BMP3005 Applied Business Finance: Enhancing Financial Performance

VerifiedAdded on 2023/06/14

|14

|3349

|498

Report

AI Summary

This report provides an overview of financial management, its importance, and its application within businesses. It defines financial management and discusses its significance in decision-making, profitability, funds distribution, and capital structure formation. The report also describes the main financial statements (profit and loss statement, statement of financial position, and cash flow statement) and explains the use of ratios (profitability, efficiency, and liquidity ratios) in financial management, using a case study to illustrate their application. Furthermore, it analyzes the case study company's profitability, liquidity, and efficiency based on ratio analysis and suggests processes the business might use to improve its financial performance. Desklib provides access to this and other solved assignments for students.

BSc (Hons) Business Management with

Foundation

BMP3005

Applied Business Finance

The concept and importance of financial

management and the processes

businesses might use to improve their

financial performance

1

Foundation

BMP3005

Applied Business Finance

The concept and importance of financial

management and the processes

businesses might use to improve their

financial performance

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction 3

Section 1: Definition and discussion of the concept and

importance of financial management 3

Section 2: Description and discussion of the main financial

statements and explain the use of ratios in financial management

4

Section 3: Using the template provided 5-9

i. Completing the Information on the ‘Business Review Template

(Ensure that you display your calculations for this detail)

5

ii. Using Excel producing an Income Statement for the Sample

Organisation (see Case Study). This should be included within your

appendices 6

iii. Using Excel completing the Balance Sheet 7

iv. Using the Case study information describing the profitability,

liquidity and efficiency of the company based on the results of ratio

analysis 8

Section 4: Using examples from the case study describing and

discussing the processes this business might use to improve their

financial performance 9

Conclusion 10

References 11

Appendix 13

2

Introduction 3

Section 1: Definition and discussion of the concept and

importance of financial management 3

Section 2: Description and discussion of the main financial

statements and explain the use of ratios in financial management

4

Section 3: Using the template provided 5-9

i. Completing the Information on the ‘Business Review Template

(Ensure that you display your calculations for this detail)

5

ii. Using Excel producing an Income Statement for the Sample

Organisation (see Case Study). This should be included within your

appendices 6

iii. Using Excel completing the Balance Sheet 7

iv. Using the Case study information describing the profitability,

liquidity and efficiency of the company based on the results of ratio

analysis 8

Section 4: Using examples from the case study describing and

discussing the processes this business might use to improve their

financial performance 9

Conclusion 10

References 11

Appendix 13

2

Introduction

Among the most important components of running a business is financial

management. It ensures that the company 's activities function smoothly and that the

distribution of funding is not disrupted. The study discusses the relevance of financial

governance, financial statement ideas, and the use of ratios in business operations. It has also

gone through key ratios like as profitability, liquidity, and efficiency ratios using the income

statement and balance sheet as an example from the case study. The financial performance of

the firm is also examined during the business performance review (Ashley and et. al., 2018).

Section 1: Definition and discussion of the concept and

importance of financial management

Financial management is a term that relates to the process of leading, controlling,

planning, and coordinating a company's financial activities. It also entails applying

management principles to an organization's financial resources, as well as having a

substantial influence on financial administration (Bano and et. al., 2021).

Keeping a sufficient stock of assets for the organisation;

Assuring investors that their investment will provide a high return;

Optimal and efficient asset use;

Creating real and secure venture freedoms to put resources into

Importance of Financial Management:

Financial Decision: It supports the company in making key financial decisions. A

decision that has the potential to bring the entire company down. It explains the various risks

and options and assists in determining the size of the investor's capital and the assets bought.

Profitability: If the books of accounts and resources are well-managed, the

organization's production will improve. It will also guarantee that the company's efficiency

and development potential are assessed.

Funds distribution: The right distribution of fiscal resources is based on the company's

earnings. It will assist the firm's fiscal ratios improve, as well as reduce expenses and raise its

monetary state.

Economic Stability: It provides immovability to a firm by addressing a solid monetary

framework and preventing commercial actions that might be harmful to the organisation, as

well as assisting in the maintenance and acquisition of further advantages.

3

Among the most important components of running a business is financial

management. It ensures that the company 's activities function smoothly and that the

distribution of funding is not disrupted. The study discusses the relevance of financial

governance, financial statement ideas, and the use of ratios in business operations. It has also

gone through key ratios like as profitability, liquidity, and efficiency ratios using the income

statement and balance sheet as an example from the case study. The financial performance of

the firm is also examined during the business performance review (Ashley and et. al., 2018).

