Business Finance Report: Melbourne Housing, Income, and Loan Analysis

VerifiedAdded on 2021/06/17

|12

|2693

|26

Report

AI Summary

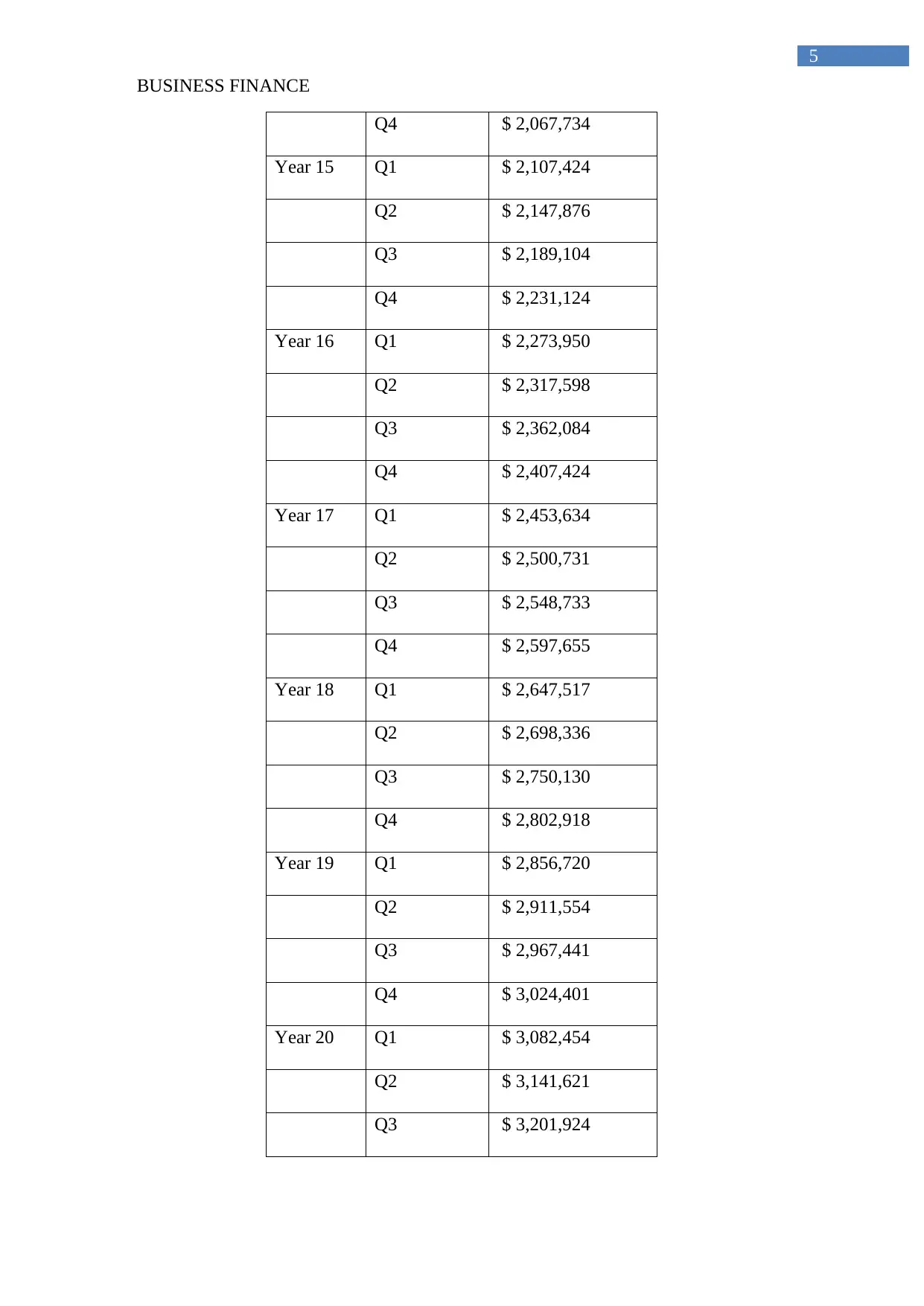

