Business Finance Report: MDL Company's Working Capital and Budgeting

VerifiedAdded on 2023/01/12

|14

|3336

|53

Report

AI Summary

This report analyzes the financial performance of MDL, a company with 30 delicatessens in the South of England, focusing on working capital management, cash flow, and budgeting. Part 1 defines cash flow, profit, working capital, receivables, inventory, and payables, detailing their interrelationships and impact on cash flow. It applies these concepts to MDL, highlighting issues with debtor payments and inventory turnover. Recommendations are made to improve cash flow and working capital, including credit policy adjustments and inventory management. Part 2 examines budgeting, outlining its purpose and types, including traditional and alternative methods like zero-based and activity-based budgeting. The report recommends activity-based budgeting for Second Sight Plc to enhance cost assessment and financial planning. The report emphasizes the importance of these financial strategies for improving business outcomes.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART 1.......................................................................................................................................3

Executive summary................................................................................................................3

1..............................................................................................................................................3

Stating the meaning of cash flow and profit along with differences......................................3

Presenting the meaning of working capital, receivables, inventory and payables.................3

Stating how changes in working capital impacts cash flow...................................................4

2. Applying the concepts of working capital to the company for showing how it affects

company’s results...................................................................................................................4

3. Recommending steps to the firm that need to be taken for improving cash flow and

thereby working capital..........................................................................................................4

PART 2.......................................................................................................................................5

Executive summary................................................................................................................5

1. Stating purpose and types of budgeting.............................................................................6

2. Demonstrating the application of traditional and alternative budgeting methods.............9

3. Analyzing budgeting system which is appropriate for business from future perspective..9

REFERENCES.........................................................................................................................11

PART 1.......................................................................................................................................3

Executive summary................................................................................................................3

1..............................................................................................................................................3

Stating the meaning of cash flow and profit along with differences......................................3

Presenting the meaning of working capital, receivables, inventory and payables.................3

Stating how changes in working capital impacts cash flow...................................................4

2. Applying the concepts of working capital to the company for showing how it affects

company’s results...................................................................................................................4

3. Recommending steps to the firm that need to be taken for improving cash flow and

thereby working capital..........................................................................................................4

PART 2.......................................................................................................................................5

Executive summary................................................................................................................5

1. Stating purpose and types of budgeting.............................................................................6

2. Demonstrating the application of traditional and alternative budgeting methods.............9

3. Analyzing budgeting system which is appropriate for business from future perspective..9

REFERENCES.........................................................................................................................11

PART 1

Executive summary

In the current times, it is highly required for the business units to make optimum

utilization of funds that contributes in the attainment of goals. This part of the assignment is

based on MDL which owns 30 delicatessens in South of England. It can be summarized from

the evaluation that manager of MDL is required to make modifications in the existing

strategic and policy framework. By this, company would become able to improve both

working capital, cash-flows and thereby profitability as well.

1.

Stating the meaning of cash flow and profit along with differences

Cash flow: It implies for the inflow and outflow that associated with business

operations pertaining to specific time frame. Cash flow presents money that business entity

has at any given time for business activities. This element of financial management presents

the extent to which liquid assets of the firm are increased.

Profit: This means return that company has generated through selling products or

services. Profitability may be served as an indicator which reflects surplus after subtracting

all the expenditure from the revenue generated.

Difference between cash flow and profit is enumerated below:

Basis of difference Cash flow Profit

Meaning It implies for the money that

flows in and out with regards

to specific time period.

Profitability accounts for the

money or amount that

remains after deducting all

the expenditure.

Measurement Under cash flow, valuation is

being done by taking into

account inventory,

receivables and payment

It is measured or calculated

by deducting al the

expenditures from revenue.

Executive summary

In the current times, it is highly required for the business units to make optimum

utilization of funds that contributes in the attainment of goals. This part of the assignment is

based on MDL which owns 30 delicatessens in South of England. It can be summarized from

the evaluation that manager of MDL is required to make modifications in the existing

strategic and policy framework. By this, company would become able to improve both

working capital, cash-flows and thereby profitability as well.

1.

