Business Finance: Analysis of Housing Market Trends and Returns

VerifiedAdded on 2021/05/31

|21

|4000

|22

Report

AI Summary

This business finance report offers a comprehensive analysis of housing market trends in Sydney, Hobart, and Newcastle over a 30-year period. It compares real estate returns with Australian stocks and bonds, evaluating the performance of residential property investments. The report examines property prices, income levels of architects, and the house price-to-income ratio in the three cities. Additionally, it explores mortgage mechanisms, referencing SUB Bank of Australia to determine mortgage conditions. The report also includes graphical representations and comparisons, providing a detailed overview of the housing market's dynamics and investment potential, with the data presented and analyzed thoroughly.

RUNNING HEAD: BUSINESS FINANCE

housing finance

housing finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business finance 1

Contents

Introduction................................................................................................................................2

Part 1..........................................................................................................................................2

Housing prices over 30 years.................................................................................................2

Real estate returns VS stock and bond returns.......................................................................3

Part 2..........................................................................................................................................5

Property prices in three cities.................................................................................................5

Comparing the prices..............................................................................................................6

Income level of an architect...................................................................................................6

The house price to income level ratio.....................................................................................6

References..................................................................................................................................7

Contents

Introduction................................................................................................................................2

Part 1..........................................................................................................................................2

Housing prices over 30 years.................................................................................................2

Real estate returns VS stock and bond returns.......................................................................3

Part 2..........................................................................................................................................5

Property prices in three cities.................................................................................................5

Comparing the prices..............................................................................................................6

Income level of an architect...................................................................................................6

The house price to income level ratio.....................................................................................6

References..................................................................................................................................7

Business finance 2

Introduction

The report contains an overall analysis of housing prices in the cities named as

Sydney, Hobart and Newcastle. In the first part, the trend in housing prices of each city over

the period of 30 years is been noticed and the performance of real estate market is evaluated.

The performance of housing is then compared to the Australian stocks and bonds. The report

also focuses on the average returns delivered by the residential property in Australia in

relation with its stocks and bonds. The performance is measured on the basis of 10 years and

20 years average annual gross returns given by the direct investment in residential property,

Australian stocks and bonds. The second part of the report contains a comparison of the

house prices in three cities respectively. The income level of an architect in those cities is

also analysed and then a house price to income level ratio is calculated. In third part how

mortgages work and taking the SUB bank of Australia for the purpose of determining the

conditions for mortgage have been analysed in general. A detailed analysis of the same has

been done in the excel sheet.

Part 1

Housing prices over 30 years

The following graph shows the trends in house prices in the cities of Australia. The

cities include Sydney, Hobart and Newcastle. In order to purchase a property in one of these

cities, the trend in their housing prices is observed over the past 30 years.

Introduction

The report contains an overall analysis of housing prices in the cities named as

Sydney, Hobart and Newcastle. In the first part, the trend in housing prices of each city over

the period of 30 years is been noticed and the performance of real estate market is evaluated.

The performance of housing is then compared to the Australian stocks and bonds. The report

also focuses on the average returns delivered by the residential property in Australia in

relation with its stocks and bonds. The performance is measured on the basis of 10 years and

20 years average annual gross returns given by the direct investment in residential property,

Australian stocks and bonds. The second part of the report contains a comparison of the

house prices in three cities respectively. The income level of an architect in those cities is

also analysed and then a house price to income level ratio is calculated. In third part how

mortgages work and taking the SUB bank of Australia for the purpose of determining the

conditions for mortgage have been analysed in general. A detailed analysis of the same has

been done in the excel sheet.

Part 1

Housing prices over 30 years

The following graph shows the trends in house prices in the cities of Australia. The

cities include Sydney, Hobart and Newcastle. In order to purchase a property in one of these

cities, the trend in their housing prices is observed over the past 30 years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business finance 3

