MOD003319: Business Finance Report on Profit, Cash Flow, and WCM

VerifiedAdded on 2022/12/27

|13

|3181

|31

Report

AI Summary

This business finance report provides a detailed analysis of profit, cash flow, and working capital management (WCM). Task 1 defines profit, cash flow, working capital, and their interrelations, assessing how changes in working capital affect cash flows and their impact on financial results. It also suggests ways to improve cash flow using WCM practices for Trend Ltd. Task 2 presents a monthly cash budget for Thorne Estates Limited from January to April 2021, followed by an analysis and recommendations for effective cash management. The report covers key financial concepts, practical applications, and recommendations for enhancing financial performance, including strategies for improving liquidity and managing risks. The analysis includes a cash budget and recommendations for effective cash management for the company.

BUSINESS REPORT FOR

MANAGER

MANAGER

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................1

TASK1.............................................................................................................................................2

a. Stating the meaning of profit and cash-flows with differences................................................2

(b) Defining working capital and its elements.............................................................................2

c. Assessing how working capital changes affect cash-flows .....................................................3

(ii) Assessing the impact of company’s working capital management on financial results........4

(iii) Analysing ways through which cash flow can be improved using WCM practices ............4

EXECUTIVE SUMMARY.............................................................................................................6

TASK 2............................................................................................................................................7

Monthly Cash Budge for four months from 1st January to 30th April 2021. .............................7

Analysing and recommending ways for effective management..................................................8

REFERENCES..............................................................................................................................11

EXECUTIVE SUMMARY.............................................................................................................1

TASK1.............................................................................................................................................2

a. Stating the meaning of profit and cash-flows with differences................................................2

(b) Defining working capital and its elements.............................................................................2

c. Assessing how working capital changes affect cash-flows .....................................................3

(ii) Assessing the impact of company’s working capital management on financial results........4

(iii) Analysing ways through which cash flow can be improved using WCM practices ............4

EXECUTIVE SUMMARY.............................................................................................................6

TASK 2............................................................................................................................................7

Monthly Cash Budge for four months from 1st January to 30th April 2021. .............................7

Analysing and recommending ways for effective management..................................................8

REFERENCES..............................................................................................................................11

EXECUTIVE SUMMARY

In Task 1, the key terms in respect to the accounting and finance is evaluated for getting a

basic understanding about the topic. It states about the impact of change in working capital of the

company on its cash flow and recommending ways for improving the working capital

management of Trend Ltd.

1

In Task 1, the key terms in respect to the accounting and finance is evaluated for getting a

basic understanding about the topic. It states about the impact of change in working capital of the

company on its cash flow and recommending ways for improving the working capital

management of Trend Ltd.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK1

a. Stating the meaning of profit and cash-flows with differences

Profit

Profit is financial benefits obtain from business or trade activities after deducting cost

incurred for it. It is the extra amount which is received on investment which classified as gross,

operating, and net profit. In order to find out profit there is a statement called profit and loss

statement. Which helps in the preparation of balance sheet, fund flow and cash flow statement.

Cash-flow

Cash-flow is a statement which shows all in and out flow of cash for associated with

business activities. There are three type of activities included in cash-flow such as operating,

financing and investing activities. For preparation of cash flow there is need of profit and loss

statement and other financial details likes balance sheet, record of purchase and sale of long term

assets etc.

Difference between profit and cash flow

Basis of difference Profit cash-flows

Usability Profit is useful for any company

but in long term purpose term. So

for year to year is more useful for

investors prospective. More profit

attract more investor.

Cash-flows is more useful for top

management for future goal setting

and decision-making.

Accountability For profit, income statement is to

be prepared which in turn

mandatory for all companies

(Soboleva and et.al., 2018).

Cash-flows is find out from cash

flow statement which is not

mandatory for all companies.

Dependability Calculation of profit is depended

on the ledgers trading accounts.

Cash-flows is prepared with the

help of financial statement.

(b) Defining working capital and its elements

Working capital-

It indicates ability to pay short debt or current liabilities, working capital define liquidity

level what are the sources to pay the short term liabilities that incurred in production activities.

Working capital= current assets-current liabilities.

