BSc Hons Business Management: Applied Finance & Performance Review

VerifiedAdded on 2023/06/14

|16

|3001

|194

Report

AI Summary

This report provides a comprehensive analysis of financial management concepts and their importance in enhancing business performance. It delves into the main financial statements, including the income statement, balance sheet, and cash flow statement, and explains the application of ratios in financial management. Using a provided template and a case study, the report calculates key financial indicators, constructs an income statement and balance sheet in Excel, and interprets the profitability, liquidity, and efficiency of the company through ratio analysis. Furthermore, it discusses processes the business might use to improve its financial performance, drawing on examples from the case study. The report concludes by summarizing the key findings and recommendations for improved financial management.

BSc (Hons) Business Management with Foundation

BMP3005

Applied Business Finance

The concept and importance of financial

management and the processes businesses

might use to improve their financial

performance

1

BMP3005

Applied Business Finance

The concept and importance of financial

management and the processes businesses

might use to improve their financial

performance

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

Introduction 3

Section 1: Definition and discussion of the concept and

importance of financial management 3

Section 2: Description and discussion of the main financial

statements and explain the use of ratios in financial management

4

Section 3: Using the template provided 5-9

i. Completing the Information on the ‘Business Review Template

(Ensure that you display your calculations for this detail)

5

ii. Using Excel producing an Income Statement for the Sample

Organisation (see Case Study). This should be included within your

appendices 6

iii. Using Excel completing the Balance Sheet 7

iv. Using the Case study information describing the profitability,

liquidity and efficiency of the company based on the results of ratio

analysis 8

3

Introduction 3

Section 1: Definition and discussion of the concept and

importance of financial management 3

Section 2: Description and discussion of the main financial

statements and explain the use of ratios in financial management

4

Section 3: Using the template provided 5-9

i. Completing the Information on the ‘Business Review Template

(Ensure that you display your calculations for this detail)

5

ii. Using Excel producing an Income Statement for the Sample

Organisation (see Case Study). This should be included within your

appendices 6

iii. Using Excel completing the Balance Sheet 7

iv. Using the Case study information describing the profitability,

liquidity and efficiency of the company based on the results of ratio

analysis 8

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section 4: Using examples from the case study describing and

discussing the processes this business might use to improve their

financial performance 9

Conclusion 10

References 11

Appendix 13

4

discussing the processes this business might use to improve their

financial performance 9

Conclusion 10

References 11

Appendix 13

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

Financial management is basically meant by managing and regulating financial

activities and practices in an organisation. For instance, it is considered as backbone of the

organisation as it undertakes necessary financial aspects and factors in order to regulate them

in an efficient manner. It involves various practices including raising funds from available

sources as well as efficient allocation of these funds in order to ensure maximum profitability

and productivity. This report assessment will be comprised of information and knowledge of

financial management and various elements and components it is comprised of

(Franceschelli, Santoro and Candelo, 2018). The procedure of financial management includes

planning, organising, directing, and controlling of financial practices in order to facilitate

financial stability in the organisation. This report assessment will be including concepts of

ratios and financial statements in order to determine financial position of the respective

organisation. Furthermore, interpretation of analysis will be provided on the basis of

mentioned case study in order to facilitate efficient understanding (Aouadi and Marsat, 2018).

Section 1: Definition and discussion of the concept and

importance of financial management

Financial management is determined as a concept of managing and controlling

financial aspects regulating in an organisation. The procedure of financial management

involves planning, organising, controlling, and directing of financial aspects and factors in

order to enhance financial stability and profitability. For instance, primary function of

financial management is to raise funds from available sources and allocation of funds in most

beneficial manner. These funds facilitates in carrying out operations and activities in a

workplace. Financial management is determined at various aims and objectives which are as

follows (Freudenreich, Lüdeke-Freund and Schaltegger, 2020):

Maximising profits: The activities and operations carried out in financial

management are aimed at maximising profits with determination and consideration of

most suitable options available. It ensures most beneficial investment by company in

order to acquire maximum profits out of it.

Cost minimising: Financial management facilitates in efficient utilisation of funds in

order to promote minimum cost incurred to organisation in carrying out activities and

operations. Moreover, strategies are developed and executed in order to reduce cost of

production.