Section 1: Definition and discussion of the concept and

importance of financial management

Financial management is a term that relates to the process of leading, controlling,

planning, and coordinating a company's financial activities. It also entails applying

management principles to an organization's financial resources, as well as having a

substantial influence on financial administration (Bano and et. al., 2021).

Keeping a sufficient stock of assets for the organisation;

Assuring investors that their investment will provide a high return;

Optimal and efficient asset use;

Creating real and secure venture freedoms to put resources into

Importance of Financial Management:

Financial Decision: It supports the company in making key financial decisions. A

decision that has the potential to bring the entire company down. It explains the various risks

and options and assists in determining the size of the investor's capital and the assets bought.

Profitability: If the books of accounts and resources are well-managed, the

organization's production will improve. It will also guarantee that the company's efficiency

and development potential are assessed.

Funds distribution: The right distribution of fiscal resources is based on the company's

earnings. It will assist the firm's fiscal ratios improve, as well as reduce expenses and raise its

monetary state.

Economic Stability: It provides immovability to a firm by addressing a solid monetary

framework and preventing commercial actions that might be harmful to the organisation, as

well as assisting in the maintenance and acquisition of further advantages.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Formation of the capital structure: The design should be appropriately created in order

to calculate the needed capital. Any business that is dependent on the quantity of cash it has

and how much it has to raise from outside sources (Black, 2019).

Section 2: Description and discussion of the main financial

statements and explain the use of ratios in financial management

Financial statements are information that every publicly traded firm is required to

keep. It depicts the firm's monetary activity. These financial statements indicate the

company's financial health and give financial statistics. These are required to be audited and

are the financial manager's duty. Internal and external sources can be used to audit these. It

ensured that the company's statements were not faked and were genuine. The following are

the statements (Büyüközkan, Göçer and Karabulut, 2019):

Profit and loss statement: This statement details the income, revenues, expenditures,

and accrued or outstanding expenses and earnings for the financial period. It also indicates

the transactions that were made throughout the time period and the expenditures that the

company had to bear in order to yield and make the sales. The organization's net profit for the

time is calculated by subtracting the period's costs and wages. It's the last item on the revenue

statement.

Statement of financial performance: This is the most important financial statement in

the company since it provides clients with a thorough overview of the company's financial

data. This statement shows the total assets as well as the obligations that the company has

agreed to pay in the future. It is also known as a financial record, which is the major concern

of businesses. In simple terms, this statement indicates the financial position of the company

at a certain point in time.

Cash flow statement: The net amount of cash inflow and outflow from the firm over a

period of time is shown in the cash flow statement. It depicts the cash flow from investing,

operating, and financing operations over a period of time. Operational operations indicate the

changes in current assets and liabilities, as well as interest and duty expenditures. The inflows

and outflows from the issuing of shareholder capital, debentures, advances, and dividend

payments are shown in the financing exercises (Chai and Ngai, 2020).

Uses of ratios in Financial management:

Monetary Ratios Analysis is an accounting strategy that assists managers in analysing

financial data that has been reported for the entire fiscal year. It is a limitless tool for the

management of a company's resources, since it allows them to examine the financial position

4

to calculate the needed capital. Any business that is dependent on the quantity of cash it has

and how much it has to raise from outside sources (Black, 2019).

Section 2: Description and discussion of the main financial

statements and explain the use of ratios in financial management

Financial statements are information that every publicly traded firm is required to

keep. It depicts the firm's monetary activity. These financial statements indicate the

company's financial health and give financial statistics. These are required to be audited and

are the financial manager's duty. Internal and external sources can be used to audit these. It

ensured that the company's statements were not faked and were genuine. The following are

the statements (Büyüközkan, Göçer and Karabulut, 2019):

Profit and loss statement: This statement details the income, revenues, expenditures,

and accrued or outstanding expenses and earnings for the financial period. It also indicates

the transactions that were made throughout the time period and the expenditures that the

company had to bear in order to yield and make the sales. The organization's net profit for the

time is calculated by subtracting the period's costs and wages. It's the last item on the revenue

statement.

Statement of financial performance: This is the most important financial statement in

the company since it provides clients with a thorough overview of the company's financial

data. This statement shows the total assets as well as the obligations that the company has

agreed to pay in the future. It is also known as a financial record, which is the major concern

of businesses. In simple terms, this statement indicates the financial position of the company

at a certain point in time.

Cash flow statement: The net amount of cash inflow and outflow from the firm over a

period of time is shown in the cash flow statement. It depicts the cash flow from investing,

operating, and financing operations over a period of time. Operational operations indicate the

changes in current assets and liabilities, as well as interest and duty expenditures. The inflows

and outflows from the issuing of shareholder capital, debentures, advances, and dividend

payments are shown in the financing exercises (Chai and Ngai, 2020).