Stating the meaning of cash flow and profit along with differences

Cash flow: It implies for the inflow and outflow that associated with business

operations pertaining to specific time frame. Cash flow presents money that business entity

has at any given time for business activities. This element of financial management presents

the extent to which liquid assets of the firm are increased.

Profit: This means return that company has generated through selling products or

services. Profitability may be served as an indicator which reflects surplus after subtracting

all the expenditure from the revenue generated.

Difference between cash flow and profit is enumerated below:

Basis of difference Cash flow Profit

Meaning It implies for the money that

flows in and out with regards

to specific time period.

Profitability accounts for the

money or amount that

remains after deducting all

the expenditure.

Measurement Under cash flow, valuation is

being done by taking into

account inventory,

receivables and payment

It is measured or calculated

by deducting al the

expenditures from revenue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

period.

Time period Cash flow provides

information about company’s

success or failure in long run

(The Critical Differences

between Cash Flow and

Profit, 2020).

Unlike cash flows, in the

case of profit success can be

identified and evaluated

within short time frame.

Nature Cash flows can be increased

or bought through the means

of long term borrowings.

However, in this, profit can

be generated through the

means of only sound

strategic framework, policies

and effectual cash

management.

Sales Here, revenue is recognized

when debtors clear their

dues.

It recognized through the

means of invoices.

Taxation In this, tax is paid in terms of

installments.

Tax is calculated by taking

into account profit generated

during the period.

Fixed assets Recorded in statement at the

time of purchase which in

turn results into decrease in

cash flow.

In this, with regards to fixed

assets, profitability decreases

due to the inclusion of

depreciation charged on the

basis of it.

Presenting the meaning of working capital, receivables, inventory and payables

Working capital: It may be served as a measure which entails the current to which

company’s liquidity position is good. In other words, working capital serves information

about company’s ability in relation to managing daily operations. In order to avoid

Time period Cash flow provides

information about company’s

success or failure in long run

(The Critical Differences

between Cash Flow and

Profit, 2020).

Unlike cash flows, in the

case of profit success can be

identified and evaluated

within short time frame.

Nature Cash flows can be increased

or bought through the means

of long term borrowings.

However, in this, profit can

be generated through the

means of only sound

strategic framework, policies

and effectual cash

management.

Sales Here, revenue is recognized

when debtors clear their

dues.

It recognized through the

means of invoices.

Taxation In this, tax is paid in terms of

installments.

Tax is calculated by taking

into account profit generated

during the period.

Fixed assets Recorded in statement at the

time of purchase which in

turn results into decrease in

cash flow.

In this, with regards to fixed

assets, profitability decreases

due to the inclusion of

depreciation charged on the

basis of it.

Presenting the meaning of working capital, receivables, inventory and payables

Working capital: It may be served as a measure which entails the current to which

company’s liquidity position is good. In other words, working capital serves information

about company’s ability in relation to managing daily operations. In order to avoid

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

undesirable conditions business unit must maintain enough cash flows for meeting short-term

cost and debt obligations (Obradovich, 2019).

Inventory: Stock may be served as a main asset of an organization that need to

converted into sales or cash for ensuring enough working capital. Period within which

company sells and replenishes its stock assists in identifying its success level.

Receivables: This includes money that customers owe due to previous credit sales. In

the case of receivables business unit needs to make focus on collecting money timely so that

it can be used for other productive activities (Gupta and Gupta, 2019).

Payables: It is one of the main component or elements of working capital which

includes money that must pay to suppliers over short term. Thus, firm should focus on

maintaining enough receivables in line with short term obligations.

Stating how changes in working capital impacts cash flow

From research, it has assessed that changes that take place in working capital has

significant impact on company’s cash flow. Moreover, high working capital shows that

management team is focusing on investing money for short term (Sultan and Murtaza, 2019).

This means company is relying on draining cash flow available from operating, financing and

investing activities. On the other side, working capital of the firm decreases when

management takes resort of short-term borrowings for financing operations. In this case, cash

flow of the firm increases and vice versa.