Receivable-

2

a. Stating the meaning of profit and cash-flows with differences

Profit

Profit is financial benefits obtain from business or trade activities after deducting cost

incurred for it. It is the extra amount which is received on investment which classified as gross,

operating, and net profit. In order to find out profit there is a statement called profit and loss

statement. Which helps in the preparation of balance sheet, fund flow and cash flow statement.

Cash-flow

Cash-flow is a statement which shows all in and out flow of cash for associated with

business activities. There are three type of activities included in cash-flow such as operating,

financing and investing activities. For preparation of cash flow there is need of profit and loss

statement and other financial details likes balance sheet, record of purchase and sale of long term

assets etc.

Difference between profit and cash flow

Basis of difference Profit cash-flows

Usability Profit is useful for any company

but in long term purpose term. So

for year to year is more useful for

investors prospective. More profit

attract more investor.

Cash-flows is more useful for top

management for future goal setting

and decision-making.

Accountability For profit, income statement is to

be prepared which in turn

mandatory for all companies

(Soboleva and et.al., 2018).

Cash-flows is find out from cash

flow statement which is not

mandatory for all companies.

Dependability Calculation of profit is depended

on the ledgers trading accounts.

Cash-flows is prepared with the

help of financial statement.

(b) Defining working capital and its elements

Working capital-

It indicates ability to pay short debt or current liabilities, working capital define liquidity

level what are the sources to pay the short term liabilities that incurred in production activities.

Working capital= current assets-current liabilities.

Receivable-

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Receivable are debtors of organization, Organization has provided stock or some assets

on credit and write as receivables in balance sheet because money will be received is future

dates. In reference to working capital it will more important because greater level of receivable

lead delay in payment impact working capital.

Inventory-

Inventory is term used for all the stock that incudes raw material, finished goods, work in

progress etc. It is useful when finding cost of goods sold and cost of production. Inventory

become more useful when it comes to working capital because as many as inventory is hold by

organization delays working cycle cannot convert into cash easily (Margasova and et.al., 2019).

Payables-

Payables are part of current liabilities that means company has obtained material,

overheads and some services at on credit for that company need to pay in future so it called as

payables because company need to pay amount for that. Company can make more payable to

make delay in payments.

c. Assessing how working capital changes affect cash-flows

Impact of working capital on cash flow-

To find out net cash flow of the organization, one should closely monitor working capital

moreover much part of cash flow is related with current assets and current liabilities. Which not

directly impact cash flow but impact indirectly. Company's much part of working capital is

relevant to cash activities like in and out of cash as the production activities take place.

For instance: If organization sells its fixed assets than the inflow of cash which increase

in cash and working capital will also go up and similarly if fixed assets is purchase, then it will

increase the value working capital and cash outflow.

Another example is purchase of inventory that not directly impact but it will lead to reduce the

cash so it has indirect impact.

it is understandable that cash flow not included the working capital part because it is related to

short term period that are not directly included cash(Roychaudhuri and et.al.,2017). Working

capital is the most impacted part of cash so it should give due consideration to working capital.

3

on credit and write as receivables in balance sheet because money will be received is future

dates. In reference to working capital it will more important because greater level of receivable

lead delay in payment impact working capital.

Inventory-

Inventory is term used for all the stock that incudes raw material, finished goods, work in

progress etc. It is useful when finding cost of goods sold and cost of production. Inventory

become more useful when it comes to working capital because as many as inventory is hold by

organization delays working cycle cannot convert into cash easily (Margasova and et.al., 2019).

Payables-

Payables are part of current liabilities that means company has obtained material,

overheads and some services at on credit for that company need to pay in future so it called as

payables because company need to pay amount for that. Company can make more payable to

make delay in payments.

c. Assessing how working capital changes affect cash-flows

Impact of working capital on cash flow-

To find out net cash flow of the organization, one should closely monitor working capital

moreover much part of cash flow is related with current assets and current liabilities. Which not

directly impact cash flow but impact indirectly. Company's much part of working capital is

relevant to cash activities like in and out of cash as the production activities take place.

For instance: If organization sells its fixed assets than the inflow of cash which increase

in cash and working capital will also go up and similarly if fixed assets is purchase, then it will

increase the value working capital and cash outflow.

