SnappyDrinks Plc: Business Finance Budgeting Report Analysis

VerifiedAdded on 2021/01/02

|15

|3740

|361

Report

AI Summary

This report delves into the core concepts of business finance budgeting, examining the purpose of budgeting, the processes involved in budget preparation, and its application in developing a business model for SnappyDrinks Plc. The report highlights traditional budgeting approaches, such as incremental budgeting, and analyzes their suitability for different parts of a business. It then explores alternative budgeting methods like rolling, zero-based, and activity-based budgeting, discussing their drawbacks and providing examples. The analysis includes a detailed cash flow statement to illustrate the application of budgeting techniques. The report concludes with an assessment of the appropriateness of various budgeting methods for SnappyDrinks Plc, providing valuable insights into cost management and financial planning.

Business Finance Budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

..........................................................................................................................................................2

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

1 The purpose of preparing a budget and the process that company needs to follow as well as

the use of budget in development of a business model...............................................................3

2 Traditional Budgeting approaches to plan the future cost management for the business........5

3 Analysing whether traditional budgetary system is appropriate to all or any parts of the

business in its planned future. ...................................................................................................7

PART 2............................................................................................................................................8

4 Understanding of the alternative budget methods and their drawbacks..................................8

5 Examples of different Budgeting methods mentioned ............................................................9

6 Analysis of the appropriateness of the budgeting method for the company..........................11

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

..........................................................................................................................................................2

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

1 The purpose of preparing a budget and the process that company needs to follow as well as

the use of budget in development of a business model...............................................................3

2 Traditional Budgeting approaches to plan the future cost management for the business........5

3 Analysing whether traditional budgetary system is appropriate to all or any parts of the

business in its planned future. ...................................................................................................7

PART 2............................................................................................................................................8

4 Understanding of the alternative budget methods and their drawbacks..................................8

5 Examples of different Budgeting methods mentioned ............................................................9

6 Analysis of the appropriateness of the budgeting method for the company..........................11

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Budgeting is a planning of a specific budget that outlines the financial and operational

goals of the business. Budget is made to estimate the future expenditure of the business of the

upcoming financial year. The basic process of budgeting involves analysis of the fixed and

variable costs of the business and then deciding to allocate the funds in order to reflect the

organizational goals. This report will highlight the purpose and process of preparing the budget

for business and the contribution of budget in preparing a business model. The report will also

highlight the traditional budgeting approaches and its use in estimating the future cost as well as

the use of traditional budgetary system in different parts of the business. Further the report will

focus on the alternative budget methods to improve on traditional approach along with the

drawbacks.

PART 1

1 The purpose of preparing a budget and the process that company needs to follow as well as the

use of budget in development of a business model.

Purpose- The purpose of preparing a budget serves to three main components- Forecast of income and expenditure- Budgeting is important in the planning process of

the business. The company need to predict its profitability in the business before

implementing any strategy (Kavussanos and Visvikis, 2016). The budget helps in

forecasting the future incomes and expenditure on the basis of past activities and hence

able to forecast the profitability of the business. Tool for decision making- The purpose of the budget is to provide a financial framework

that helps in the decision making process for the company in various activities. For

example the budget predicts the outcomes of the advertising cost and returns and hence

help the company to decide whether to invest the money in advertising activity or

not(Brigham and et.al., 2016).

Monitor business performance- The main purpose of the budgeting is to monitor and

measure the actual business performance with the estimated performance so as to lower

down the variance (difference between the actual and the expected) in the business

(Purpose of Budgeting, 2018).

Budgeting is a planning of a specific budget that outlines the financial and operational

goals of the business. Budget is made to estimate the future expenditure of the business of the

upcoming financial year. The basic process of budgeting involves analysis of the fixed and

variable costs of the business and then deciding to allocate the funds in order to reflect the

organizational goals. This report will highlight the purpose and process of preparing the budget

for business and the contribution of budget in preparing a business model. The report will also

highlight the traditional budgeting approaches and its use in estimating the future cost as well as

the use of traditional budgetary system in different parts of the business. Further the report will

focus on the alternative budget methods to improve on traditional approach along with the

drawbacks.

PART 1

1 The purpose of preparing a budget and the process that company needs to follow as well as the

use of budget in development of a business model.

Purpose- The purpose of preparing a budget serves to three main components- Forecast of income and expenditure- Budgeting is important in the planning process of

the business. The company need to predict its profitability in the business before

implementing any strategy (Kavussanos and Visvikis, 2016). The budget helps in

forecasting the future incomes and expenditure on the basis of past activities and hence

able to forecast the profitability of the business. Tool for decision making- The purpose of the budget is to provide a financial framework

that helps in the decision making process for the company in various activities. For

example the budget predicts the outcomes of the advertising cost and returns and hence

help the company to decide whether to invest the money in advertising activity or

not(Brigham and et.al., 2016).

Monitor business performance- The main purpose of the budgeting is to monitor and

measure the actual business performance with the estimated performance so as to lower

down the variance (difference between the actual and the expected) in the business

(Purpose of Budgeting, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Process of preparing a budget by organization- The following are the steps involved in the

budget preparation of an organization-

11 Strategic Plan- The first step in the budget preparation involves having a written

strategic plan. This thing ensures the use of organizational resources in supporting a

particular strategy of the organization. In simple terms it means budgeting towards the

vision of the company(Antony, Rodgers and Gijo, 2016).

11 Business Goals- The business goals are the steps that the organization takes to

implement its strategic plan and these goals are to be funded by the budget being

prepared. Hence, this step involves implementing the business goals so that the budget

will able to estimate the financial requirements for achieving these goals.

11 Revenue projections- Revenue projections are the estimates of the revenue by the

company in the upcoming year. These projections are based on the historical financial

performance of the company (Webb, 2015). These projections should link with the

organizational goal in order to initiate the business growth.

