Dysonica Plc: Financial Analysis, Budgeting, and Cost Reduction

VerifiedAdded on 2023/06/10

|14

|2544

|135

Report

AI Summary

This report provides a comprehensive analysis of business finance principles applied to Dysonica, focusing on cost classification, reduction strategies, and financial forecasting. It examines fixed, variable, and semi-variable costs, advocating for activity-based costing or marginal costing to enhance cost control. A 12-month cash flow forecast is presented, highlighting potential cash inflows and outflows, with recommendations for managing currency exchange risks and improving overall financial health. The report concludes that effective financial management is crucial for Dysonica's competitiveness, emphasizing the importance of cost reduction and accurate budgeting for sustained success in the global market. Desklib offers this solved assignment and many other resources for students.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

Classify cost according to behaviour........................................................................................................3

TASK 2..........................................................................................................................................................5

Discuss the judgments and conclusions based on cost reduction strategy.............................................5

TASK 3..........................................................................................................................................................5

Preparation a 12 - month forecast/budget for the business up to 30 April 2023....................................5

TASK 4........................................................................................................................................................11

Clear justifications are needed to support the conclusions and recommendations made in your

evaluation..............................................................................................................................................11

CONCLUSION.............................................................................................................................................11

REFERENCES..............................................................................................................................................13

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

Classify cost according to behaviour........................................................................................................3

TASK 2..........................................................................................................................................................5

Discuss the judgments and conclusions based on cost reduction strategy.............................................5

TASK 3..........................................................................................................................................................5

Preparation a 12 - month forecast/budget for the business up to 30 April 2023....................................5

TASK 4........................................................................................................................................................11

Clear justifications are needed to support the conclusions and recommendations made in your

evaluation..............................................................................................................................................11

CONCLUSION.............................................................................................................................................11

REFERENCES..............................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance is the backbone of any firm. It is nearly hard to prosper lacking solid financial

backing. Business finance refers to the finances and credit used in a business. Financial is the

underpinning of any firm. Finance is required to acquire property, products, natural resources,

and other enabling business (Beladi, Deng, and Hu, 2021). Financial management can give the tools

needed to devise solutions to address the deficit. Dysonica is a large multinational inventive firm

that was founded in the United Kingdom but now works globally. Its items are accessible on the

main street and also internet. Competitive pressure has resulted in several price initiatives,

including the relocation of production from the United Kingdom.

TASK 1

Classify cost according to behaviour

Fixed cost:

Factory and storage rent: 18000 per month = 18000*12 = 216000

Insurance: 500 per month = 500*12 = 6000

Machinery: 1500 per month = 1500*12 = 18000

Utilities: 500 per month = 500*12 = 6000

Variable Cost:

Direct labour: 17500 per month

Raw material: 15000

Semi variable cost:

Office and sales staff: 9000 per month = 9000*12 = 18000

Logistics cost: 3000 per month

Fixed Costs £ Variable Costs £ Semi-variable

Costs

£

Finance is the backbone of any firm. It is nearly hard to prosper lacking solid financial

backing. Business finance refers to the finances and credit used in a business. Financial is the

underpinning of any firm. Finance is required to acquire property, products, natural resources,

and other enabling business (Beladi, Deng, and Hu, 2021). Financial management can give the tools

needed to devise solutions to address the deficit. Dysonica is a large multinational inventive firm

that was founded in the United Kingdom but now works globally. Its items are accessible on the

main street and also internet. Competitive pressure has resulted in several price initiatives,

including the relocation of production from the United Kingdom.

TASK 1

Classify cost according to behaviour

Fixed cost:

Factory and storage rent: 18000 per month = 18000*12 = 216000

Insurance: 500 per month = 500*12 = 6000

Machinery: 1500 per month = 1500*12 = 18000

Utilities: 500 per month = 500*12 = 6000

Variable Cost:

Direct labour: 17500 per month

Raw material: 15000

Semi variable cost:

Office and sales staff: 9000 per month = 9000*12 = 18000

Logistics cost: 3000 per month

Fixed Costs £ Variable Costs £ Semi-variable

Costs

£

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

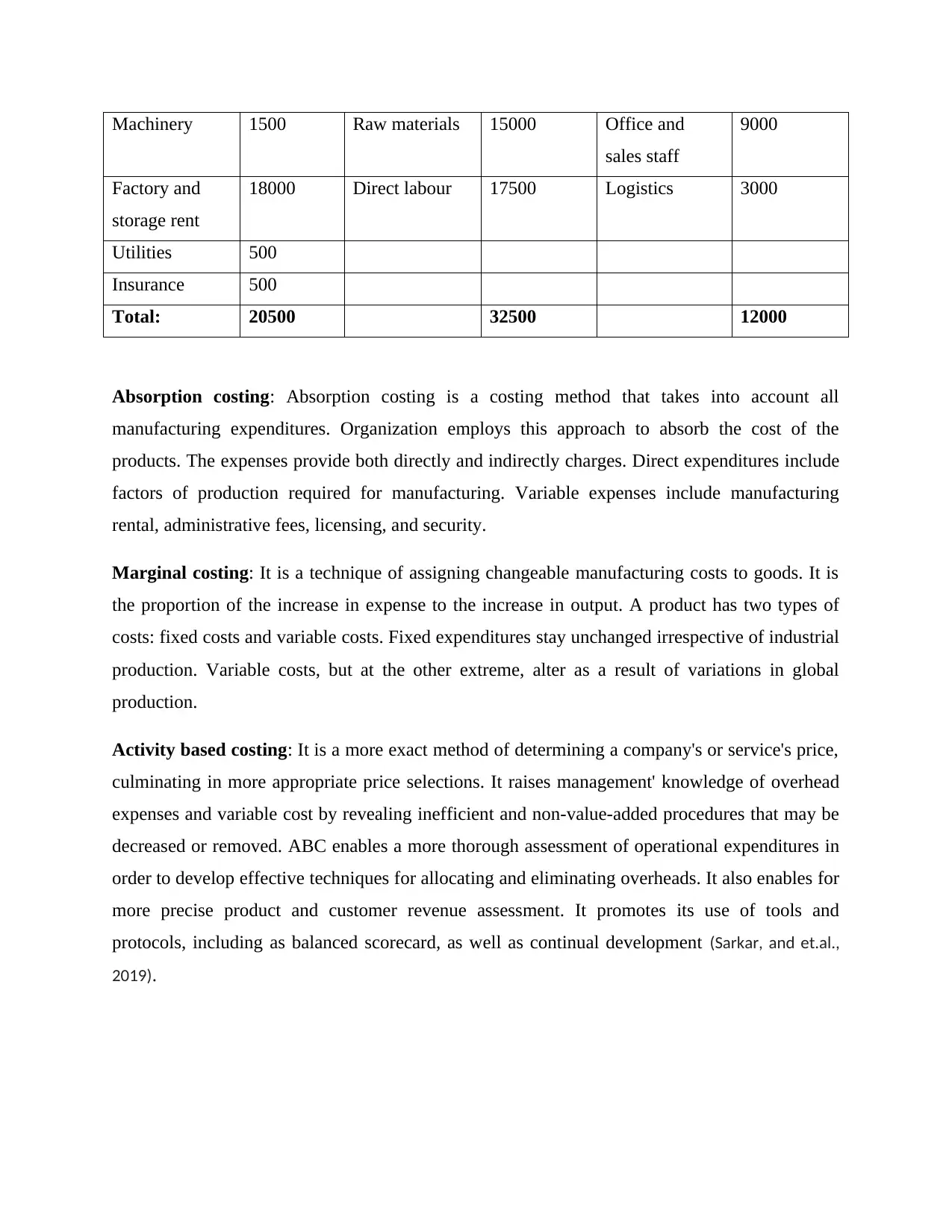

Machinery 1500 Raw materials 15000 Office and

sales staff

9000

Factory and

storage rent

18000 Direct labour 17500 Logistics 3000

Utilities 500

Insurance 500

Total: 20500 32500 12000

Absorption costing: Absorption costing is a costing method that takes into account all

manufacturing expenditures. Organization employs this approach to absorb the cost of the

products. The expenses provide both directly and indirectly charges. Direct expenditures include

factors of production required for manufacturing. Variable expenses include manufacturing

rental, administrative fees, licensing, and security.

Marginal costing: It is a technique of assigning changeable manufacturing costs to goods. It is

the proportion of the increase in expense to the increase in output. A product has two types of

costs: fixed costs and variable costs. Fixed expenditures stay unchanged irrespective of industrial

production. Variable costs, but at the other extreme, alter as a result of variations in global

production.

Activity based costing: It is a more exact method of determining a company's or service's price,

culminating in more appropriate price selections. It raises management' knowledge of overhead

expenses and variable cost by revealing inefficient and non-value-added procedures that may be

decreased or removed. ABC enables a more thorough assessment of operational expenditures in

order to develop effective techniques for allocating and eliminating overheads. It also enables for

more precise product and customer revenue assessment. It promotes its use of tools and

protocols, including as balanced scorecard, as well as continual development (Sarkar, and et.al.,

2019).

sales staff

9000

Factory and

storage rent

18000 Direct labour 17500 Logistics 3000

Utilities 500

Insurance 500

Total: 20500 32500 12000

Absorption costing: Absorption costing is a costing method that takes into account all

manufacturing expenditures. Organization employs this approach to absorb the cost of the

products. The expenses provide both directly and indirectly charges. Direct expenditures include

factors of production required for manufacturing. Variable expenses include manufacturing

rental, administrative fees, licensing, and security.

Marginal costing: It is a technique of assigning changeable manufacturing costs to goods. It is

the proportion of the increase in expense to the increase in output. A product has two types of

costs: fixed costs and variable costs. Fixed expenditures stay unchanged irrespective of industrial

production. Variable costs, but at the other extreme, alter as a result of variations in global

production.

Activity based costing: It is a more exact method of determining a company's or service's price,

culminating in more appropriate price selections. It raises management' knowledge of overhead

expenses and variable cost by revealing inefficient and non-value-added procedures that may be

decreased or removed. ABC enables a more thorough assessment of operational expenditures in

order to develop effective techniques for allocating and eliminating overheads. It also enables for

more precise product and customer revenue assessment. It promotes its use of tools and

protocols, including as balanced scorecard, as well as continual development (Sarkar, and et.al.,

2019).

