Business Finance Report: Cashflow, Budgeting, and Financial Analysis

VerifiedAdded on 2023/01/13

|11

|3198

|89

Report

AI Summary

This report provides a comprehensive analysis of key business finance concepts, focusing on cash flow, working capital, budgeting, and financial statements. Part A delves into the differences between profit and cash flow, examining working capital, receivables, inventory, and payables. It then applies these concepts to Mediterranean Delights Ltd (MDL), evaluating its financial performance and recommending steps to improve cash flow. Part B explores budgeting methods, including traditional and alternative approaches like rolling and zero-based budgeting, along with their advantages and disadvantages. The report concludes by analyzing the application of these budgeting methods to Second Sight Plc and offers recommendations for achieving future financial targets. The report is a detailed exploration of financial concepts and practical applications, offering valuable insights for students.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

PART A...........................................................................................................................................1

Executive summary.....................................................................................................................1

Question 1...................................................................................................................................1

2. Applying the above mentioned concepts in Mediterranean Delights Ltd (“MDL”)...............3

3. Recommend what steps to improve company’s cashflow......................................................4

PART B............................................................................................................................................5

Executive summary.....................................................................................................................5

i) Understating of budget formation............................................................................................5

ii) Implanting of methods and cost management........................................................................6

iii) Evaluation of traditional or alternative budgetary system.....................................................7

REFERENCES ...............................................................................................................................9

PART A...........................................................................................................................................1

Executive summary.....................................................................................................................1

Question 1...................................................................................................................................1

2. Applying the above mentioned concepts in Mediterranean Delights Ltd (“MDL”)...............3

3. Recommend what steps to improve company’s cashflow......................................................4

PART B............................................................................................................................................5

Executive summary.....................................................................................................................5

i) Understating of budget formation............................................................................................5

ii) Implanting of methods and cost management........................................................................6

iii) Evaluation of traditional or alternative budgetary system.....................................................7

REFERENCES ...............................................................................................................................9

