Business Finance Assignment: Capital Structure and Valuation

VerifiedAdded on 2020/04/21

|12

|1687

|174

Homework Assignment

AI Summary

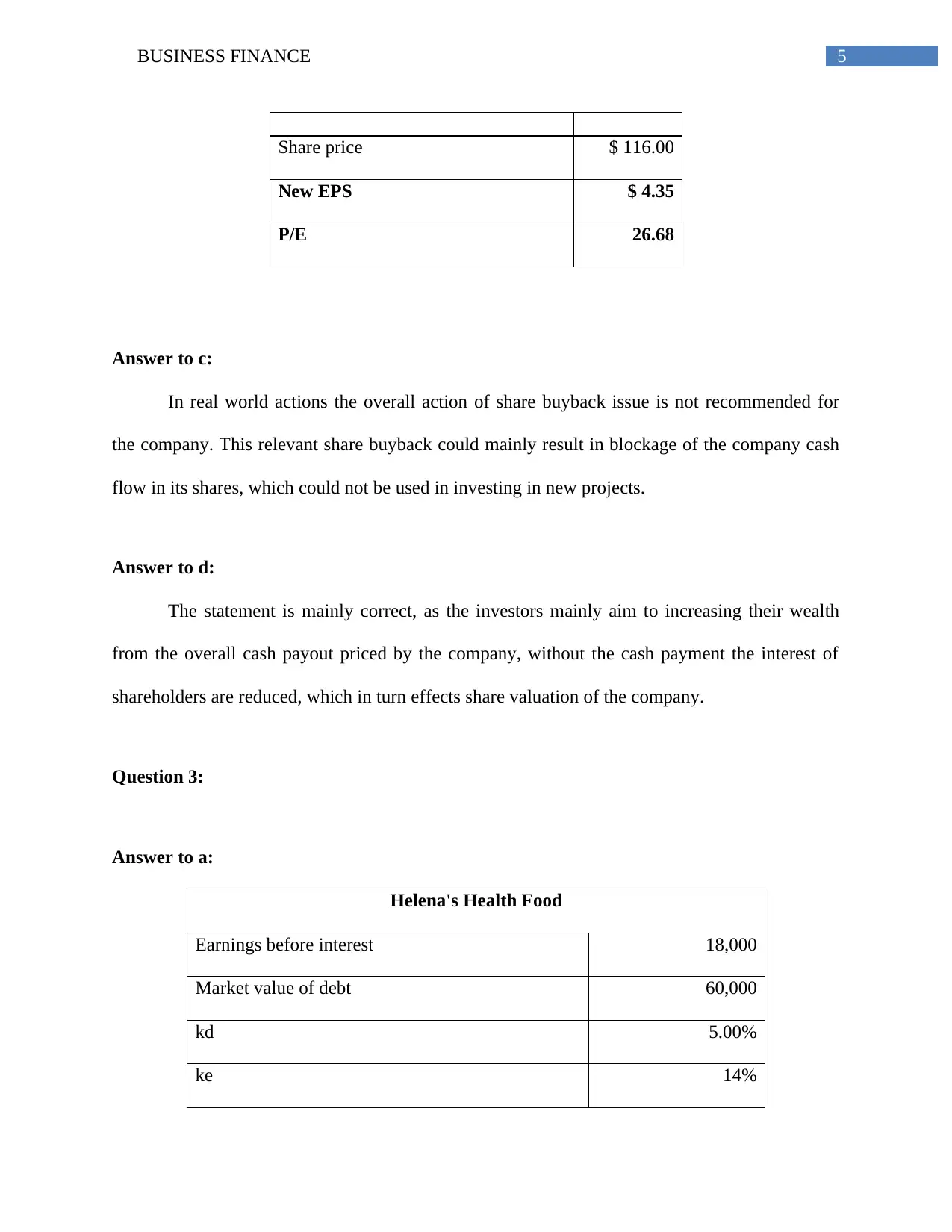

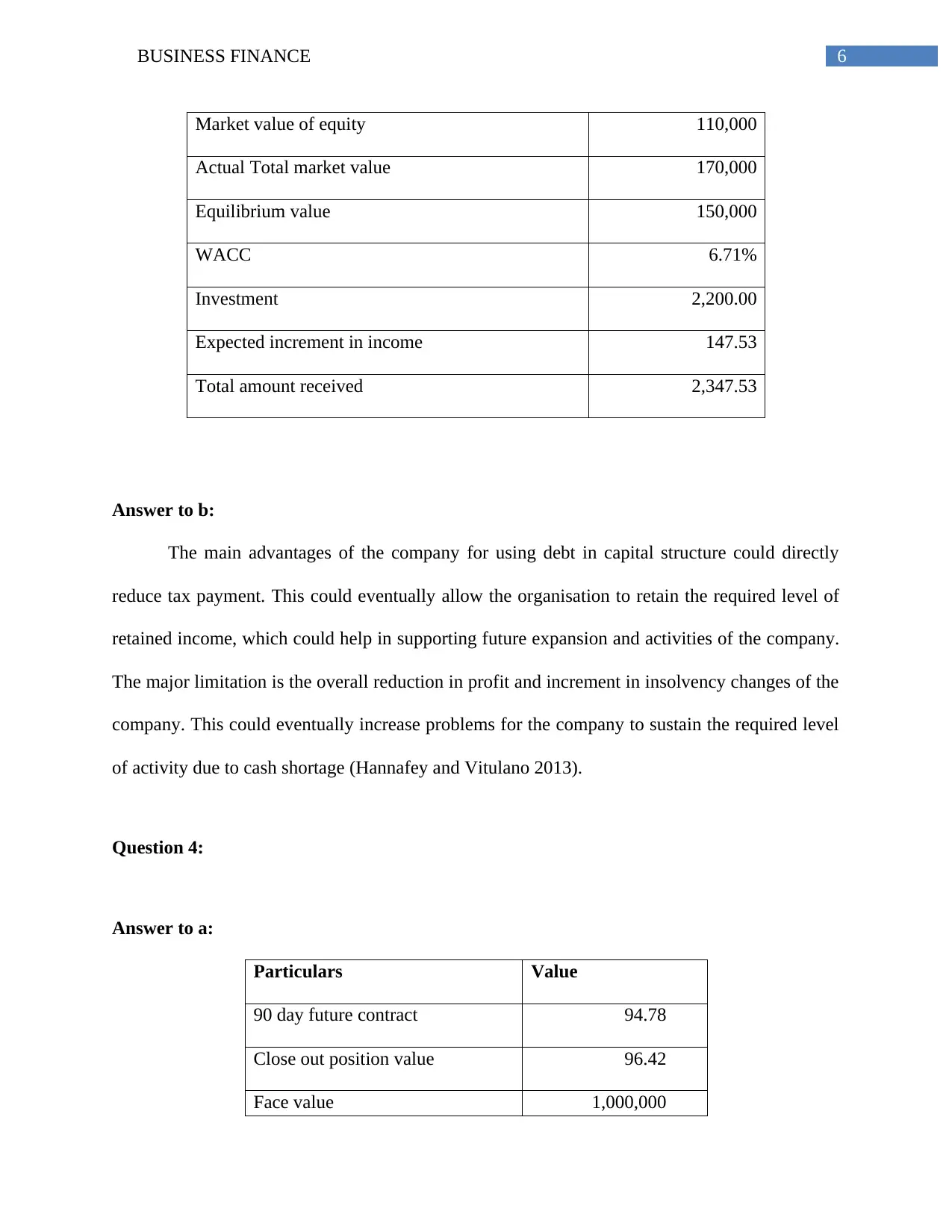

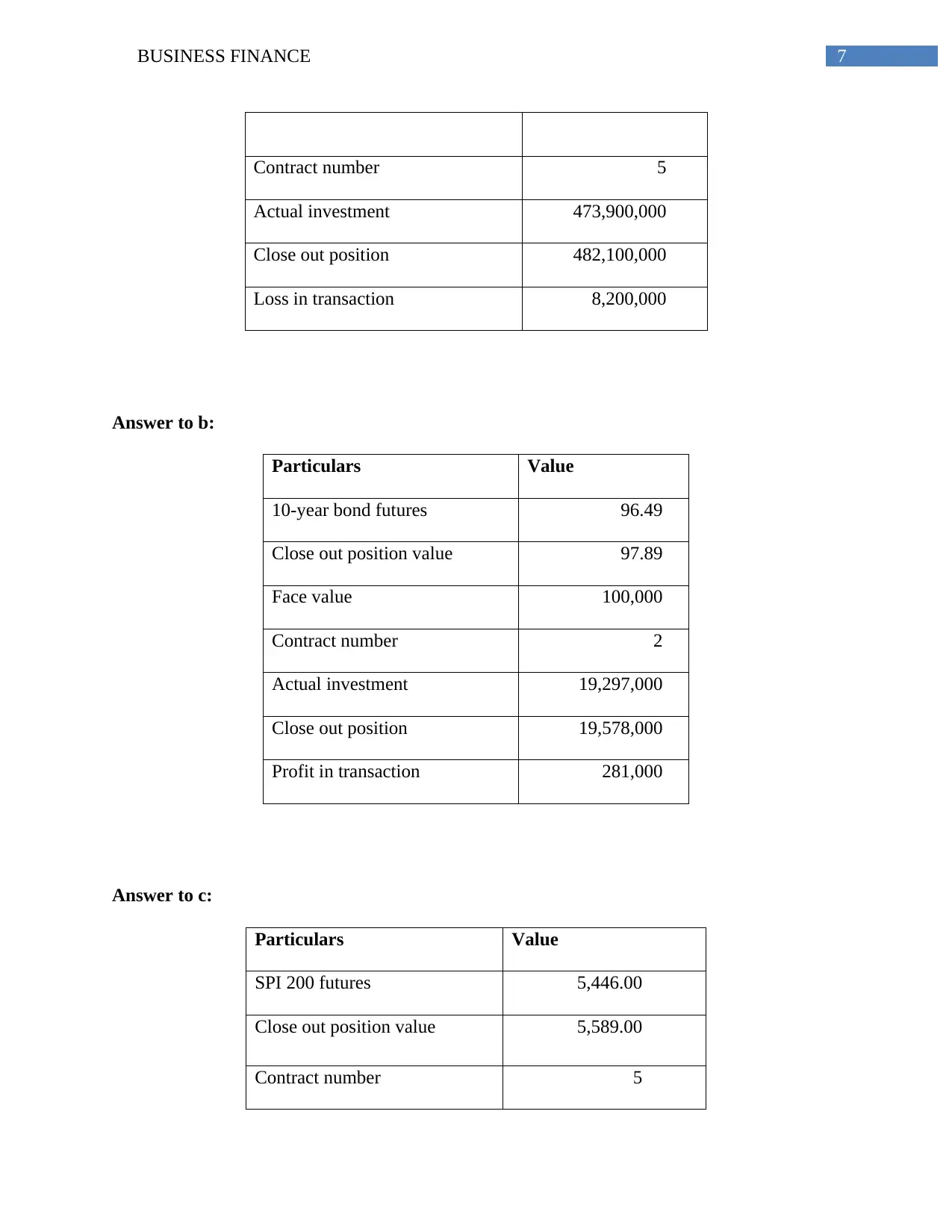

