Business Finance and Economics: Assignment Report - Financial Analysis

VerifiedAdded on 2022/12/01

|10

|3163

|182

Report

AI Summary

This report addresses key aspects of Business Finance and Economics, fulfilling the requirements of a Level 4 assignment. It begins by examining the main determinants of business performance, differentiating between micro- and macroeconomic factors, and discussing economic influences on an organization's competitive environment. The report then explores the role and importance of accounting within an organization, covering both financial reporting and decision-making processes. It distinguishes between the major financial statements, explaining their layouts and key terms. A significant portion of the report involves calculating and interpreting financial ratios for XYZ Plc, demonstrating an understanding of organizational performance. Finally, it delves into management accounting, highlighting its significance in planning, control, and decision-making. The report incorporates relevant theories, concepts, and formulas throughout its analysis, providing a comprehensive overview of the subject matter.

Business Finance and

Economics

Economics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1........................................................................................................................................3

Main determinants of business performance and distinguish whether these are micro- or

macroeconomic. Discuss the economic factors that affect the competitive environment of an

organisation..................................................................................................................................3

Question 2........................................................................................................................................4

Role of accounting within an organisation and highlight its importance with respect to both

reporting and decision-making....................................................................................................4

Question 3........................................................................................................................................5

Distinguish between the major financial statements and explain the layout and terms used

within each Statement..................................................................................................................5

Question 4........................................................................................................................................6

Calculate and interpret the following ratios for XYZ Plc............................................................6

Question 5........................................................................................................................................8

Management accounting and discuss how this is important for planning, control and decision-

making within an organisation.....................................................................................................8

REFERENCES..............................................................................................................................10

Question 1........................................................................................................................................3

Main determinants of business performance and distinguish whether these are micro- or

macroeconomic. Discuss the economic factors that affect the competitive environment of an

organisation..................................................................................................................................3

Question 2........................................................................................................................................4

Role of accounting within an organisation and highlight its importance with respect to both

reporting and decision-making....................................................................................................4

Question 3........................................................................................................................................5

Distinguish between the major financial statements and explain the layout and terms used

within each Statement..................................................................................................................5

Question 4........................................................................................................................................6

Calculate and interpret the following ratios for XYZ Plc............................................................6

Question 5........................................................................................................................................8

Management accounting and discuss how this is important for planning, control and decision-

making within an organisation.....................................................................................................8

REFERENCES..............................................................................................................................10

Question 1

Main determinants of business performance and distinguish whether these are micro- or

macroeconomic. Discuss the economic factors that affect the competitive environment of

an organisation.

Micro Environment Factors

Suppliers: As suppliers have authority, they will influence the company's growth. When

the manufacturer is the sole or main manufacturer with their goods; the customer is not

critical to the supplier's operation; and the supplier's inventory is an integral part of the

customer's final piece and/or business, that distributor wields control (Cepiku, 2020).

Resellers: Whether a company's product is sold by third-party resellers or industry

mediators such as supermarkets, wholesalers, and so on, certain resellers have an effect

on the company's marketing performance. For example, when a retail vendor has a good

reputation, that reputation may be used to advertise the product.

Customers: Whether they sell certain goods and services towards customers can be

heavily influenced by who the consumers are (B2B or B2C, local or foreign, etc.)

regarding their motivations for purchasing the product.

The population at large: The Company has a responsibility to the general public. Every

decision taken by the organisation must be seen in the eyes of most people and how much

it affects them. The government has every right to assist them in fulfilling certain

objectives, as well as to discourage them from doing so.

Macro Environment Factors

Popular economic changes, such as country/region, age, race, educational attainment,

household behaviour, unique influences, and developments, have an influence on

different consumer segments.

Economic factors: Both the organization's efficiency and the customer's judgement

process are affected by the economic climate (Dabbicco and Mattei, 2021).

Natural/physical forces: It is essential to consider the Earth's regeneration of

environmental assets like trees, agricultural goods, aquatic products, and so on. Natural

non-renewable commodities such as oil, gas, minerals, and others can also have a bearing

on the organization's production.

Main determinants of business performance and distinguish whether these are micro- or

macroeconomic. Discuss the economic factors that affect the competitive environment of

an organisation.

Micro Environment Factors

Suppliers: As suppliers have authority, they will influence the company's growth. When

the manufacturer is the sole or main manufacturer with their goods; the customer is not

critical to the supplier's operation; and the supplier's inventory is an integral part of the

customer's final piece and/or business, that distributor wields control (Cepiku, 2020).

Resellers: Whether a company's product is sold by third-party resellers or industry

mediators such as supermarkets, wholesalers, and so on, certain resellers have an effect

on the company's marketing performance. For example, when a retail vendor has a good

reputation, that reputation may be used to advertise the product.

Customers: Whether they sell certain goods and services towards customers can be

heavily influenced by who the consumers are (B2B or B2C, local or foreign, etc.)

regarding their motivations for purchasing the product.

The population at large: The Company has a responsibility to the general public. Every

decision taken by the organisation must be seen in the eyes of most people and how much

it affects them. The government has every right to assist them in fulfilling certain

objectives, as well as to discourage them from doing so.

