Business Performance Analysis Report - Finance Module, 2023

VerifiedAdded on 2023/01/04

|13

|3512

|32

Report

AI Summary

This report provides a comprehensive analysis of business performance, focusing on financial statements, including the profit and loss statement and the statement of financial position. It delves into key financial concepts such as accrual accounting versus cash accounting, and the critical differences between profit and cash flow. The report also examines budgeting and its purposes in company finance, including the benefits of forming a limited company and listing it on a stock exchange. The analysis utilizes financial ratios like the interest coverage ratio, operating profit margin, current ratio, and debt-to-equity ratio to assess the financial health of a hypothetical company, T Shirts Ltd. The report highlights the importance of financial planning, cash management, and understanding the relationship between profitability and cash flow for effective business decision-making. The analysis includes supporting calculations and aims to provide a clear overview of the company's financial performance over a two-year period, offering insights into its strengths, weaknesses, and potential areas for improvement. The report concludes by emphasizing the significance of financial ratios in evaluating the firm's performance.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Part 1 Business Performance Analysis............................................................................................3

1.1 Analysis of statement of Profit or Loss............................................................................3

1.2 Analysis of statement of Financial Position.....................................................................4

Part 2 Understanding Financial Information and cash management...............................................5

2.1 Concept of Accrual accounting versus cash accounting..................................................5

2.2 Difference between profit and cash flow..........................................................................6

Part 3 Budget and Company Finance...............................................................................................7

3.1 Budget and purposes of preparing a budget.....................................................................7

3.2 Benefits of forming a limited company and listing it on stock exchange........................8

REFERENCES..............................................................................................................................10

Appendices.....................................................................................................................................11

Supporting Calculations.......................................................................................................11

Part 1 Business Performance Analysis............................................................................................3

1.1 Analysis of statement of Profit or Loss............................................................................3

1.2 Analysis of statement of Financial Position.....................................................................4

Part 2 Understanding Financial Information and cash management...............................................5

2.1 Concept of Accrual accounting versus cash accounting..................................................5

2.2 Difference between profit and cash flow..........................................................................6

Part 3 Budget and Company Finance...............................................................................................7

3.1 Budget and purposes of preparing a budget.....................................................................7

3.2 Benefits of forming a limited company and listing it on stock exchange........................8

REFERENCES..............................................................................................................................10

Appendices.....................................................................................................................................11

Supporting Calculations.......................................................................................................11

Part 1 Business Performance Analysis

1.1 Analysis of statement of Profit or Loss

The financial results or sales statement, because it is generally known, is among the

company's preliminary statements that communicate about its financial activities in a specific

timeframe (Chandra, 2017). This is a financial document summarising all of the profits and

expenditures of a corporation. This covers revenues from advertising and other revenues as well

as administrative costs, expense of that same products sold, various expenses resulting in the

organization's net revenue. Net profits can be correct or incorrect, i.e. the company can benefit

across both benefit and loss.

The business's descriptive financial statements has also been analysed to determine the

financial results of T shirts Ltd. but the first aspect which is examined at would be its revenue,

expenses as well as profitability. It is shown in the initial glance that perhaps the group posted a

decline from its sales between £ 2,101,000 during 2018 towards £ 1,366,000 during 2019, which

may be attributed to less interest leading to financial uncertainty. These have reduced the

purchase price from the previous year that has allowed it to record a smaller decline in total

revenue. Going ahead, it has reported a rise in operating costs, and while the spike would not

seem unusual, increasing revenue may be attributed to normal rises in administrative costs such

as publicity and advertising. In 2019, the organization reported a loss between tax and interest,

however in the preceding year was already in a successful condition. The group has reported a

rise in financial expenses by more than 1.5 percent, which indicates that this year the company,

is taking on additional debt with increased costs. The consequence is a massive negative during

2019 that was in 2018 at such a positive stage. With remaining earnings, this deficit may have

been changed. No detail mostly on dividend strategy of T Shirts Ltd was given. Diverse

accounting ratios were listed in the below order to provide a clearer quantitative overview of

financial results over 2 years:

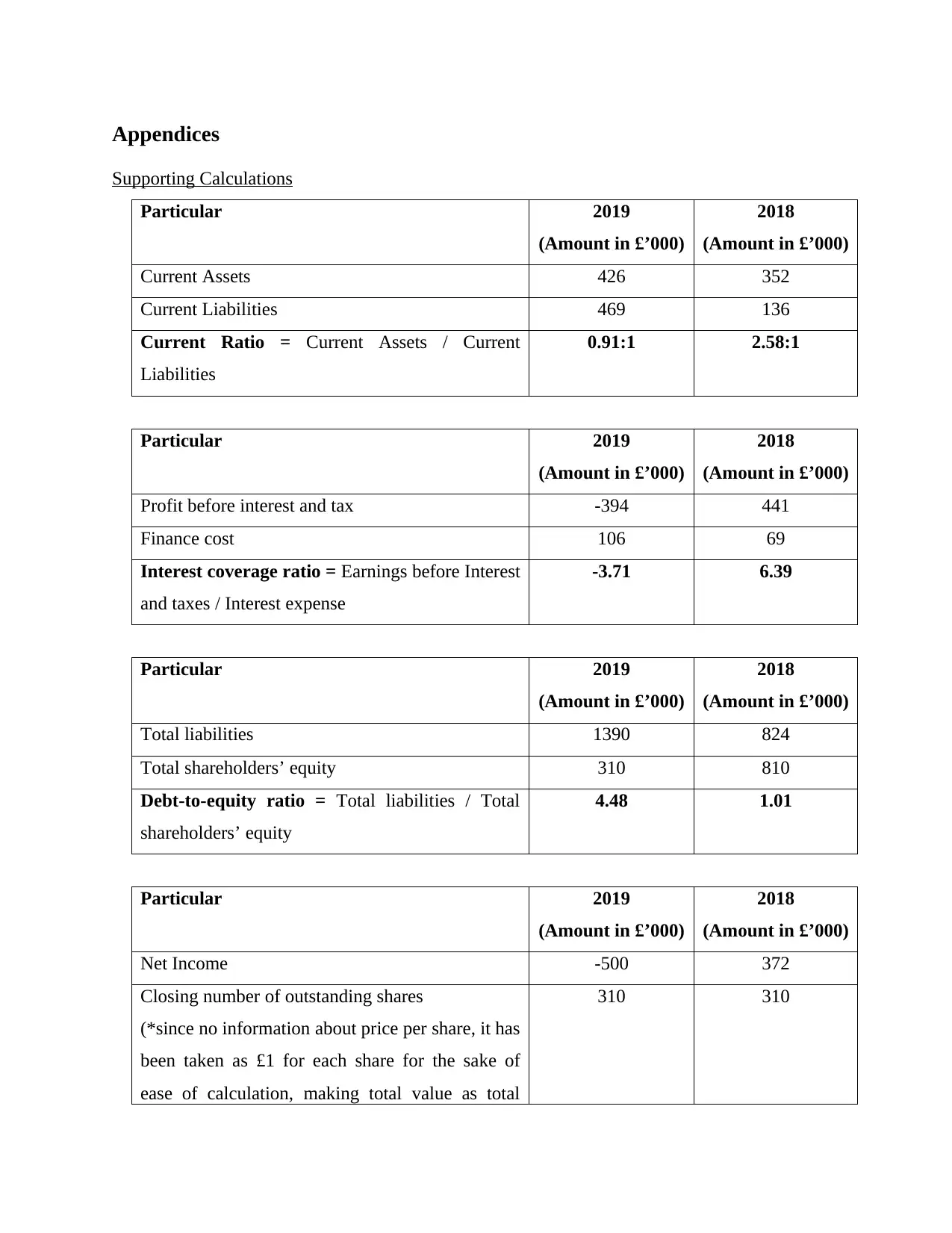

Interest coverage ratio-It is a sovereign debt cum accounting package used only to

determine the willingness of the firm to meet its financial expenses from its profits (Greenbaum,

Thakor and Boot, 2019). The greater the number, the easier it is for industry. T shirt Ltd.

registered 3.71 times the potential to cover attention in 2019, although it became 6.39 times in

2018. The decline may be related to the enhanced cost of fund transfer lending that was missing

1.1 Analysis of statement of Profit or Loss

The financial results or sales statement, because it is generally known, is among the

company's preliminary statements that communicate about its financial activities in a specific

timeframe (Chandra, 2017). This is a financial document summarising all of the profits and

expenditures of a corporation. This covers revenues from advertising and other revenues as well

as administrative costs, expense of that same products sold, various expenses resulting in the

organization's net revenue. Net profits can be correct or incorrect, i.e. the company can benefit

across both benefit and loss.

The business's descriptive financial statements has also been analysed to determine the

financial results of T shirts Ltd. but the first aspect which is examined at would be its revenue,

expenses as well as profitability. It is shown in the initial glance that perhaps the group posted a

decline from its sales between £ 2,101,000 during 2018 towards £ 1,366,000 during 2019, which

may be attributed to less interest leading to financial uncertainty. These have reduced the

purchase price from the previous year that has allowed it to record a smaller decline in total

revenue. Going ahead, it has reported a rise in operating costs, and while the spike would not

seem unusual, increasing revenue may be attributed to normal rises in administrative costs such

as publicity and advertising. In 2019, the organization reported a loss between tax and interest,

however in the preceding year was already in a successful condition. The group has reported a

rise in financial expenses by more than 1.5 percent, which indicates that this year the company,

is taking on additional debt with increased costs. The consequence is a massive negative during

2019 that was in 2018 at such a positive stage. With remaining earnings, this deficit may have

been changed. No detail mostly on dividend strategy of T Shirts Ltd was given. Diverse

accounting ratios were listed in the below order to provide a clearer quantitative overview of

financial results over 2 years:

Interest coverage ratio-It is a sovereign debt cum accounting package used only to

determine the willingness of the firm to meet its financial expenses from its profits (Greenbaum,

Thakor and Boot, 2019). The greater the number, the easier it is for industry. T shirt Ltd.

registered 3.71 times the potential to cover attention in 2019, although it became 6.39 times in

2018. The decline may be related to the enhanced cost of fund transfer lending that was missing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in 2018 as well as the volume of loans that will have interest rates has also risen. And, this can

also never be forgotten because, as in 2018, the corporation would not have revenues to offset its

financial expenses in 2019.