Uses of ratios in Financial management:

Monetary Ratios Analysis is an accounting strategy that assists managers in analysing

financial data that has been reported for the entire fiscal year. It is a limitless tool for the

management of a company's resources, since it allows them to examine the financial position

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of the company. It aids senior management in making short and long-term company

decisions, as well as categorising patterns in those decisions by comparing them to past years.

The following are the most common applications of percentage assessment:

Financial ratios assist key supervisors in making decisions: In the computation of

extents and following definite judgments of these proportions, monetary reports, benefits,

pattern of returns, acquisition capacity, and recompense of the business are used. The

decision-makers are given a concise overview of what has to be done in the future to obtain

rewards.

Efficiencies in Operations: The ratios are used to determine a company's liquidity,

solvency, and productivity. It aids management in maintaining cheap costs while maintaining

high skill levels in order to accomplish the company's strategic goals (Goodwin, Stein and

Amelung, 2021).

Comparative analysis: Proportional analysis of the business is used to compare

various components in monetary information reporting. It evaluates the company's financial

performance and establishes a benchmark against which it can be compared to other

companies in the same industry.

Section 3: Using the template provided:

i. Completing the Information on the ‘Business Review Template

(Ensure that you display your calculations for this detail)

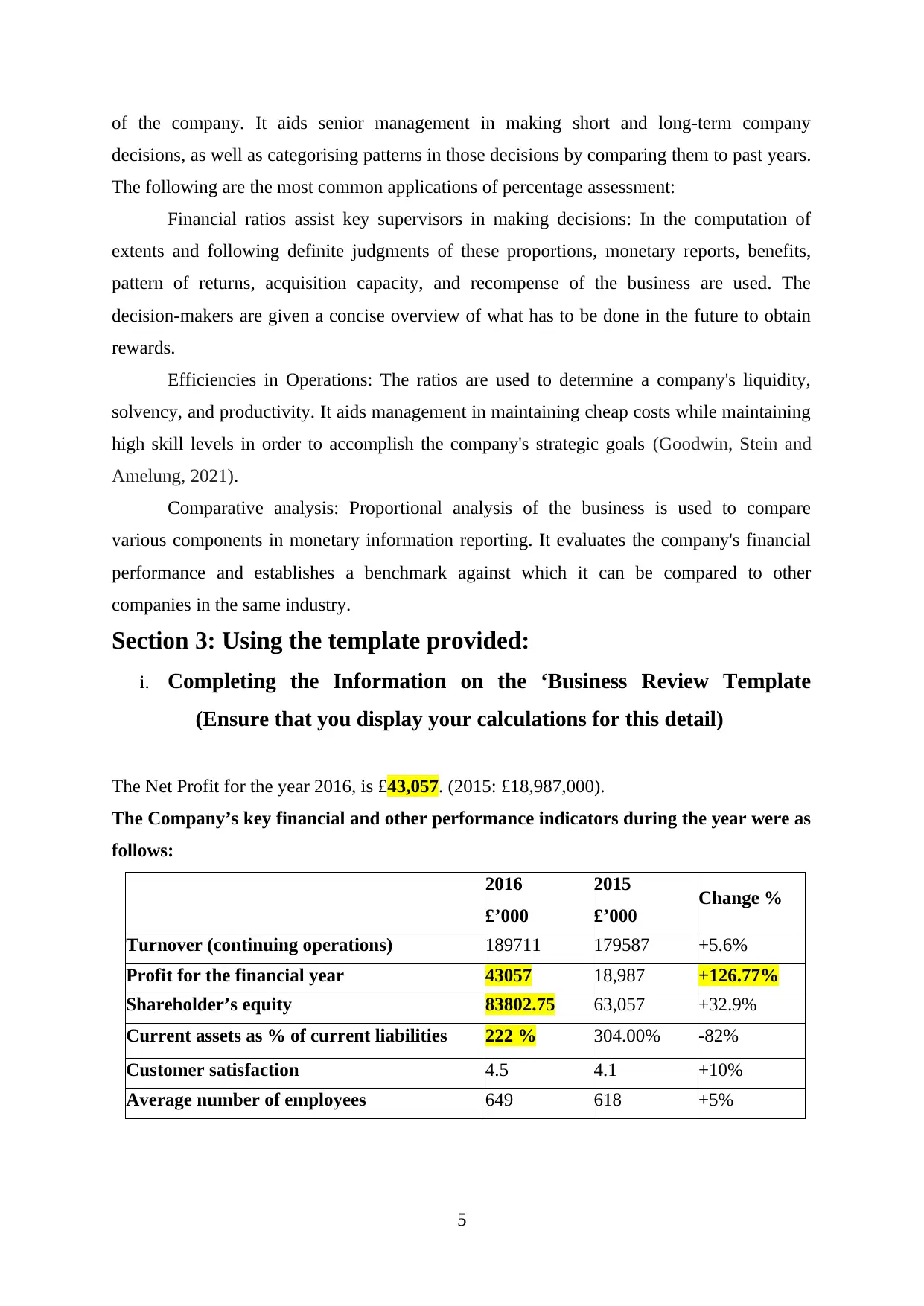

The Net Profit for the year 2016, is £43,057. (2015: £18,987,000).

The Company’s key financial and other performance indicators during the year were as

follows:

2016

£’000

2015

£’000 Change %

Turnover (continuing operations) 189711 179587 +5.6%

Profit for the financial year 43057 18,987 +126.77%

Shareholder’s equity 83802.75 63,057 +32.9%

Current assets as % of current liabilities 222 % 304.00% -82%

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

5

decisions, as well as categorising patterns in those decisions by comparing them to past years.