5

Financial management is basically meant by managing and regulating financial

activities and practices in an organisation. For instance, it is considered as backbone of the

organisation as it undertakes necessary financial aspects and factors in order to regulate them

in an efficient manner. It involves various practices including raising funds from available

sources as well as efficient allocation of these funds in order to ensure maximum profitability

and productivity. This report assessment will be comprised of information and knowledge of

financial management and various elements and components it is comprised of

(Franceschelli, Santoro and Candelo, 2018). The procedure of financial management includes

planning, organising, directing, and controlling of financial practices in order to facilitate

financial stability in the organisation. This report assessment will be including concepts of

ratios and financial statements in order to determine financial position of the respective

organisation. Furthermore, interpretation of analysis will be provided on the basis of

mentioned case study in order to facilitate efficient understanding (Aouadi and Marsat, 2018).

Section 1: Definition and discussion of the concept and

importance of financial management

Financial management is determined as a concept of managing and controlling

financial aspects regulating in an organisation. The procedure of financial management

involves planning, organising, controlling, and directing of financial aspects and factors in

order to enhance financial stability and profitability. For instance, primary function of

financial management is to raise funds from available sources and allocation of funds in most

beneficial manner. These funds facilitates in carrying out operations and activities in a

workplace. Financial management is determined at various aims and objectives which are as

follows (Freudenreich, Lüdeke-Freund and Schaltegger, 2020):

Maximising profits: The activities and operations carried out in financial

management are aimed at maximising profits with determination and consideration of

most suitable options available. It ensures most beneficial investment by company in

order to acquire maximum profits out of it.

Cost minimising: Financial management facilitates in efficient utilisation of funds in

order to promote minimum cost incurred to organisation in carrying out activities and

operations. Moreover, strategies are developed and executed in order to reduce cost of

production.

5

Reducing risk: Accumulating information and analysis of acquired information and

knowledge allows company in being ready for future circumstances as well as

reducing risk to minimum possible extent.

Importance of Financial Management:

Financial Planning: Financial management facilitates in efficient financial planning

in an organisation. For instance, it enables company's management in determining

and fulfilling financial needs and requirements of organisation in order to carry out

activities and operations. Moreover, it involves strategic planning with consideration

of various financial factors and aspects in order to execute these strategies in a

organised and efficient manner.

Allocation of funds: This is basically meant by use of funds or investment of these

acquired funds in order to ensure maximum profitability from these investments.

Furthermore, efficient allocation of funds results in minimising cost incurred to

business as well as acquiring maximum benefits out of it. Therefore, in order to

acquire these benefits, there is a necessity of implementing financial management.

Investment opportunities: Efficient financial management practices and activities

facilitates in conquering investment opportunities. For instance, with consideration

and prior preparation of future circumstances, management of companies could

vanquish future opportunities for investment. Furthermore, in order to conquer these

investment opportunities, financial management has to implemented in an

organisation.

Financial stability: Financial management plays a crucial role in providing financial

stability to organisation in order to carry out activities and operations. Moreover,

consideration of various aspects and factors in financial management reduces the

chances of risk and losses to organisation which results in providing financial

stability to business organisation. Furthermore, financial stability of organisation

directly leads to economic growth and stability in an economic nation (Hermes,

Lensink and Meesters, 2018).

Section 2: Description and discussion of the main financial

statements and explain the use of ratios in financial management

Financial statement is meant by records of financial practices and operations carried

out in an business entity. This formal record of financial aspects determine current financial

6

knowledge allows company in being ready for future circumstances as well as

reducing risk to minimum possible extent.

Importance of Financial Management:

Financial Planning: Financial management facilitates in efficient financial planning

in an organisation. For instance, it enables company's management in determining

and fulfilling financial needs and requirements of organisation in order to carry out

activities and operations. Moreover, it involves strategic planning with consideration

of various financial factors and aspects in order to execute these strategies in a

organised and efficient manner.

Allocation of funds: This is basically meant by use of funds or investment of these

acquired funds in order to ensure maximum profitability from these investments.