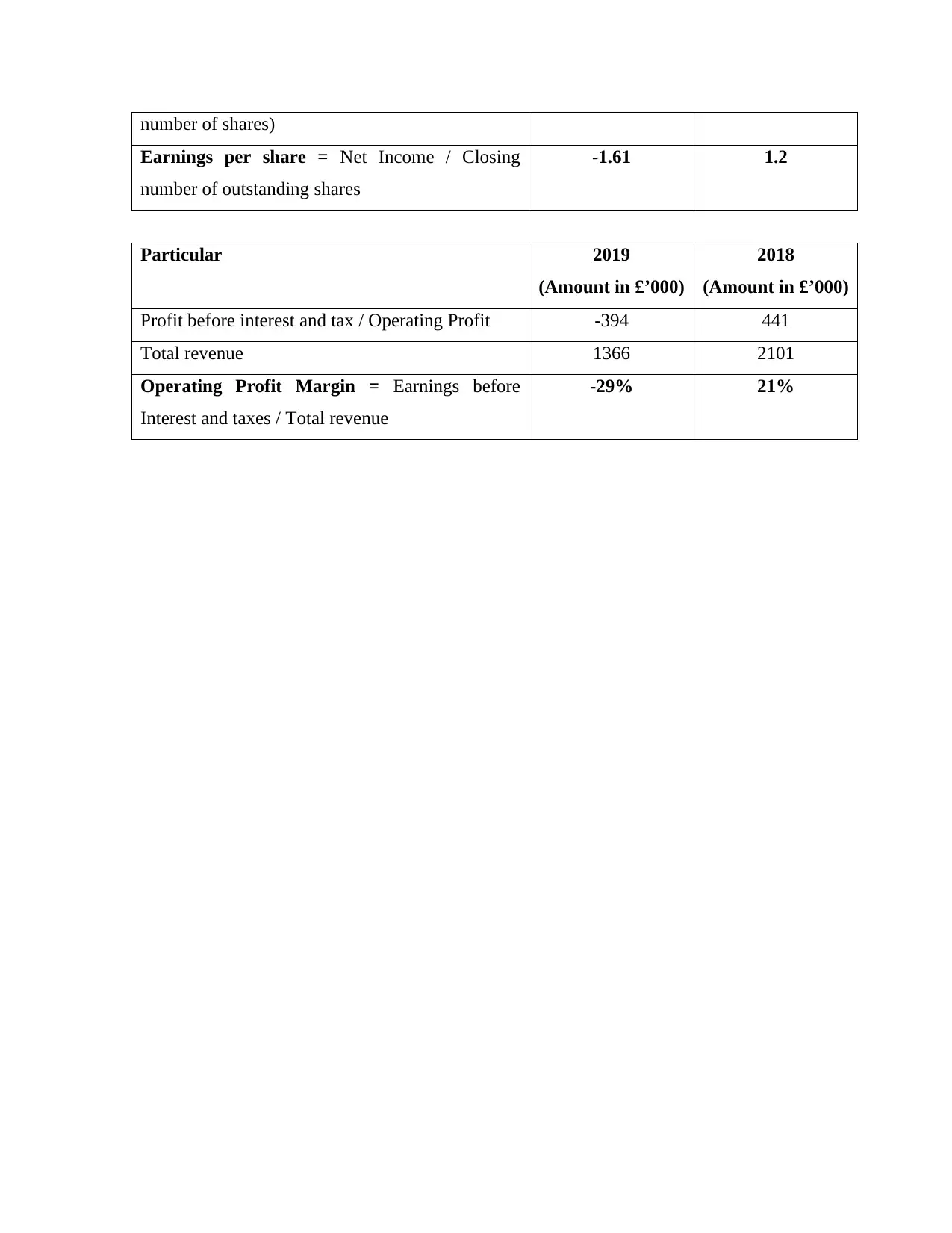

Operating gross profit measure that is assesses the productivity of a business by paying

variable manufacturing expenses to produce profit on revenue. T shirt Ltd posted an operating

income margin of 21 percent in 2018, although due to reasons mentioned above, it has an

operational loss ratio of 29 percent in 2019.

1.2 Analysis of statement of Financial Position

Another final declaration by a company that represents a capital structure at a particular time

seems to be the financial report or cash flow statement, because it is generally known (Fazzini,

2018). This covers the accounting results of company properties, liabilities of the company of

investors in such a way as to compare assets with the other two. The net sales defined in the

declaration of profits forms component of the investment of the owners.