TASK 2

Discuss the judgments and conclusions based on cost reduction strategy

From the several costing strategies listed previously, it is advised that Dysonica Plc utilise

activity-based spending or marginal costing to enables the firm control expenses that may come

from various operations. This enables the firm to separate expenses based on its procedures and

determine which one is spending the majority of the costs, guiding administration to decrease

costs and optimize its strategies accordingly. Activity-based costing is a one-stop solution for

businesses to control their expenses. It allows businesses to specify expenses as they occur rather

than combining them with some other expenditure. In this manner, the actual price source is

recognised, and organisations may concentrate on properly controlling that respective cost

heading rather than concentrating on other inflexible drivers. The distribution of overhead costs

is more objective and accurate since overhead expenditures are divided and structured into

categories depending on the number of operations. To make things easier, ABC classifies

expenses by function instead of putting all costs together again to estimate the firm's indirectly

expenses (Rashid, and Hersi, 2021).

Traditionally unidentifiable expenditures, such as depreciation, are now identifiable to individual

tasks through the use of activity-based accounting. The ABC approach can effect the unit price

of low-volume commodities by shifting administrative expenditures from elevated goods to

reduced goods.

TASK 3

Preparation a 12 - month forecast/budget for the business up to 30 April 2023

Predicting prospective income and expenditure is part of cash flow forecasting. A cash

flow prediction is an important tool for their organization since it tells them if they will have

sufficient income to operate or develop their firm. This will reveal when more money is leaving

the company than coming in. A cash flow projection is a technique used by financial and

administration experts to anticipate impending cash needs across their organisation. The primary

goal of financial planning is to help with cash management; the greater the organisation, the

more complicated and difficult cash flow statement gets.

Following is the cash flow forecast for the business of Dysonica' up to 30th April 2023

Discuss the judgments and conclusions based on cost reduction strategy

From the several costing strategies listed previously, it is advised that Dysonica Plc utilise

activity-based spending or marginal costing to enables the firm control expenses that may come

from various operations. This enables the firm to separate expenses based on its procedures and

determine which one is spending the majority of the costs, guiding administration to decrease

costs and optimize its strategies accordingly. Activity-based costing is a one-stop solution for

businesses to control their expenses. It allows businesses to specify expenses as they occur rather

than combining them with some other expenditure. In this manner, the actual price source is

recognised, and organisations may concentrate on properly controlling that respective cost

heading rather than concentrating on other inflexible drivers. The distribution of overhead costs

is more objective and accurate since overhead expenditures are divided and structured into

categories depending on the number of operations. To make things easier, ABC classifies

expenses by function instead of putting all costs together again to estimate the firm's indirectly

expenses (Rashid, and Hersi, 2021).

Traditionally unidentifiable expenditures, such as depreciation, are now identifiable to individual

tasks through the use of activity-based accounting. The ABC approach can effect the unit price

of low-volume commodities by shifting administrative expenditures from elevated goods to

reduced goods.

TASK 3

Preparation a 12 - month forecast/budget for the business up to 30 April 2023

Predicting prospective income and expenditure is part of cash flow forecasting. A cash

flow prediction is an important tool for their organization since it tells them if they will have

sufficient income to operate or develop their firm. This will reveal when more money is leaving

the company than coming in. A cash flow projection is a technique used by financial and

administration experts to anticipate impending cash needs across their organisation. The primary

goal of financial planning is to help with cash management; the greater the organisation, the

more complicated and difficult cash flow statement gets.

Following is the cash flow forecast for the business of Dysonica' up to 30th April 2023