Macro Environment Factors

Popular economic changes, such as country/region, age, race, educational attainment,

household behaviour, unique influences, and developments, have an influence on

different consumer segments.

Economic factors: Both the organization's efficiency and the customer's judgement

process are affected by the economic climate (Dabbicco and Mattei, 2021).

Natural/physical forces: It is essential to consider the Earth's regeneration of

environmental assets like trees, agricultural goods, aquatic products, and so on. Natural

non-renewable commodities such as oil, gas, minerals, and others can also have a bearing

on the organization's production.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Technological factors: The expertise and experience used in manufacturing, as well as the

equipment and materials used for the goods and services, will all have an effect on the

company's smooth operation and must be taken into account.

Economic factors that affect the competitive environment of an organisation.

Interest rates: Interest rates can be seen in a variety of ways, levied by a variety of individuals.

The present system for lending rates is obviously important to financial entities, but it may also

have an effect on businesses whose plans depend on big loans.

Exchange rates: While currency values are a complex topic, they must simply adhere to those

that work with imports and exports. Changing currency values can influence how much a

business must pay a foreign vendor to appease them, affecting profitability and requiring a

significant resources to keep track of.

Recession: Any economic downturn has the power to alter consumer buying habits, forcing

businesses to lower costs or clear less volumes. Economic conditions are only one of the several

existing, external influences that may have an effect on companies. Since they are related to the

economies on a larger scale, they have such a significant impact on the inner workings of every

business. Rates of interest, currency exchange, and taxation are all instances (Ferreira and

Dickason, 2018).

Question 2

Role of accounting within an organisation and highlight its importance with respect to both

reporting and decision-making.

Importance of accounting in financial reporting

Accounting seems to be the method of gathering, reviewing, and sharing financial data for

the purpose of making decisions. Accountants who have been educated in the basic procedures

and methods of the field are usually the ones who review financial data. Many subjects and

procedures applicable to that same accounting profession are included in this program. Although

many participants may use what they've learned in this class to continue their education by

becoming accountants or business people, some will choose to follow other careers.

A good knowledge of accounting, on the other hand, will also be a valuable guide for many

people. In reality, it's difficult to imagine a career where an understanding of accounting

standards will be detrimental. As a result, irrespective of the chosen career, another of the aims

equipment and materials used for the goods and services, will all have an effect on the

company's smooth operation and must be taken into account.

Economic factors that affect the competitive environment of an organisation.

Interest rates: Interest rates can be seen in a variety of ways, levied by a variety of individuals.

The present system for lending rates is obviously important to financial entities, but it may also

have an effect on businesses whose plans depend on big loans.

Exchange rates: While currency values are a complex topic, they must simply adhere to those

that work with imports and exports. Changing currency values can influence how much a

business must pay a foreign vendor to appease them, affecting profitability and requiring a

significant resources to keep track of.

Recession: Any economic downturn has the power to alter consumer buying habits, forcing

businesses to lower costs or clear less volumes. Economic conditions are only one of the several

existing, external influences that may have an effect on companies. Since they are related to the

economies on a larger scale, they have such a significant impact on the inner workings of every

business. Rates of interest, currency exchange, and taxation are all instances (Ferreira and

Dickason, 2018).

Question 2

Role of accounting within an organisation and highlight its importance with respect to both

reporting and decision-making.

Importance of accounting in financial reporting

Accounting seems to be the method of gathering, reviewing, and sharing financial data for

the purpose of making decisions. Accountants who have been educated in the basic procedures

and methods of the field are usually the ones who review financial data. Many subjects and

procedures applicable to that same accounting profession are included in this program. Although

many participants may use what they've learned in this class to continue their education by

becoming accountants or business people, some will choose to follow other careers.

A good knowledge of accounting, on the other hand, will also be a valuable guide for many

people. In reality, it's difficult to imagine a career where an understanding of accounting

standards will be detrimental. As a result, irrespective of the chosen career, another of the aims

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of this program is to have a solid overview of how financial data is processed being used in the

marketplace. Before investing in making or lending the capital, lenders and investors have to

learn a few things about each other. So this entails digging around in the company's tax records.

Generally, they must present these income reports to investment managers. They will be able to

learn about the performance this way. The financial accounts, financial estimates, and

sustainability claims would be inaccurate and unsupported if any calculate the volume are

disorganised (Finkler, Smith and Calabrese, 2018)

More specifically, accountants ensure that all clients appreciate the value of financial data,

and they collaborate with both people and businesses to help others use financial data to solve

issues. Really, gathering all of the data is the simple part these days; all you have to do is open

accounting tools. Assessing, decoding, and sharing facts is the difficult aspect. Of instance, they

must present it in a straightforward and concise manner when successfully engaging with people

from various professional fields. In almost any case, accounting can now be described as the

method of evaluating and summarising market operations, analysing financial data, and reporting

data to managers as well as other decision-makers.

