MOD003319 Business Finance: Cash Budget, Profit, Expenditure Analysis

VerifiedAdded on 2023/06/08

|9

|2919

|353

Report

AI Summary

This report provides a comprehensive analysis of business finance, focusing on cash budgeting for Surya Trading, distinguishing between cash and profits, and differentiating between capital and revenue expenditure, expenses and drawings, gross and net profit, cash budget and cash flow statement, and accruals and prepayments. Key financial terms such as assets, liabilities, ordinary shares, preference shares, dividends, stock exchange, venture capital, and budgets are also defined. The report uses a case study approach to illustrate practical applications of financial concepts. Desklib provides students access to a variety of resources including solved assignments and past papers.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1.1.........................................................................................................................................3

Construct cash budget for Surya Trading for the period ending on 31 December, 2022.......3

TASK 2.1.........................................................................................................................................4

A. In your view, are cash and profits same? Suggest any business transactions that do not

involve an immediate movement of cash?.............................................................................4

B. Distinguish between...........................................................................................................5

C. Define the following terms:...............................................................................................6

Conclusion.......................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................3

TASK 1.1.........................................................................................................................................3

Construct cash budget for Surya Trading for the period ending on 31 December, 2022.......3

TASK 2.1.........................................................................................................................................4

A. In your view, are cash and profits same? Suggest any business transactions that do not

involve an immediate movement of cash?.............................................................................4

B. Distinguish between...........................................................................................................5

C. Define the following terms:...............................................................................................6

Conclusion.......................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

The one of the most important aspects of the company is its finances. It is the cornerstone of

the company and involves financial management. The business's finances are a key component,

as they relate to the credit and financing methods used by the business organisation. For

successful business operations, business finance is necessary. It involves actions connected to the

acquisition and preservation of capital assets for the purpose of achieving financial business

enterprise goals (Amstad and et.al., 2020). For the purchase of assets, products, raw materials,

and other economic activities, every firm needs a finance. The report is based on the case study

of Surya which is confident for making large scale to a trading business for this cash budget is

prepared for the Surya Trading company from the given data. In addition, the report will cover

about cash & profits are same, difference between several terms of related to financial

accounting.