11 Fixed cost projections- This step involves estimating fixed costs for the company on the

basis of current and past fixed expenses by the company such as salary of the employees,

rent, electricity and other fixed costs of the company.

11 Variable cost projections – It involves the fluctuating costs of the company that needs to

be controlled in order to gain more revenue. For example- supply costs, overtime costs

etc (Gibb, 2016).

11 Annual Goal expenses- This steps involves budgeting the goal oriented costs of the

company. For example- if the sales department of the company has a goal of increasing

the sales by 10% then the cost incurred I achieving this goal such as marketing and

promotional costs, travelling costs etc., should also be estimated by the budget(Doss and

et.al., 2017).

11 Target profit margin- This step involves setting up targets for profits of the company

which is the primary objective of business. Here the estimates of profit are being made as

the targets to be achieved by the company(Fairclough, 2016).

11 Board approval- This step involves the approval of the budget by the board president or

the owner of the company. This involves review of the owner in relation to the expected

performance and the actual performance of the business.

budget preparation of an organization-

11 Strategic Plan- The first step in the budget preparation involves having a written

strategic plan. This thing ensures the use of organizational resources in supporting a

particular strategy of the organization. In simple terms it means budgeting towards the

vision of the company(Antony, Rodgers and Gijo, 2016).

11 Business Goals- The business goals are the steps that the organization takes to

implement its strategic plan and these goals are to be funded by the budget being

prepared. Hence, this step involves implementing the business goals so that the budget

will able to estimate the financial requirements for achieving these goals.

11 Revenue projections- Revenue projections are the estimates of the revenue by the

company in the upcoming year. These projections are based on the historical financial

performance of the company (Webb, 2015). These projections should link with the

organizational goal in order to initiate the business growth.

11 Fixed cost projections- This step involves estimating fixed costs for the company on the

basis of current and past fixed expenses by the company such as salary of the employees,

rent, electricity and other fixed costs of the company.

11 Variable cost projections – It involves the fluctuating costs of the company that needs to

be controlled in order to gain more revenue. For example- supply costs, overtime costs

etc (Gibb, 2016).

11 Annual Goal expenses- This steps involves budgeting the goal oriented costs of the

company. For example- if the sales department of the company has a goal of increasing

the sales by 10% then the cost incurred I achieving this goal such as marketing and

promotional costs, travelling costs etc., should also be estimated by the budget(Doss and

et.al., 2017).

11 Target profit margin- This step involves setting up targets for profits of the company

which is the primary objective of business. Here the estimates of profit are being made as

the targets to be achieved by the company(Fairclough, 2016).

11 Board approval- This step involves the approval of the budget by the board president or

the owner of the company. This involves review of the owner in relation to the expected

performance and the actual performance of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11 Budget review- Here the Budget is reviewed by a particular committee in-charged and

the various variances in the performance are being identified along with the issues with it

(10 Steps to Developing and Managing a Budget, 2016).

111 Dealing with budget variances- In this step there is the determination of the cause for

the variance identified in the above step and the strategies and solutions to reduce this

variances are being implemented to improve the actual performance(Loader and Norton,

2015).

Use of budget process in developing a business model for SnappyDrinks Plc-

The development of business model for SnappyDrinks Plc involves different activities and the

use of budget steps for this development are given below-

Innovation process of the new product (Health drink with Low-sugar exotic fruit

flavours)- The budget steps such as determination of fixed and variable costs of the

product will give a clear picture of the total cost of the innovation process.

Planning of marketing campaign- The marketing campaign needs to be planned in

order to carry forward the goods innovated in the market. This will involve the annual

goal expenses estimation by budget process that will include the cost of the different

marketing and sales goals by SnappyDrinks Plc(Dhingra and et.al., 2016).

Expansion of the sales team- This will include the estimation of the revenues from the

budget process of the company so that managers of SnappyDrinks Plc are able to

undertake the cost of increasing the sales staffs of the company.

Expansion of the business in other countries- SnappyDrinks Plc is planning to expand

its business in Gulf countries, North America and China. So the company needs to frame

a strategic plan for this process as well as estimate the revenues of the company so that it

gets an clear idea of investing those funds in these countries.

2 Traditional Budgeting approaches to plan the future cost management for the business

Traditional budgeting is a method of budgeting that depends on the exact preceding year's

spending to the budgeting of the current year. The companies prefer this type of budgeting in

order to prepare the budget quickly with the available data without any complications(Webb,

2015).

the various variances in the performance are being identified along with the issues with it

(10 Steps to Developing and Managing a Budget, 2016).

111 Dealing with budget variances- In this step there is the determination of the cause for

the variance identified in the above step and the strategies and solutions to reduce this

variances are being implemented to improve the actual performance(Loader and Norton,

2015).

Use of budget process in developing a business model for SnappyDrinks Plc-

The development of business model for SnappyDrinks Plc involves different activities and the

use of budget steps for this development are given below-

Innovation process of the new product (Health drink with Low-sugar exotic fruit

flavours)- The budget steps such as determination of fixed and variable costs of the

product will give a clear picture of the total cost of the innovation process.

Planning of marketing campaign- The marketing campaign needs to be planned in

order to carry forward the goods innovated in the market. This will involve the annual

goal expenses estimation by budget process that will include the cost of the different

marketing and sales goals by SnappyDrinks Plc(Dhingra and et.al., 2016).

Expansion of the sales team- This will include the estimation of the revenues from the

budget process of the company so that managers of SnappyDrinks Plc are able to

undertake the cost of increasing the sales staffs of the company.

Expansion of the business in other countries- SnappyDrinks Plc is planning to expand

its business in Gulf countries, North America and China. So the company needs to frame

a strategic plan for this process as well as estimate the revenues of the company so that it

gets an clear idea of investing those funds in these countries.