Importance of accounting in decision making

Aside from that, the nation's economic growth necessitates sufficient, accurate, and essential

knowledge regarding economic decisions through businessmen, employees, state administrators,

as well as others. Along with other aspects of economic growth and administration, the growth of

a books of accounts that can produce the requisite data and be trusted in decision-making is

critical. Financial knowledge that is both qualitative and accurate is critical throughout the

decision-making phase, and its accessibility is of particular significance for market managers and

of national interest in particular.

This information is valuable not just for international investors as well as big enterprises, but also

for smaller firms because it offers crucial information regarding decision-making processes such

as strategy, monitoring, and assessment. The objectives of this research is to have a summary of

financial statement developments as well as knowledge, as well as the impact accounting data

has on judgement, knowledge management requirements, and how they've been actually met, in

attempt to see financial data as being one of the communication for increasing efficiency through

decision-making of economic agents (entities) and then use to reach results (Laruelle, 2021).

marketplace. Before investing in making or lending the capital, lenders and investors have to

learn a few things about each other. So this entails digging around in the company's tax records.

Generally, they must present these income reports to investment managers. They will be able to

learn about the performance this way. The financial accounts, financial estimates, and

sustainability claims would be inaccurate and unsupported if any calculate the volume are

disorganised (Finkler, Smith and Calabrese, 2018)

More specifically, accountants ensure that all clients appreciate the value of financial data,

and they collaborate with both people and businesses to help others use financial data to solve

issues. Really, gathering all of the data is the simple part these days; all you have to do is open

accounting tools. Assessing, decoding, and sharing facts is the difficult aspect. Of instance, they

must present it in a straightforward and concise manner when successfully engaging with people

from various professional fields. In almost any case, accounting can now be described as the

method of evaluating and summarising market operations, analysing financial data, and reporting

data to managers as well as other decision-makers.

Importance of accounting in decision making

Aside from that, the nation's economic growth necessitates sufficient, accurate, and essential

knowledge regarding economic decisions through businessmen, employees, state administrators,

as well as others. Along with other aspects of economic growth and administration, the growth of

a books of accounts that can produce the requisite data and be trusted in decision-making is

critical. Financial knowledge that is both qualitative and accurate is critical throughout the

decision-making phase, and its accessibility is of particular significance for market managers and

of national interest in particular.

This information is valuable not just for international investors as well as big enterprises, but also

for smaller firms because it offers crucial information regarding decision-making processes such

as strategy, monitoring, and assessment. The objectives of this research is to have a summary of

financial statement developments as well as knowledge, as well as the impact accounting data

has on judgement, knowledge management requirements, and how they've been actually met, in

attempt to see financial data as being one of the communication for increasing efficiency through

decision-making of economic agents (entities) and then use to reach results (Laruelle, 2021).

