Investment Decisions, Performance Indicators and Pricing Strategies

VerifiedAdded on 2023/06/18

|16

|2511

|203

Report

AI Summary

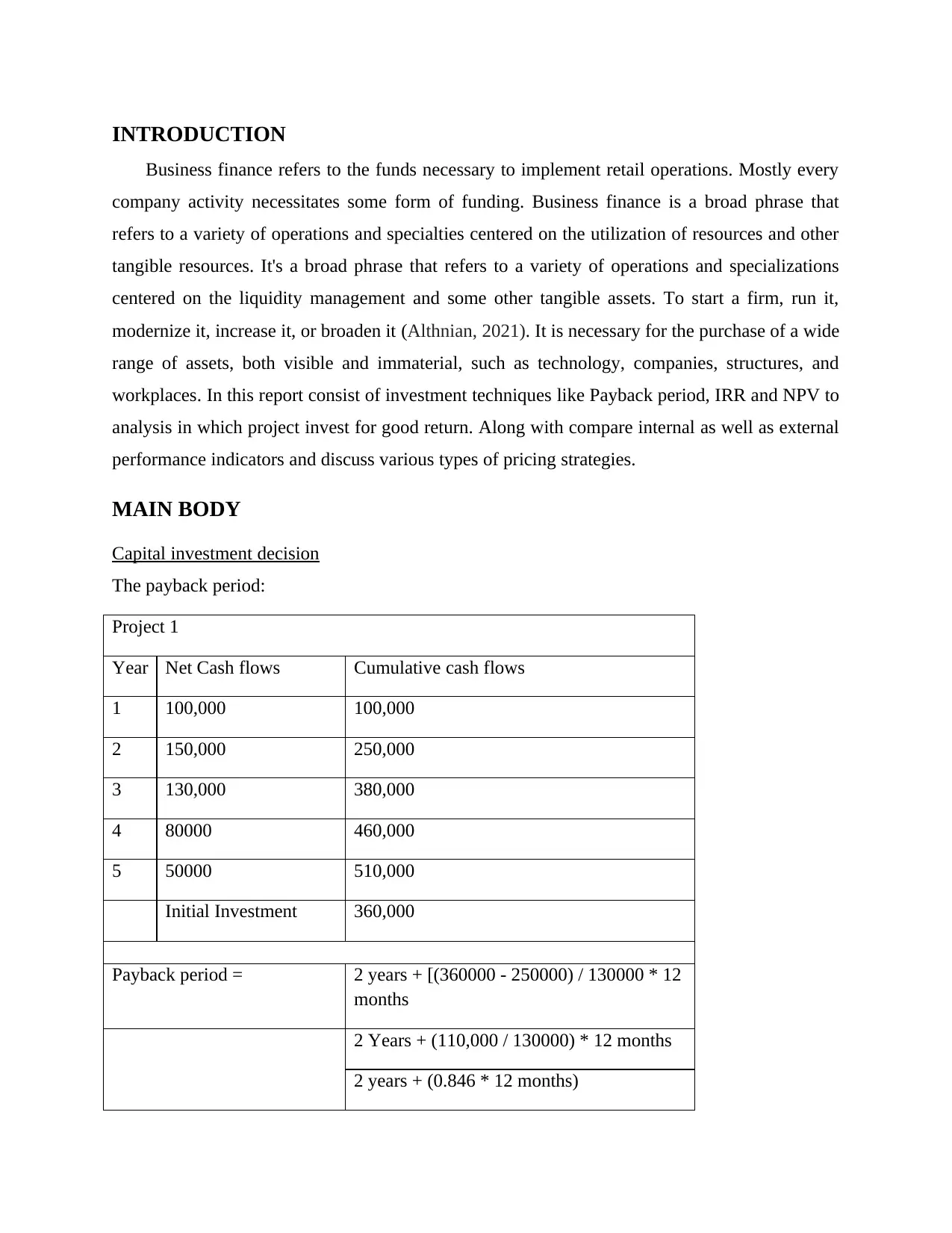