In order to examine the financial condition of T Shirts Ltd., its financial situation statement

was analysed. It could be seen in the first calculation that there is indeed a decline in the market

amount of money invested, which is supposedly due to depreciation. Owing to lower demand

and decreased revenue, the closing stock price has risen, which indicates that the business has an

idle stock level in its warehouses. It must improve its marketing steps, and it will quickly have

expired stock. It is confirmed that the company has eased its lending policies to draw more

buyers, reflected in the rise in prior year current liabilities. The unusual truth is that even the firm

registered no short - term liabilities reserves in 2019, which is not a positive indicator of the

company's current assets. The firm has announced the same equity capital for both years,

meaning that T shirts Ltd. have not released any additional equity in 2019. In 2018, the firm

announced an ending balance of £ 500 of remaining profits that had to be used to balance off the

whole year's losses. Hence the retained amount of profits this year has been zero. Long-term

loans however have risen since 2018, suggesting that in 2019 debt payments are being obtained.

Payment period too have grown, but it seems to be in the normal market path from looking only

at ratio of growth. Also it recorded using cash outflow in 2019 that is at a far higher pace than

mortgages, according to data given.

In order to get a clearer comparative overview of T Shirts Ltd's two-year financial situation,

the following financial ratios were determined:

also never be forgotten because, as in 2018, the corporation would not have revenues to offset its

financial expenses in 2019.

Operating gross profit measure that is assesses the productivity of a business by paying

variable manufacturing expenses to produce profit on revenue. T shirt Ltd posted an operating

income margin of 21 percent in 2018, although due to reasons mentioned above, it has an

operational loss ratio of 29 percent in 2019.

1.2 Analysis of statement of Financial Position

Another final declaration by a company that represents a capital structure at a particular time

seems to be the financial report or cash flow statement, because it is generally known (Fazzini,

2018). This covers the accounting results of company properties, liabilities of the company of

investors in such a way as to compare assets with the other two. The net sales defined in the

declaration of profits forms component of the investment of the owners.

In order to examine the financial condition of T Shirts Ltd., its financial situation statement

was analysed. It could be seen in the first calculation that there is indeed a decline in the market

amount of money invested, which is supposedly due to depreciation. Owing to lower demand

and decreased revenue, the closing stock price has risen, which indicates that the business has an

idle stock level in its warehouses. It must improve its marketing steps, and it will quickly have

expired stock. It is confirmed that the company has eased its lending policies to draw more

buyers, reflected in the rise in prior year current liabilities. The unusual truth is that even the firm

registered no short - term liabilities reserves in 2019, which is not a positive indicator of the

company's current assets. The firm has announced the same equity capital for both years,

meaning that T shirts Ltd. have not released any additional equity in 2019. In 2018, the firm

announced an ending balance of £ 500 of remaining profits that had to be used to balance off the

whole year's losses. Hence the retained amount of profits this year has been zero. Long-term

loans however have risen since 2018, suggesting that in 2019 debt payments are being obtained.

Payment period too have grown, but it seems to be in the normal market path from looking only

at ratio of growth. Also it recorded using cash outflow in 2019 that is at a far higher pace than

mortgages, according to data given.

In order to get a clearer comparative overview of T Shirts Ltd's two-year financial situation,

the following financial ratios were determined:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Present ratio: That is a financial leverage that used determine the efficacy of the cash flow

(Samonas, 2015). The greater the ratio, that stronger this is for the firm's cash. T shirts Ltd. had a

recorded current ratio of 2.58:1 in 2018, although it slipped to just 0.91:1 in 2019, showing a

decline in the capacity of the current profits of the firm to meet its financial obligations. It may

be attributed to the reason that the enterprise has used a large amount through debt financing to

finance its activities.

Debt-to-equity ratio-It is a financial measure that assesses that much of the debt could be

financed if required by equity. The greater is the percentage, the greater the standard chance. In

2019, T shirts Ltd posted a ratio of 4.48, while in 2018 it was just 1.01, due respectively to a rise

in retained earnings as well as a reduction in that will to capital gains.

Earnings per share is indeed a low profitability calculation that indicates the firm’s

profitability throughout regards to the corporation's share capital (Cortesi and et.al., 2015). The

greater the proportion, the stronger the situation will be T shirts Ltd. produced strong EPS of 1.2

in 2018 while pessimistic 1.6 in 2019 due to losses affecting the business in both years as

shareholder equity is unaltered.

Part 2 Understanding Financial Information and cash management

2.1 Concept of Accrual accounting versus cash accounting

Accrual accounting-This approach involves collection and measurement company cash products

irrespective not on whether money transactions have been implicated. It is premised on the

equity method that certain profits and losses should be identified in the very same time frame

where either the who are due or reimbursement has been swapped, with whatever occurs first. T

shirts Ltd, for instance, have a monthly overall sale of £ 100,000. From which, 60% is in money

whilst also 40 percent is on loans, of which fee will be did receive later. To have a realistic

image of cash the business follows repayment financial reporting and graphic novel purchases in

both configurations.