The following are the most common applications of percentage assessment:

Financial ratios assist key supervisors in making decisions: In the computation of

extents and following definite judgments of these proportions, monetary reports, benefits,

pattern of returns, acquisition capacity, and recompense of the business are used. The

decision-makers are given a concise overview of what has to be done in the future to obtain

rewards.

Efficiencies in Operations: The ratios are used to determine a company's liquidity,

solvency, and productivity. It aids management in maintaining cheap costs while maintaining

high skill levels in order to accomplish the company's strategic goals (Goodwin, Stein and

Amelung, 2021).

Comparative analysis: Proportional analysis of the business is used to compare

various components in monetary information reporting. It evaluates the company's financial

performance and establishes a benchmark against which it can be compared to other

companies in the same industry.

Section 3: Using the template provided:

i. Completing the Information on the ‘Business Review Template

(Ensure that you display your calculations for this detail)

The Net Profit for the year 2016, is £43,057. (2015: £18,987,000).

The Company’s key financial and other performance indicators during the year were as

follows:

2016

£’000

2015

£’000 Change %

Turnover (continuing operations) 189711 179587 +5.6%

Profit for the financial year 43057 18,987 +126.77%

Shareholder’s equity 83802.75 63,057 +32.9%

Current assets as % of current liabilities 222 % 304.00% -82%

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

5

The purchase of the Extinguishers company on 1 May 2015, which contributed a full year's

contribution in 2016, raised turnover from ongoing operations by 5.6 percent.

Gross Profit = £81,125

Net Profit = £43057

Net Profit increased in 2016 by 126.77% during the year.

Shareholders’ equity increased by 32.9% by £20,745.75.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current

Liabilities) is 1.47:1

The company’s “current ratio” (Current Assets divided by Current Liabilities.) is 2.22: 1.

(The calculation are shown in appendix)

v. Using Excel producing an Income Statement for the Sample

Organisation (see Case Study)