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

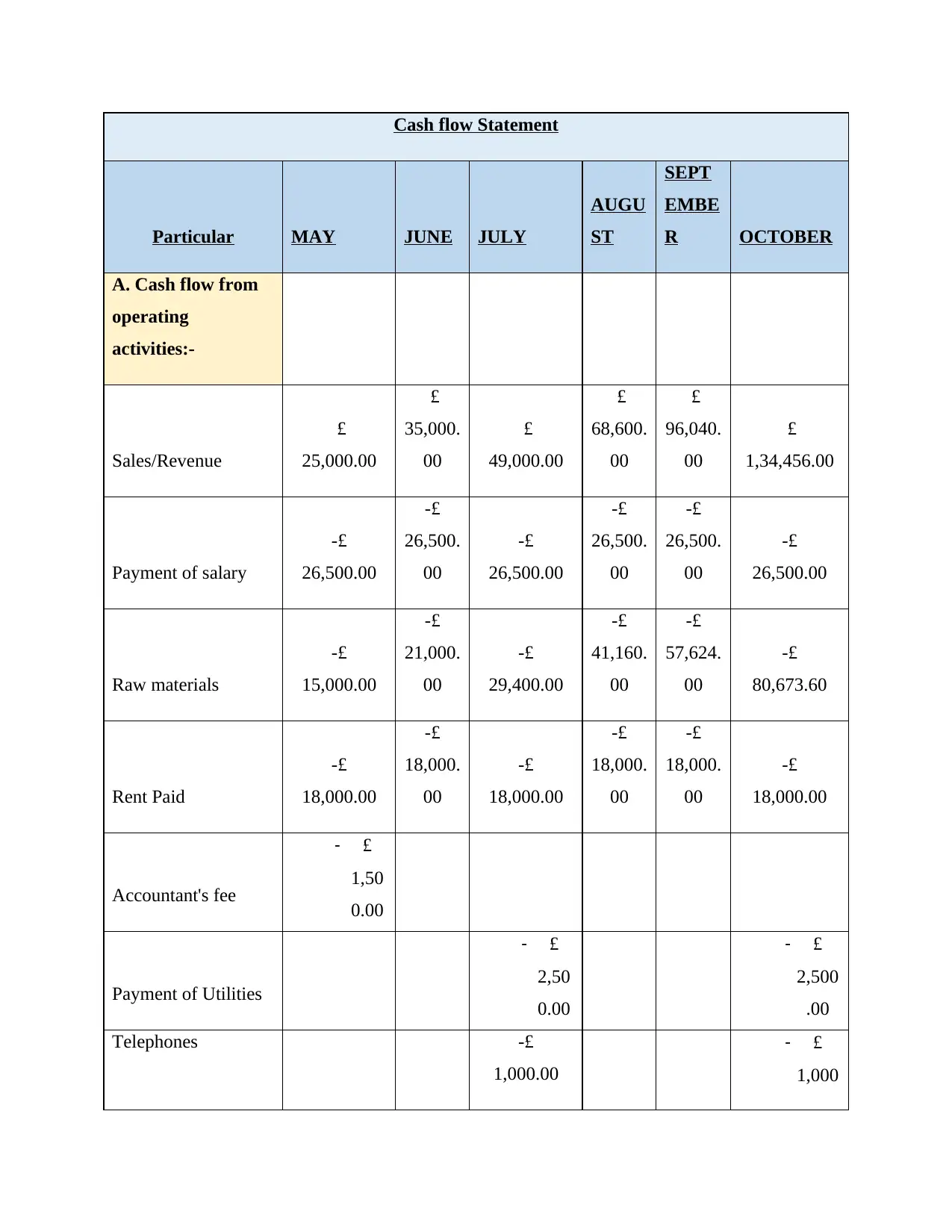

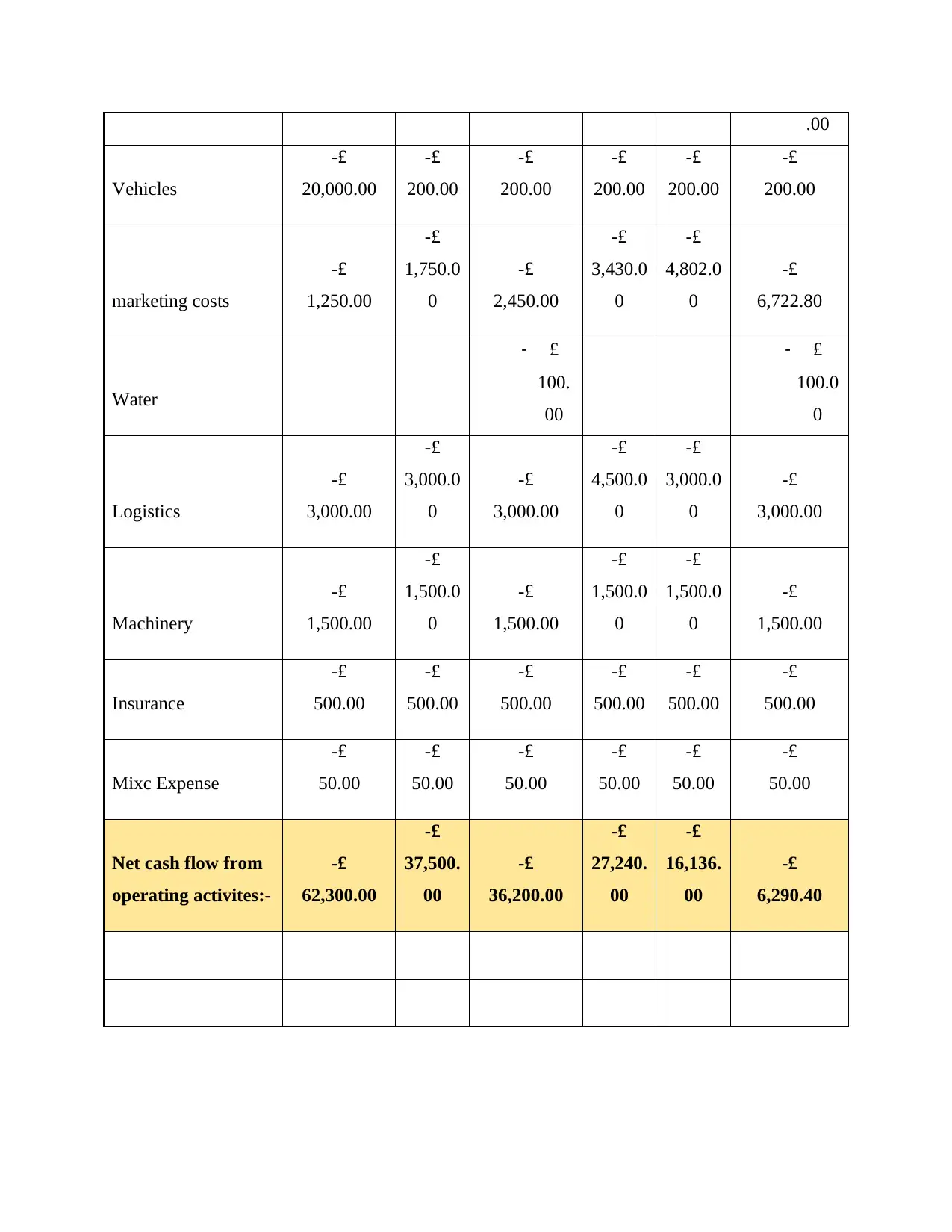

Cash flow Statement

Particular MAY JUNE JULY

AUGU

ST

SEPT

EMBE

R OCTOBER

A. Cash flow from

operating

activities:-

Sales/Revenue

£

25,000.00

£

35,000.