2. Applying the concepts of working capital to the company for showing how it affects

company’s results

By evaluating case scenario it has identified that MDL is facing difficulty pertaining

to two aspects mainly. This includes default made by debtors and lower stock conversion

rate. Given case scenario entails that firm is reluctant in relation to pushing its customers fall

under the category of doing less frequent payment. Now, due to dispute firm is facing issue in

getting stock on time. In this, firm will take more time for converting stock into cash within

appropriate time frame. This will place direct impact on company’s cash flow and overall

results. Moreover, insufficient stock level may result into loss of customer base and thereby

sales as well as profitability. Along with this, Company is facing issues in getting funds from

debtors on time. Due to this, MDL failed to maintain enough current assets in against to the

obligations. This in turn creates obstacles in performing daily activities or funding day to day

cost and debt obligations (Obradovich, 2019).

Inventory: Stock may be served as a main asset of an organization that need to

converted into sales or cash for ensuring enough working capital. Period within which

company sells and replenishes its stock assists in identifying its success level.

Receivables: This includes money that customers owe due to previous credit sales. In

the case of receivables business unit needs to make focus on collecting money timely so that

it can be used for other productive activities (Gupta and Gupta, 2019).

Payables: It is one of the main component or elements of working capital which

includes money that must pay to suppliers over short term. Thus, firm should focus on

maintaining enough receivables in line with short term obligations.

Stating how changes in working capital impacts cash flow

From research, it has assessed that changes that take place in working capital has

significant impact on company’s cash flow. Moreover, high working capital shows that

management team is focusing on investing money for short term (Sultan and Murtaza, 2019).

This means company is relying on draining cash flow available from operating, financing and

investing activities. On the other side, working capital of the firm decreases when

management takes resort of short-term borrowings for financing operations. In this case, cash

flow of the firm increases and vice versa.

2. Applying the concepts of working capital to the company for showing how it affects

company’s results

By evaluating case scenario it has identified that MDL is facing difficulty pertaining

to two aspects mainly. This includes default made by debtors and lower stock conversion

rate. Given case scenario entails that firm is reluctant in relation to pushing its customers fall

under the category of doing less frequent payment. Now, due to dispute firm is facing issue in

getting stock on time. In this, firm will take more time for converting stock into cash within

appropriate time frame. This will place direct impact on company’s cash flow and overall

results. Moreover, insufficient stock level may result into loss of customer base and thereby

sales as well as profitability. Along with this, Company is facing issues in getting funds from

debtors on time. Due to this, MDL failed to maintain enough current assets in against to the

obligations. This in turn creates obstacles in performing daily activities or funding day to day

operation which closely impacts organizational cash flows. Hence, for improving results

business unit is required to take suitable measures regarding working capital and cash flow

management.

3. Recommending steps to the firm that need to be taken for improving cash flow and thereby

working capital

Budgeting refers to the process that helps in creating plan for spending money and

balancing income level. Cited case situation presents that MDL is facing issues in receiving

amount from debtors. There are several customers who are making default in paying funds

that owed to them. This situation is placing direct impact on company’s working capital and

cash flow position. For business management, in the context of MDL, working capital is

considered as the most essential aspect that needed to carry out daily operations prominently.

In this regard, manager of MDL is required to take significant measure for enhancing both

working capital and thereby cash flow as well.

For reducing debt level and improving receivable period manager of MDL should

make focus on evaluating credit rating of debtors. By doing this, company can

identify customers who do not make payment on time. In this way, such measure

helps in improving receivable period and thereby cash flow as well.

Along with this, by replacing short term obligation with long-term business

organization can manage and improves its working capital. Moreover, working capital

is mainly used for meeting short-term obligations from current assets (Le and et.al.,

2018).

In addition to this, MDL should focus on undertaking promotional tools and

techniques. By this, company would become able to convert stock into cash more

frequently. Thus, inventory turnover ratio or period can be improved by MDL through

employing inventory management and promotional strategies.

Furthermore, company’s working capital and cash flow increases when supplier

payment period is higher. Accordingly, focus needs to be placed on contacting

supplier which offers credit for longer duration.

business unit is required to take suitable measures regarding working capital and cash flow

management.