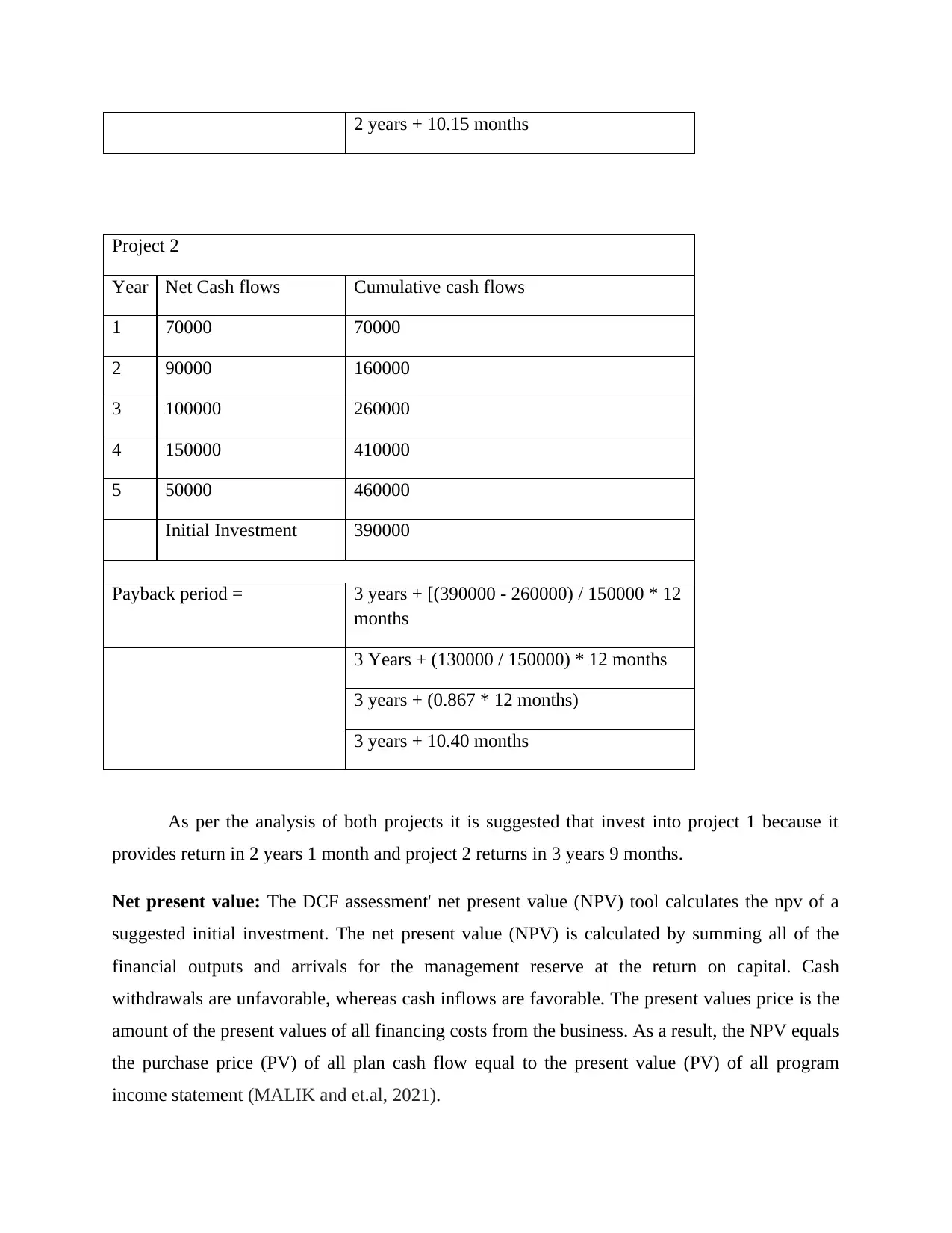

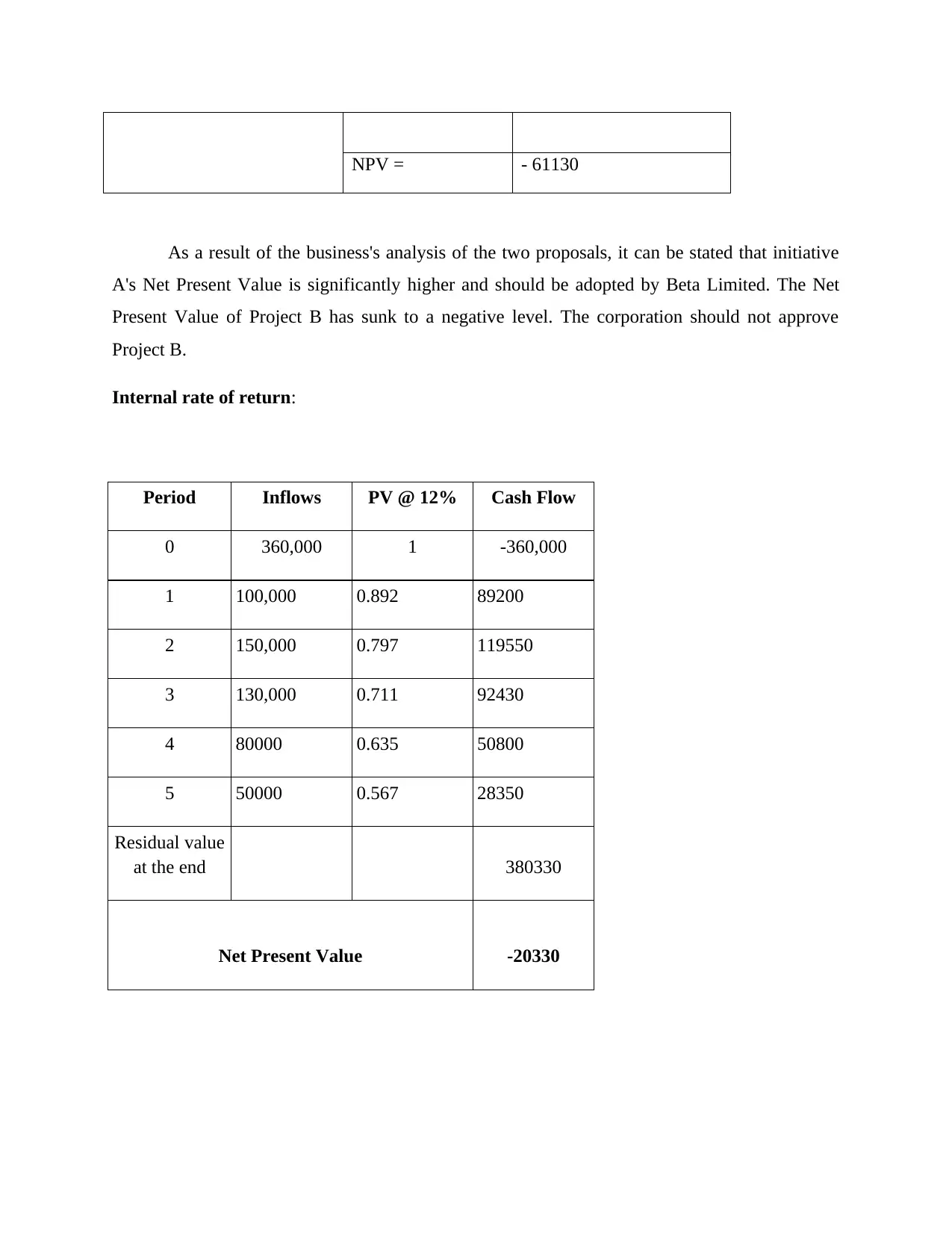

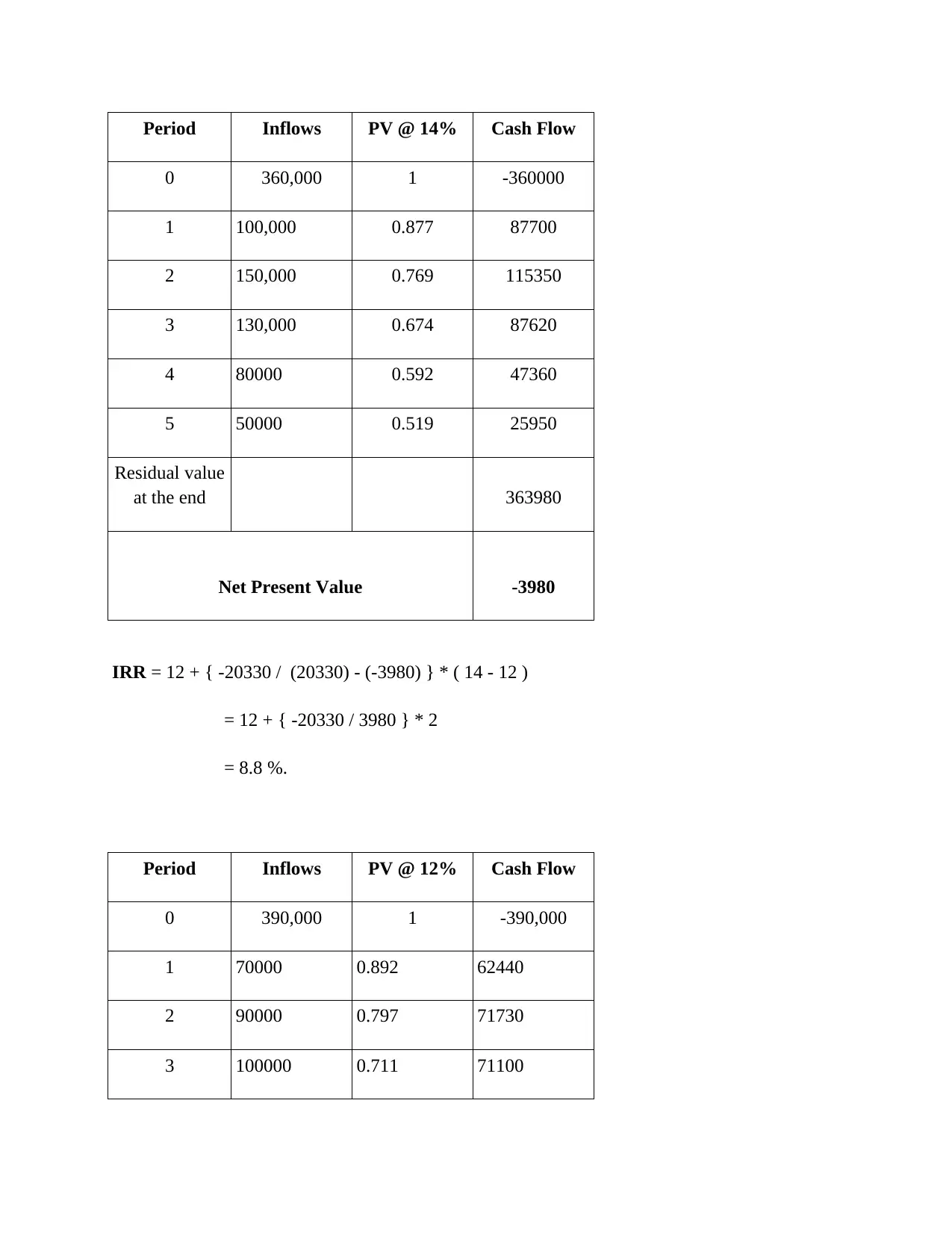

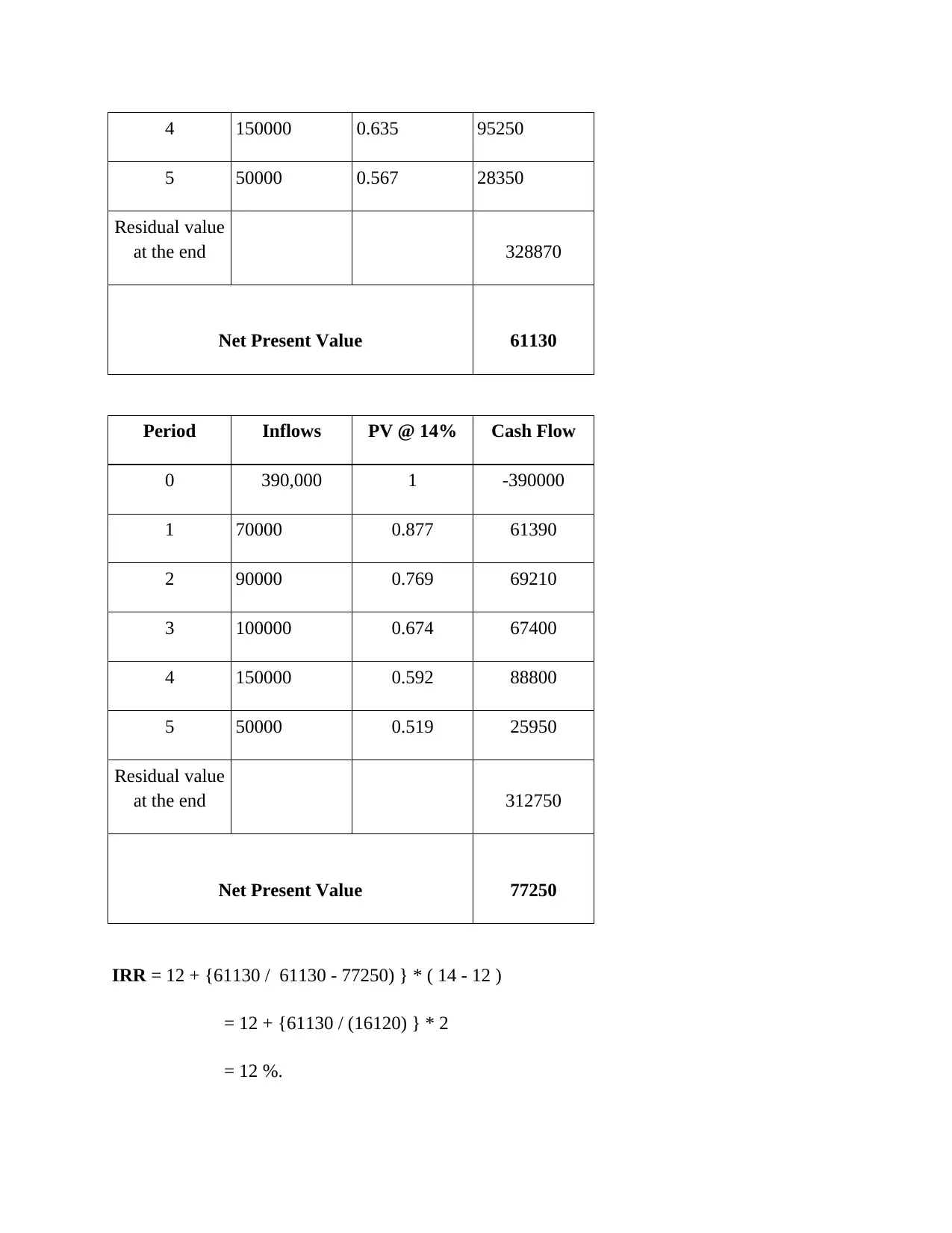

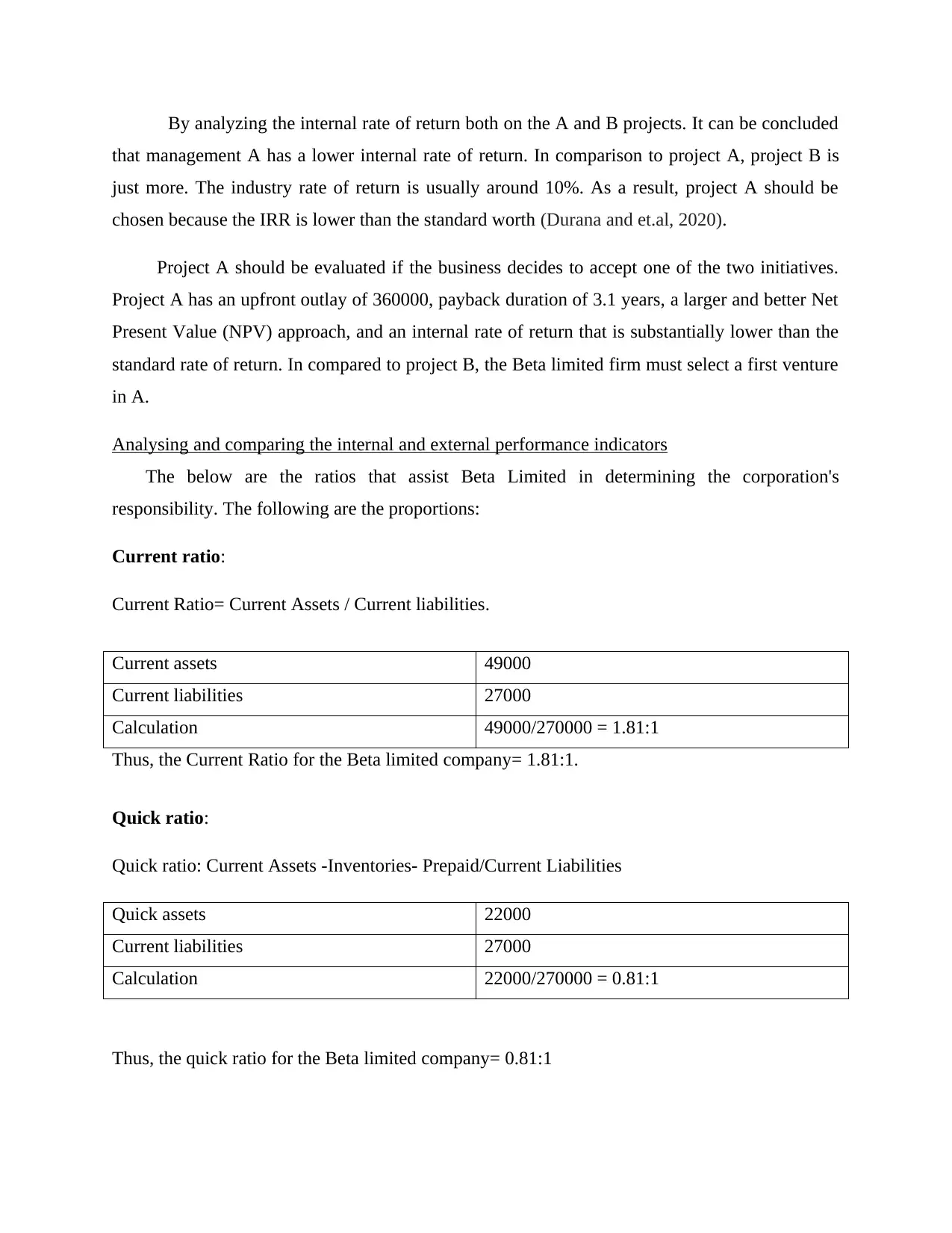