Another example is purchase of inventory that not directly impact but it will lead to reduce the

cash so it has indirect impact.

it is understandable that cash flow not included the working capital part because it is related to

short term period that are not directly included cash(Roychaudhuri and et.al.,2017). Working

capital is the most impacted part of cash so it should give due consideration to working capital.

3

(ii) Assessing the impact of company’s working capital management on financial results

Organization is working in field of cloths where the production activities became more

important. So the value of working capital will be most, and value of cash-flows are to be high.

Organization should manage these activities with due respect because in industries like textiles

and manufacturing cash and working cycle became more essentials. So the organization is

receiving investment TL company can be used for the purpose of improving working capital.

Step can be taken for improvement of cash-flows and working capital-

Reduction in period of receivable-

Company can opt a policy where reduction in the period of receivable can be made to

make more useful and convincing for the payment to supplier.

Increase in period of payable-

It is another tool to increase the level to working capital to can make working cycle easy

for the organization. It provides more liquidity for production and settlement of short term

expenses.

Increase in investment-

TL company has made investment to acquired 30% stake in the organization, lead to

increase the cash amount so excessive amount can be further invested to increase movement of

cash.

Increase in the profit-

From the money received from investment can used for working capital and reinvested to

get more profitability.

If company uses the fund in working capital and for re-investment purpose it will be

better utilization of fund (Aquila and et.al., 2017). It helps in the increases of financial efficiency

and results.

(iii) Analysing ways through which cash flow can be improved using WCM practices

working capital management can be used to get more efficient cash-flows management and

improvement of cash circulation in and out of organization.

Improvement in liquidity-

with the help of increase in volume of working capital, in decrease in the period of

receivable and inverse with payable organization can find more liquidity. It can be used in many

ways to payment of short term loan and liabilities, So the management of cash will also improve.

4

Organization is working in field of cloths where the production activities became more

important. So the value of working capital will be most, and value of cash-flows are to be high.

Organization should manage these activities with due respect because in industries like textiles

and manufacturing cash and working cycle became more essentials. So the organization is

receiving investment TL company can be used for the purpose of improving working capital.

Step can be taken for improvement of cash-flows and working capital-

Reduction in period of receivable-

Company can opt a policy where reduction in the period of receivable can be made to

make more useful and convincing for the payment to supplier.

Increase in period of payable-

It is another tool to increase the level to working capital to can make working cycle easy

for the organization. It provides more liquidity for production and settlement of short term

expenses.

Increase in investment-

TL company has made investment to acquired 30% stake in the organization, lead to

increase the cash amount so excessive amount can be further invested to increase movement of

cash.

Increase in the profit-

From the money received from investment can used for working capital and reinvested to

get more profitability.

If company uses the fund in working capital and for re-investment purpose it will be

better utilization of fund (Aquila and et.al., 2017). It helps in the increases of financial efficiency

and results.

(iii) Analysing ways through which cash flow can be improved using WCM practices

working capital management can be used to get more efficient cash-flows management and

improvement of cash circulation in and out of organization.

Improvement in liquidity-

with the help of increase in volume of working capital, in decrease in the period of

receivable and inverse with payable organization can find more liquidity. It can be used in many

ways to payment of short term loan and liabilities, So the management of cash will also improve.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysing risk and its segmentation -

There are many risks associated with the market that lead to decrease in the efficiency of

working capital. In working capital, the risk which effect most is credit risk due to this many

times payment cannot be received at time and liquidity reduces.

So in accordance with the risk payable can be segmented and better result can be opt. By these

cash cycle will not frequently affect.

Improvement in accounts receivable and payable-

To obtain the better cash cycle organization can make control over all debtors and

creditors. Organization can have classified these in small group and give the rating according to

their behaviour in payment history to allocated group to improvement in future payment and

accountability. It leads to the improvement in management of cash-flows.

Segment for controllable and uncontrollable expenses-

From making segment of cost or expenses organization can control expenses needs to be

control It helps in reduction of cost and wastage (Foerster, Tsagarelis and Wang, 2017). And

the uncontrollable cost can be estimated for the future projects.

Control over working capital-

If all the segment is made, then the control be an easy job for the management and help in

deciding about use of excessive money that is not useable for that period.