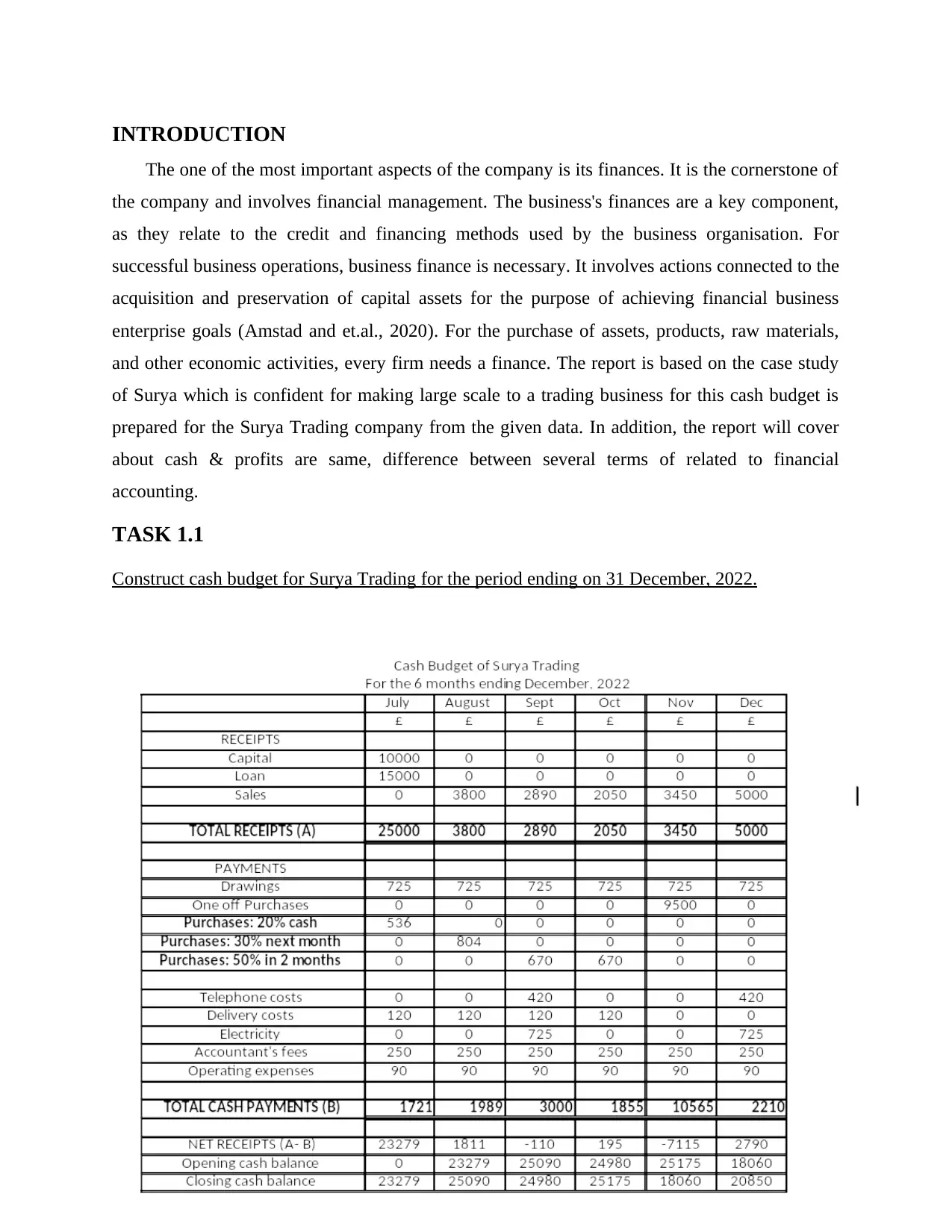

TASK 1.1

Construct cash budget for Surya Trading for the period ending on 31 December, 2022.

The one of the most important aspects of the company is its finances. It is the cornerstone of

the company and involves financial management. The business's finances are a key component,

as they relate to the credit and financing methods used by the business organisation. For

successful business operations, business finance is necessary. It involves actions connected to the

acquisition and preservation of capital assets for the purpose of achieving financial business

enterprise goals (Amstad and et.al., 2020). For the purchase of assets, products, raw materials,

and other economic activities, every firm needs a finance. The report is based on the case study

of Surya which is confident for making large scale to a trading business for this cash budget is

prepared for the Surya Trading company from the given data. In addition, the report will cover

about cash & profits are same, difference between several terms of related to financial

accounting.

TASK 1.1

Construct cash budget for Surya Trading for the period ending on 31 December, 2022.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2.1

A. In your view, are cash and profits same? Suggest any business transactions that do not involve

an immediate movement of cash?

From the point of view, no, cash and profits in terms of accounting are not same in several

ways they distinct from each other.

Cash: This is refereed as flows in and out from business throughout certain period of time. This

helps in measuring the ability of company to pay its bills. The cash balance is the cash received

minus cash paid during the time period. According to economics terms, cash is hard which is in

the form of physical and tangible in currency form such as paper money and coins. Cash is

considered a current asset in auditing and financial accounting, which includes money or money

of a similar nature that may be purchased immediately or in near future which can be in the form

of positive and negative (Anagol, and Pareek, 2019). Positive cash flow meant that the

organisation was bringing in more money than it was spending. A negative cash flow indicates

that the company is spending more money than it is bringing in. Operating cash flow, investment

cash flow, and financing cash flow are the three categories under which cash flow is categorized.

Profits: The profits are shown in the income statement which shows the earning that is derived

from revenue minus expenses. The profits can be net profit or gross profit. In the terms of

accounting, profit is difference between the receiving of revenue by an organisation from its

output and cost incurring on inputs. It is a measure of the organization's profits, which are the

primary concern of the owner in the process of generating income through market production.

The distribution of profits to stakeholders and business owners occurs in the form of dividend

payments or reinvestment in the entity. The profits of the organisation can be either positive or

negative in numbers. If profits occurred negative them it is represented as loss for the business

organisation that is recorded on the credit side of Profit and loss account.

