Business Economics: Impact on Firm Decisions and Economy Report

VerifiedAdded on 2022/12/14

|10

|2593

|123

Report

AI Summary

This business economics report provides a comprehensive overview of key economic principles and their application in a business context. The report begins with an introduction to economics and business economics, highlighting their relationship and the role of economists in shaping business strategies. It then delves into fundamental economic problems, exploring how firms make decisions under scarcity, and examines various economic systems, including traditional, command, free market, and mixed systems. A significant portion of the report is dedicated to demand and supply, detailing the factors that influence them and their impact on market equilibrium. The report further analyzes market structures, including imperfect competition, and explores consumer behavior and its influence on firm production decisions. The report concludes by summarizing the key takeaways and emphasizing the importance of economic understanding in effective business management.

Business Economics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Economics and Business economics...........................................................................................3

Relationship between Economics and Business environment.....................................................3

Role of Economists......................................................................................................................4

Fundamental economic problem and firm behaviour..................................................................4

Economic systems.......................................................................................................................5

Demand and its factors................................................................................................................6

Change in demand and Quantity Demanded...............................................................................6

Supply and its factors...................................................................................................................8

Market Structure..........................................................................................................................9

Consumer Behaviour and Firm Production Decisions................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Economics and Business economics...........................................................................................3

Relationship between Economics and Business environment.....................................................3

Role of Economists......................................................................................................................4

Fundamental economic problem and firm behaviour..................................................................4

Economic systems.......................................................................................................................5

Demand and its factors................................................................................................................6

Change in demand and Quantity Demanded...............................................................................6

Supply and its factors...................................................................................................................8

Market Structure..........................................................................................................................9

Consumer Behaviour and Firm Production Decisions................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

In this study highlights the economics and its components put effects on the business

decisions and firm’s behaviour. A description of economics and its relationship with the business

environment is explained. Also the types of economic systems with demand and supply along

with its factors are mentioned (Spulber, 2019). At the end the structure of market with types of

imperfect competition and consumer behaviour and firm’s production decisions are outlined. So,

the whole study will describe the functions of business economics that influence the economy

and business decision making and will provide information how demand and supply effects the

economy.

MAIN BODY

Economics and Business economics

Economics is a discipline of the economy that help in the decision making. It analyse the

use of resources that are scarce and limited. Economics deals with the factors of production and

consumption of goods and services. It helps to understand the functions of production so the

businesses would take informed decisions to produce enough goods and services that satisfy the

needs of the consumers. The economics is divided into two categories i.e. microeconomics that

focus on the individual level and factors that effects the decision making of an individual and

macroeconomics that focus on the whole economy of a country and factors that influence the

economy as a whole. Also, Business economics is a field of economics that integrate economic

theories and models within the business practices to facilitate business decision making

(Carriere-Swallow, and Haksar, 2019). It focuses on the factors that are contributing to the

structure of business i.e. capital, labour, taxes and so on. Business economics help the managers

of the organisations to analyse issues arises in the business and provide alternate course of action

to take effective decisions. Business economics link business structure and practises with

economic theories and models which provide both micro and macroeconomics tools and

techniques to optimise business functions.

Relationship between Economics and Business environment

The role of economics in the business environment is understand the impact of micro and

macro factors of the business. Micro factors creates direct impact as it concern with the areas

within which the organisation operates. It consist of customers, suppliers, competitors and

public. These factors creates influence over the supply, demand and overall functioning of the

In this study highlights the economics and its components put effects on the business

decisions and firm’s behaviour. A description of economics and its relationship with the business

environment is explained. Also the types of economic systems with demand and supply along

with its factors are mentioned (Spulber, 2019). At the end the structure of market with types of

imperfect competition and consumer behaviour and firm’s production decisions are outlined. So,

the whole study will describe the functions of business economics that influence the economy

and business decision making and will provide information how demand and supply effects the

economy.

