Business Finance Report: Performance Analysis, Cash and Budgeting

VerifiedAdded on 2023/01/05

|12

|3647

|40

Report

AI Summary

This business finance report provides a detailed analysis of T shirts Ltd.'s financial performance using income statements and balance sheets from 2018 and 2019. It examines key financial ratios such as interest coverage, operating profit margin, current ratio, debt-to-equity ratio, and earnings per share to assess the company's profitability, liquidity, and solvency. The report also contrasts accrual versus cash accounting methods, highlighting the differences between profit and cash flow, and discusses the importance of budgeting in business. Furthermore, it explores the benefits of forming a limited company and listing it on the stock exchange. Desklib offers this and many other solved assignments for students.

Business Finance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Part 1 Business Performance Analysis............................................................................................3

1.1 Analysis of statement of Profit or Loss............................................................................3

1.2 Analysis of statement of Financial Position.....................................................................4

Part 2 Understanding Financial Information and cash management...............................................5

2.1 Concept of Accrual accounting versus cash accounting..................................................5

2.2 Difference between profit and cash flow..........................................................................6

Part 3 Budget and Company Finance...............................................................................................7

3.1 Budget and purposes of preparing a budget.....................................................................7

3.2 Benefits of forming a limited company and listing it on stock exchange........................8

Appendices.....................................................................................................................................10

Supporting Calculations.......................................................................................................10

Bibliography.........................................................................................................................12

2

Part 1 Business Performance Analysis............................................................................................3

1.1 Analysis of statement of Profit or Loss............................................................................3

1.2 Analysis of statement of Financial Position.....................................................................4

Part 2 Understanding Financial Information and cash management...............................................5

2.1 Concept of Accrual accounting versus cash accounting..................................................5

2.2 Difference between profit and cash flow..........................................................................6

Part 3 Budget and Company Finance...............................................................................................7

3.1 Budget and purposes of preparing a budget.....................................................................7

3.2 Benefits of forming a limited company and listing it on stock exchange........................8

Appendices.....................................................................................................................................10

Supporting Calculations.......................................................................................................10

Bibliography.........................................................................................................................12

2

Part 1 Business Performance Analysis

1.1 Analysis of statement of Profit or Loss

Statement of financial performance or income statement as it is popularly called, is one of

the final statements of the company which tells about its financial performance over a period of

time (Chandra, 2017). It is a statement of accounting summary of all of a company’s revenues

and expenses. It includes revenue earned from sales and other sources as well as operating

expenses, cost of goods sold, other expenses to result in net income for the organisation. Net

income can be both positive or negative i.e. can result in both profit or loss for the organisation.

To analyse financial performance of T shirts Ltd., summary income statement of the

company has been assessed and the first thing that is looked at is its revenue, profits and

margins. In the first look, it can be said that company has registered a decrease from £2,101,000

in 2018 to £1,366,000 in 2019 in its revenue which could be due to less demand due to instability

in economic environment. It has reduced its cost of sales from earlier year, which has helped it in

registering lesser reduction in gross profit. Moving forward, it has registered in increase in

operating expenses but since the increment does not look exceptional, it could be due to regular

increase in the operational cost like marketing and promotions to increase sales. Company has

registered a loss in 2019 before interest and tax which was at profitable state in previous year.

Company has registered more than 1.5 times increase in finance cost which shows that company

has taken new debt at higher rates this year. Resulting is net loss in 2019 which was at profitable

state in 2018. This loss would have been adjusted in retained earnings. No information had been

provided about dividend policy of the T shirts Ltd. To have a better comparative analysis of

financial performance of two years, various financial ratios are mentioned below:

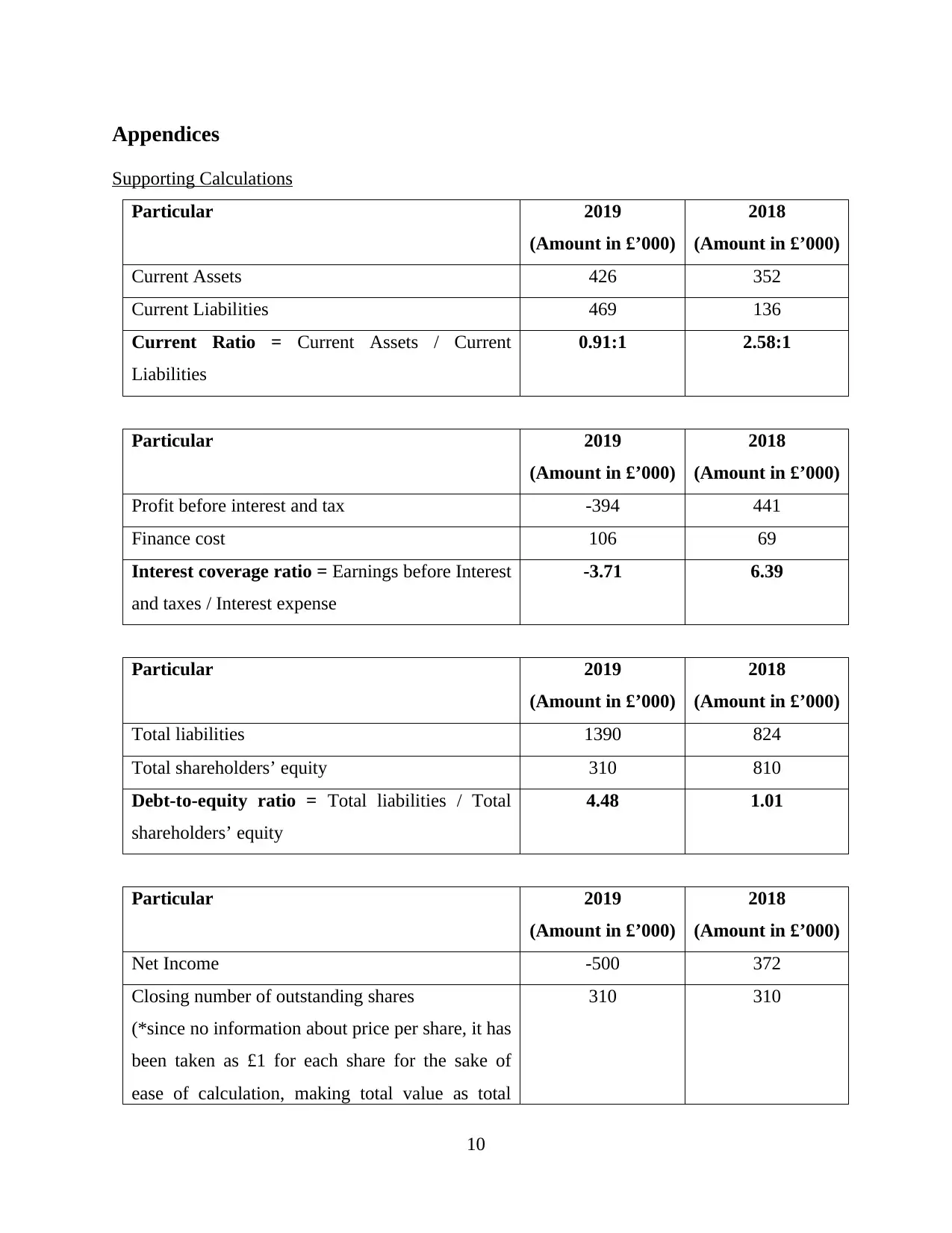

Interest coverage ratio – It is a solvency cum coverage ratio which is used to assess

company’s ability to meet its finance cost from its earnings (Greenbaum, Thakor and

Boot, 2019). Higher the ratio, better it is for company. T shirt Ltd. has reported 3.71

times interest coverage ability in 2019 while in 2018, it was 6.39 times. Reduction can be

owed to the high finance cost of bank overdraft which was absent in 2018 and also loan

amount has also increased which would be having interest cost. And, this should also not

be ignored that in 2019 company does not have profits to cover finance cost from it like

in 2018.

3

1.1 Analysis of statement of Profit or Loss

Statement of financial performance or income statement as it is popularly called, is one of

the final statements of the company which tells about its financial performance over a period of

time (Chandra, 2017). It is a statement of accounting summary of all of a company’s revenues

and expenses. It includes revenue earned from sales and other sources as well as operating

expenses, cost of goods sold, other expenses to result in net income for the organisation. Net

income can be both positive or negative i.e. can result in both profit or loss for the organisation.

To analyse financial performance of T shirts Ltd., summary income statement of the

company has been assessed and the first thing that is looked at is its revenue, profits and

margins. In the first look, it can be said that company has registered a decrease from £2,101,000

in 2018 to £1,366,000 in 2019 in its revenue which could be due to less demand due to instability

in economic environment. It has reduced its cost of sales from earlier year, which has helped it in

registering lesser reduction in gross profit. Moving forward, it has registered in increase in

operating expenses but since the increment does not look exceptional, it could be due to regular

increase in the operational cost like marketing and promotions to increase sales. Company has

registered a loss in 2019 before interest and tax which was at profitable state in previous year.

Company has registered more than 1.5 times increase in finance cost which shows that company

has taken new debt at higher rates this year. Resulting is net loss in 2019 which was at profitable

state in 2018. This loss would have been adjusted in retained earnings. No information had been

provided about dividend policy of the T shirts Ltd. To have a better comparative analysis of

financial performance of two years, various financial ratios are mentioned below:

Interest coverage ratio – It is a solvency cum coverage ratio which is used to assess

company’s ability to meet its finance cost from its earnings (Greenbaum, Thakor and