2 Traditional Budgeting approaches to plan the future cost management for the business

Traditional budgeting is a method of budgeting that depends on the exact preceding year's

spending to the budgeting of the current year. The companies prefer this type of budgeting in

order to prepare the budget quickly with the available data without any complications(Webb,

2015).

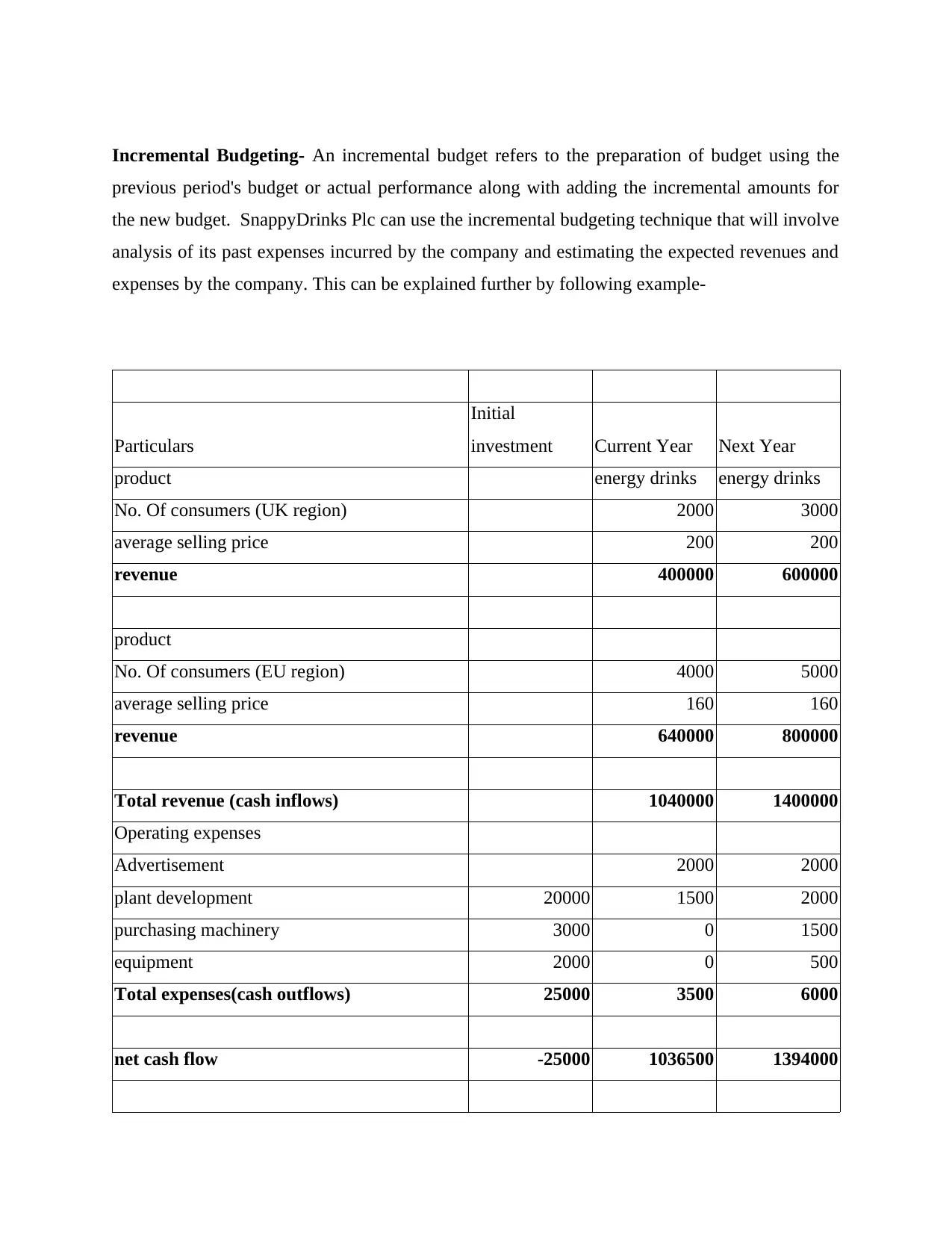

Incremental Budgeting- An incremental budget refers to the preparation of budget using the

previous period's budget or actual performance along with adding the incremental amounts for

the new budget. SnappyDrinks Plc can use the incremental budgeting technique that will involve

analysis of its past expenses incurred by the company and estimating the expected revenues and

expenses by the company. This can be explained further by following example-

Particulars

Initial

investment Current Year Next Year

product energy drinks energy drinks

No. Of consumers (UK region) 2000 3000

average selling price 200 200

revenue 400000 600000

product

No. Of consumers (EU region) 4000 5000

average selling price 160 160

revenue 640000 800000

Total revenue (cash inflows) 1040000 1400000

Operating expenses

Advertisement 2000 2000

plant development 20000 1500 2000

purchasing machinery 3000 0 1500

equipment 2000 0 500

Total expenses(cash outflows) 25000 3500 6000

net cash flow -25000 1036500 1394000

previous period's budget or actual performance along with adding the incremental amounts for

the new budget. SnappyDrinks Plc can use the incremental budgeting technique that will involve

analysis of its past expenses incurred by the company and estimating the expected revenues and

expenses by the company. This can be explained further by following example-

Particulars

Initial

investment Current Year Next Year

product energy drinks energy drinks

No. Of consumers (UK region) 2000 3000

average selling price 200 200

revenue 400000 600000

product

No. Of consumers (EU region) 4000 5000

average selling price 160 160

revenue 640000 800000

Total revenue (cash inflows) 1040000 1400000

Operating expenses

Advertisement 2000 2000

plant development 20000 1500 2000

purchasing machinery 3000 0 1500

equipment 2000 0 500

Total expenses(cash outflows) 25000 3500 6000

net cash flow -25000 1036500 1394000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

