Analysis of Financial Statements: Canadian Companies Assignment

VerifiedAdded on 2023/01/17

|9

|1768

|66

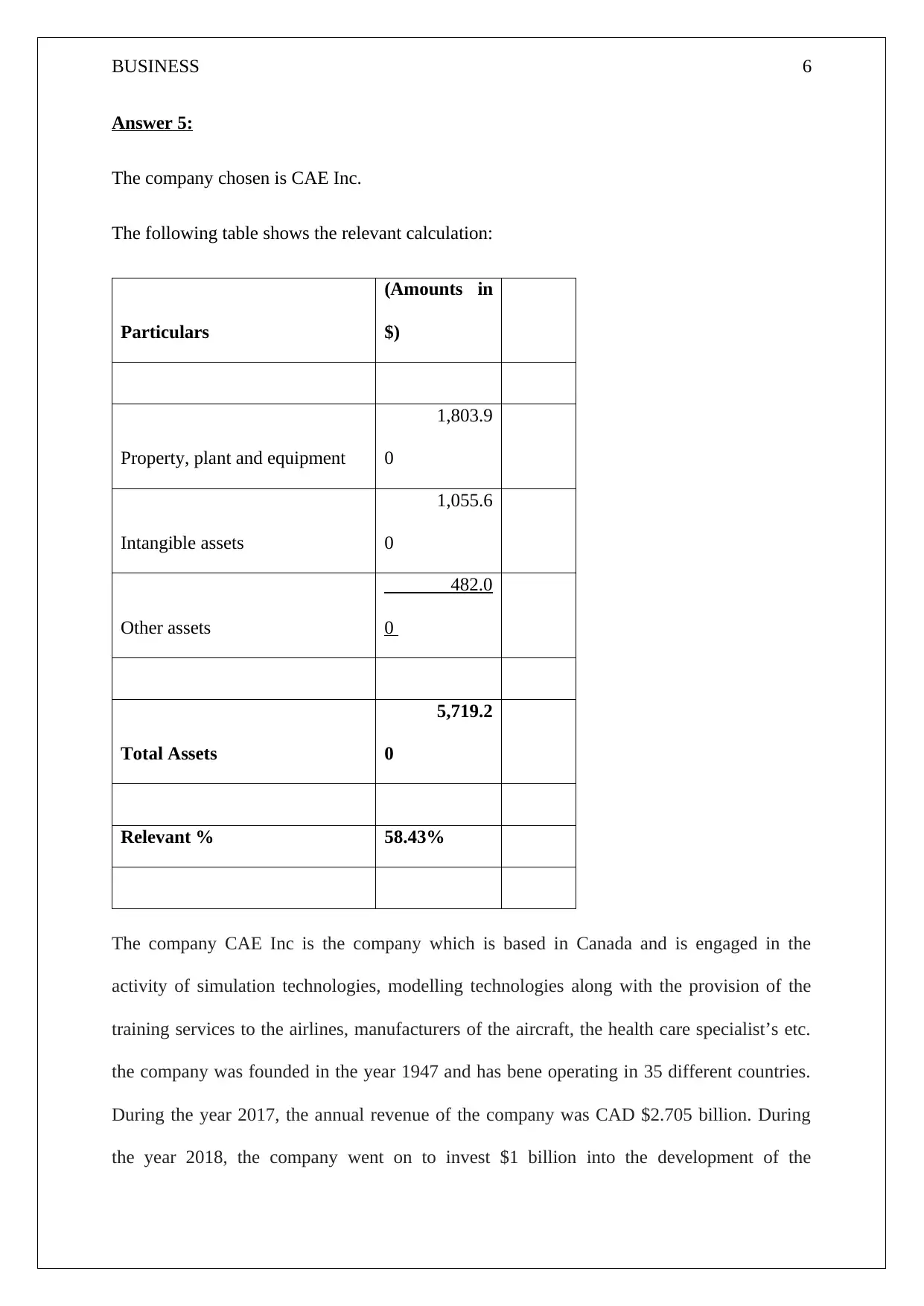

Homework Assignment

AI Summary

This document provides a comprehensive analysis of a business finance assignment focusing on Canadian companies listed on the Toronto Stock Exchange. The assignment explores several key areas, including the application of IFRS 9 to financial statements, specifically referencing CAE Inc. and Hexo Corp. It examines the impact of cash and receivables on total assets, the pros and cons of liquid assets, and the ethical implications of financial misconduct within a business context. The document also covers revenue recognition principles, impairment of long-lived assets, and the importance of fair value adjustments. The assignment requires analysis of financial statements, identification of relevant percentages, and addressing ethical dilemmas, offering a practical understanding of financial reporting and ethical decision-making in business.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.