This is included within appendix

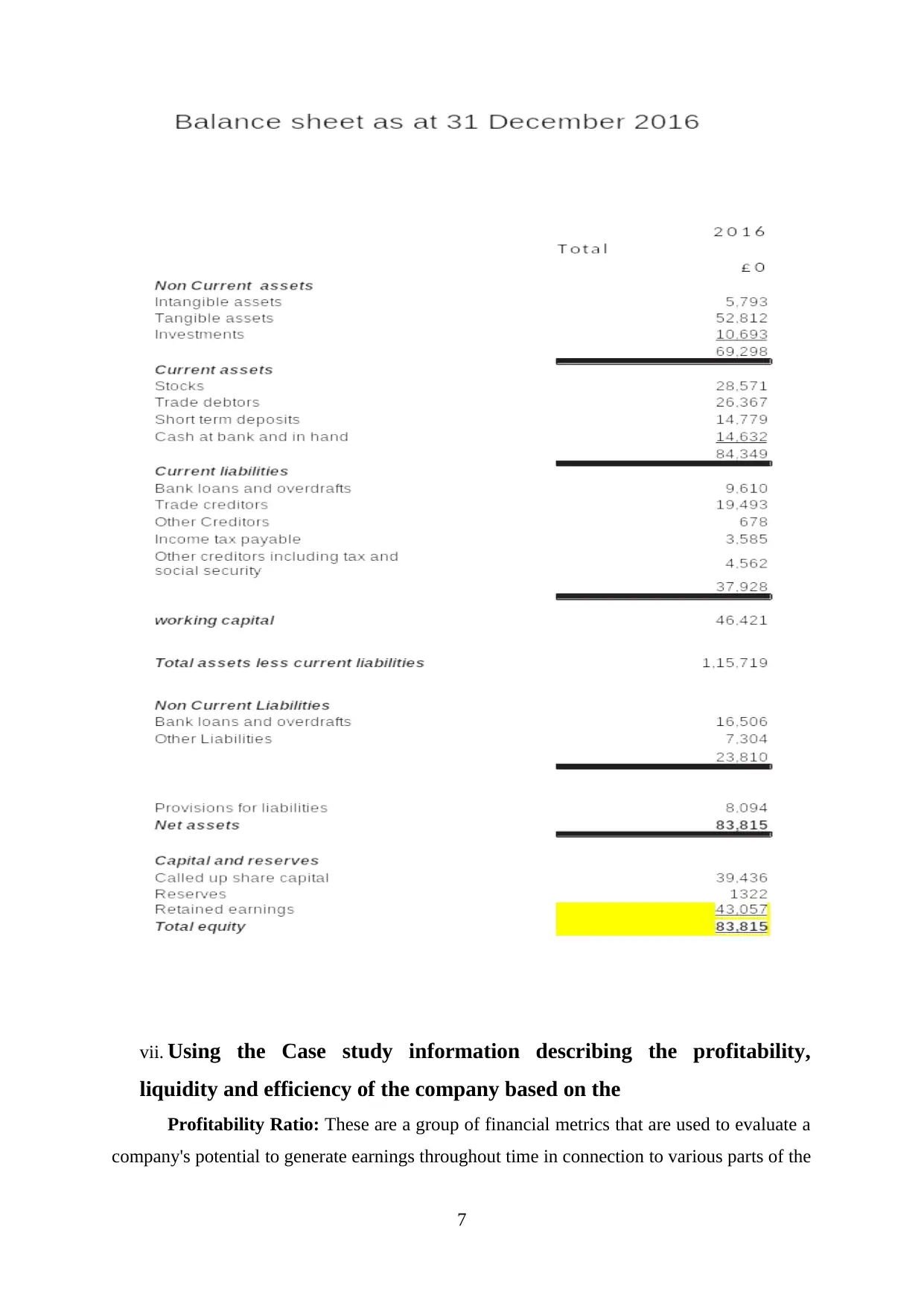

vi. Using Excel completing the Balance Sheet

6

contribution in 2016, raised turnover from ongoing operations by 5.6 percent.

Gross Profit = £81,125

Net Profit = £43057

Net Profit increased in 2016 by 126.77% during the year.

Shareholders’ equity increased by 32.9% by £20,745.75.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current

Liabilities) is 1.47:1

The company’s “current ratio” (Current Assets divided by Current Liabilities.) is 2.22: 1.

(The calculation are shown in appendix)

v. Using Excel producing an Income Statement for the Sample

Organisation (see Case Study)

This is included within appendix

vi. Using Excel completing the Balance Sheet

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

vii. Using the Case study information describing the profitability,

liquidity and efficiency of the company based on the

Profitability Ratio: These are a group of financial metrics that are used to evaluate a

company's potential to generate earnings throughout time in connection to various parts of the

7

liquidity and efficiency of the company based on the

Profitability Ratio: These are a group of financial metrics that are used to evaluate a

company's potential to generate earnings throughout time in connection to various parts of the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

income statement and balance sheet of a fiscal year based on the company's performance.

Gross profit margin, net profit margin, return on assets, and return on equity are among the

most important profitability measures.

Gross Profit Margin= (Revenue – cost of Sales) / Revenue * 100

= (189,711 – 108,586) / 189,711 * 100 = 42.76%

Net Profit Margin = (Net profit/ Revenue) *100

= (43,057/189,711) * 100 = 22.70%

Interpretation: The above ratios represent the profit percentage as a proportion of

revenue earned, taking into account both operating and non-operating expenditures. The

gross profit margin is the percentage of money left over after expenses are deducted from the

revenue, whereas the net profit margin is the percentage of money left over after expenses are

deducted. The gross profit is 42.76 percent, but the net profit is 22.7 percent, indicating a

profit decrease of around 20%. As a result, the firm must reduce its overhead expenditures,

that are preventing it from generating greater net revenue. It is critical for the investor to

compare earnings with those of other firms in the same industry in order to determine the

company's actual position in the industry (Littlechild, 2018).