00

£

49,000.00

£

68,600.

00

£

96,040.

00

£

1,34,456.00

Payment of salary

-£

26,500.00

-£

26,500.

00

-£

26,500.00

-£

26,500.

00

-£

26,500.

00

-£

26,500.00

Raw materials

-£

15,000.00

-£

21,000.

00

-£

29,400.00

-£

41,160.

00

-£

57,624.

00

-£

80,673.60

Rent Paid

-£

18,000.00

-£

18,000.

00

-£

18,000.00

-£

18,000.

00

-£

18,000.

00

-£

18,000.00

Accountant's fee

- £

1,50

0.00

Payment of Utilities

- £

2,50

0.00

- £

2,500

.00

Telephones -£

1,000.00

- £

1,000

Particular MAY JUNE JULY

AUGU

ST

SEPT

EMBE

R OCTOBER

A. Cash flow from

operating

activities:-

Sales/Revenue

£

25,000.00

£

35,000.

00

£

49,000.00

£

68,600.

00

£

96,040.

00

£

1,34,456.00

Payment of salary

-£

26,500.00

-£

26,500.

00

-£

26,500.00

-£

26,500.

00

-£

26,500.

00

-£

26,500.00

Raw materials

-£

15,000.00

-£

21,000.

00

-£

29,400.00

-£

41,160.

00

-£

57,624.

00

-£

80,673.60

Rent Paid

-£

18,000.00

-£

18,000.

00

-£

18,000.00

-£

18,000.

00

-£

18,000.

00

-£

18,000.00

Accountant's fee

- £

1,50

0.00

Payment of Utilities

- £

2,50

0.00

- £

2,500

.00

Telephones -£

1,000.00

- £

1,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

.00

Vehicles

-£

20,000.00

-£

200.00

-£

200.00

-£

200.00

-£

200.00

-£

200.00

marketing costs

-£

1,250.00

-£

1,750.0

0

-£

2,450.00

-£

3,430.0

0

-£

4,802.0

0

-£

6,722.80

Water

- £

100.

00

- £

100.0

0

Logistics

-£

3,000.00

-£

3,000.0

0

-£

3,000.00

-£

4,500.0

0

-£

3,000.0

0

-£

3,000.00

Machinery

-£

1,500.00

-£

1,500.0

0

-£

1,500.00

-£

1,500.0

0

-£

1,500.0

0

-£

1,500.00

Insurance

-£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

500.00

Mixc Expense

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

50.00

Net cash flow from

operating activites:-

-£

62,300.00

-£

37,500.

00

-£

36,200.00

-£

27,240.

00

-£

16,136.

00

-£

6,290.40

Vehicles

-£

20,000.00

-£

200.00

-£

200.00

-£

200.00

-£

200.00

-£

200.00

marketing costs

-£

1,250.00

-£

1,750.0

0

-£

2,450.00

-£

3,430.0

0

-£

4,802.0

0

-£

6,722.80

Water

- £

100.

00

- £

100.0

0

Logistics

-£

3,000.00

-£

3,000.0

0

-£

3,000.00

-£

4,500.0

0

-£

3,000.0

0

-£

3,000.00

Machinery

-£

1,500.00

-£

1,500.0

0

-£

1,500.00

-£

1,500.0

0

-£

1,500.0

0

-£

1,500.00

Insurance

-£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

500.00

Mixc Expense

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

50.00

Net cash flow from

operating activites:-

-£

62,300.00

-£

37,500.

00

-£

36,200.00

-£

27,240.

00

-£

16,136.