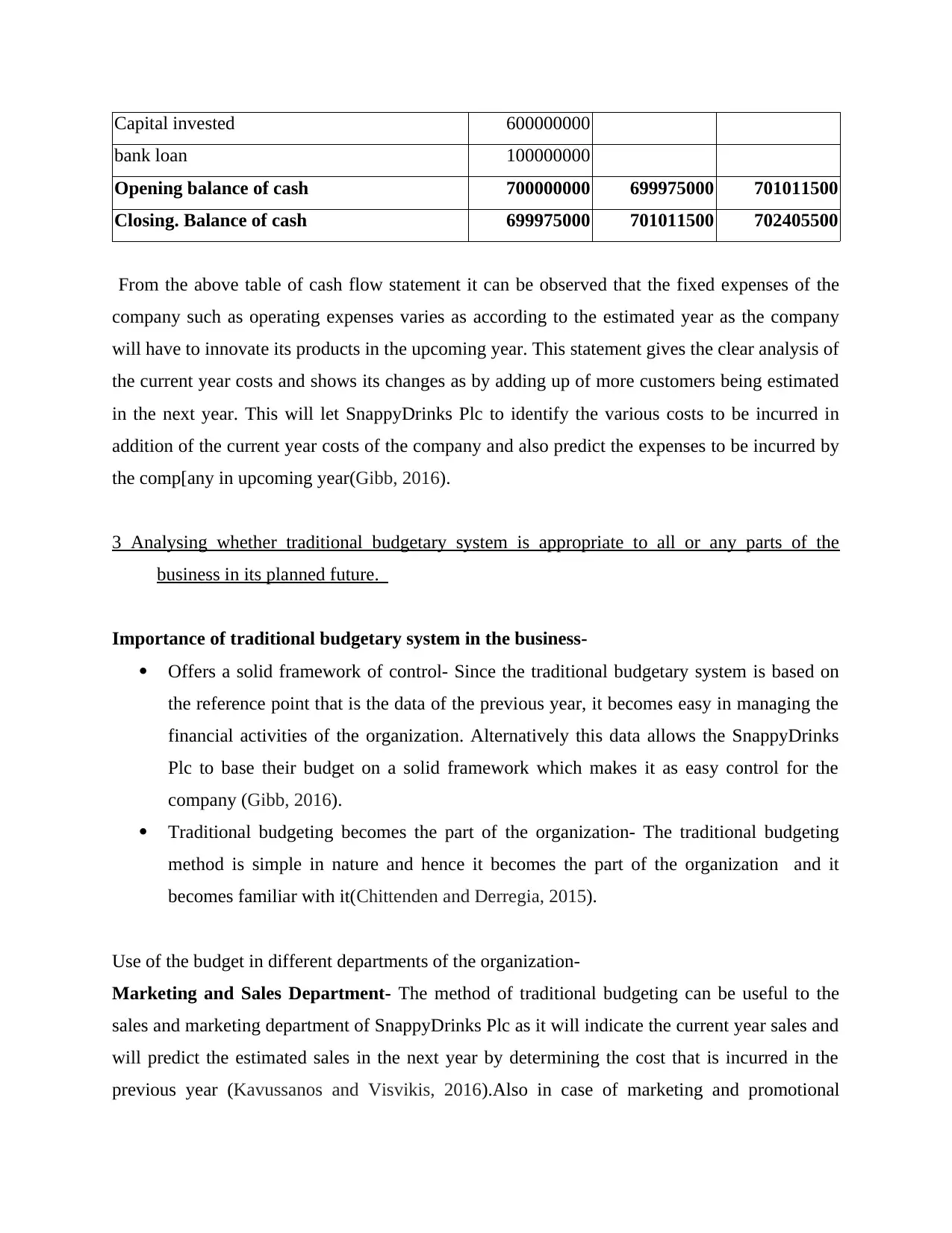

Capital invested 600000000

bank loan 100000000

Opening balance of cash 700000000 699975000 701011500

Closing. Balance of cash 699975000 701011500 702405500

From the above table of cash flow statement it can be observed that the fixed expenses of the

company such as operating expenses varies as according to the estimated year as the company

will have to innovate its products in the upcoming year. This statement gives the clear analysis of

the current year costs and shows its changes as by adding up of more customers being estimated

in the next year. This will let SnappyDrinks Plc to identify the various costs to be incurred in

addition of the current year costs of the company and also predict the expenses to be incurred by

the comp[any in upcoming year(Gibb, 2016).

3 Analysing whether traditional budgetary system is appropriate to all or any parts of the

business in its planned future.

Importance of traditional budgetary system in the business-

Offers a solid framework of control- Since the traditional budgetary system is based on

the reference point that is the data of the previous year, it becomes easy in managing the

financial activities of the organization. Alternatively this data allows the SnappyDrinks

Plc to base their budget on a solid framework which makes it as easy control for the

company (Gibb, 2016).

Traditional budgeting becomes the part of the organization- The traditional budgeting

method is simple in nature and hence it becomes the part of the organization and it

becomes familiar with it(Chittenden and Derregia, 2015).

Use of the budget in different departments of the organization-

Marketing and Sales Department- The method of traditional budgeting can be useful to the

sales and marketing department of SnappyDrinks Plc as it will indicate the current year sales and

will predict the estimated sales in the next year by determining the cost that is incurred in the

previous year (Kavussanos and Visvikis, 2016).Also in case of marketing and promotional

bank loan 100000000

Opening balance of cash 700000000 699975000 701011500

Closing. Balance of cash 699975000 701011500 702405500

From the above table of cash flow statement it can be observed that the fixed expenses of the

company such as operating expenses varies as according to the estimated year as the company

will have to innovate its products in the upcoming year. This statement gives the clear analysis of

the current year costs and shows its changes as by adding up of more customers being estimated

in the next year. This will let SnappyDrinks Plc to identify the various costs to be incurred in

addition of the current year costs of the company and also predict the expenses to be incurred by

the comp[any in upcoming year(Gibb, 2016).

