Business Finance Report: Costing, Budgeting, and Variance Analysis

VerifiedAdded on 2022/12/09

|8

|1903

|70

Report

AI Summary

This report provides a detailed overview of cost accounting and its various methods. It begins by defining cost accounting and then delves into budgeting techniques, including incremental, activity-based, value proposition, and zero-based budgeting. The report analyzes the advantages and disadvantages of each method, using a case study of the Arnold Company to illustrate the application of incremental budgeting. It then presents a revised budget and discusses the budget monitoring process, including variance analysis. The second part of the report focuses on different costing approaches, such as process costing, job costing, and activity-based costing, with a comparison of traditional business-wide rate and activity-based approaches. The report concludes by highlighting the importance of cost accounting in making informed business decisions.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.................................................................................................................................3

Question 1.............................................................................................................................................3

A.1) Approaches of budget setting....................................................................................................3

A.2) Revised budget..........................................................................................................................5

Part B.....................................................................................................................................................5

B.1) Different approach of costing....................................................................................................5

B.2) Traditional business wide rate....................................................................................................6

B.3) Activity based approach.............................................................................................................7

CONCLUSION.....................................................................................................................................7

REFERENCES......................................................................................................................................8

INTRODUCTION.................................................................................................................................3

Question 1.............................................................................................................................................3

A.1) Approaches of budget setting....................................................................................................3

A.2) Revised budget..........................................................................................................................5

Part B.....................................................................................................................................................5

B.1) Different approach of costing....................................................................................................5

B.2) Traditional business wide rate....................................................................................................6

B.3) Activity based approach.............................................................................................................7

CONCLUSION.....................................................................................................................................7

REFERENCES......................................................................................................................................8

INTRODUCTION

Cost accounting is a process that involves identifying and measuring the total cost

incurred to make the product or service ready to sale in the respective target market. This

report will discuss about different costing techniques. Henceforth, report will emphasis over

budgeting technique. Furthermore, project will discuss about the method to develop the total

cost.

Question 1

A.1) Approaches of budget setting

Budget setting is a process in which different cost is identified by the enterprises

related to the upcoming financial year. These costs will be related to different functional

areas and direction related to the business entity. There are certain techniques like

incremental budgeting, activity based budgeting, value proposition budgeting and zero based

budgeting techniques that are used and explored by the organisations in order to prepare the

best suitable budget practices.

Incremental budgeting

Incremental budgeting technique is a process in which the last or previous year

financial records bring out and make increment based on needs and requirements to prepare

the latest and modified budget out of it. This is very common technique of budgeting as it is

simple and understanding to prepare budget in this fashion. This technique is favourable only

f the cost drivers do not get influenced with any of the element or factor. Incremental

budgeting is a fast forward method to prepare the best suitable budget in favour of the entity

(Galvin and Power, 2020). This analysis and assume the expected cost to be incurred in the

coming financial year and prepare the best suitable budget. This budget technique completely

focuses over the internal driver but external cost drivers are completely ignored under this

practice.

Activity based budgeting

Activity based budgeting technique is a method of budgeting in which a top down

budgeting approach is used. Under this practice on the basis of the output target set by the

company budget is prepared by assuming the overall expected cost to be incurred over

operations. For example if a business entity set a target of $100 in revenue is has a set a target

Cost accounting is a process that involves identifying and measuring the total cost

incurred to make the product or service ready to sale in the respective target market. This

report will discuss about different costing techniques. Henceforth, report will emphasis over

budgeting technique. Furthermore, project will discuss about the method to develop the total

cost.

Question 1

A.1) Approaches of budget setting

Budget setting is a process in which different cost is identified by the enterprises

related to the upcoming financial year. These costs will be related to different functional

areas and direction related to the business entity. There are certain techniques like

incremental budgeting, activity based budgeting, value proposition budgeting and zero based

budgeting techniques that are used and explored by the organisations in order to prepare the

best suitable budget practices.

Incremental budgeting

Incremental budgeting technique is a process in which the last or previous year

financial records bring out and make increment based on needs and requirements to prepare

the latest and modified budget out of it. This is very common technique of budgeting as it is

simple and understanding to prepare budget in this fashion. This technique is favourable only

f the cost drivers do not get influenced with any of the element or factor. Incremental

budgeting is a fast forward method to prepare the best suitable budget in favour of the entity

(Galvin and Power, 2020). This analysis and assume the expected cost to be incurred in the

coming financial year and prepare the best suitable budget. This budget technique completely

focuses over the internal driver but external cost drivers are completely ignored under this

practice.