Difference between Cash and Profits

The Cash helps in specifying the organisation inflow and outflow of cash whereas profits

is representation of amount which is been left over after deducting all expenditures or

after payment of all expenses of organisation.

The cash flow of business organisation helps in determining long-term financial stability

which is absolute in terms. The profits are about of showing success of business.

A. In your view, are cash and profits same? Suggest any business transactions that do not involve

an immediate movement of cash?

From the point of view, no, cash and profits in terms of accounting are not same in several

ways they distinct from each other.

Cash: This is refereed as flows in and out from business throughout certain period of time. This

helps in measuring the ability of company to pay its bills. The cash balance is the cash received

minus cash paid during the time period. According to economics terms, cash is hard which is in

the form of physical and tangible in currency form such as paper money and coins. Cash is

considered a current asset in auditing and financial accounting, which includes money or money

of a similar nature that may be purchased immediately or in near future which can be in the form

of positive and negative (Anagol, and Pareek, 2019). Positive cash flow meant that the

organisation was bringing in more money than it was spending. A negative cash flow indicates

that the company is spending more money than it is bringing in. Operating cash flow, investment

cash flow, and financing cash flow are the three categories under which cash flow is categorized.

Profits: The profits are shown in the income statement which shows the earning that is derived

from revenue minus expenses. The profits can be net profit or gross profit. In the terms of

accounting, profit is difference between the receiving of revenue by an organisation from its

output and cost incurring on inputs. It is a measure of the organization's profits, which are the

primary concern of the owner in the process of generating income through market production.

The distribution of profits to stakeholders and business owners occurs in the form of dividend

payments or reinvestment in the entity. The profits of the organisation can be either positive or

negative in numbers. If profits occurred negative them it is represented as loss for the business

organisation that is recorded on the credit side of Profit and loss account.

Difference between Cash and Profits

The Cash helps in specifying the organisation inflow and outflow of cash whereas profits

is representation of amount which is been left over after deducting all expenditures or

after payment of all expenses of organisation.

The cash flow of business organisation helps in determining long-term financial stability

which is absolute in terms. The profits are about of showing success of business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A company's profits are unaffected by payments made to creditors or collected from

debtors. On the contrary cash, is impacted by how invoices are paid and the real money

that the business organisation receives in its bank account (Baber, 2019).

On the balance sheet of an entity the cash are shown on the asset side whereas the on the

debit side of profit and loss account profit are shown along with added to the capital of

company on liabilities side.

Business transactions that do not have an instant involvement of cash

Credit transaction are termed as transactions in which there is no immediate or instant

exchange or involvement of cash at the time of occurrence of transactions. By putting it in

another way that means in case of these transactions cash is paid or received but at some future

date. In the current business situation, products or services are either bought or sold on credit,

meaning that there no instant involvement of cash. Credit transactions involve payments that are

settled at a future time. Credit transactions are those that use the phrase "on credit or account."

B. Distinguish between

a) Capital Expenditure and revenue expenditure

A company's capital expenditures are the sums of money used to purchase new assets or

improve the quality of existing ones. These costs are long-term, capitalised, and reported in the

cash flow statement of the company. These costs are not recurring in any way. The return on

these investments is typically long-term and not restricted to a single year (Bakhadirov,

Pashayev, and Farooq, 2020). Contrarily, revenue expenditure refers to the funds that entities use

to fund their ongoing operations. These expenses are not capitalised and are incurred for a

shorter time period that is limited to an accounting year. They are recurrent in nature and are

stated in the income statement.

b) Expenses and Drawings

The term "expense" refers to an enterprise's ongoing operating costs, such as rent,

electricity, wages, light, and insurance. The gross profit from the profit and loss account is

deducted for these costs. Drawings, on the other hand, refer to money taken out of a business for

the owner's personal benefit. Although it differs from salaries in that the owner is not a concern's

employee and they are free to withdraw any amount, these withdrawals are taken out of the

organization's owner capital on the balance sheet.

c) Gross profit and Net profit

debtors. On the contrary cash, is impacted by how invoices are paid and the real money

that the business organisation receives in its bank account (Baber, 2019).

