Business Finance and Accounting Report: Budgeting and Finance

VerifiedAdded on 2023/01/12

|10

|3004

|97

Report

AI Summary

This report provides a comprehensive analysis of business finance and accounting principles, focusing on working capital, cash flow management, and budgeting methods. Part 1 defines profit and cash flow, differentiates between them, and explains the terms working capital, accounts receivable, inventory, and payables. It then examines the effects of changing working capital on cash flow and analyzes the impact of working capital on Mediterranean Delights Ltd, offering recommendations for effective cash flow management. Part 2 delves into budgeting, defining its meaning and exploring the advantages and disadvantages of various budgetary approaches, including traditional, rolling, zero-based, and activity-based budgeting. It assesses the effects of different budgeting methods on Second Sight plc and considers the appropriateness of traditional versus modern budgeting systems for future projects. The report uses case studies to illustrate concepts and provides a detailed exploration of financial management.

Business finance and accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

PART 1............................................................................................................................................1

EXICUTIVE SUMMERY...............................................................................................................1

1) a) Explanation of profit and cash flow and their differences..................................................1

b)Explanation of the terms working capital, account receivables, inventory and payables.......2

C) Effect of changing working capital on cash flow..................................................................2

2)Effect of working capital on Mediterranean Delights Ltd.......................................................3

3)Analysis and recommendation for effective cash flow management......................................3

PART2.............................................................................................................................................4

EXICUTIVE SUMMERY...............................................................................................................4

1)Meaning of budget and advantages and disadvantages of various budgetary approaches.....4

2)Effect of budgeting methods on Second sight plc...................................................................6

3)Analysing whether traditional or modern budgetary system is

appropriate for all or any parts of the business for future projects............................................6

REFERENCES................................................................................................................................8

PART 1............................................................................................................................................1

EXICUTIVE SUMMERY...............................................................................................................1

1) a) Explanation of profit and cash flow and their differences..................................................1

b)Explanation of the terms working capital, account receivables, inventory and payables.......2

C) Effect of changing working capital on cash flow..................................................................2

2)Effect of working capital on Mediterranean Delights Ltd.......................................................3

3)Analysis and recommendation for effective cash flow management......................................3

PART2.............................................................................................................................................4

EXICUTIVE SUMMERY...............................................................................................................4

1)Meaning of budget and advantages and disadvantages of various budgetary approaches.....4

2)Effect of budgeting methods on Second sight plc...................................................................6

3)Analysing whether traditional or modern budgetary system is

appropriate for all or any parts of the business for future projects............................................6

REFERENCES................................................................................................................................8

