ACC3004 Business Finance: Portfolio Analysis of CBA and Lez Foxwell

VerifiedAdded on 2023/06/07

|19

|2826

|361

Report

AI Summary

This report provides a comprehensive analysis of several business finance issues. It begins with a case study on CBA (Commonwealth Bank of Australia) valuation, calculating market capitalization, forecasting cash flows, determining return on shares, and analyzing remuneration policies. It further examines CBA's dividend policy, calculating growth rates in EPS and prospective P/E ratios. The report then transitions to a capital budgeting case study involving Lez Foxwell, evaluating project viability using payback period and discounted payback period methods, and comparing these with net present value (NPV) analysis under different cost of capital scenarios. The report concludes by providing detailed calculations and justifications for investment decisions based on the financial metrics assessed.

RUNNING HEAD: BUSINESS FINANCE

Business finance

Business finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business finance 2

Contents

Requirement 1.............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................3

Question 3...............................................................................................................................................4

Question 4...............................................................................................................................................4

Question 5...............................................................................................................................................5

Question 6...............................................................................................................................................6

Requirement 2.............................................................................................................................................6

Question 4...............................................................................................................................................6

Requirement 3.............................................................................................................................................7

Question 1...............................................................................................................................................7

Question 2...............................................................................................................................................8

Question 3.............................................................................................................................................10

Requirement 4...........................................................................................................................................12

Question 4.............................................................................................................................................12

Question 5.............................................................................................................................................13

Question 7.............................................................................................................................................15

Requirement 5...........................................................................................................................................16

References.................................................................................................................................................18

Contents

Requirement 1.............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................3

Question 3...............................................................................................................................................4

Question 4...............................................................................................................................................4

Question 5...............................................................................................................................................5

Question 6...............................................................................................................................................6

Requirement 2.............................................................................................................................................6

Question 4...............................................................................................................................................6

Requirement 3.............................................................................................................................................7

Question 1...............................................................................................................................................7

Question 2...............................................................................................................................................8

Question 3.............................................................................................................................................10

Requirement 4...........................................................................................................................................12

Question 4.............................................................................................................................................12

Question 5.............................................................................................................................................13

Question 7.............................................................................................................................................15

Requirement 5...........................................................................................................................................16

References.................................................................................................................................................18

Business finance 3

Requirement 1

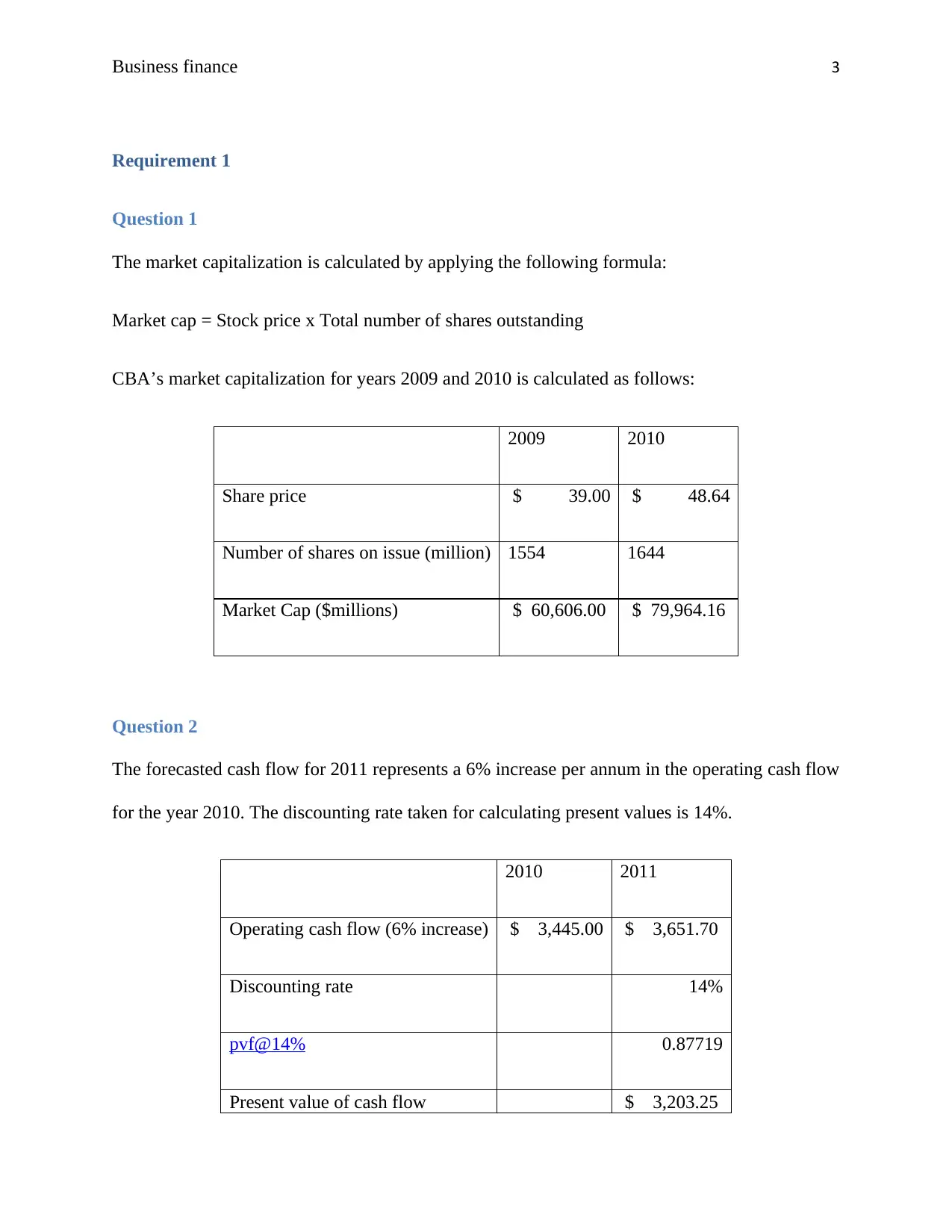

Question 1

The market capitalization is calculated by applying the following formula:

Market cap = Stock price x Total number of shares outstanding

CBA’s market capitalization for years 2009 and 2010 is calculated as follows:

2009 2010

Share price $ 39.00 $ 48.64

Number of shares on issue (million) 1554 1644

Market Cap ($millions) $ 60,606.00 $ 79,964.16

Question 2

The forecasted cash flow for 2011 represents a 6% increase per annum in the operating cash flow

for the year 2010. The discounting rate taken for calculating present values is 14%.

2010 2011

Operating cash flow (6% increase) $ 3,445.00 $ 3,651.70

Discounting rate 14%

pvf@14% 0.87719

Present value of cash flow $ 3,203.25

Requirement 1

Question 1

The market capitalization is calculated by applying the following formula:

Market cap = Stock price x Total number of shares outstanding

CBA’s market capitalization for years 2009 and 2010 is calculated as follows:

2009 2010

Share price $ 39.00 $ 48.64

Number of shares on issue (million) 1554 1644

Market Cap ($millions) $ 60,606.00 $ 79,964.16

Question 2

The forecasted cash flow for 2011 represents a 6% increase per annum in the operating cash flow

for the year 2010. The discounting rate taken for calculating present values is 14%.

2010 2011

Operating cash flow (6% increase) $ 3,445.00 $ 3,651.70

Discounting rate 14%

pvf@14% 0.87719

Present value of cash flow $ 3,203.25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business finance 4

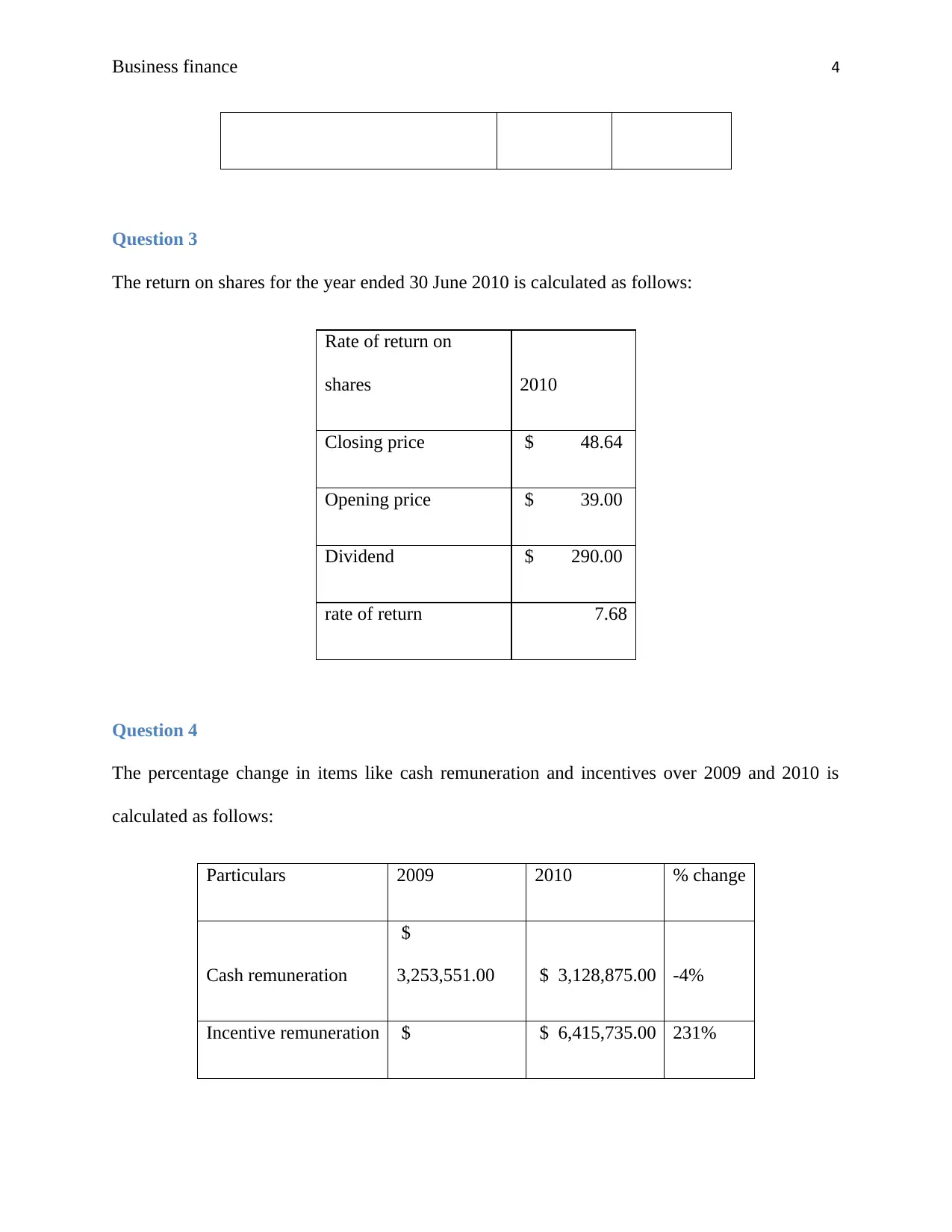

Question 3

The return on shares for the year ended 30 June 2010 is calculated as follows:

Rate of return on

shares 2010

Closing price $ 48.64

Opening price $ 39.00

Dividend $ 290.00

rate of return 7.68

Question 4

The percentage change in items like cash remuneration and incentives over 2009 and 2010 is

calculated as follows:

Particulars 2009 2010 % change

Cash remuneration

$

3,253,551.00 $ 3,128,875.00 -4%

Incentive remuneration $ $ 6,415,735.00 231%

Question 3

The return on shares for the year ended 30 June 2010 is calculated as follows:

Rate of return on

shares 2010

Closing price $ 48.64

Opening price $ 39.00

Dividend $ 290.00

rate of return 7.68

Question 4

The percentage change in items like cash remuneration and incentives over 2009 and 2010 is

calculated as follows:

Particulars 2009 2010 % change

Cash remuneration

$

3,253,551.00 $ 3,128,875.00 -4%

Incentive remuneration $ $ 6,415,735.00 231%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business finance 5

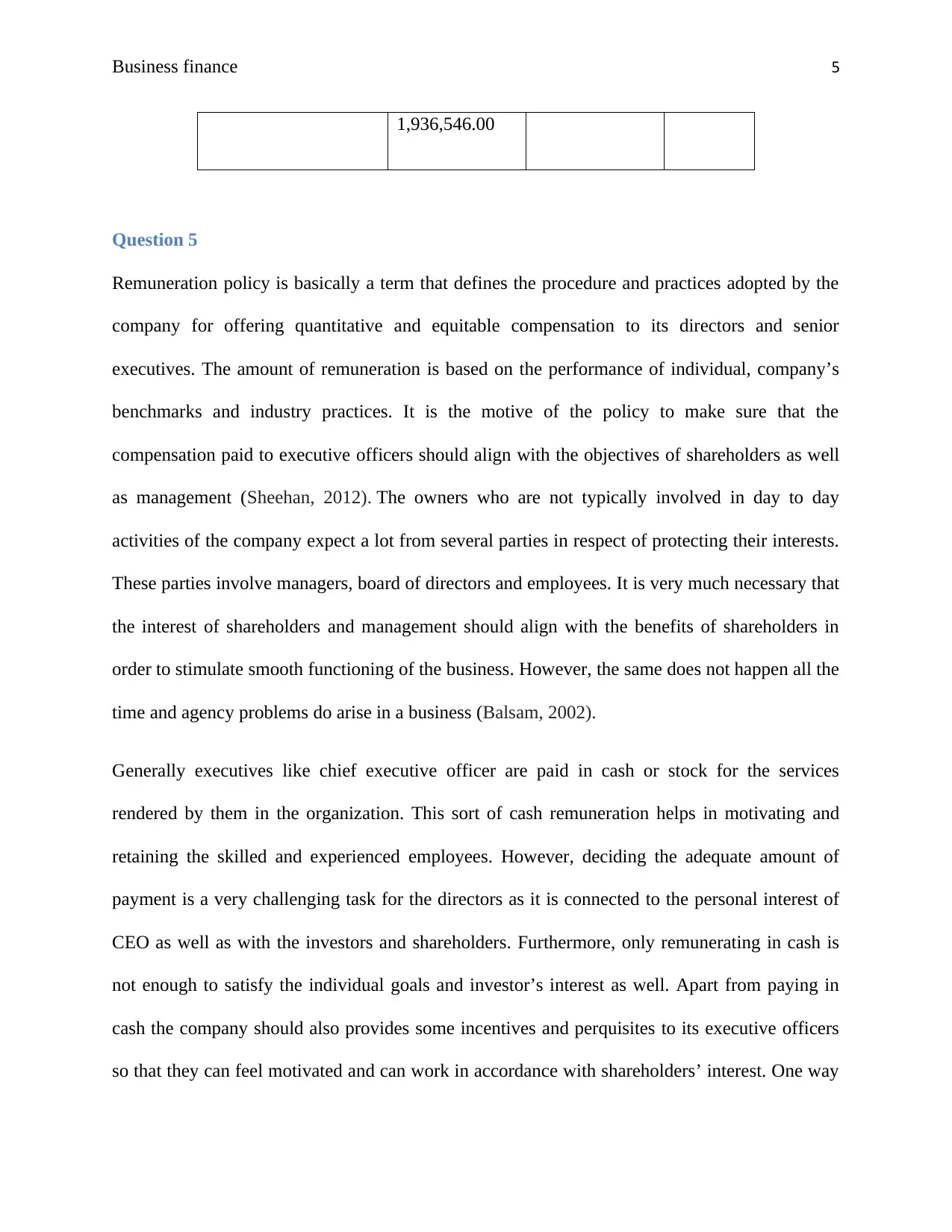

1,936,546.00

Question 5

Remuneration policy is basically a term that defines the procedure and practices adopted by the

company for offering quantitative and equitable compensation to its directors and senior

executives. The amount of remuneration is based on the performance of individual, company’s

benchmarks and industry practices. It is the motive of the policy to make sure that the

compensation paid to executive officers should align with the objectives of shareholders as well

as management (Sheehan, 2012). The owners who are not typically involved in day to day

activities of the company expect a lot from several parties in respect of protecting their interests.