MAIN BODY

Economics and Business economics

Economics is a discipline of the economy that help in the decision making. It analyse the

use of resources that are scarce and limited. Economics deals with the factors of production and

consumption of goods and services. It helps to understand the functions of production so the

businesses would take informed decisions to produce enough goods and services that satisfy the

needs of the consumers. The economics is divided into two categories i.e. microeconomics that

focus on the individual level and factors that effects the decision making of an individual and

macroeconomics that focus on the whole economy of a country and factors that influence the

economy as a whole. Also, Business economics is a field of economics that integrate economic

theories and models within the business practices to facilitate business decision making

(Carriere-Swallow, and Haksar, 2019). It focuses on the factors that are contributing to the

structure of business i.e. capital, labour, taxes and so on. Business economics help the managers

of the organisations to analyse issues arises in the business and provide alternate course of action

to take effective decisions. Business economics link business structure and practises with

economic theories and models which provide both micro and macroeconomics tools and

techniques to optimise business functions.

Relationship between Economics and Business environment

The role of economics in the business environment is understand the impact of micro and

macro factors of the business. Micro factors creates direct impact as it concern with the areas

within which the organisation operates. It consist of customers, suppliers, competitors and

public. These factors creates influence over the supply, demand and overall functioning of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business within an organisation. The impact is for short period and business can easily cope with

the effect generated by micro factors. While macro factors are related to the economy. These

factors creates an impact over the industries within which all the business is operated. The macro

factors that effects the business environment are continuously changing and the businesses have

no control over (Halbert and Ingulli, 2020). The macro factors consists of economic,

demographic, technological, political, legal, social, cultural and natural components. Economics

helps in to understand businesses these micro and macro factors which create challenges within

the environment the business operates. By using different theories and models of the economics

management of the organisations will be able to understand the effects of these factors and

strategy formulation or decision making becomes easy.

Role of Economists

The economist generate three values in the economy viz. achievement, serving public and

conformity of rules. Economist help and give recommendations in policy formulation. They

conduct studies how resources like land, labour, raw materials, goods and services are distributed

and consumed among the population. They collect, analyse and monitors trends and indicators of

the economies. Many of the economists are specialised in a particular field of economics. The

microeconomic indicators like supply and demand of an individual organisations and its impact

on the organisations production and profits are determined and analysed by the micro-economists

(O'Brien, 2017). While macro-economists do research on the economic trends and perform

forecasts on the factors like unemployment, productivity, inflation, economic growth, etc. The

economists that are hired by the organisations are the micro-economists that help to solve issues

and provide expertise regarding micro environment of the organisation. Thus, economists in the

nation provide valuable inputs by conducting studies of the major economic factors and by

forecasting help in the policy formulation and decision making.

Fundamental economic problem and firm behaviour

The resources are scarce and consumption is unlimited. The basic fundamental problem of

every economy are the question regarding production of resources i.e. what, how and whom. As

the wants of the people in an economy is unlimited it is not possible to produce enough with

limited resources. In order to produce and distribute goods and services the firms/organisations

have to examine the fundamental problems. The first and foremost issue is regarding the problem

of what sort of goods are to be produced and what are not. The main objective of the firm is to

the effect generated by micro factors. While macro factors are related to the economy. These

factors creates an impact over the industries within which all the business is operated. The macro

factors that effects the business environment are continuously changing and the businesses have

no control over (Halbert and Ingulli, 2020). The macro factors consists of economic,

demographic, technological, political, legal, social, cultural and natural components. Economics

helps in to understand businesses these micro and macro factors which create challenges within

the environment the business operates. By using different theories and models of the economics

management of the organisations will be able to understand the effects of these factors and

strategy formulation or decision making becomes easy.

Role of Economists

The economist generate three values in the economy viz. achievement, serving public and

conformity of rules. Economist help and give recommendations in policy formulation. They

conduct studies how resources like land, labour, raw materials, goods and services are distributed

and consumed among the population. They collect, analyse and monitors trends and indicators of

the economies. Many of the economists are specialised in a particular field of economics. The

microeconomic indicators like supply and demand of an individual organisations and its impact

on the organisations production and profits are determined and analysed by the micro-economists

(O'Brien, 2017). While macro-economists do research on the economic trends and perform

forecasts on the factors like unemployment, productivity, inflation, economic growth, etc. The

economists that are hired by the organisations are the micro-economists that help to solve issues

and provide expertise regarding micro environment of the organisation. Thus, economists in the

nation provide valuable inputs by conducting studies of the major economic factors and by

forecasting help in the policy formulation and decision making.