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

House prices

Sydney Hobart New Castle

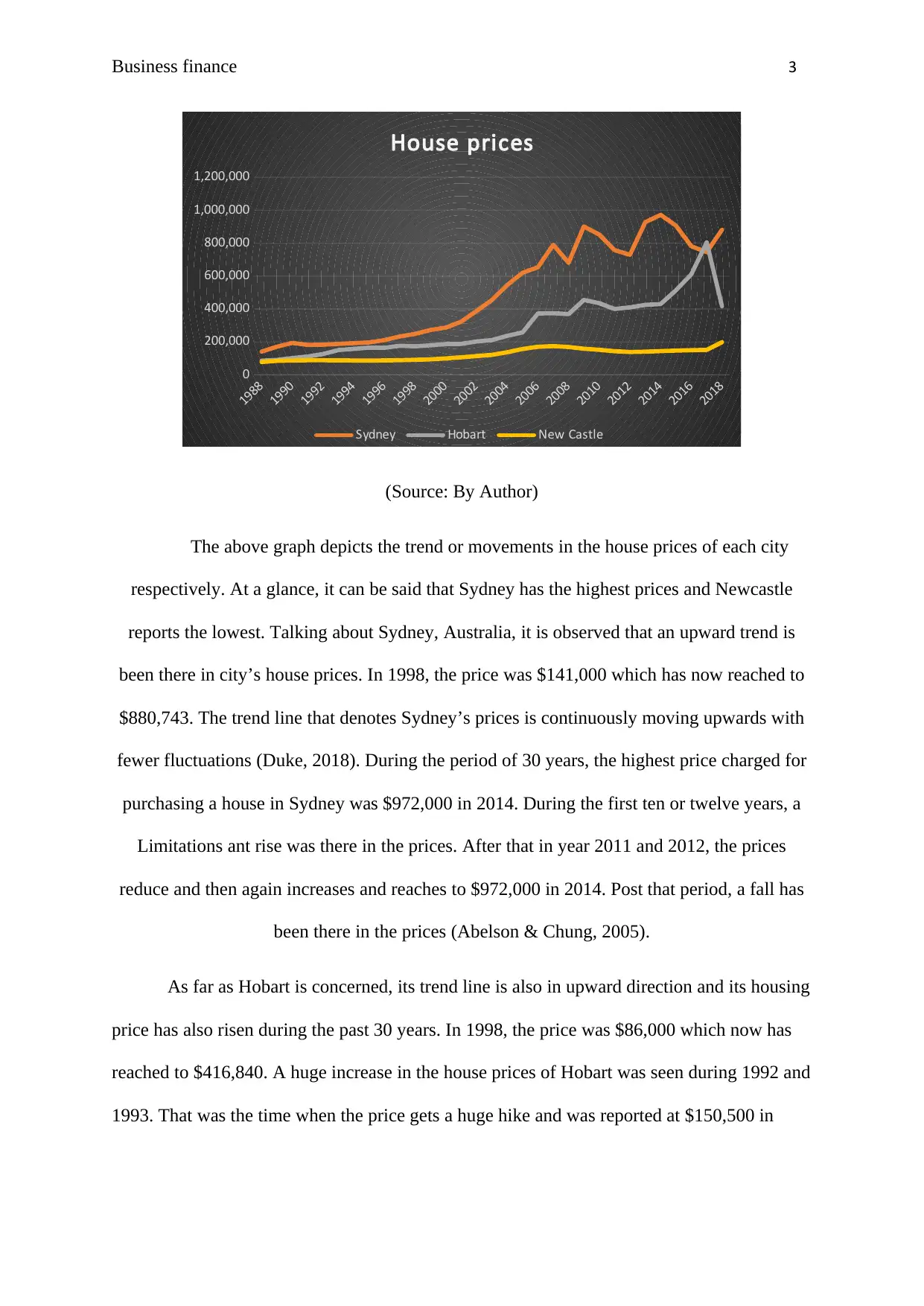

(Source: By Author)

The above graph depicts the trend or movements in the house prices of each city

respectively. At a glance, it can be said that Sydney has the highest prices and Newcastle

reports the lowest. Talking about Sydney, Australia, it is observed that an upward trend is

been there in city’s house prices. In 1998, the price was $141,000 which has now reached to

$880,743. The trend line that denotes Sydney’s prices is continuously moving upwards with

fewer fluctuations (Duke, 2018). During the period of 30 years, the highest price charged for

purchasing a house in Sydney was $972,000 in 2014. During the first ten or twelve years, a

Limitations ant rise was there in the prices. After that in year 2011 and 2012, the prices

reduce and then again increases and reaches to $972,000 in 2014. Post that period, a fall has

been there in the prices (Abelson & Chung, 2005).

As far as Hobart is concerned, its trend line is also in upward direction and its housing

price has also risen during the past 30 years. In 1998, the price was $86,000 which now has

reached to $416,840. A huge increase in the house prices of Hobart was seen during 1992 and

1993. That was the time when the price gets a huge hike and was reported at $150,500 in

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

House prices

Sydney Hobart New Castle

(Source: By Author)

The above graph depicts the trend or movements in the house prices of each city

respectively. At a glance, it can be said that Sydney has the highest prices and Newcastle

reports the lowest. Talking about Sydney, Australia, it is observed that an upward trend is

been there in city’s house prices. In 1998, the price was $141,000 which has now reached to

$880,743. The trend line that denotes Sydney’s prices is continuously moving upwards with

fewer fluctuations (Duke, 2018). During the period of 30 years, the highest price charged for

purchasing a house in Sydney was $972,000 in 2014. During the first ten or twelve years, a

Limitations ant rise was there in the prices. After that in year 2011 and 2012, the prices

reduce and then again increases and reaches to $972,000 in 2014. Post that period, a fall has

been there in the prices (Abelson & Chung, 2005).

As far as Hobart is concerned, its trend line is also in upward direction and its housing

price has also risen during the past 30 years. In 1998, the price was $86,000 which now has

reached to $416,840. A huge increase in the house prices of Hobart was seen during 1992 and

1993. That was the time when the price gets a huge hike and was reported at $150,500 in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business finance 4