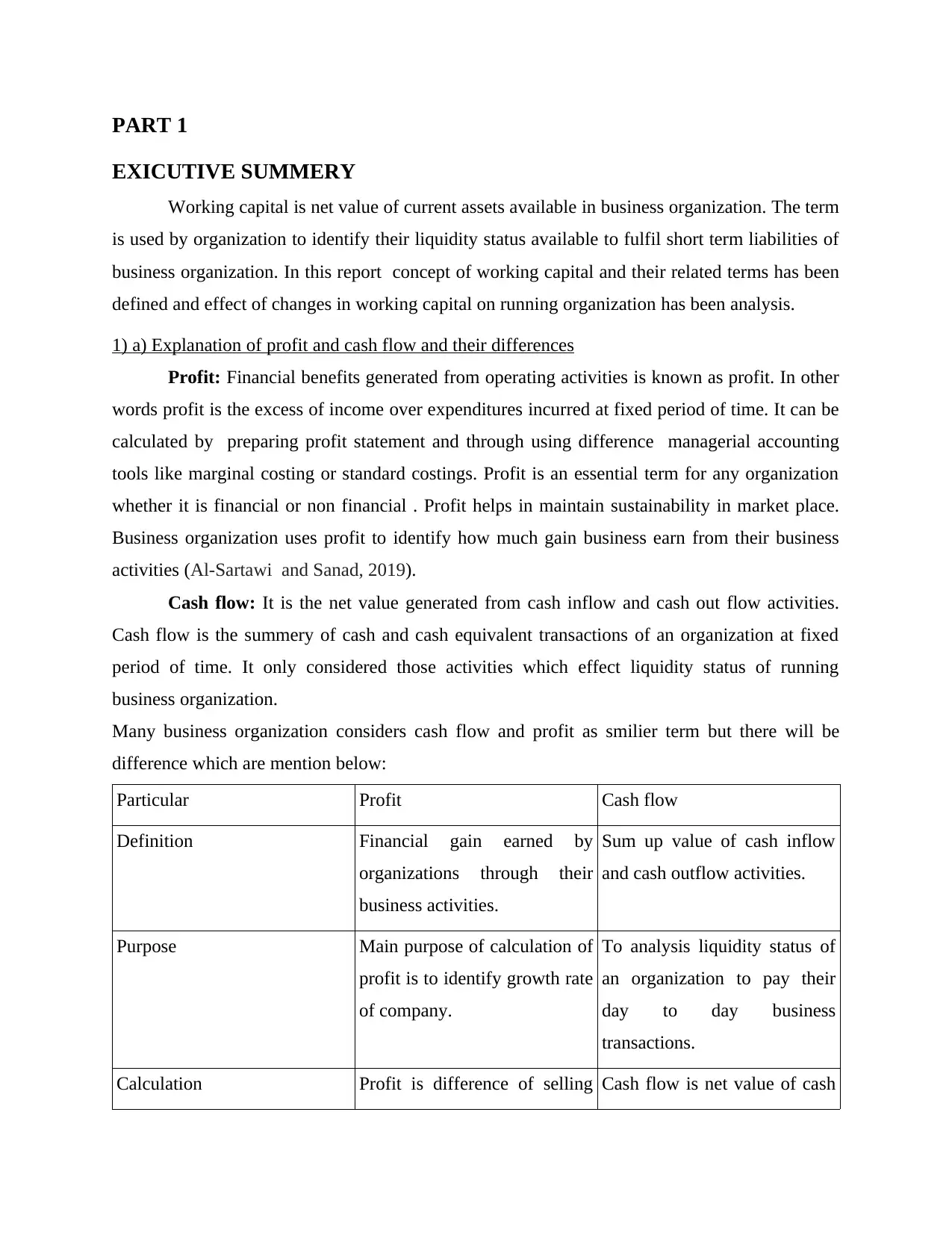

PART 1

EXICUTIVE SUMMERY

Working capital is net value of current assets available in business organization. The term

is used by organization to identify their liquidity status available to fulfil short term liabilities of

business organization. In this report concept of working capital and their related terms has been

defined and effect of changes in working capital on running organization has been analysis.

1) a) Explanation of profit and cash flow and their differences

Profit: Financial benefits generated from operating activities is known as profit. In other

words profit is the excess of income over expenditures incurred at fixed period of time. It can be

calculated by preparing profit statement and through using difference managerial accounting

tools like marginal costing or standard costings. Profit is an essential term for any organization

whether it is financial or non financial . Profit helps in maintain sustainability in market place.

Business organization uses profit to identify how much gain business earn from their business

activities (Al-Sartawi and Sanad, 2019).

Cash flow: It is the net value generated from cash inflow and cash out flow activities.

Cash flow is the summery of cash and cash equivalent transactions of an organization at fixed

period of time. It only considered those activities which effect liquidity status of running

business organization.

Many business organization considers cash flow and profit as smilier term but there will be

difference which are mention below:

Particular Profit Cash flow

Definition Financial gain earned by

organizations through their

business activities.

Sum up value of cash inflow

and cash outflow activities.

Purpose Main purpose of calculation of

profit is to identify growth rate

of company.

To analysis liquidity status of

an organization to pay their

day to day business

transactions.

Calculation Profit is difference of selling Cash flow is net value of cash

EXICUTIVE SUMMERY

Working capital is net value of current assets available in business organization. The term

is used by organization to identify their liquidity status available to fulfil short term liabilities of

business organization. In this report concept of working capital and their related terms has been

defined and effect of changes in working capital on running organization has been analysis.

