ACC00152 Business Finance: NPV Analysis of Investment Options for SSF

VerifiedAdded on 2023/06/14

|5

|934

|406

Report

AI Summary

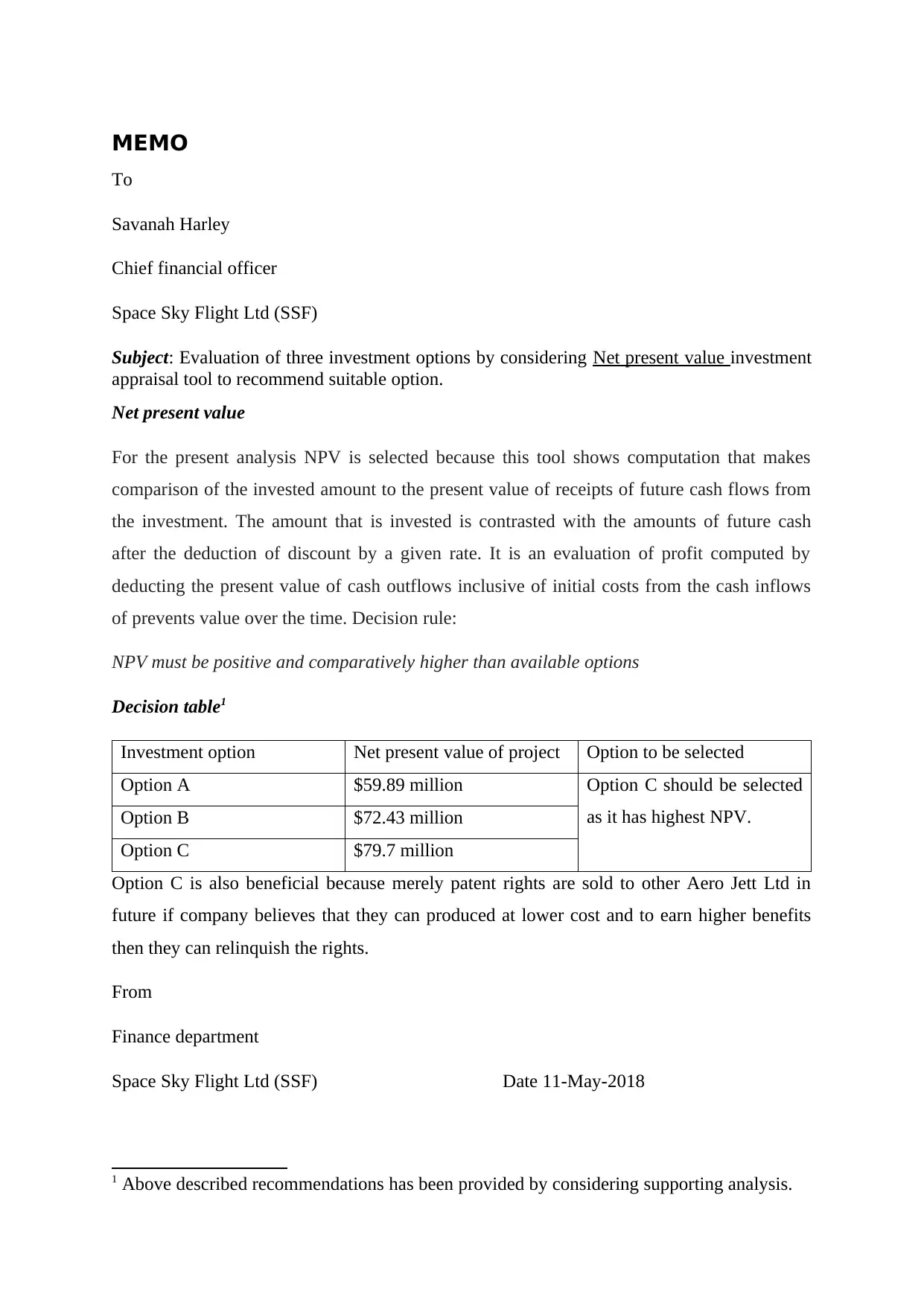

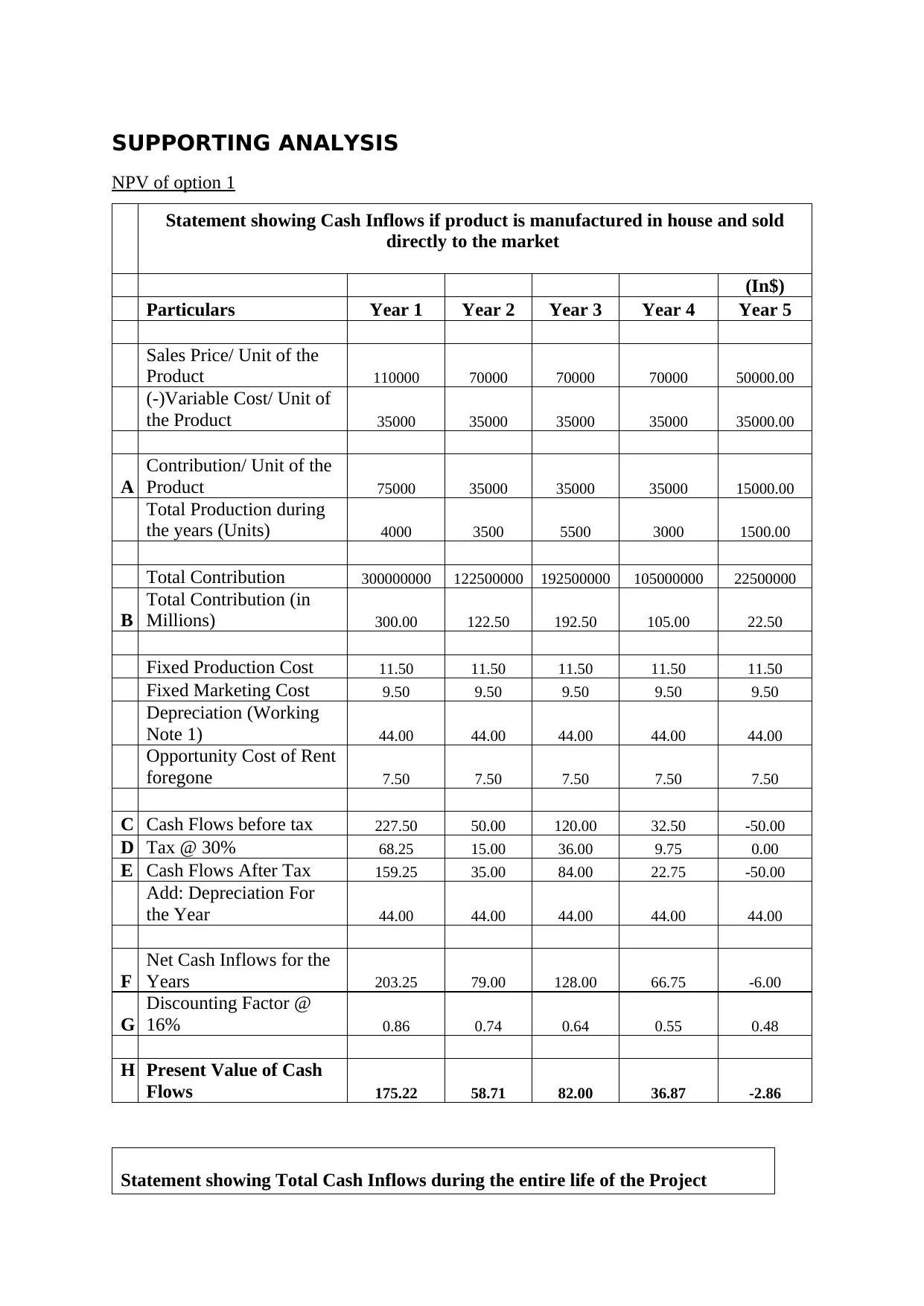

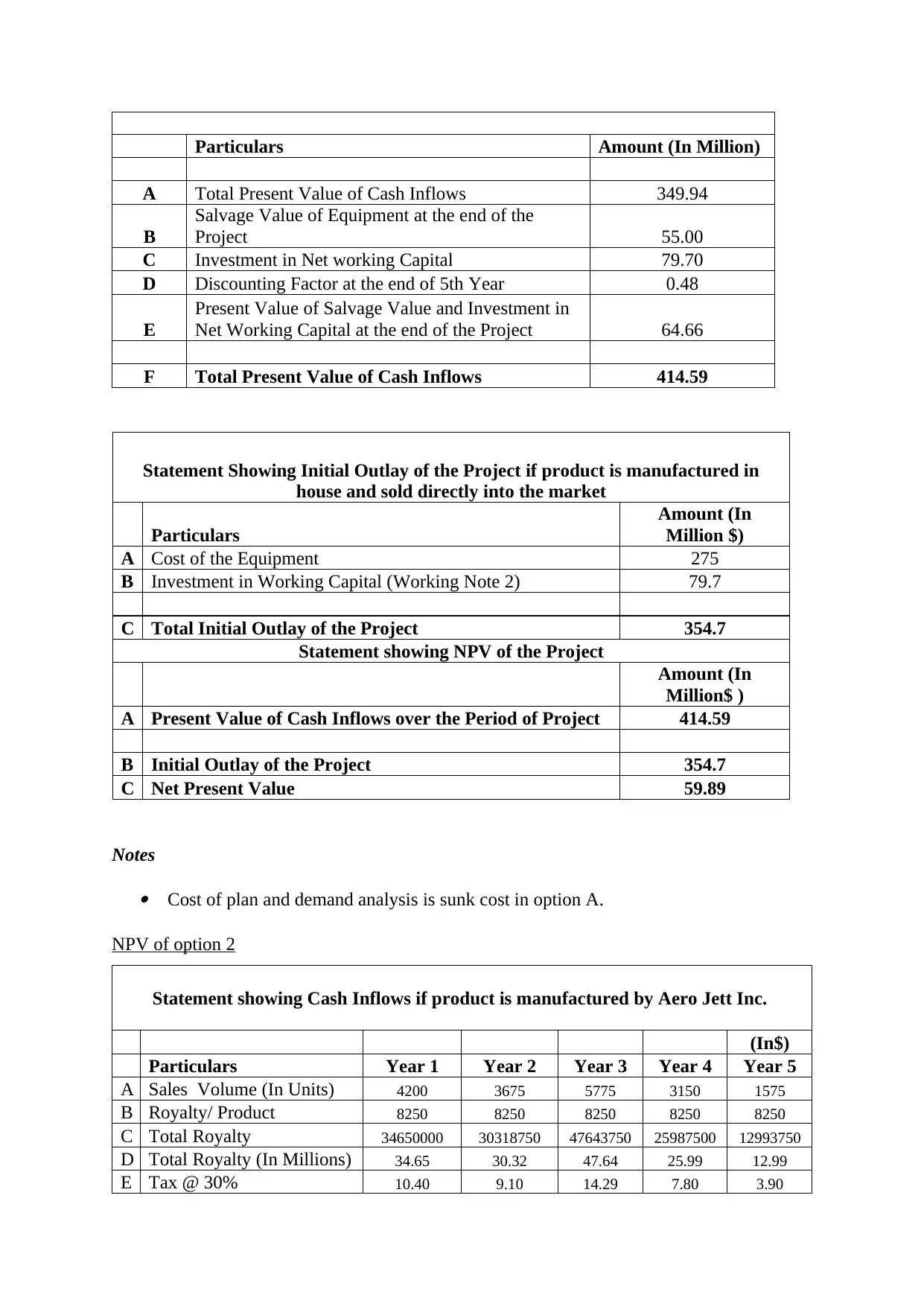

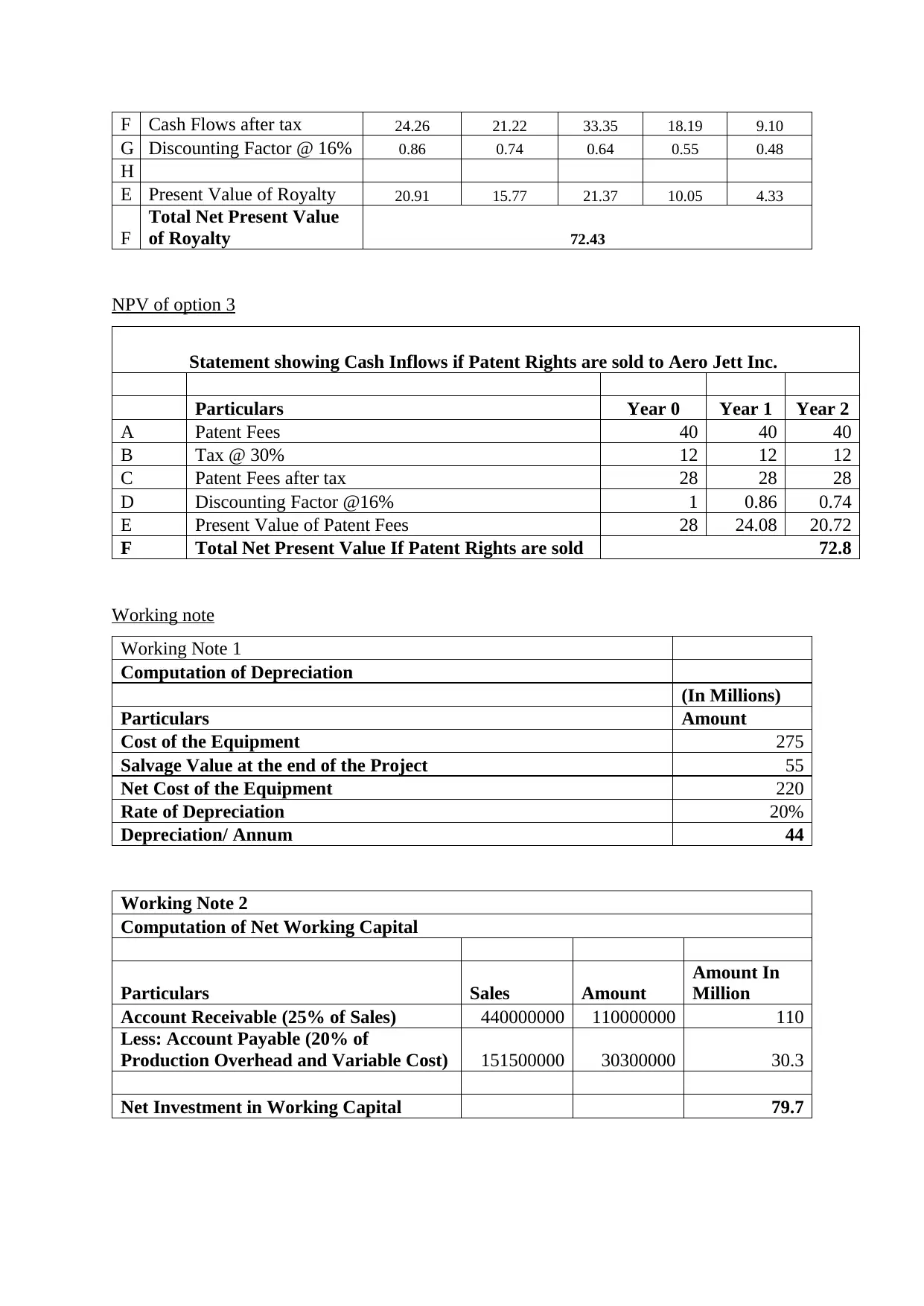

This report provides an evaluation of three investment options for Space Sky Flight Ltd (SSF) using Net Present Value (NPV) analysis. The CFO, Savanah Harley, requested an analysis to determine the best approach for bringing a newly developed drone to market: manufacturing in-house, licensing to another company, or selling patent rights. The analysis includes detailed cash flow projections, discounting factors, and NPV calculations for each option. Option C, selling patent rights to Aero Jett Inc., is identified as the most financially beneficial, with the highest NPV of $79.7 million, compared to option A's $59.89 million and option B's $72.43 million. The report recommends further analysis and consideration of additional factors before making a final decision, emphasizing that SSF can relinquish the rights if they can produce at a lower cost and earn higher benefits. Desklib provides access to similar solved assignments and resources for students.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.