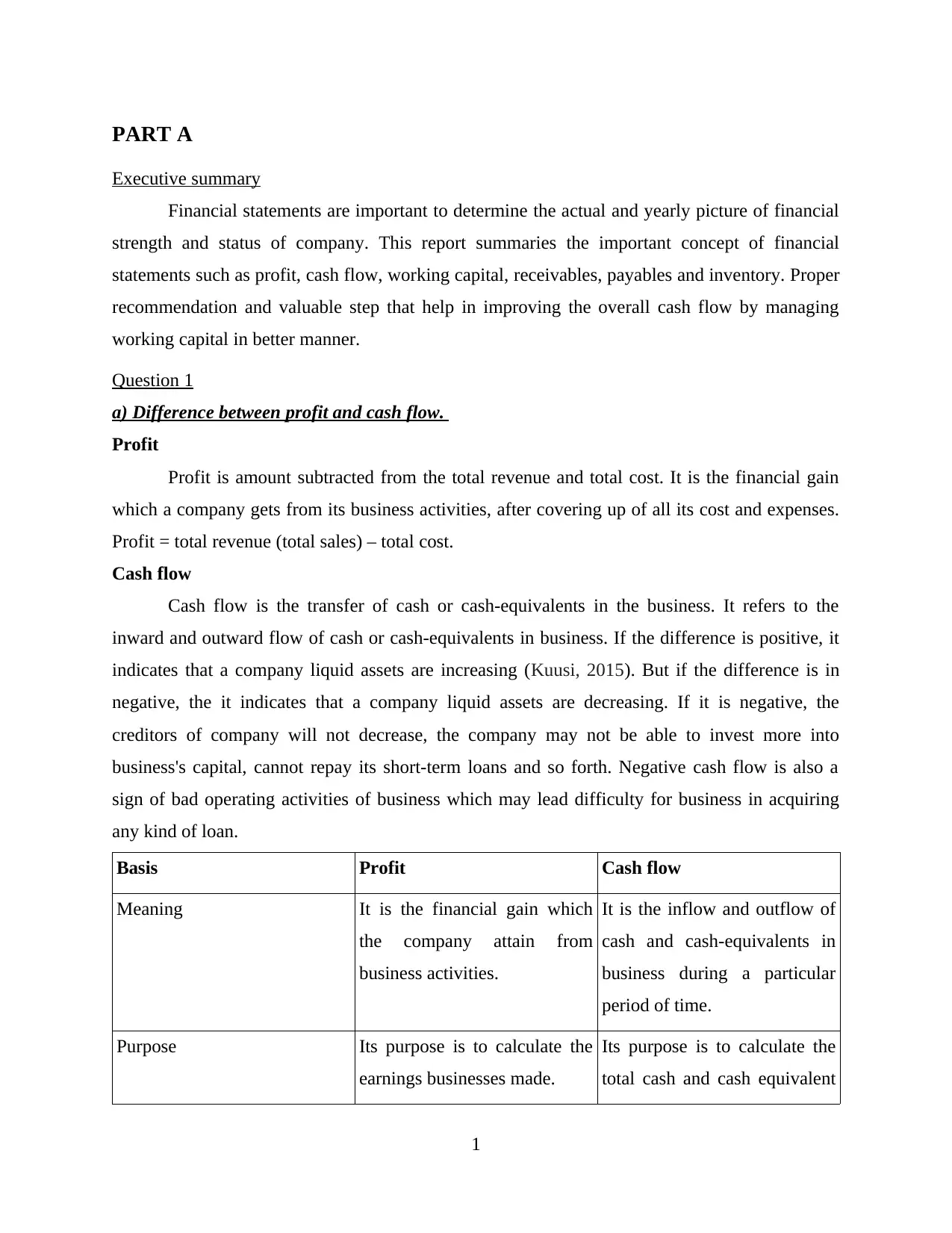

PART A

Executive summary

Financial statements are important to determine the actual and yearly picture of financial

strength and status of company. This report summaries the important concept of financial

statements such as profit, cash flow, working capital, receivables, payables and inventory. Proper

recommendation and valuable step that help in improving the overall cash flow by managing

working capital in better manner.

Question 1

a) Difference between profit and cash flow.

Profit

Profit is amount subtracted from the total revenue and total cost. It is the financial gain

which a company gets from its business activities, after covering up of all its cost and expenses.

Profit = total revenue (total sales) – total cost.

Cash flow

Cash flow is the transfer of cash or cash-equivalents in the business. It refers to the

inward and outward flow of cash or cash-equivalents in business. If the difference is positive, it

indicates that a company liquid assets are increasing (Kuusi, 2015). But if the difference is in

negative, the it indicates that a company liquid assets are decreasing. If it is negative, the

creditors of company will not decrease, the company may not be able to invest more into

business's capital, cannot repay its short-term loans and so forth. Negative cash flow is also a

sign of bad operating activities of business which may lead difficulty for business in acquiring

any kind of loan.

Basis Profit Cash flow

Meaning It is the financial gain which

the company attain from

business activities.

It is the inflow and outflow of

cash and cash-equivalents in

business during a particular

period of time.

Purpose Its purpose is to calculate the

earnings businesses made.

Its purpose is to calculate the

total cash and cash equivalent

1

Executive summary

Financial statements are important to determine the actual and yearly picture of financial

strength and status of company. This report summaries the important concept of financial

statements such as profit, cash flow, working capital, receivables, payables and inventory. Proper

recommendation and valuable step that help in improving the overall cash flow by managing

working capital in better manner.

Question 1

a) Difference between profit and cash flow.

Profit

Profit is amount subtracted from the total revenue and total cost. It is the financial gain

which a company gets from its business activities, after covering up of all its cost and expenses.

Profit = total revenue (total sales) – total cost.

Cash flow

Cash flow is the transfer of cash or cash-equivalents in the business. It refers to the

inward and outward flow of cash or cash-equivalents in business. If the difference is positive, it

indicates that a company liquid assets are increasing (Kuusi, 2015). But if the difference is in

negative, the it indicates that a company liquid assets are decreasing. If it is negative, the

creditors of company will not decrease, the company may not be able to invest more into

business's capital, cannot repay its short-term loans and so forth. Negative cash flow is also a

sign of bad operating activities of business which may lead difficulty for business in acquiring

any kind of loan.

Basis Profit Cash flow

Meaning It is the financial gain which

the company attain from

business activities.

It is the inflow and outflow of

cash and cash-equivalents in

business during a particular

period of time.

Purpose Its purpose is to calculate the

earnings businesses made.

Its purpose is to calculate the

total cash and cash equivalent

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

available with a company after

paying for its expenses.

Basic formulae Profit= Total sales- total cost Cash inflow/outflow = Total

cash receivables- total cash

payables (Ofei-Mensah and

Bennett, 2013).

b) Meaning of Working Capital,

Receivables, Inventory and Payables

Working capital

Working capital is the difference between company's current assets and current liabilities.

Current assets include – cash available in hand and bank, debtors and inventories of raw

materials and finished goods. Whereas current liabilities include- creditors, tax, wages, and the

current portion of long-term debt. Working capital is used to evaluate company's operational

efficiency and its short term financial health. Where as, a company has positive working capital

if the ratio between its current assets and liabilities are equal or more than. But high working

capital is also not good because it indicates that the business has excesses inventory or they are

not investing its excess cash.