1) a) Explanation of profit and cash flow and their differences

Profit: Financial benefits generated from operating activities is known as profit. In other

words profit is the excess of income over expenditures incurred at fixed period of time. It can be

calculated by preparing profit statement and through using difference managerial accounting

tools like marginal costing or standard costings. Profit is an essential term for any organization

whether it is financial or non financial . Profit helps in maintain sustainability in market place.

Business organization uses profit to identify how much gain business earn from their business

activities (Al-Sartawi and Sanad, 2019).

Cash flow: It is the net value generated from cash inflow and cash out flow activities.

Cash flow is the summery of cash and cash equivalent transactions of an organization at fixed

period of time. It only considered those activities which effect liquidity status of running

business organization.

Many business organization considers cash flow and profit as smilier term but there will be

difference which are mention below:

Particular Profit Cash flow

Definition Financial gain earned by

organizations through their

business activities.

Sum up value of cash inflow

and cash outflow activities.

Purpose Main purpose of calculation of

profit is to identify growth rate

of company.

To analysis liquidity status of

an organization to pay their

day to day business

transactions.

Calculation Profit is difference of selling Cash flow is net value of cash

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

amount and cost of production

It can be calculated by

preparing profit statement.

inflow and outflow activities.

Managers prepared cash flow

statement for calculating net

amount.

b)Explanation of the terms working capital, account receivables, inventory and payables

Working capital: It is financial metric which represents money available for daily

business transaction within an organization. It is essential part of an entity, managers uses

working capital term to analysis financial position of their organizational market place. It

determined operation efficiency of business. Working capital is the sum up of current assets of

company. Manager uses net working capital which ca be calculate by identifying difference

between current assets and current liabilities (Bassemir and Novotny‐Farkas, 2018).

Account receivables: Net amount claim by company on their customers for utilizing

their products and services. It is considered as assets of business entity and shown in current

assets side of balance sheet.

Inventory: It is most essential part of working capital. This term is defines as net value

of raw materials and essential equipment used by business organization for producing and

supplying their product to customers.

Payable: This term defines as amount claim by creditors to company for trading their

products to run business organization. Account payable generates liabilities on company thus it

will be shown in current liability side in balance sheet.

C) Effect of changing working capital on cash flow

Working capital and cash flow both are essential terms for organization to run their

business organization effectively. Managers uses working capital ratio to identity their liquidity

rate. Cash flow considered only cash and cash equivalent activities Increment in current liability

increase cash inflows and increment in current assets value generated cash outflow actives. This

defines that when ratio of working capital increase then it will adversely effect on cash flows as

cash outflow activities generated . On the other side decrement in working capital, positevly

affect cash slow as it help in generating cash inflow activities.

It can be calculated by

preparing profit statement.

inflow and outflow activities.

Managers prepared cash flow

statement for calculating net

amount.

b)Explanation of the terms working capital, account receivables, inventory and payables

Working capital: It is financial metric which represents money available for daily

business transaction within an organization. It is essential part of an entity, managers uses

working capital term to analysis financial position of their organizational market place. It

determined operation efficiency of business. Working capital is the sum up of current assets of

company. Manager uses net working capital which ca be calculate by identifying difference

between current assets and current liabilities (Bassemir and Novotny‐Farkas, 2018).

Account receivables: Net amount claim by company on their customers for utilizing

their products and services. It is considered as assets of business entity and shown in current

assets side of balance sheet.

Inventory: It is most essential part of working capital. This term is defines as net value

of raw materials and essential equipment used by business organization for producing and

supplying their product to customers.

Payable: This term defines as amount claim by creditors to company for trading their

products to run business organization. Account payable generates liabilities on company thus it

will be shown in current liability side in balance sheet.