These parties involve managers, board of directors and employees. It is very much necessary that

the interest of shareholders and management should align with the benefits of shareholders in

order to stimulate smooth functioning of the business. However, the same does not happen all the

time and agency problems do arise in a business (Balsam, 2002).

Generally executives like chief executive officer are paid in cash or stock for the services

rendered by them in the organization. This sort of cash remuneration helps in motivating and

retaining the skilled and experienced employees. However, deciding the adequate amount of

payment is a very challenging task for the directors as it is connected to the personal interest of

CEO as well as with the investors and shareholders. Furthermore, only remunerating in cash is

not enough to satisfy the individual goals and investor’s interest as well. Apart from paying in

cash the company should also provides some incentives and perquisites to its executive officers

so that they can feel motivated and can work in accordance with shareholders’ interest. One way

1,936,546.00

Question 5

Remuneration policy is basically a term that defines the procedure and practices adopted by the

company for offering quantitative and equitable compensation to its directors and senior

executives. The amount of remuneration is based on the performance of individual, company’s

benchmarks and industry practices. It is the motive of the policy to make sure that the

compensation paid to executive officers should align with the objectives of shareholders as well

as management (Sheehan, 2012). The owners who are not typically involved in day to day

activities of the company expect a lot from several parties in respect of protecting their interests.

These parties involve managers, board of directors and employees. It is very much necessary that

the interest of shareholders and management should align with the benefits of shareholders in

order to stimulate smooth functioning of the business. However, the same does not happen all the

time and agency problems do arise in a business (Balsam, 2002).

Generally executives like chief executive officer are paid in cash or stock for the services

rendered by them in the organization. This sort of cash remuneration helps in motivating and

retaining the skilled and experienced employees. However, deciding the adequate amount of

payment is a very challenging task for the directors as it is connected to the personal interest of

CEO as well as with the investors and shareholders. Furthermore, only remunerating in cash is

not enough to satisfy the individual goals and investor’s interest as well. Apart from paying in

cash the company should also provides some incentives and perquisites to its executive officers

so that they can feel motivated and can work in accordance with shareholders’ interest. One way

Business finance 6

to do the same is to give some percentage of shareholdings to managers and employees so that

they can also think from the perspective of shareholders and are promoted to protect the same.

Therefore, it can be said that cash remuneration alone does not align with the interest and

benefits of CEO and shareholders (Bolton, Mehran and Shapiro, 2015).

Question 6

Other types of remuneration policies include paying the compensation that contains two elements

that are fixed and variable. The fixed element comprises of allowances, salary, provident fund,

gratuity and other perquisites. On the other side, the variable should include the pay based on the

annual performance of the executives that may be a fixed amount or a percentage of profits

(Bettis, Bizjak, Coles and Kalpathy, 2018). Along with this, various stock options and different

types of allowances should also be included in the remuneration of the chief executive officer.

Furthermore, providing various retirement, medical, insurance benefits will anyway motivate

them to work in the best interest of the organization. Once the personal goals of CEO will be

satisfied, the will eventually result in alignment of shareholders’ interest also.

Requirement 2

Question 4

Calculation of growth rate in EPS for

2010

EPS (cents) 395.5

DPS (cents) 290

Retention ratio 27%

to do the same is to give some percentage of shareholdings to managers and employees so that

they can also think from the perspective of shareholders and are promoted to protect the same.

Therefore, it can be said that cash remuneration alone does not align with the interest and

benefits of CEO and shareholders (Bolton, Mehran and Shapiro, 2015).

Question 6

Other types of remuneration policies include paying the compensation that contains two elements

that are fixed and variable. The fixed element comprises of allowances, salary, provident fund,

gratuity and other perquisites. On the other side, the variable should include the pay based on the

annual performance of the executives that may be a fixed amount or a percentage of profits

(Bettis, Bizjak, Coles and Kalpathy, 2018). Along with this, various stock options and different

types of allowances should also be included in the remuneration of the chief executive officer.

Furthermore, providing various retirement, medical, insurance benefits will anyway motivate

them to work in the best interest of the organization. Once the personal goals of CEO will be

satisfied, the will eventually result in alignment of shareholders’ interest also.

Requirement 2

Question 4

Calculation of growth rate in EPS for

2010

EPS (cents) 395.5

DPS (cents) 290

Retention ratio 27%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business finance 7

