Finance Case Study: TVM, Bond Valuation, and Risk/Return Analysis

VerifiedAdded on 2022/09/23

|13

|2141

|26

Homework Assignment

AI Summary

This finance assignment, prepared for ACC00716, delves into the core concepts of financial analysis, including time value of money (TVM) and bond valuation. The assignment begins with calculations related to loan amounts, revenue forecasts, and effective interest rates for different loan options. It then proceeds to determine periodic payments, yield to maturity (YTM), and bond prices. Furthermore, the assignment extends to risk and return analysis, calculating expected returns using the Capital Asset Pricing Model (CAPM) and determining portfolio beta. It includes the analysis of a case company's stock and a hypothetical company to illustrate the risk-return trade-off and the importance of diversification in portfolio management. The assignment concludes with a discussion on the modern portfolio theory, highlighting the significance of diversification in mitigating unsystematic risk and constructing optimal portfolios, referencing the Markowitz efficient frontier and the capital allocation line.

Running head: QUESTION AND ANSWER

Question and Answer

Name of the Student:

Name of the University:

Author Note:

Question and Answer

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1Answer to Question 1:Answer to Question 1:

Table of Contents

Answer to Question 1:................................................................................................................2

Part a:.....................................................................................................................................2

Part b:.....................................................................................................................................2

Part c:.....................................................................................................................................3

Part d:.....................................................................................................................................4

Part e:.....................................................................................................................................5

Part f:......................................................................................................................................5

Answer to Question 2:................................................................................................................6

Part a:.....................................................................................................................................6

Part b:.....................................................................................................................................7

Answer to Question 3:................................................................................................................8

References:...............................................................................................................................11

Table of Contents

Answer to Question 1:................................................................................................................2

Part a:.....................................................................................................................................2

Part b:.....................................................................................................................................2

Part c:.....................................................................................................................................3

Part d:.....................................................................................................................................4

Part e:.....................................................................................................................................5

Part f:......................................................................................................................................5

Answer to Question 2:................................................................................................................6

Part a:.....................................................................................................................................6

Part b:.....................................................................................................................................7

Answer to Question 3:................................................................................................................8

References:...............................................................................................................................11

2Answer to Question 1:Answer to Question 1:

Answer to Question 1:

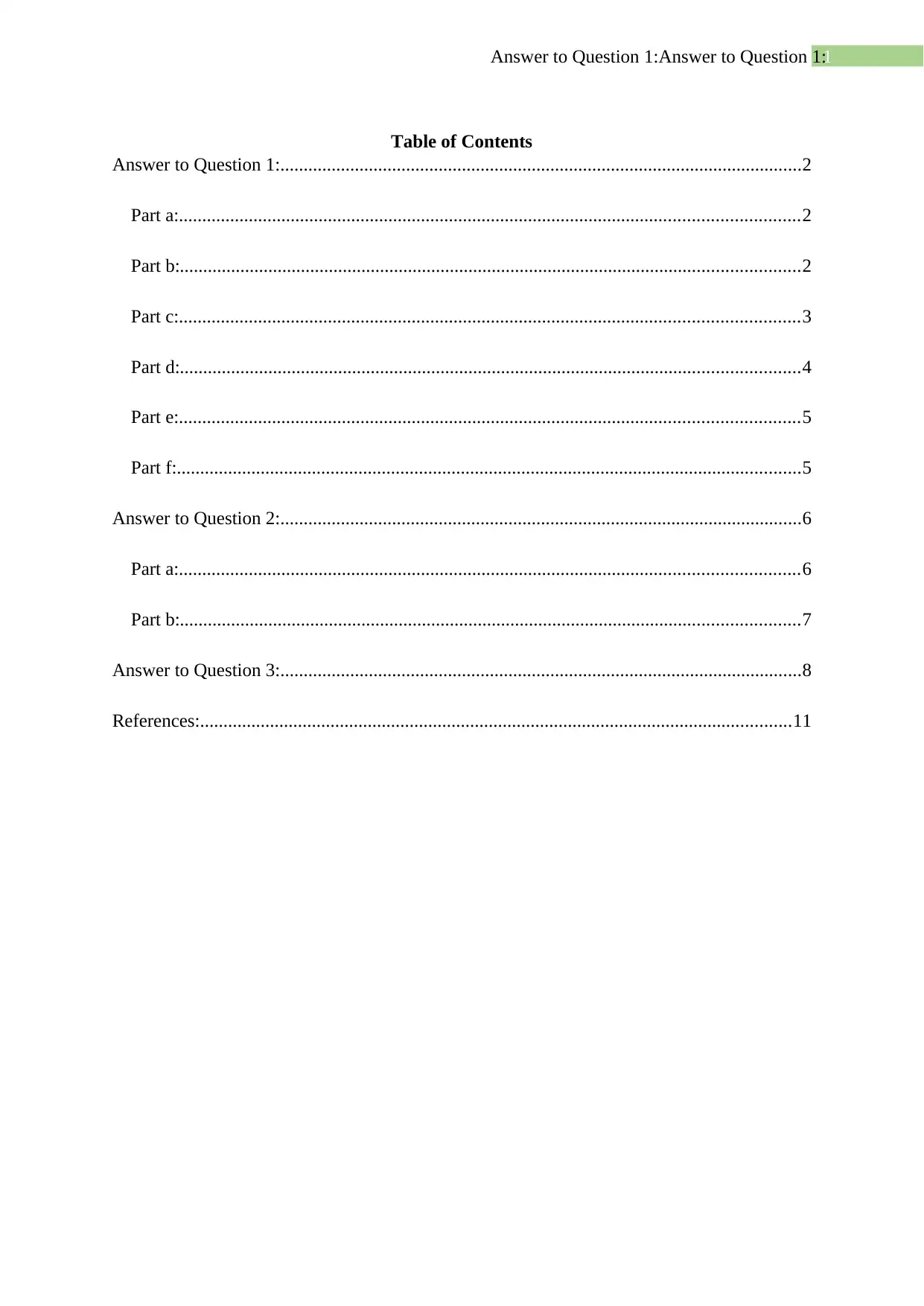

Part a:

The amount of loan which is taken by the company for the equipment is $27724.9.

The calculation in excel is provided in the figure below along with the excel formula which is

used for the calculation.