C) Effect of changing working capital on cash flow

Working capital and cash flow both are essential terms for organization to run their

business organization effectively. Managers uses working capital ratio to identity their liquidity

rate. Cash flow considered only cash and cash equivalent activities Increment in current liability

increase cash inflows and increment in current assets value generated cash outflow actives. This

defines that when ratio of working capital increase then it will adversely effect on cash flows as

cash outflow activities generated . On the other side decrement in working capital, positevly

affect cash slow as it help in generating cash inflow activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2)Effect of working capital on Mediterranean Delights Ltd

Mediterranean Delights Ltd is situated in England. The company had supply chain of

restaurant at different places all over England which help in provides their products and services

to their customers. Effect of working capital and their related terms are mention below:

1. Profit: Mediterranean Delights Ltd earn 50 million pound in preceding financial year.

Due to lack of knowledge available related to interest amount and liability of tax it has

been assumed that 250 million is their net amount of value.

2. Receivables: Due to dispute arises with San Pedro, ration of receivables increase which

adversely effect on working capital cycle as it will be chances company lost their

potential customers.

3. Payable: Due to lack of managerial policies company unable to found suppliers with

whom they trade on benefits . Ratio of payables is increase which means company take

long time to pay their debt. In case of MDL conflicts arises them with Maltese

agricultural group, Valletta Ltd as they provides them low quality of material.

4. Ash flow: This term considered only cash and cash equivalent activities. In the last year

cash inflow activities generated by selling their products. Company invest with Italian

company and pay amount to them it will generated outflows. Company also has turnover

of 50 million in last year (Cockcroft and Russell, 201Hasibuan and Syahrial, 2019).

5. Working capital: The term refers to net amount of current assets after deducting current

liabilities. Working capital of Maltese agricultural group, Valletta Ltd will be adversely

affect on their business activities due to disputes and effective management policies

Companies working capital status is shown negative result but due to strong financial

position company van bear their day to day operation activities transaction easily.

3)Analysis and recommendation for effective cash flow management

Mediterranean Delights Ltd is run their business from past 30 years. The company earn

excellent profit in past year but due to lack of effective policy of management, company suffers

from many problem. Mediterranean Delights Ltd have conflict with their potential customers and

their supplier also sue on them regarding non payment of purchasing raw material. All the things

will adversely effect on their cash flow activities. It will decrease their growth rate. To overcome

this problems manager needs to formulate effective working capital management policies

Mediterranean Delights Ltd is situated in England. The company had supply chain of

restaurant at different places all over England which help in provides their products and services

to their customers. Effect of working capital and their related terms are mention below:

1. Profit: Mediterranean Delights Ltd earn 50 million pound in preceding financial year.

Due to lack of knowledge available related to interest amount and liability of tax it has

been assumed that 250 million is their net amount of value.

2. Receivables: Due to dispute arises with San Pedro, ration of receivables increase which

adversely effect on working capital cycle as it will be chances company lost their

potential customers.

3. Payable: Due to lack of managerial policies company unable to found suppliers with

whom they trade on benefits . Ratio of payables is increase which means company take

long time to pay their debt. In case of MDL conflicts arises them with Maltese

agricultural group, Valletta Ltd as they provides them low quality of material.

4. Ash flow: This term considered only cash and cash equivalent activities. In the last year

cash inflow activities generated by selling their products. Company invest with Italian

company and pay amount to them it will generated outflows. Company also has turnover

of 50 million in last year (Cockcroft and Russell, 201Hasibuan and Syahrial, 2019).

5. Working capital: The term refers to net amount of current assets after deducting current

liabilities. Working capital of Maltese agricultural group, Valletta Ltd will be adversely

affect on their business activities due to disputes and effective management policies

Companies working capital status is shown negative result but due to strong financial

position company van bear their day to day operation activities transaction easily.

3)Analysis and recommendation for effective cash flow management

Mediterranean Delights Ltd is run their business from past 30 years. The company earn

excellent profit in past year but due to lack of effective policy of management, company suffers

from many problem. Mediterranean Delights Ltd have conflict with their potential customers and

their supplier also sue on them regarding non payment of purchasing raw material. All the things

will adversely effect on their cash flow activities. It will decrease their growth rate. To overcome

this problems manager needs to formulate effective working capital management policies

through which they can easily bear debt liabilities of their operational activities. For this purpose

they need to make effective debtor policy which help in attracting customers and influencing

them to pay their liability in short time period. It will help in generating cash inflow activities.