00

-£

6,290.40

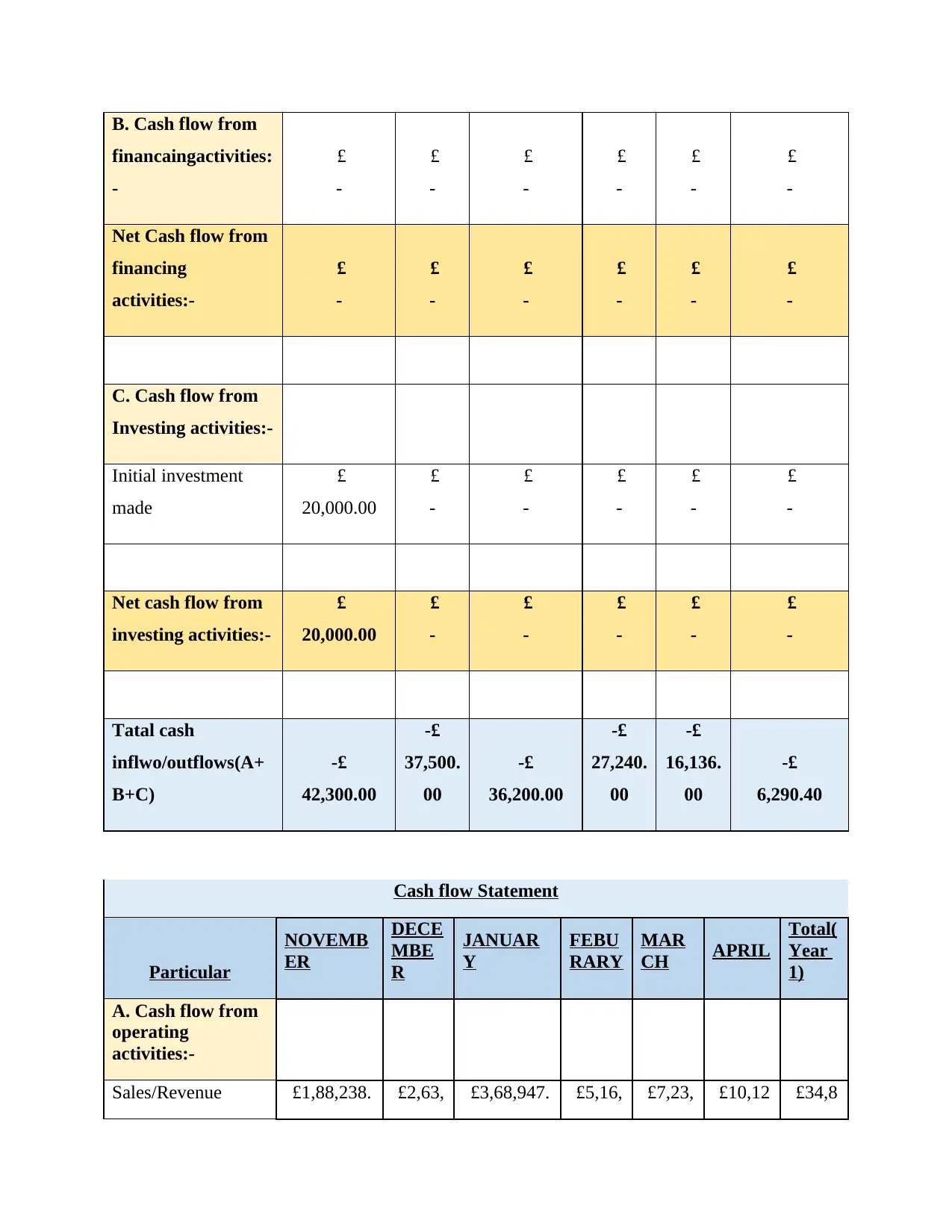

B. Cash flow from

financaingactivities:

-

£

-

£

-

£

-

£

-

£

-

£

-

Net Cash flow from

financing

activities:-

£

-

£

-

£

-

£

-

£

-

£

-

C. Cash flow from

Investing activities:-

Initial investment

made

£

20,000.00

£

-

£

-

£

-

£

-

£

-

Net cash flow from

investing activities:-

£

20,000.00

£

-

£

-

£

-

£

-

£

-

Tatal cash

inflwo/outflows(A+

B+C)

-£

42,300.00

-£

37,500.

00

-£

36,200.00

-£

27,240.

00

-£

16,136.

00

-£

6,290.40

Cash flow Statement

Particular

NOVEMB

ER

DECE

MBE

R

JANUAR

Y

FEBU

RARY

MAR

CH APRIL

Total(

Year

1)