Receivables

Receivables are the amount which the customers or other party owned to the company. It

is the amount which the company will receive in near future. They are shown under assets

category in balance sheet as people ( to which the company allows to purchase goods or services

on credit) owe to the company. Receivables are recorded into books at the time of sale and get

erase when the payments are done from customers. The amount of total receivables decreases

when payment is received.

Inventory

Inventory is the stock or goods available with the company which it meant for resale.

Inventory may include the stock of raw materials, finished and semi-finished goods company has

stored with itself or in warehouse (Blaak, Openjuru and Zeelen, 2013). It is classified as an asset

and shown in assets category in balance sheet. There are 3 types of inventories, namely, raw

materials, work-in-progress, and finished goods.

Payables

2

paying for its expenses.

Basic formulae Profit= Total sales- total cost Cash inflow/outflow = Total

cash receivables- total cash

payables (Ofei-Mensah and

Bennett, 2013).

b) Meaning of Working Capital,

Receivables, Inventory and Payables

Working capital

Working capital is the difference between company's current assets and current liabilities.

Current assets include – cash available in hand and bank, debtors and inventories of raw

materials and finished goods. Whereas current liabilities include- creditors, tax, wages, and the

current portion of long-term debt. Working capital is used to evaluate company's operational

efficiency and its short term financial health. Where as, a company has positive working capital

if the ratio between its current assets and liabilities are equal or more than. But high working

capital is also not good because it indicates that the business has excesses inventory or they are

not investing its excess cash.

Receivables

Receivables are the amount which the customers or other party owned to the company. It

is the amount which the company will receive in near future. They are shown under assets

category in balance sheet as people ( to which the company allows to purchase goods or services

on credit) owe to the company. Receivables are recorded into books at the time of sale and get

erase when the payments are done from customers. The amount of total receivables decreases

when payment is received.

Inventory

Inventory is the stock or goods available with the company which it meant for resale.

Inventory may include the stock of raw materials, finished and semi-finished goods company has

stored with itself or in warehouse (Blaak, Openjuru and Zeelen, 2013). It is classified as an asset

and shown in assets category in balance sheet. There are 3 types of inventories, namely, raw

materials, work-in-progress, and finished goods.