Benefits-The most notable advantage of accrual accounting would be that it offers an objective

view of the financial status of a business by comparing actual cash flow with projected potential

cash flows (Gigli and Mariani, 2018). This simpler view of retained earnings makes it really easy

for a T-shirts Ltd boss to handle their existing tasks and finances and also aids in better

preparation for the prospect.

(Samonas, 2015). The greater the ratio, that stronger this is for the firm's cash. T shirts Ltd. had a

recorded current ratio of 2.58:1 in 2018, although it slipped to just 0.91:1 in 2019, showing a

decline in the capacity of the current profits of the firm to meet its financial obligations. It may

be attributed to the reason that the enterprise has used a large amount through debt financing to

finance its activities.

Debt-to-equity ratio-It is a financial measure that assesses that much of the debt could be

financed if required by equity. The greater is the percentage, the greater the standard chance. In

2019, T shirts Ltd posted a ratio of 4.48, while in 2018 it was just 1.01, due respectively to a rise

in retained earnings as well as a reduction in that will to capital gains.

Earnings per share is indeed a low profitability calculation that indicates the firm’s

profitability throughout regards to the corporation's share capital (Cortesi and et.al., 2015). The

greater the proportion, the stronger the situation will be T shirts Ltd. produced strong EPS of 1.2

in 2018 while pessimistic 1.6 in 2019 due to losses affecting the business in both years as

shareholder equity is unaltered.

Part 2 Understanding Financial Information and cash management

2.1 Concept of Accrual accounting versus cash accounting

Accrual accounting-This approach involves collection and measurement company cash products

irrespective not on whether money transactions have been implicated. It is premised on the

equity method that certain profits and losses should be identified in the very same time frame

where either the who are due or reimbursement has been swapped, with whatever occurs first. T

shirts Ltd, for instance, have a monthly overall sale of £ 100,000. From which, 60% is in money

whilst also 40 percent is on loans, of which fee will be did receive later. To have a realistic

image of cash the business follows repayment financial reporting and graphic novel purchases in

both configurations.

Benefits-The most notable advantage of accrual accounting would be that it offers an objective

view of the financial status of a business by comparing actual cash flow with projected potential

cash flows (Gigli and Mariani, 2018). This simpler view of retained earnings makes it really easy

for a T-shirts Ltd boss to handle their existing tasks and finances and also aids in better

preparation for the prospect.

Limitations-This technique is relatively difficult and more costly to follow. It takes some time

and professional professionals to assess earned compensation and make the appropriate change

to the accounting records. In addition, the maintenance of accounting payables and receivables

includes additional requirements. However most of the small firms favour the modified cash

process.

Cash accounting-This approach includes the recognition, calculation and documentation of

payments only where transfers and markets are concerned. Consequently, small firms favour

such accounting approach but it is not ideal for major businesses because it would reveal their

identity financial status (Aleinikov, Kuter and Musaelyan, 2017). A self-employed person has £

2000 in monthly revenue. 80 percent of which is currency, while 20 percent is on loan. The

trader uses the form of cash accounting which reports only cash transactions, leaving trade

debtors records as and then when money is received, since the merchant is only important in

explaining money in hand.

Benefits- The approach is easy and straightforward to enforce. With no need to train trained

workers to pursue this strategy, then there is no need to monitor accounts receivables and

payables, making reporting transparent and simple to follow. Thus the, small businessmen use it

because they are only worried about the money they already have in their possession.

Limitations-The main drawback of this strategy is that it ignores representing the true image of

company losses that have already been incurred but are not yet paid are now not compensated

for, granting the organisation a greater role than it truly is. As this approach does not represent a

true and full image, large corporations such as T shirts Ltd in difficult payments under the

Commonly Agreed Accounting Rules are not permitted to use it (GAAP).

2.2 Difference between profit and cash flow

Profit-Profit and net profits, despite subtracting all company operating costs from the sales,

the positive amount stays (Hogianto and Sebastian, 2019). It can either be shared among holders

or recouped back into the business. When costs outweigh earnings, it is considered a failure for

the corporation. It is measured by the financial statement that is divided into 3 parameters of the

proposed: total revenue, net margin and operating earnings.

Cash flow-Cash balance is refers to as the net amount between the in and out exchange of

money by an organisation at a given period of time. It's both correct and incorrect, thus. The

financial statement is recorded in 3 groups: operating, spending as well as cash flow funding.

and professional professionals to assess earned compensation and make the appropriate change

to the accounting records. In addition, the maintenance of accounting payables and receivables

includes additional requirements. However most of the small firms favour the modified cash

process.

Cash accounting-This approach includes the recognition, calculation and documentation of

payments only where transfers and markets are concerned. Consequently, small firms favour

such accounting approach but it is not ideal for major businesses because it would reveal their

identity financial status (Aleinikov, Kuter and Musaelyan, 2017). A self-employed person has £

2000 in monthly revenue. 80 percent of which is currency, while 20 percent is on loan. The

trader uses the form of cash accounting which reports only cash transactions, leaving trade

debtors records as and then when money is received, since the merchant is only important in

explaining money in hand.