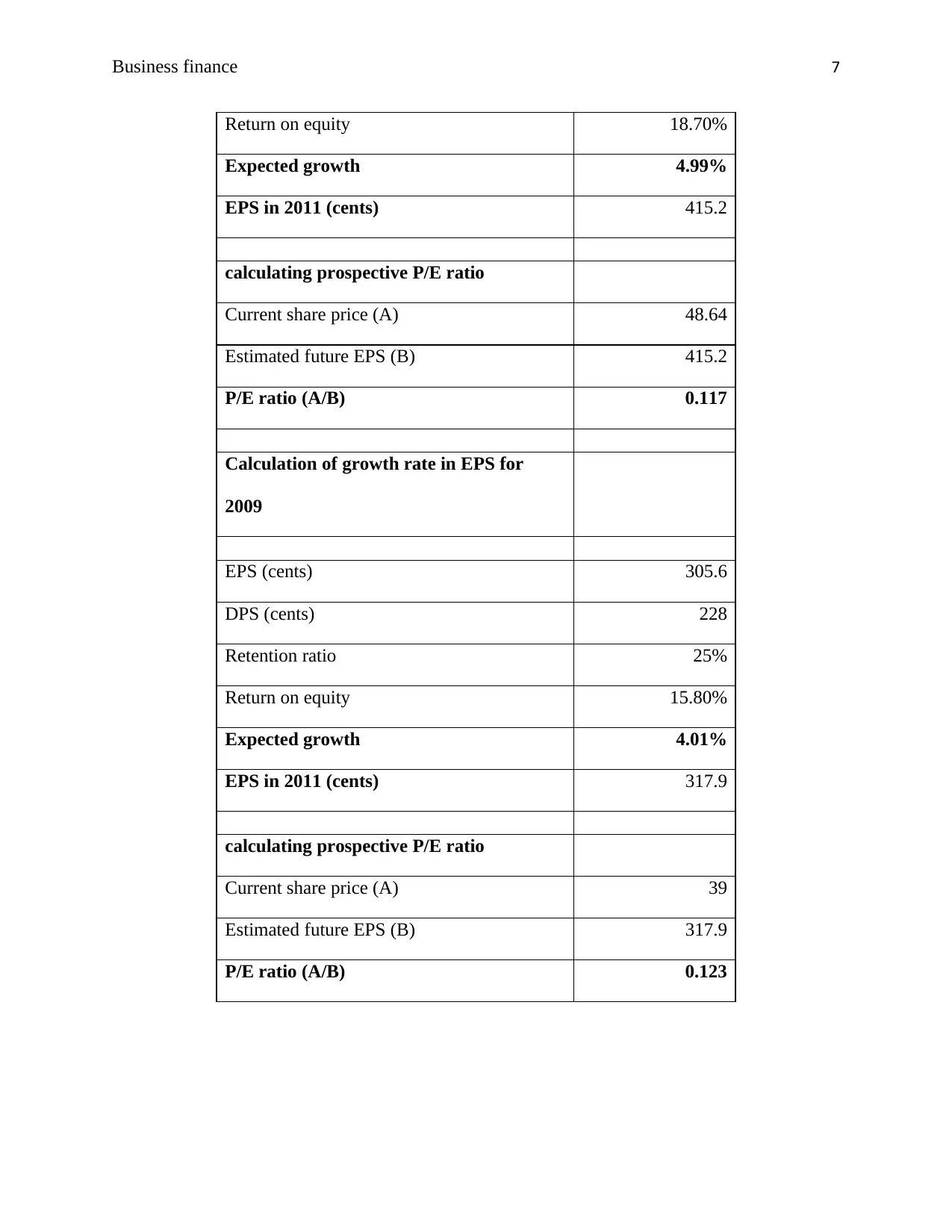

Return on equity 18.70%

Expected growth 4.99%

EPS in 2011 (cents) 415.2

calculating prospective P/E ratio

Current share price (A) 48.64

Estimated future EPS (B) 415.2

P/E ratio (A/B) 0.117

Calculation of growth rate in EPS for

2009

EPS (cents) 305.6

DPS (cents) 228

Retention ratio 25%

Return on equity 15.80%

Expected growth 4.01%

EPS in 2011 (cents) 317.9

calculating prospective P/E ratio

Current share price (A) 39

Estimated future EPS (B) 317.9

P/E ratio (A/B) 0.123

Return on equity 18.70%

Expected growth 4.99%

EPS in 2011 (cents) 415.2

calculating prospective P/E ratio

Current share price (A) 48.64

Estimated future EPS (B) 415.2

P/E ratio (A/B) 0.117

Calculation of growth rate in EPS for

2009

EPS (cents) 305.6

DPS (cents) 228

Retention ratio 25%

Return on equity 15.80%

Expected growth 4.01%

EPS in 2011 (cents) 317.9

calculating prospective P/E ratio

Current share price (A) 39

Estimated future EPS (B) 317.9

P/E ratio (A/B) 0.123

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business finance 8

Requirement 3

Question 1

Capital budgeting is a planning procedure which is used to determine the viability and feasibility

of an investment proposal available with the organization. The techniques of capital budgeting

evaluates projects that include long term investments of the organization such as installation of

new machinery, purchase of new plant, building or equipment. In simple words, it is a process

used by the companies to select the best proposal in which making investment will generate high

returns (Baker, Jabbouri and Dyaz, 2017). The cash flows generated are evaluated by using

various investment appraisal methods such as net present value, payback period and internal rate

of return. The decision of selection is completely based on these methods as they provide reliable

information about the profitability of the available projects (BiermanJr and Smidt, 2014).

The process of capital budgeting is important for the firm because it creates measurability and

accountability. It helps the firm to know about the risk and return involved in making the

investment in a particular project. Furthermore, measuring the effectiveness of the proposal is

very important for the companies and the process of capital budgeting allows them to do the

same. It also vital in a way that it helps the business in developing and formulating long term

strategic goals as well as seeking out the the new investment opportunities (Borgonovo, 2017).