A. Cash flow from

operating

activities:-

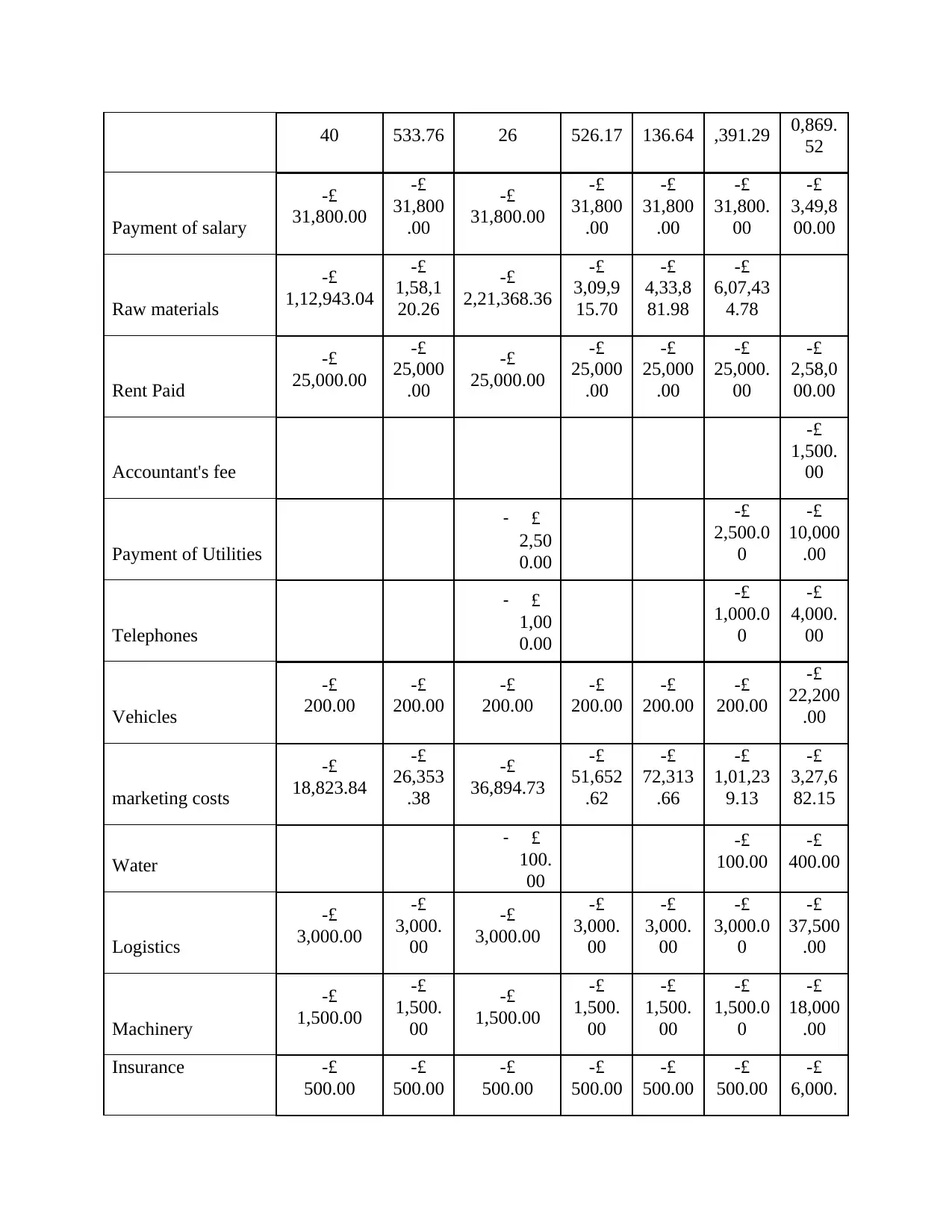

Sales/Revenue £1,88,238. £2,63, £3,68,947. £5,16, £7,23, £10,12 £34,8

financaingactivities:

-

£

-

£

-

£

-

£

-

£

-

£

-

Net Cash flow from

financing

activities:-

£

-

£

-

£

-

£

-

£

-

£

-

C. Cash flow from

Investing activities:-

Initial investment

made

£

20,000.00

£

-

£

-

£

-

£

-

£

-

Net cash flow from

investing activities:-

£

20,000.00

£

-

£

-

£

-

£

-

£

-

Tatal cash

inflwo/outflows(A+

B+C)

-£

42,300.00

-£

37,500.

00

-£

36,200.00

-£

27,240.

00

-£

16,136.

00

-£

6,290.40

Cash flow Statement

Particular

NOVEMB

ER

DECE

MBE

R

JANUAR

Y

FEBU

RARY

MAR

CH APRIL

Total(

Year

1)

A. Cash flow from

operating

activities:-

Sales/Revenue £1,88,238. £2,63, £3,68,947. £5,16, £7,23, £10,12 £34,8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

40 533.76 26 526.17 136.64 ,391.29 0,869.

52

Payment of salary

-£

31,800.00

-£

31,800

.00

-£

31,800.00

-£

31,800

.00

-£

31,800

.00

-£

31,800.

00

-£

3,49,8

00.00

Raw materials

-£

1,12,943.04

-£

1,58,1

20.26

-£

2,21,368.36

-£

3,09,9

15.70

-£

4,33,8

81.98

-£

6,07,43

4.78

Rent Paid

-£

25,000.00

-£

25,000

.00

-£

25,000.00

-£

25,000

.00

-£

25,000

.00

-£

25,000.

00

-£

2,58,0

00.00

Accountant's fee

-£

1,500.

00

Payment of Utilities

- £

2,50

0.00

-£

2,500.0

0

-£

10,000

.00

Telephones

- £

1,00

0.00

-£

1,000.0

0

-£

4,000.

00

Vehicles

-£

200.00

-£

200.00

-£

200.00

-£

200.00

-£

200.00

-£

200.00

-£

22,200

.00

marketing costs

-£

18,823.84

-£

26,353

.38

-£

36,894.73

-£

51,652

.62

-£

72,313

.66

-£

1,01,23

9.13

-£

3,27,6

82.15

Water

- £

100.

00

-£

100.00

-£

400.00

Logistics

-£

3,000.00

-£

3,000.

00

-£

3,000.00

-£

3,000.

00

-£

3,000.

00

-£

3,000.0

0

-£

37,500

.00

Machinery

-£

1,500.00

-£

1,500.

00

-£

1,500.00

-£

1,500.

00

-£

1,500.

00

-£

1,500.0

0

-£

18,000

.00

Insurance -£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

6,000.

52

Payment of salary

-£

31,800.00

-£

31,800

.00

-£

31,800.00

-£

31,800

.00

-£

31,800

.00

-£

31,800.

00

-£

3,49,8

00.00

Raw materials

-£

1,12,943.04

-£

1,58,1

20.26

-£

2,21,368.36

-£

3,09,9

15.70

-£

4,33,8

81.98

-£

6,07,43

4.78

Rent Paid

-£

25,000.00

-£

25,000

.00

-£

25,000.00

-£

25,000

.00

-£

25,000

.00

-£

25,000.

00

-£

2,58,0

00.00

Accountant's fee

-£

1,500.

00

Payment of Utilities

- £

2,50

0.00

-£

2,500.0

0

-£

10,000

.00

Telephones

- £

1,00

0.00

-£

1,000.0

0

-£

4,000.

00

Vehicles

-£

200.00

-£

200.00

-£

200.00

-£

200.00

-£

200.00

-£

200.00

-£

22,200

.00

marketing costs

-£

18,823.84

-£

26,353

.38

-£

36,894.73

-£

51,652

.62

-£

72,313

.66

-£

1,01,23

9.13

-£

3,27,6

82.15

Water

- £

100.

00

-£

100.00

-£

400.00

Logistics

-£

3,000.00

-£

3,000.

00

-£

3,000.00

-£

3,000.