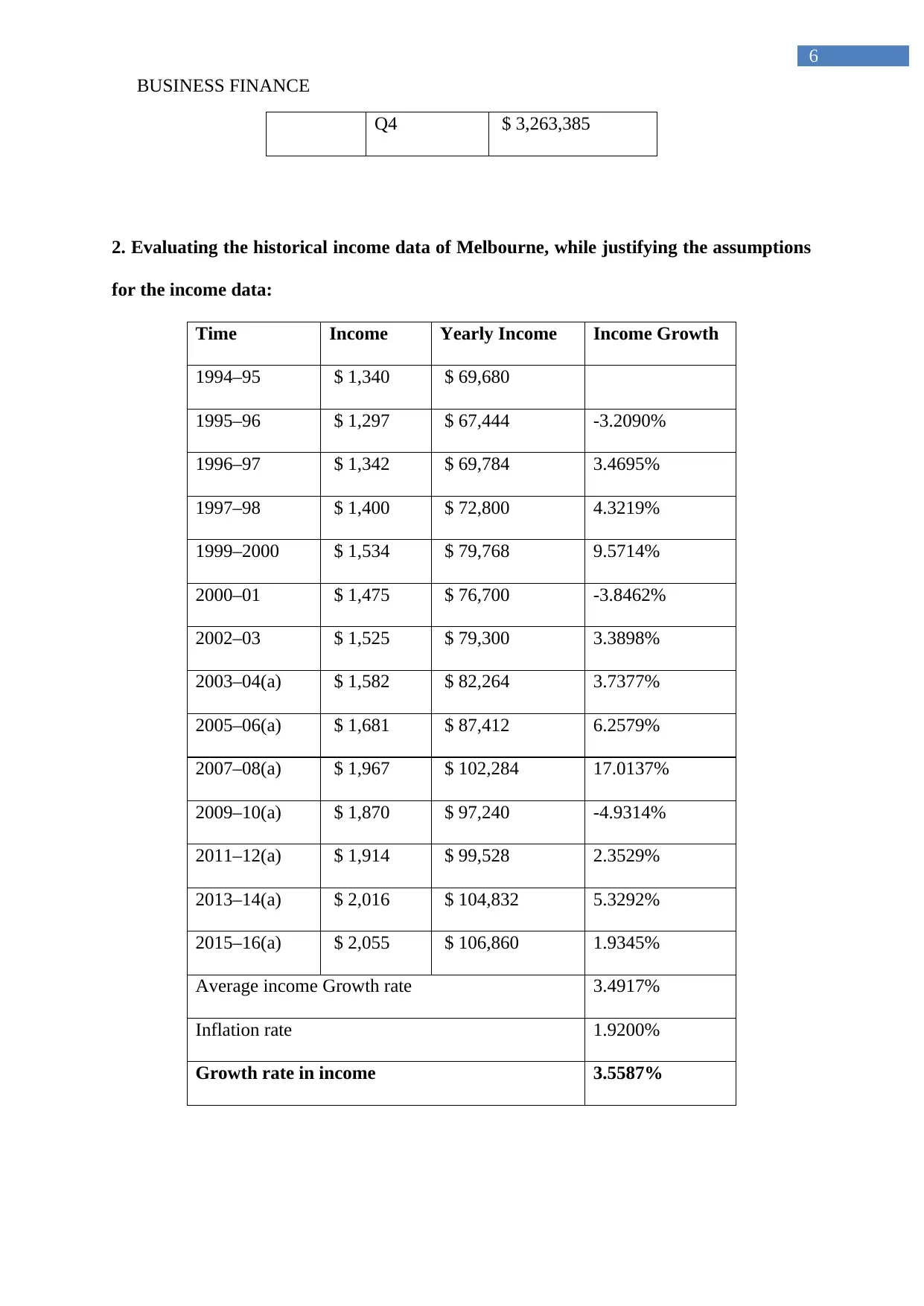

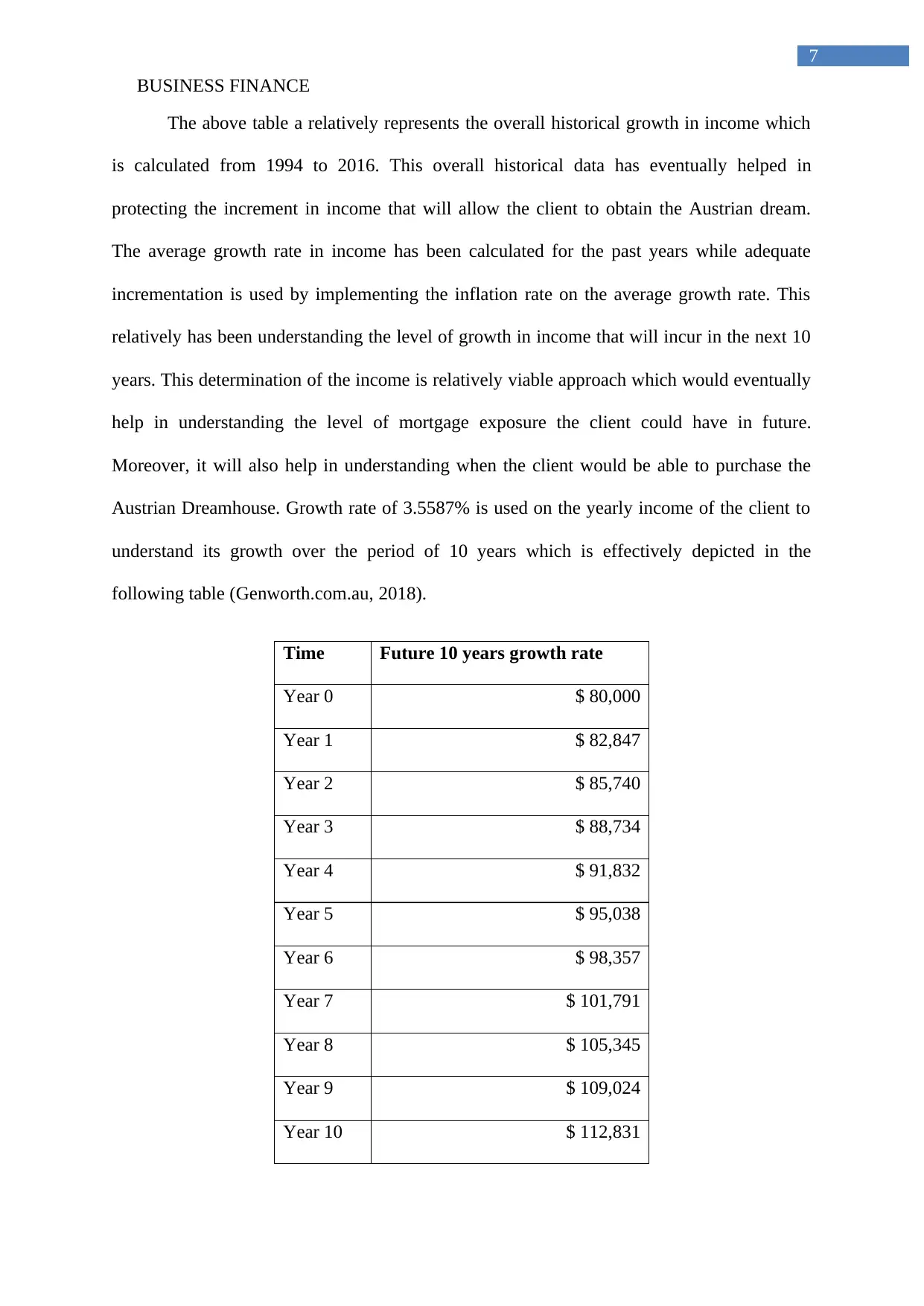

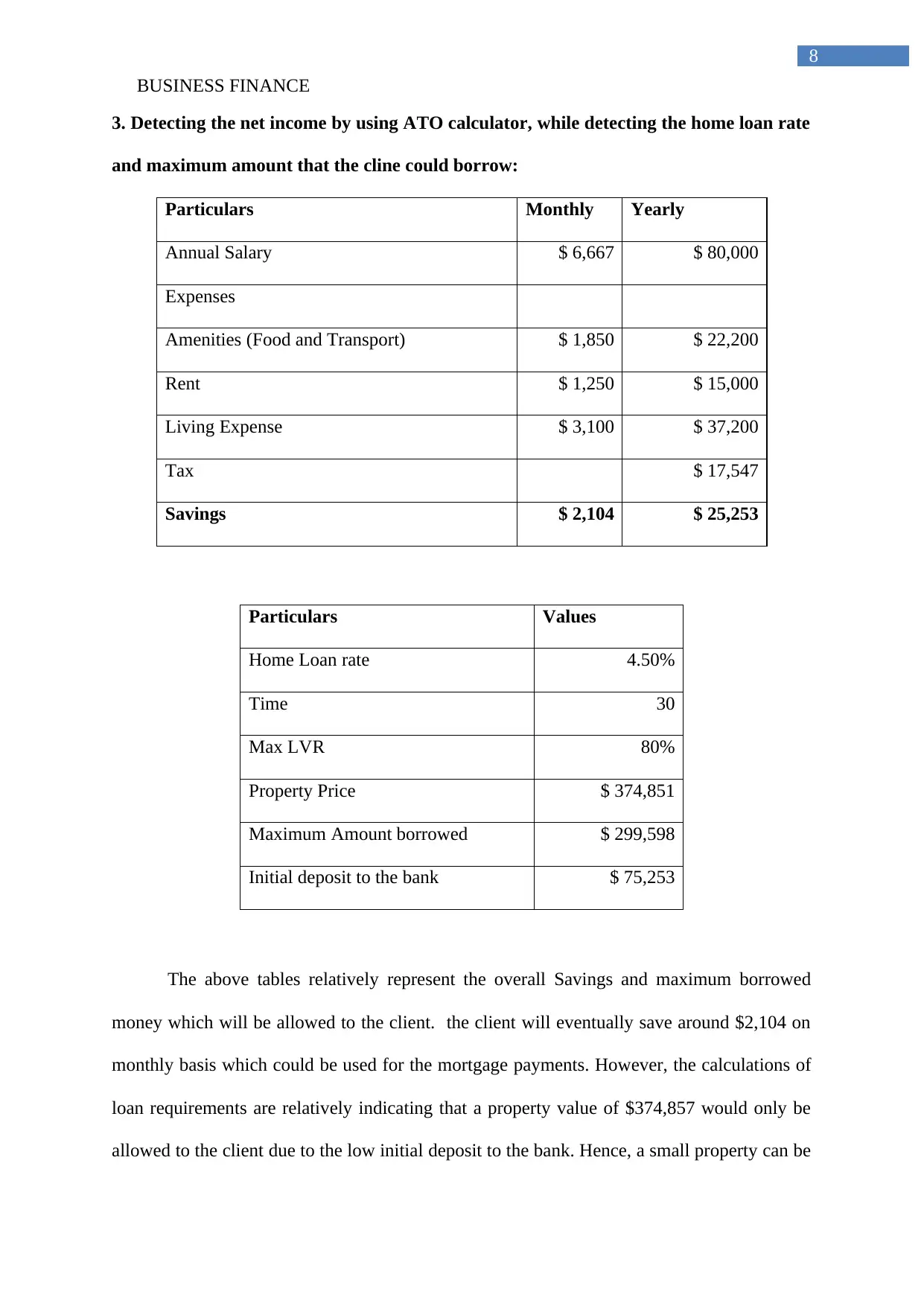

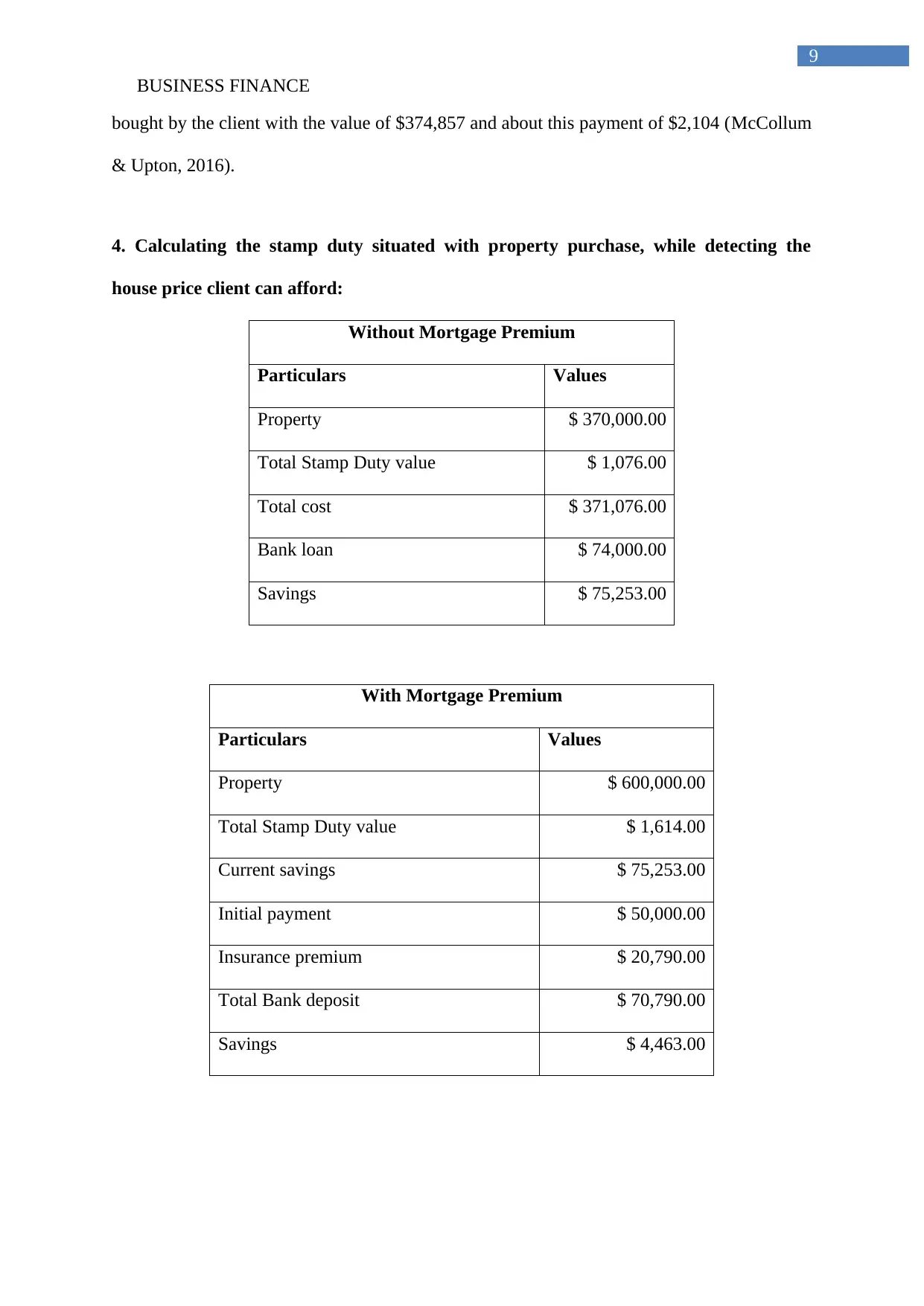

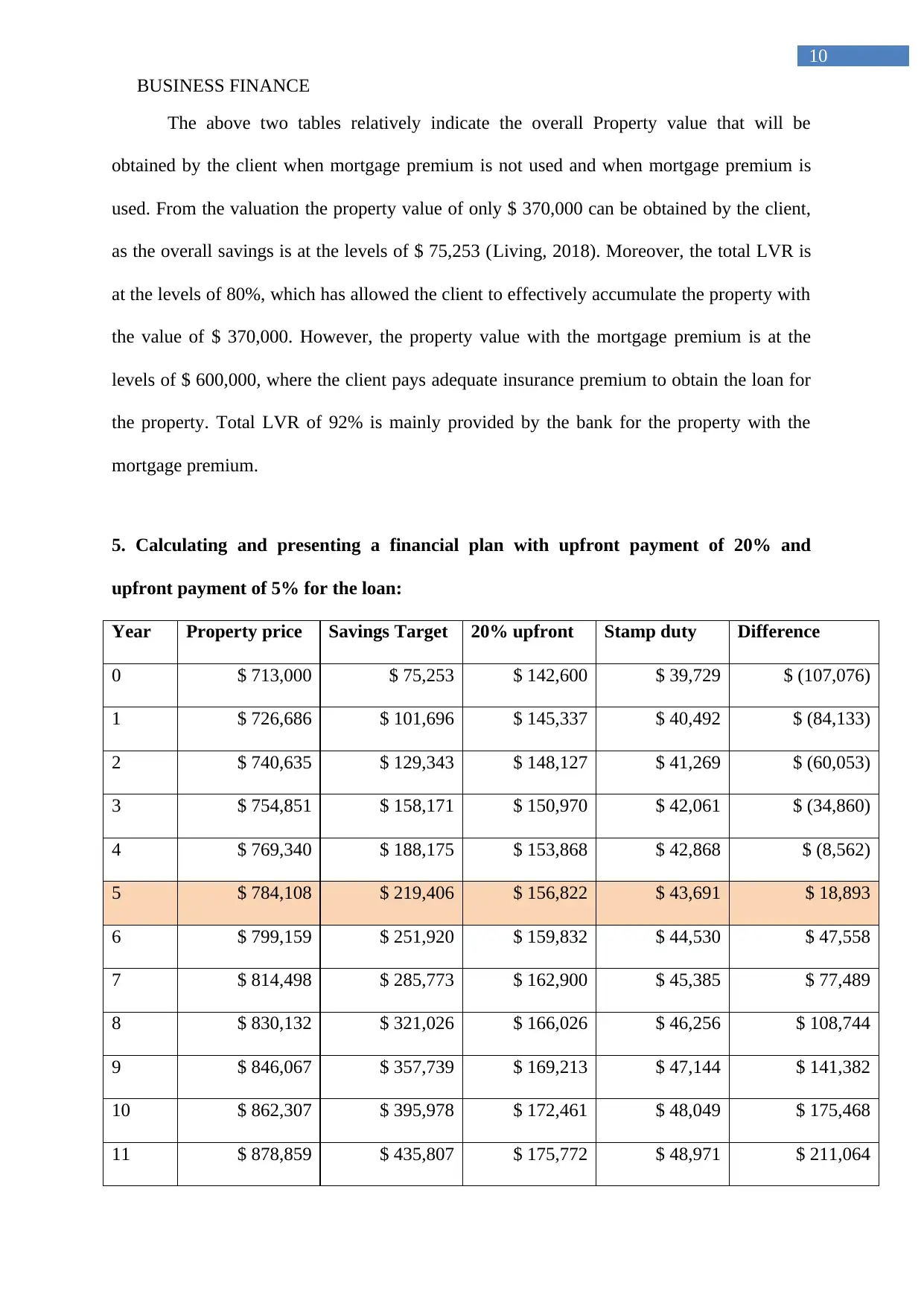