Activity based budgeting

Activity based budgeting technique is a method of budgeting in which a top down

budgeting approach is used. Under this practice on the basis of the output target set by the

company budget is prepared by assuming the overall expected cost to be incurred over

operations. For example if a business entity set a target of $100 in revenue is has a set a target

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

first determining the activities that needed to incorporate in order to achieve the target. Based

on the activities identified overall cost is measured that is further resulted into setting up the

best suitable budget for the organisation (Hanly and et.al., 2017). This technique is also

preferable in many cases for the organisations to explore in order to make up the best suitable

budget for the business enterprises.

Value proposition budgeting

Value proposition budgeting is a technique involve analysing and assessing the cost

that is expected to be incurred by the business entity. Under this budget only such values are

involved that create some kind of value to the business entity. Only such cost or items that are

included that create some kind of value for the potential customers associated with respective

business entity. The basic aim of this budget is to avoid the unnecessary expenses from the

business and develop the budget that suit with the business requirements of the organisation.

This budget requires clearly understanding of the cost that needed to include in the budget

and the cost that can be eliminated from the budgetary cost. Value proposition budget allow

the business entity to achieve the best suitable balance in the budgetary direction to meet up

different business objectives.

Zero based budgeting

Zero based budgeting is a most commonly used budgeting technique that is used by

majority of the business entities. This budget assume that all department cost is zero and they

need to work from the scratch. There is not any singe cost that get approved without any clear

judgement and understanding (Kianian, Kurdve and Andersson, 2019). This budget is a very

tight to deliver or involve any cost in the whole budgetary situation. This can also be stated as

the bottom line budget technique. This technique is effective only if there is urgent need or

requirements related to the cost containment for example at a time of the business

organisation are experiencing some serious financial reinforcement this technique is effective

enough to use. This technique is best suitable to address the discretionary cost rather than

overcome the operating cost in the business.

Arnold Company is doing its business operations from many years. Company in

currently using the incremental based approach to set the budget. This technique allow the

organisation to effectively analysis the cost that incurred in the company in past and based on

the market situation or needs and requirements company add some value to the budgetary

on the activities identified overall cost is measured that is further resulted into setting up the

best suitable budget for the organisation (Hanly and et.al., 2017). This technique is also

preferable in many cases for the organisations to explore in order to make up the best suitable

budget for the business enterprises.

Value proposition budgeting

Value proposition budgeting is a technique involve analysing and assessing the cost

that is expected to be incurred by the business entity. Under this budget only such values are

involved that create some kind of value to the business entity. Only such cost or items that are

included that create some kind of value for the potential customers associated with respective

business entity. The basic aim of this budget is to avoid the unnecessary expenses from the

business and develop the budget that suit with the business requirements of the organisation.

This budget requires clearly understanding of the cost that needed to include in the budget

and the cost that can be eliminated from the budgetary cost. Value proposition budget allow

the business entity to achieve the best suitable balance in the budgetary direction to meet up

different business objectives.

Zero based budgeting

Zero based budgeting is a most commonly used budgeting technique that is used by

majority of the business entities. This budget assume that all department cost is zero and they

need to work from the scratch. There is not any singe cost that get approved without any clear

judgement and understanding (Kianian, Kurdve and Andersson, 2019). This budget is a very

tight to deliver or involve any cost in the whole budgetary situation. This can also be stated as

the bottom line budget technique. This technique is effective only if there is urgent need or

requirements related to the cost containment for example at a time of the business

organisation are experiencing some serious financial reinforcement this technique is effective

enough to use. This technique is best suitable to address the discretionary cost rather than

overcome the operating cost in the business.

Arnold Company is doing its business operations from many years. Company in

currently using the incremental based approach to set the budget. This technique allow the

organisation to effectively analysis the cost that incurred in the company in past and based on

the market situation or needs and requirements company add some value to the budgetary

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost so that total estimated cost related to every single expenditure company can identify.

This technique is effective in context to the business entity as it allow the organisation to

evaluate the expected cost to be incurred by the organisation in next financial year.