3. Recommending steps to the firm that need to be taken for improving cash flow and thereby

working capital

Budgeting refers to the process that helps in creating plan for spending money and

balancing income level. Cited case situation presents that MDL is facing issues in receiving

amount from debtors. There are several customers who are making default in paying funds

that owed to them. This situation is placing direct impact on company’s working capital and

cash flow position. For business management, in the context of MDL, working capital is

considered as the most essential aspect that needed to carry out daily operations prominently.

In this regard, manager of MDL is required to take significant measure for enhancing both

working capital and thereby cash flow as well.

For reducing debt level and improving receivable period manager of MDL should

make focus on evaluating credit rating of debtors. By doing this, company can

identify customers who do not make payment on time. In this way, such measure

helps in improving receivable period and thereby cash flow as well.

Along with this, by replacing short term obligation with long-term business

organization can manage and improves its working capital. Moreover, working capital

is mainly used for meeting short-term obligations from current assets (Le and et.al.,

2018).

In addition to this, MDL should focus on undertaking promotional tools and

techniques. By this, company would become able to convert stock into cash more

frequently. Thus, inventory turnover ratio or period can be improved by MDL through

employing inventory management and promotional strategies.

Furthermore, company’s working capital and cash flow increases when supplier

payment period is higher. Accordingly, focus needs to be placed on contacting

supplier which offers credit for longer duration.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It has assessed from the evaluation that MDL facing issues in relation to recovering

amount from debtor. Thus, for improving cash flow manager is required to tighten or strict

credit policies. By doing this, firm would become able to receive payment on time and

thereby can meet day to day activities prominently. Further, for managing cash flows

company should offer credit to the debtors for short span over longer duration. Hence, by

practicing all such strategies MDL would become able to get desired level of outcome or

success.

PART 2

Executive summary

This report is based on the case scenario of Second Sight Plc which offers sunglasses

to the customers. According to the case, company is currently applying traditional budgeting

system for the purpose of cost assessment. It can be inferred from the evaluation that

company should undertake activity based budgeting method for developing financial plan.

Further, it has been articulated that using alternative methods of budgeting Second Sight Plc

would become able to present appropriate view of cost and profitability aspect.

1. Stating purpose and types of budgeting

Budget may be served as a plan that associated with specific time frame, which

contains information about both income and expenses. Thus, for getting or assessing

information about cash inflows and outflows Second Sight Plc prepares budget using

traditional method or system.

With regards to business management, Second Sight Plc emphasizes on preparing

budget. In the context of business organization, purpose of budgeting is enumerated below:

Budget helps in making forecast about income and expenditure associated with future

activities. By preparing budgets, manager can do prediction that business unit will

generate profit or loss in the upcoming time period.

It offers a financial framework which aid in decision making aspects. Moreover, it

provides manager with framework which helps in doing comparison of current

performance in against to the standards. By this, Second Sight Plc can assess

deficiency and take corrective action for future (Budget: Definition, Purpose,

amount from debtor. Thus, for improving cash flow manager is required to tighten or strict

credit policies. By doing this, firm would become able to receive payment on time and

thereby can meet day to day activities prominently. Further, for managing cash flows

company should offer credit to the debtors for short span over longer duration. Hence, by

practicing all such strategies MDL would become able to get desired level of outcome or

success.

PART 2

Executive summary

This report is based on the case scenario of Second Sight Plc which offers sunglasses

to the customers. According to the case, company is currently applying traditional budgeting

system for the purpose of cost assessment. It can be inferred from the evaluation that

company should undertake activity based budgeting method for developing financial plan.

Further, it has been articulated that using alternative methods of budgeting Second Sight Plc

would become able to present appropriate view of cost and profitability aspect.

1. Stating purpose and types of budgeting

Budget may be served as a plan that associated with specific time frame, which

contains information about both income and expenses. Thus, for getting or assessing

information about cash inflows and outflows Second Sight Plc prepares budget using

traditional method or system.

With regards to business management, Second Sight Plc emphasizes on preparing

budget. In the context of business organization, purpose of budgeting is enumerated below:

Budget helps in making forecast about income and expenditure associated with future

activities. By preparing budgets, manager can do prediction that business unit will

generate profit or loss in the upcoming time period.