Figure 1: Amount of Loan taken by the Company

Source: By the Author

Part b:

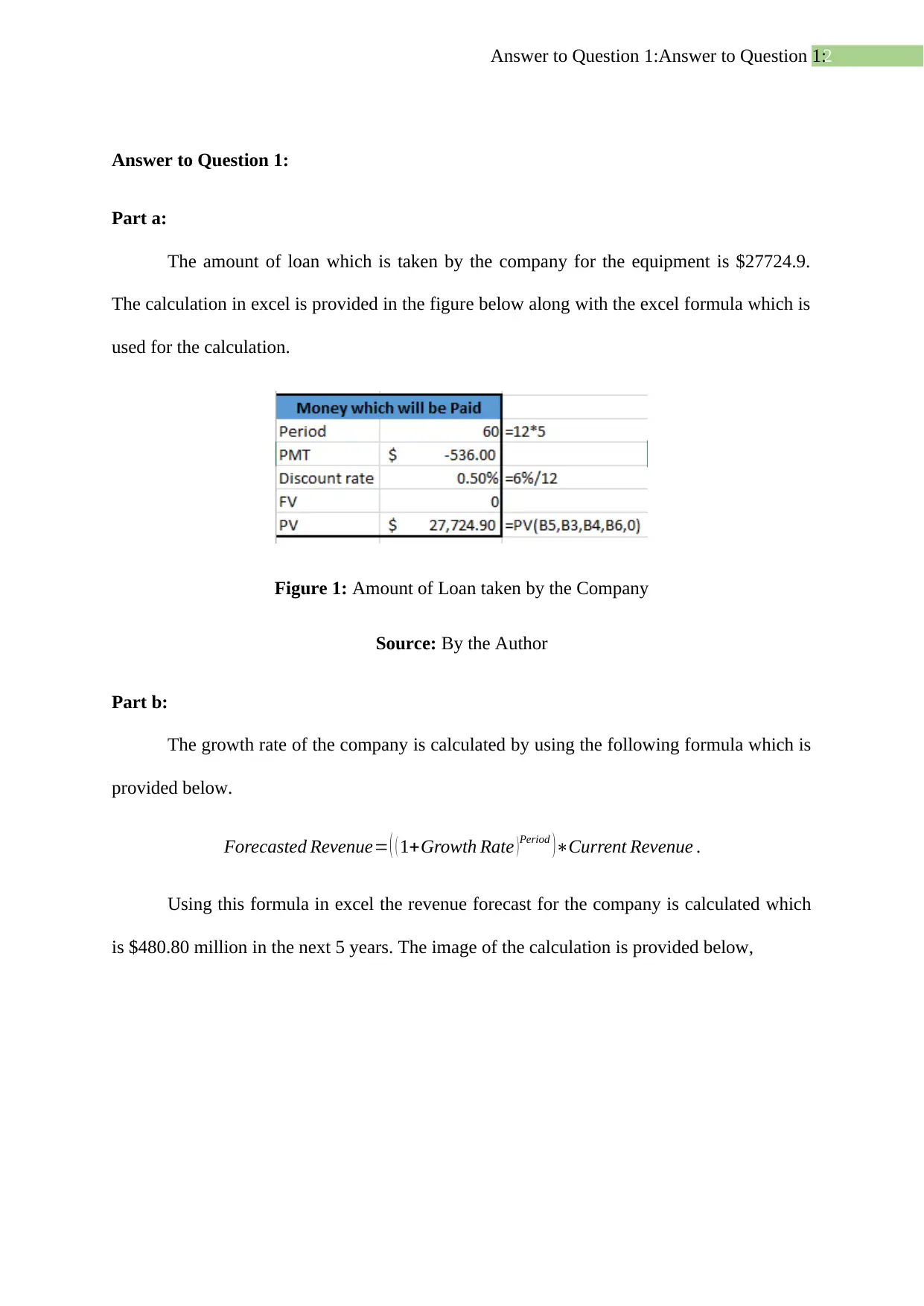

The growth rate of the company is calculated by using the following formula which is

provided below.

Forecasted Revenue= ( ( 1+Growth Rate ) Period )∗Current Revenue .

Using this formula in excel the revenue forecast for the company is calculated which

is $480.80 million in the next 5 years. The image of the calculation is provided below,

Answer to Question 1:

Part a:

The amount of loan which is taken by the company for the equipment is $27724.9.

The calculation in excel is provided in the figure below along with the excel formula which is

used for the calculation.

Figure 1: Amount of Loan taken by the Company

Source: By the Author

Part b:

The growth rate of the company is calculated by using the following formula which is

provided below.

Forecasted Revenue= ( ( 1+Growth Rate ) Period )∗Current Revenue .

Using this formula in excel the revenue forecast for the company is calculated which

is $480.80 million in the next 5 years. The image of the calculation is provided below,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3Answer to Question 1:Answer to Question 1:

Figure 2: Annual Revenue Forecast

Source: By the Author

Part c:

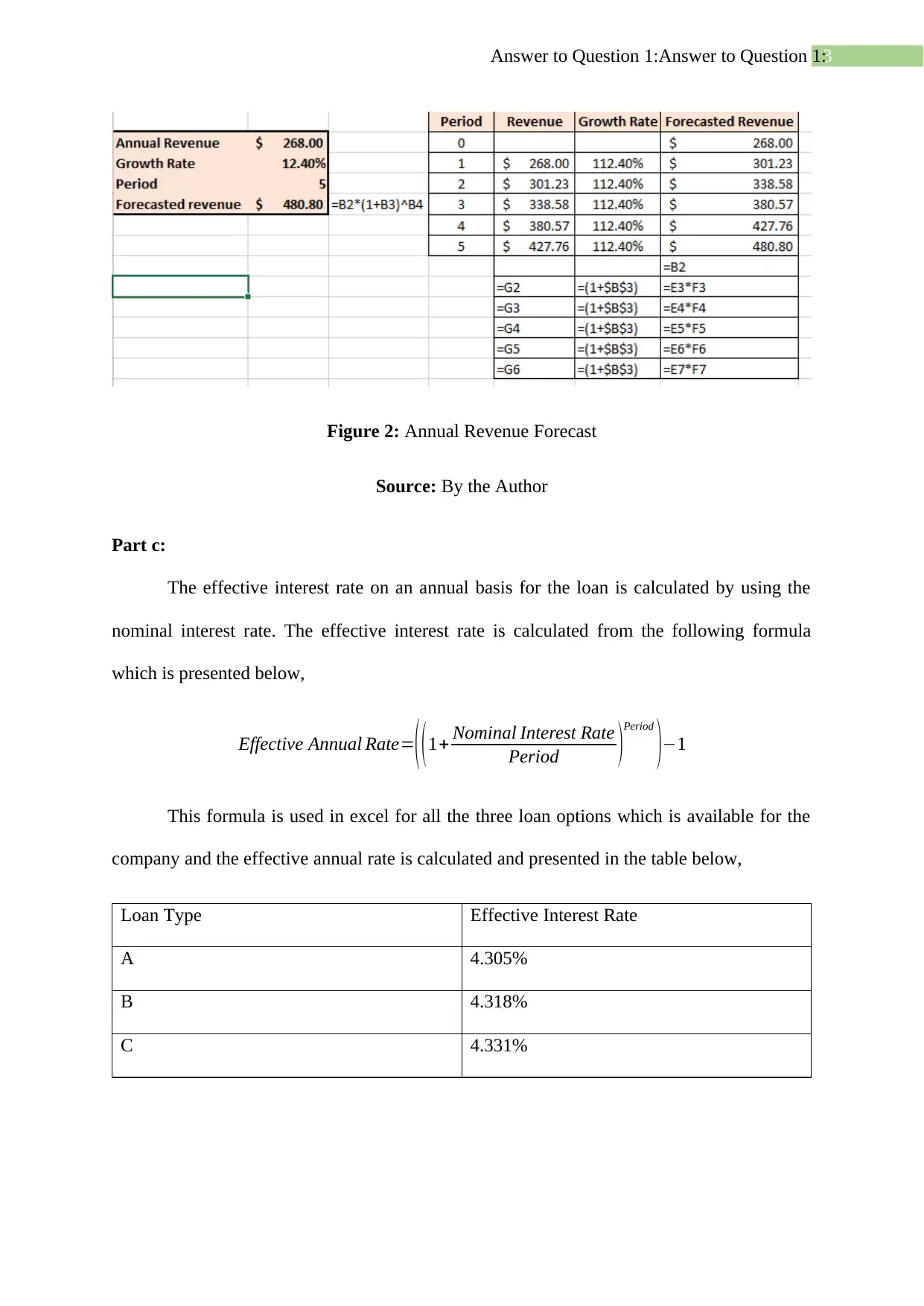

The effective interest rate on an annual basis for the loan is calculated by using the

nominal interest rate. The effective interest rate is calculated from the following formula

which is presented below,

Effective Annual Rate=

( (1+ Nominal Interest Rate

Period )Period

)−1

This formula is used in excel for all the three loan options which is available for the

company and the effective annual rate is calculated and presented in the table below,

Loan Type Effective Interest Rate

A 4.305%

B 4.318%

C 4.331%

Figure 2: Annual Revenue Forecast

Source: By the Author

Part c:

The effective interest rate on an annual basis for the loan is calculated by using the

nominal interest rate. The effective interest rate is calculated from the following formula

which is presented below,

Effective Annual Rate=

( (1+ Nominal Interest Rate

Period )Period

)−1

This formula is used in excel for all the three loan options which is available for the

company and the effective annual rate is calculated and presented in the table below,

Loan Type Effective Interest Rate

A 4.305%

B 4.318%

C 4.331%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4Answer to Question 1:Answer to Question 1:

The loan option A has the lowest effective interest rate out of the three options which

means Loan option A would cost the company the lowest interest rate and should be chosen

by the company. Also the calculation in excel which has been done is presented in the figure

below,

Figure 3: Effective interest rate of loan options

Source: By the Author

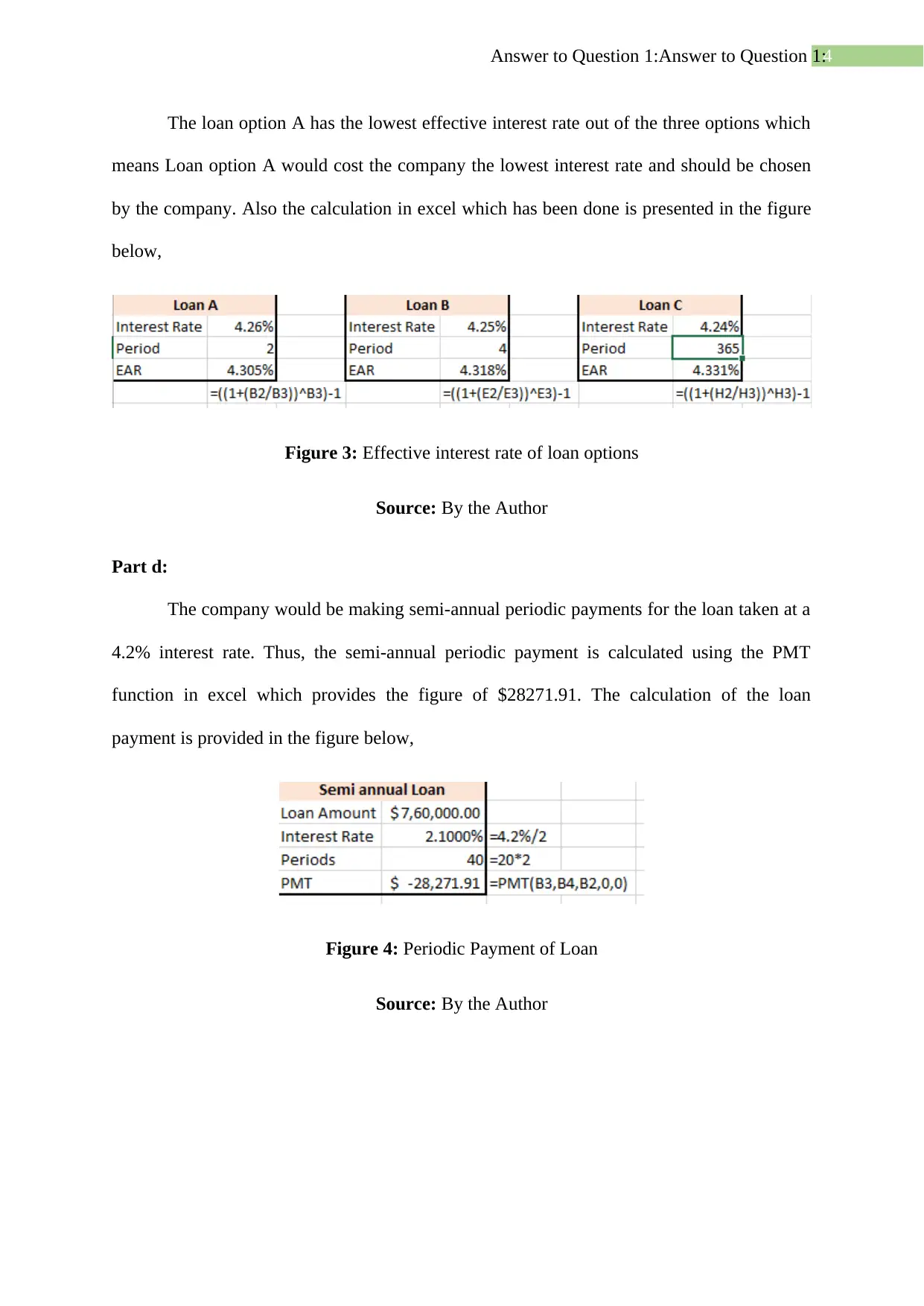

Part d:

The company would be making semi-annual periodic payments for the loan taken at a

4.2% interest rate. Thus, the semi-annual periodic payment is calculated using the PMT

function in excel which provides the figure of $28271.91. The calculation of the loan

payment is provided in the figure below,

Figure 4: Periodic Payment of Loan

Source: By the Author

The loan option A has the lowest effective interest rate out of the three options which

means Loan option A would cost the company the lowest interest rate and should be chosen

by the company. Also the calculation in excel which has been done is presented in the figure

below,

Figure 3: Effective interest rate of loan options

Source: By the Author

Part d:

The company would be making semi-annual periodic payments for the loan taken at a

4.2% interest rate. Thus, the semi-annual periodic payment is calculated using the PMT

function in excel which provides the figure of $28271.91. The calculation of the loan

payment is provided in the figure below,

Figure 4: Periodic Payment of Loan

Source: By the Author

5Answer to Question 1:Answer to Question 1:

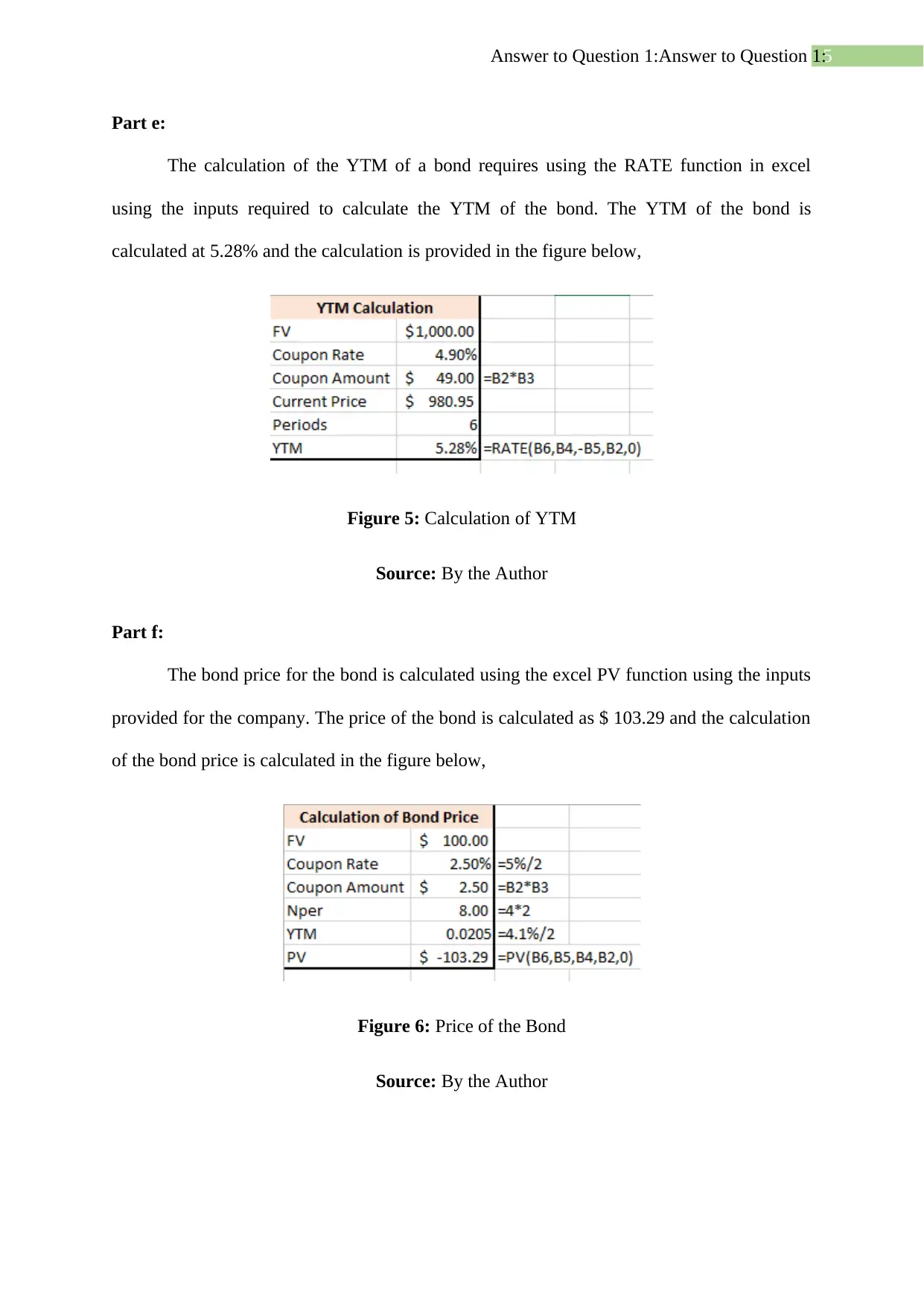

Part e:

The calculation of the YTM of a bond requires using the RATE function in excel

using the inputs required to calculate the YTM of the bond. The YTM of the bond is