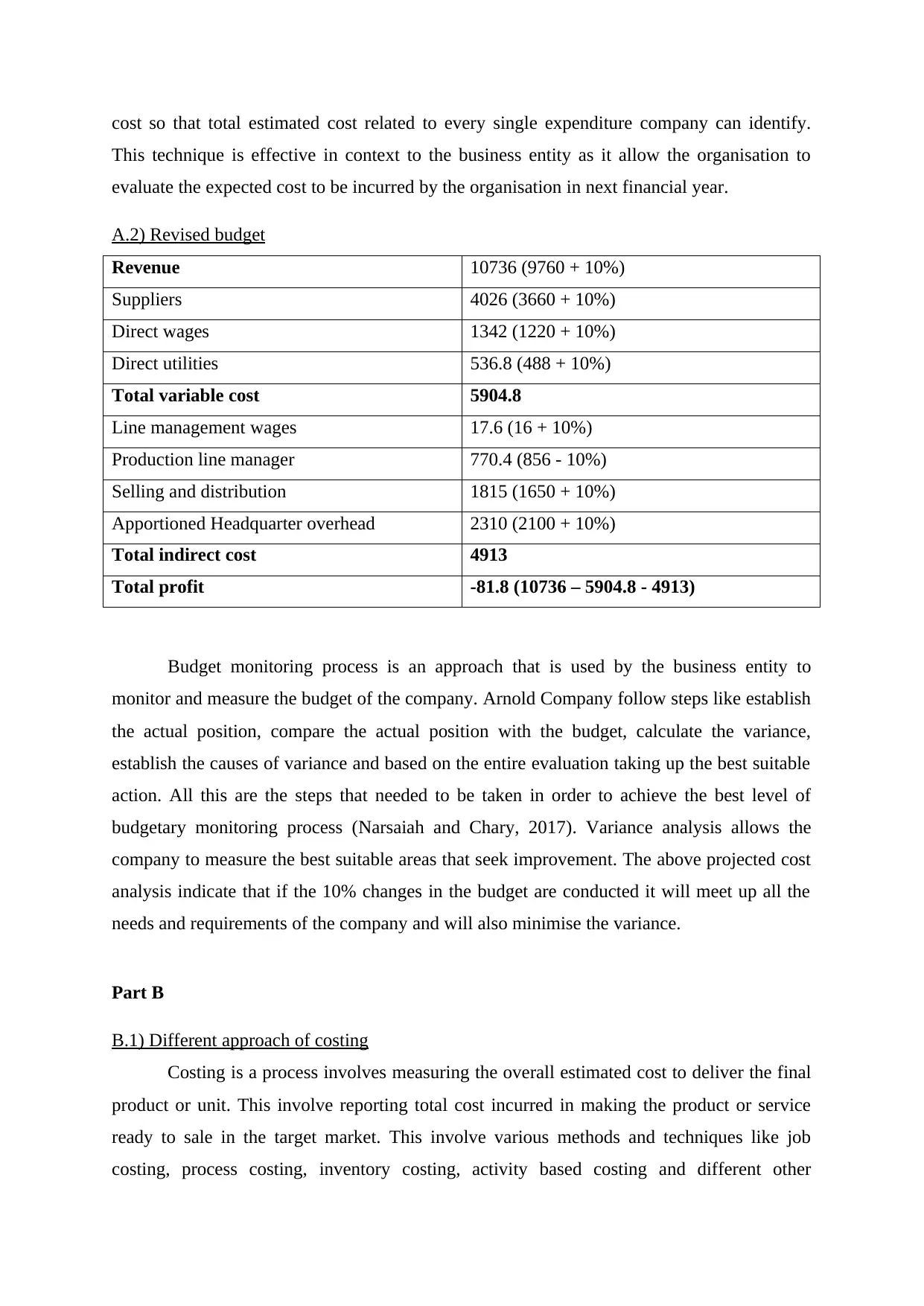

A.2) Revised budget

Revenue 10736 (9760 + 10%)

Suppliers 4026 (3660 + 10%)

Direct wages 1342 (1220 + 10%)

Direct utilities 536.8 (488 + 10%)

Total variable cost 5904.8

Line management wages 17.6 (16 + 10%)

Production line manager 770.4 (856 - 10%)

Selling and distribution 1815 (1650 + 10%)