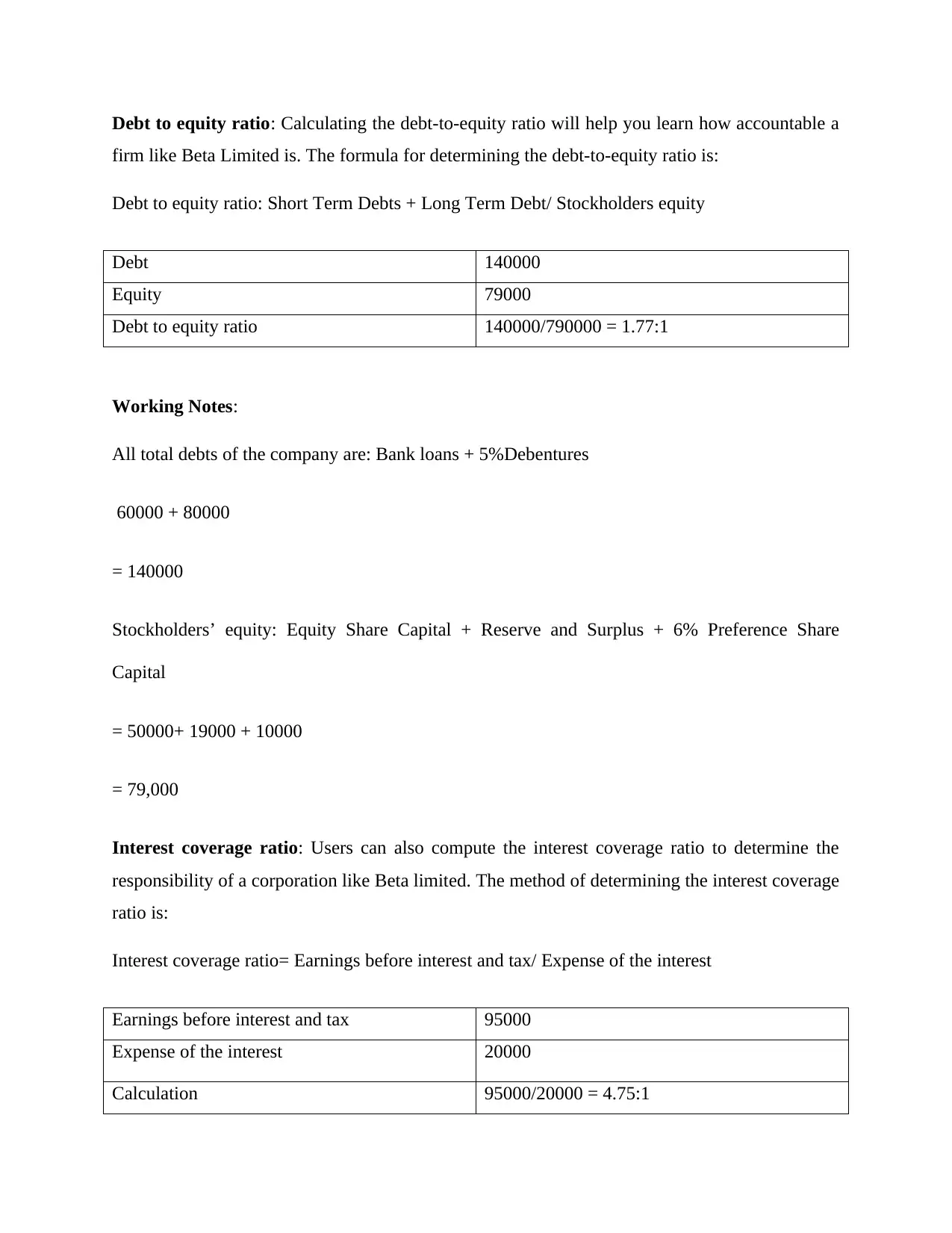

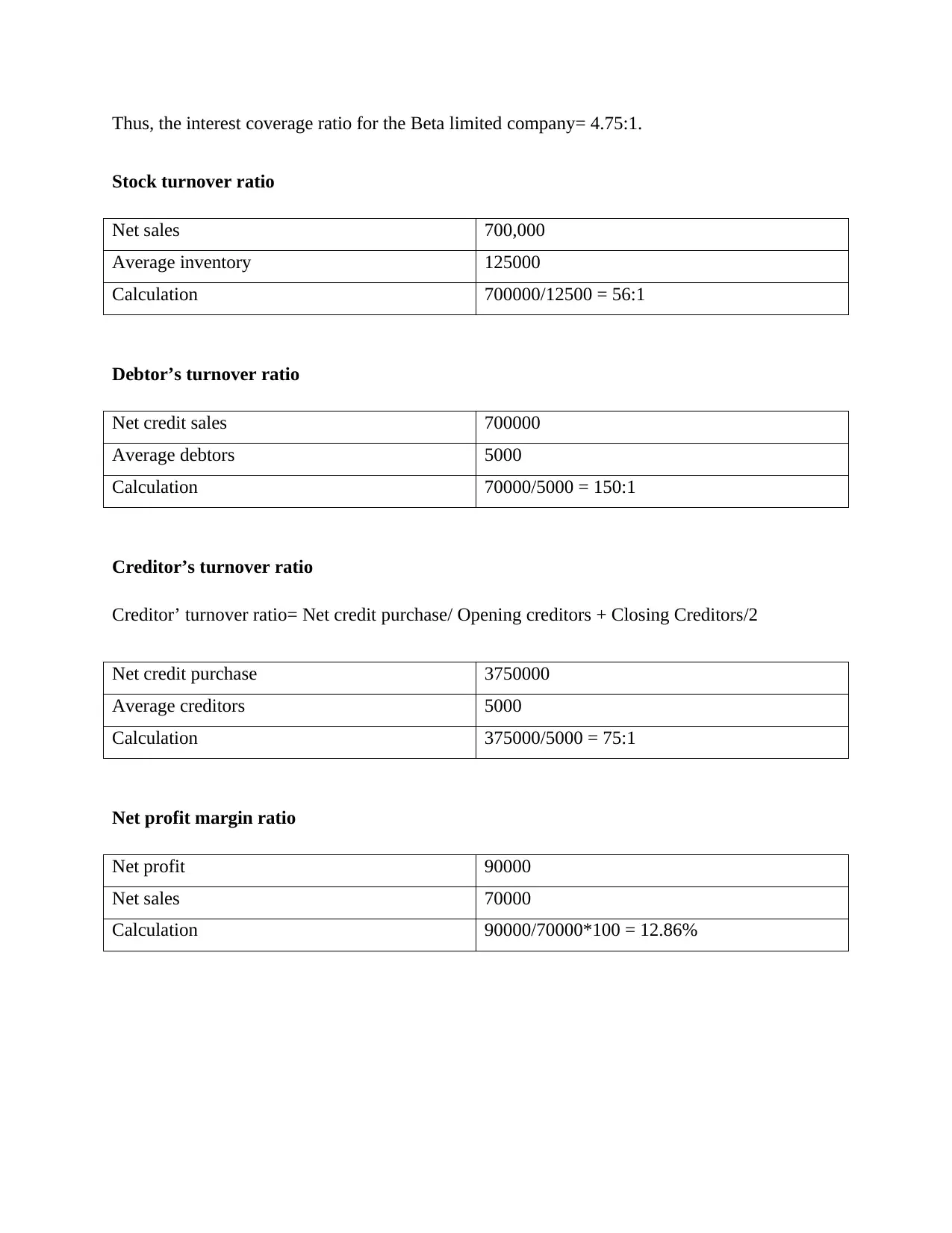

This report provides a comprehensive analysis of business finance, focusing on capital investment decisions and performance indicators. It begins by evaluating investment opportunities using methods such as the payback period, net present value (NPV), and internal rate of return (IRR) to determine the most profitable project for Beta Limited, recommending Project A based on its superior NPV and IRR. The report then delves into analyzing and comparing internal and external performance indicators through financial ratios like current ratio, quick ratio, debt-to-equity ratio, and interest coverage ratio, assessing Beta Limited's financial health and operational efficiency. External factors influencing Beta Limited's performance, such as credit facility and target audience, are also discussed alongside internal factors like resources and capabilities. Finally, the report explores different pricing strategies, including cost-plus pricing, value pricing, and penetration pricing, providing a holistic view of financial decision-making in a business context.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.