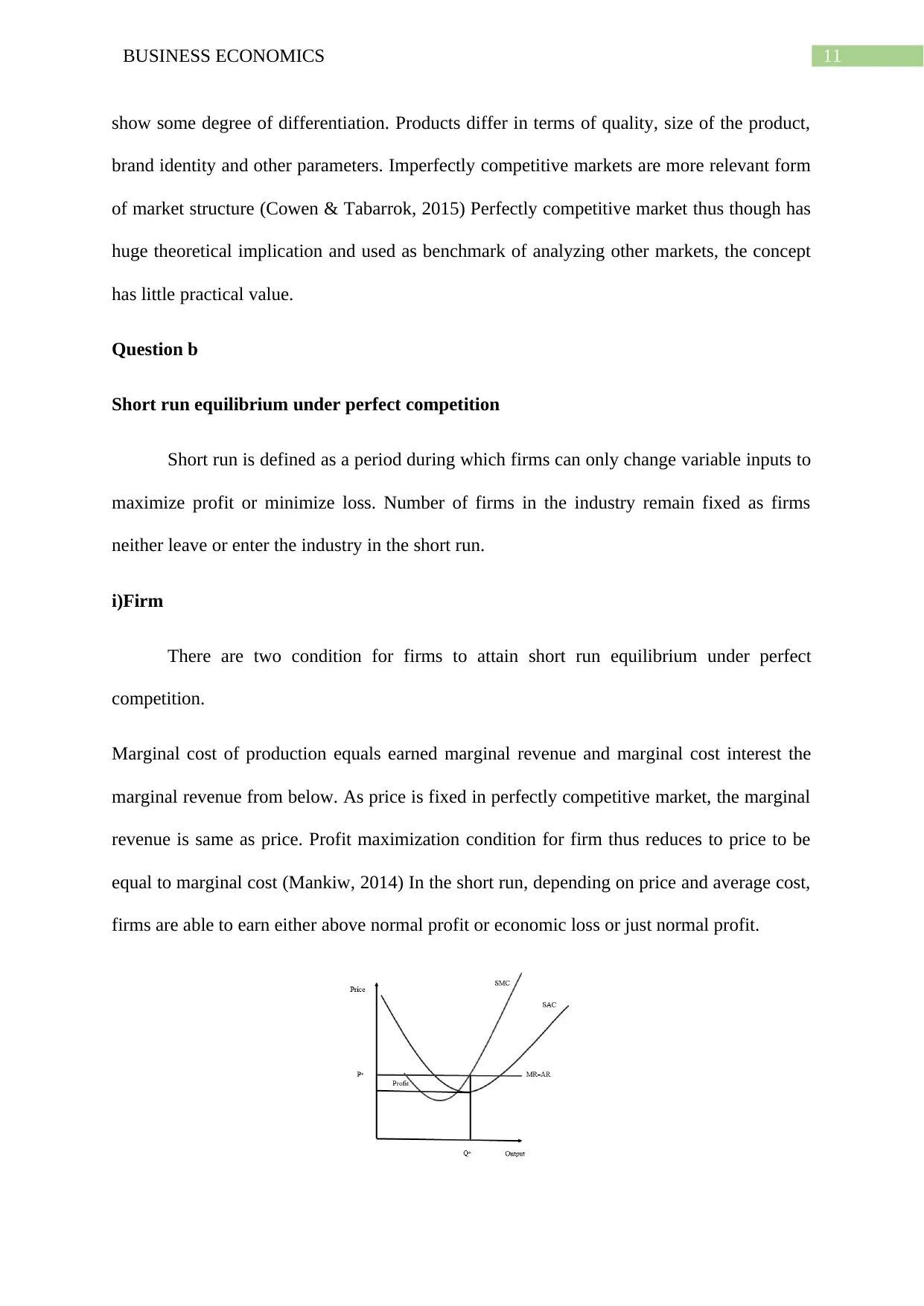

Question b

Short run equilibrium under perfect competition

Short run is defined as a period during which firms can only change variable inputs to

maximize profit or minimize loss. Number of firms in the industry remain fixed as firms

neither leave or enter the industry in the short run.

i)Firm

There are two condition for firms to attain short run equilibrium under perfect

competition.

Marginal cost of production equals earned marginal revenue and marginal cost interest the

marginal revenue from below. As price is fixed in perfectly competitive market, the marginal

revenue is same as price. Profit maximization condition for firm thus reduces to price to be

equal to marginal cost (Mankiw, 2014) In the short run, depending on price and average cost,

firms are able to earn either above normal profit or economic loss or just normal profit.

show some degree of differentiation. Products differ in terms of quality, size of the product,

brand identity and other parameters. Imperfectly competitive markets are more relevant form

of market structure (Cowen & Tabarrok, 2015) Perfectly competitive market thus though has

huge theoretical implication and used as benchmark of analyzing other markets, the concept

has little practical value.

Question b

Short run equilibrium under perfect competition

Short run is defined as a period during which firms can only change variable inputs to

maximize profit or minimize loss. Number of firms in the industry remain fixed as firms

neither leave or enter the industry in the short run.

i)Firm

There are two condition for firms to attain short run equilibrium under perfect

competition.

Marginal cost of production equals earned marginal revenue and marginal cost interest the

marginal revenue from below. As price is fixed in perfectly competitive market, the marginal

revenue is same as price. Profit maximization condition for firm thus reduces to price to be

equal to marginal cost (Mankiw, 2014) In the short run, depending on price and average cost,

firms are able to earn either above normal profit or economic loss or just normal profit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.