Apportioned Headquarter overhead 2310 (2100 + 10%)

Total indirect cost 4913

Total profit -81.8 (10736 – 5904.8 - 4913)

Budget monitoring process is an approach that is used by the business entity to

monitor and measure the budget of the company. Arnold Company follow steps like establish

the actual position, compare the actual position with the budget, calculate the variance,

establish the causes of variance and based on the entire evaluation taking up the best suitable

action. All this are the steps that needed to be taken in order to achieve the best level of

budgetary monitoring process (Narsaiah and Chary, 2017). Variance analysis allows the

company to measure the best suitable areas that seek improvement. The above projected cost

analysis indicate that if the 10% changes in the budget are conducted it will meet up all the

needs and requirements of the company and will also minimise the variance.

Part B

B.1) Different approach of costing

Costing is a process involves measuring the overall estimated cost to deliver the final

product or unit. This involve reporting total cost incurred in making the product or service

ready to sale in the target market. This involve various methods and techniques like job

costing, process costing, inventory costing, activity based costing and different other

This technique is effective in context to the business entity as it allow the organisation to

evaluate the expected cost to be incurred by the organisation in next financial year.

A.2) Revised budget

Revenue 10736 (9760 + 10%)

Suppliers 4026 (3660 + 10%)

Direct wages 1342 (1220 + 10%)

Direct utilities 536.8 (488 + 10%)

Total variable cost 5904.8

Line management wages 17.6 (16 + 10%)

Production line manager 770.4 (856 - 10%)

Selling and distribution 1815 (1650 + 10%)

Apportioned Headquarter overhead 2310 (2100 + 10%)

Total indirect cost 4913

Total profit -81.8 (10736 – 5904.8 - 4913)

Budget monitoring process is an approach that is used by the business entity to

monitor and measure the budget of the company. Arnold Company follow steps like establish

the actual position, compare the actual position with the budget, calculate the variance,

establish the causes of variance and based on the entire evaluation taking up the best suitable

action. All this are the steps that needed to be taken in order to achieve the best level of

budgetary monitoring process (Narsaiah and Chary, 2017). Variance analysis allows the

company to measure the best suitable areas that seek improvement. The above projected cost

analysis indicate that if the 10% changes in the budget are conducted it will meet up all the

needs and requirements of the company and will also minimise the variance.

Part B

B.1) Different approach of costing

Costing is a process involves measuring the overall estimated cost to deliver the final

product or unit. This involve reporting total cost incurred in making the product or service

ready to sale in the target market. This involve various methods and techniques like job

costing, process costing, inventory costing, activity based costing and different other