Payables

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

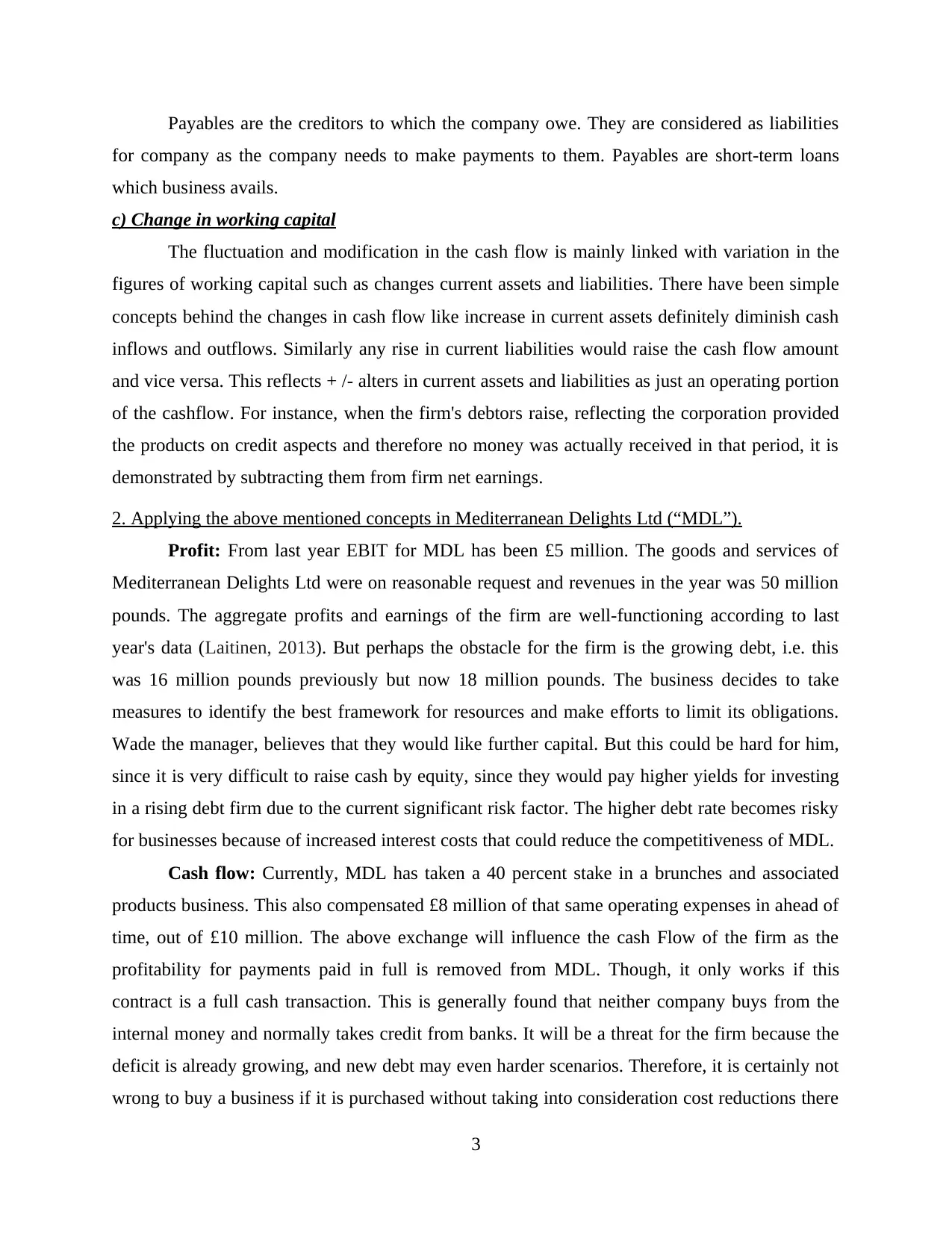

Payables are the creditors to which the company owe. They are considered as liabilities

for company as the company needs to make payments to them. Payables are short-term loans

which business avails.

c) Change in working capital

The fluctuation and modification in the cash flow is mainly linked with variation in the

figures of working capital such as changes current assets and liabilities. There have been simple

concepts behind the changes in cash flow like increase in current assets definitely diminish cash

inflows and outflows. Similarly any rise in current liabilities would raise the cash flow amount

and vice versa. This reflects + /- alters in current assets and liabilities as just an operating portion

of the cashflow. For instance, when the firm's debtors raise, reflecting the corporation provided

the products on credit aspects and therefore no money was actually received in that period, it is

demonstrated by subtracting them from firm net earnings.

2. Applying the above mentioned concepts in Mediterranean Delights Ltd (“MDL”).

Profit: From last year EBIT for MDL has been £5 million. The goods and services of

Mediterranean Delights Ltd were on reasonable request and revenues in the year was 50 million

pounds. The aggregate profits and earnings of the firm are well-functioning according to last

year's data (Laitinen, 2013). But perhaps the obstacle for the firm is the growing debt, i.e. this

was 16 million pounds previously but now 18 million pounds. The business decides to take

measures to identify the best framework for resources and make efforts to limit its obligations.

Wade the manager, believes that they would like further capital. But this could be hard for him,

since it is very difficult to raise cash by equity, since they would pay higher yields for investing

in a rising debt firm due to the current significant risk factor. The higher debt rate becomes risky

for businesses because of increased interest costs that could reduce the competitiveness of MDL.

Cash flow: Currently, MDL has taken a 40 percent stake in a brunches and associated

products business. This also compensated £8 million of that same operating expenses in ahead of

time, out of £10 million. The above exchange will influence the cash Flow of the firm as the

profitability for payments paid in full is removed from MDL. Though, it only works if this

contract is a full cash transaction. This is generally found that neither company buys from the

internal money and normally takes credit from banks. It will be a threat for the firm because the

deficit is already growing, and new debt may even harder scenarios. Therefore, it is certainly not

wrong to buy a business if it is purchased without taking into consideration cost reductions there

3

for company as the company needs to make payments to them. Payables are short-term loans

which business avails.

c) Change in working capital

The fluctuation and modification in the cash flow is mainly linked with variation in the

figures of working capital such as changes current assets and liabilities. There have been simple

concepts behind the changes in cash flow like increase in current assets definitely diminish cash

inflows and outflows. Similarly any rise in current liabilities would raise the cash flow amount

and vice versa. This reflects + /- alters in current assets and liabilities as just an operating portion

of the cashflow. For instance, when the firm's debtors raise, reflecting the corporation provided

the products on credit aspects and therefore no money was actually received in that period, it is

demonstrated by subtracting them from firm net earnings.

2. Applying the above mentioned concepts in Mediterranean Delights Ltd (“MDL”).

Profit: From last year EBIT for MDL has been £5 million. The goods and services of

Mediterranean Delights Ltd were on reasonable request and revenues in the year was 50 million

pounds. The aggregate profits and earnings of the firm are well-functioning according to last

year's data (Laitinen, 2013). But perhaps the obstacle for the firm is the growing debt, i.e. this

was 16 million pounds previously but now 18 million pounds. The business decides to take

measures to identify the best framework for resources and make efforts to limit its obligations.