Fundamental economic problem and firm behaviour

The resources are scarce and consumption is unlimited. The basic fundamental problem of

every economy are the question regarding production of resources i.e. what, how and whom. As

the wants of the people in an economy is unlimited it is not possible to produce enough with

limited resources. In order to produce and distribute goods and services the firms/organisations

have to examine the fundamental problems. The first and foremost issue is regarding the problem

of what sort of goods are to be produced and what are not. The main objective of the firm is to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

maximise profits and with the limited availability of the resources the choice of goods is difficult

(Christianto and Smarandache, 2018). Firms have to analyse the consumer demand and other

economic factors that effects the production of chosen goods and services. The next issue is to

how to produce the selected goods and services. Firms have to decide how much raw materials

and resources are required and what are the methods and technologies are to be used in order to

perform production. Lastly the challenge is for whom the production should have to be done. It

help in the determination of how much the firm should produce goods and service which fulfils

the current demand and to maintain smooth supply of the goods and services to the consumers in

the economy.

Economic systems

Every economy have its own set of functions. These functions are based on different

systems that economies adopt in order to address the fundamental economic problems. These

systems are as follows:

Traditional economic system: In this system a surplus produce is a rare occurrence. Each

individual in the economy has a specific role to follow. The societies are closely related to each

other and are socially satisfied. But the drawback is that they lack access to the technology and

advancement.

Command economic system: In this system the economy is controlled by the centralised power.

Most of the economies have governments as the central authority that have controlled over the

planning and distribution of the resources. This system is have the ability to create a healthy

supply of the nation’s resources.

Free Market/ Laissez faire economic system: In this system resources are allocated through

the exchange between the free and self-directed market forces (Tronin and et.al, 2019). The firms

and individual act in a self-interest to determine how resources get allocated. There is no

government intervention as it is free-market economy.

Mixed economic system: In this system there is a combination of market forces and various

economic systems. The sensitive areas of the economy is controlled by the government of the

nation. Also the regulation of the private sectors are done by the governments. The resources in

the economy is allocated by provisioning for both public and private sector of the economy.

(Christianto and Smarandache, 2018). Firms have to analyse the consumer demand and other

economic factors that effects the production of chosen goods and services. The next issue is to

how to produce the selected goods and services. Firms have to decide how much raw materials

and resources are required and what are the methods and technologies are to be used in order to

perform production. Lastly the challenge is for whom the production should have to be done. It

help in the determination of how much the firm should produce goods and service which fulfils

the current demand and to maintain smooth supply of the goods and services to the consumers in

the economy.

Economic systems

Every economy have its own set of functions. These functions are based on different

systems that economies adopt in order to address the fundamental economic problems. These

systems are as follows:

Traditional economic system: In this system a surplus produce is a rare occurrence. Each

individual in the economy has a specific role to follow. The societies are closely related to each

other and are socially satisfied. But the drawback is that they lack access to the technology and

advancement.

Command economic system: In this system the economy is controlled by the centralised power.

Most of the economies have governments as the central authority that have controlled over the

planning and distribution of the resources. This system is have the ability to create a healthy

supply of the nation’s resources.

Free Market/ Laissez faire economic system: In this system resources are allocated through

the exchange between the free and self-directed market forces (Tronin and et.al, 2019). The firms

and individual act in a self-interest to determine how resources get allocated. There is no

government intervention as it is free-market economy.

Mixed economic system: In this system there is a combination of market forces and various

economic systems. The sensitive areas of the economy is controlled by the government of the

nation. Also the regulation of the private sectors are done by the governments. The resources in

the economy is allocated by provisioning for both public and private sector of the economy.

Demand and its factors

Demand is an element of economics consist of consumer’s desire and willingness to

purchase goods and services. There are different factors that affects the demand in an economy

which are as follows:

Price of Goods and Services: With the increase in price of the goods and services the demand

tends to decrease and with decrease in the price the demand will increase.

Income of Consumers: The more the income of the consumers the higher is the demand for the

goods and services. More income means more purchasing power. On the contrary, when the

income of the consumer decreases the demand of the goods and services also falls.

Taste and Preferences of the Consumers: When consumer’s preference changes the demand

for the related goods and services also changes (Toro-González and et.al, 2020). People have the

tendency to try new and more goods and services that are introduced in the markets which led

the taste and preference to shift, accordingly the demand increases and decreases.