They need to solve dispute problem with their creditors so that they cannot bear penalty amount .

Mediterranean Delights Ltd needs to use effective environment scanning tool which help in

identifying potential supplier which provides them high quality of raw materiel at discount rate.

They also need to change their cash management policies. They need to focus on activites by

which they generated more profit ( AugustKim, Li, and Liu, Z2018).

PART2

EXICUTIVE SUMMERY

Budget is detailed plan of a business organizations which covered all the part of business

activities. Managers prepared budgets to identify future income. It play important role in

business finance. In this report concept of budgeting methods has been analysis and how

effectively traditional and modern methods of preparation of budget effete on business decision

process is defined specifically It will help in understanding how management take decision

related to preparation of making budget.

1)Meaning of budget and advantages and disadvantages of various budgetary approaches

Budget: It is a numerical statement which is used for identifying future income and

expenditure of an running business entity. In other words, Budget is predetermined statement of

expected future earning and payments. It is technique of managerial accounting. Every

organization. prepare budget it is essential part of managerial process. Managers prepared budget

for performance evaluation of their employees. Business organisation prepared budget for taking

best decision which help in achieving goals with optimum utilization of resources. Process of

preparation of budget statement is known as budgeting. Following are the methods managers

used for preparation of budget.

Traditional budgeting method: In this method budgets are prepared by considering past

year data. Managers prepared future budget with the uses of previous years performance data of

company.

Advantages:

they need to make effective debtor policy which help in attracting customers and influencing

them to pay their liability in short time period. It will help in generating cash inflow activities.

They need to solve dispute problem with their creditors so that they cannot bear penalty amount .

Mediterranean Delights Ltd needs to use effective environment scanning tool which help in

identifying potential supplier which provides them high quality of raw materiel at discount rate.

They also need to change their cash management policies. They need to focus on activites by

which they generated more profit ( AugustKim, Li, and Liu, Z2018).

PART2

EXICUTIVE SUMMERY

Budget is detailed plan of a business organizations which covered all the part of business

activities. Managers prepared budgets to identify future income. It play important role in

business finance. In this report concept of budgeting methods has been analysis and how

effectively traditional and modern methods of preparation of budget effete on business decision

process is defined specifically It will help in understanding how management take decision

related to preparation of making budget.

1)Meaning of budget and advantages and disadvantages of various budgetary approaches

Budget: It is a numerical statement which is used for identifying future income and

expenditure of an running business entity. In other words, Budget is predetermined statement of

expected future earning and payments. It is technique of managerial accounting. Every

organization. prepare budget it is essential part of managerial process. Managers prepared budget

for performance evaluation of their employees. Business organisation prepared budget for taking

best decision which help in achieving goals with optimum utilization of resources. Process of

preparation of budget statement is known as budgeting. Following are the methods managers

used for preparation of budget.

Traditional budgeting method: In this method budgets are prepared by considering past

year data. Managers prepared future budget with the uses of previous years performance data of

company.

Advantages:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is cost effective technique of budgeting as organizations need not to incurred expense

on research and hiring expert for preparation of budget.

Preparation of budget with this method is very easy to understand statement of budget

Disadvantage:

It does not provides accurate and reliable data as budgets is prepared by considering last

past years data.

Employees does not feel motivated because budgets are prepared by top level of

management (Linares-Mustarós, Coenders, G. and Vives-Mestres, 201Mnif Sellami, and

Gafsi, 2019).

Alternative methods: With changes of business environment new methods are

developed. Following are the methods of modern techniques of preparation of budget

Rolling budget: In this method budgets are prepared on continuously basis until the time

period of achieving goal does not completed. It is also known as roll-over budget.

Advantages:

With the use of this method workforce focusing on achieving their goal at fix time.