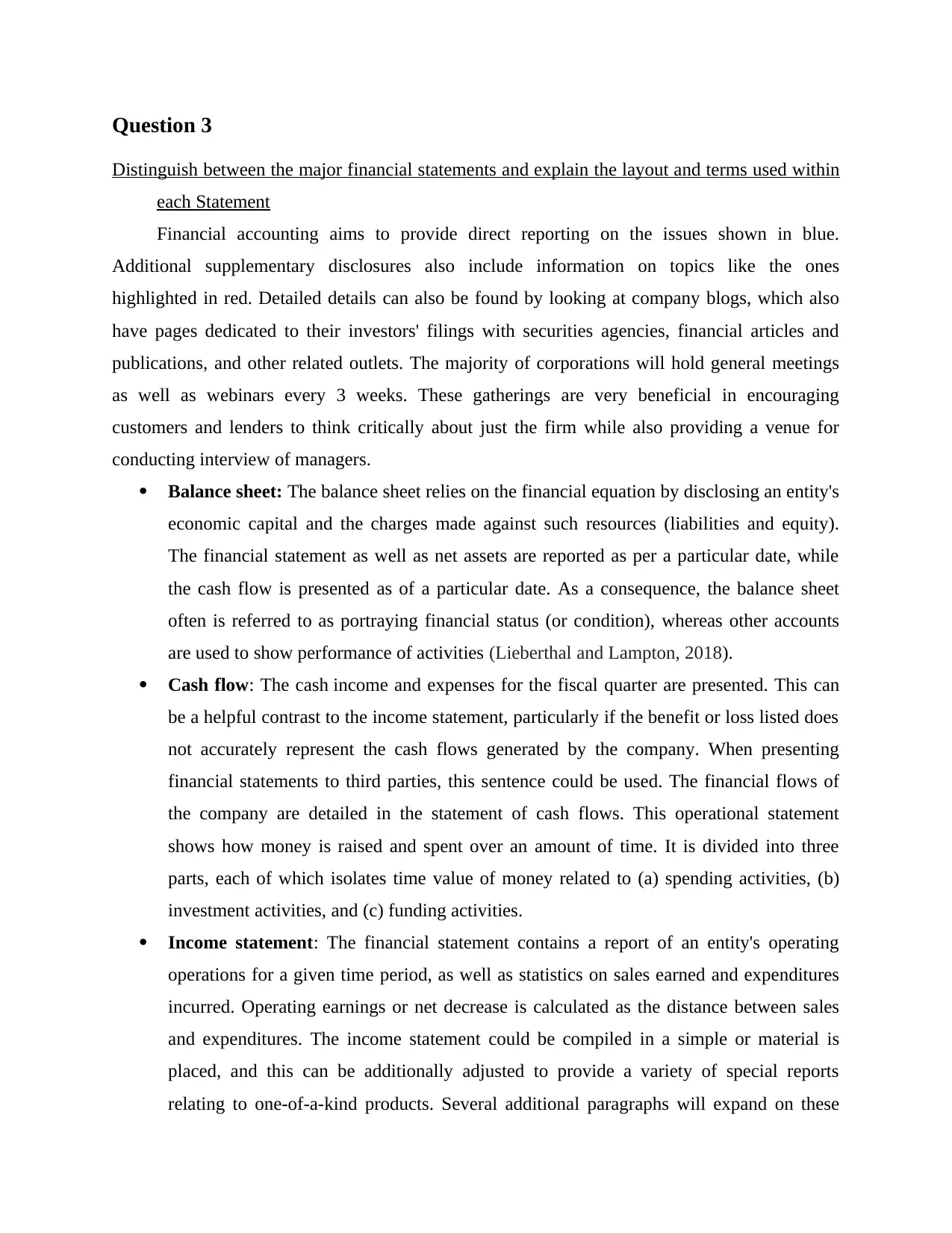

Question 3

Distinguish between the major financial statements and explain the layout and terms used within

each Statement

Financial accounting aims to provide direct reporting on the issues shown in blue.

Additional supplementary disclosures also include information on topics like the ones

highlighted in red. Detailed details can also be found by looking at company blogs, which also

have pages dedicated to their investors' filings with securities agencies, financial articles and

publications, and other related outlets. The majority of corporations will hold general meetings

as well as webinars every 3 weeks. These gatherings are very beneficial in encouraging

customers and lenders to think critically about just the firm while also providing a venue for

conducting interview of managers.

Balance sheet: The balance sheet relies on the financial equation by disclosing an entity's

economic capital and the charges made against such resources (liabilities and equity).

The financial statement as well as net assets are reported as per a particular date, while

the cash flow is presented as of a particular date. As a consequence, the balance sheet

often is referred to as portraying financial status (or condition), whereas other accounts

are used to show performance of activities (Lieberthal and Lampton, 2018).

Cash flow: The cash income and expenses for the fiscal quarter are presented. This can

be a helpful contrast to the income statement, particularly if the benefit or loss listed does

not accurately represent the cash flows generated by the company. When presenting

financial statements to third parties, this sentence could be used. The financial flows of

the company are detailed in the statement of cash flows. This operational statement

shows how money is raised and spent over an amount of time. It is divided into three

parts, each of which isolates time value of money related to (a) spending activities, (b)

investment activities, and (c) funding activities.

Income statement: The financial statement contains a report of an entity's operating

operations for a given time period, as well as statistics on sales earned and expenditures

incurred. Operating earnings or net decrease is calculated as the distance between sales

and expenditures. The income statement could be compiled in a simple or material is

placed, and this can be additionally adjusted to provide a variety of special reports

relating to one-of-a-kind products. Several additional paragraphs will expand on these

Distinguish between the major financial statements and explain the layout and terms used within

each Statement

Financial accounting aims to provide direct reporting on the issues shown in blue.

Additional supplementary disclosures also include information on topics like the ones

highlighted in red. Detailed details can also be found by looking at company blogs, which also

have pages dedicated to their investors' filings with securities agencies, financial articles and

publications, and other related outlets. The majority of corporations will hold general meetings

as well as webinars every 3 weeks. These gatherings are very beneficial in encouraging

customers and lenders to think critically about just the firm while also providing a venue for

conducting interview of managers.

Balance sheet: The balance sheet relies on the financial equation by disclosing an entity's

economic capital and the charges made against such resources (liabilities and equity).

The financial statement as well as net assets are reported as per a particular date, while

the cash flow is presented as of a particular date. As a consequence, the balance sheet

often is referred to as portraying financial status (or condition), whereas other accounts

are used to show performance of activities (Lieberthal and Lampton, 2018).

Cash flow: The cash income and expenses for the fiscal quarter are presented. This can

be a helpful contrast to the income statement, particularly if the benefit or loss listed does

not accurately represent the cash flows generated by the company. When presenting

financial statements to third parties, this sentence could be used. The financial flows of

the company are detailed in the statement of cash flows. This operational statement

shows how money is raised and spent over an amount of time. It is divided into three

parts, each of which isolates time value of money related to (a) spending activities, (b)

investment activities, and (c) funding activities.