2. Efficiency Ratio: This metric assesses how well a corporation manages its assets and

liabilities. It assesses how quickly the company collects payments from consumers

and how long it takes to complete debt payback, as well as the asset and equity

turnover. Asset turnover, stock turnover, receivable turnover, and accounts payable

turnover ratio are the most important ratios.

Asset turnover Ratio= Total Sales/ Total assets = 189,711/153,647 = 1.23

Stock Turnover Ratio = Cost of Sales/ Stock = (108,586/28,571) = 3.8

Accounts receivable Days = 365/ Debtors Turnover Ratio

=365/ 7.19 = 50.77 days

Accounts Payable Days = 365/ Creditors Turnover Ratio

= 365/7.04 = 51.84 days

Interpretation: The average client takes 51 days to pay off their debt, while creditors

take 52 days to collect their money. As a result, the firm pays and receives debts and

payments virtually simultaneously. However, it might be a constraint since if the receivable

days decrease, it can pose problems for the organisation, even if the days are only a few days

apart. The inventory turnover rate is 3.8, which implies that the entire stock investment flows

roughly 4 times every year, or 3 months per year. The total assets turnover ratio of 1.23

8

Gross profit margin, net profit margin, return on assets, and return on equity are among the

most important profitability measures.

Gross Profit Margin= (Revenue – cost of Sales) / Revenue * 100

= (189,711 – 108,586) / 189,711 * 100 = 42.76%

Net Profit Margin = (Net profit/ Revenue) *100

= (43,057/189,711) * 100 = 22.70%

Interpretation: The above ratios represent the profit percentage as a proportion of

revenue earned, taking into account both operating and non-operating expenditures. The

gross profit margin is the percentage of money left over after expenses are deducted from the

revenue, whereas the net profit margin is the percentage of money left over after expenses are

deducted. The gross profit is 42.76 percent, but the net profit is 22.7 percent, indicating a

profit decrease of around 20%. As a result, the firm must reduce its overhead expenditures,

that are preventing it from generating greater net revenue. It is critical for the investor to

compare earnings with those of other firms in the same industry in order to determine the

company's actual position in the industry (Littlechild, 2018).

2. Efficiency Ratio: This metric assesses how well a corporation manages its assets and

liabilities. It assesses how quickly the company collects payments from consumers

and how long it takes to complete debt payback, as well as the asset and equity

turnover. Asset turnover, stock turnover, receivable turnover, and accounts payable

turnover ratio are the most important ratios.

Asset turnover Ratio= Total Sales/ Total assets = 189,711/153,647 = 1.23

Stock Turnover Ratio = Cost of Sales/ Stock = (108,586/28,571) = 3.8

Accounts receivable Days = 365/ Debtors Turnover Ratio

=365/ 7.19 = 50.77 days

Accounts Payable Days = 365/ Creditors Turnover Ratio

= 365/7.04 = 51.84 days

Interpretation: The average client takes 51 days to pay off their debt, while creditors

take 52 days to collect their money. As a result, the firm pays and receives debts and

payments virtually simultaneously. However, it might be a constraint since if the receivable

days decrease, it can pose problems for the organisation, even if the days are only a few days

apart. The inventory turnover rate is 3.8, which implies that the entire stock investment flows

roughly 4 times every year, or 3 months per year. The total assets turnover ratio of 1.23

8

indicates that the company is performing well and generating enough revenue at the

conclusion of the fiscal year to stay in business.

3. Liquidity Ratio: It assesses a company's capacity to meet its financial obligations and

also informs us about its solvency. Current assets, current liabilities, and stock are used to

calculate these ratios. The current and quick ratios are the most important ratios (Lohaus and

Habermann, 2019).

Current Ratio = Current Assets/ Current Liabilities

= 84,349/ 37,928 = 2.22:1

Quick Ratio = (Current Assets- Stock)/ Current Liabilities

= (84,349 - 28571)/ 37,928 = 1.47:1

Interpretation: The aforementioned ratios provide information regarding the

company's liquidation status. The optimal current-to-quick ratio is 2:1, while the quick-to-

current ratio is 1:1. The current assets to liabilities ratio is 2.22, indicating that the business is

solvent. However, when deducting stock from current assets, the quick ratio remains at 1.47,

indicating that the company has enough cash to pay down its creditors and is doing so

successfully.

Section 4: Using examples from the case study describing and

discussing the processes this business might use to improve their

financial performance.

Since investors opt to invest in a company based on its financial performance,

financial performance is a life-sustaining feature of the firm. As a result, it's critical to make

the right financial judgments when it comes to funding options. Though, because the

company's existence and survival are dependent on earnings, wealth maximisation is the

primary priority. Financial ratios assist managers and financial organisations in making the

best decisions. Based on the computations, it has been determined that:

The current assets to current liabilities ratio has decreased by 82 percent from the

previous year, indicating that the company's cash outflow has increased and it is

losing liquidity.