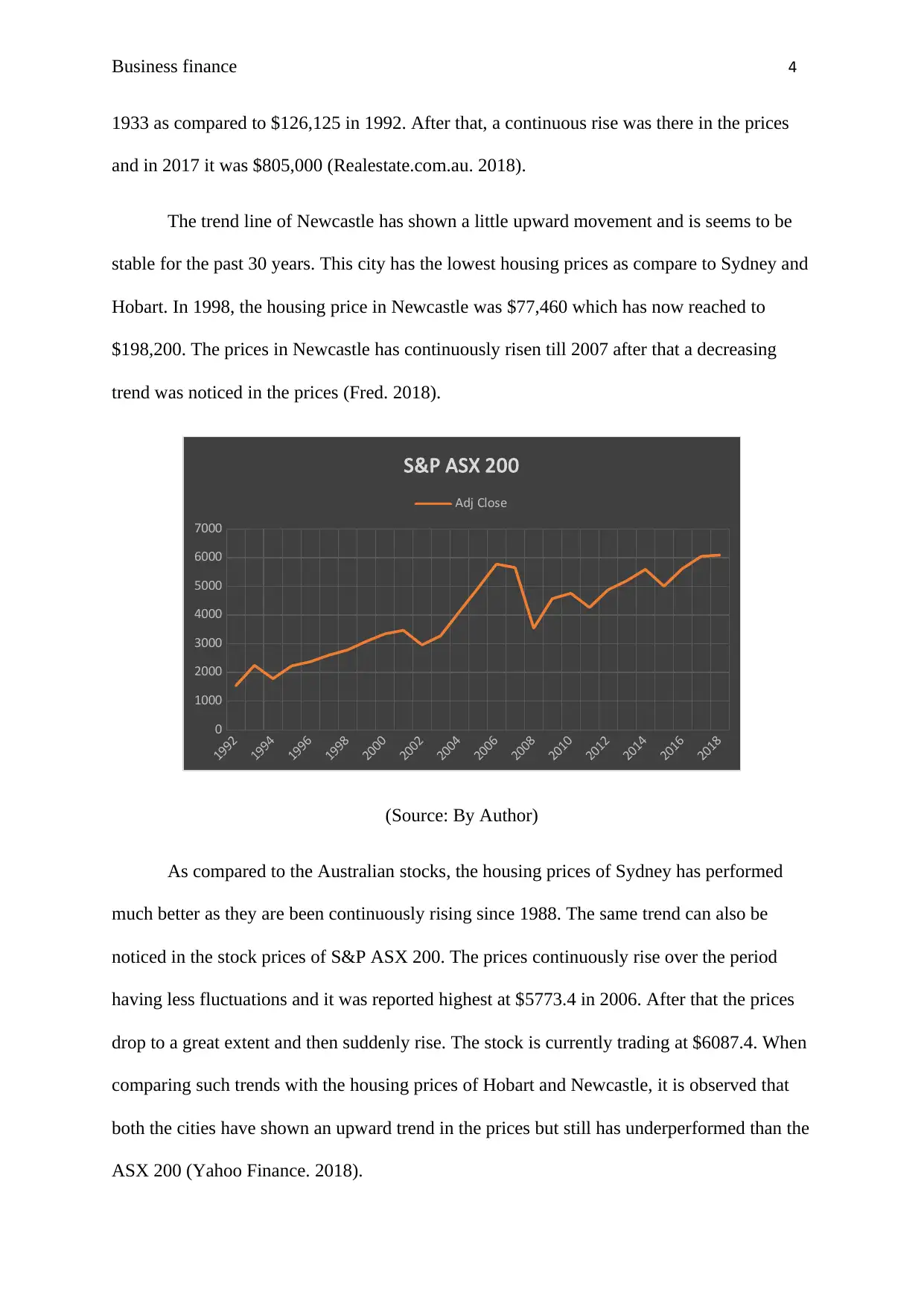

1933 as compared to $126,125 in 1992. After that, a continuous rise was there in the prices

and in 2017 it was $805,000 (Realestate.com.au. 2018).

The trend line of Newcastle has shown a little upward movement and is seems to be

stable for the past 30 years. This city has the lowest housing prices as compare to Sydney and

Hobart. In 1998, the housing price in Newcastle was $77,460 which has now reached to

$198,200. The prices in Newcastle has continuously risen till 2007 after that a decreasing

trend was noticed in the prices (Fred. 2018).

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

0

1000

2000

3000

4000

5000

6000

7000

S&P ASX 200

Adj Close

(Source: By Author)

As compared to the Australian stocks, the housing prices of Sydney has performed

much better as they are been continuously rising since 1988. The same trend can also be

noticed in the stock prices of S&P ASX 200. The prices continuously rise over the period

having less fluctuations and it was reported highest at $5773.4 in 2006. After that the prices

drop to a great extent and then suddenly rise. The stock is currently trading at $6087.4. When

comparing such trends with the housing prices of Hobart and Newcastle, it is observed that

both the cities have shown an upward trend in the prices but still has underperformed than the

ASX 200 (Yahoo Finance. 2018).

1933 as compared to $126,125 in 1992. After that, a continuous rise was there in the prices

and in 2017 it was $805,000 (Realestate.com.au. 2018).

The trend line of Newcastle has shown a little upward movement and is seems to be

stable for the past 30 years. This city has the lowest housing prices as compare to Sydney and

Hobart. In 1998, the housing price in Newcastle was $77,460 which has now reached to

$198,200. The prices in Newcastle has continuously risen till 2007 after that a decreasing

trend was noticed in the prices (Fred. 2018).