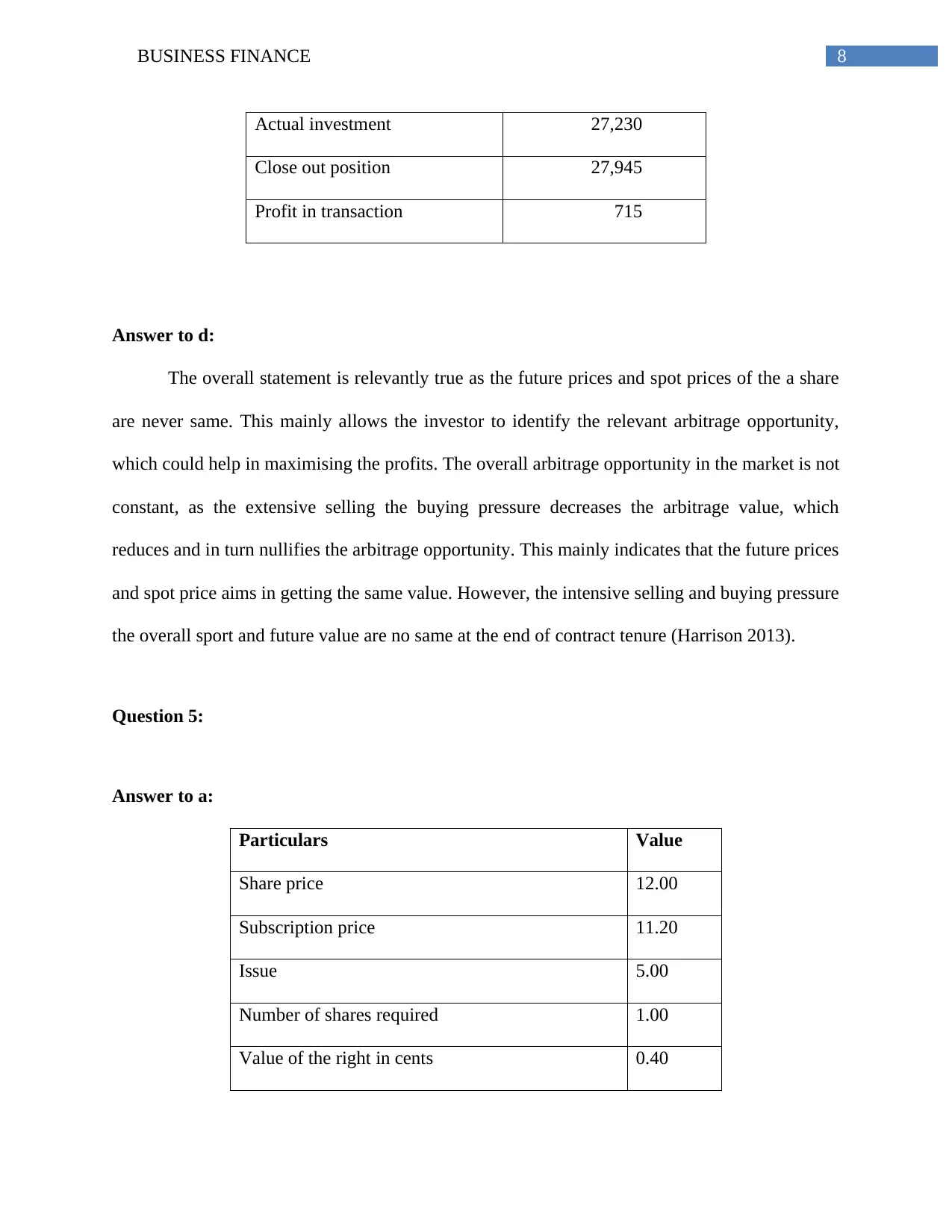

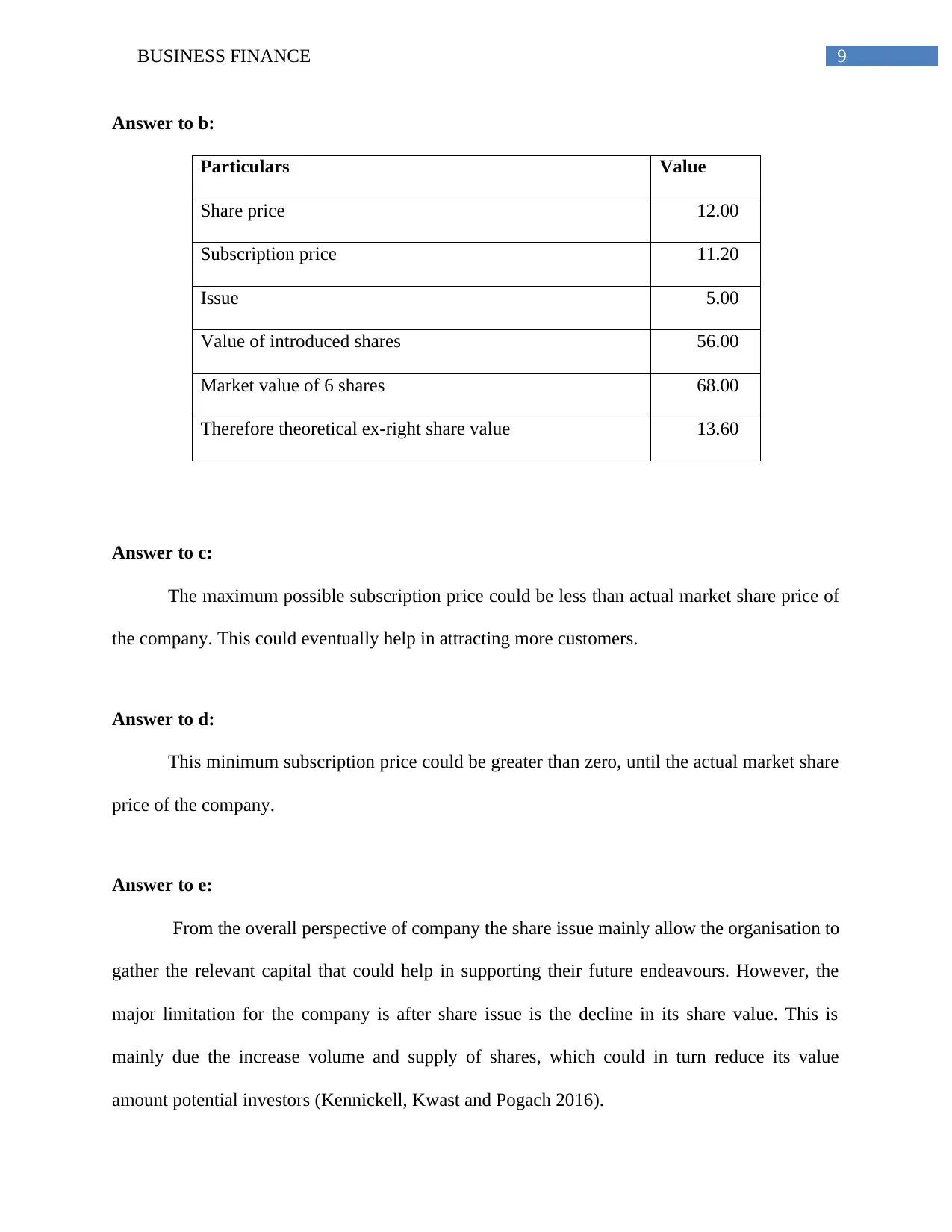

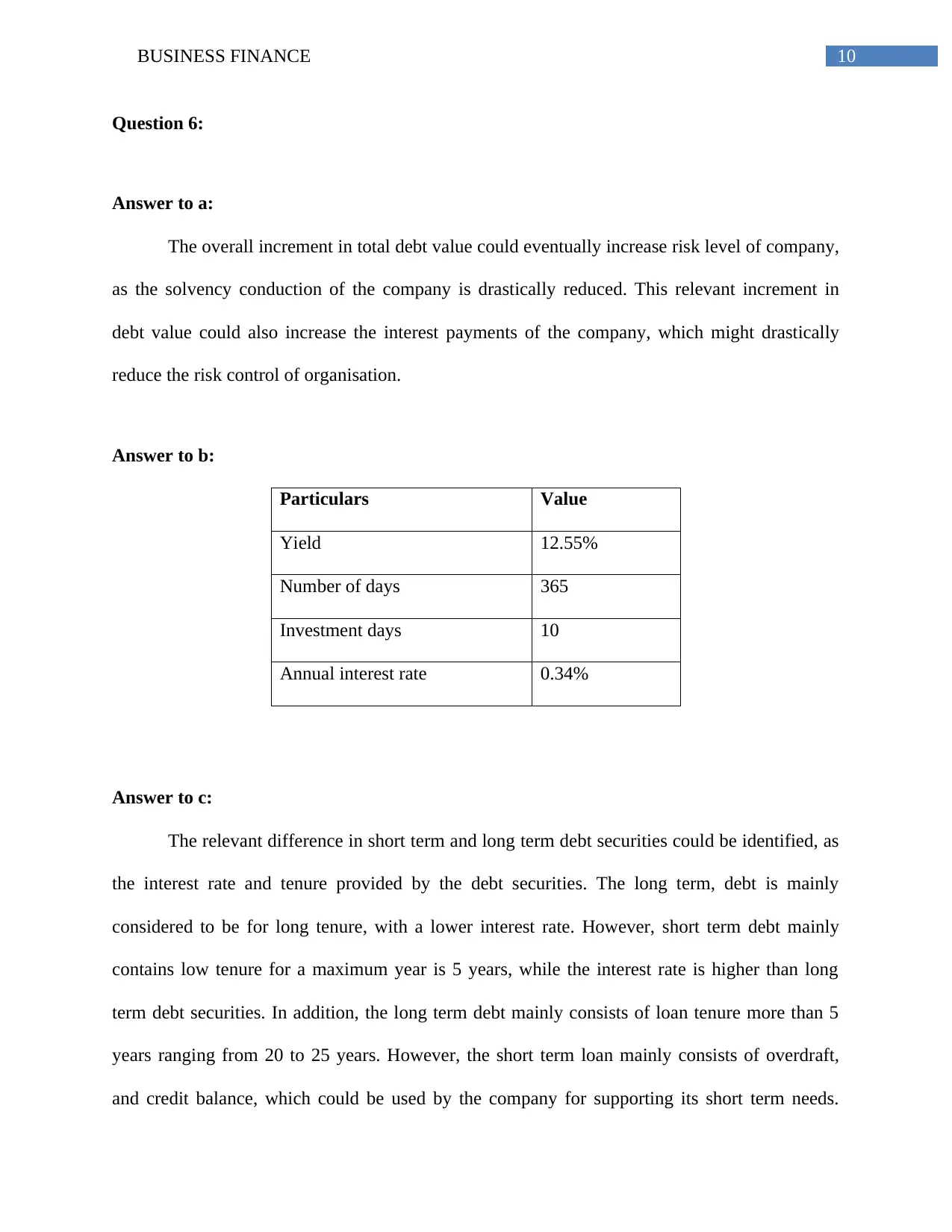

This Business Finance assignment solution provides a comprehensive analysis of various financial concepts. The assignment covers topics such as managerial flexibility in investment decisions, dividend payment versus share repurchase, and the use of debt in capital structure. It includes calculations and explanations related to share valuation, earnings per share (EPS), and the impact of financial decisions on shareholder wealth. Furthermore, the document explores future contracts, bond futures, and stock index futures, offering insights into hedging and arbitrage opportunities. It also examines share issues, subscription prices, and their implications for company capital. Finally, the assignment delves into short-term and long-term debt securities, analyzing their characteristics and impact on a company's financial health. The assignment is supported by relevant references and bibliographies.

1 out of 12

Related Documents

![Corporate Finance Assignment - [University Name], [Course Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fuo%2F094009c5b53d4253926258a7330aca34.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.