On the balance sheet of an entity the cash are shown on the asset side whereas the on the

debit side of profit and loss account profit are shown along with added to the capital of

company on liabilities side.

Business transactions that do not have an instant involvement of cash

Credit transaction are termed as transactions in which there is no immediate or instant

exchange or involvement of cash at the time of occurrence of transactions. By putting it in

another way that means in case of these transactions cash is paid or received but at some future

date. In the current business situation, products or services are either bought or sold on credit,

meaning that there no instant involvement of cash. Credit transactions involve payments that are

settled at a future time. Credit transactions are those that use the phrase "on credit or account."

B. Distinguish between

a) Capital Expenditure and revenue expenditure

A company's capital expenditures are the sums of money used to purchase new assets or

improve the quality of existing ones. These costs are long-term, capitalised, and reported in the

cash flow statement of the company. These costs are not recurring in any way. The return on

these investments is typically long-term and not restricted to a single year (Bakhadirov,

Pashayev, and Farooq, 2020). Contrarily, revenue expenditure refers to the funds that entities use

to fund their ongoing operations. These expenses are not capitalised and are incurred for a

shorter time period that is limited to an accounting year. They are recurrent in nature and are

stated in the income statement.

b) Expenses and Drawings

The term "expense" refers to an enterprise's ongoing operating costs, such as rent,

electricity, wages, light, and insurance. The gross profit from the profit and loss account is

deducted for these costs. Drawings, on the other hand, refer to money taken out of a business for

the owner's personal benefit. Although it differs from salaries in that the owner is not a concern's

employee and they are free to withdraw any amount, these withdrawals are taken out of the

organization's owner capital on the balance sheet.

c) Gross profit and Net profit

After subtracting the cost of items sold, a company's gross profit is the amount it made

during that time. Purchases of materials, labour costs incurred, and other costs are included in the

cost of goods sold. When determining total sales, all sales within an accounting period are taken

into consideration (Colaco, 2022). On the other hand, net profit is the sum of revenue after the

cost of products sold and other operational costs are subtracted. Because it is recorded at the

bottom of the revenue statement, it is also known as the bottom line. It can be acquired after

taking away all costs incurred during that specific period.

d) Cash Budget and Cash Flow Statement

The cash budget is an in-depth plan that outlines how cash will be obtained and used

throughout a specified time period. It stands for anticipated cash inflow and outflow. It is simple

to comprehend. It represents the basic minimum of cash that a business must hold in order to

cover its cash needs. It is frequently made for shorter time periods, such as daily, weekly,

monthly, half-yearly, etc. A thorough analysis or representation of how financial resources are

acquired and used over a specific time period is provided by the cash flow statement. It is a key

external statement that includes the sources of cash and illustrates cash usage. For the long

period of time it is prepared, usually once a year.

e) Accruals and Prepayments

Accrued expenses are those which is related from the current period that have not yet

been deducted from income and did not show up in the expenditure balance. This item is

recorded in the profit and loss account and is displayed on the liabilities side of the company's

balance sheet. Prepayments, on the other hand, are costs incurred within the current period but

connected to the following accounting year (Gang and et. al., 2017). As a result, the balance of

expenses reflected in the income statement is reduced by these costs. It appears on the balance

sheet of the company as an asset.

C. Define the following terms:

a) Asset: A sole proprietor or business that owns or controls economic value it does so in

the hope that it will eventually bring about a benefit. These are acquired or produced to

increase a company's worth or enhance the operation of the company, and they are

recorded on the debit side of a company's balance sheet. It can increase sales, reduce

during that time. Purchases of materials, labour costs incurred, and other costs are included in the

cost of goods sold. When determining total sales, all sales within an accounting period are taken

into consideration (Colaco, 2022). On the other hand, net profit is the sum of revenue after the

cost of products sold and other operational costs are subtracted. Because it is recorded at the

bottom of the revenue statement, it is also known as the bottom line. It can be acquired after

taking away all costs incurred during that specific period.