Change related goods price level: When there is an increase or decrease in the price of

complementary and substitute goods that are related to the primary goods, the demand of the

goods is also affected by this change.

Advertisement: It is the method of influence the consumer to buy the products and services.

Advertisements are made in various media like newspapers, electronic media i.e. television,

radio, etc. A successful advertisement will create an effect on the mind of consumers which

increase the demand.

Expectation of consumer: If the consumers in an economy expects that the price in the future

for the goods and services increases then they started to purchase in great quantity in present

period which in result increase the demand of the product and vice versa.

Change in demand and Quantity Demanded

Change in demand means the increase and decrease in the demand of the goods and

services due to various factors of demand while price remains the same. The demand curve that

represent demand of goods and services in relation to price.

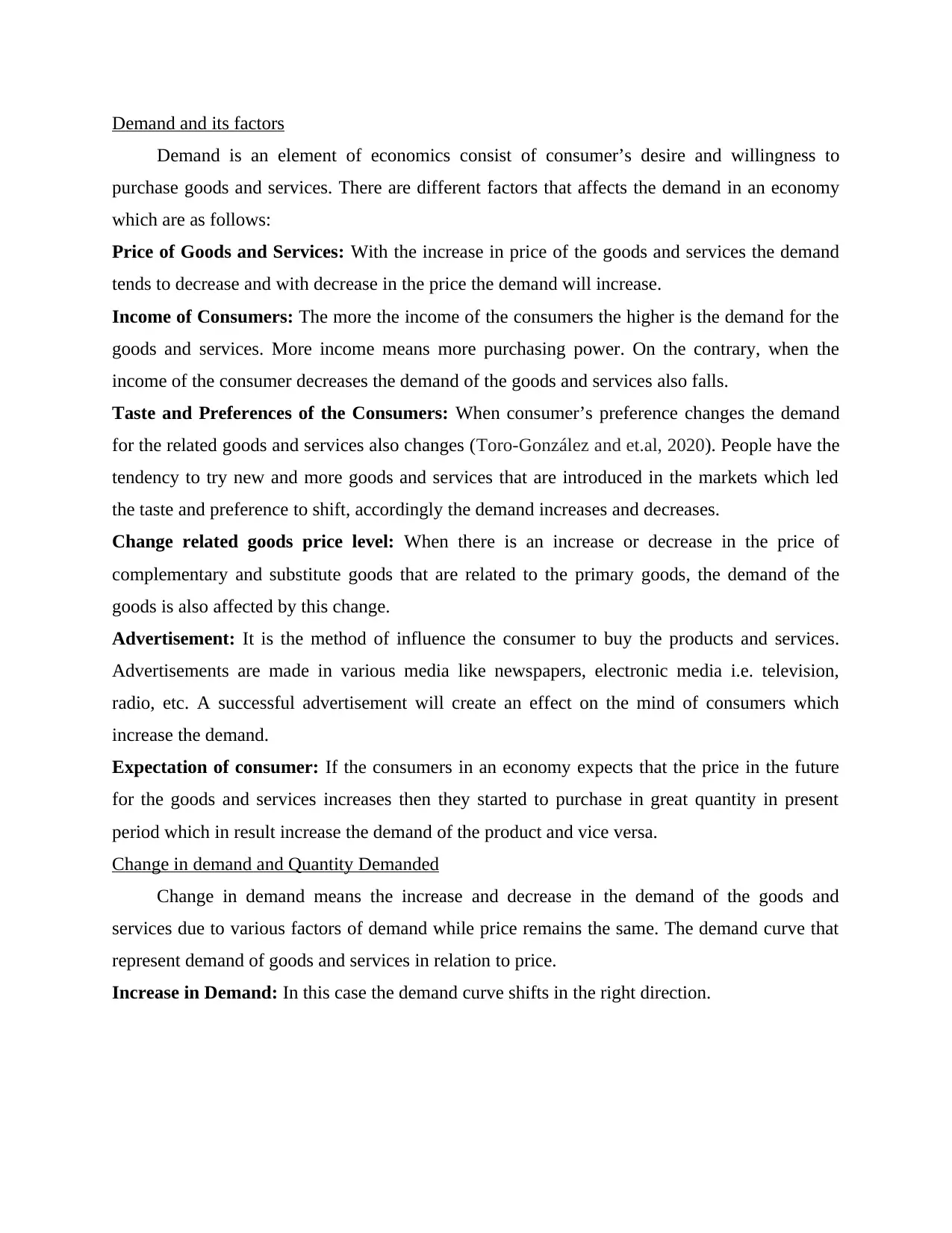

Increase in Demand: In this case the demand curve shifts in the right direction.