3 Analysing whether traditional budgetary system is appropriate to all or any parts of the

business in its planned future.

Importance of traditional budgetary system in the business-

Offers a solid framework of control- Since the traditional budgetary system is based on

the reference point that is the data of the previous year, it becomes easy in managing the

financial activities of the organization. Alternatively this data allows the SnappyDrinks

Plc to base their budget on a solid framework which makes it as easy control for the

company (Gibb, 2016).

Traditional budgeting becomes the part of the organization- The traditional budgeting

method is simple in nature and hence it becomes the part of the organization and it

becomes familiar with it(Chittenden and Derregia, 2015).

Use of the budget in different departments of the organization-

Marketing and Sales Department- The method of traditional budgeting can be useful to the

sales and marketing department of SnappyDrinks Plc as it will indicate the current year sales and

will predict the estimated sales in the next year by determining the cost that is incurred in the

previous year (Kavussanos and Visvikis, 2016).Also in case of marketing and promotional

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

activities the method will flash the outcomes of promotional activities in previous year and be

able to predict the next year expenses.

Operations department- The traditional budget system will display the previous year cost of

production incurred and thus it will predict the upcoming year's cost as according to the rising

demand and inflation in the economy(Morcol and et.al., 2017).

Finance department- Traditional budgetary system can be useful for the finance department to

determine the profit of the company as on the basis of the previous year's profit. Also, the

company can be able to analyse its financial stability.

Thus, the traditional budget approach will be appropriate to all the parts of the

organization in estimating the costs and revenues for SnappyDrinks Plc.

PART 2

4 Understanding of the alternative budget methods and their drawbacks

Rolling budget method- Rolling budget also known as continuous budgeting involves

continuous update of the new budget period after the completion of one budget period. It simply

involves the incremental extension of the existing budget model. This helps the business in

always having a budget that extends one year into future.

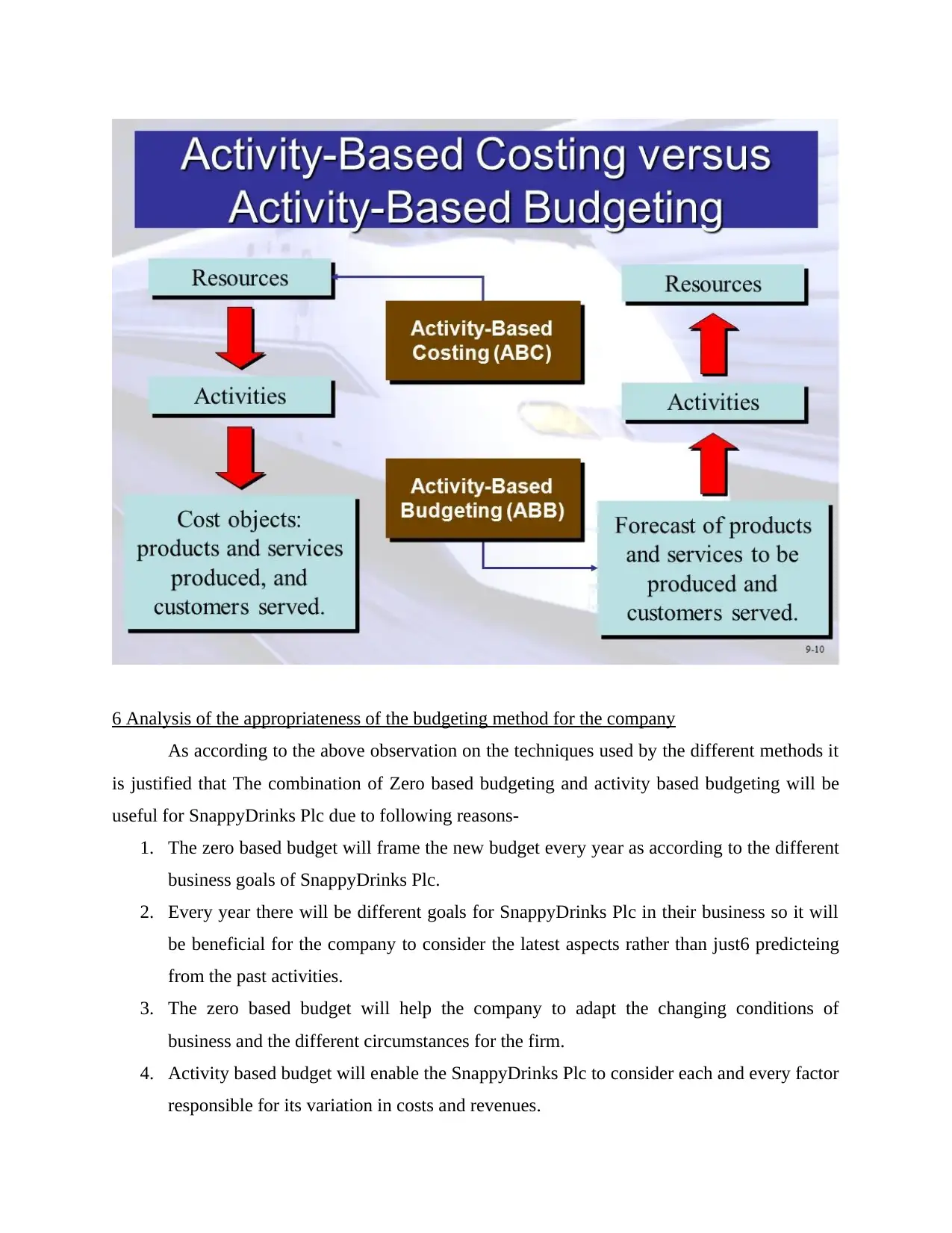

Zero based budgeting method- Zero based budgeting is a method in which all the expenses are

justified for every new period. The process starts with zero base and every function of the

organization is analysed for its needs and costs. Budgets are later built around the requirements

for the upcoming period(Storey, 2016).