5

There are many risks associated with the market that lead to decrease in the efficiency of

working capital. In working capital, the risk which effect most is credit risk due to this many

times payment cannot be received at time and liquidity reduces.

So in accordance with the risk payable can be segmented and better result can be opt. By these

cash cycle will not frequently affect.

Improvement in accounts receivable and payable-

To obtain the better cash cycle organization can make control over all debtors and

creditors. Organization can have classified these in small group and give the rating according to

their behaviour in payment history to allocated group to improvement in future payment and

accountability. It leads to the improvement in management of cash-flows.

Segment for controllable and uncontrollable expenses-

From making segment of cost or expenses organization can control expenses needs to be

control It helps in reduction of cost and wastage (Foerster, Tsagarelis and Wang, 2017). And

the uncontrollable cost can be estimated for the future projects.

Control over working capital-

If all the segment is made, then the control be an easy job for the management and help in

deciding about use of excessive money that is not useable for that period.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

In second part of report, forecasted cash budget for the 4 months is being prepared based

on the information given. After creation of budget, the analysis of the same is carried out upon

which the point of suggestion and recommendation is being provided to the Thorne Estates

Limited for effective management of the cash of the company.

6

In second part of report, forecasted cash budget for the 4 months is being prepared based

on the information given. After creation of budget, the analysis of the same is carried out upon

which the point of suggestion and recommendation is being provided to the Thorne Estates

Limited for effective management of the cash of the company.