Demand is an element of economics consist of consumer’s desire and willingness to

purchase goods and services. There are different factors that affects the demand in an economy

which are as follows:

Price of Goods and Services: With the increase in price of the goods and services the demand

tends to decrease and with decrease in the price the demand will increase.

Income of Consumers: The more the income of the consumers the higher is the demand for the

goods and services. More income means more purchasing power. On the contrary, when the

income of the consumer decreases the demand of the goods and services also falls.

Taste and Preferences of the Consumers: When consumer’s preference changes the demand

for the related goods and services also changes (Toro-González and et.al, 2020). People have the

tendency to try new and more goods and services that are introduced in the markets which led

the taste and preference to shift, accordingly the demand increases and decreases.

Change related goods price level: When there is an increase or decrease in the price of

complementary and substitute goods that are related to the primary goods, the demand of the

goods is also affected by this change.

Advertisement: It is the method of influence the consumer to buy the products and services.

Advertisements are made in various media like newspapers, electronic media i.e. television,

radio, etc. A successful advertisement will create an effect on the mind of consumers which

increase the demand.

Expectation of consumer: If the consumers in an economy expects that the price in the future

for the goods and services increases then they started to purchase in great quantity in present

period which in result increase the demand of the product and vice versa.

Change in demand and Quantity Demanded

Change in demand means the increase and decrease in the demand of the goods and

services due to various factors of demand while price remains the same. The demand curve that

represent demand of goods and services in relation to price.

Increase in Demand: In this case the demand curve shifts in the right direction.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