Since non-operating costs such as administrative expenditures and interest have

decreased, the net profit has increased by 126.77 percent.

Customer satisfaction demonstrates that the company is investing more and

supporting its growth, resulting in a higher staff retention rate.

9

conclusion of the fiscal year to stay in business.

3. Liquidity Ratio: It assesses a company's capacity to meet its financial obligations and

also informs us about its solvency. Current assets, current liabilities, and stock are used to

calculate these ratios. The current and quick ratios are the most important ratios (Lohaus and

Habermann, 2019).

Current Ratio = Current Assets/ Current Liabilities

= 84,349/ 37,928 = 2.22:1

Quick Ratio = (Current Assets- Stock)/ Current Liabilities

= (84,349 - 28571)/ 37,928 = 1.47:1

Interpretation: The aforementioned ratios provide information regarding the

company's liquidation status. The optimal current-to-quick ratio is 2:1, while the quick-to-

current ratio is 1:1. The current assets to liabilities ratio is 2.22, indicating that the business is

solvent. However, when deducting stock from current assets, the quick ratio remains at 1.47,

indicating that the company has enough cash to pay down its creditors and is doing so

successfully.

Section 4: Using examples from the case study describing and

discussing the processes this business might use to improve their

financial performance.

Since investors opt to invest in a company based on its financial performance,

financial performance is a life-sustaining feature of the firm. As a result, it's critical to make

the right financial judgments when it comes to funding options. Though, because the

company's existence and survival are dependent on earnings, wealth maximisation is the

primary priority. Financial ratios assist managers and financial organisations in making the

best decisions. Based on the computations, it has been determined that:

The current assets to current liabilities ratio has decreased by 82 percent from the

previous year, indicating that the company's cash outflow has increased and it is

losing liquidity.

Since non-operating costs such as administrative expenditures and interest have

decreased, the net profit has increased by 126.77 percent.

Customer satisfaction demonstrates that the company is investing more and

supporting its growth, resulting in a higher staff retention rate.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assuming that shareholder equity is increasing, more shares are being sold, revenues

are increasing, and operational expenditures are decreasing.

Improvements that can be done are as follows:

Marketing tactics that may be used to improve the firm include lowering expenses and

making effective use of resources, both of which will help the company generate more

revenue. Presenting on social media, for example, is a better and less expensive means

of reaching the greatest number of people.

Utilization of resources effectively and efficiently, resulting in lower costs and higher

prices, as well as profit leveraging. It will also boost the company's production and

efficiency.

The leverage in working capital requirements may be demonstrated by lowering

inventory and improving inventory turnover.

Conclusion

The report concludes that financial management plays a critical role in the running of

the company. It manages finances, makes business choices, and reports on the profitability,

economic stability, and solvency of the company. The financial accounts are a summary of

the business. Every company must keep these records and have them audited by authorised

individuals both internally and externally. It tells all about the assets, liabilities, shareholder's

equity, profits, revenues, inflow and outflow of cash. Financial ratios help in analyzing the

solvency and the efficiency of the enterprise. Hence, from the above calculate ratios of the

case study, it is analyzed that the company is earning a high net profit but it can lower its

inventory cost which will help in increasing the revenues and also in the net earnings. It

contains information about the company's assets, liabilities, shareholder equity, earnings,

revenues, and cash inflow and outflow. Financial ratios aid in the analysis of a company's

solvency and efficiency. As a result of the case study's calculated ratios, it is determined that

the firm has a high net profit, but it can reduce its inventory costs, which will assist increase

revenues and net earnings.

10

are increasing, and operational expenditures are decreasing.

Improvements that can be done are as follows:

Marketing tactics that may be used to improve the firm include lowering expenses and

making effective use of resources, both of which will help the company generate more

revenue. Presenting on social media, for example, is a better and less expensive means

of reaching the greatest number of people.

Utilization of resources effectively and efficiently, resulting in lower costs and higher

prices, as well as profit leveraging. It will also boost the company's production and

efficiency.

The leverage in working capital requirements may be demonstrated by lowering

inventory and improving inventory turnover.