6

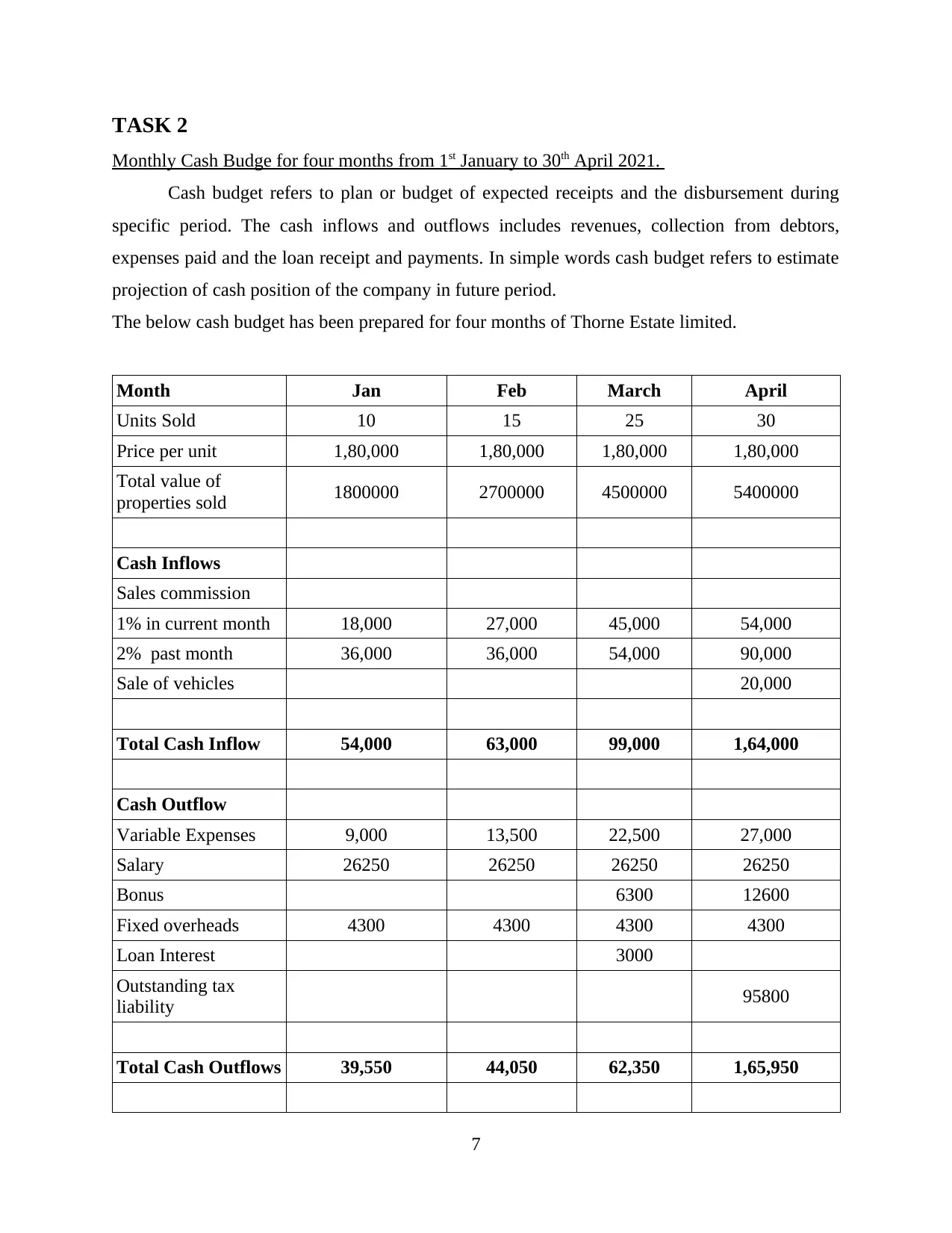

TASK 2

Monthly Cash Budge for four months from 1st January to 30th April 2021.

Cash budget refers to plan or budget of expected receipts and the disbursement during

specific period. The cash inflows and outflows includes revenues, collection from debtors,

expenses paid and the loan receipt and payments. In simple words cash budget refers to estimate

projection of cash position of the company in future period.

The below cash budget has been prepared for four months of Thorne Estate limited.

Month Jan Feb March April

Units Sold 10 15 25 30

Price per unit 1,80,000 1,80,000 1,80,000 1,80,000

Total value of

properties sold 1800000 2700000 4500000 5400000

Cash Inflows

Sales commission

1% in current month 18,000 27,000 45,000 54,000

2% past month 36,000 36,000 54,000 90,000

Sale of vehicles 20,000

Total Cash Inflow 54,000 63,000 99,000 1,64,000

Cash Outflow

Variable Expenses 9,000 13,500 22,500 27,000

Salary 26250 26250 26250 26250

Bonus 6300 12600

Fixed overheads 4300 4300 4300 4300

Loan Interest 3000

Outstanding tax

liability 95800

Total Cash Outflows 39,550 44,050 62,350 1,65,950

7

Monthly Cash Budge for four months from 1st January to 30th April 2021.

Cash budget refers to plan or budget of expected receipts and the disbursement during

specific period. The cash inflows and outflows includes revenues, collection from debtors,

expenses paid and the loan receipt and payments. In simple words cash budget refers to estimate

projection of cash position of the company in future period.

The below cash budget has been prepared for four months of Thorne Estate limited.