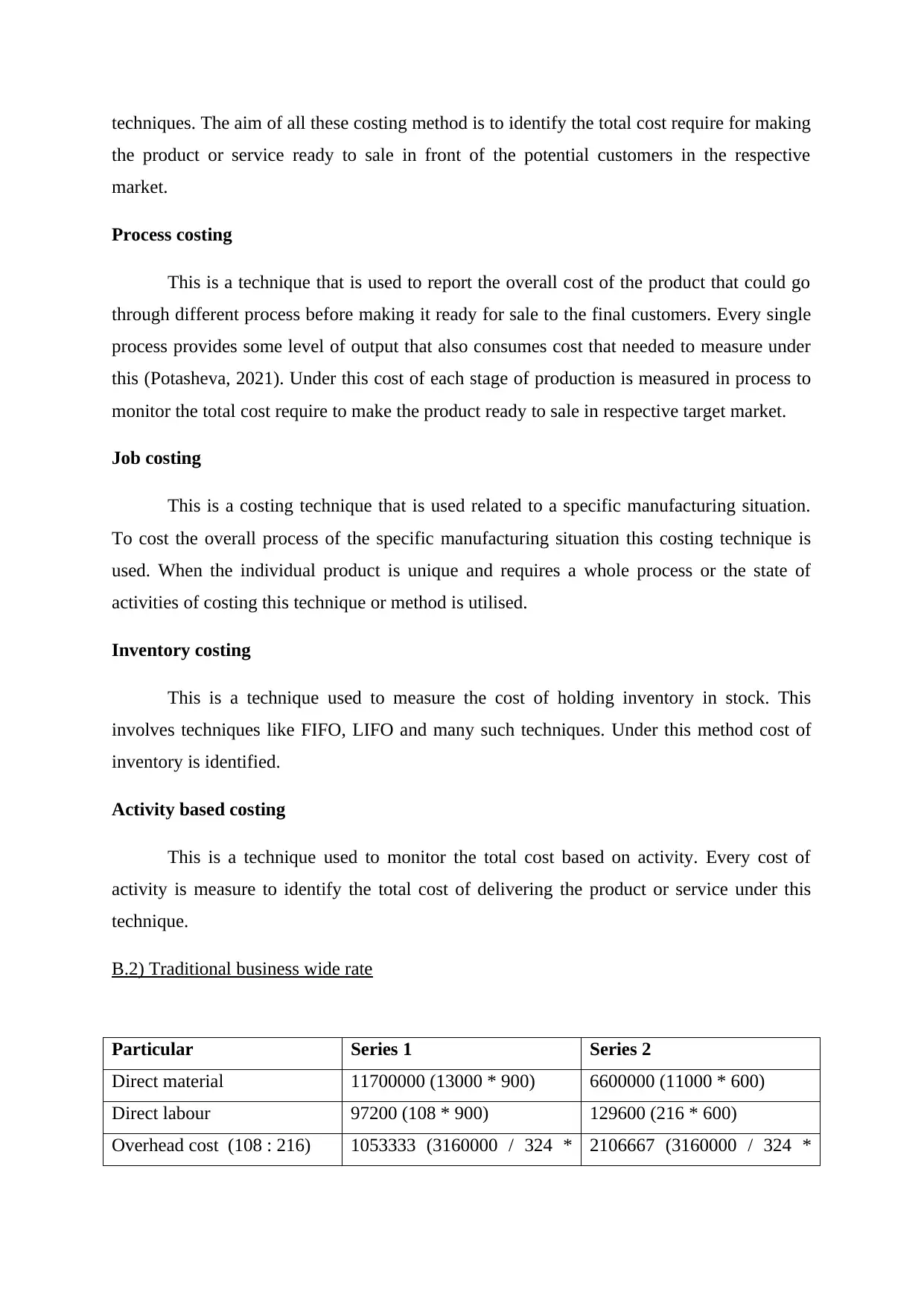

techniques. The aim of all these costing method is to identify the total cost require for making

the product or service ready to sale in front of the potential customers in the respective

market.

Process costing

This is a technique that is used to report the overall cost of the product that could go

through different process before making it ready for sale to the final customers. Every single

process provides some level of output that also consumes cost that needed to measure under

this (Potasheva, 2021). Under this cost of each stage of production is measured in process to

monitor the total cost require to make the product ready to sale in respective target market.

Job costing

This is a costing technique that is used related to a specific manufacturing situation.

To cost the overall process of the specific manufacturing situation this costing technique is

used. When the individual product is unique and requires a whole process or the state of

activities of costing this technique or method is utilised.

Inventory costing

This is a technique used to measure the cost of holding inventory in stock. This

involves techniques like FIFO, LIFO and many such techniques. Under this method cost of

inventory is identified.

Activity based costing

This is a technique used to monitor the total cost based on activity. Every cost of

activity is measure to identify the total cost of delivering the product or service under this

technique.

B.2) Traditional business wide rate

Particular Series 1 Series 2

Direct material 11700000 (13000 * 900) 6600000 (11000 * 600)

Direct labour 97200 (108 * 900) 129600 (216 * 600)

Overhead cost (108 : 216) 1053333 (3160000 / 324 * 2106667 (3160000 / 324 *

the product or service ready to sale in front of the potential customers in the respective

market.

Process costing

This is a technique that is used to report the overall cost of the product that could go

through different process before making it ready for sale to the final customers. Every single

process provides some level of output that also consumes cost that needed to measure under

this (Potasheva, 2021). Under this cost of each stage of production is measured in process to

monitor the total cost require to make the product ready to sale in respective target market.

Job costing

This is a costing technique that is used related to a specific manufacturing situation.

To cost the overall process of the specific manufacturing situation this costing technique is

used. When the individual product is unique and requires a whole process or the state of

activities of costing this technique or method is utilised.

Inventory costing

This is a technique used to measure the cost of holding inventory in stock. This

involves techniques like FIFO, LIFO and many such techniques. Under this method cost of

inventory is identified.