calculated at 5.28% and the calculation is provided in the figure below,

Figure 5: Calculation of YTM

Source: By the Author

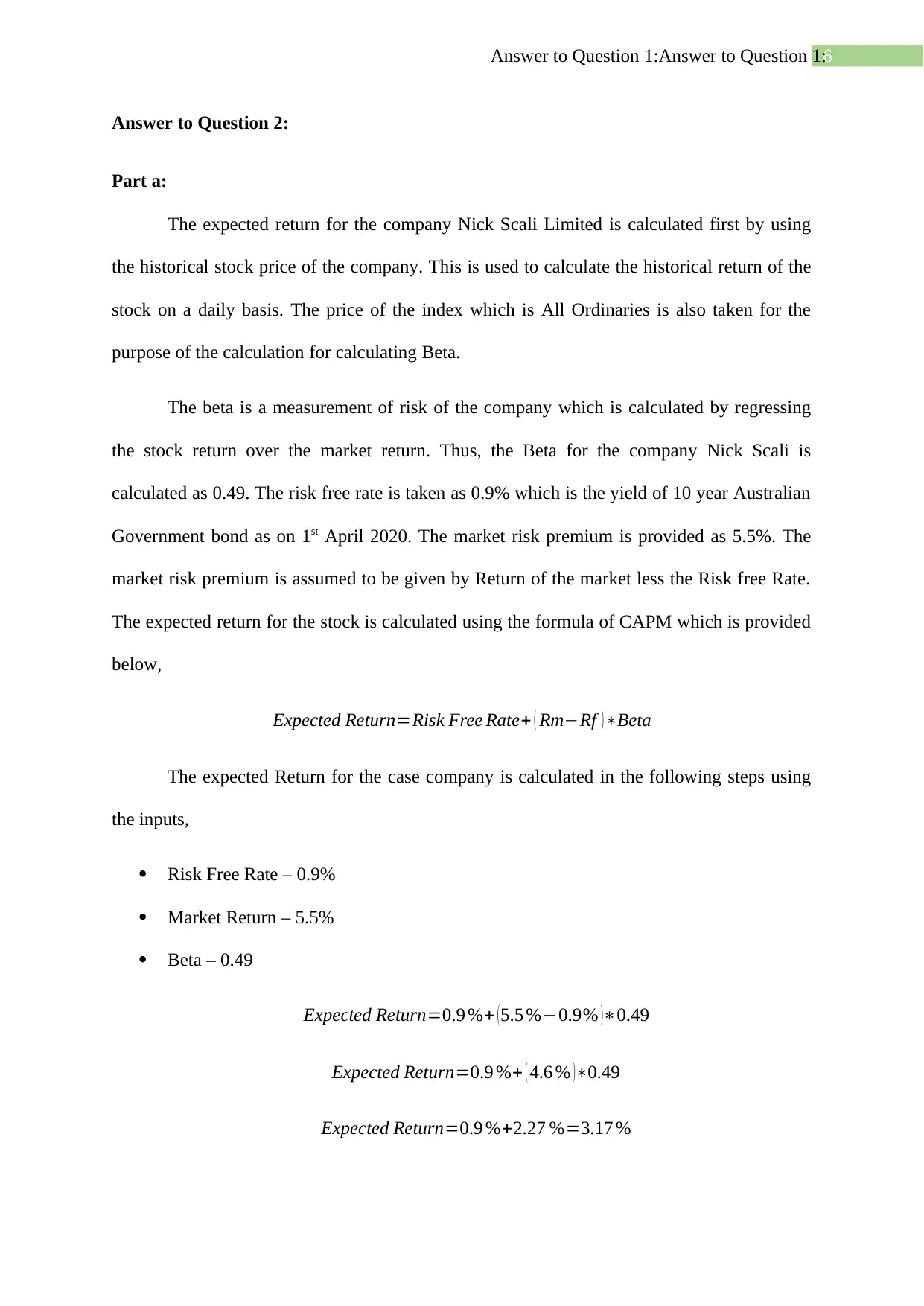

Part f:

The bond price for the bond is calculated using the excel PV function using the inputs

provided for the company. The price of the bond is calculated as $ 103.29 and the calculation

of the bond price is calculated in the figure below,

Figure 6: Price of the Bond

Source: By the Author

Part e:

The calculation of the YTM of a bond requires using the RATE function in excel

using the inputs required to calculate the YTM of the bond. The YTM of the bond is

calculated at 5.28% and the calculation is provided in the figure below,

Figure 5: Calculation of YTM

Source: By the Author

Part f:

The bond price for the bond is calculated using the excel PV function using the inputs

provided for the company. The price of the bond is calculated as $ 103.29 and the calculation

of the bond price is calculated in the figure below,

Figure 6: Price of the Bond

Source: By the Author

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6Answer to Question 1:Answer to Question 1:

Answer to Question 2:

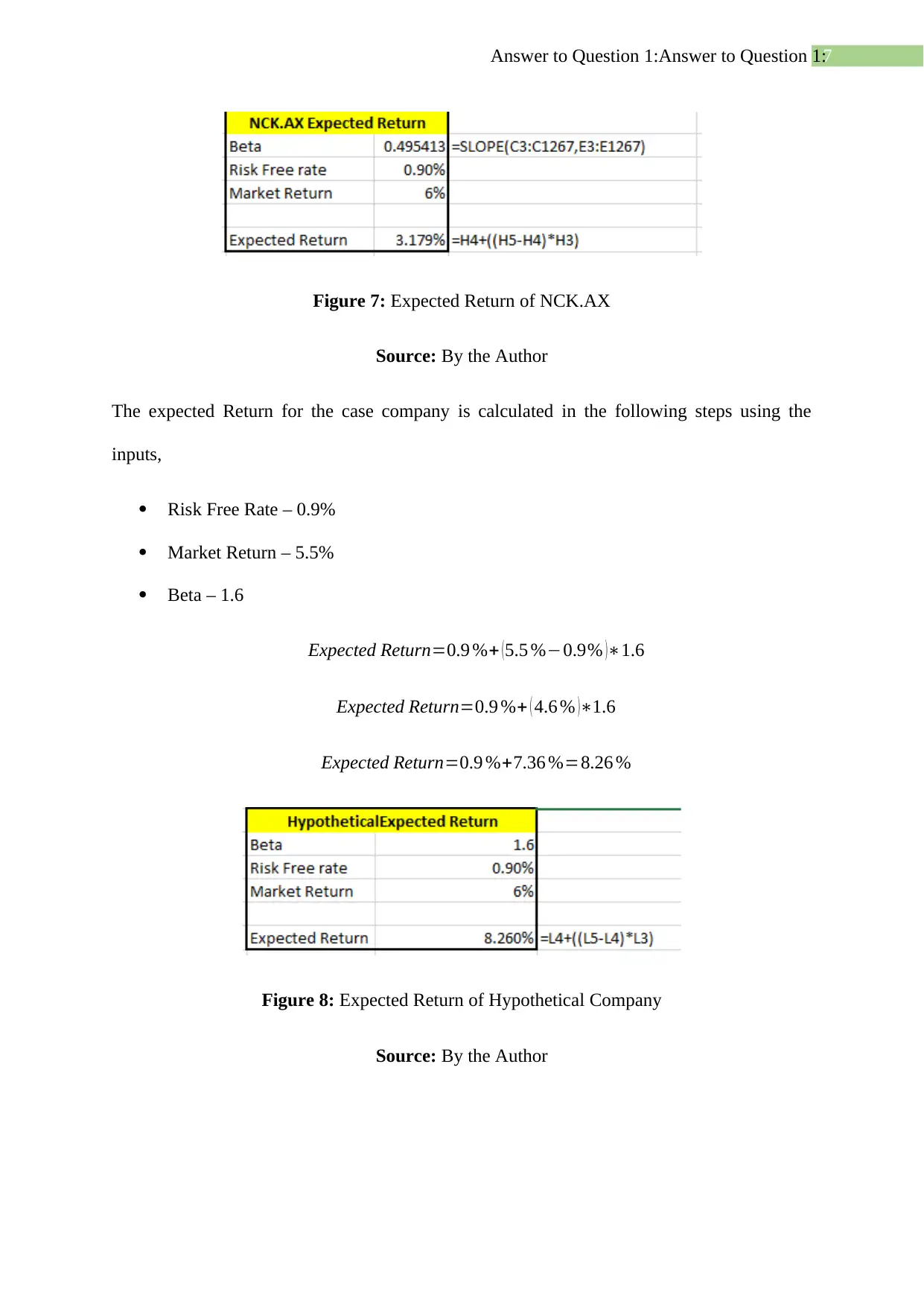

Part a:

The expected return for the company Nick Scali Limited is calculated first by using

the historical stock price of the company. This is used to calculate the historical return of the

stock on a daily basis. The price of the index which is All Ordinaries is also taken for the

purpose of the calculation for calculating Beta.

The beta is a measurement of risk of the company which is calculated by regressing

the stock return over the market return. Thus, the Beta for the company Nick Scali is

calculated as 0.49. The risk free rate is taken as 0.9% which is the yield of 10 year Australian

Government bond as on 1st April 2020. The market risk premium is provided as 5.5%. The

market risk premium is assumed to be given by Return of the market less the Risk free Rate.

The expected return for the stock is calculated using the formula of CAPM which is provided

below,

Expected Return=Risk Free Rate+ ( Rm−Rf )∗Beta

The expected Return for the case company is calculated in the following steps using

the inputs,

Risk Free Rate – 0.9%

Market Return – 5.5%

Beta – 0.49

Expected Return=0.9 %+ ( 5.5 %−0.9% )∗0.49

Expected Return=0.9 %+ ( 4.6 % )∗0.49

Expected Return=0.9 %+2.27 %=3.17 %

Answer to Question 2:

Part a:

The expected return for the company Nick Scali Limited is calculated first by using

the historical stock price of the company. This is used to calculate the historical return of the

stock on a daily basis. The price of the index which is All Ordinaries is also taken for the

purpose of the calculation for calculating Beta.

The beta is a measurement of risk of the company which is calculated by regressing

the stock return over the market return. Thus, the Beta for the company Nick Scali is

calculated as 0.49. The risk free rate is taken as 0.9% which is the yield of 10 year Australian

Government bond as on 1st April 2020. The market risk premium is provided as 5.5%. The

market risk premium is assumed to be given by Return of the market less the Risk free Rate.

The expected return for the stock is calculated using the formula of CAPM which is provided

below,

Expected Return=Risk Free Rate+ ( Rm−Rf )∗Beta

The expected Return for the case company is calculated in the following steps using

the inputs,

Risk Free Rate – 0.9%

Market Return – 5.5%

Beta – 0.49

Expected Return=0.9 %+ ( 5.5 %−0.9% )∗0.49

Expected Return=0.9 %+ ( 4.6 % )∗0.49

Expected Return=0.9 %+2.27 %=3.17 %

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7Answer to Question 1:Answer to Question 1:

Figure 7: Expected Return of NCK.AX

Source: By the Author

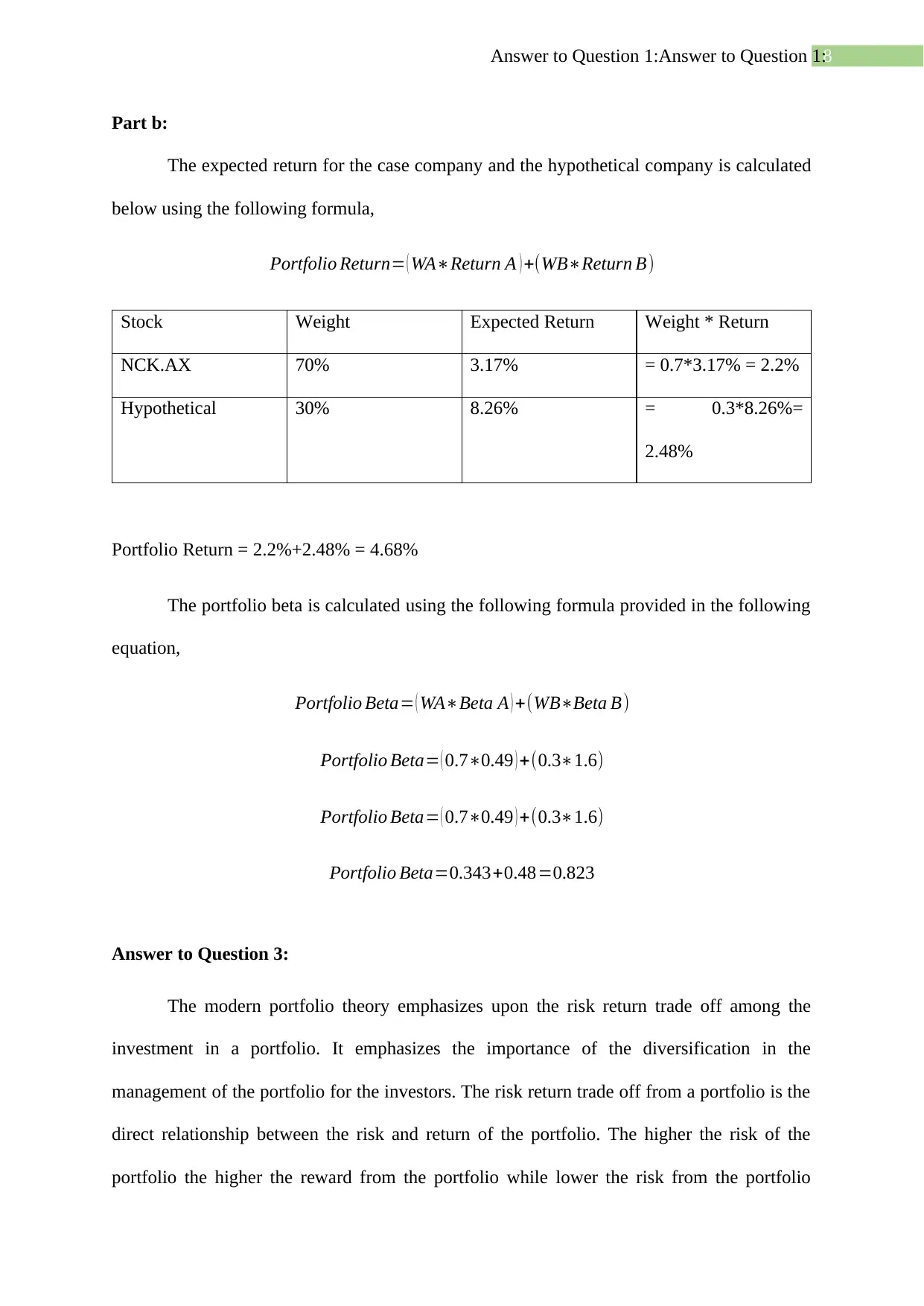

The expected Return for the case company is calculated in the following steps using the