Boot, 2019). Higher the ratio, better it is for company. T shirt Ltd. has reported 3.71

times interest coverage ability in 2019 while in 2018, it was 6.39 times. Reduction can be

owed to the high finance cost of bank overdraft which was absent in 2018 and also loan

amount has also increased which would be having interest cost. And, this should also not

be ignored that in 2019 company does not have profits to cover finance cost from it like

in 2018.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

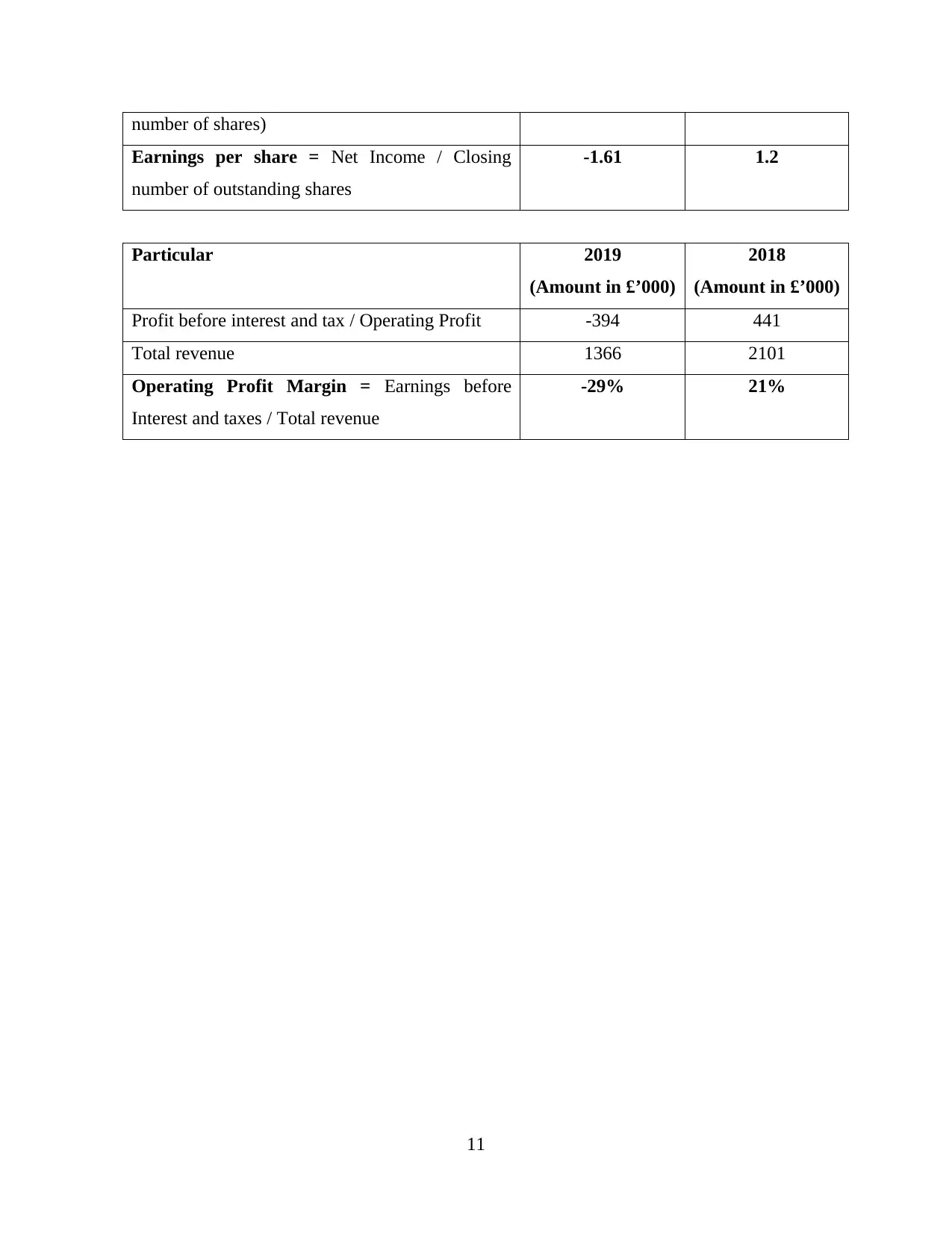

Operating profit margin – It is a profitability ratio which assess a company’s efficiency

of generating profit on sales after paying of variable cost of production. T shirt Ltd had

reported operating profit margin of 21% in 2018 while in 2019, it has a operating loss

margin of 29% owing to factors discussed above.

1.2 Analysis of statement of Financial Position

Statement of financial position or Balance Sheet as it is popularly called is another final

statement of a company which reflects financial position of a company at a certain point of time

(Fazzini, 2018). It includes financial performance of business assets, liabilities and shareholders’

equity in the manner that assets are equivalent to latter two. Net income determined in income

statement becomes part of the shareholders’ equity.