It offers a financial framework which aid in decision making aspects. Moreover, it

provides manager with framework which helps in doing comparison of current

performance in against to the standards. By this, Second Sight Plc can assess

deficiency and take corrective action for future (Budget: Definition, Purpose,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Elements and Steps, 2020). In this way, budget can be served as a tool which helps in

monitoring or evaluating business performance.

Helps in determining accountability of managers and planning about incentives for

concerned departments.

There are several traditional and alternative budgeting methods available which can be

undertaken by Second Sight Plc such as follows:

Traditional budgeting methods

Incremental budget is recognized as traditional method in which past year’s budget is

used for arriving at new one. In this, business unit makes marginal changes in the previous

year’s plan or framework. Moreover, managers assume that all the concerned departments

will continue with the recent activities, income and expenses (Incremental Budgeting –

Meaning, Advantages and Disadvantages, 2020).

Strengths Weaknesses

Easy to implement as it does not

involve complex calculation.

Such budgeting method assists in

ensuring continuing funding of

departments.

Facilitates both operational and

funding stability.

This budget ignores changing

circumstances which in turn limits its

significance to a great extent.

It leads extra spending and creates the

situation of budgetary slack.

Incremental budgets may result into

wastage of resources which in turn

hampers potential growth.

Alternative budgeting methods

Zero based budgeting

It involves budget preparation which starts from scratch or zero base for developing

the new one. ZBB includes re-evaluation of every item of cash flow statement and focuses of

justifying the same. In this, all the expenses are calculated on the basis of activities that need

to be performed in current period.

monitoring or evaluating business performance.

Helps in determining accountability of managers and planning about incentives for

concerned departments.

There are several traditional and alternative budgeting methods available which can be

undertaken by Second Sight Plc such as follows:

Traditional budgeting methods

Incremental budget is recognized as traditional method in which past year’s budget is

used for arriving at new one. In this, business unit makes marginal changes in the previous

year’s plan or framework. Moreover, managers assume that all the concerned departments

will continue with the recent activities, income and expenses (Incremental Budgeting –

Meaning, Advantages and Disadvantages, 2020).

Strengths Weaknesses

Easy to implement as it does not

involve complex calculation.

Such budgeting method assists in

ensuring continuing funding of

departments.

Facilitates both operational and

funding stability.

This budget ignores changing

circumstances which in turn limits its

significance to a great extent.

It leads extra spending and creates the

situation of budgetary slack.

Incremental budgets may result into

wastage of resources which in turn

hampers potential growth.

Alternative budgeting methods

Zero based budgeting

It involves budget preparation which starts from scratch or zero base for developing

the new one. ZBB includes re-evaluation of every item of cash flow statement and focuses of

justifying the same. In this, all the expenses are calculated on the basis of activities that need

to be performed in current period.

Strengths Weaknesses

Highly appropriate for non-profit and

service organizations.

Ensures optimum utilization of

financial resources by eliminating

bottlenecks or undesirable activities

from operations.

Assists in promoting operational

efficiency as it is not based on

incremental approach or method.

ZBB is time consuming process

because it involves more paper work.

Requires high manpower because

each item of every department is

evaluated for budget preparation

(Zero Based Budgeting – Meaning,

Advantages and Disadvantages,

2020).

Imposes high cost because for budget

preparation company needs to make

focus on conducting training &

development session.

Activity based budgeting

According to this method, budgets are prepared through considering all the overhead

cost or expenditure. In this, activities that incur cost are analyzed and researched deeply for

the purpose of cost ascertainment as well as allocation.

Strengths Weaknesses

Focuses on making evaluation or

assessment of each cost driver.

Helps in gaining competitive edge as

it ensures production cost saving and

thereby assists in setting appropriate

pricing framework.

ABB assists in eliminating

bottlenecks and improving

relationship with both business units

and customers.

In ABB, firm requires competent

workforce having understanding

about cost drivers and aspects

pertaining to resource allocation.

For preparing budget according to

ABB company needs lot of resources.

Moreover, business unit has to

include team of higher management

for doing numerous analyses.

Further, under ABB, firm needs team

Highly appropriate for non-profit and

service organizations.