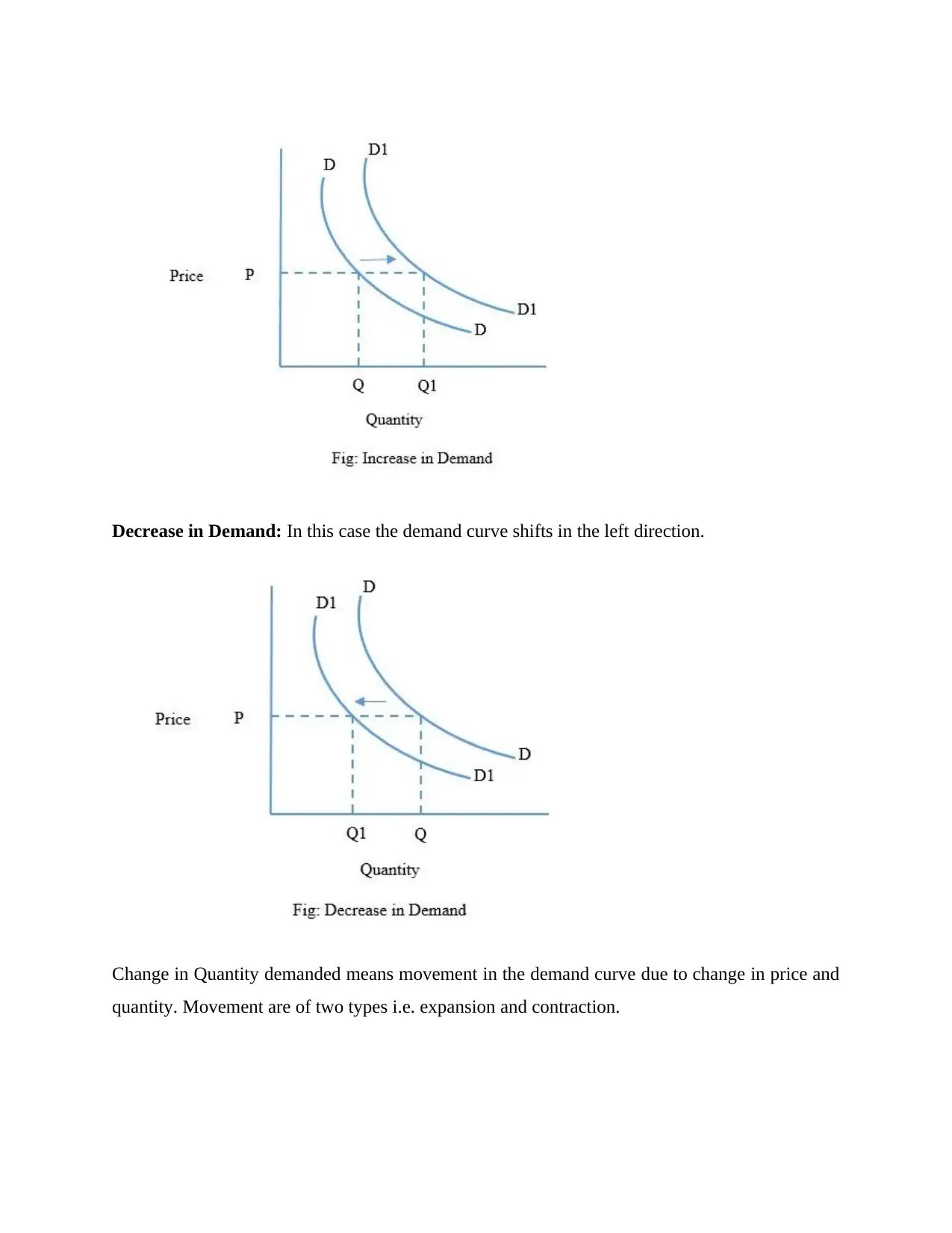

Decrease in Demand: In this case the demand curve shifts in the left direction.