Activity based costing

This is a technique used to monitor the total cost based on activity. Every cost of

activity is measure to identify the total cost of delivering the product or service under this

technique.

B.2) Traditional business wide rate

Particular Series 1 Series 2

Direct material 11700000 (13000 * 900) 6600000 (11000 * 600)

Direct labour 97200 (108 * 900) 129600 (216 * 600)

Overhead cost (108 : 216) 1053333 (3160000 / 324 * 2106667 (3160000 / 324 *

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

108) 216)

Total cost 12850533 8836267

Add: 40% mark up 5140213 3534507

Total selling price 17990746 12370774

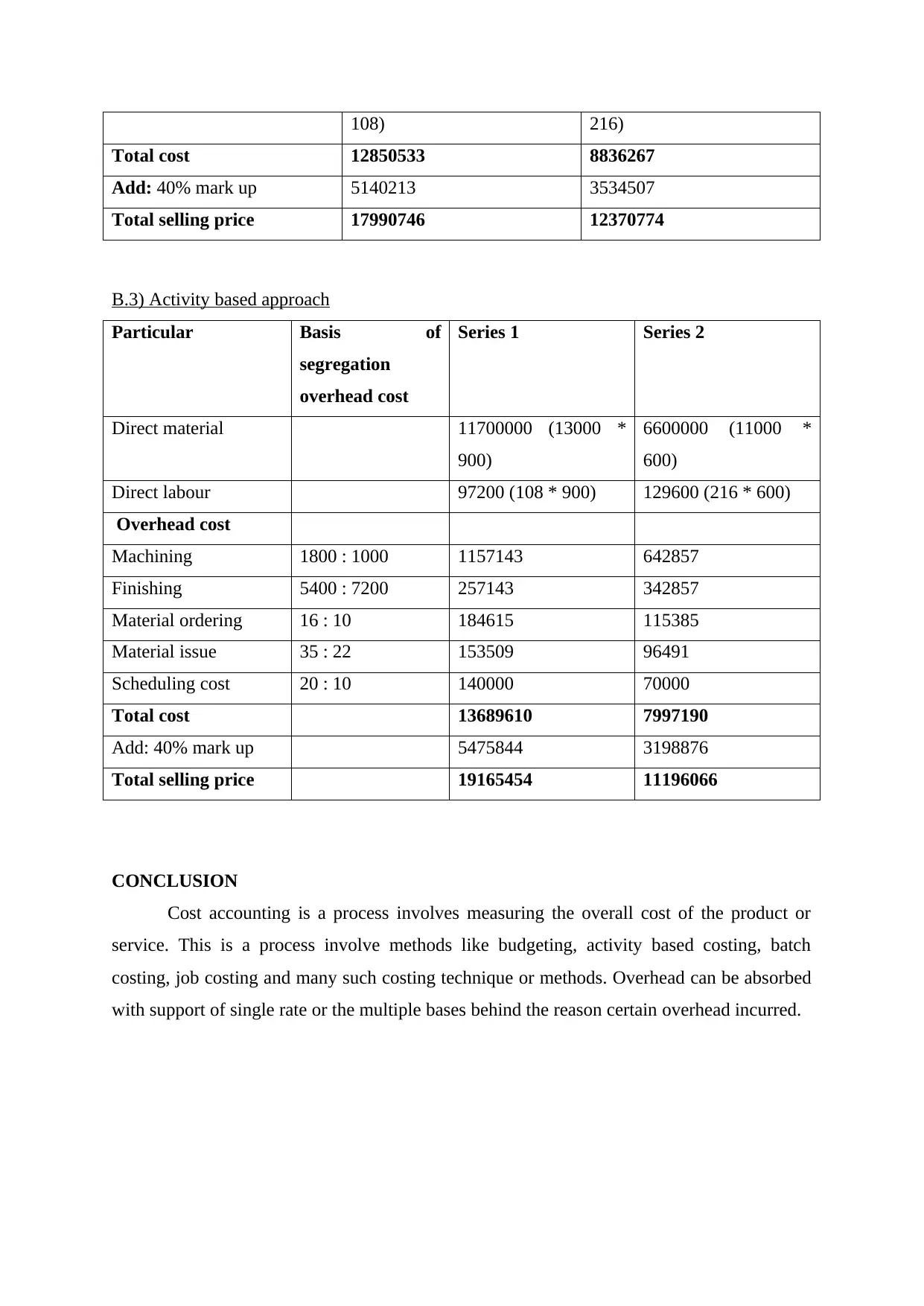

B.3) Activity based approach

Particular Basis of

segregation

overhead cost

Series 1 Series 2

Direct material 11700000 (13000 *

900)