inputs,

Risk Free Rate – 0.9%

Market Return – 5.5%

Beta – 1.6

Expected Return=0.9 %+ (5.5 %−0.9% )∗1.6

Expected Return=0.9 %+ ( 4.6 % )∗1.6

Expected Return=0.9 %+7.36 %=8.26 %

Figure 8: Expected Return of Hypothetical Company

Source: By the Author

Figure 7: Expected Return of NCK.AX

Source: By the Author

The expected Return for the case company is calculated in the following steps using the

inputs,

Risk Free Rate – 0.9%

Market Return – 5.5%

Beta – 1.6

Expected Return=0.9 %+ (5.5 %−0.9% )∗1.6

Expected Return=0.9 %+ ( 4.6 % )∗1.6

Expected Return=0.9 %+7.36 %=8.26 %

Figure 8: Expected Return of Hypothetical Company

Source: By the Author

8Answer to Question 1:Answer to Question 1:

Part b:

The expected return for the case company and the hypothetical company is calculated

below using the following formula,

Portfolio Return= ( WA∗Return A ) +(WB∗Return B)

Stock Weight Expected Return Weight * Return

NCK.AX 70% 3.17% = 0.7*3.17% = 2.2%

Hypothetical 30% 8.26% = 0.3*8.26%=

2.48%

Portfolio Return = 2.2%+2.48% = 4.68%

The portfolio beta is calculated using the following formula provided in the following

equation,

Portfolio Beta= ( WA∗Beta A ) +(WB∗Beta B)

Portfolio Beta= ( 0.7∗0.49 ) +(0.3∗1.6)

Portfolio Beta= ( 0.7∗0.49 ) +(0.3∗1.6)

Portfolio Beta=0.343+0.48=0.823

Answer to Question 3:

The modern portfolio theory emphasizes upon the risk return trade off among the

investment in a portfolio. It emphasizes the importance of the diversification in the

management of the portfolio for the investors. The risk return trade off from a portfolio is the

direct relationship between the risk and return of the portfolio. The higher the risk of the

portfolio the higher the reward from the portfolio while lower the risk from the portfolio

Part b:

The expected return for the case company and the hypothetical company is calculated

below using the following formula,

Portfolio Return= ( WA∗Return A ) +(WB∗Return B)

Stock Weight Expected Return Weight * Return

NCK.AX 70% 3.17% = 0.7*3.17% = 2.2%

Hypothetical 30% 8.26% = 0.3*8.26%=

2.48%

Portfolio Return = 2.2%+2.48% = 4.68%

The portfolio beta is calculated using the following formula provided in the following

equation,

Portfolio Beta= ( WA∗Beta A ) +(WB∗Beta B)

Portfolio Beta= ( 0.7∗0.49 ) +(0.3∗1.6)

Portfolio Beta= ( 0.7∗0.49 ) +(0.3∗1.6)

Portfolio Beta=0.343+0.48=0.823

Answer to Question 3:

The modern portfolio theory emphasizes upon the risk return trade off among the

investment in a portfolio. It emphasizes the importance of the diversification in the

management of the portfolio for the investors. The risk return trade off from a portfolio is the

direct relationship between the risk and return of the portfolio. The higher the risk of the

portfolio the higher the reward from the portfolio while lower the risk from the portfolio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9Answer to Question 1:Answer to Question 1:

lower the return. This can be understood by the empirical example between bonds and equity,

where bonds are considered relatively less risky than equity. Thus the return which is

required by the debt providers of the company is less than the equity providers since the debt

is covered by the assets of the company (Chandra 2017).

Thus, as per empirical theory between the risk return trade off, higher the risk higher

the return required by the investors. Here the importance of diversification benefit arises in

the portfolio, where the unsystematic risk from the portfolio is reduced while the investors

are rewarded for the systematic risk. The unsystematic risk implies the risk which is only

faced by a particular company and not the overall market, while systematic risk implies the

risk which affects the overall market. The investor can diversify the portfolio which means

reducing or eliminating the unsystematic risk from the portfolio (Antchak, Ziakas and Getz

2019).

The elimination of the unsystematic risk depends on the correlation between the asset

class and also upon the correlation among the investment in the asset class. The correlation

between the bond and the equity asset class is low which has been observed during the

market crashes. As when the market crashes the price of equity falls while debt rises which

implies a negative correlation among the asset class. Thus, when the economy is expected to

boom, the manager can increases the level of equity in a portfolio while reduce the level of

debt since equity performs well in economic boom generating higher return. Also when the

investments with in the asset class have lower correlation the benefits of diversification is

higher in the portfolio. This reduces the unsystematic risk or diversifiable risk from the

portfolio and the investor is awarded for the systematic risk.

Based on this knowledge the company Nick Scali which has a beta of 0.49 while an

expected return of 3.17% and the hypothetical company has beta of 1.6 and a return of

lower the return. This can be understood by the empirical example between bonds and equity,

where bonds are considered relatively less risky than equity. Thus the return which is

required by the debt providers of the company is less than the equity providers since the debt

is covered by the assets of the company (Chandra 2017).

Thus, as per empirical theory between the risk return trade off, higher the risk higher

the return required by the investors. Here the importance of diversification benefit arises in

the portfolio, where the unsystematic risk from the portfolio is reduced while the investors

are rewarded for the systematic risk. The unsystematic risk implies the risk which is only

faced by a particular company and not the overall market, while systematic risk implies the

risk which affects the overall market. The investor can diversify the portfolio which means

reducing or eliminating the unsystematic risk from the portfolio (Antchak, Ziakas and Getz

2019).