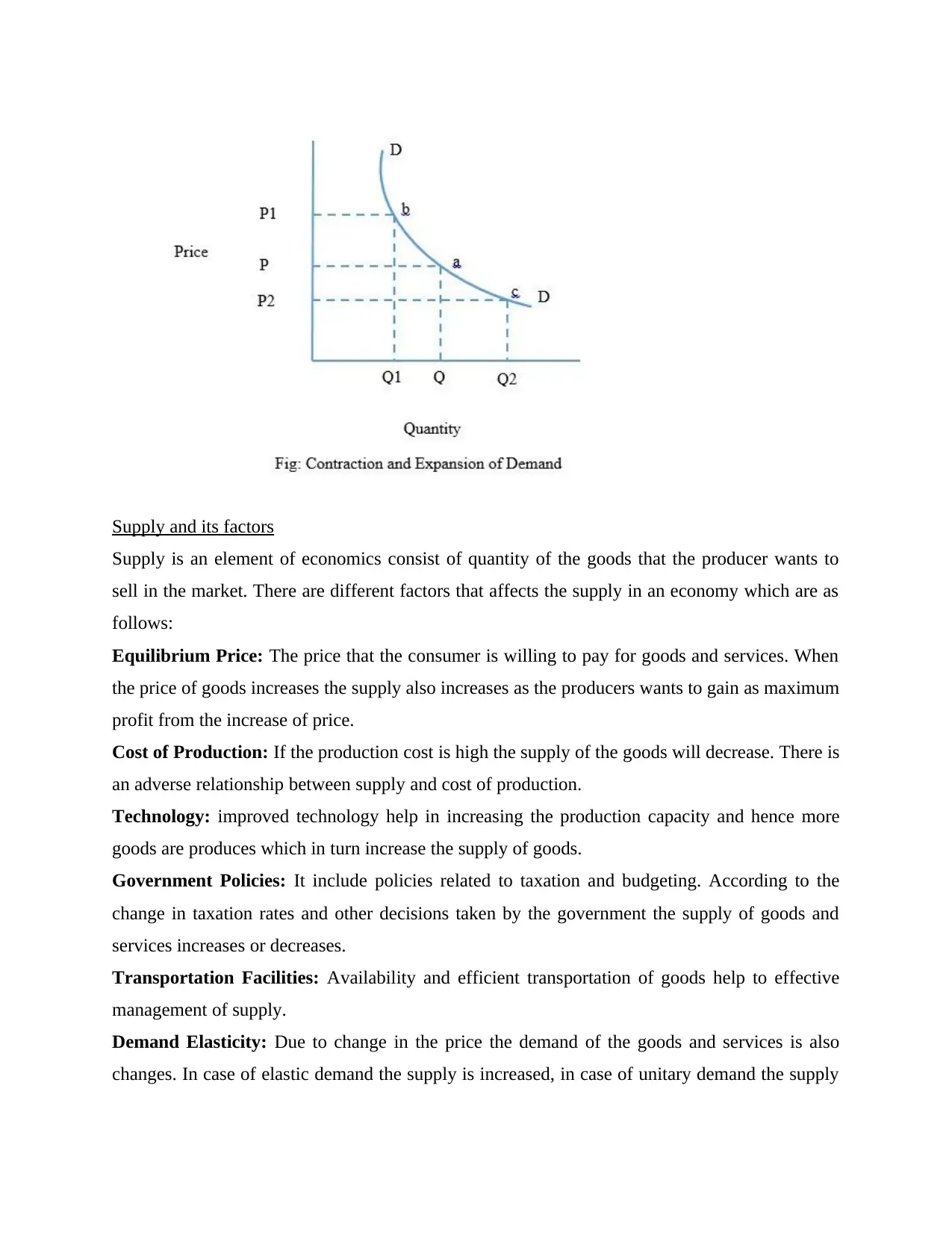

Change in Quantity demanded means movement in the demand curve due to change in price and

quantity. Movement are of two types i.e. expansion and contraction.

Change in Quantity demanded means movement in the demand curve due to change in price and

quantity. Movement are of two types i.e. expansion and contraction.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Supply and its factors

Supply is an element of economics consist of quantity of the goods that the producer wants to

sell in the market. There are different factors that affects the supply in an economy which are as

follows:

Equilibrium Price: The price that the consumer is willing to pay for goods and services. When

the price of goods increases the supply also increases as the producers wants to gain as maximum

profit from the increase of price.

Cost of Production: If the production cost is high the supply of the goods will decrease. There is

an adverse relationship between supply and cost of production.

Technology: improved technology help in increasing the production capacity and hence more

goods are produces which in turn increase the supply of goods.

Government Policies: It include policies related to taxation and budgeting. According to the

change in taxation rates and other decisions taken by the government the supply of goods and

services increases or decreases.

Transportation Facilities: Availability and efficient transportation of goods help to effective

management of supply.

Demand Elasticity: Due to change in the price the demand of the goods and services is also

changes. In case of elastic demand the supply is increased, in case of unitary demand the supply

Supply is an element of economics consist of quantity of the goods that the producer wants to

sell in the market. There are different factors that affects the supply in an economy which are as

follows:

Equilibrium Price: The price that the consumer is willing to pay for goods and services. When

the price of goods increases the supply also increases as the producers wants to gain as maximum

profit from the increase of price.

Cost of Production: If the production cost is high the supply of the goods will decrease. There is

an adverse relationship between supply and cost of production.

Technology: improved technology help in increasing the production capacity and hence more

goods are produces which in turn increase the supply of goods.

Government Policies: It include policies related to taxation and budgeting. According to the

change in taxation rates and other decisions taken by the government the supply of goods and

services increases or decreases.

Transportation Facilities: Availability and efficient transportation of goods help to effective

management of supply.

Demand Elasticity: Due to change in the price the demand of the goods and services is also

changes. In case of elastic demand the supply is increased, in case of unitary demand the supply

will increase but not in the same proportion as in elastic demand and in case of inelastic demand

the supply is not much affected (Burke and Abayasekara, 2018).

Market Structure

The structure refers to the competition in the market for goods and services. The market structure

in an economy is affected by the various elements i.e. buyers and sellers in the market. Product

differentiation, entry and exit into the market.

Imperfect competition

In this type of market structure there are many sellers and all are selling heterogeneous goods

and services.

Types

Monopolistic competition: Large number of sellers with different types of goods.

Monopoly: Only single seller of goods with no competition.

Oligopoly: Few seller forms a cartel to sell products at high market price.

Monopsony: Number of sellers in the market and only single buyer.

Oligopsony: Few number of buyers and many sellers.

Consumer Behaviour and Firm Production Decisions

The buying pattern of the consumers in an economy is known as consumer behaviour. From

the analysis of the consumer behaviour firms can understand the expectation and consumption

pattern. It help firms to identify the tastes and preferences of the consumers, so that the firms will

produce those goods and services that attract the consumers and they tend to buy more.