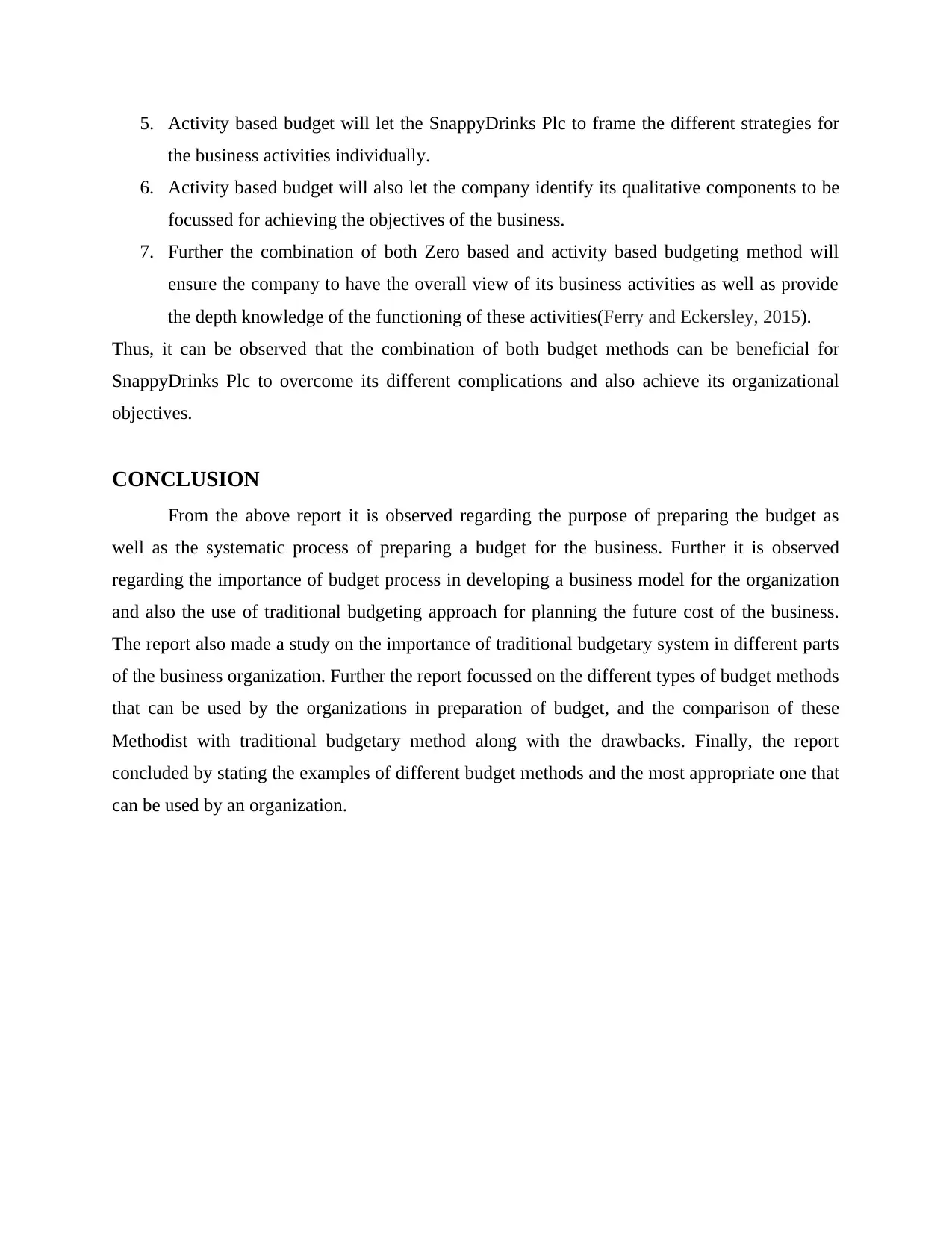

Activity based budgeting method- Activity based budgeting is a system that records, researches

and analyses the activities that leads to the cost for a business. Activity based budgets are more

than adjusting previous budgets to account for inflation or business development. This method

considers both qualitative and quantitative aspects of the budget for the company(Kavussanos

and Visvikis, 2016).

Improvement attempts of the methods on the traditional approach

able to predict the next year expenses.

Operations department- The traditional budget system will display the previous year cost of

production incurred and thus it will predict the upcoming year's cost as according to the rising

demand and inflation in the economy(Morcol and et.al., 2017).

Finance department- Traditional budgetary system can be useful for the finance department to

determine the profit of the company as on the basis of the previous year's profit. Also, the

company can be able to analyse its financial stability.

Thus, the traditional budget approach will be appropriate to all the parts of the

organization in estimating the costs and revenues for SnappyDrinks Plc.

PART 2

4 Understanding of the alternative budget methods and their drawbacks

Rolling budget method- Rolling budget also known as continuous budgeting involves

continuous update of the new budget period after the completion of one budget period. It simply

involves the incremental extension of the existing budget model. This helps the business in

always having a budget that extends one year into future.

Zero based budgeting method- Zero based budgeting is a method in which all the expenses are

justified for every new period. The process starts with zero base and every function of the

organization is analysed for its needs and costs. Budgets are later built around the requirements

for the upcoming period(Storey, 2016).