Benefits- The approach is easy and straightforward to enforce. With no need to train trained

workers to pursue this strategy, then there is no need to monitor accounts receivables and

payables, making reporting transparent and simple to follow. Thus the, small businessmen use it

because they are only worried about the money they already have in their possession.

Limitations-The main drawback of this strategy is that it ignores representing the true image of

company losses that have already been incurred but are not yet paid are now not compensated

for, granting the organisation a greater role than it truly is. As this approach does not represent a

true and full image, large corporations such as T shirts Ltd in difficult payments under the

Commonly Agreed Accounting Rules are not permitted to use it (GAAP).

2.2 Difference between profit and cash flow

Profit-Profit and net profits, despite subtracting all company operating costs from the sales,

the positive amount stays (Hogianto and Sebastian, 2019). It can either be shared among holders

or recouped back into the business. When costs outweigh earnings, it is considered a failure for

the corporation. It is measured by the financial statement that is divided into 3 parameters of the

proposed: total revenue, net margin and operating earnings.

Cash flow-Cash balance is refers to as the net amount between the in and out exchange of

money by an organisation at a given period of time. It's both correct and incorrect, thus. The

financial statement is recorded in 3 groups: operating, spending as well as cash flow funding.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Basis of difference Profit Cash flow

Revenue generated Accrued income or the income

that is owed for the year, not just

whether necessarily earned, is

expressed in the financial gains

statement.

In cash balance, only

those sales that have been

realized in money are

obtained.

Expenses incurred Both costs due for the fixed

time, regardless about whether or

not these have been paid during the

fixed time, are factored in the

estimation of benefit or loss.

When reviewing the cash

balance statement, just those

costs that are incurred in cash

during the stated balance sheet

are taken into consideration.

Adequacy Adequate earnings do not always

imply that the corporation has

sufficient money, since it often

requires non-cash costs and sales

(Ozerov and et.al., 2017).

Adequate investment returns

do not always indicate the

company earns adequate

income and that positive cash

flows may be the outcome of a

profitable product the raises

other costs and also profits.

Part 3 Budget and Company Finance

3.1 Budget and purposes of preparing a budget

An expenditure plan is a structured calculation of business activities, i.e. income and

expenditure, in quantitative terms over a determined period of time. These are focused on

financial accounts; cash balance statements, corporate priorities and market conditions. Since the

economic world is complicated, a business must plan flexible budgets that can be tailored as per

program planning (Ehrhardt and Brigham, 2016). A business plans different kinds of budgets

that are listed below:

Master budget-This document is a summary of all frontline services that represents the total

forecasts and projections for the business as a whole in the same financial year. This covers

multiple budgets, like:

Revenue generated Accrued income or the income

that is owed for the year, not just

whether necessarily earned, is

expressed in the financial gains

statement.

In cash balance, only

those sales that have been

realized in money are

obtained.

Expenses incurred Both costs due for the fixed

time, regardless about whether or

not these have been paid during the

fixed time, are factored in the

estimation of benefit or loss.

When reviewing the cash

balance statement, just those

costs that are incurred in cash

during the stated balance sheet

are taken into consideration.

Adequacy Adequate earnings do not always

imply that the corporation has

sufficient money, since it often

requires non-cash costs and sales

(Ozerov and et.al., 2017).

Adequate investment returns

do not always indicate the

company earns adequate

income and that positive cash

flows may be the outcome of a

profitable product the raises

other costs and also profits.

Part 3 Budget and Company Finance

3.1 Budget and purposes of preparing a budget

An expenditure plan is a structured calculation of business activities, i.e. income and

expenditure, in quantitative terms over a determined period of time. These are focused on

financial accounts; cash balance statements, corporate priorities and market conditions. Since the

economic world is complicated, a business must plan flexible budgets that can be tailored as per

program planning (Ehrhardt and Brigham, 2016). A business plans different kinds of budgets

that are listed below:

Master budget-This document is a summary of all frontline services that represents the total

forecasts and projections for the business as a whole in the same financial year. This covers

multiple budgets, like:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Operating schedule-This budget involves the analysis of any of the profits and expenditures

anticipated from its normal business activities. This covers the cost of manufacturing goods,

depreciation and operating expenditures, etc. (Brealey and et.al., 2018).

Cash forecast-This budget provides an approximation of all cash inflows and outflows produced

during that time. This allows the brand optimise its transactions as per the flow of resources

throughout the sector.

Reasons in budget preparation: The following are separate objectives over which the

organisation plans expenditures:

Facilitates in planning and management-The main objective of budget research is to analyse an

organisation prepare and coordinate its operations for the defined time. Other than preparation, it

also serves as the goal or objective for the managerial position of operation and assessment.

Preparing budgets that are consistent over a long stretch of time enables them to keep in

accordance with the lengthy budgetary targets.