Furthermore, efficient allocation of funds results in minimising cost incurred to

business as well as acquiring maximum benefits out of it. Therefore, in order to

acquire these benefits, there is a necessity of implementing financial management.

Investment opportunities: Efficient financial management practices and activities

facilitates in conquering investment opportunities. For instance, with consideration

and prior preparation of future circumstances, management of companies could

vanquish future opportunities for investment. Furthermore, in order to conquer these

investment opportunities, financial management has to implemented in an

organisation.

Financial stability: Financial management plays a crucial role in providing financial

stability to organisation in order to carry out activities and operations. Moreover,

consideration of various aspects and factors in financial management reduces the

chances of risk and losses to organisation which results in providing financial

stability to business organisation. Furthermore, financial stability of organisation

directly leads to economic growth and stability in an economic nation (Hermes,

Lensink and Meesters, 2018).

Section 2: Description and discussion of the main financial

statements and explain the use of ratios in financial management

Financial statement is meant by records of financial practices and operations carried

out in an business entity. This formal record of financial aspects determine current financial

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

components in an organisation including assets, owner's equity, and liabilities. It includes

various financial records such as balance sheet, income statement, cash flow statement, etc.

All these financial records determine financial position and stability of business organisation

with consideration of various financial aspects. These financial statements are taken into

consideration by government in order to audit upon various aspects including tax, finance,

investment, etc. There are various financial records included in financial statements, major of

them are as follows (Jackson, 2019):

Profit and loss statement: It is meant by representation of analysed financial aspects

in order to provide an efficient understanding. For instance, it includes costs, revenue,

expenses, incurred to business organisation in an financial year or a defined duration

of time. Moreover, it conclusively determines overall profit or loss incurred to

company by carrying out operations and activities. This is one of the major and

primary financial record or statement issues by business entities at the end of every

financial year. Furthermore, profit and loss statement are analysed and prepared for

representation with consideration of monetary as well as accrual methods of

accounting.

Balance sheet: A balance sheet is a financial statement that determines records of

various financial aspects. For instance, it includes aspects such as assets of company,

liabilities of company, and shareholder's equity. This financial record basically

determines as Assets is equals to sum of liabilities and shareholder's equity.

Moreover, this financial statements considers interpretation of analysed current

balance of assets, liabilities, and shareholder's equity. Furthermore, if the amount of

cash is not equal to sum of liabilities and shareholder's equity, then there must be an

error or any element not taken into consideration. Therefore, corrective measures are

initiated in order to interpret appropriate financial records.

Cash Flow statement: This financial statement includes recording financial aspects

of cash and cash equivalents. For instance, it determines amount of cash and cash

equivalents acquired by an organisation as well as paid by company. This financial

statement also determines performance of company in terms of financial perspectives

over a particular period of time. Moreover, it involves representation of fluctuation in

cash and cash equivalents in investment, operations, and financial practices over a

defined period of time. Therefore, it includes interpretation of cash inflow and

outflow with reference to business organisation (Jones and et. al., 2018).

Uses of ratios in Financial management:

7

various financial records such as balance sheet, income statement, cash flow statement, etc.

All these financial records determine financial position and stability of business organisation

with consideration of various financial aspects. These financial statements are taken into

consideration by government in order to audit upon various aspects including tax, finance,

investment, etc. There are various financial records included in financial statements, major of

them are as follows (Jackson, 2019):

Profit and loss statement: It is meant by representation of analysed financial aspects

in order to provide an efficient understanding. For instance, it includes costs, revenue,

expenses, incurred to business organisation in an financial year or a defined duration

of time. Moreover, it conclusively determines overall profit or loss incurred to

company by carrying out operations and activities. This is one of the major and

primary financial record or statement issues by business entities at the end of every

financial year. Furthermore, profit and loss statement are analysed and prepared for

representation with consideration of monetary as well as accrual methods of

accounting.

Balance sheet: A balance sheet is a financial statement that determines records of

various financial aspects. For instance, it includes aspects such as assets of company,

liabilities of company, and shareholder's equity. This financial record basically

determines as Assets is equals to sum of liabilities and shareholder's equity.