The elimination of the unsystematic risk depends on the correlation between the asset

class and also upon the correlation among the investment in the asset class. The correlation

between the bond and the equity asset class is low which has been observed during the

market crashes. As when the market crashes the price of equity falls while debt rises which

implies a negative correlation among the asset class. Thus, when the economy is expected to

boom, the manager can increases the level of equity in a portfolio while reduce the level of

debt since equity performs well in economic boom generating higher return. Also when the

investments with in the asset class have lower correlation the benefits of diversification is

higher in the portfolio. This reduces the unsystematic risk or diversifiable risk from the

portfolio and the investor is awarded for the systematic risk.

Based on this knowledge the company Nick Scali which has a beta of 0.49 while an

expected return of 3.17% and the hypothetical company has beta of 1.6 and a return of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10Answer to Question 1:Answer to Question 1:

8.26%. This highlights the direct relationship between risk return of the portfolio. The Beta of

the portfolio is 0.82 while the expected return is 4.7%. The investor has been able to increase

the risk of the investment along with the return as per the risk tolerance level. However, the

portfolio constructed cannot be defined as the optimal portfolio for the investor. The optimal

portfolio factors in the available various set of opportunity of the portfolio investment which

is available for the investor and constructs the portfolio which provides the highest level of

return for the least level of risk (Nawrocka 2018).

The optimal portfolio for investment is constructed using the Markowitz efficient

frontier curve, which is a curve consisting of various risk and return level for the portfolio.

The capital allocation line is also constructed using the market portfolio and the risk free rate

of investment. The optimal portfolio or the portfolio which maximizes the return while

reducing the risk is a tangent with the capital allocation line. This portfolio should be selected

by a rational investor as it reduces the unsystematic risk to the maximum level,

The Beta is a measure to analyse the risk of the investment as it measures the risk

with respect to the market portfolio. The market portfolio is assumed to be the diversified

portfolio which has a beta which is equal to 1. A beta measure less than 1 implies a less risky

investment and more than 1 implies high risk investment. The NCK.AX stock is a low risk

investment which provides a lower return which is increased when invested in the portfolio.

The hypothetical company is a high risk investment which is reduced in the portfolio. Thus

the correlation is one of the most important determinants which provides diversification to

the portfolio. Higher the correlation the lower the diversification benefit while lower the

correlation the higher the diversification benefit (Alford, Luchtenberg and Reddie 2018).

8.26%. This highlights the direct relationship between risk return of the portfolio. The Beta of

the portfolio is 0.82 while the expected return is 4.7%. The investor has been able to increase

the risk of the investment along with the return as per the risk tolerance level. However, the

portfolio constructed cannot be defined as the optimal portfolio for the investor. The optimal

portfolio factors in the available various set of opportunity of the portfolio investment which

is available for the investor and constructs the portfolio which provides the highest level of

return for the least level of risk (Nawrocka 2018).

The optimal portfolio for investment is constructed using the Markowitz efficient

frontier curve, which is a curve consisting of various risk and return level for the portfolio.

The capital allocation line is also constructed using the market portfolio and the risk free rate

of investment. The optimal portfolio or the portfolio which maximizes the return while

reducing the risk is a tangent with the capital allocation line. This portfolio should be selected

by a rational investor as it reduces the unsystematic risk to the maximum level,

The Beta is a measure to analyse the risk of the investment as it measures the risk

with respect to the market portfolio. The market portfolio is assumed to be the diversified

portfolio which has a beta which is equal to 1. A beta measure less than 1 implies a less risky

investment and more than 1 implies high risk investment. The NCK.AX stock is a low risk

investment which provides a lower return which is increased when invested in the portfolio.

The hypothetical company is a high risk investment which is reduced in the portfolio. Thus

the correlation is one of the most important determinants which provides diversification to

the portfolio. Higher the correlation the lower the diversification benefit while lower the

correlation the higher the diversification benefit (Alford, Luchtenberg and Reddie 2018).

11Answer to Question 1:Answer to Question 1:

References:

Alford, R.M., Luchtenberg, K.F. and Reddie, W.D., 2018. Portfolio Management and

Earnings Management: Evidence from Property and Casualty Insurers. Journal of

Accounting & Finance (2158-3625), 18(4).

Antchak, V., Ziakas, V. and Getz, D., 2019. Event portfolio management: theory and

methods for event management and tourism. Goodfellow.

Bloomberg - Are you a robot? (2020). Available at:

https://www.bloomberg.com/markets/rates-bonds/government-bonds/australia (Accessed: 13

April 2020).

Chakrabarty, R., Roy, T. and Chaudhuri, K.S., 2017. A production: inventory model for

defective items with shortages incorporating inflation and time value of money. International

Journal of Applied and Computational Mathematics, 3(1), pp.195-212.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-hill education.

Dong, J., Korobenko, L. and Deniz Sezer, A., 2020. A variation of Merton's corporate bond

valuation model for firms with illiquid but observable assets. Quantitative Finance, 20(3),

pp.483-497.

García-Schmidt, M. and Woodford, M., 2019. Are low interest rates deflationary? A paradox

of perfect-foresight analysis. American Economic Review, 109(1), pp.86-120.

Kahn, M.J. and Baum, N., 2020. Time Value of Money, or What Is the Real Financial Value

of an Opportunity?. In The Business Basics of Building and Managing a Healthcare

Practice (pp. 9-12). Springer, Cham.

References:

Alford, R.M., Luchtenberg, K.F. and Reddie, W.D., 2018. Portfolio Management and

Earnings Management: Evidence from Property and Casualty Insurers. Journal of

Accounting & Finance (2158-3625), 18(4).

Antchak, V., Ziakas, V. and Getz, D., 2019. Event portfolio management: theory and

methods for event management and tourism. Goodfellow.

Bloomberg - Are you a robot? (2020). Available at:

https://www.bloomberg.com/markets/rates-bonds/government-bonds/australia (Accessed: 13

April 2020).

Chakrabarty, R., Roy, T. and Chaudhuri, K.S., 2017. A production: inventory model for

defective items with shortages incorporating inflation and time value of money. International

Journal of Applied and Computational Mathematics, 3(1), pp.195-212.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-hill education.

Dong, J., Korobenko, L. and Deniz Sezer, A., 2020. A variation of Merton's corporate bond

valuation model for firms with illiquid but observable assets. Quantitative Finance, 20(3),

pp.483-497.

García-Schmidt, M. and Woodford, M., 2019. Are low interest rates deflationary? A paradox

of perfect-foresight analysis. American Economic Review, 109(1), pp.86-120.

Kahn, M.J. and Baum, N., 2020. Time Value of Money, or What Is the Real Financial Value

of an Opportunity?. In The Business Basics of Building and Managing a Healthcare

Practice (pp. 9-12). Springer, Cham.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.