To analyse financial position of T shirts Ltd., its statement of financial position has been

assessed. From first assessment, it can be seen that there is reduction in book value of fixed

assets which is supposedly owed to depreciation. Closing inventory balance has increased,

probably due to lesser demand and reduced sales, which means company has unutilised

inventory balance lying in its warehouse. It needs to increase its promotional measures otherwise

it will have obsolete stock soon. It is reported that company has relaxed its credit policy to attract

more customers which is being reflected in increment in accounts receivables from previous

year. Strange fact is that company has reported no cash and cash equivalents in 2019 which is not

a good sign for liquidity of the company. Company has reported same share capital both the

years which means that no new capital has been issued in 2019 by T shirts Ltd. Company had

reported closing balance of £500 of retained earnings in 2018 which must have been utilised to

square off the loss generated this year. Hence, this year’s retained earnings balance is zero. Long

term borrowings have also increased from 2018 which means new loans have been acquired in

2019. Trade payables have also increased but by looking at the percentage of increase, it seems

in regular business course. In year 2019, it has also reported availing bank overdraft which is at

much higher rate than loans as per information provided, which was being reflected in higher

finance cost in income statement. To have a better comparative analysis of financial position of

two years of T shirts Ltd, below mentioned financial ratios have been determined:

Current ratio – It is a liquidity ratio which is used to assess efficiency of its working

capital (Samonas, 2015). Higher the ratio, better it is for liquidity of the company. T

shirts Ltd. has a reported current ratio of 2.58:1 in 2018 while in 2019, it slipped to only

4

of generating profit on sales after paying of variable cost of production. T shirt Ltd had

reported operating profit margin of 21% in 2018 while in 2019, it has a operating loss

margin of 29% owing to factors discussed above.

1.2 Analysis of statement of Financial Position

Statement of financial position or Balance Sheet as it is popularly called is another final

statement of a company which reflects financial position of a company at a certain point of time

(Fazzini, 2018). It includes financial performance of business assets, liabilities and shareholders’

equity in the manner that assets are equivalent to latter two. Net income determined in income

statement becomes part of the shareholders’ equity.

To analyse financial position of T shirts Ltd., its statement of financial position has been

assessed. From first assessment, it can be seen that there is reduction in book value of fixed

assets which is supposedly owed to depreciation. Closing inventory balance has increased,

probably due to lesser demand and reduced sales, which means company has unutilised

inventory balance lying in its warehouse. It needs to increase its promotional measures otherwise

it will have obsolete stock soon. It is reported that company has relaxed its credit policy to attract

more customers which is being reflected in increment in accounts receivables from previous

year. Strange fact is that company has reported no cash and cash equivalents in 2019 which is not

a good sign for liquidity of the company. Company has reported same share capital both the

years which means that no new capital has been issued in 2019 by T shirts Ltd. Company had

reported closing balance of £500 of retained earnings in 2018 which must have been utilised to

square off the loss generated this year. Hence, this year’s retained earnings balance is zero. Long

term borrowings have also increased from 2018 which means new loans have been acquired in

2019. Trade payables have also increased but by looking at the percentage of increase, it seems

in regular business course. In year 2019, it has also reported availing bank overdraft which is at

much higher rate than loans as per information provided, which was being reflected in higher

finance cost in income statement. To have a better comparative analysis of financial position of

two years of T shirts Ltd, below mentioned financial ratios have been determined:

Current ratio – It is a liquidity ratio which is used to assess efficiency of its working

capital (Samonas, 2015). Higher the ratio, better it is for liquidity of the company. T

shirts Ltd. has a reported current ratio of 2.58:1 in 2018 while in 2019, it slipped to only

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.91:1 which shows reduction in ability of company’s current assets to pay off its current

liabilities. It can be owed to the fact that company has availed bank overdraft of

significant amount to support its operations.

Debt-to-equity ratio – It is a solvency ratio which assess how much of company’s debt

can be funded by equity if need arises. Higher the ratio, more is likelihood of default. T

shirts Ltd has reported ratio of 4.48 in 2019 while in 2018, it was only 1.01 which can be

owed to both increase in current liabilities and decrease in equity due to retained earnings

used to adjust loss.

Earnings per share – It is a market prospect ratio i.e. it shows profitability of company in

relation to outstanding shares of the company (Cortesi and et.al., 2015). More the ratio,

better it is. T shirts Ltd. has reported EPS of positive 1.2 in 2018 while negative 1.6 in

2019 owing to loss faced by company as share capital is unchanged in both the years.

Part 2 Understanding Financial Information and cash management

2.1 Concept of Accrual accounting versus cash accounting

Below mentioned are two methods of accounting entries:

Accrual accounting – This method involves measuring and recording financial transactions

of business regardless of whether cash exchanges have been involved or not. It is based on

matching principle which says that all revenues and expenses should be recognised in the same

period in which either they become due or payment has been exchanged, whichever takes place

first. For example, T shirts Ltd has a total monthly sale of £100,000. Out of which, 60% is in

cash while 40% is on credit, payment of which will be received later. Company follows accrual

accounting and books sales from both modes to get a true picture of profit.

Benefits – Most important benefit of accrual accounting is that it gives an accurate

picture position of a company’s financial position by combining current cash flow with

certainly expected future cash flows (Gigli and Mariani, 2018). This clearer picture of

cash flows makes it easier for a manager of T-shirts Ltd to manage their present

operations and resources and helps in better future planning as well.

