Business Finance Homework: Financial Analysis and Valuation

VerifiedAdded on 2020/02/19

|8

|1240

|48

Homework Assignment

AI Summary

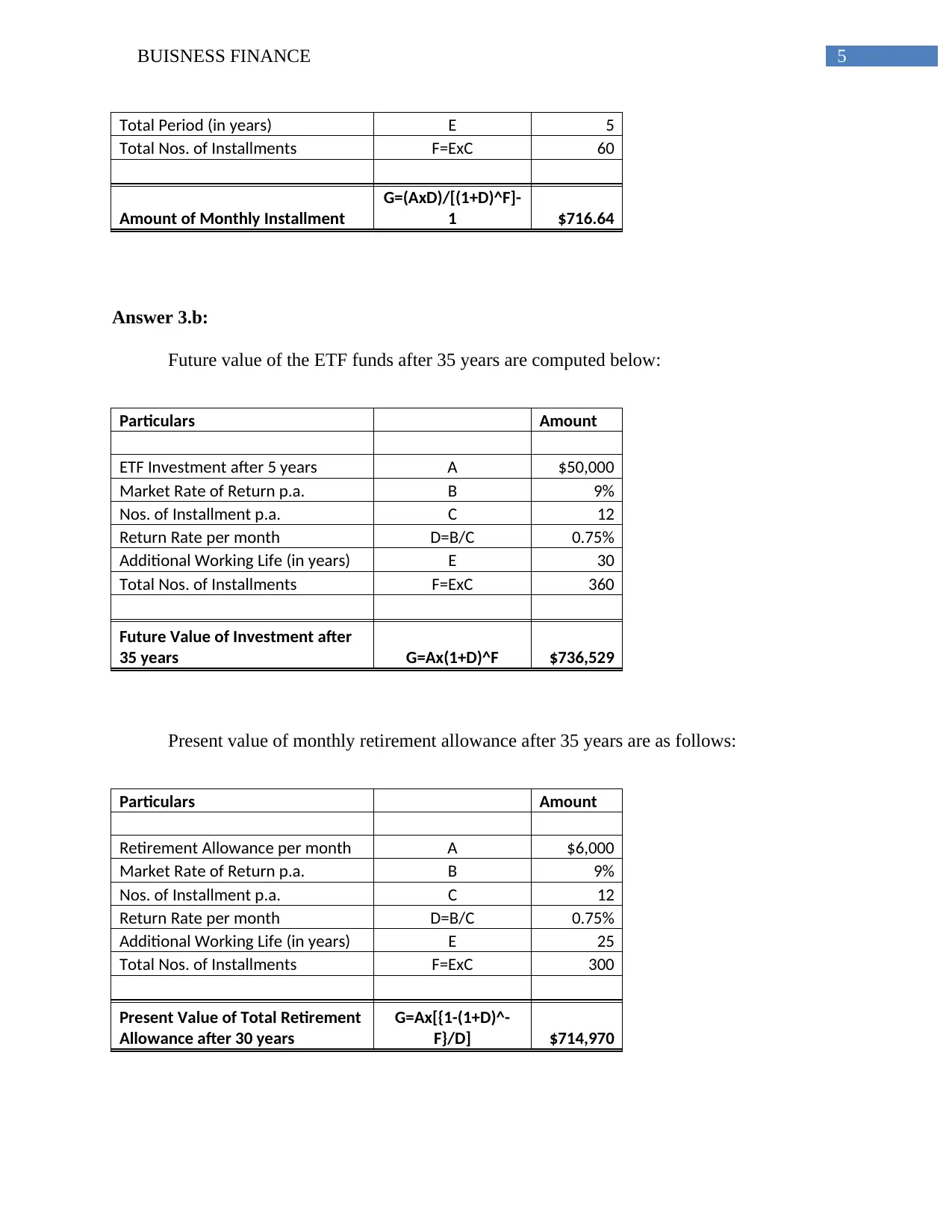

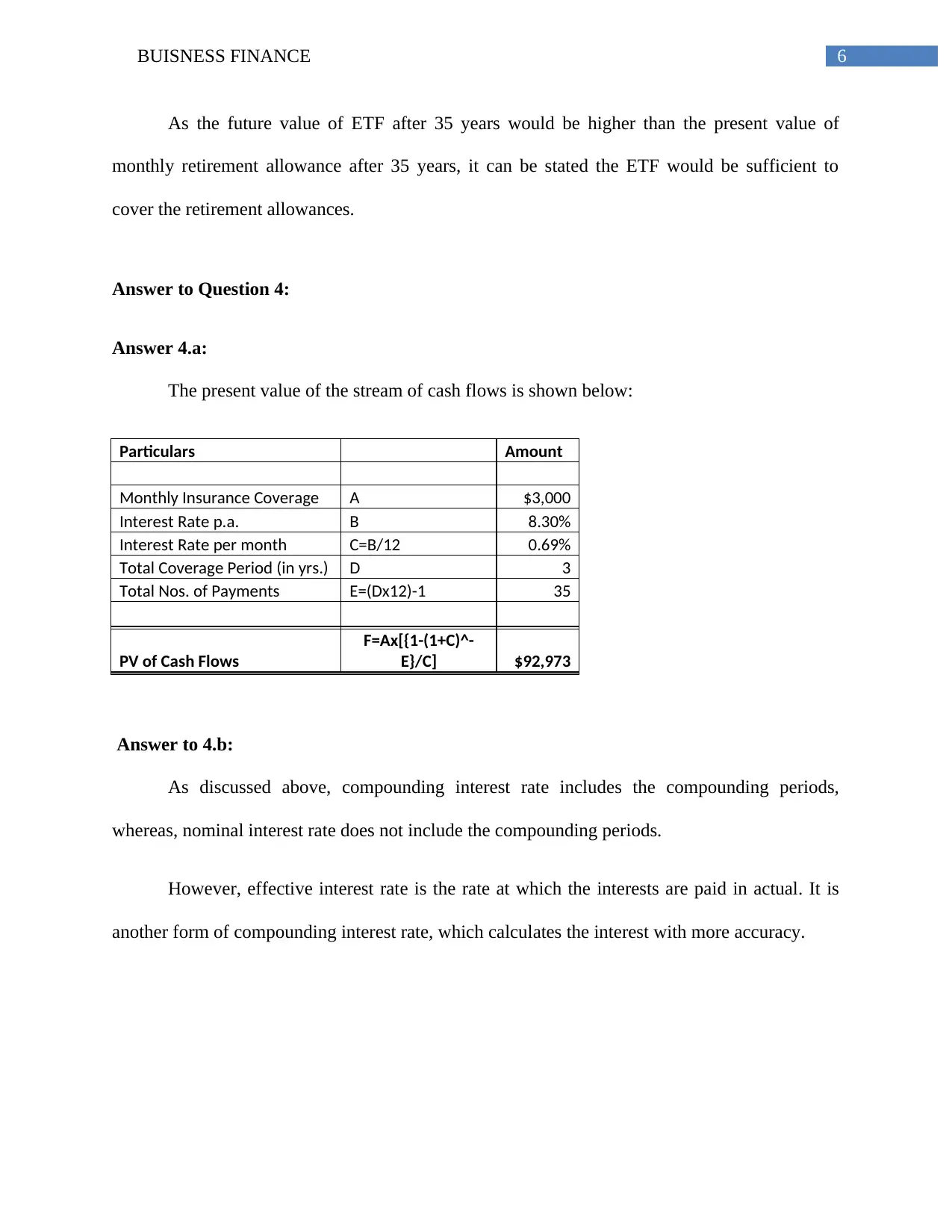

This document presents a comprehensive solution to a business finance assignment, addressing key concepts such as asset maximization, nominal and compounding interest rates, and investment valuation. The assignment delves into calculations of present and future values, analyzing the profitability of investments and the impact of interest rates on financial decisions. It includes detailed calculations for loan installments, future value of ETF funds, and present value of retirement allowances. Furthermore, the solution explores the present value of cash flows from insurance coverage, offering a complete understanding of financial planning and investment strategies. The assignment covers various aspects of finance, providing a well-rounded analysis of financial concepts and their practical applications.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.