Income statement: The financial statement contains a report of an entity's operating

operations for a given time period, as well as statistics on sales earned and expenditures

incurred. Operating earnings or net decrease is calculated as the distance between sales

and expenditures. The income statement could be compiled in a simple or material is

placed, and this can be additionally adjusted to provide a variety of special reports

relating to one-of-a-kind products. Several additional paragraphs will expand on these

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

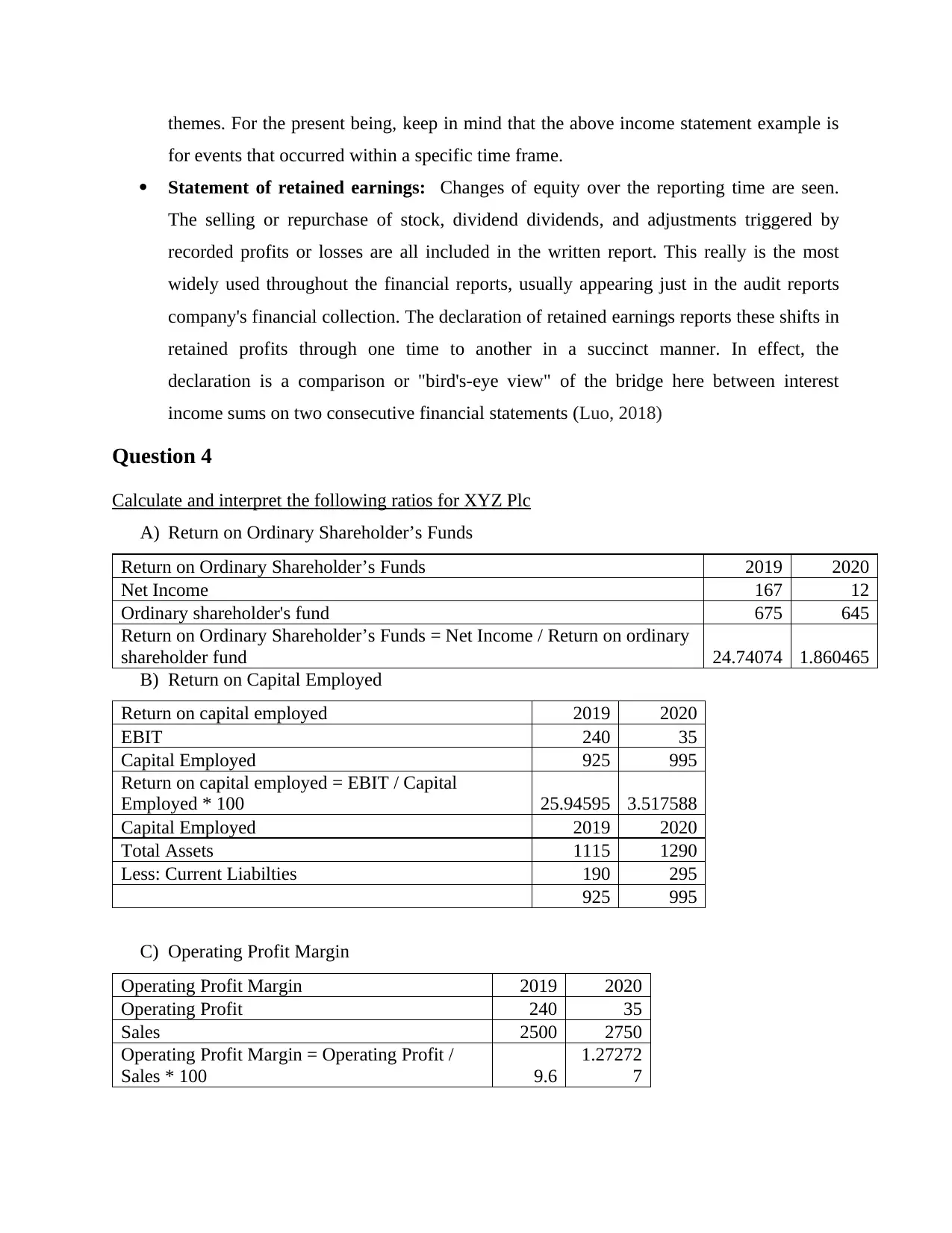

themes. For the present being, keep in mind that the above income statement example is

for events that occurred within a specific time frame.

Statement of retained earnings: Changes of equity over the reporting time are seen.

The selling or repurchase of stock, dividend dividends, and adjustments triggered by

recorded profits or losses are all included in the written report. This really is the most

widely used throughout the financial reports, usually appearing just in the audit reports

company's financial collection. The declaration of retained earnings reports these shifts in

retained profits through one time to another in a succinct manner. In effect, the

declaration is a comparison or "bird's-eye view" of the bridge here between interest

income sums on two consecutive financial statements (Luo, 2018)

Question 4

Calculate and interpret the following ratios for XYZ Plc

A) Return on Ordinary Shareholder’s Funds

Return on Ordinary Shareholder’s Funds 2019 2020

Net Income 167 12

Ordinary shareholder's fund 675 645

Return on Ordinary Shareholder’s Funds = Net Income / Return on ordinary

shareholder fund 24.74074 1.860465

B) Return on Capital Employed

Return on capital employed 2019 2020

EBIT 240 35

Capital Employed 925 995

Return on capital employed = EBIT / Capital

Employed * 100 25.94595 3.517588

Capital Employed 2019 2020

Total Assets 1115 1290

Less: Current Liabilties 190 295

925 995

C) Operating Profit Margin

Operating Profit Margin 2019 2020

Operating Profit 240 35

Sales 2500 2750

Operating Profit Margin = Operating Profit /

Sales * 100 9.6

1.27272

7

for events that occurred within a specific time frame.