This method help in identifying performance evaluation of various departments.

Disadvantage:

It is very time consuming process.

Using rolling budgets can increase uncertainty of regular activities running organization.

Zero based budget: In this method budgets are prepared from scratch level. Managers started

from initial level and prepared budget on the basis of collection of research data. This type of

method is useful for newly established organization.

Advantage:

By using this method organization can be utilizing their resource effectively.

It will provided accurate information related future earning and expenses.

Disadvantage:

Due to rigid process of budgeting business organization can not focusing on opportunities

and threat in market economy.

It incurred high cost of preparation of budget by this method.

on research and hiring expert for preparation of budget.

Preparation of budget with this method is very easy to understand statement of budget

Disadvantage:

It does not provides accurate and reliable data as budgets is prepared by considering last

past years data.

Employees does not feel motivated because budgets are prepared by top level of

management (Linares-Mustarós, Coenders, G. and Vives-Mestres, 201Mnif Sellami, and

Gafsi, 2019).

Alternative methods: With changes of business environment new methods are

developed. Following are the methods of modern techniques of preparation of budget

Rolling budget: In this method budgets are prepared on continuously basis until the time

period of achieving goal does not completed. It is also known as roll-over budget.

Advantages:

With the use of this method workforce focusing on achieving their goal at fix time.

This method help in identifying performance evaluation of various departments.

Disadvantage:

It is very time consuming process.

Using rolling budgets can increase uncertainty of regular activities running organization.

Zero based budget: In this method budgets are prepared from scratch level. Managers started

from initial level and prepared budget on the basis of collection of research data. This type of

method is useful for newly established organization.

Advantage:

By using this method organization can be utilizing their resource effectively.

It will provided accurate information related future earning and expenses.

Disadvantage:

Due to rigid process of budgeting business organization can not focusing on opportunities

and threat in market economy.

It incurred high cost of preparation of budget by this method.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based budgeting: It is most useful technique for manufacturing organizations.

In this technique budgets are prepared on the basis of activity costing. Managers identify cost

incurred on allocation of resources and then prepare budget on the basis of collection of allocated

data. It is very useful method. Following are the benefit sand drawbacks of activity based

budgeting method:

Advantage:

It will help in managing time of organization by reducing wastage activities.

It is flexible method manager can be used this method by analysing market demand.

Disadvantage:

It is complex and hardly to understand process.

Budgets are prepared on the basis of second source of information.

2)Effect of budgeting methods on Second sight plc

Second Sight is multinational business organization which run their sunglasses business all over

the England. Headquarter of this is situated at Manchester. Now the company want to expand

their business units in India and Netherlands. Management can be used traditional as well as

modern technique of budgeting to identify future earning and formulation of policies to achieve

these project. In traditional budgeting method, budgets are prepared on the basis of past year

data. Manager will be used this method as it will help them in saving their cost and provided

data. Manager department of this organization will be used modern methods of preparation of

budgets as it will help in provides accurate data which will help in deicide in best options related

to projects (Muñoz‐Torres, Fernández‐Izquierdo, Rivera‐Lirio and Escrig‐Olmedo, 2019). Zero

based method help them to prepared budget on the basis of analysing present information. If they

prepared their budget from activity budgeting then it will help them in utilization their resource

efficiently. Second Sight Plc is run their business since past 10 years they earn 250 million

turnover in last year. It is responsibility of their managers to countries run their business by

current probability rate and for this purpose they can be apply methods of budgeting which help

them in taking better decision.

In this technique budgets are prepared on the basis of activity costing. Managers identify cost

incurred on allocation of resources and then prepare budget on the basis of collection of allocated

data. It is very useful method. Following are the benefit sand drawbacks of activity based

budgeting method:

Advantage:

It will help in managing time of organization by reducing wastage activities.

It is flexible method manager can be used this method by analysing market demand.

Disadvantage:

It is complex and hardly to understand process.

Budgets are prepared on the basis of second source of information.