Activity based budgeting method- Activity based budgeting is a system that records, researches

and analyses the activities that leads to the cost for a business. Activity based budgets are more

than adjusting previous budgets to account for inflation or business development. This method

considers both qualitative and quantitative aspects of the budget for the company(Kavussanos

and Visvikis, 2016).

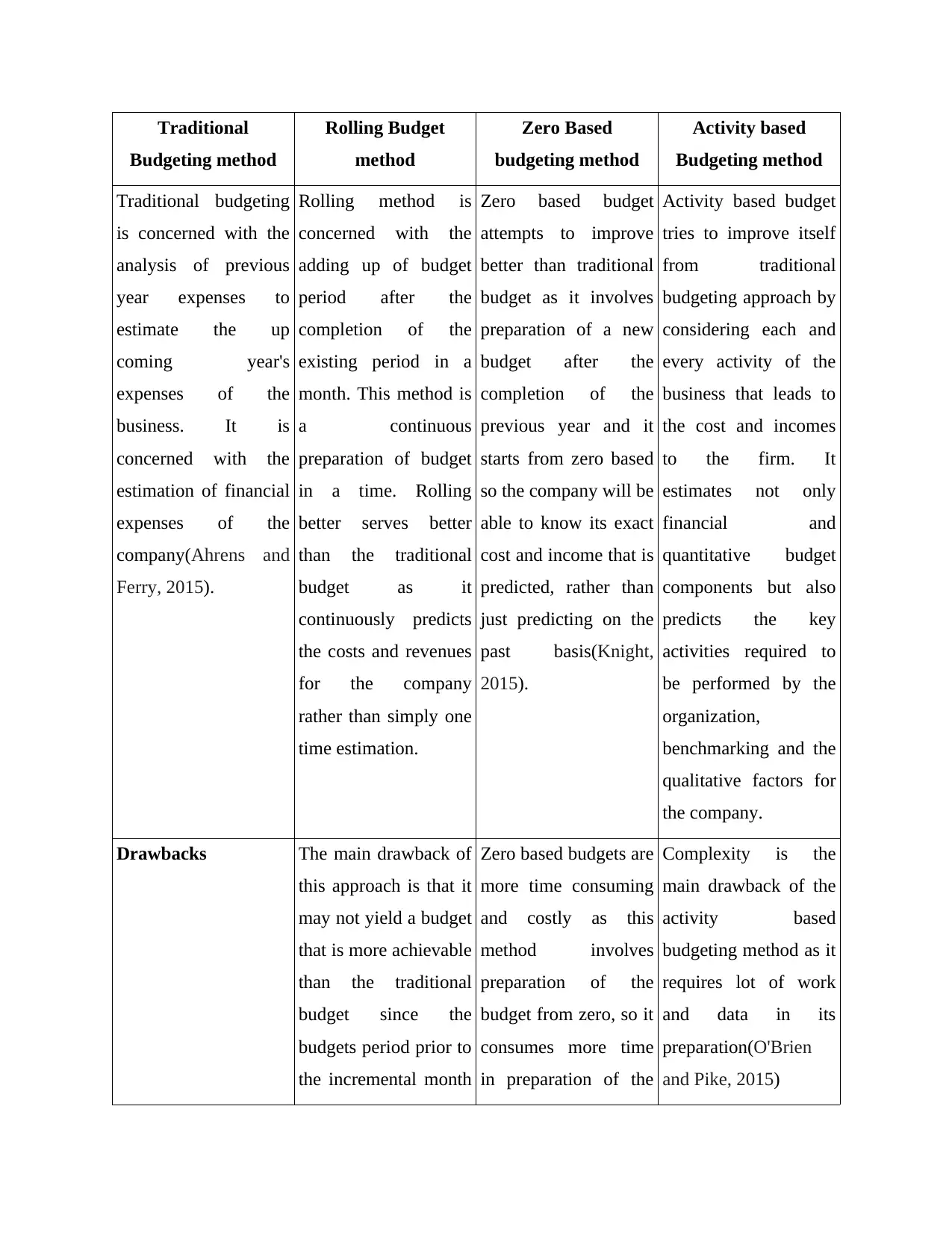

Improvement attempts of the methods on the traditional approach

Traditional

Budgeting method

Rolling Budget

method

Zero Based

budgeting method

Activity based

Budgeting method

Traditional budgeting

is concerned with the

analysis of previous

year expenses to

estimate the up

coming year's

expenses of the

business. It is

concerned with the

estimation of financial

expenses of the

company(Ahrens and

Ferry, 2015).

Rolling method is

concerned with the

adding up of budget

period after the

completion of the

existing period in a

month. This method is

a continuous

preparation of budget

in a time. Rolling

better serves better

than the traditional

budget as it

continuously predicts

the costs and revenues

for the company

rather than simply one

time estimation.

Zero based budget

attempts to improve

better than traditional

budget as it involves

preparation of a new

budget after the

completion of the

previous year and it

starts from zero based

so the company will be

able to know its exact

cost and income that is

predicted, rather than

just predicting on the

past basis(Knight,

2015).

Activity based budget

tries to improve itself

from traditional

budgeting approach by

considering each and

every activity of the

business that leads to

the cost and incomes

to the firm. It

estimates not only

financial and

quantitative budget

components but also

predicts the key

activities required to

be performed by the

organization,

benchmarking and the

qualitative factors for

the company.