d) Cash Budget and Cash Flow Statement

The cash budget is an in-depth plan that outlines how cash will be obtained and used

throughout a specified time period. It stands for anticipated cash inflow and outflow. It is simple

to comprehend. It represents the basic minimum of cash that a business must hold in order to

cover its cash needs. It is frequently made for shorter time periods, such as daily, weekly,

monthly, half-yearly, etc. A thorough analysis or representation of how financial resources are

acquired and used over a specific time period is provided by the cash flow statement. It is a key

external statement that includes the sources of cash and illustrates cash usage. For the long

period of time it is prepared, usually once a year.

e) Accruals and Prepayments

Accrued expenses are those which is related from the current period that have not yet

been deducted from income and did not show up in the expenditure balance. This item is

recorded in the profit and loss account and is displayed on the liabilities side of the company's

balance sheet. Prepayments, on the other hand, are costs incurred within the current period but

connected to the following accounting year (Gang and et. al., 2017). As a result, the balance of

expenses reflected in the income statement is reduced by these costs. It appears on the balance

sheet of the company as an asset.

C. Define the following terms:

a) Asset: A sole proprietor or business that owns or controls economic value it does so in

the hope that it will eventually bring about a benefit. These are acquired or produced to

increase a company's worth or enhance the operation of the company, and they are

recorded on the debit side of a company's balance sheet. It can increase sales, reduce

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

costs, or generate cash flow. The asset is categorised into tangible, intangible, financial,

fixed, and current asset etc.

b) Liabilities: It is the sum that a person or business is required to repay. These are

eliminated over time by redistributing economic gains such as money, goods, or services.

These are disclosed on the balance sheet's credit side (Gourieroux and et.al., 2018). Debt,

creditors, security interests, deferred revenue, bonds, warranties, and unpaid bills are all

included. Its nature prevents depreciation. It is in charge of the company's cash outflows.

Liabilities include things like short-term loans, leases, and bank overdrafts.

c) Ordinary Shares: These shares, which are also referred to as common shares, are

regarded as stocks that are traded publicly. Every single share of prescribed stock entitles

its owner or holder to one vote at a meeting of stakeholders in an organisation. However,

unlike holders of preference shares, the holders of these shares are not guaranteed a

dividend. Following the distribution of dividends to preference shareholders, a dividend

will be paid to holders of ordinary shares.

d) Preference Shares: These are sometimes referred to as preferred stock. These are the

shares of an entity that receive dividend payments before paying dividend of regular

shares. Preference shareholders are entitled to dividends before equity owners in the

event of a company's liquidation (Lundstrum, 2018). In contrast to ordinary shares,

preference shares often have a fixed dividend. At the organization's annual meeting of

shareholders, their shareholders do not exercise voting rights.

e) Dividend: It is the distribution of an organization's profits to its preferred and equity

shareholders. An entity can pay a portion of its profit as a dividend to the company's

stockholders when it has a surplus. It is typically distributed quarterly and might be paid

out in cash or put toward buying more stock. Until the date they hold their investment in

the firm but before the date of the declaration of ex-dividend, stockholders of companies

that regularly pay off their dividend are entitled to collect their proportions.

f) Stock Exchange: A stock trader can purchase and sell shares on this market. It is also

known as a "bourse" or "securities exchange." Shares of stocks, bonds, and other

financial instruments are included in stock exchange (Nicoletti, 2018). Additionally, it

offers services for the issuance and redemption of securities. Stocks and bonds are

offered in an initial public offering, or IPO, on the main market, after which trading takes

fixed, and current asset etc.

b) Liabilities: It is the sum that a person or business is required to repay. These are

eliminated over time by redistributing economic gains such as money, goods, or services.

These are disclosed on the balance sheet's credit side (Gourieroux and et.al., 2018). Debt,

creditors, security interests, deferred revenue, bonds, warranties, and unpaid bills are all

included. Its nature prevents depreciation. It is in charge of the company's cash outflows.