00

-£

3,000.

00

-£

3,000.0

0

-£

37,500

.00

Machinery

-£

1,500.00

-£

1,500.

00

-£

1,500.00

-£

1,500.

00

-£

1,500.

00

-£

1,500.0

0

-£

18,000

.00

Insurance -£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

6,000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

00

Mix Expense

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

600.00

Net cash flow from

operating

activities:-

- £

5,57

8.48

£

17,010

.13

£

45,034.18

£

92,907

.85

£

1,54,8

90.99

£

2,38,06

7.39

£

24,45,

187.37

B. Cash flow from

financing

activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

Net Cash flow

from financing

activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

C. Cash flow from

Investing

activities:-

Initial investment

made

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000

.00

Net cash flow from

investing

activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000

.00

Total cash

inflow/outflows(A+

B+C)

-£

5,578.48

£

17,010

.13

£

45,034.18

£

92,907

.85

£

1,54,8

90.99

£

2,38,06

7.39

£

24,65,

187.37

Mix Expense

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

600.00

Net cash flow from

operating

activities:-

- £

5,57

8.48

£

17,010

.13

£

45,034.18

£

92,907

.85

£

1,54,8

90.99

£

2,38,06

7.39

£

24,45,

187.37

B. Cash flow from

financing

activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

Net Cash flow

from financing

activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

C. Cash flow from

Investing

activities:-

Initial investment

made

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000

.00

Net cash flow from

investing

activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000

.00

Total cash

inflow/outflows(A+

B+C)

-£

5,578.48

£

17,010

.13

£

45,034.18

£

92,907

.85

£

1,54,8

90.99

£

2,38,06

7.39

£

24,65,

187.37

TASK 4

Clear justifications are needed to support the conclusions and recommendations made in your

evaluation

The cash flow budget given above demonstrates that Dysonica's company is performing

well. The company can get a considerable quantity of cash flow in various periods, resulting in

favourable liquid assets for the company. The company's sales are expanding at a rapid pace in

such seasons, as predicted, indicating that the company is able to sell enough items to maintain

itself in a competitive marketplace. The entire cash injection in the company in the first year was

£ 2,465,187, which is a wonderful chance for the company since they may engage in various

scenarios for the company and help Dysonica expand. The firm must minimise its costs,

particularly those spent as a result of the currency exchange rate between nations such as the

United Kingdom and China. The company might employ financial derivatives to evaluate the

transaction at a predefined rate that would assist the company control the costs associated with

this component of the operation. It can be noted that the firm has adverse cash inflows, which

implies that the company had a cash flow in the first six to eight years of operation, indicating

that the company either has to increase sales or cut expenditures (Utomo, and Pamungkas, 2018).

The cash outflow has an indirect impact on the firm's financial condition, which is a critical

condition for any company succeed in a highly market and worldwide. Costs could be reduced

by employing a different link of supplies and reviewing which initiatives are in control and

which are losing money in the control of the company.

CONCLUSION

According to the above-mentioned assessment, company finance and administration of these

money is a big and crucial aspect in the performance of the company. Businesses that operate on

a global scale, such as Dysonica, confront tough rivalry. To stay ahead of the competition in a

competitive field, they must lower the many costs that the firm faces. Cash flow projections are a

fantastic method of measuring the influx or cash outflows into or out of a firm at the conclusion

of a predefined timeframe, and the company may use it to establish its own budgeting. Marginal

and activity-based spending are two of the greatest costing techniques that a company may

adopt. Dysonica reduces the possibility of inaccuracy and counts each expense that must be

Clear justifications are needed to support the conclusions and recommendations made in your

evaluation

The cash flow budget given above demonstrates that Dysonica's company is performing

well. The company can get a considerable quantity of cash flow in various periods, resulting in

favourable liquid assets for the company. The company's sales are expanding at a rapid pace in

such seasons, as predicted, indicating that the company is able to sell enough items to maintain

itself in a competitive marketplace. The entire cash injection in the company in the first year was

£ 2,465,187, which is a wonderful chance for the company since they may engage in various

scenarios for the company and help Dysonica expand. The firm must minimise its costs,

particularly those spent as a result of the currency exchange rate between nations such as the

United Kingdom and China. The company might employ financial derivatives to evaluate the

transaction at a predefined rate that would assist the company control the costs associated with

this component of the operation. It can be noted that the firm has adverse cash inflows, which

implies that the company had a cash flow in the first six to eight years of operation, indicating

that the company either has to increase sales or cut expenditures (Utomo, and Pamungkas, 2018).

The cash outflow has an indirect impact on the firm's financial condition, which is a critical

condition for any company succeed in a highly market and worldwide. Costs could be reduced

by employing a different link of supplies and reviewing which initiatives are in control and

which are losing money in the control of the company.

CONCLUSION

According to the above-mentioned assessment, company finance and administration of these

money is a big and crucial aspect in the performance of the company. Businesses that operate on

a global scale, such as Dysonica, confront tough rivalry. To stay ahead of the competition in a

competitive field, they must lower the many costs that the firm faces. Cash flow projections are a

fantastic method of measuring the influx or cash outflows into or out of a firm at the conclusion

of a predefined timeframe, and the company may use it to establish its own budgeting. Marginal

and activity-based spending are two of the greatest costing techniques that a company may

adopt. Dysonica reduces the possibility of inaccuracy and counts each expense that must be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.