Month Jan Feb March April

Units Sold 10 15 25 30

Price per unit 1,80,000 1,80,000 1,80,000 1,80,000

Total value of

properties sold 1800000 2700000 4500000 5400000

Cash Inflows

Sales commission

1% in current month 18,000 27,000 45,000 54,000

2% past month 36,000 36,000 54,000 90,000

Sale of vehicles 20,000

Total Cash Inflow 54,000 63,000 99,000 1,64,000

Cash Outflow

Variable Expenses 9,000 13,500 22,500 27,000

Salary 26250 26250 26250 26250

Bonus 6300 12600

Fixed overheads 4300 4300 4300 4300

Loan Interest 3000

Outstanding tax

liability 95800

Total Cash Outflows 39,550 44,050 62,350 1,65,950

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

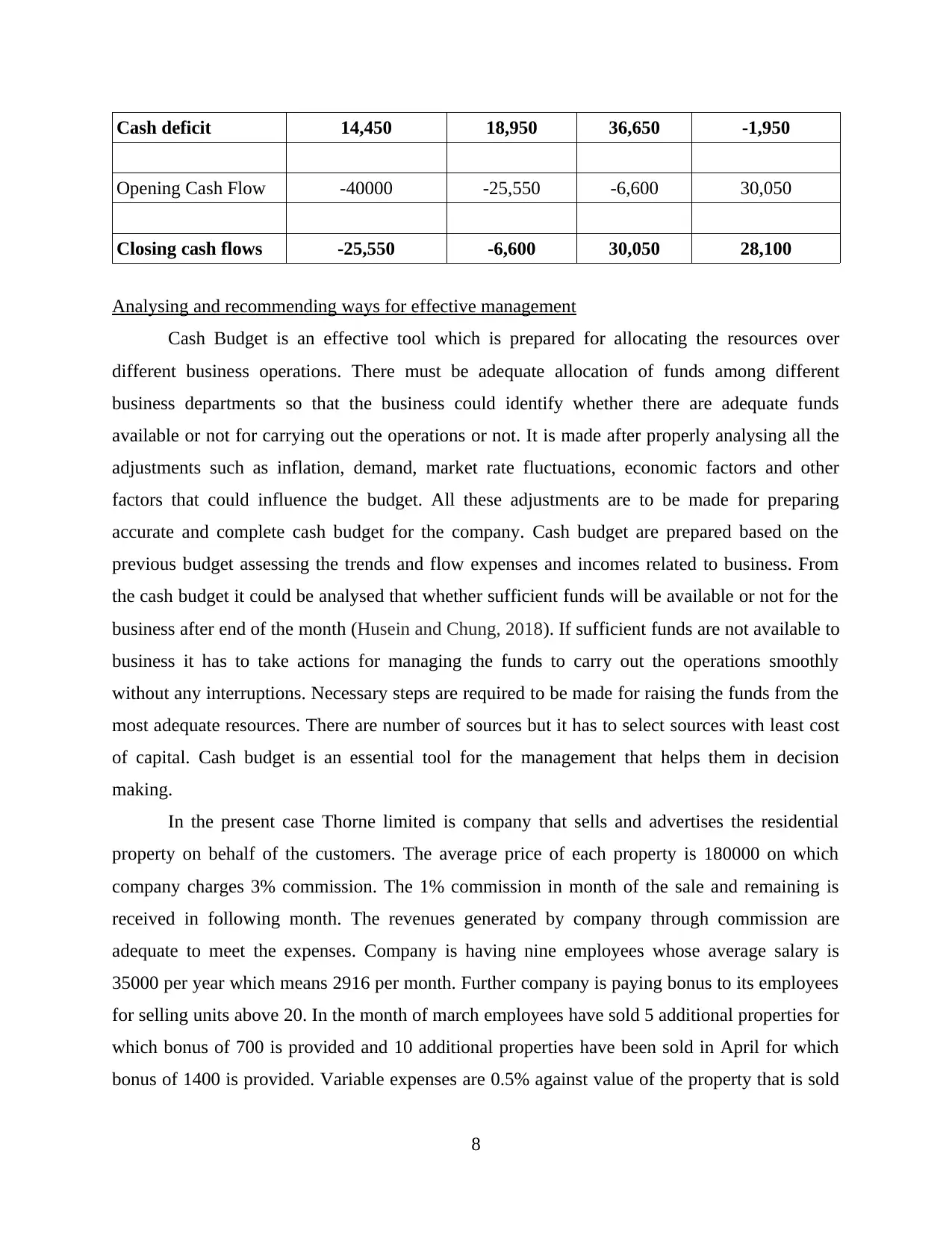

Cash deficit 14,450 18,950 36,650 -1,950

Opening Cash Flow -40000 -25,550 -6,600 30,050

Closing cash flows -25,550 -6,600 30,050 28,100

Analysing and recommending ways for effective management

Cash Budget is an effective tool which is prepared for allocating the resources over

different business operations. There must be adequate allocation of funds among different

business departments so that the business could identify whether there are adequate funds

available or not for carrying out the operations or not. It is made after properly analysing all the

adjustments such as inflation, demand, market rate fluctuations, economic factors and other

factors that could influence the budget. All these adjustments are to be made for preparing

accurate and complete cash budget for the company. Cash budget are prepared based on the

previous budget assessing the trends and flow expenses and incomes related to business. From

the cash budget it could be analysed that whether sufficient funds will be available or not for the

business after end of the month (Husein and Chung, 2018). If sufficient funds are not available to

business it has to take actions for managing the funds to carry out the operations smoothly

without any interruptions. Necessary steps are required to be made for raising the funds from the

most adequate resources. There are number of sources but it has to select sources with least cost

of capital. Cash budget is an essential tool for the management that helps them in decision

making.