Helps to fix accountability-Budgets are the standard for influence, as mentioned previously. This

allows managers to determine differences from the objectives and to determine the accountability

of those responsible for the overlooked performance. Total management helps repairing funding

gaps and boost in investments. This mostly makes the business manage its staff members, and

moreover allows workers improve their skills qualifications.

Reports are created in percentages and enable a corporation maintain leverage of its finances

(Argenti, 2018). If a corporation is able to exert more leverage of its resources, they were

capable of achieving their targets more effectively and increase their net worth. Enhanced

technical and financial efficiency deteriorates stress mostly on organization's assets and

minimises undue financial assertions.

3.2 Benefits of forming a limited company and listing it on stock exchange

A limited partnership is a type of company business arrangement in which the legitimate

possession of a corporation is divided by giving it the status of a distinct legal person itself from

shareholders. They are regulated by the rules set down in the Corporations Act and should be

registered at Company Accounts in the United Kingdom. In the United Kingdom, there are 3

types of limited business: private firm limited by stock, private limited liability company as well

as limited company.

anticipated from its normal business activities. This covers the cost of manufacturing goods,

depreciation and operating expenditures, etc. (Brealey and et.al., 2018).

Cash forecast-This budget provides an approximation of all cash inflows and outflows produced

during that time. This allows the brand optimise its transactions as per the flow of resources

throughout the sector.

Reasons in budget preparation: The following are separate objectives over which the

organisation plans expenditures:

Facilitates in planning and management-The main objective of budget research is to analyse an

organisation prepare and coordinate its operations for the defined time. Other than preparation, it

also serves as the goal or objective for the managerial position of operation and assessment.

Preparing budgets that are consistent over a long stretch of time enables them to keep in

accordance with the lengthy budgetary targets.

Helps to fix accountability-Budgets are the standard for influence, as mentioned previously. This

allows managers to determine differences from the objectives and to determine the accountability

of those responsible for the overlooked performance. Total management helps repairing funding

gaps and boost in investments. This mostly makes the business manage its staff members, and

moreover allows workers improve their skills qualifications.

Reports are created in percentages and enable a corporation maintain leverage of its finances

(Argenti, 2018). If a corporation is able to exert more leverage of its resources, they were

capable of achieving their targets more effectively and increase their net worth. Enhanced

technical and financial efficiency deteriorates stress mostly on organization's assets and

minimises undue financial assertions.

3.2 Benefits of forming a limited company and listing it on stock exchange

A limited partnership is a type of company business arrangement in which the legitimate

possession of a corporation is divided by giving it the status of a distinct legal person itself from

shareholders. They are regulated by the rules set down in the Corporations Act and should be

registered at Company Accounts in the United Kingdom. In the United Kingdom, there are 3

types of limited business: private firm limited by stock, private limited liability company as well

as limited company.

Benefits of forming a limited company: The advantages of creating a business entity are

described below:

A limited partnership is independent from its holders, i.e. this can try and negotiate by its own

behalf and can prosecute or be sued over it. Separate legal body it grants it the moral right to

receive and retain the gains generated from its activities (Miley, 2018).

Limited liability-A legal separation makes companies liable for trying to square its own current

assets and liabilities, and if the business refuses to pay its obligations, managers and owners

really aren't held liable to pay these other obligations individually.

Stock exchange listing benefits: The advantages of listing a corporation on a stock market are

listed below:

Generating revenue thru the public share issue-After listing a corporation on any stock market, it

can purchase it's own shareholders and everyone can buy shares in stock holdings that help it

start raising much greater capital.

Expanding the market share: Firm’s in market capitalization is liable to have a broad market

share, going to promote the threat of property to large numbers of investors without increasing

effort into work by a single campaign group to influence decision-making (Ehrhardt and

Brigham, 2016).

described below:

A limited partnership is independent from its holders, i.e. this can try and negotiate by its own

behalf and can prosecute or be sued over it. Separate legal body it grants it the moral right to

receive and retain the gains generated from its activities (Miley, 2018).

Limited liability-A legal separation makes companies liable for trying to square its own current

assets and liabilities, and if the business refuses to pay its obligations, managers and owners

really aren't held liable to pay these other obligations individually.

Stock exchange listing benefits: The advantages of listing a corporation on a stock market are

listed below:

Generating revenue thru the public share issue-After listing a corporation on any stock market, it

can purchase it's own shareholders and everyone can buy shares in stock holdings that help it

start raising much greater capital.

Expanding the market share: Firm’s in market capitalization is liable to have a broad market

share, going to promote the threat of property to large numbers of investors without increasing

effort into work by a single campaign group to influence decision-making (Ehrhardt and

Brigham, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Aleinikov, D., Kuter, M. and Musaelyan, A., 2017, December. The early cash account books.

In International Conference on Information Technology Science (pp. 195-207).

Springer, Cham.

Argenti, J., 2018. Practical corporate planning. Routledge.

