Business Finance Individual Assignment: Tesla Deal Financial Analysis

VerifiedAdded on 2022/11/24

|10

|1590

|229

Report

AI Summary

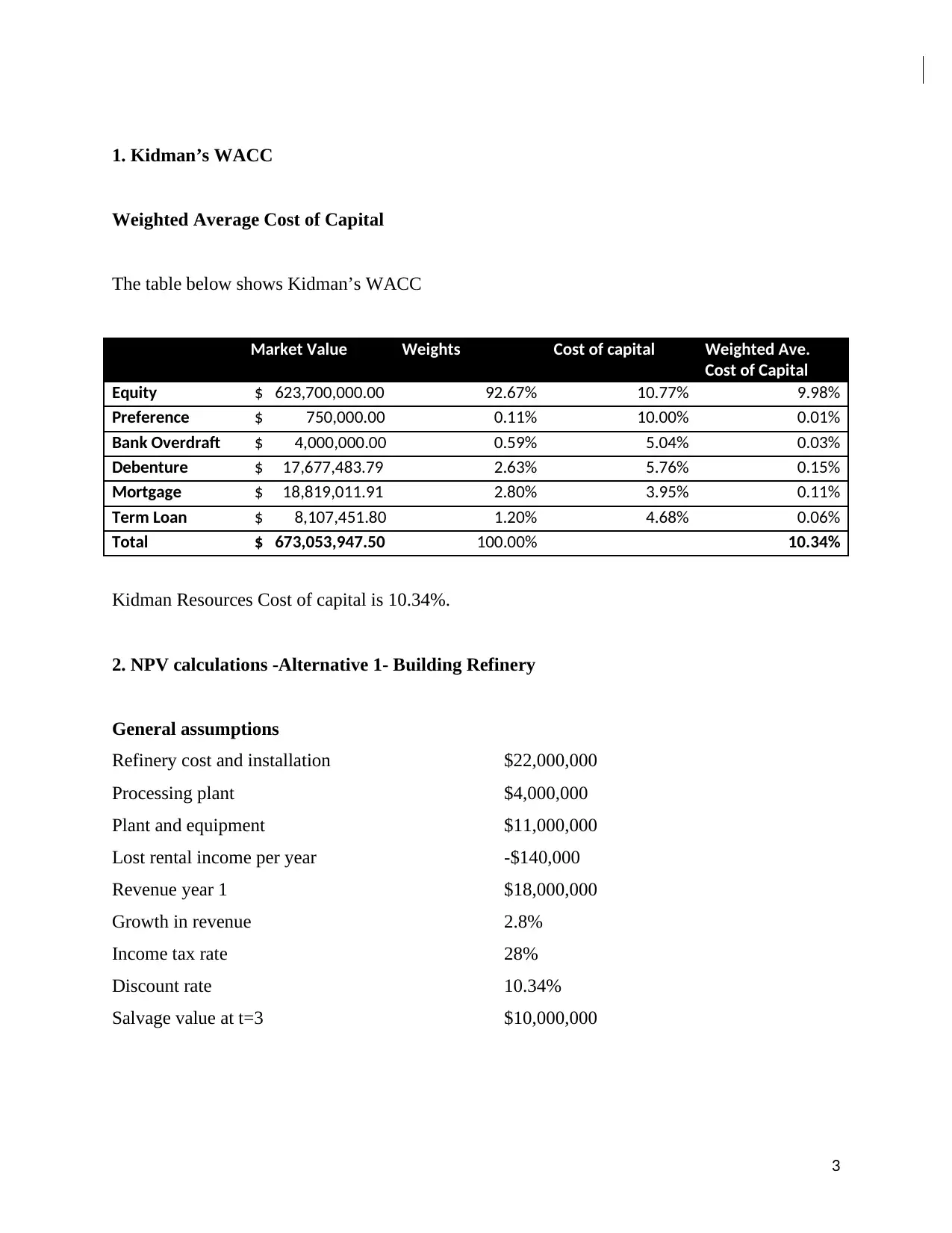

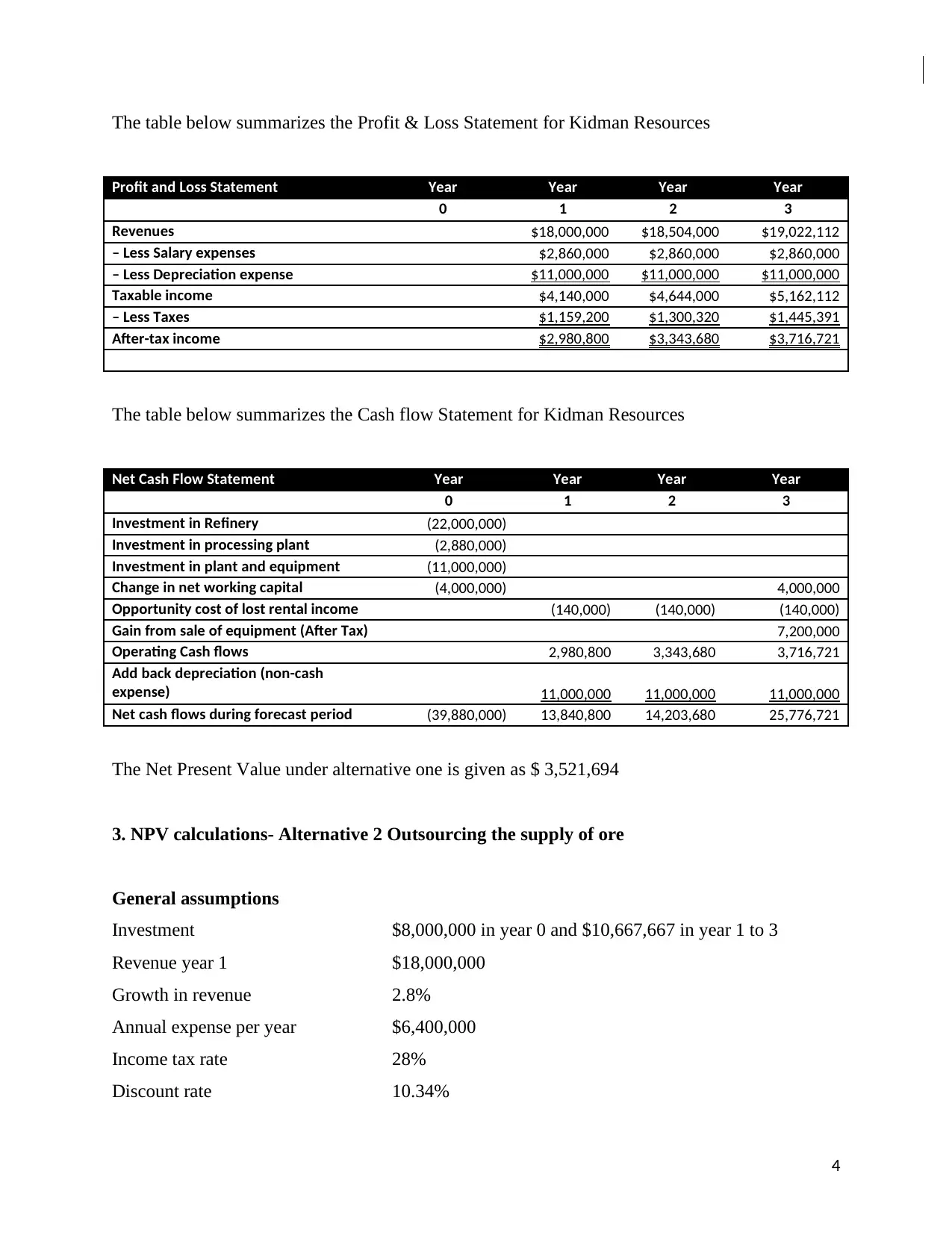

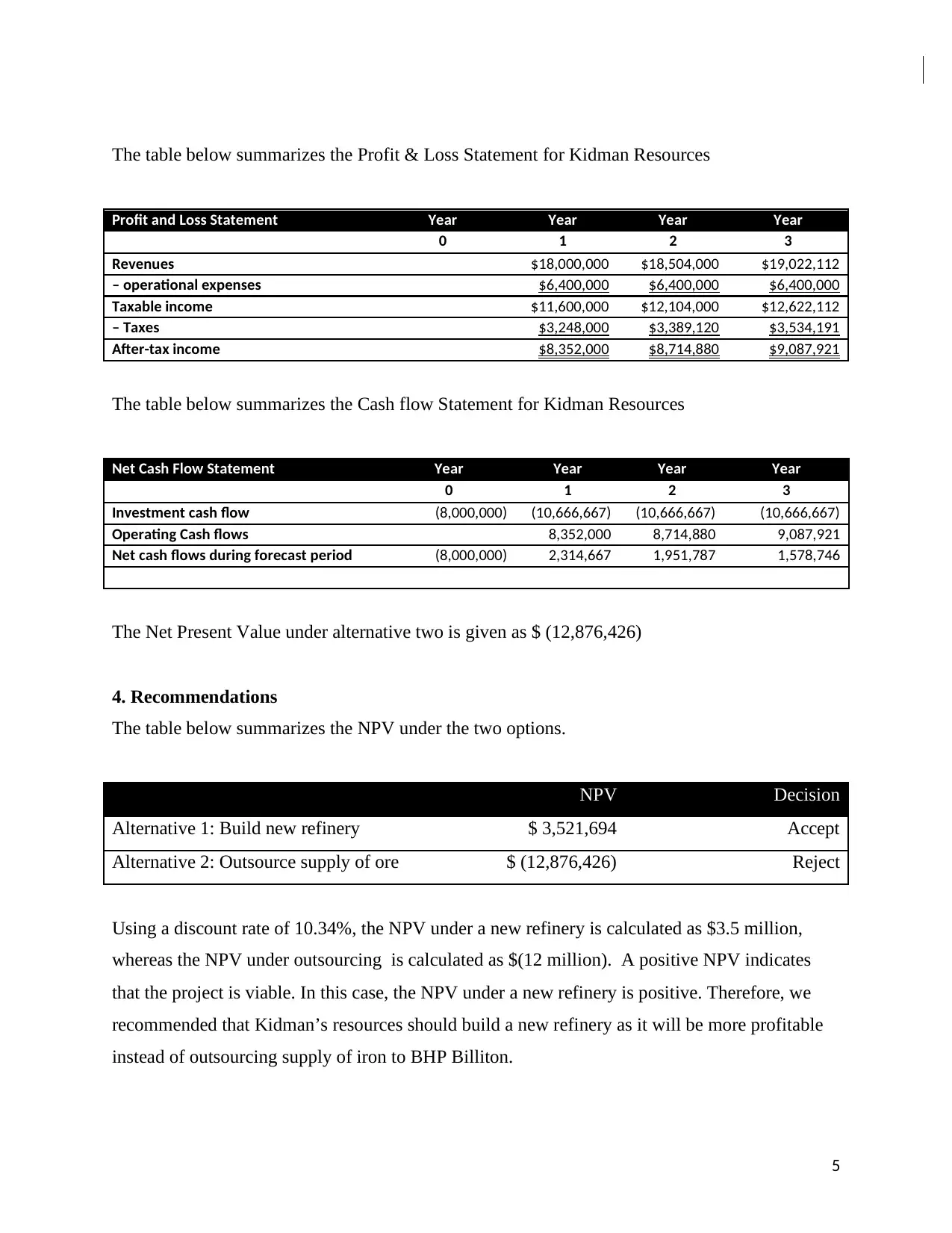

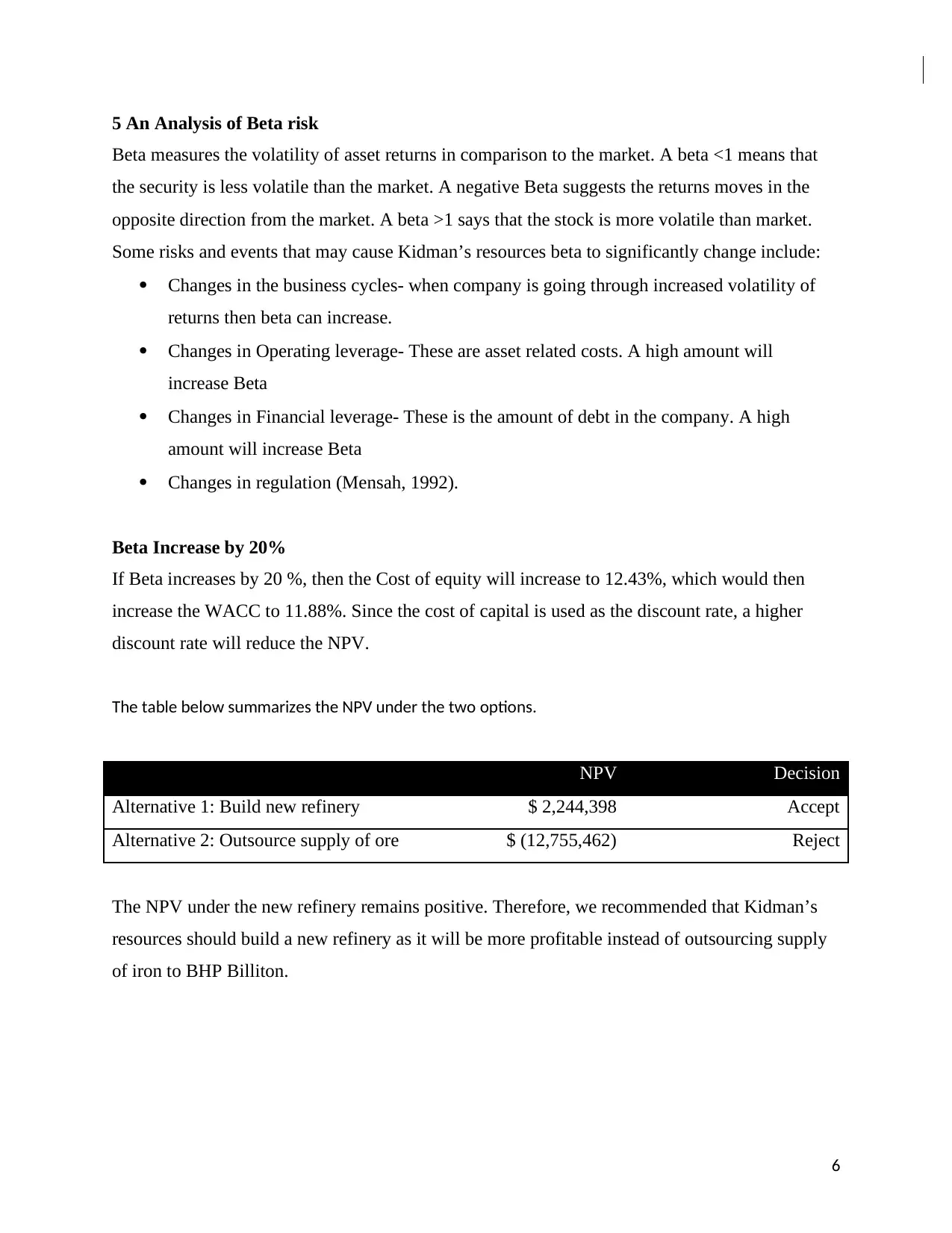

This assignment analyzes the financial decisions facing Kidman Resources regarding a deal to supply Tesla with lithium hydroxide. The core of the analysis involves evaluating two options: building a new refinery or outsourcing the supply of ore. The report calculates the Weighted Average Cost of Capital (WACC) for Kidman Resources and uses Net Present Value (NPV) to assess the profitability of each option. The analysis includes detailed financial statements, including profit and loss and cash flow statements, for both scenarios. Recommendations are made based on the NPV calculations, considering the potential impact of beta risk on the project's viability. The assignment demonstrates the application of financial principles to real-world business decisions, offering insights into investment appraisal and risk management.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.