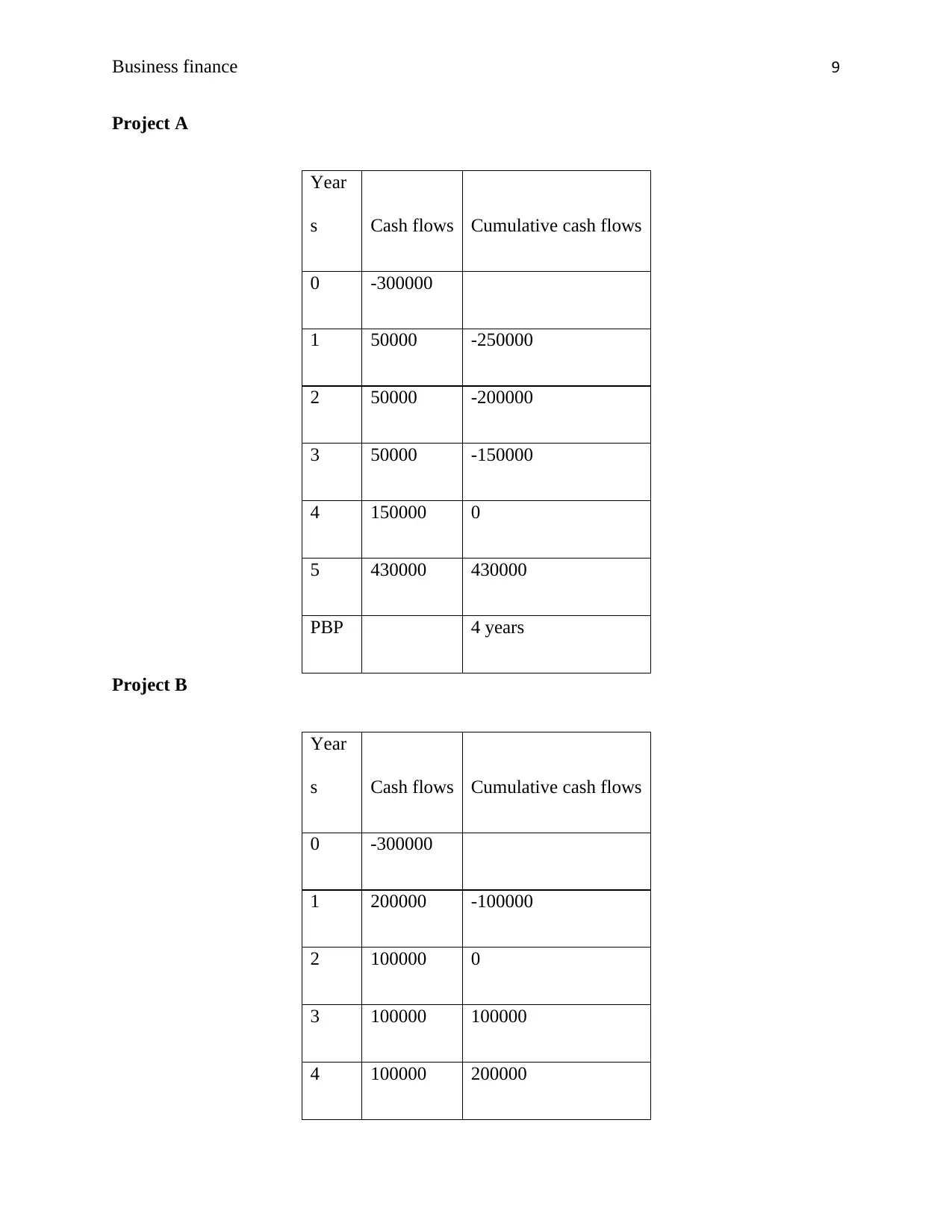

Question 2

Payback period is the simplest technique that determines the amount of time or number of years

taken by a project to recoup or recover its initial investments. It is one of the appraisal techniques

and is mostly used to know about the feasibility of the proposal in future (Daunfeldt and

Hartwig, 2014). The payback period of the two projects is as follows:

Requirement 3

Question 1

Capital budgeting is a planning procedure which is used to determine the viability and feasibility

of an investment proposal available with the organization. The techniques of capital budgeting

evaluates projects that include long term investments of the organization such as installation of

new machinery, purchase of new plant, building or equipment. In simple words, it is a process

used by the companies to select the best proposal in which making investment will generate high

returns (Baker, Jabbouri and Dyaz, 2017). The cash flows generated are evaluated by using

various investment appraisal methods such as net present value, payback period and internal rate

of return. The decision of selection is completely based on these methods as they provide reliable

information about the profitability of the available projects (BiermanJr and Smidt, 2014).

The process of capital budgeting is important for the firm because it creates measurability and

accountability. It helps the firm to know about the risk and return involved in making the

investment in a particular project. Furthermore, measuring the effectiveness of the proposal is

very important for the companies and the process of capital budgeting allows them to do the

same. It also vital in a way that it helps the business in developing and formulating long term

strategic goals as well as seeking out the the new investment opportunities (Borgonovo, 2017).

Question 2

Payback period is the simplest technique that determines the amount of time or number of years

taken by a project to recoup or recover its initial investments. It is one of the appraisal techniques

and is mostly used to know about the feasibility of the proposal in future (Daunfeldt and

Hartwig, 2014). The payback period of the two projects is as follows:

Business finance 9

Project A

Year

s Cash flows Cumulative cash flows

0 -300000

1 50000 -250000

2 50000 -200000

3 50000 -150000

4 150000 0

5 430000 430000

PBP 4 years

Project B

Year

s Cash flows Cumulative cash flows

0 -300000

1 200000 -100000

2 100000 0

3 100000 100000

4 100000 200000

Project A

Year

s Cash flows Cumulative cash flows

0 -300000

1 50000 -250000

2 50000 -200000

3 50000 -150000

4 150000 0

5 430000 430000

PBP 4 years

Project B

Year

s Cash flows Cumulative cash flows

0 -300000

1 200000 -100000

2 100000 0

3 100000 100000

4 100000 200000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business finance 10