Brealey, R.A. and et.al., 2018. Principles of Corporate Finance, 12/e (Vol. 12). McGraw-Hill

Education.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-hill education.

Cortesi, A. and et.al., 2015. Advanced Financial Accounting: Financial Statement Analysis–

Accounting Issues–Group Accounts. EGEA spa.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

learning.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

learning.

Fazzini, M., 2018. Financial Statement Analysis. In Business Valuation (pp. 39-76). Palgrave

Macmillan, Cham.

Gigli, S. and Mariani, L., 2018. Lost in the transition from cash to accrual

accounting. International Journal of Public Sector Management.

Greenbaum, S.I., Thakor, A.V. and Boot, A.W., 2019. Contemporary financial intermediation.

Academic Press.

Hogianto, W. and Sebastian, H., 2019. Use of Profit and Cash Flow to Predict the Condition of

Financial Distress. Available at SSRN 3319862.

Miley, V., 2018. Budget cuts hit corporate oversight. Green Left Weekly. (1181). p.9.

Ozerov, E.S. and et.al., 2017, September. Selecting the best use option for assets in a corporate

management system. In 2017 6th International Conference on Reliability, Infocom

Technologies and Optimization (Trends and Future Directions)(ICRITO) (pp. 162-170).

IEEE.

Samonas, M., 2015. Financial forecasting, analysis, and modelling: a framework for long-term

forecasting. John Wiley & Sons.

Books and Journals

Aleinikov, D., Kuter, M. and Musaelyan, A., 2017, December. The early cash account books.

In International Conference on Information Technology Science (pp. 195-207).

Springer, Cham.

Argenti, J., 2018. Practical corporate planning. Routledge.

Brealey, R.A. and et.al., 2018. Principles of Corporate Finance, 12/e (Vol. 12). McGraw-Hill

Education.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-hill education.

Cortesi, A. and et.al., 2015. Advanced Financial Accounting: Financial Statement Analysis–

Accounting Issues–Group Accounts. EGEA spa.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

learning.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

learning.

Fazzini, M., 2018. Financial Statement Analysis. In Business Valuation (pp. 39-76). Palgrave

Macmillan, Cham.

Gigli, S. and Mariani, L., 2018. Lost in the transition from cash to accrual

accounting. International Journal of Public Sector Management.

Greenbaum, S.I., Thakor, A.V. and Boot, A.W., 2019. Contemporary financial intermediation.

Academic Press.

Hogianto, W. and Sebastian, H., 2019. Use of Profit and Cash Flow to Predict the Condition of

Financial Distress. Available at SSRN 3319862.

Miley, V., 2018. Budget cuts hit corporate oversight. Green Left Weekly. (1181). p.9.

Ozerov, E.S. and et.al., 2017, September. Selecting the best use option for assets in a corporate

management system. In 2017 6th International Conference on Reliability, Infocom

Technologies and Optimization (Trends and Future Directions)(ICRITO) (pp. 162-170).

IEEE.

Samonas, M., 2015. Financial forecasting, analysis, and modelling: a framework for long-term

forecasting. John Wiley & Sons.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appendices

Supporting Calculations

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Current Assets 426 352

Current Liabilities 469 136

Current Ratio = Current Assets / Current

Liabilities

0.91:1 2.58:1

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Profit before interest and tax -394 441

Finance cost 106 69

Interest coverage ratio = Earnings before Interest

and taxes / Interest expense

-3.71 6.39

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Total liabilities 1390 824

Total shareholders’ equity 310 810

Debt-to-equity ratio = Total liabilities / Total

shareholders’ equity

4.48 1.01

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Net Income -500 372

Closing number of outstanding shares

(*since no information about price per share, it has

been taken as £1 for each share for the sake of

ease of calculation, making total value as total

310 310

Supporting Calculations

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Current Assets 426 352

Current Liabilities 469 136

Current Ratio = Current Assets / Current

Liabilities

0.91:1 2.58:1

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Profit before interest and tax -394 441

Finance cost 106 69

Interest coverage ratio = Earnings before Interest

and taxes / Interest expense

-3.71 6.39

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Total liabilities 1390 824

Total shareholders’ equity 310 810

Debt-to-equity ratio = Total liabilities / Total

shareholders’ equity

4.48 1.01

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Net Income -500 372

Closing number of outstanding shares

(*since no information about price per share, it has

been taken as £1 for each share for the sake of

ease of calculation, making total value as total

310 310

number of shares)

Earnings per share = Net Income / Closing

number of outstanding shares

-1.61 1.2

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Profit before interest and tax / Operating Profit -394 441

Total revenue 1366 2101

Operating Profit Margin = Earnings before

Interest and taxes / Total revenue

-29% 21%

Earnings per share = Net Income / Closing

number of outstanding shares

-1.61 1.2

Particular 2019

(Amount in £’000)

2018

(Amount in £’000)

Profit before interest and tax / Operating Profit -394 441

Total revenue 1366 2101

Operating Profit Margin = Earnings before

Interest and taxes / Total revenue

-29% 21%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.