Liabilities include things like short-term loans, leases, and bank overdrafts.

c) Ordinary Shares: These shares, which are also referred to as common shares, are

regarded as stocks that are traded publicly. Every single share of prescribed stock entitles

its owner or holder to one vote at a meeting of stakeholders in an organisation. However,

unlike holders of preference shares, the holders of these shares are not guaranteed a

dividend. Following the distribution of dividends to preference shareholders, a dividend

will be paid to holders of ordinary shares.

d) Preference Shares: These are sometimes referred to as preferred stock. These are the

shares of an entity that receive dividend payments before paying dividend of regular

shares. Preference shareholders are entitled to dividends before equity owners in the

event of a company's liquidation (Lundstrum, 2018). In contrast to ordinary shares,

preference shares often have a fixed dividend. At the organization's annual meeting of

shareholders, their shareholders do not exercise voting rights.

e) Dividend: It is the distribution of an organization's profits to its preferred and equity

shareholders. An entity can pay a portion of its profit as a dividend to the company's

stockholders when it has a surplus. It is typically distributed quarterly and might be paid

out in cash or put toward buying more stock. Until the date they hold their investment in

the firm but before the date of the declaration of ex-dividend, stockholders of companies

that regularly pay off their dividend are entitled to collect their proportions.

f) Stock Exchange: A stock trader can purchase and sell shares on this market. It is also

known as a "bourse" or "securities exchange." Shares of stocks, bonds, and other

financial instruments are included in stock exchange (Nicoletti, 2018). Additionally, it

offers services for the issuance and redemption of securities. Stocks and bonds are

offered in an initial public offering, or IPO, on the main market, after which trading takes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

place on the secondary market. An individual can invest in a variety of shares, including

penny stocks and blue chips.

g) Venture Capital: It is a form of personal equity and funding that is given by investors to

start-up enterprises and mid-cap corporations with the expectation that they will be

around in the long run. It is typically received through reputable investors, investment

firms, and other financial institutions (Phan and et.al., 2019). Although it isn't always

expressed in monetary terms, it can also be processed as a management and technical

skill. It is typically given to small businesses with the potential for significant growth.

h) Budget: The term "budget" refers to an analysis of the expected earnings and expenses

for a specific future time period. It is typically organised and periodically evaluated. It

might be made for one person, a group of people, an organisation, or a government

agency that regulates. It is a financial strategy created for a specific time frame. It

includes projected costs and expenses, cash inflows and outflows, assets, liabilities, and

sales volume and revenue from such sales (Rohde and et.al., 2018).

i) Capital Income: Capital income is defined as money that an organisation derives from

its assets other than its production process. Capital gains and dividends on stocks make

up this amount. It results through the passing of time rather than from the use of an asset.

j) Company: A legal body that represents a group of people, whether they are natural,

legal, or a combination of the two. In order to accomplish a certain and predetermined

goal, the company's members collaborate on a single goal. Members of the company have

limited liability. It is a legal construct that has a perpetual succession and a common seal

next to its name. In accordance with the corporate legislation that governs its authority, it

may be set up in various ways for taxation and financial obligation purposes (Tran,

2019).

Conclusion

From the above report it is been concluded that business finance provides the support to

business organisation which leads to in its growth and helps in attaining productivity. In the

finance it covers several terms such as cash budget, expenses, drawings, assets & liabilities,

venture capital and many more that all are important for the business.

penny stocks and blue chips.

g) Venture Capital: It is a form of personal equity and funding that is given by investors to

start-up enterprises and mid-cap corporations with the expectation that they will be

around in the long run. It is typically received through reputable investors, investment

firms, and other financial institutions (Phan and et.al., 2019). Although it isn't always

expressed in monetary terms, it can also be processed as a management and technical

skill. It is typically given to small businesses with the potential for significant growth.

h) Budget: The term "budget" refers to an analysis of the expected earnings and expenses

for a specific future time period. It is typically organised and periodically evaluated. It

might be made for one person, a group of people, an organisation, or a government

agency that regulates. It is a financial strategy created for a specific time frame. It

includes projected costs and expenses, cash inflows and outflows, assets, liabilities, and

sales volume and revenue from such sales (Rohde and et.al., 2018).

i) Capital Income: Capital income is defined as money that an organisation derives from

its assets other than its production process. Capital gains and dividends on stocks make

up this amount. It results through the passing of time rather than from the use of an asset.

j) Company: A legal body that represents a group of people, whether they are natural,

legal, or a combination of the two. In order to accomplish a certain and predetermined

goal, the company's members collaborate on a single goal. Members of the company have

limited liability. It is a legal construct that has a perpetual succession and a common seal

next to its name. In accordance with the corporate legislation that governs its authority, it

may be set up in various ways for taxation and financial obligation purposes (Tran,

2019).