In the present case Thorne limited is company that sells and advertises the residential

property on behalf of the customers. The average price of each property is 180000 on which

company charges 3% commission. The 1% commission in month of the sale and remaining is

received in following month. The revenues generated by company through commission are

adequate to meet the expenses. Company is having nine employees whose average salary is

35000 per year which means 2916 per month. Further company is paying bonus to its employees

for selling units above 20. In the month of march employees have sold 5 additional properties for

which bonus of 700 is provided and 10 additional properties have been sold in April for which

bonus of 1400 is provided. Variable expenses are 0.5% against value of the property that is sold

8

Opening Cash Flow -40000 -25,550 -6,600 30,050

Closing cash flows -25,550 -6,600 30,050 28,100

Analysing and recommending ways for effective management

Cash Budget is an effective tool which is prepared for allocating the resources over

different business operations. There must be adequate allocation of funds among different

business departments so that the business could identify whether there are adequate funds

available or not for carrying out the operations or not. It is made after properly analysing all the

adjustments such as inflation, demand, market rate fluctuations, economic factors and other

factors that could influence the budget. All these adjustments are to be made for preparing

accurate and complete cash budget for the company. Cash budget are prepared based on the

previous budget assessing the trends and flow expenses and incomes related to business. From

the cash budget it could be analysed that whether sufficient funds will be available or not for the

business after end of the month (Husein and Chung, 2018). If sufficient funds are not available to

business it has to take actions for managing the funds to carry out the operations smoothly

without any interruptions. Necessary steps are required to be made for raising the funds from the

most adequate resources. There are number of sources but it has to select sources with least cost

of capital. Cash budget is an essential tool for the management that helps them in decision

making.

In the present case Thorne limited is company that sells and advertises the residential

property on behalf of the customers. The average price of each property is 180000 on which

company charges 3% commission. The 1% commission in month of the sale and remaining is

received in following month. The revenues generated by company through commission are

adequate to meet the expenses. Company is having nine employees whose average salary is

35000 per year which means 2916 per month. Further company is paying bonus to its employees

for selling units above 20. In the month of march employees have sold 5 additional properties for

which bonus of 700 is provided and 10 additional properties have been sold in April for which

bonus of 1400 is provided. Variable expenses are 0.5% against value of the property that is sold

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and they have to be paid in same month. These expenses will increase with increase in properties

sold and vice versa. It means company is required to keep proper control over these expenses so

that there is no further increase in expenses. The fixed overheads are 4300 per month that will be

paid in every month in which they occur (Aithal 2017). These are related to the expenditures

which are related to power, rental and hire charges which are constant irrespective of amount of

output. Company is also required to account for the interest expenses in making of cash budget

as it is financial obligation which has to be paid every year at scheduled time. The rent of office

amount at 42000 for the year therefore it will be counted as prepaid rent in the budget and cash

will be taken for rent every year. The rent is to be paid once in year by the company in may.

There is outstanding tax liability for the company which will be paid in April. The tax liability is

charged on business profits amounting to 95800. It will paid in single one time payment by the

company. The amount of tax liability is high and have significant impact on cash flows as it has

to take out one time payment of considerable amount.

Thorne has planned to dispose surplus vehicles that are having book value. Sales

proceeds will be accounted as cash inflows in month of April. The proceeds could be used for

any business purpose as per the policies of company. The vehicles are sold for 20000 on which it

is earning a cash profit of 5000. The profit is received in monetary terms therefore accounted in

cash budget of company. Company had a opening cash balance with deficit of 40000 that is

negative cash balance of 40000. company is running out of cash for which it is required to take

necessary steps so that it could convert the negative balance into positive balance. Company is

required to maintain strong monitoring over the costs and expenses of the business to maintain

the cash flows (Margasova and et.al., 2019). It is essential for the business to maintain proper

inflow and cash outflows for smooth functioning of operations.

Company can negotiate with the officer owner to reduce the rent so that it would reduce

the rent cost. The payment of interest could be broken down into months so that burden is not

laid on one month of whole quarter. It could be analysed from the above budget that company is

not having adequate cash flows throughout the year.