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

0

1000

2000

3000

4000

5000

6000

7000

S&P ASX 200

Adj Close

(Source: By Author)

As compared to the Australian stocks, the housing prices of Sydney has performed

much better as they are been continuously rising since 1988. The same trend can also be

noticed in the stock prices of S&P ASX 200. The prices continuously rise over the period

having less fluctuations and it was reported highest at $5773.4 in 2006. After that the prices

drop to a great extent and then suddenly rise. The stock is currently trading at $6087.4. When

comparing such trends with the housing prices of Hobart and Newcastle, it is observed that

both the cities have shown an upward trend in the prices but still has underperformed than the

ASX 200 (Yahoo Finance. 2018).

Business finance 5

Real estate returns VS stock and bond returns

It is historically and statistically true that Australian residential property or real estate

market has offered high and stable returns in for of both capital growth and rental income.

Evaluating the past five years, it is observed that residential properties situated in the capital

cities of Australia has offered relatively high returns based on their historical performance.

(Source: Brickx.com, 2017)

The above graph shows the real estate returns generated by the capital cities of

Australia. It can be seen that Sydney has offered highest returns of 85.3% over the five years

and also its prices have increased limitation instantly. Whereas, Hobart has only offered

28.8% returns as per its historical performance. Melbourne offered returns of 51.7% which

are pretty good but less than Sydney (Brickx.com. 2017).

When comparing such residential property returns to Australian stocks, bonds and

other assets over the time period, following chart is been shown

Real estate returns VS stock and bond returns

It is historically and statistically true that Australian residential property or real estate

market has offered high and stable returns in for of both capital growth and rental income.

Evaluating the past five years, it is observed that residential properties situated in the capital

cities of Australia has offered relatively high returns based on their historical performance.

(Source: Brickx.com, 2017)

The above graph shows the real estate returns generated by the capital cities of

Australia. It can be seen that Sydney has offered highest returns of 85.3% over the five years

and also its prices have increased limitation instantly. Whereas, Hobart has only offered

28.8% returns as per its historical performance. Melbourne offered returns of 51.7% which

are pretty good but less than Sydney (Brickx.com. 2017).

When comparing such residential property returns to Australian stocks, bonds and

other assets over the time period, following chart is been shown

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business finance 6

(Source: Brickx.com, 2017)

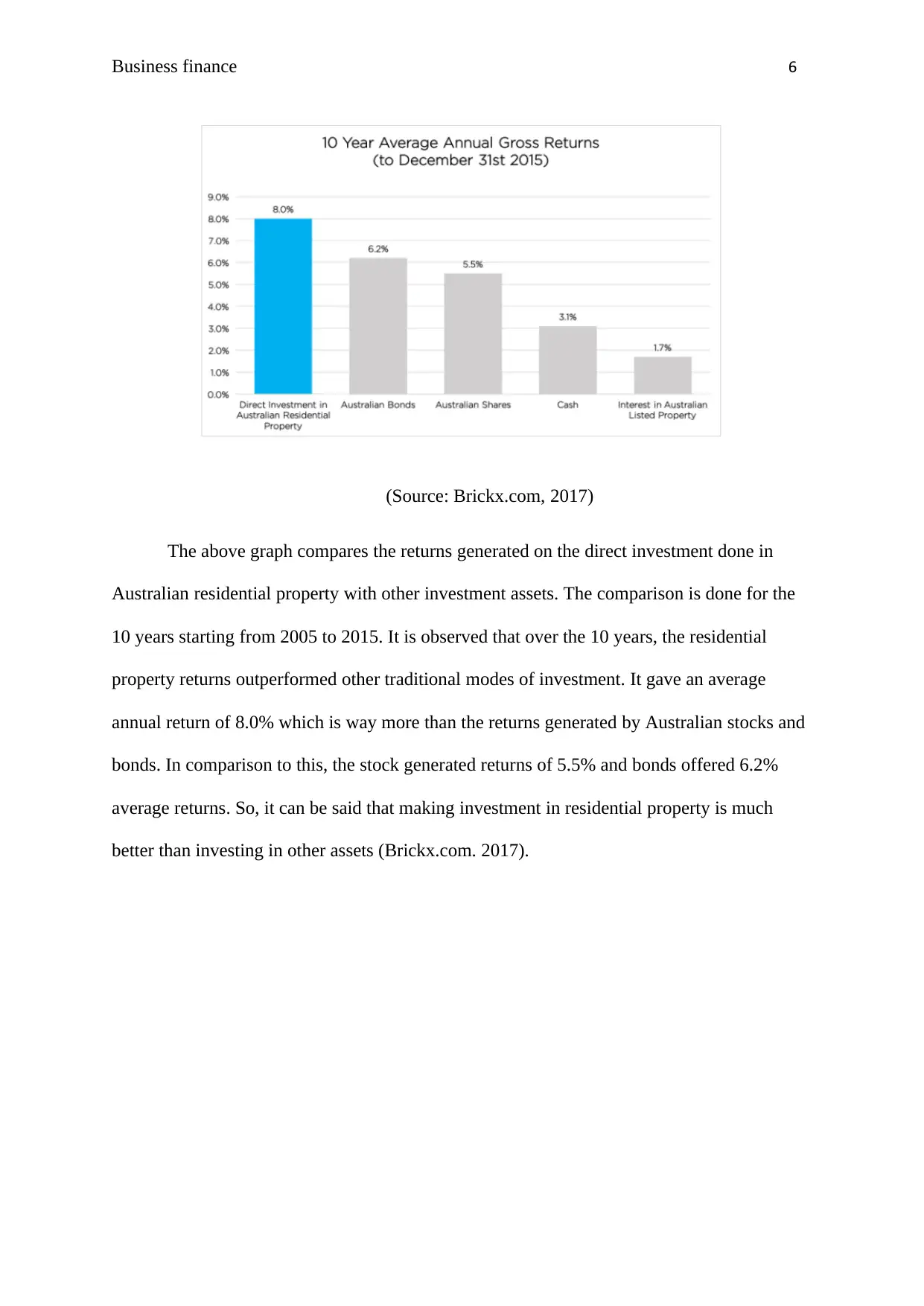

The above graph compares the returns generated on the direct investment done in

Australian residential property with other investment assets. The comparison is done for the