CONCLUSION

From the above study it has been concluded that the economics plays an important role in

understanding the production and consumption functions of an economy (Ahuja, 2017). The

economists conduct study and help to develop flexible economic policies which provide aid to

the firms to resolve the fundamental problems of the economy. There are different types of

factors that effects the demand and supply of goods and services which are applied differently in

different market structures.

the supply is not much affected (Burke and Abayasekara, 2018).

Market Structure

The structure refers to the competition in the market for goods and services. The market structure

in an economy is affected by the various elements i.e. buyers and sellers in the market. Product

differentiation, entry and exit into the market.

Imperfect competition

In this type of market structure there are many sellers and all are selling heterogeneous goods

and services.

Types

Monopolistic competition: Large number of sellers with different types of goods.

Monopoly: Only single seller of goods with no competition.

Oligopoly: Few seller forms a cartel to sell products at high market price.

Monopsony: Number of sellers in the market and only single buyer.

Oligopsony: Few number of buyers and many sellers.

Consumer Behaviour and Firm Production Decisions

The buying pattern of the consumers in an economy is known as consumer behaviour. From

the analysis of the consumer behaviour firms can understand the expectation and consumption

pattern. It help firms to identify the tastes and preferences of the consumers, so that the firms will

produce those goods and services that attract the consumers and they tend to buy more.

CONCLUSION

From the above study it has been concluded that the economics plays an important role in

understanding the production and consumption functions of an economy (Ahuja, 2017). The

economists conduct study and help to develop flexible economic policies which provide aid to

the firms to resolve the fundamental problems of the economy. There are different types of

factors that effects the demand and supply of goods and services which are applied differently in

different market structures.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Ahuja, H.L., 2017. Business economics. S. Chand Publishing.

Burke, P.J. and Abayasekara, A., 2018. The price elasticity of electricity demand in the United

States: A three-dimensional analysis. The Energy Journal, 39(2).

Carriere-Swallow, M.Y. and Haksar, M.V., 2019. The economics and implications of data: an

integrated perspective. International Monetary Fund.

Christianto, V. and Smarandache, F., 2018. A glimpse into 5 fundamental problems in

economics theorizing, and their possible resolution. Dilbert to, p.138.

Halbert, T. and Ingulli, E., 2020. Law and ethics in the business environment. Cengage Learning.

O'Brien, D.P., 2017. The classical economists revisited. Princeton University Press.

Spulber, D.F., 2019. The economics of markets and platforms. Journal of Economics &

Management Strategy, 28(1), pp.159-172.

Toro-González and et.al, 2020. Factors influencing demand for public transport in

Colombia. Research in Transportation Business & Management, 36, p.100514.

Tronin and et.al, 2019. Formation of innovative strategies of regional economic

development. Space and Culture, India, 7(2), pp.65-75.

Online

Understanding Of Micro And Macro Factors That Affect Your Business, 2021. [Online].

Available through < https://www.mageplaza.com/blog/micro-and-macro-factors-affect-your-

business.html >

Books and Journals

Ahuja, H.L., 2017. Business economics. S. Chand Publishing.

Burke, P.J. and Abayasekara, A., 2018. The price elasticity of electricity demand in the United

States: A three-dimensional analysis. The Energy Journal, 39(2).

Carriere-Swallow, M.Y. and Haksar, M.V., 2019. The economics and implications of data: an

integrated perspective. International Monetary Fund.

Christianto, V. and Smarandache, F., 2018. A glimpse into 5 fundamental problems in

economics theorizing, and their possible resolution. Dilbert to, p.138.

Halbert, T. and Ingulli, E., 2020. Law and ethics in the business environment. Cengage Learning.

O'Brien, D.P., 2017. The classical economists revisited. Princeton University Press.

Spulber, D.F., 2019. The economics of markets and platforms. Journal of Economics &

Management Strategy, 28(1), pp.159-172.

Toro-González and et.al, 2020. Factors influencing demand for public transport in

Colombia. Research in Transportation Business & Management, 36, p.100514.

Tronin and et.al, 2019. Formation of innovative strategies of regional economic

development. Space and Culture, India, 7(2), pp.65-75.

Online

Understanding Of Micro And Macro Factors That Affect Your Business, 2021. [Online].

Available through < https://www.mageplaza.com/blog/micro-and-macro-factors-affect-your-

business.html >

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.