Wade the manager, believes that they would like further capital. But this could be hard for him,

since it is very difficult to raise cash by equity, since they would pay higher yields for investing

in a rising debt firm due to the current significant risk factor. The higher debt rate becomes risky

for businesses because of increased interest costs that could reduce the competitiveness of MDL.

Cash flow: Currently, MDL has taken a 40 percent stake in a brunches and associated

products business. This also compensated £8 million of that same operating expenses in ahead of

time, out of £10 million. The above exchange will influence the cash Flow of the firm as the

profitability for payments paid in full is removed from MDL. Though, it only works if this

contract is a full cash transaction. This is generally found that neither company buys from the

internal money and normally takes credit from banks. It will be a threat for the firm because the

deficit is already growing, and new debt may even harder scenarios. Therefore, it is certainly not

wrong to buy a business if it is purchased without taking into consideration cost reductions there

3

are a few benefits for doing so. A further downside is that the current capital bought from the

firm often goes together with the transaction and thus enhances cash inflow.

Working capital: There are actually two debtors, i.e. Delios Ltd and San

Pedro Ltd. MDL offered Delios on a credit standard valued £ 1.5 million. Respective company

often struggles with San Pedro conflict of £ 2 million in deliveries. As a result, MDL accounts

receivable increases and thus no cash enters company that decreases the cash flow and thus

negatively affects the profitability and financial state of the business.

3. Recommend steps to improve company’s cashflow

From the cash study, it is determined that MDL has been facing number of issues which

impact the cash flow. So proper measures must be provided to improve the profitability of

company. These are discussed underneath:

Managing payable and receivable: MDL can successfully manage the investors by

growing liquidity as capital stays in the business for a longer period. They could thus

demand the suppliers to repay for the products which are purchased on credit basis. As a

results this will improves their operational investment cycle (Finger and El Benni, 2014).

Tight policies for debtors: Mediterranean Delights Ltd still has very stringent demands

on its mortgage holders' dues, but they still have to be really rigid and take measures and

get Delios Ltd as well as other debtors' capital. As they can provide overpayment

opportunities to creditor. The firm must also overcome the San Pedro dispute as a matter

of urgency which help to increase the cash flow.

Assessing the debt volume: MDL must consider cutting the loans and sometimes even

take out loans of interest quickly such that upcoming punishments can be avoided. This

aid to increase the working capital of company in respective accounting year.

4

firm often goes together with the transaction and thus enhances cash inflow.

Working capital: There are actually two debtors, i.e. Delios Ltd and San

Pedro Ltd. MDL offered Delios on a credit standard valued £ 1.5 million. Respective company

often struggles with San Pedro conflict of £ 2 million in deliveries. As a result, MDL accounts

receivable increases and thus no cash enters company that decreases the cash flow and thus

negatively affects the profitability and financial state of the business.

3. Recommend steps to improve company’s cashflow

From the cash study, it is determined that MDL has been facing number of issues which

impact the cash flow. So proper measures must be provided to improve the profitability of

company. These are discussed underneath:

Managing payable and receivable: MDL can successfully manage the investors by

growing liquidity as capital stays in the business for a longer period. They could thus

demand the suppliers to repay for the products which are purchased on credit basis. As a

results this will improves their operational investment cycle (Finger and El Benni, 2014).

Tight policies for debtors: Mediterranean Delights Ltd still has very stringent demands

on its mortgage holders' dues, but they still have to be really rigid and take measures and

get Delios Ltd as well as other debtors' capital. As they can provide overpayment

opportunities to creditor. The firm must also overcome the San Pedro dispute as a matter

of urgency which help to increase the cash flow.

Assessing the debt volume: MDL must consider cutting the loans and sometimes even

take out loans of interest quickly such that upcoming punishments can be avoided. This

aid to increase the working capital of company in respective accounting year.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART B

Executive summary

The below report summaries the actual purpose of making budgets including traditional

and alternative budgeting approaches. It also covers the application of these different budgets

applied to Second Sight Plc and proper recommendation which help in getting over the future

targets.

i) Understating of budget formation

The planning of the budget has become an important aspect to plan and measure results

(Mazikana, 2019). The budget is designed for three main purposes like forecasting the company's

revenue, expenses and profits and helping to take strategic decisions on the market and

ultimately assessing and tracking the company's performance.

a) Traditional budgeting approaches:

All those spending plans which are formulated with traditional procedure that idly

includes last year budgeted information in order to plan for future income and expenses. Thus in

traditional budgeting previous budgets are consider base which support to predicts the income,

profit and sales and make proper adjustments to increase the profitability in current or future

year. Some of important advantages and disadvantages are discussed underneath:

Advantages: This budgets is simple, systematic and less time taken to formulate and

implement. This is because in current year budgets only few changes are made mainly on areas

which are non productive in previous year. Most importantly traditional budget ease the process

of taking loan from bank as company can easily present the income and expenses throughout the

year. It also support company to eliminate the unproductive operation due to which operating

cost are higher and make better plan to increase profit.