Limitations – This method is relatively complex and more expensive to adopt. It takes

time and skilled personnel to determine accrued benefits and make necessary adjustment

to the books of accounts. Also, it makes additional requirement for maintaining

5

liabilities. It can be owed to the fact that company has availed bank overdraft of

significant amount to support its operations.

Debt-to-equity ratio – It is a solvency ratio which assess how much of company’s debt

can be funded by equity if need arises. Higher the ratio, more is likelihood of default. T

shirts Ltd has reported ratio of 4.48 in 2019 while in 2018, it was only 1.01 which can be

owed to both increase in current liabilities and decrease in equity due to retained earnings

used to adjust loss.

Earnings per share – It is a market prospect ratio i.e. it shows profitability of company in

relation to outstanding shares of the company (Cortesi and et.al., 2015). More the ratio,

better it is. T shirts Ltd. has reported EPS of positive 1.2 in 2018 while negative 1.6 in

2019 owing to loss faced by company as share capital is unchanged in both the years.

Part 2 Understanding Financial Information and cash management

2.1 Concept of Accrual accounting versus cash accounting

Below mentioned are two methods of accounting entries:

Accrual accounting – This method involves measuring and recording financial transactions

of business regardless of whether cash exchanges have been involved or not. It is based on

matching principle which says that all revenues and expenses should be recognised in the same

period in which either they become due or payment has been exchanged, whichever takes place

first. For example, T shirts Ltd has a total monthly sale of £100,000. Out of which, 60% is in

cash while 40% is on credit, payment of which will be received later. Company follows accrual

accounting and books sales from both modes to get a true picture of profit.

Benefits – Most important benefit of accrual accounting is that it gives an accurate

picture position of a company’s financial position by combining current cash flow with

certainly expected future cash flows (Gigli and Mariani, 2018). This clearer picture of

cash flows makes it easier for a manager of T-shirts Ltd to manage their present

operations and resources and helps in better future planning as well.

Limitations – This method is relatively complex and more expensive to adopt. It takes

time and skilled personnel to determine accrued benefits and make necessary adjustment

to the books of accounts. Also, it makes additional requirement for maintaining

5

accounting receivables and payables. Therefore, many small businesses prefer cash

method of accounting.

Cash accounting – This method involves recognising, measuring and recording of

transactions only when payments are involved and exchanges. Therefore, this method of

accounting is preferred by small businesses while it is not suitable for large companies as it will

obscure their true financial position (Aleinikov, Kuter and Musaelyan, 2017). For example, a

sole trader has a monthly sale of £2000. Out of which, 80% is cash while 20% has been on

credit. Trader follows cash accounting method and records only cash sale, leaving entries for

credit sales as and when payment will be received, for the trader is only interested in knowing

cash in hand.

Benefits – It is simple and easy to implement method. There is no need to employ skilled

personnel to adopt this method and also, there is no need to track accounts receivable and

payables which makes accounting straightforward and easy to read. Therefore, small

businesses use it for they are only concerned the money they have in hand at the moment.

Limitations – Biggest limitation of this method is that it prevents reflection of true picture

of business-like liabilities that have been accrued but not yet paid for, are not accounted

for, giving out better position of the business than actually is. Since this method does not

reflect accurate and complete picture, it is not allowed to use by large companies like T

shirts Ltd with complex transactions under Generally Accepted Accounting Principles

(GAAP).

2.2 Difference between profit and cash flow

Profit – Profit or net income, is net balance remaining after deducting all operating

expenses of business from its revenues (Hogianto and Sebastian, 2019). It can either be

distributed among owners or reinvested back in the business. When expenses exceed revenues, it

is termed as loss for the business. It is determined from income statement which is divided into

three categories of profits – gross profit, operating profit and net profit.

Cash flow – Net balance of in and out movement of cash from a business at a specific

point of time is referred to as cash flow. Therefore, it can be both positive or negative. It is

reported in cash flow statement which is divided into three categories – operating, investing and

financing cash flow.

Basis of difference Profit Cash flow

6

method of accounting.

Cash accounting – This method involves recognising, measuring and recording of

transactions only when payments are involved and exchanges. Therefore, this method of

accounting is preferred by small businesses while it is not suitable for large companies as it will

obscure their true financial position (Aleinikov, Kuter and Musaelyan, 2017). For example, a

sole trader has a monthly sale of £2000. Out of which, 80% is cash while 20% has been on

credit. Trader follows cash accounting method and records only cash sale, leaving entries for

credit sales as and when payment will be received, for the trader is only interested in knowing

cash in hand.

Benefits – It is simple and easy to implement method. There is no need to employ skilled

personnel to adopt this method and also, there is no need to track accounts receivable and

payables which makes accounting straightforward and easy to read. Therefore, small

businesses use it for they are only concerned the money they have in hand at the moment.

Limitations – Biggest limitation of this method is that it prevents reflection of true picture

of business-like liabilities that have been accrued but not yet paid for, are not accounted

for, giving out better position of the business than actually is. Since this method does not

reflect accurate and complete picture, it is not allowed to use by large companies like T

shirts Ltd with complex transactions under Generally Accepted Accounting Principles

(GAAP).