The company's cash flow are fluctuating which makes it important for the company to

make an investment into short term and long terms investment option in order to generate higher

return in the future. By implementing systematic strategy and management plans it will help in

effectively meeting up with the future cash requirements such for expansion. And in addition, the

9

sold and vice versa. It means company is required to keep proper control over these expenses so

that there is no further increase in expenses. The fixed overheads are 4300 per month that will be

paid in every month in which they occur (Aithal 2017). These are related to the expenditures

which are related to power, rental and hire charges which are constant irrespective of amount of

output. Company is also required to account for the interest expenses in making of cash budget

as it is financial obligation which has to be paid every year at scheduled time. The rent of office

amount at 42000 for the year therefore it will be counted as prepaid rent in the budget and cash

will be taken for rent every year. The rent is to be paid once in year by the company in may.

There is outstanding tax liability for the company which will be paid in April. The tax liability is

charged on business profits amounting to 95800. It will paid in single one time payment by the

company. The amount of tax liability is high and have significant impact on cash flows as it has

to take out one time payment of considerable amount.

Thorne has planned to dispose surplus vehicles that are having book value. Sales

proceeds will be accounted as cash inflows in month of April. The proceeds could be used for

any business purpose as per the policies of company. The vehicles are sold for 20000 on which it

is earning a cash profit of 5000. The profit is received in monetary terms therefore accounted in

cash budget of company. Company had a opening cash balance with deficit of 40000 that is

negative cash balance of 40000. company is running out of cash for which it is required to take

necessary steps so that it could convert the negative balance into positive balance. Company is

required to maintain strong monitoring over the costs and expenses of the business to maintain

the cash flows (Margasova and et.al., 2019). It is essential for the business to maintain proper

inflow and cash outflows for smooth functioning of operations.

Company can negotiate with the officer owner to reduce the rent so that it would reduce

the rent cost. The payment of interest could be broken down into months so that burden is not

laid on one month of whole quarter. It could be analysed from the above budget that company is

not having adequate cash flows throughout the year.

The company's cash flow are fluctuating which makes it important for the company to

make an investment into short term and long terms investment option in order to generate higher

return in the future. By implementing systematic strategy and management plans it will help in

effectively meeting up with the future cash requirements such for expansion. And in addition, the

9

organization would not be required to take additional funds in terms of loan or bank overdraft

(Nørreklit, Mitchell and Nielsen, 2017). Also, it is crucial for the company to take into

consideration various aspects such as the size of the excess amount of cash, the time frame for

which it is made available along with the level of risk being associated with different types of

investment instruments. Thorne Estates is required to understand that the investment of the

surplus cash balance is a component of the treasury function and as the size of the company is

not that large, therefore, it can definitely put a close eye on the management of the cash

surpluses.

In addition to this, the negative opening cash balance is expected to be because of the

usage of the overdraft facilities by the company amounting to 40000 in which interest is charged

pertaining to the amount which is overdrawn. But it is highly recommended to the management

to understand the positive and negative implication of bank overdraft on the business. On

positive side, it is very flexible and interest is charged only on the overdrawn amount in contrast

to it, it involves the risk of interest rate which might rise as it is variable. Along with that,

overdraft amount can be called out or repayable at any time on demand. Thus, these are the

certain point of recommendation which the organization if follows will result into effectively and

properly management of the cash flow of the Thorne Estates.

10

(Nørreklit, Mitchell and Nielsen, 2017). Also, it is crucial for the company to take into

consideration various aspects such as the size of the excess amount of cash, the time frame for

which it is made available along with the level of risk being associated with different types of

investment instruments. Thorne Estates is required to understand that the investment of the

surplus cash balance is a component of the treasury function and as the size of the company is

not that large, therefore, it can definitely put a close eye on the management of the cash

surpluses.

In addition to this, the negative opening cash balance is expected to be because of the

usage of the overdraft facilities by the company amounting to 40000 in which interest is charged

pertaining to the amount which is overdrawn. But it is highly recommended to the management

to understand the positive and negative implication of bank overdraft on the business. On

positive side, it is very flexible and interest is charged only on the overdrawn amount in contrast

to it, it involves the risk of interest rate which might rise as it is variable. Along with that,

overdraft amount can be called out or repayable at any time on demand. Thus, these are the

certain point of recommendation which the organization if follows will result into effectively and

properly management of the cash flow of the Thorne Estates.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.