Statement of retained earnings: Changes of equity over the reporting time are seen.

The selling or repurchase of stock, dividend dividends, and adjustments triggered by

recorded profits or losses are all included in the written report. This really is the most

widely used throughout the financial reports, usually appearing just in the audit reports

company's financial collection. The declaration of retained earnings reports these shifts in

retained profits through one time to another in a succinct manner. In effect, the

declaration is a comparison or "bird's-eye view" of the bridge here between interest

income sums on two consecutive financial statements (Luo, 2018)

Question 4

Calculate and interpret the following ratios for XYZ Plc

A) Return on Ordinary Shareholder’s Funds

Return on Ordinary Shareholder’s Funds 2019 2020

Net Income 167 12

Ordinary shareholder's fund 675 645

Return on Ordinary Shareholder’s Funds = Net Income / Return on ordinary

shareholder fund 24.74074 1.860465

B) Return on Capital Employed

Return on capital employed 2019 2020

EBIT 240 35

Capital Employed 925 995

Return on capital employed = EBIT / Capital

Employed * 100 25.94595 3.517588

Capital Employed 2019 2020

Total Assets 1115 1290

Less: Current Liabilties 190 295

925 995

C) Operating Profit Margin

Operating Profit Margin 2019 2020

Operating Profit 240 35

Sales 2500 2750

Operating Profit Margin = Operating Profit /

Sales * 100 9.6

1.27272

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

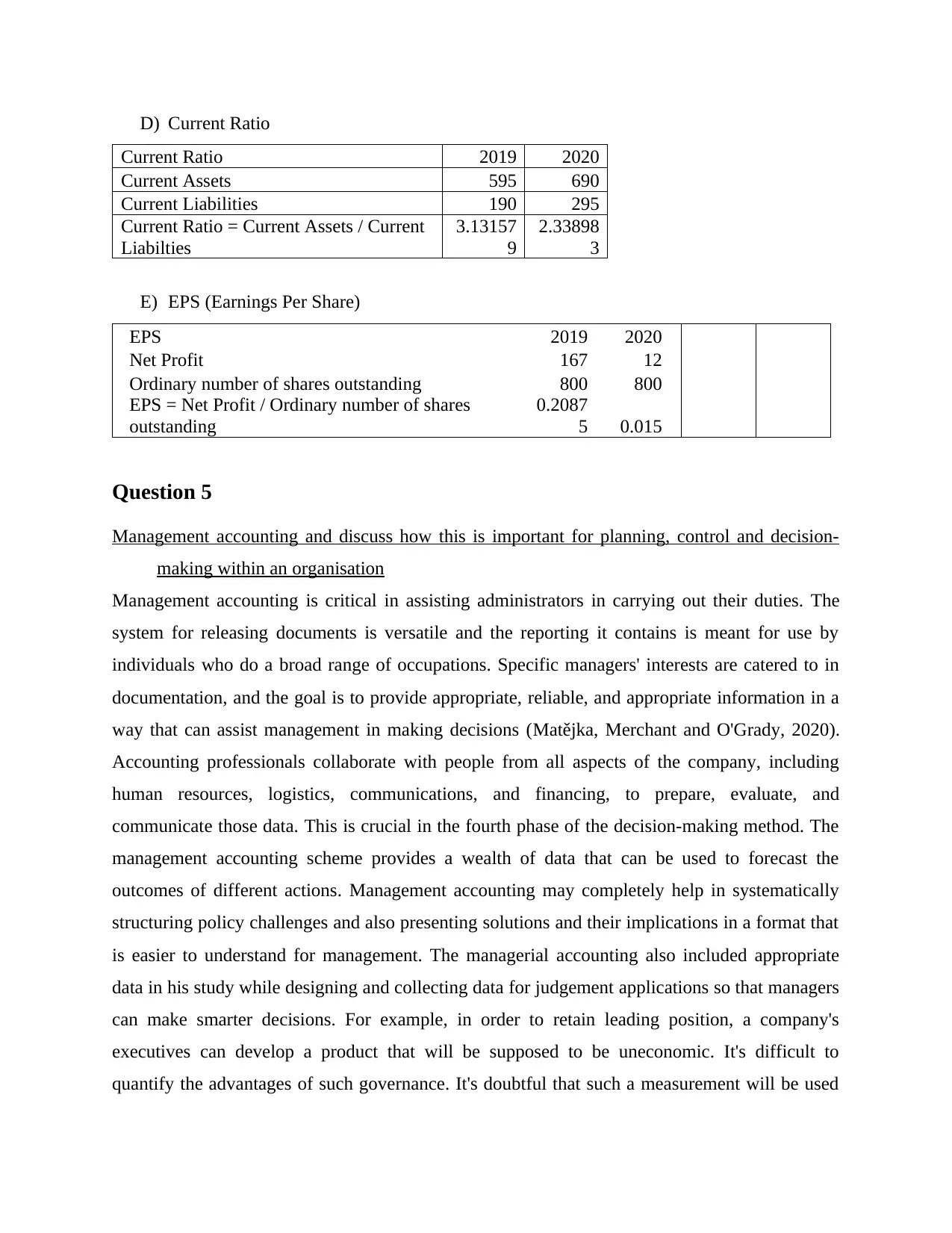

D) Current Ratio

Current Ratio 2019 2020

Current Assets 595 690

Current Liabilities 190 295

Current Ratio = Current Assets / Current

Liabilties

3.13157

9

2.33898

3

E) EPS (Earnings Per Share)