Conclusion

From the above report it is been concluded that business finance provides the support to

business organisation which leads to in its growth and helps in attaining productivity. In the

finance it covers several terms such as cash budget, expenses, drawings, assets & liabilities,

venture capital and many more that all are important for the business.

REFERENCES

Books and Journals

Amstad and et.al., 2020. The Handbook of China's Financial System. Princeton University Press.

Anagol, S. and Pareek, A., 2019. Should business groups be in finance? Evidence from Indian

mutual funds. Journal of Development Economics, 139. pp.229-248.

Baber, H., 2019. Financial inclusion and FinTech: A comparative study of countries following

Islamic finance and conventional finance. Qualitative Research in Financial Markets.

Bakhadirov, M., Pashayev, Z. and Farooq, O., 2020. Effect of location on access to finance:

international evidence on the moderating role of employee training. Review of

Behavioral Finance.

Colaco, H.M., 2022. Ethical and professional standards of the CFA¬ Æ Program and finance-

related university education. In Embedding Sustainability, Corporate Social Responsibility and

Ethics in Business Education (pp. 133-143). Edward Elgar Publishing

Gang and et. al., 2017. Credit Card Business and Consumer Finance of China, Japan, and South

Korea. Development of Consumer Finance in East Asia, pp.43-94.

Gourieroux and et.al., 2018. Financial econometrics. Princeton University Press

Lundstrum, L.L., 2018. The Firm, the Market, and the Rising Finance Professional. Journal of

the Academy of Business Education, 19.

Nicoletti, B., 2018. Fintech and procurement finance 4.0. In Procurement Finance (pp. 155-248).

Palgrave Macmillan, Cham

Phan and et.al., 2019. Segmentation of financial clients by attitudes and behavior. International

Journal of Bank Marketing.

Rohde and et.al., 2018. Competing by investments or efficiency? Exploring financial and

sporting efficiency of club ownership structures in European football. Sport Management

Review, 21(5), pp.563-581.

Tran, Q.T., 2019. Corporate cash holdings and financial crisis: new evidence from an emerging

marke. Eurasian Business Review, pp.1-15.

Books and Journals

Amstad and et.al., 2020. The Handbook of China's Financial System. Princeton University Press.

Anagol, S. and Pareek, A., 2019. Should business groups be in finance? Evidence from Indian

mutual funds. Journal of Development Economics, 139. pp.229-248.

Baber, H., 2019. Financial inclusion and FinTech: A comparative study of countries following

Islamic finance and conventional finance. Qualitative Research in Financial Markets.

Bakhadirov, M., Pashayev, Z. and Farooq, O., 2020. Effect of location on access to finance:

international evidence on the moderating role of employee training. Review of

Behavioral Finance.

Colaco, H.M., 2022. Ethical and professional standards of the CFA¬ Æ Program and finance-

related university education. In Embedding Sustainability, Corporate Social Responsibility and

Ethics in Business Education (pp. 133-143). Edward Elgar Publishing

Gang and et. al., 2017. Credit Card Business and Consumer Finance of China, Japan, and South

Korea. Development of Consumer Finance in East Asia, pp.43-94.

Gourieroux and et.al., 2018. Financial econometrics. Princeton University Press

Lundstrum, L.L., 2018. The Firm, the Market, and the Rising Finance Professional. Journal of

the Academy of Business Education, 19.

Nicoletti, B., 2018. Fintech and procurement finance 4.0. In Procurement Finance (pp. 155-248).

Palgrave Macmillan, Cham

Phan and et.al., 2019. Segmentation of financial clients by attitudes and behavior. International

Journal of Bank Marketing.

Rohde and et.al., 2018. Competing by investments or efficiency? Exploring financial and

sporting efficiency of club ownership structures in European football. Sport Management

Review, 21(5), pp.563-581.

Tran, Q.T., 2019. Corporate cash holdings and financial crisis: new evidence from an emerging

marke. Eurasian Business Review, pp.1-15.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.