2.2 Difference between profit and cash flow

Profit – Profit or net income, is net balance remaining after deducting all operating

expenses of business from its revenues (Hogianto and Sebastian, 2019). It can either be

distributed among owners or reinvested back in the business. When expenses exceed revenues, it

is termed as loss for the business. It is determined from income statement which is divided into

three categories of profits – gross profit, operating profit and net profit.

Cash flow – Net balance of in and out movement of cash from a business at a specific

point of time is referred to as cash flow. Therefore, it can be both positive or negative. It is

reported in cash flow statement which is divided into three categories – operating, investing and

financing cash flow.

Basis of difference Profit Cash flow

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Revenue generated Accrued revenue or the revenue

which gets due for the period gets

reflected in profit/loss statement

whether or not actually received.

Only those revenues which

have been realised in cash are

taken in cash flow.

Expenses incurred All the expenses which gets due in

the specified period irrespective of

the fact that whether they were paid

in the specified period or not are

taken into account while calculating

profit or loss.

Only those expenses which

gets paid in cash in specified

accounting period is taken in

consideration while preparing

cash flow statement.

Adequacy Adequate profits do not necessarily

mean that business is running with

adequate cash as it includes non-

cash expenses and revenues as well

(Ozerov and et.al., 2017).

Adequate cash flows do not

necessarily mean that business

is generating sufficient profits

as well for good cash flows

can be result of a successful

product which will increase

other expenses as well which

impacts profits.

Part 3 Budget and Company Finance

3.1 Budget and purposes of preparing a budget

A budget is a formal estimation of business transactions i.e. revenue and expenses for a

definite period of time in quantified terms. They are based on financial statements, cash flow

statement, company targets and market situation. Since, business environment is dynamic, a

company shall prepare flexible budgets which can be modified according to situational

requirements (Ehrhardt and Brigham, 2016). A company prepares various types of budgets

which are below mentioned:

7

which gets due for the period gets

reflected in profit/loss statement

whether or not actually received.

Only those revenues which

have been realised in cash are

taken in cash flow.

Expenses incurred All the expenses which gets due in

the specified period irrespective of

the fact that whether they were paid

in the specified period or not are

taken into account while calculating

profit or loss.

Only those expenses which

gets paid in cash in specified

accounting period is taken in

consideration while preparing

cash flow statement.

Adequacy Adequate profits do not necessarily

mean that business is running with

adequate cash as it includes non-

cash expenses and revenues as well

(Ozerov and et.al., 2017).

Adequate cash flows do not

necessarily mean that business

is generating sufficient profits

as well for good cash flows

can be result of a successful

product which will increase

other expenses as well which

impacts profits.

Part 3 Budget and Company Finance

3.1 Budget and purposes of preparing a budget

A budget is a formal estimation of business transactions i.e. revenue and expenses for a

definite period of time in quantified terms. They are based on financial statements, cash flow

statement, company targets and market situation. Since, business environment is dynamic, a

company shall prepare flexible budgets which can be modified according to situational

requirements (Ehrhardt and Brigham, 2016). A company prepares various types of budgets

which are below mentioned:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Master budget – This budget is compilation of all the departmental budgets and is

reflection of overall projections and forecasts for the entire company in that definite fiscal

year. It includes various budgets such as:

Operating budget – This budget includes the estimation of all revenues and expenses

that the company expects from its day-to-day business operations. It includes costs of

goods sold, overhead and administrative costs, etc. (Brealey and et.al., 2018)

Cash budget – This budget includes estimation of all inflows and outflows of cash

generated during the said period. It helps company streamline its payments according

to cash availability in the business.

Purposes of preparing a budget – Below mentioned are various purposes for which budgets

are prepared by the company:

Aids in planning and controlling – Primary purpose of preparing budgets is that it helps a

company plan and organise its activities for the specified period. Other than planning, it

also acts as standard or target for the monitoring and controlling function of the

management. Preparing budgets with a consistency over a long period of time helps them

stay aligned with their long-term financial goals.

Helps in responsibility fixation – As discussed earlier, budgets act as standard for

controlling. It helps managers in determining variances from the targets and fixing

responsibility of those who are accountable for the missed performance. Better control

helps fixing revenue leakages and increase in savings. This not only helps company in

employee management but also helps employees in developing their professional

capabilities.

Gain financial control – Budgets are prepared in numbers and helps a company gain

control over their finances (Argenti, 2018). When a company is able to exercise better

control over their finances, they are able to achieve their goals faster and have an

improvement in their net worth. Improved operational and financial performance reduces

stress over the resources of the company and minimise unnecessary financial arguments.