Ensures optimum utilization of

financial resources by eliminating

bottlenecks or undesirable activities

from operations.

Assists in promoting operational

efficiency as it is not based on

incremental approach or method.

ZBB is time consuming process

because it involves more paper work.

Requires high manpower because

each item of every department is

evaluated for budget preparation

(Zero Based Budgeting – Meaning,

Advantages and Disadvantages,

2020).

Imposes high cost because for budget

preparation company needs to make

focus on conducting training &

development session.

Activity based budgeting

According to this method, budgets are prepared through considering all the overhead

cost or expenditure. In this, activities that incur cost are analyzed and researched deeply for

the purpose of cost ascertainment as well as allocation.

Strengths Weaknesses

Focuses on making evaluation or

assessment of each cost driver.

Helps in gaining competitive edge as

it ensures production cost saving and

thereby assists in setting appropriate

pricing framework.

ABB assists in eliminating

bottlenecks and improving

relationship with both business units

and customers.

In ABB, firm requires competent

workforce having understanding

about cost drivers and aspects

pertaining to resource allocation.

For preparing budget according to

ABB company needs lot of resources.

Moreover, business unit has to

include team of higher management

for doing numerous analyses.

Further, under ABB, firm needs team

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of trained personnel which in turn

imposes high cost (Activity based

budgeting, 2020).

Rolling budgets

This budgeting tool focuses on including highly updated information as it follows

dynamic approach, Accordingly, budget is prepared and reviewed on quarterly basis rather

than preparation for 12 months.

Strengths Weaknesses

Facilitates effectual planning and

control

Ensures change appreciation

Contributes in wisely spending

Time intensive exercise

Demotivate personnel due to the lack

of having updated information

2. Demonstrating the application of traditional and alternative budgeting methods

By doing assessment, it has found that incremental budget helps in making competent

or effectual plan about future cost management. The below depicted cash budget clearly

exhibits that additions are done in sales as well as expenditures. Considering such budget

manager of Second Sight Plc can compare existing performance and take measures for

performance improvement.

Traditional method: Incremental budget

Particulars

Janua

ry

Februa

ry

Marc

h April May June

Opening cash balance 10000 16500

23292

.5

30387

.5

37795

.2

45526

.3

Sales 15000 15450 15914 16391 16883 17389

Other income 2000 2000 2000 2000 2000 2000

Total cash inflows 27000 33950 41206 48778 56677 64915

imposes high cost (Activity based

budgeting, 2020).

Rolling budgets

This budgeting tool focuses on including highly updated information as it follows

dynamic approach, Accordingly, budget is prepared and reviewed on quarterly basis rather

than preparation for 12 months.

Strengths Weaknesses

Facilitates effectual planning and

control

Ensures change appreciation

Contributes in wisely spending

Time intensive exercise

Demotivate personnel due to the lack

of having updated information

2. Demonstrating the application of traditional and alternative budgeting methods

By doing assessment, it has found that incremental budget helps in making competent

or effectual plan about future cost management. The below depicted cash budget clearly

exhibits that additions are done in sales as well as expenditures. Considering such budget

manager of Second Sight Plc can compare existing performance and take measures for

performance improvement.

Traditional method: Incremental budget

Particulars

Janua

ry

Februa

ry

Marc

h April May June

Opening cash balance 10000 16500

23292

.5

30387

.5

37795

.2

45526

.3

Sales 15000 15450 15914 16391 16883 17389

Other income 2000 2000 2000 2000 2000 2000

Total cash inflows 27000 33950 41206 48778 56677 64915

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

.4 .8 .5

Material 3000 3060 3121 3184 3247 3312

Labour 2250 2250 2250 2250 2250 2250

Other expenses 2250 2318 2387 2459 2532 2608

Administration, selling &

distribution expenses 3000 3030

3060.

3

3090.

9

3121.

81

3153.

03

Total cash outflows 10500

10657.