5 100000 300000

PBP 2 years

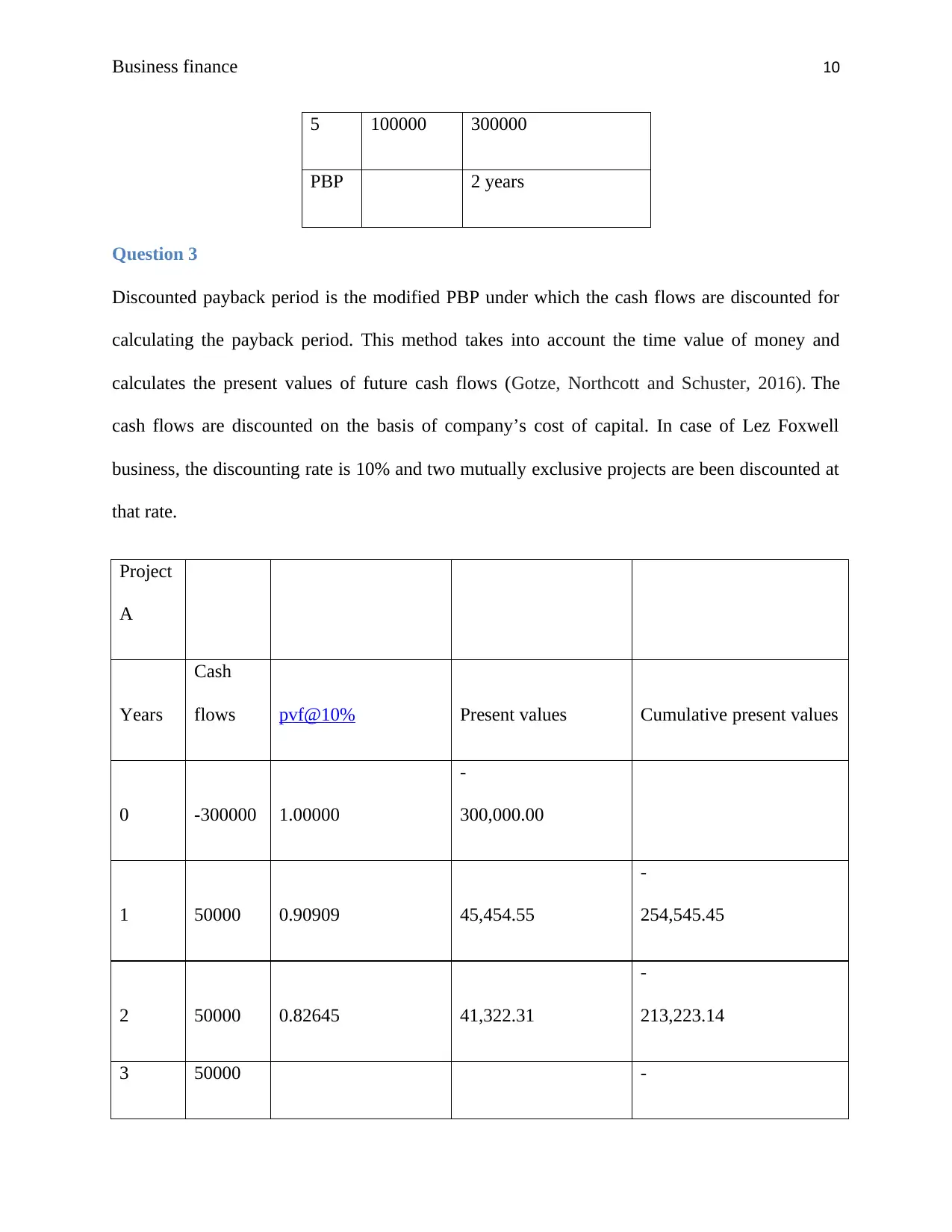

Question 3

Discounted payback period is the modified PBP under which the cash flows are discounted for

calculating the payback period. This method takes into account the time value of money and

calculates the present values of future cash flows (Gotze, Northcott and Schuster, 2016). The

cash flows are discounted on the basis of company’s cost of capital. In case of Lez Foxwell

business, the discounting rate is 10% and two mutually exclusive projects are been discounted at

that rate.

Project

A

Years

Cash

flows pvf@10% Present values Cumulative present values

0 -300000 1.00000

-

300,000.00

1 50000 0.90909 45,454.55

-

254,545.45

2 50000 0.82645 41,322.31

-

213,223.14

3 50000 -

5 100000 300000

PBP 2 years

Question 3

Discounted payback period is the modified PBP under which the cash flows are discounted for

calculating the payback period. This method takes into account the time value of money and

calculates the present values of future cash flows (Gotze, Northcott and Schuster, 2016). The

cash flows are discounted on the basis of company’s cost of capital. In case of Lez Foxwell

business, the discounting rate is 10% and two mutually exclusive projects are been discounted at

that rate.

Project

A

Years

Cash

flows pvf@10% Present values Cumulative present values

0 -300000 1.00000

-

300,000.00

1 50000 0.90909 45,454.55

-

254,545.45

2 50000 0.82645 41,322.31

-

213,223.14

3 50000 -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business finance 11