10 years starting from 2005 to 2015. It is observed that over the 10 years, the residential

property returns outperformed other traditional modes of investment. It gave an average

annual return of 8.0% which is way more than the returns generated by Australian stocks and

bonds. In comparison to this, the stock generated returns of 5.5% and bonds offered 6.2%

average returns. So, it can be said that making investment in residential property is much

better than investing in other assets (Brickx.com. 2017).

(Source: Brickx.com, 2017)

The above graph compares the returns generated on the direct investment done in

Australian residential property with other investment assets. The comparison is done for the

10 years starting from 2005 to 2015. It is observed that over the 10 years, the residential

property returns outperformed other traditional modes of investment. It gave an average

annual return of 8.0% which is way more than the returns generated by Australian stocks and

bonds. In comparison to this, the stock generated returns of 5.5% and bonds offered 6.2%

average returns. So, it can be said that making investment in residential property is much

better than investing in other assets (Brickx.com. 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business finance 7

(Source: Brickx.com, 2017)

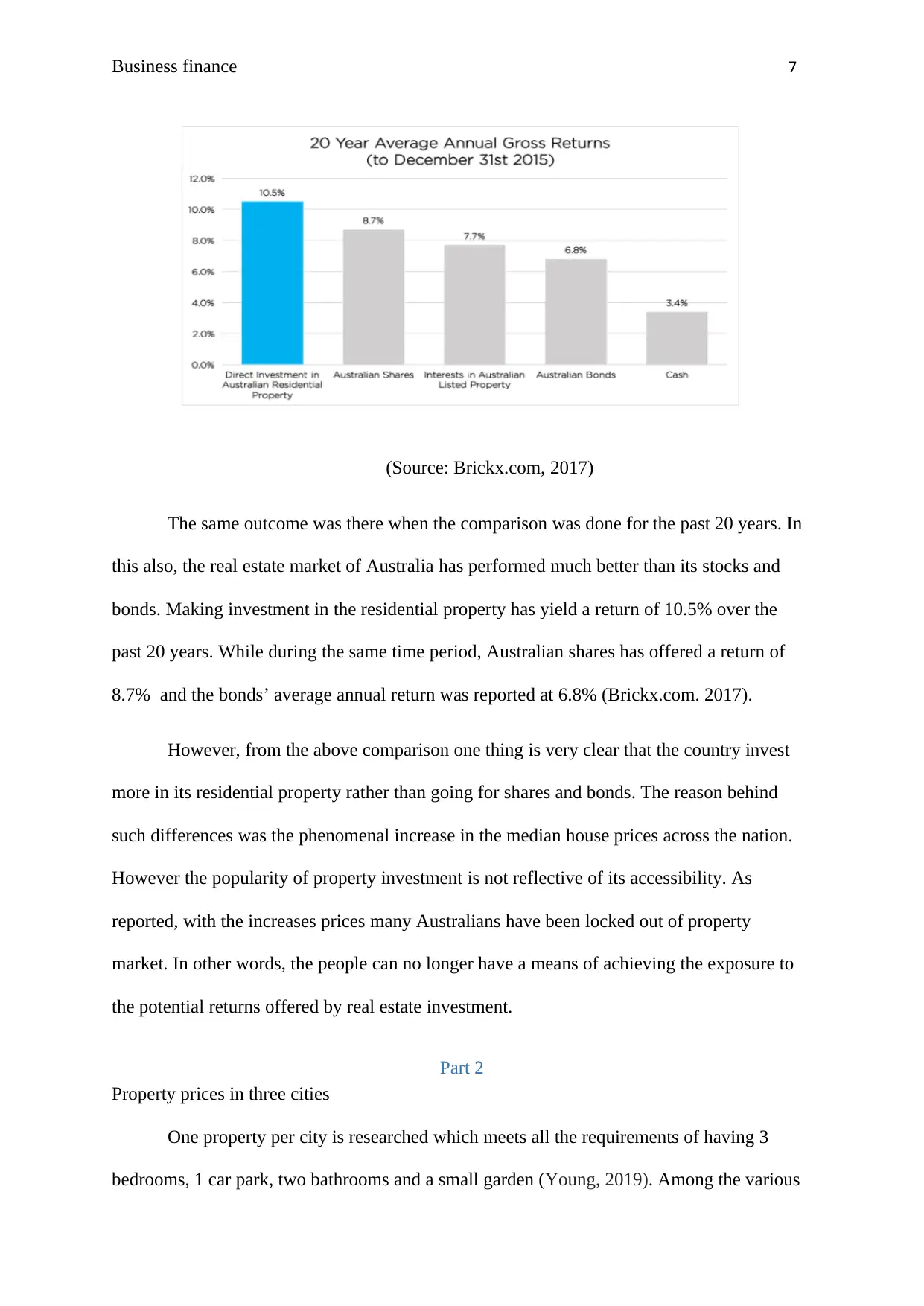

The same outcome was there when the comparison was done for the past 20 years. In

this also, the real estate market of Australia has performed much better than its stocks and

bonds. Making investment in the residential property has yield a return of 10.5% over the

past 20 years. While during the same time period, Australian shares has offered a return of

8.7% and the bonds’ average annual return was reported at 6.8% (Brickx.com. 2017).