6600000 (11000 *

600)

Direct labour 97200 (108 * 900) 129600 (216 * 600)

Overhead cost

Machining 1800 : 1000 1157143 642857

Finishing 5400 : 7200 257143 342857

Material ordering 16 : 10 184615 115385

Material issue 35 : 22 153509 96491

Scheduling cost 20 : 10 140000 70000

Total cost 13689610 7997190

Add: 40% mark up 5475844 3198876

Total selling price 19165454 11196066

CONCLUSION

Cost accounting is a process involves measuring the overall cost of the product or

service. This is a process involve methods like budgeting, activity based costing, batch

costing, job costing and many such costing technique or methods. Overhead can be absorbed

with support of single rate or the multiple bases behind the reason certain overhead incurred.

Total cost 12850533 8836267

Add: 40% mark up 5140213 3534507

Total selling price 17990746 12370774

B.3) Activity based approach

Particular Basis of

segregation

overhead cost

Series 1 Series 2

Direct material 11700000 (13000 *

900)

6600000 (11000 *

600)

Direct labour 97200 (108 * 900) 129600 (216 * 600)

Overhead cost

Machining 1800 : 1000 1157143 642857

Finishing 5400 : 7200 257143 342857

Material ordering 16 : 10 184615 115385

Material issue 35 : 22 153509 96491

Scheduling cost 20 : 10 140000 70000

Total cost 13689610 7997190

Add: 40% mark up 5475844 3198876

Total selling price 19165454 11196066

CONCLUSION

Cost accounting is a process involves measuring the overall cost of the product or

service. This is a process involve methods like budgeting, activity based costing, batch

costing, job costing and many such costing technique or methods. Overhead can be absorbed

with support of single rate or the multiple bases behind the reason certain overhead incurred.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Galvin, D. and Power, C., 2020. A micro-costing study: comparing a standard intravenous

patient-controlled analgesia system with a novel sublingual patient-controlled

analgesia system. Irish Journal of Medical Science (1971-). pp.1-5.

Hanly, P. and et.al., 2017. Making implicit assumptions explicit in the costing of informal

care: The case of head and neck cancer in Ireland. PharmacoEconomics. 35(5).

pp.591-601.

Kianian, B., Kurdve, M. and Andersson, C., 2019. Comparing life cycle costing and

performance part costing in assessing acquisition and operational cost of new

manufacturing technologies. Procedia CIRP. 80. pp.428-433.

Narsaiah, N. and Chary, T. S., 2017. Activity Based Costing and Profitability of IT

Companies-A Case Study. JIMS8M: The Journal of Indian Management &

Strategy. 22(1). pp.4-11.

Potasheva, O., 2021. Automation problems of ABC costing in Russia. In Current

Achievements, Challenges and Digital Chances of Knowledge Based Economy (pp.

331-339). Springer, Cham.

Books and Journals

Galvin, D. and Power, C., 2020. A micro-costing study: comparing a standard intravenous

patient-controlled analgesia system with a novel sublingual patient-controlled

analgesia system. Irish Journal of Medical Science (1971-). pp.1-5.

Hanly, P. and et.al., 2017. Making implicit assumptions explicit in the costing of informal

care: The case of head and neck cancer in Ireland. PharmacoEconomics. 35(5).

pp.591-601.

Kianian, B., Kurdve, M. and Andersson, C., 2019. Comparing life cycle costing and

performance part costing in assessing acquisition and operational cost of new

manufacturing technologies. Procedia CIRP. 80. pp.428-433.

Narsaiah, N. and Chary, T. S., 2017. Activity Based Costing and Profitability of IT

Companies-A Case Study. JIMS8M: The Journal of Indian Management &

Strategy. 22(1). pp.4-11.

Potasheva, O., 2021. Automation problems of ABC costing in Russia. In Current

Achievements, Challenges and Digital Chances of Knowledge Based Economy (pp.

331-339). Springer, Cham.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.