2)Effect of budgeting methods on Second sight plc

Second Sight is multinational business organization which run their sunglasses business all over

the England. Headquarter of this is situated at Manchester. Now the company want to expand

their business units in India and Netherlands. Management can be used traditional as well as

modern technique of budgeting to identify future earning and formulation of policies to achieve

these project. In traditional budgeting method, budgets are prepared on the basis of past year

data. Manager will be used this method as it will help them in saving their cost and provided

data. Manager department of this organization will be used modern methods of preparation of

budgets as it will help in provides accurate data which will help in deicide in best options related

to projects (Muñoz‐Torres, Fernández‐Izquierdo, Rivera‐Lirio and Escrig‐Olmedo, 2019). Zero

based method help them to prepared budget on the basis of analysing present information. If they

prepared their budget from activity budgeting then it will help them in utilization their resource

efficiently. Second Sight Plc is run their business since past 10 years they earn 250 million

turnover in last year. It is responsibility of their managers to countries run their business by

current probability rate and for this purpose they can be apply methods of budgeting which help

them in taking better decision.

3)Analysing whether traditional or modern budgetary system is

appropriate for all or any parts of the business for future projects

Budget is essential part of strategic management. This numerical statement help

management to determined best alternative among other alternative. Success of business models

depends on the skills of managers preparation of budget. Business organization choose methods

for budgeting process according to external and internal environment factors of organization. In

the case of Second sight manager will be choose budgeting method which help in providing

accurate information related to future. Budgeting methods help in providing direction and

guidelines of preparation of budget but not all methods are suitable on particular budgets. Each

budgeting method has its own benefits and drawbacks. Second Sight is prepare budget for their

new projects which is run in Indian and Netherlands target market. For Indian market they can

use Zero based budgeting and rolling budgeting methods both provides relevant information

related to future earning because trading in Indian market is too risky and difficult process.

Business organization would not apply traditional and activity based budgeting method for

Indian project because Second Sight would not trade their products in India (Ng, 2018.).

Market segment is also difference in Indian sector thus they need to start from zero basis to

research all the market condition of India and formulate polices on the basis of new data. Rolling

based budget is also effective for this project as in this technique they ca change their polices

after analysing market condition within short time period but it is time consuming process as

compare to zero bas3ed budgeting method. For Netherlands project manager will be choose

traditional method. Market requirement of this country is similar as Manchester market thus it is

effective for Second Sight plc to apply this method it will give best results. They can also used

activity based budgeting technique for this project as market area is limited. Activity based

budgeting method help in in allocation of resource in best ways.

appropriate for all or any parts of the business for future projects

Budget is essential part of strategic management. This numerical statement help

management to determined best alternative among other alternative. Success of business models

depends on the skills of managers preparation of budget. Business organization choose methods

for budgeting process according to external and internal environment factors of organization. In

the case of Second sight manager will be choose budgeting method which help in providing

accurate information related to future. Budgeting methods help in providing direction and

guidelines of preparation of budget but not all methods are suitable on particular budgets. Each

budgeting method has its own benefits and drawbacks. Second Sight is prepare budget for their

new projects which is run in Indian and Netherlands target market. For Indian market they can

use Zero based budgeting and rolling budgeting methods both provides relevant information

related to future earning because trading in Indian market is too risky and difficult process.

Business organization would not apply traditional and activity based budgeting method for

Indian project because Second Sight would not trade their products in India (Ng, 2018.).

Market segment is also difference in Indian sector thus they need to start from zero basis to

research all the market condition of India and formulate polices on the basis of new data. Rolling

based budget is also effective for this project as in this technique they ca change their polices

after analysing market condition within short time period but it is time consuming process as

compare to zero bas3ed budgeting method. For Netherlands project manager will be choose

traditional method. Market requirement of this country is similar as Manchester market thus it is

effective for Second Sight plc to apply this method it will give best results. They can also used

activity based budgeting technique for this project as market area is limited. Activity based

budgeting method help in in allocation of resource in best ways.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journals

Al-Sartawi, A.M.M. and Sanad, Z., 2019. Institutional ownership and corporate governance:

evidence from Bahrain. Afro-Asian Journal of Finance and Accounting 9(1) .pp.101-

115.