However, from the above comparison one thing is very clear that the country invest

more in its residential property rather than going for shares and bonds. The reason behind

such differences was the phenomenal increase in the median house prices across the nation.

However the popularity of property investment is not reflective of its accessibility. As

reported, with the increases prices many Australians have been locked out of property

market. In other words, the people can no longer have a means of achieving the exposure to

the potential returns offered by real estate investment.

Part 2

Property prices in three cities

One property per city is researched which meets all the requirements of having 3

bedrooms, 1 car park, two bathrooms and a small garden (Young, 2019). Among the various

(Source: Brickx.com, 2017)

The same outcome was there when the comparison was done for the past 20 years. In

this also, the real estate market of Australia has performed much better than its stocks and

bonds. Making investment in the residential property has yield a return of 10.5% over the

past 20 years. While during the same time period, Australian shares has offered a return of

8.7% and the bonds’ average annual return was reported at 6.8% (Brickx.com. 2017).

However, from the above comparison one thing is very clear that the country invest

more in its residential property rather than going for shares and bonds. The reason behind

such differences was the phenomenal increase in the median house prices across the nation.

However the popularity of property investment is not reflective of its accessibility. As

reported, with the increases prices many Australians have been locked out of property

market. In other words, the people can no longer have a means of achieving the exposure to

the potential returns offered by real estate investment.

Part 2

Property prices in three cities

One property per city is researched which meets all the requirements of having 3

bedrooms, 1 car park, two bathrooms and a small garden (Young, 2019). Among the various

Business finance 8

properties available in Australia’s capital cities, following are been chosen from Sydney,

Hobart and Newcastle

Cities House Property

Sydney 15 Kale Road, Spring Farm, NSW 2570

Hobart 5 Gardenia Grove, Sandy Bay, TAS 7005

Newcastle Kirkwood Place, Gosforth, Newcastle upon Tyne

The above properties are selected from each city and the do match with all the three

requirements that are needed. Since, situated in different cities the prices are also different. A

snapshot of their prices is as follows:

Cities House Property Prices

Sydney 15 Kale Road, Spring Farm, NSW 2570 $749,950

Hobart 5 Gardenia Grove, Sandy Bay, TAS 7005 $840,00 plus

Newcastl

e

64, Park Avenue, Cooks Hill NSW 2300 $1087500

Comparing the prices

Looking at the prices, the house property in Newcastle seems to be the most

expensive than the other two. Despite the prices, the amenities provided are better (Hurley,

Wood & Groenhart, 2018). The house property in Sydney is situated at the riverside estate of

the spring farm and is a beautifully designed home. It is located close to schools, main market

and sporting fields which are easily accessible. The property offers 3 bedrooms, 2 bathrooms,

a garden area and 2 car parking lots. All these are the requirements which are needed to be

properties available in Australia’s capital cities, following are been chosen from Sydney,

Hobart and Newcastle

Cities House Property

Sydney 15 Kale Road, Spring Farm, NSW 2570

Hobart 5 Gardenia Grove, Sandy Bay, TAS 7005

Newcastle Kirkwood Place, Gosforth, Newcastle upon Tyne

The above properties are selected from each city and the do match with all the three

requirements that are needed. Since, situated in different cities the prices are also different. A

snapshot of their prices is as follows:

Cities House Property Prices

Sydney 15 Kale Road, Spring Farm, NSW 2570 $749,950

Hobart 5 Gardenia Grove, Sandy Bay, TAS 7005 $840,00 plus

Newcastl

e

64, Park Avenue, Cooks Hill NSW 2300 $1087500

Comparing the prices

Looking at the prices, the house property in Newcastle seems to be the most

expensive than the other two. Despite the prices, the amenities provided are better (Hurley,

Wood & Groenhart, 2018). The house property in Sydney is situated at the riverside estate of

the spring farm and is a beautifully designed home. It is located close to schools, main market

and sporting fields which are easily accessible. The property offers 3 bedrooms, 2 bathrooms,

a garden area and 2 car parking lots. All these are the requirements which are needed to be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business finance 9

fulfilled. The land area is 390sqm. The house is stylish and gives a perfect view of riverside

(Realestateview.com. 2018).

On the other hand, the property located in Hobart is situated in a quiet street which is

surrounded by other quality homes. It gives a view of River Derwent, have high end fixtures

and fittings and provides a comfortable living. It has 3 bedrooms, 2 modern style bathrooms

and 2 car parking. Along with this the house is surrounded by many bushes providing a

garden area also. With the land area of 860sqm, it perfectly fits with the requirements.

However, the prices are too high to afford (Realestateview.com. 2018).