Conclusion

The report concludes that financial management plays a critical role in the running of

the company. It manages finances, makes business choices, and reports on the profitability,

economic stability, and solvency of the company. The financial accounts are a summary of

the business. Every company must keep these records and have them audited by authorised

individuals both internally and externally. It tells all about the assets, liabilities, shareholder's

equity, profits, revenues, inflow and outflow of cash. Financial ratios help in analyzing the

solvency and the efficiency of the enterprise. Hence, from the above calculate ratios of the

case study, it is analyzed that the company is earning a high net profit but it can lower its

inventory cost which will help in increasing the revenues and also in the net earnings. It

contains information about the company's assets, liabilities, shareholder equity, earnings,

revenues, and cash inflow and outflow. Financial ratios aid in the analysis of a company's

solvency and efficiency. As a result of the case study's calculated ratios, it is determined that

the firm has a high net profit, but it can reduce its inventory costs, which will assist increase

revenues and net earnings.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Ashley, R., Gersonius, B., Digman, C., Horton, B., Smith, B. and Shaffer, P., 2018. Including

uncertainty in valuing blue and green infrastructure for stormwater

management. Ecosystem services, 33, pp.237-246.

Bano, C., Coffey, D., Al Tawil, K., Karuppaiah, K., Tavakkolizadeh, A., Rose, V.,

Tahmassebi, R. and Colegate-Stone, T., 2021. Management of Open Elbow

Fractures-The Experiences and Outcomes from a UK Major Trauma Centre. Journal

of Shoulder and Elbow Surgery.

Black, K., 2019. Business statistics: for contemporary decision making. John Wiley & Sons.

Büyüközkan, G., Göçer, F. and Karabulut, Y., 2019. A new group decision making approach

with IF AHP and IF VIKOR for selecting hazardous waste

carriers. Measurement, 134, pp.66-82.

Chai, J. and Ngai, E.W., 2020. Decision-making techniques in supplier selection: Recent

accomplishments and what lies ahead. Expert Systems with Applications, 140,

p.112903.

Goodwin, N., Stein, V. and Amelung, V., 2021. What is integrated care?. In Handbook

integrated care (pp. 3-25). Springer, Cham.

Littlechild, S., 2018. Economic regulation of privatised airports: some lessons from UK

experience. Transportation Research Part A: Policy and Practice, 114, pp.100-114.

Lohaus, D. and Habermann, W., 2019. Presenteeism: A review and research

directions. Human Resource Management Review, 29(1), pp.43-58.

11

Ashley, R., Gersonius, B., Digman, C., Horton, B., Smith, B. and Shaffer, P., 2018. Including

uncertainty in valuing blue and green infrastructure for stormwater

management. Ecosystem services, 33, pp.237-246.

Bano, C., Coffey, D., Al Tawil, K., Karuppaiah, K., Tavakkolizadeh, A., Rose, V.,

Tahmassebi, R. and Colegate-Stone, T., 2021. Management of Open Elbow

Fractures-The Experiences and Outcomes from a UK Major Trauma Centre. Journal

of Shoulder and Elbow Surgery.

Black, K., 2019. Business statistics: for contemporary decision making. John Wiley & Sons.

Büyüközkan, G., Göçer, F. and Karabulut, Y., 2019. A new group decision making approach

with IF AHP and IF VIKOR for selecting hazardous waste

carriers. Measurement, 134, pp.66-82.

Chai, J. and Ngai, E.W., 2020. Decision-making techniques in supplier selection: Recent

accomplishments and what lies ahead. Expert Systems with Applications, 140,

p.112903.

Goodwin, N., Stein, V. and Amelung, V., 2021. What is integrated care?. In Handbook

integrated care (pp. 3-25). Springer, Cham.

Littlechild, S., 2018. Economic regulation of privatised airports: some lessons from UK

experience. Transportation Research Part A: Policy and Practice, 114, pp.100-114.

Lohaus, D. and Habermann, W., 2019. Presenteeism: A review and research

directions. Human Resource Management Review, 29(1), pp.43-58.

11

Shapiro, A.C. and Hanouna, P., 2019. Multinational financial management. John Wiley &

Sons.

Treviño, L.J. and Doh, J.P., 2021. Internationalization of the firm: A discourse-based

view. Journal of International Business Studies, 52(7), pp.1375-1393.

Zachariadis, M., Hileman, G. and Scott, S.V., 2019. Governance and control in distributed

ledgers: Understanding the challenges facing blockchain technology in financial

services. Information and Organization, 29(2), pp.105-117.

12

Sons.

Treviño, L.J. and Doh, J.P., 2021. Internationalization of the firm: A discourse-based

view. Journal of International Business Studies, 52(7), pp.1375-1393.

Zachariadis, M., Hileman, G. and Scott, S.V., 2019. Governance and control in distributed

ledgers: Understanding the challenges facing blockchain technology in financial

services. Information and Organization, 29(2), pp.105-117.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.