Drawbacks The main drawback of

this approach is that it

may not yield a budget

that is more achievable

than the traditional

budget since the

budgets period prior to

the incremental month

Zero based budgets are

more time consuming

and costly as this

method involves

preparation of the

budget from zero, so it

consumes more time

in preparation of the

Complexity is the

main drawback of the

activity based

budgeting method as it

requires lot of work

and data in its

preparation(O'Brien

and Pike, 2015)

Budgeting method

Rolling Budget

method

Zero Based

budgeting method

Activity based

Budgeting method

Traditional budgeting

is concerned with the

analysis of previous

year expenses to

estimate the up

coming year's

expenses of the

business. It is

concerned with the

estimation of financial

expenses of the

company(Ahrens and

Ferry, 2015).

Rolling method is

concerned with the

adding up of budget

period after the

completion of the

existing period in a

month. This method is

a continuous

preparation of budget

in a time. Rolling

better serves better

than the traditional

budget as it

continuously predicts

the costs and revenues

for the company

rather than simply one

time estimation.

Zero based budget

attempts to improve

better than traditional

budget as it involves

preparation of a new

budget after the

completion of the

previous year and it

starts from zero based

so the company will be

able to know its exact

cost and income that is

predicted, rather than

just predicting on the

past basis(Knight,

2015).

Activity based budget

tries to improve itself

from traditional

budgeting approach by

considering each and

every activity of the

business that leads to

the cost and incomes

to the firm. It

estimates not only

financial and

quantitative budget

components but also

predicts the key

activities required to

be performed by the

organization,

benchmarking and the

qualitative factors for

the company.

Drawbacks The main drawback of

this approach is that it

may not yield a budget

that is more achievable

than the traditional

budget since the

budgets period prior to

the incremental month

Zero based budgets are

more time consuming

and costly as this

method involves

preparation of the

budget from zero, so it

consumes more time

in preparation of the

Complexity is the

main drawback of the

activity based

budgeting method as it

requires lot of work

and data in its

preparation(O'Brien

and Pike, 2015)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

just added are not

revised(Martin and

Hofmann, 2017).

budget along with the

cost at every time.

5 Examples of different Budgeting methods mentioned

Rolling Budgeting Method-

Zero Based Budgeting method-

Activity based Budgeting method-

revised(Martin and

Hofmann, 2017).

budget along with the

cost at every time.

5 Examples of different Budgeting methods mentioned

Rolling Budgeting Method-

Zero Based Budgeting method-

Activity based Budgeting method-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6 Analysis of the appropriateness of the budgeting method for the company

As according to the above observation on the techniques used by the different methods it

is justified that The combination of Zero based budgeting and activity based budgeting will be

useful for SnappyDrinks Plc due to following reasons-

1. The zero based budget will frame the new budget every year as according to the different

business goals of SnappyDrinks Plc.

2. Every year there will be different goals for SnappyDrinks Plc in their business so it will

be beneficial for the company to consider the latest aspects rather than just6 predicteing

from the past activities.

3. The zero based budget will help the company to adapt the changing conditions of

business and the different circumstances for the firm.

4. Activity based budget will enable the SnappyDrinks Plc to consider each and every factor

responsible for its variation in costs and revenues.

As according to the above observation on the techniques used by the different methods it

is justified that The combination of Zero based budgeting and activity based budgeting will be

useful for SnappyDrinks Plc due to following reasons-

1. The zero based budget will frame the new budget every year as according to the different

business goals of SnappyDrinks Plc.

2. Every year there will be different goals for SnappyDrinks Plc in their business so it will

be beneficial for the company to consider the latest aspects rather than just6 predicteing

from the past activities.

3. The zero based budget will help the company to adapt the changing conditions of

business and the different circumstances for the firm.

4. Activity based budget will enable the SnappyDrinks Plc to consider each and every factor

responsible for its variation in costs and revenues.

5. Activity based budget will let the SnappyDrinks Plc to frame the different strategies for

the business activities individually.

6. Activity based budget will also let the company identify its qualitative components to be

focussed for achieving the objectives of the business.

7. Further the combination of both Zero based and activity based budgeting method will

ensure the company to have the overall view of its business activities as well as provide

the depth knowledge of the functioning of these activities(Ferry and Eckersley, 2015).

Thus, it can be observed that the combination of both budget methods can be beneficial for

SnappyDrinks Plc to overcome its different complications and also achieve its organizational

objectives.

CONCLUSION

From the above report it is observed regarding the purpose of preparing the budget as

well as the systematic process of preparing a budget for the business. Further it is observed

regarding the importance of budget process in developing a business model for the organization

and also the use of traditional budgeting approach for planning the future cost of the business.

The report also made a study on the importance of traditional budgetary system in different parts

of the business organization. Further the report focussed on the different types of budget methods

that can be used by the organizations in preparation of budget, and the comparison of these

Methodist with traditional budgetary method along with the drawbacks. Finally, the report

concluded by stating the examples of different budget methods and the most appropriate one that

can be used by an organization.

the business activities individually.

6. Activity based budget will also let the company identify its qualitative components to be

focussed for achieving the objectives of the business.

7. Further the combination of both Zero based and activity based budgeting method will

ensure the company to have the overall view of its business activities as well as provide

the depth knowledge of the functioning of these activities(Ferry and Eckersley, 2015).

Thus, it can be observed that the combination of both budget methods can be beneficial for

SnappyDrinks Plc to overcome its different complications and also achieve its organizational

objectives.

CONCLUSION

From the above report it is observed regarding the purpose of preparing the budget as

well as the systematic process of preparing a budget for the business. Further it is observed

regarding the importance of budget process in developing a business model for the organization

and also the use of traditional budgeting approach for planning the future cost of the business.

The report also made a study on the importance of traditional budgetary system in different parts

of the business organization. Further the report focussed on the different types of budget methods

that can be used by the organizations in preparation of budget, and the comparison of these

Methodist with traditional budgetary method along with the drawbacks. Finally, the report

concluded by stating the examples of different budget methods and the most appropriate one that

can be used by an organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.