The house in Newcastle is available at very high price worth $1,087500 and also

fulfils all the requirements. It is located in the area which covers the local shops, cafes, close

to transport facilities and fireplaces. (Li, Bao, Sellis, Yan & Zhang, 2018). The house is six

bedroom semi-detached bungalow which offer beautiful private gardens, 3 garage spaces, a

balcony, and I ground swimming pool and secure parking facility. A bungalow style house

offers great facilities apart from the mentioned above include alarm and floorboards

(Onthemarket.com. 2018).

Income level of an architect

Architects are been known for designing and creating new houses and building. In

different cities of world they are been paid differently (Akimov & Stevenson, 2017). Talking

about Sydney, the average income of a design architect is $62,457 per year. The skills which

make a person to get highly paid for his profile are Arch CAD, GRAPHISOFT, Project

management and many more. While, in Hobart architects are paid $92,939 per year. This is

almost 1.6 times more than the median wage of the country. However, the tax charges on

income level amounted to $23,878.07 which makes the net income of $69,060.57. In

fulfilled. The land area is 390sqm. The house is stylish and gives a perfect view of riverside

(Realestateview.com. 2018).

On the other hand, the property located in Hobart is situated in a quiet street which is

surrounded by other quality homes. It gives a view of River Derwent, have high end fixtures

and fittings and provides a comfortable living. It has 3 bedrooms, 2 modern style bathrooms

and 2 car parking. Along with this the house is surrounded by many bushes providing a

garden area also. With the land area of 860sqm, it perfectly fits with the requirements.

However, the prices are too high to afford (Realestateview.com. 2018).

The house in Newcastle is available at very high price worth $1,087500 and also

fulfils all the requirements. It is located in the area which covers the local shops, cafes, close

to transport facilities and fireplaces. (Li, Bao, Sellis, Yan & Zhang, 2018). The house is six

bedroom semi-detached bungalow which offer beautiful private gardens, 3 garage spaces, a

balcony, and I ground swimming pool and secure parking facility. A bungalow style house

offers great facilities apart from the mentioned above include alarm and floorboards

(Onthemarket.com. 2018).

Income level of an architect

Architects are been known for designing and creating new houses and building. In

different cities of world they are been paid differently (Akimov & Stevenson, 2017). Talking

about Sydney, the average income of a design architect is $62,457 per year. The skills which

make a person to get highly paid for his profile are Arch CAD, GRAPHISOFT, Project

management and many more. While, in Hobart architects are paid $92,939 per year. This is

almost 1.6 times more than the median wage of the country. However, the tax charges on

income level amounted to $23,878.07 which makes the net income of $69,060.57. In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business finance 10

Newcastle, the average income level of an architect is $107,500. In April, 2018 the income

level roses by $7,635 that is 25% increase was there.