3.2 Benefits of forming a limited company and listing it on stock exchange

A limited company is a form of corporate business structure in which legal ownership of

company is separated from its shareholders and directors by conferring it a status of separate

legal entity. They are governed by the provisions stated under Companies Act and must

8

reflection of overall projections and forecasts for the entire company in that definite fiscal

year. It includes various budgets such as:

Operating budget – This budget includes the estimation of all revenues and expenses

that the company expects from its day-to-day business operations. It includes costs of

goods sold, overhead and administrative costs, etc. (Brealey and et.al., 2018)

Cash budget – This budget includes estimation of all inflows and outflows of cash

generated during the said period. It helps company streamline its payments according

to cash availability in the business.

Purposes of preparing a budget – Below mentioned are various purposes for which budgets

are prepared by the company:

Aids in planning and controlling – Primary purpose of preparing budgets is that it helps a

company plan and organise its activities for the specified period. Other than planning, it

also acts as standard or target for the monitoring and controlling function of the

management. Preparing budgets with a consistency over a long period of time helps them

stay aligned with their long-term financial goals.

Helps in responsibility fixation – As discussed earlier, budgets act as standard for

controlling. It helps managers in determining variances from the targets and fixing

responsibility of those who are accountable for the missed performance. Better control

helps fixing revenue leakages and increase in savings. This not only helps company in

employee management but also helps employees in developing their professional

capabilities.

Gain financial control – Budgets are prepared in numbers and helps a company gain

control over their finances (Argenti, 2018). When a company is able to exercise better

control over their finances, they are able to achieve their goals faster and have an

improvement in their net worth. Improved operational and financial performance reduces

stress over the resources of the company and minimise unnecessary financial arguments.

3.2 Benefits of forming a limited company and listing it on stock exchange

A limited company is a form of corporate business structure in which legal ownership of

company is separated from its shareholders and directors by conferring it a status of separate

legal entity. They are governed by the provisions stated under Companies Act and must

8

necessarily be incorporated at Companies House in UK. There are three types of limited

companies in UK – private company limited by shares, private company limited by guarantee

and public limited company.

Benefits of forming a limited company – Below mentioned are benefits of forming a

limited company:

Separate legal entity – A limited company is separate from its owners i.e. it can enter into

contracts on its own name and can sue or be sued for it. It gives it legal right to earn and

keep the profits earned from its operations (Miley, 2018).

Limited liability – Separate legal entity makes a company responsible for squaring its

own debts and liabilities and in case, the company fails to pay its liabilities, owners and

directors are not held personally responsible to pay off those liabilities. They will only be

responsible up to the amount which unpaid on shares subscribed or the guarantee they

have made on behalf of the company.

Finance options – Other than share capital, companies often find it easier to look for

better sources of finance than other business forms. For example, it can go for stock

exchange listing or can get corporate debt, etc.

Benefits of listing on stock exchange – Below mentioned are benefits of listing a company

on a stock exchange:

Raising capital through public issue of shares – Post listing a company on any stock

exchange, it can sell its shares to the public and anyone can invest in the company shares

which help it raise much larger capital than any other business organisation form.

Widening the shareholder base – Companies listed on stock exchanges have wide

shareholder base, it helps spread the risk of ownership to large number of investors with

no single pressure group mounting pressure over management to influence decision-

making (Ehrhardt and Brigham, 2016).

Growth and expansion opportunities – Listing on a stock exchange not only provide

better finance opportunities but also enables wider market reach to improve its chances of

growth and expansion by pursuing new projects, make acquisitions, etc.

9

companies in UK – private company limited by shares, private company limited by guarantee

and public limited company.

Benefits of forming a limited company – Below mentioned are benefits of forming a

limited company:

Separate legal entity – A limited company is separate from its owners i.e. it can enter into

contracts on its own name and can sue or be sued for it. It gives it legal right to earn and

keep the profits earned from its operations (Miley, 2018).

Limited liability – Separate legal entity makes a company responsible for squaring its

own debts and liabilities and in case, the company fails to pay its liabilities, owners and

directors are not held personally responsible to pay off those liabilities. They will only be

responsible up to the amount which unpaid on shares subscribed or the guarantee they

have made on behalf of the company.

Finance options – Other than share capital, companies often find it easier to look for

better sources of finance than other business forms. For example, it can go for stock

exchange listing or can get corporate debt, etc.

Benefits of listing on stock exchange – Below mentioned are benefits of listing a company

on a stock exchange:

Raising capital through public issue of shares – Post listing a company on any stock

exchange, it can sell its shares to the public and anyone can invest in the company shares

which help it raise much larger capital than any other business organisation form.

Widening the shareholder base – Companies listed on stock exchanges have wide

shareholder base, it helps spread the risk of ownership to large number of investors with

no single pressure group mounting pressure over management to influence decision-

making (Ehrhardt and Brigham, 2016).