Disadvantages: This expenditure plan takes too long and money for administrators and is

wasteful at many-times due to additional activity coming in the action. As the executives have

too many of the right numbers, the key reason for planning a proposal is often overlooked in the

competitive emphasis (Buck and et. al., 2013).

b) Alternative budget methods:

Rolling budgets:

5

Executive summary

The below report summaries the actual purpose of making budgets including traditional

and alternative budgeting approaches. It also covers the application of these different budgets

applied to Second Sight Plc and proper recommendation which help in getting over the future

targets.

i) Understating of budget formation

The planning of the budget has become an important aspect to plan and measure results

(Mazikana, 2019). The budget is designed for three main purposes like forecasting the company's

revenue, expenses and profits and helping to take strategic decisions on the market and

ultimately assessing and tracking the company's performance.

a) Traditional budgeting approaches:

All those spending plans which are formulated with traditional procedure that idly

includes last year budgeted information in order to plan for future income and expenses. Thus in

traditional budgeting previous budgets are consider base which support to predicts the income,

profit and sales and make proper adjustments to increase the profitability in current or future

year. Some of important advantages and disadvantages are discussed underneath:

Advantages: This budgets is simple, systematic and less time taken to formulate and

implement. This is because in current year budgets only few changes are made mainly on areas

which are non productive in previous year. Most importantly traditional budget ease the process

of taking loan from bank as company can easily present the income and expenses throughout the

year. It also support company to eliminate the unproductive operation due to which operating

cost are higher and make better plan to increase profit.

Disadvantages: This expenditure plan takes too long and money for administrators and is

wasteful at many-times due to additional activity coming in the action. As the executives have

too many of the right numbers, the key reason for planning a proposal is often overlooked in the

competitive emphasis (Buck and et. al., 2013).

b) Alternative budget methods:

Rolling budgets:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The expenditure rolling is indeed a sort of continually getting organized program. This

essentially includes reviewing the budget and planning new proposals for the next cycle. Thus, it

is stated that ones the old budgets get expired a new plan is prepared to get implemented.

Advantages: The revolving budget lets action plan quick instead of lengthy-term so

effectively preparing. This reduces the volatility in the program. Managers is also strategically

saving on savings and it can be easily adapted to market changes with this strategy.

Disadvantages: The budget's major weakness is that it's not available all year round and it

will only be modified incrementally. The workers can also become demoralized as when the

goals change frequently (Hofstede, 2012). This plan requires more time and cost to get prepared

and implemented.

Zero based budgets:

Zero-based budgets are plans designed by conception as well as for the fiscal year a

totally new program is being planned. This forecasts the company's entire profitability and

investments once more for forecasting or preparing the future growth expenditures and profits.

Advantages: The budget is more comprehensive because it gives a clear understanding of

all spending, since each functioning agency will take a close look at its expenditures. It also adds

to increasing unnecessary expenses and events.

Disadvantages: This budget requires more and more time and good strength of worker

are engaged to prepare ZBB. This also increase cost for company as entire member engaged on

ZBB required specific training and guideline which make easier for them to analyse each product

line of company.

Activity-based budgets

This spending plan is prepared by considering the method of activity costing. As a results it

includes entire overhead costs in order to make sure which activity are better and profitable.

Advantages: It allows the company to stay competitive throughout the sector and supports

the analysis of all costs of each commercial activity.

Disadvantages: It ensures that the different risks incurring by companies are well known.

The approach is dynamic in nature which needs a lot of corporate resources and energy (Cardoş,

2014).

ii) Implanting of methods and cost management

Second Sight Plc is an international company which produces prescription

6

essentially includes reviewing the budget and planning new proposals for the next cycle. Thus, it

is stated that ones the old budgets get expired a new plan is prepared to get implemented.

Advantages: The revolving budget lets action plan quick instead of lengthy-term so

effectively preparing. This reduces the volatility in the program. Managers is also strategically

saving on savings and it can be easily adapted to market changes with this strategy.