EPS 2019 2020

Net Profit 167 12

Ordinary number of shares outstanding 800 800

EPS = Net Profit / Ordinary number of shares

outstanding

0.2087

5 0.015

Question 5

Management accounting and discuss how this is important for planning, control and decision-

making within an organisation

Management accounting is critical in assisting administrators in carrying out their duties. The

system for releasing documents is versatile and the reporting it contains is meant for use by

individuals who do a broad range of occupations. Specific managers' interests are catered to in

documentation, and the goal is to provide appropriate, reliable, and appropriate information in a

way that can assist management in making decisions (Matějka, Merchant and O'Grady, 2020).

Accounting professionals collaborate with people from all aspects of the company, including

human resources, logistics, communications, and financing, to prepare, evaluate, and

communicate those data. This is crucial in the fourth phase of the decision-making method. The

management accounting scheme provides a wealth of data that can be used to forecast the

outcomes of different actions. Management accounting may completely help in systematically

structuring policy challenges and also presenting solutions and their implications in a format that

is easier to understand for management. The managerial accounting also included appropriate

data in his study while designing and collecting data for judgement applications so that managers

can make smarter decisions. For example, in order to retain leading position, a company's

executives can develop a product that will be supposed to be uneconomic. It's difficult to

quantify the advantages of such governance. It's doubtful that such a measurement will be used

Current Ratio 2019 2020

Current Assets 595 690

Current Liabilities 190 295

Current Ratio = Current Assets / Current

Liabilties

3.13157

9

2.33898

3

E) EPS (Earnings Per Share)

EPS 2019 2020

Net Profit 167 12

Ordinary number of shares outstanding 800 800

EPS = Net Profit / Ordinary number of shares

outstanding

0.2087

5 0.015

Question 5

Management accounting and discuss how this is important for planning, control and decision-

making within an organisation

Management accounting is critical in assisting administrators in carrying out their duties. The

system for releasing documents is versatile and the reporting it contains is meant for use by

individuals who do a broad range of occupations. Specific managers' interests are catered to in

documentation, and the goal is to provide appropriate, reliable, and appropriate information in a

way that can assist management in making decisions (Matějka, Merchant and O'Grady, 2020).

Accounting professionals collaborate with people from all aspects of the company, including

human resources, logistics, communications, and financing, to prepare, evaluate, and

communicate those data. This is crucial in the fourth phase of the decision-making method. The

management accounting scheme provides a wealth of data that can be used to forecast the

outcomes of different actions. Management accounting may completely help in systematically

structuring policy challenges and also presenting solutions and their implications in a format that

is easier to understand for management. The managerial accounting also included appropriate

data in his study while designing and collecting data for judgement applications so that managers

can make smarter decisions. For example, in order to retain leading position, a company's

executives can develop a product that will be supposed to be uneconomic. It's difficult to

quantify the advantages of such governance. It's doubtful that such a measurement will be used

in the marketing employee's assessment of the latest product's viability. However, it's very likely

that even a study based on that review would mention the failure to measure those benefits. That

is, administrative accountants' analyses are quite able to find variables with financial

implications which is not included in the statements (Meyer, 2017).”

Importance

Planning: Although it offers input for decision-making and since the whole budgeting process is

built through accounting-related data, management accounting is tightly integrated into strategy.

MA assists administrators in organising by producing analyses that estimate the impact of certain

activities on an organization's ability to accomplish its objectives. For instance, if a company

purchases a profit objective for the year, it must also decide how to achieve that goal (Musso and

Weare, 2020).

Controlling: Management accounting aids in monitoring by providing production and

management analyses that highlight discrepancies between anticipated and real results. These

reviews serve as a foundation for taking the requisite corrective steps to keep activities under

control. Through use of output and monitoring reports adheres to the leadership by exception

theory. In the event of substantial discrepancies between planned budget and real performance, a

manager would typically examine and decide what went horribly wrong and, where necessary,

which superiors or divisions need assistance.

Decision-making: Making a choice is the act of deciding between opposing options. Each of the

three managerial positions mentioned above, namely planning, organising, and managing,

requires decision-making. A boss can't prepare without making choices, and he or she must pick

between conflicting targets and strategies for achieving those goals. Managers must focus on an

organisational framework and specific steps to be done on a day-to-day basis, just as they must

decide on an organisational goals and functional measures to be taken until day activities.

Managers throughout the control role must determine whether or not variances become worth

examining (Moreland, 2018).

that even a study based on that review would mention the failure to measure those benefits. That

is, administrative accountants' analyses are quite able to find variables with financial

implications which is not included in the statements (Meyer, 2017).”