Bassemir, M. and Novotny‐Farkas, Z., 2018. IFRS adoption, reporting incentives and financial

reporting quality in private firms. Journal of Business Finance & Accounting, 45(7-8).

pp.759-796.

Cockcroft, S. and Russell, M., 2018. Big data opportunities for accounting and finance practice

and research. Australian Accounting Review, 28(3). pp.323-333.

Hasibuan, R. P. S. and Syahrial, H., 2019, August. Analysis Of The Implementation Effects Of

Accrual-Based Governmental Accounting Standards On The Financial Statement

Qualities. In Proceeding ICOPOID 2019 The 2nd International Conference on Politic

of Islamic Development (Vol. 1, No. 1, pp. 18-29).

Kim, J. B., Li, B. and Liu, Z., 2018. Does social performance influence breadth of

ownership?. Journal of Business Finance & Accounting, 45(9-10). pp.1164-1194.

Linares-Mustarós, S., Coenders, G. and Vives-Mestres, M., 2018. Financial performance and

distress profiles. From classification according to financial ratios to compositional

classification. Advances in Accounting 40 pp.1-10.

Mnif Sellami, Y. and Gafsi, Y., 2019. Institutional and economic factors affecting the adoption

of international public sector accounting standards. International Journal of Public

Administration, 42(2).pp.119-131.

Muñoz‐Torres, M. J., Fernández‐Izquierdo, M. Á., Rivera‐Lirio, J. M. and Escrig‐Olmedo, E.,

2019. Can environmental, social, and governance rating agencies favor business models

that promote a more sustainable development?. Corporate Social Responsibility and

Environmental Management, 26(2) pp.439-452.

Ng, A. W., 2018. From sustainability accounting to a green financing system: institutional

legitimacy and market heterogeneity in a global financial centre. Journal of Cleaner

Production, 195.pp.585-592.

Books and journals

Al-Sartawi, A.M.M. and Sanad, Z., 2019. Institutional ownership and corporate governance:

evidence from Bahrain. Afro-Asian Journal of Finance and Accounting 9(1) .pp.101-

115.

Bassemir, M. and Novotny‐Farkas, Z., 2018. IFRS adoption, reporting incentives and financial

reporting quality in private firms. Journal of Business Finance & Accounting, 45(7-8).

pp.759-796.

Cockcroft, S. and Russell, M., 2018. Big data opportunities for accounting and finance practice

and research. Australian Accounting Review, 28(3). pp.323-333.

Hasibuan, R. P. S. and Syahrial, H., 2019, August. Analysis Of The Implementation Effects Of

Accrual-Based Governmental Accounting Standards On The Financial Statement

Qualities. In Proceeding ICOPOID 2019 The 2nd International Conference on Politic

of Islamic Development (Vol. 1, No. 1, pp. 18-29).

Kim, J. B., Li, B. and Liu, Z., 2018. Does social performance influence breadth of

ownership?. Journal of Business Finance & Accounting, 45(9-10). pp.1164-1194.

Linares-Mustarós, S., Coenders, G. and Vives-Mestres, M., 2018. Financial performance and

distress profiles. From classification according to financial ratios to compositional

classification. Advances in Accounting 40 pp.1-10.

Mnif Sellami, Y. and Gafsi, Y., 2019. Institutional and economic factors affecting the adoption

of international public sector accounting standards. International Journal of Public

Administration, 42(2).pp.119-131.

Muñoz‐Torres, M. J., Fernández‐Izquierdo, M. Á., Rivera‐Lirio, J. M. and Escrig‐Olmedo, E.,

2019. Can environmental, social, and governance rating agencies favor business models

that promote a more sustainable development?. Corporate Social Responsibility and

Environmental Management, 26(2) pp.439-452.

Ng, A. W., 2018. From sustainability accounting to a green financing system: institutional

legitimacy and market heterogeneity in a global financial centre. Journal of Cleaner

Production, 195.pp.585-592.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.