Growth and expansion opportunities – Listing on a stock exchange not only provide

better finance opportunities but also enables wider market reach to improve its chances of

growth and expansion by pursuing new projects, make acquisitions, etc.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Appendices

Supporting Calculations

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Current Assets 426 352

Current Liabilities 469 136

Current Ratio = Current Assets / Current

Liabilities

0.91:1 2.58:1

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Profit before interest and tax -394 441

Finance cost 106 69

Interest coverage ratio = Earnings before Interest

and taxes / Interest expense

-3.71 6.39

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Total liabilities 1390 824

Total shareholders’ equity 310 810

Debt-to-equity ratio = Total liabilities / Total

shareholders’ equity

4.48 1.01

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Net Income -500 372

Closing number of outstanding shares

(*since no information about price per share, it has

been taken as £1 for each share for the sake of

ease of calculation, making total value as total

310 310

10

Supporting Calculations

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Current Assets 426 352

Current Liabilities 469 136

Current Ratio = Current Assets / Current

Liabilities

0.91:1 2.58:1

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Profit before interest and tax -394 441

Finance cost 106 69

Interest coverage ratio = Earnings before Interest

and taxes / Interest expense

-3.71 6.39

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Total liabilities 1390 824

Total shareholders’ equity 310 810

Debt-to-equity ratio = Total liabilities / Total

shareholders’ equity

4.48 1.01

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Net Income -500 372

Closing number of outstanding shares

(*since no information about price per share, it has

been taken as £1 for each share for the sake of

ease of calculation, making total value as total

310 310

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

number of shares)

Earnings per share = Net Income / Closing

number of outstanding shares

-1.61 1.2

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Profit before interest and tax / Operating Profit -394 441

Total revenue 1366 2101

Operating Profit Margin = Earnings before

Interest and taxes / Total revenue

-29% 21%

11

Earnings per share = Net Income / Closing

number of outstanding shares

-1.61 1.2

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Profit before interest and tax / Operating Profit -394 441

Total revenue 1366 2101

Operating Profit Margin = Earnings before

Interest and taxes / Total revenue

-29% 21%

11

Bibliography

Books and Journal

Aleinikov, D., Kuter, M. and Musaelyan, A., 2017, December. The early cash account books.

In International Conference on Information Technology Science (pp. 195-207).

Springer, Cham.

Argenti, J., 2018. Practical corporate planning. Routledge.

Brealey, R.A. and et.al., 2018. Principles of Corporate Finance, 12/e (Vol. 12). McGraw-Hill

Education.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-hill education.

Cortesi, A. and et.al., 2015. Advanced Financial Accounting: Financial Statement Analysis–

Accounting Issues–Group Accounts. EGEA spa.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

learning.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

learning.

Fazzini, M., 2018. Financial Statement Analysis. In Business Valuation (pp. 39-76). Palgrave

Macmillan, Cham.

Gigli, S. and Mariani, L., 2018. Lost in the transition from cash to accrual

accounting. International Journal of Public Sector Management.

Greenbaum, S.I., Thakor, A.V. and Boot, A.W., 2019. Contemporary financial intermediation.

Academic Press.

Hogianto, W. and Sebastian, H., 2019. Use of Profit and Cash Flow to Predict the Condition of

Financial Distress. Available at SSRN 3319862.

Miley, V., 2018. Budget cuts hit corporate oversight. Green Left Weekly. (1181). p.9.

Ozerov, E.S. and et.al., 2017, September. Selecting the best use option for assets in a corporate

management system. In 2017 6th International Conference on Reliability, Infocom

Technologies and Optimization (Trends and Future Directions)(ICRITO) (pp. 162-170).

IEEE.

Samonas, M., 2015. Financial forecasting, analysis, and modelling: a framework for long-term

forecasting. John Wiley & Sons.

12

Books and Journal

Aleinikov, D., Kuter, M. and Musaelyan, A., 2017, December. The early cash account books.

In International Conference on Information Technology Science (pp. 195-207).

Springer, Cham.

Argenti, J., 2018. Practical corporate planning. Routledge.

Brealey, R.A. and et.al., 2018. Principles of Corporate Finance, 12/e (Vol. 12). McGraw-Hill

Education.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-hill education.

Cortesi, A. and et.al., 2015. Advanced Financial Accounting: Financial Statement Analysis–

Accounting Issues–Group Accounts. EGEA spa.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

learning.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

learning.

Fazzini, M., 2018. Financial Statement Analysis. In Business Valuation (pp. 39-76). Palgrave

Macmillan, Cham.

Gigli, S. and Mariani, L., 2018. Lost in the transition from cash to accrual

accounting. International Journal of Public Sector Management.

Greenbaum, S.I., Thakor, A.V. and Boot, A.W., 2019. Contemporary financial intermediation.

Academic Press.

Hogianto, W. and Sebastian, H., 2019. Use of Profit and Cash Flow to Predict the Condition of

Financial Distress. Available at SSRN 3319862.

Miley, V., 2018. Budget cuts hit corporate oversight. Green Left Weekly. (1181). p.9.

Ozerov, E.S. and et.al., 2017, September. Selecting the best use option for assets in a corporate

management system. In 2017 6th International Conference on Reliability, Infocom

Technologies and Optimization (Trends and Future Directions)(ICRITO) (pp. 162-170).

IEEE.

Samonas, M., 2015. Financial forecasting, analysis, and modelling: a framework for long-term

forecasting. John Wiley & Sons.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.