Importance

Planning: Although it offers input for decision-making and since the whole budgeting process is

built through accounting-related data, management accounting is tightly integrated into strategy.

MA assists administrators in organising by producing analyses that estimate the impact of certain

activities on an organization's ability to accomplish its objectives. For instance, if a company

purchases a profit objective for the year, it must also decide how to achieve that goal (Musso and

Weare, 2020).

Controlling: Management accounting aids in monitoring by providing production and

management analyses that highlight discrepancies between anticipated and real results. These

reviews serve as a foundation for taking the requisite corrective steps to keep activities under

control. Through use of output and monitoring reports adheres to the leadership by exception

theory. In the event of substantial discrepancies between planned budget and real performance, a

manager would typically examine and decide what went horribly wrong and, where necessary,

which superiors or divisions need assistance.

Decision-making: Making a choice is the act of deciding between opposing options. Each of the

three managerial positions mentioned above, namely planning, organising, and managing,

requires decision-making. A boss can't prepare without making choices, and he or she must pick

between conflicting targets and strategies for achieving those goals. Managers must focus on an

organisational framework and specific steps to be done on a day-to-day basis, just as they must

decide on an organisational goals and functional measures to be taken until day activities.

Managers throughout the control role must determine whether or not variances become worth

examining (Moreland, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Cepiku, D., 2020. Performance management in a networked organization: the

OECD. International Journal of Public Sector Management.

Dabbicco, G. and Mattei, G., 2021. The reconciliation of budgeting with financial reporting: A

comparative study of Italy and the UK. Public Money & Management, 41(2), pp.127-

137.

Ferreira, S.J. and Dickason, Z., 2018. The effect of gender and ethnicity on financial risk

tolerance in South African. Gender and Behaviour, 16(1), pp.10851-10862.

Finkler, S.A., Smith, D.L. and Calabrese, T.D., 2018. Financial management for public, health,

and not-for-profit organizations. CQ Press.

Huang, J., Yang, W. and Tu, Y., 2020. Financing mode decision in a supply chain with financial

constraint. International Journal of Production Economics, 220, p.107441.

Laruelle, A., 2021. Voting to select projects in participatory budgeting. European Journal of

Operational Research, 288(2), pp.598-604.

Lieberthal, K.G. and Lampton, D.M. eds., 2018. Bureaucracy, politics, and decision making in

post-Mao China (Vol. 14). University of California Press.

Luo, T., 2018. Research on decision-making of complex venture capital based on financial big

data platform. Complexity, 2018.

Matějka, M., Merchant, K.A. and O'Grady, W., 2020. An empirical investigation of beyond

budgeting practices. Journal of Management Accounting Research, pp.0000-0000.

Meyer, M., 2017. Is financial literacy a determinant of health?. The Patient-Patient-Centered

Outcomes Research, 10(4), pp.381-387.

Moreland, K.A., 2018. Seeking financial advice and other desirable financial behaviors. Journal

of Financial Counseling and Planning, 29(2), pp.198-207.

Musso, J.A. and Weare, C., 2020. Performance management goldilocks style: A transaction cost

analysis of incentive intensity in performance regimes. Public Performance &

Management Review, 43(1), pp.1-27.

Books and Journals

Cepiku, D., 2020. Performance management in a networked organization: the

OECD. International Journal of Public Sector Management.

Dabbicco, G. and Mattei, G., 2021. The reconciliation of budgeting with financial reporting: A

comparative study of Italy and the UK. Public Money & Management, 41(2), pp.127-

137.

Ferreira, S.J. and Dickason, Z., 2018. The effect of gender and ethnicity on financial risk

tolerance in South African. Gender and Behaviour, 16(1), pp.10851-10862.

Finkler, S.A., Smith, D.L. and Calabrese, T.D., 2018. Financial management for public, health,

and not-for-profit organizations. CQ Press.

Huang, J., Yang, W. and Tu, Y., 2020. Financing mode decision in a supply chain with financial

constraint. International Journal of Production Economics, 220, p.107441.

Laruelle, A., 2021. Voting to select projects in participatory budgeting. European Journal of

Operational Research, 288(2), pp.598-604.

Lieberthal, K.G. and Lampton, D.M. eds., 2018. Bureaucracy, politics, and decision making in

post-Mao China (Vol. 14). University of California Press.

Luo, T., 2018. Research on decision-making of complex venture capital based on financial big

data platform. Complexity, 2018.

Matějka, M., Merchant, K.A. and O'Grady, W., 2020. An empirical investigation of beyond

budgeting practices. Journal of Management Accounting Research, pp.0000-0000.

Meyer, M., 2017. Is financial literacy a determinant of health?. The Patient-Patient-Centered

Outcomes Research, 10(4), pp.381-387.

Moreland, K.A., 2018. Seeking financial advice and other desirable financial behaviors. Journal

of Financial Counseling and Planning, 29(2), pp.198-207.

Musso, J.A. and Weare, C., 2020. Performance management goldilocks style: A transaction cost

analysis of incentive intensity in performance regimes. Public Performance &

Management Review, 43(1), pp.1-27.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.