Disadvantages: The budget's major weakness is that it's not available all year round and it

will only be modified incrementally. The workers can also become demoralized as when the

goals change frequently (Hofstede, 2012). This plan requires more time and cost to get prepared

and implemented.

Zero based budgets:

Zero-based budgets are plans designed by conception as well as for the fiscal year a

totally new program is being planned. This forecasts the company's entire profitability and

investments once more for forecasting or preparing the future growth expenditures and profits.

Advantages: The budget is more comprehensive because it gives a clear understanding of

all spending, since each functioning agency will take a close look at its expenditures. It also adds

to increasing unnecessary expenses and events.

Disadvantages: This budget requires more and more time and good strength of worker

are engaged to prepare ZBB. This also increase cost for company as entire member engaged on

ZBB required specific training and guideline which make easier for them to analyse each product

line of company.

Activity-based budgets

This spending plan is prepared by considering the method of activity costing. As a results it

includes entire overhead costs in order to make sure which activity are better and profitable.

Advantages: It allows the company to stay competitive throughout the sector and supports

the analysis of all costs of each commercial activity.

Disadvantages: It ensures that the different risks incurring by companies are well known.

The approach is dynamic in nature which needs a lot of corporate resources and energy (Cardoş,

2014).

ii) Implanting of methods and cost management

Second Sight Plc is an international company which produces prescription

6

glasses and sunglasses for a number of leading international brands. The company

headquarter is in Manchester and have production centre in UK and France. The company

reported profits of 250 million pounds the year before. The organization seeks to spend and open

a new facility in the Netherlands with an Indian company as a Joint venture. The following are

defined budgetary topic which are applied to Second Sight Plc:

Traditional budgeting: This financial planning strategy is based primarily on estimates

and last year's financial side. It is recognized that a traditional method to expenditure forecasts

helps to build continuity in an operational sense. It centralizes the cost predictions and helps

bookkeepers build a suitable cost identification framework. In the conventional budget process

the accountant has used where estimates are based on the financial performance of the last year.

The last full year's income is projected to be £250 million. In the process of designing the

program, the sales projections must be taken into account through the incorporation new outlets

with Indian company in a new market of Neatherland.

Alternative budgets: The alternative monetary procedure primarily helps maintain the

genuineness of current operations and estimates. The prediction is based primarily on realistic

adjustments and developments with sophisticated forecasting instruments. Different methods are

explored in alternate budgeting. The transaction and expenditure formation method change

primarily according to the proposed amendments in the rolling spending plan. The budget

formulation is suggested from the above case primarily because of growth and expansion.

Budget rolling is known as a possible tool for money management business development

programs. Enhanced personnel costs, repairs of boats, depreciation costs, taxes and costs.

Another alternative approach in which companies can use the alternate expenditure method is the

zero-based strategy (Pais and Gama, 2015). A new budget for expanded market can be produced

through clients at the initial stage. It allows not only to preserve a legal framework in which risks

are weighed, but also to evaluate differences and improvements at the final stage.

iii) Evaluation of traditional or alternative budgetary system

Second Sight Plc form now onwards must implement the alternative budget prcoess in order to

plan for future income and expenses. This is because there are different reason which makes

alternative budgeting more effective. Such as:

This aid in connecting and positioning the income and expenses of Second Sight Plc such

as in the respective scenario expansion strategy might be suitable for the yearly budget.

7

headquarter is in Manchester and have production centre in UK and France. The company

reported profits of 250 million pounds the year before. The organization seeks to spend and open

a new facility in the Netherlands with an Indian company as a Joint venture. The following are

defined budgetary topic which are applied to Second Sight Plc:

Traditional budgeting: This financial planning strategy is based primarily on estimates

and last year's financial side. It is recognized that a traditional method to expenditure forecasts

helps to build continuity in an operational sense. It centralizes the cost predictions and helps

bookkeepers build a suitable cost identification framework. In the conventional budget process

the accountant has used where estimates are based on the financial performance of the last year.

The last full year's income is projected to be £250 million. In the process of designing the

program, the sales projections must be taken into account through the incorporation new outlets

with Indian company in a new market of Neatherland.

Alternative budgets: The alternative monetary procedure primarily helps maintain the

genuineness of current operations and estimates. The prediction is based primarily on realistic

adjustments and developments with sophisticated forecasting instruments. Different methods are

explored in alternate budgeting. The transaction and expenditure formation method change

primarily according to the proposed amendments in the rolling spending plan. The budget

formulation is suggested from the above case primarily because of growth and expansion.

Budget rolling is known as a possible tool for money management business development

programs. Enhanced personnel costs, repairs of boats, depreciation costs, taxes and costs.