0.75131 37,565.74 175,657.40

4 150000 0.68301 102,452.02

-

73,205.38

5 430000 0.62092 266,996.17 193,790.79

PBP 4.27 years

Project

B

Years

Cash

flows pvf@10% Present values Cumulative present values

0 -300000 1.00000

-

300,000.00

1 200000 0.90909 181,818.18

-

118,181.82

2 100000 0.82645 82,644.63

-

35,537.19

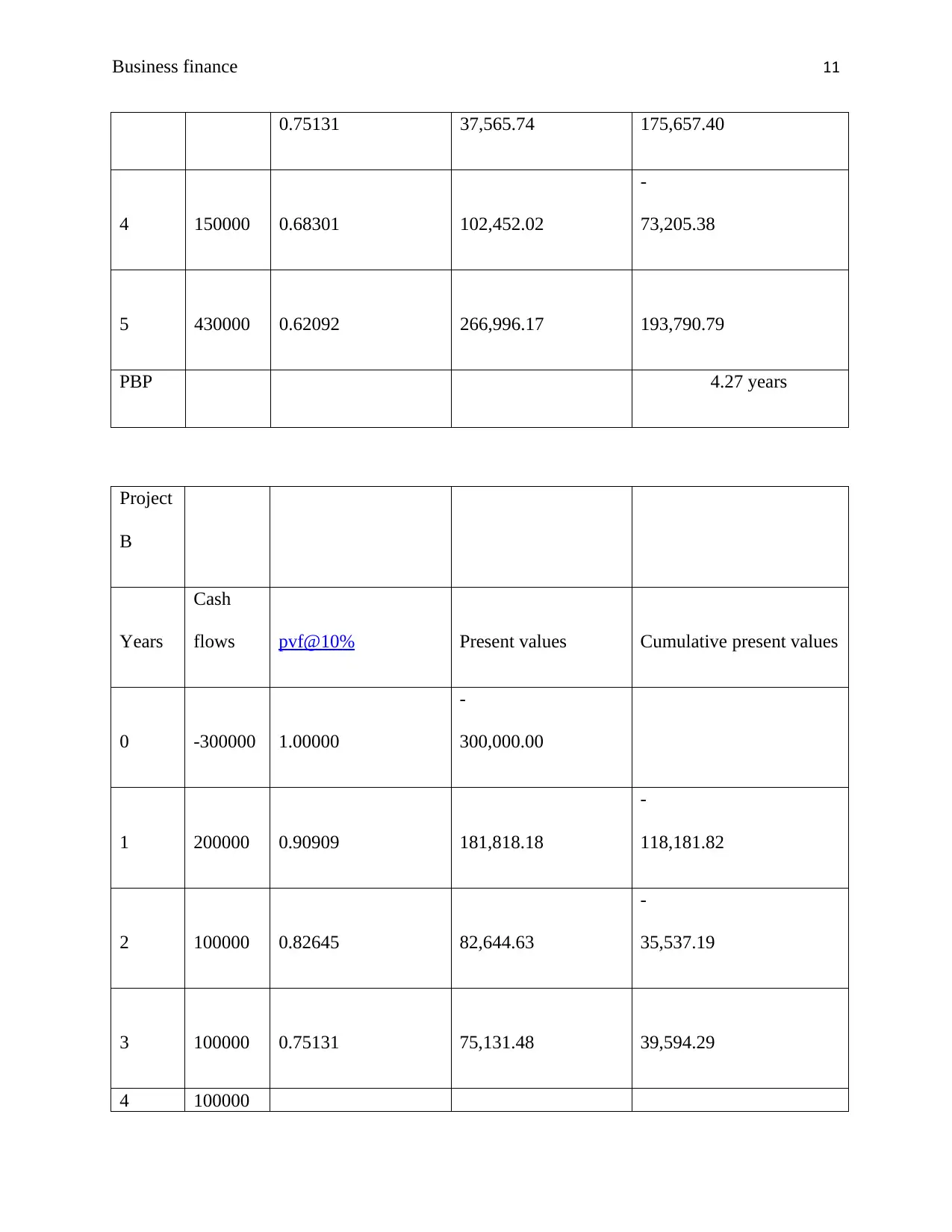

3 100000 0.75131 75,131.48 39,594.29

4 100000

0.75131 37,565.74 175,657.40

4 150000 0.68301 102,452.02

-

73,205.38

5 430000 0.62092 266,996.17 193,790.79

PBP 4.27 years

Project

B

Years

Cash

flows pvf@10% Present values Cumulative present values

0 -300000 1.00000

-

300,000.00

1 200000 0.90909 181,818.18

-

118,181.82

2 100000 0.82645 82,644.63

-

35,537.19

3 100000 0.75131 75,131.48 39,594.29

4 100000

Business finance 12

0.68301 68,301.35 107,895.64

5 100000 0.62092 62,092.13 169,987.77

PBP 2.5 years

Requirement 4

Question 4

Following are the limitations of using payback period:

The simple payback period fails to consider the concept of time value of money and does

not adjust the cash flows accordingly.

Another weakness is that it does not take into account the additional cash flows that are

generated after payback period.

Although it is the simplest method but it fails to reflect the overall profitability of one

project when compared with another.

The method cannot consider complex cash flows that occur with capital investments

(Shapiro, 2008).

All such are the drawbacks of payback period method and therefore it is sometime used as

preliminary evaluation technique, further supported by methods like NPV and IRR. Despite

having such limitations, the method is useful in many ways. They are as follows:

0.68301 68,301.35 107,895.64

5 100000 0.62092 62,092.13 169,987.77

PBP 2.5 years

Requirement 4

Question 4

Following are the limitations of using payback period:

The simple payback period fails to consider the concept of time value of money and does

not adjust the cash flows accordingly.

Another weakness is that it does not take into account the additional cash flows that are

generated after payback period.

Although it is the simplest method but it fails to reflect the overall profitability of one

project when compared with another.

The method cannot consider complex cash flows that occur with capital investments

(Shapiro, 2008).

All such are the drawbacks of payback period method and therefore it is sometime used as

preliminary evaluation technique, further supported by methods like NPV and IRR. Despite

having such limitations, the method is useful in many ways. They are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.