5

10818

.5

10983

.2

11151

.5

11323

.6

Cash surplus/ closing cash balance 16500 23293 30387 37795 45526 53592

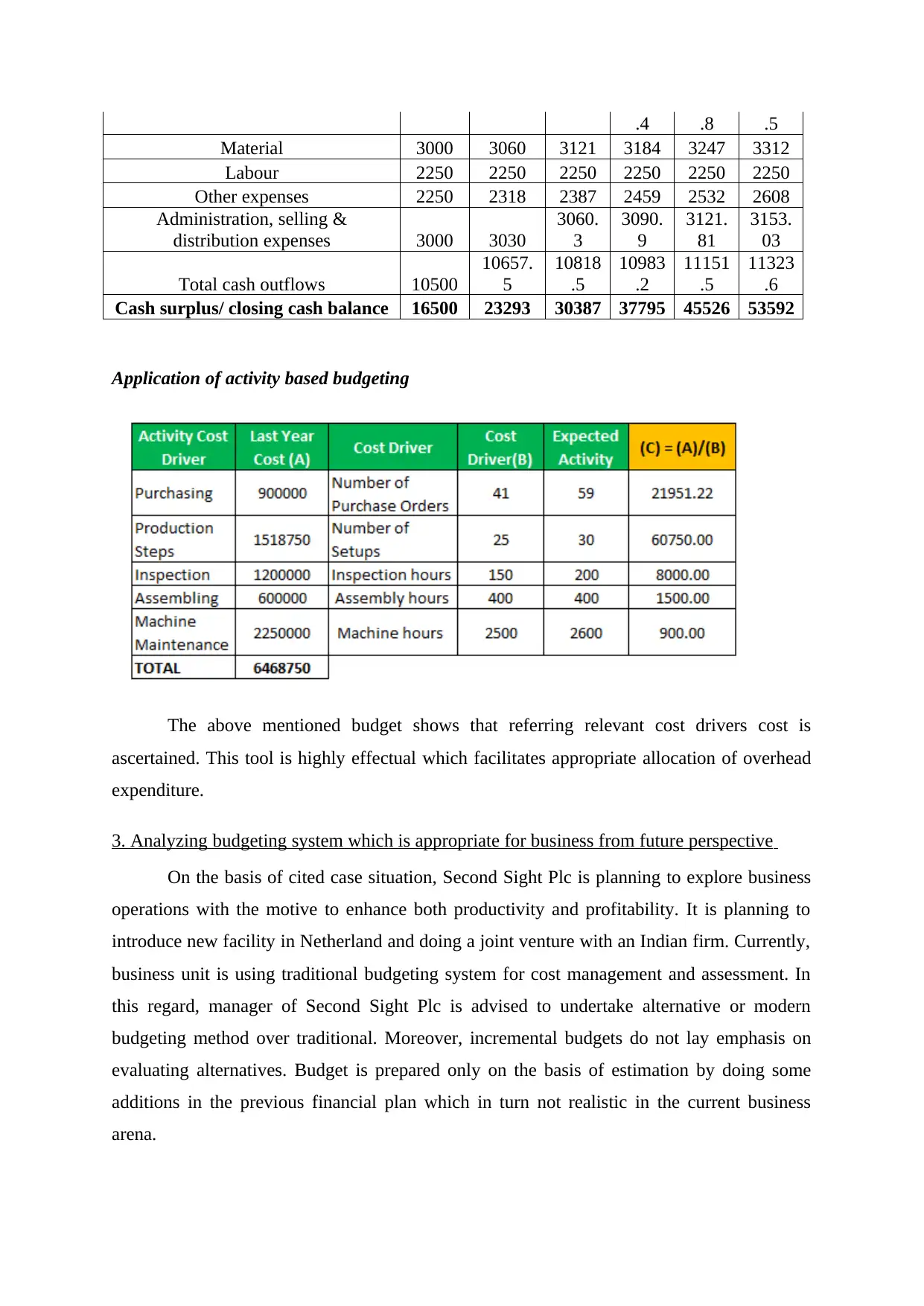

Application of activity based budgeting

The above mentioned budget shows that referring relevant cost drivers cost is

ascertained. This tool is highly effectual which facilitates appropriate allocation of overhead

expenditure.