Another alternative approach in which companies can use the alternate expenditure method is the

zero-based strategy (Pais and Gama, 2015). A new budget for expanded market can be produced

through clients at the initial stage. It allows not only to preserve a legal framework in which risks

are weighed, but also to evaluate differences and improvements at the final stage.

iii) Evaluation of traditional or alternative budgetary system

Second Sight Plc form now onwards must implement the alternative budget prcoess in order to

plan for future income and expenses. This is because there are different reason which makes

alternative budgeting more effective. Such as:

This aid in connecting and positioning the income and expenses of Second Sight Plc such

as in the respective scenario expansion strategy might be suitable for the yearly budget.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Furthermore Balance Scorecard techniques may be implemented to review the prepared

budget.

Moreover, rolling budget is more effective than fixed plans as they can be modified and

altered according to the need of business task, market condition as well as economic

circumstances. It can be altered on monthly, weekly basis and make easier for manager to

focus on short-term goals.

Second Sight Plc can also reduce project details and make them more descriptive and

compatible with the key performance metrics (Hofstede, 2012). Traditional plans are

highly detailed and KPIs can shift their emphasis. This will also permit decentralization

in the decision-making process and will therefore make the budget clearer for everybody.

8

budget.

Moreover, rolling budget is more effective than fixed plans as they can be modified and

altered according to the need of business task, market condition as well as economic

circumstances. It can be altered on monthly, weekly basis and make easier for manager to

focus on short-term goals.

Second Sight Plc can also reduce project details and make them more descriptive and

compatible with the key performance metrics (Hofstede, 2012). Traditional plans are

highly detailed and KPIs can shift their emphasis. This will also permit decentralization

in the decision-making process and will therefore make the budget clearer for everybody.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Kuusi, T., 2015. Alternatives for measuring structural budgetary position.

Ofei-Mensah, A. and Bennett, J., 2013. Transaction costs of alternative greenhouse gas policies

in the Australian transport energy sector. Ecological Economics. 88. pp.214-221.

Blaak, M., Openjuru, G. L. and Zeelen, J., 2013. Non-formal vocational education in Uganda:

Practical empowerment through a workable alternative. International Journal of

Educational Development. 33(1). pp.88-97.

Laitinen, E. K., 2013. Financial and non-financial variables in predicting failure of small

business reorganisation. International Journal of Accounting and Finance. 4(1). pp.1-34.

Finger, R. and El Benni, N., 2014. Alternative specifications of reference income levels in the

income stabilization tool. In Agricultural Cooperative Management and Policy (pp. 65-

85). Springer, Cham.

Mazikana, A. T., 2019. The Effect of Budgetary Controls on the Performance of an

Organization. Available at SSRN 3445247.

Buck, N. and et. al., 2013. Working Capital: life and labour in contemporary London.

Routledge.

Hofstede, G. H., 2012. The game of budget control. Routledge.

Cardoş, I. R., 2014. New trends in budgeting–a literature review. SEA–Practical Application of

Science. 2(04). pp.483-489.

Pais, M. A. and Gama, P. M., 2015. Working capital management and SMEs profitability:

Portuguese evidence. International Journal of Managerial Finance. 11(3). pp.341-358.

9

Books and Journals:

Kuusi, T., 2015. Alternatives for measuring structural budgetary position.

Ofei-Mensah, A. and Bennett, J., 2013. Transaction costs of alternative greenhouse gas policies

in the Australian transport energy sector. Ecological Economics. 88. pp.214-221.

Blaak, M., Openjuru, G. L. and Zeelen, J., 2013. Non-formal vocational education in Uganda:

Practical empowerment through a workable alternative. International Journal of

Educational Development. 33(1). pp.88-97.

Laitinen, E. K., 2013. Financial and non-financial variables in predicting failure of small

business reorganisation. International Journal of Accounting and Finance. 4(1). pp.1-34.

Finger, R. and El Benni, N., 2014. Alternative specifications of reference income levels in the

income stabilization tool. In Agricultural Cooperative Management and Policy (pp. 65-

85). Springer, Cham.

Mazikana, A. T., 2019. The Effect of Budgetary Controls on the Performance of an

Organization. Available at SSRN 3445247.

Buck, N. and et. al., 2013. Working Capital: life and labour in contemporary London.

Routledge.

Hofstede, G. H., 2012. The game of budget control. Routledge.

Cardoş, I. R., 2014. New trends in budgeting–a literature review. SEA–Practical Application of

Science. 2(04). pp.483-489.

Pais, M. A. and Gama, P. M., 2015. Working capital management and SMEs profitability:

Portuguese evidence. International Journal of Managerial Finance. 11(3). pp.341-358.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.