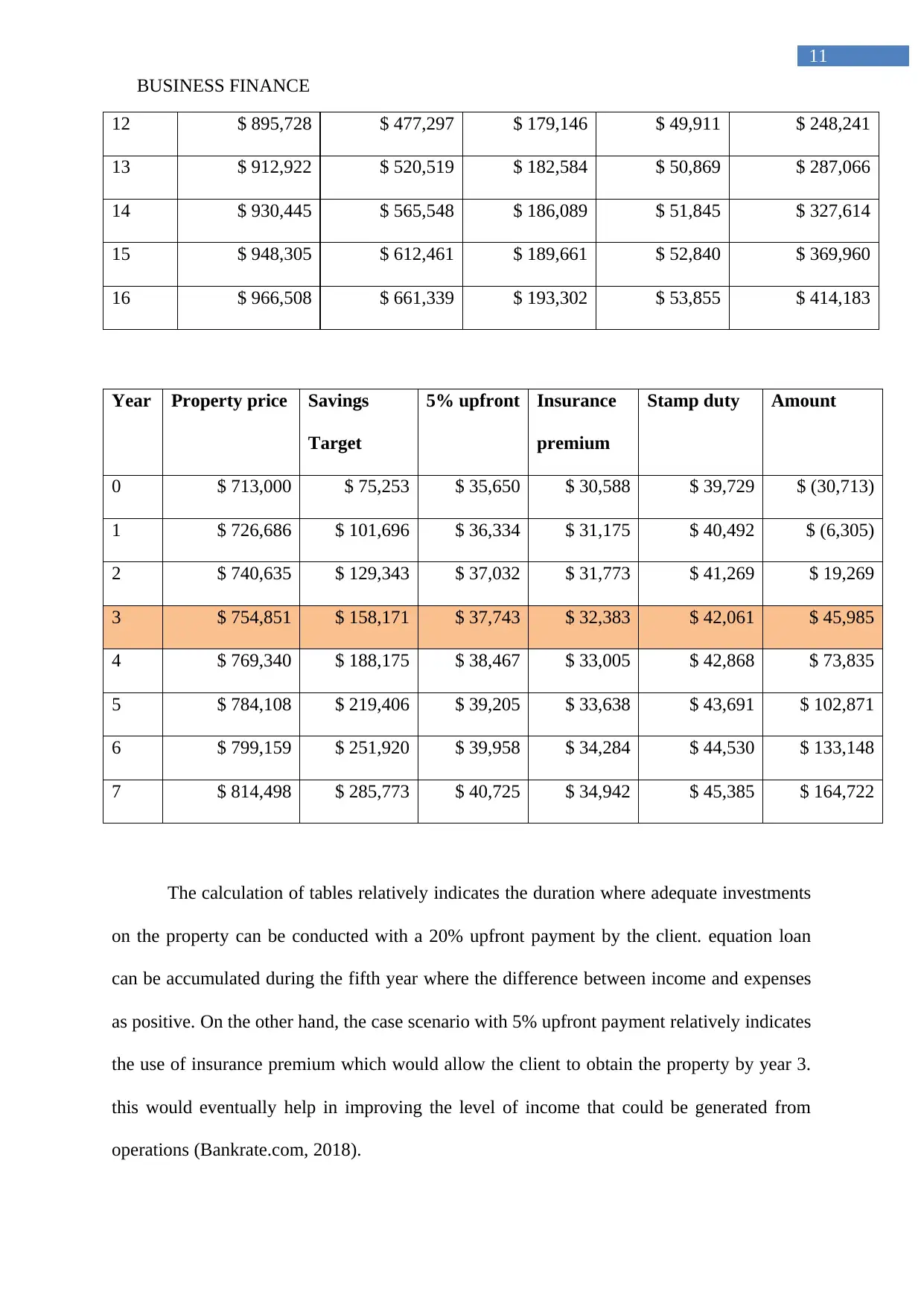

This report provides a comprehensive analysis of the Melbourne housing market, examining historical housing price growth from 2002 to 2017 and projecting future prices. It evaluates historical income data from 1994 to 2016, incorporating inflation to forecast income growth. The report includes calculations for net income using an ATO calculator, determining home loan rates, and assessing the maximum borrowing amount. It calculates stamp duty, determines affordable house prices, and presents financial plans with 20% and 5% upfront payments. Furthermore, it assesses the impact of interest rate increments on mortgage payments and outlines a financial plan while addressing associated risks and assumptions. The analysis utilizes data from the ABS website and other financial resources to support its findings and recommendations.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.