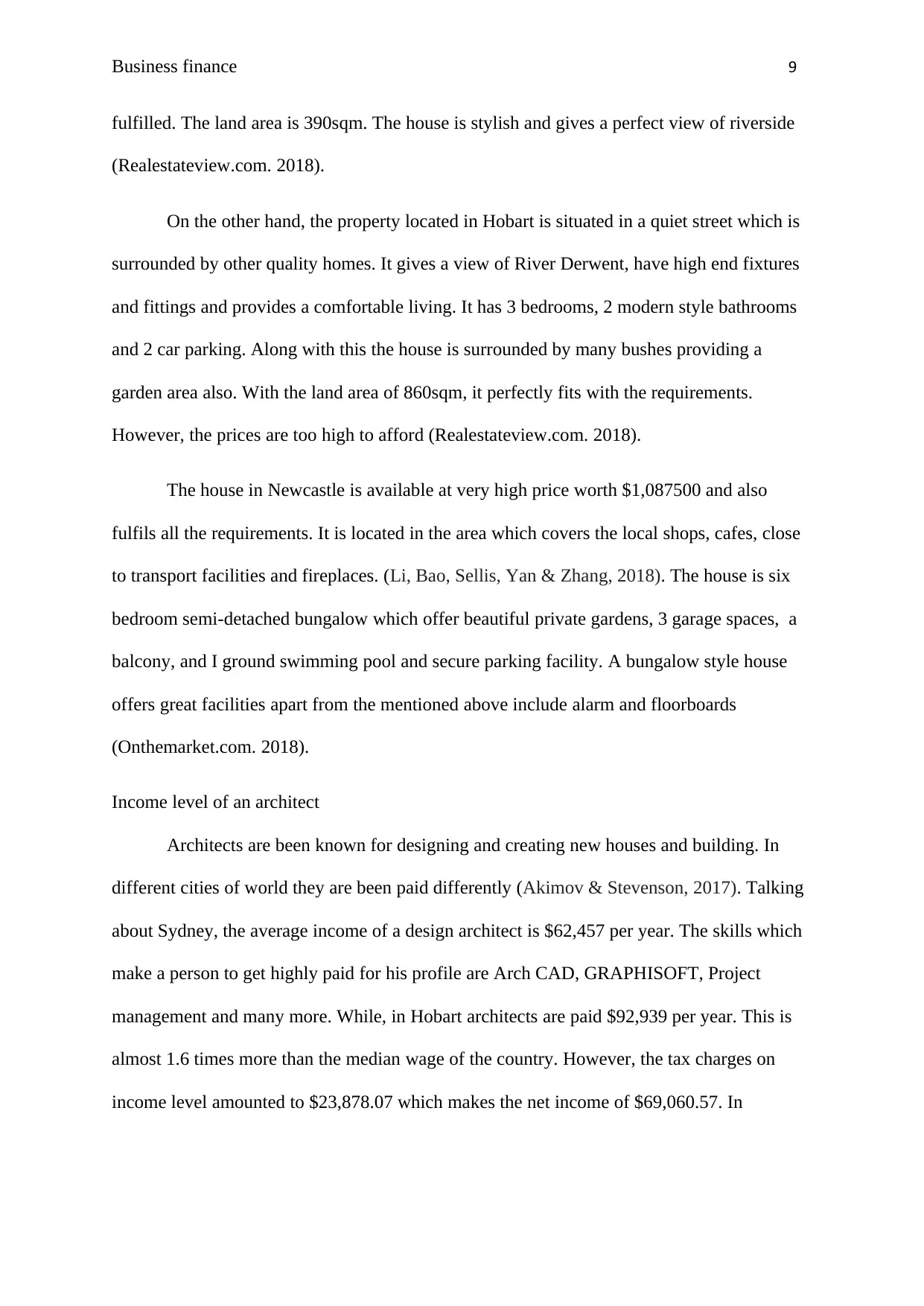

The house price to income level ratio

Sydney Hobart Newcastle

House prices 749,950 840,000 1087500

Average income level 62,457 23,878.07 107,500

House price to average income

level 12.01 35.18 10.12

Sydney Hobart Newcastle

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

House price to average income level

House price to average income level

(Source: By Author)

Part 3

How mortgages work

The mortgage market is very well developed in Australia and there is a huge choice of

mortgage providers and products. A sound knowledge of mortgage is useful in determining

about the different types of mortgages. As an expert there are wide varieties to access the

Newcastle, the average income level of an architect is $107,500. In April, 2018 the income

level roses by $7,635 that is 25% increase was there.

The house price to income level ratio

Sydney Hobart Newcastle

House prices 749,950 840,000 1087500

Average income level 62,457 23,878.07 107,500

House price to average income

level 12.01 35.18 10.12

Sydney Hobart Newcastle

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

House price to average income level

House price to average income level

(Source: By Author)

Part 3

How mortgages work

The mortgage market is very well developed in Australia and there is a huge choice of

mortgage providers and products. A sound knowledge of mortgage is useful in determining

about the different types of mortgages. As an expert there are wide varieties to access the

Business finance 11

options. The first decision shall be the decision about the rates whether the selection shall be

the variable and fixed rate. Fixed rate mortgages are associated with the same interest rate

will be applicable for the duration of the agreement (Blöchliger, Égert, Alvarez & Paciorek,

2015). They are applicable usually for few years. Variable rate mortgages however can

fluctuate according to the variability of cost. They typically track the standard variable rate

which is decided by the bank, or the central bank rates. Another option for the first buyers

can be is the hybrid options which contain the discounted variable rate, before moving on to

the bank’s standard variable rate. This is sold as a honeymoon offer, especially for new

customers but might end up costing more than what is expected as the standard variable rate

is not necessary the best reliable rate available for the customers.

There are also certain types of products which are available only to the buyers in

specific situations (Wilson, 2015). This is also known as the professional package under

which the services are revolving around the concept of the home loans which is made

available to the professional buyers which are made variable for professional buyers.

Applying for home loans requires some conditions which are discussed as follows.

The personal information includes the fulltime employment history, current and

previous addresses, details of the current assets are required to put up collateral security such

as car, bike or other properties and most importantly the proof of your income and current

outgoing expenses (Robertson & Rogers, 2017).

Current records of the salary, latest return of the tax and notices if nay for the purpose

of assessment, copies of the recent credit card statements are required which confirms the

credit limits. The last six months bank statements. Also the stamp duty and lender’s mortgage

insurance is reviewed.

options. The first decision shall be the decision about the rates whether the selection shall be

the variable and fixed rate. Fixed rate mortgages are associated with the same interest rate

will be applicable for the duration of the agreement (Blöchliger, Égert, Alvarez & Paciorek,

2015). They are applicable usually for few years. Variable rate mortgages however can

fluctuate according to the variability of cost. They typically track the standard variable rate

which is decided by the bank, or the central bank rates. Another option for the first buyers

can be is the hybrid options which contain the discounted variable rate, before moving on to

the bank’s standard variable rate. This is sold as a honeymoon offer, especially for new

customers but might end up costing more than what is expected as the standard variable rate

is not necessary the best reliable rate available for the customers.

There are also certain types of products which are available only to the buyers in

specific situations (Wilson, 2015). This is also known as the professional package under

which the services are revolving around the concept of the home loans which is made

available to the professional buyers which are made variable for professional buyers.

Applying for home loans requires some conditions which are discussed as follows.

The personal information includes the fulltime employment history, current and

previous addresses, details of the current assets are required to put up collateral security such

as car, bike or other properties and most importantly the proof of your income and current

outgoing expenses (Robertson & Rogers, 2017).

Current records of the salary, latest return of the tax and notices if nay for the purpose

of assessment, copies of the recent credit card statements are required which confirms the

credit limits. The last six months bank statements. Also the stamp duty and lender’s mortgage

insurance is reviewed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.