3. Analyzing budgeting system which is appropriate for business from future perspective

On the basis of cited case situation, Second Sight Plc is planning to explore business

operations with the motive to enhance both productivity and profitability. It is planning to

introduce new facility in Netherland and doing a joint venture with an Indian firm. Currently,

business unit is using traditional budgeting system for cost management and assessment. In

this regard, manager of Second Sight Plc is advised to undertake alternative or modern

budgeting method over traditional. Moreover, incremental budgets do not lay emphasis on

evaluating alternatives. Budget is prepared only on the basis of estimation by doing some

additions in the previous financial plan which in turn not realistic in the current business

arena.

Material 3000 3060 3121 3184 3247 3312

Labour 2250 2250 2250 2250 2250 2250

Other expenses 2250 2318 2387 2459 2532 2608

Administration, selling &

distribution expenses 3000 3030

3060.

3

3090.

9

3121.

81

3153.

03

Total cash outflows 10500

10657.

5

10818

.5

10983

.2

11151

.5

11323

.6

Cash surplus/ closing cash balance 16500 23293 30387 37795 45526 53592

Application of activity based budgeting

The above mentioned budget shows that referring relevant cost drivers cost is

ascertained. This tool is highly effectual which facilitates appropriate allocation of overhead

expenditure.

3. Analyzing budgeting system which is appropriate for business from future perspective

On the basis of cited case situation, Second Sight Plc is planning to explore business

operations with the motive to enhance both productivity and profitability. It is planning to

introduce new facility in Netherland and doing a joint venture with an Indian firm. Currently,

business unit is using traditional budgeting system for cost management and assessment. In

this regard, manager of Second Sight Plc is advised to undertake alternative or modern

budgeting method over traditional. Moreover, incremental budgets do not lay emphasis on

evaluating alternatives. Budget is prepared only on the basis of estimation by doing some

additions in the previous financial plan which in turn not realistic in the current business

arena.

Referring all such aspect it is recommended to Second Sight Plc to adopt activity

based budgeting method. It is suggested because Second Sight Plc is involved in producing

prescribed sunglasses and other ones for leading international brands. Thus, activity based

method will prove to be more beneficial for the firm in the context of cost assessment and

budget formulation. In the dynamic business arena, activity based budgeting is highly

suitable because in this overhead cost allotted to the related activity as per the driver

identified. ABB focuses on analyzing activities deeply that incurs cost for the purpose of

resource allocation (Activity based budgeting, 2020). By undertaking this method, firm can

bring efficiency in the activities by justifying the cost drivers.

There are several benefits which company will attain by undertaking ABB method for

cost ascertainment and resource allocation. The rationale behind this, it eliminates

unnecessary activities from the operations and contributes in profit maximization. By taking

into account all the above depicted aspects it can be presented that ABB will be suitable for

all parts of the business with regards to Second Sight Plc. Hence, in the near future, through

undertaking modern budgeting method namely ABB Second Sight Plc can prepare

appropriate and realistic budgeting framework. Referring this, business unit can do

monitoring of current performance effectually and thereby finds deficiencies. In this way,

ABB helps in taking corrective measure for future and setting appropriate financial plan for

future.

based budgeting method. It is suggested because Second Sight Plc is involved in producing

prescribed sunglasses and other ones for leading international brands. Thus, activity based

method will prove to be more beneficial for the firm in the context of cost assessment and

budget formulation. In the dynamic business arena, activity based budgeting is highly

suitable because in this overhead cost allotted to the related activity as per the driver

identified. ABB focuses on analyzing activities deeply that incurs cost for the purpose of

resource allocation (Activity based budgeting, 2020). By undertaking this method, firm can

bring efficiency in the activities by justifying the cost drivers.

There are several benefits which company will attain by undertaking ABB method for

cost ascertainment and resource allocation. The rationale behind this, it eliminates

unnecessary activities from the operations and contributes in profit maximization. By taking

into account all the above depicted aspects it can be presented that ABB will be suitable for

all parts of the business with regards to Second Sight Plc. Hence, in the near future, through

undertaking modern budgeting method namely ABB Second Sight Plc can prepare

appropriate and realistic budgeting framework. Referring this, business unit can do

monitoring of current performance effectually and thereby finds deficiencies. In this way,

ABB helps in taking corrective measure for future and setting appropriate financial plan for

future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.