Moreover, this financial statements considers interpretation of analysed current

balance of assets, liabilities, and shareholder's equity. Furthermore, if the amount of

cash is not equal to sum of liabilities and shareholder's equity, then there must be an

error or any element not taken into consideration. Therefore, corrective measures are

initiated in order to interpret appropriate financial records.

Cash Flow statement: This financial statement includes recording financial aspects

of cash and cash equivalents. For instance, it determines amount of cash and cash

equivalents acquired by an organisation as well as paid by company. This financial

statement also determines performance of company in terms of financial perspectives

over a particular period of time. Moreover, it involves representation of fluctuation in

cash and cash equivalents in investment, operations, and financial practices over a

defined period of time. Therefore, it includes interpretation of cash inflow and

outflow with reference to business organisation (Jones and et. al., 2018).

Uses of ratios in Financial management:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ratio are comparison units used to determine comparison of various factors and

aspects. For instance, it is meant by measurement of two or more components and

determining their relationship among each other in order to provide efficient understanding.

Ratios are often used in financial management in facilitating efficient understanding of

current financial position of business entity as well as supports in decision-making practices

in financial management. Furthermore, it involves various ratios in order to facilitate efficient

understanding of financial information of several aspects and factors (Yunis, Tarhini and

Kassar, 2018). There are various uses of ratios in financial management which are as follows:

Efficient comparison: Ratios are primarily used in financial management in order to

compare various elements or components of finance over time or among each other.

For instance, it determines proportion or amount of element with reference to another

defined financial element. Moreover, it facilitates in identification and determination

of financial performance of business organisation in order to determine if productivity

of an business organisation is increasing or degrading over time. Furthermore, it also

comparison as well as understanding of the same among different elements and

components in finance.

Trend Line: Trend line is determined as graphical representation of information or

data in order to understand the flow of resulting outcome. Ratios facilitates in

interpretation of financial performance in the form of trend line with analysis and

recording these outcomes of analysis. For instance, it shows financial performance

over defined period of time (Jung, Herbohn and Clarkson, 2018).

Operational efficiency: It is meant by representation of efficiency of an

organisation's management with comparing overall operating expense. For instance, it

determines how efficient is management of particular company in keeping lower cost

and acquiring higher profits. Furthermore, ratios used to determine operational

efficiency include asset turnover ratio, receivables turnover ratio, and inventory

turnover ratio (Lai, Sun and Ren, 2018).

Section 3: Using the template provided:

v. Completing the Information on the ‘Business Review Template

(Ensure that you display your calculations for this detail)

8

aspects. For instance, it is meant by measurement of two or more components and

determining their relationship among each other in order to provide efficient understanding.

Ratios are often used in financial management in facilitating efficient understanding of

current financial position of business entity as well as supports in decision-making practices

in financial management. Furthermore, it involves various ratios in order to facilitate efficient

understanding of financial information of several aspects and factors (Yunis, Tarhini and

Kassar, 2018). There are various uses of ratios in financial management which are as follows:

Efficient comparison: Ratios are primarily used in financial management in order to

compare various elements or components of finance over time or among each other.

For instance, it determines proportion or amount of element with reference to another

defined financial element. Moreover, it facilitates in identification and determination

of financial performance of business organisation in order to determine if productivity

of an business organisation is increasing or degrading over time. Furthermore, it also

comparison as well as understanding of the same among different elements and

components in finance.

Trend Line: Trend line is determined as graphical representation of information or

data in order to understand the flow of resulting outcome. Ratios facilitates in

interpretation of financial performance in the form of trend line with analysis and

recording these outcomes of analysis. For instance, it shows financial performance

over defined period of time (Jung, Herbohn and Clarkson, 2018).

Operational efficiency: It is meant by representation of efficiency of an

organisation's management with comparing overall operating expense. For instance, it

determines how efficient is management of particular company in keeping lower cost

and acquiring higher profits. Furthermore, ratios used to determine operational

efficiency include asset turnover ratio, receivables turnover ratio, and inventory

turnover ratio (Lai, Sun and Ren, 2018).

Section 3: Using the template provided:

v. Completing the Information on the ‘Business Review Template

(Ensure that you display your calculations for this detail)

8

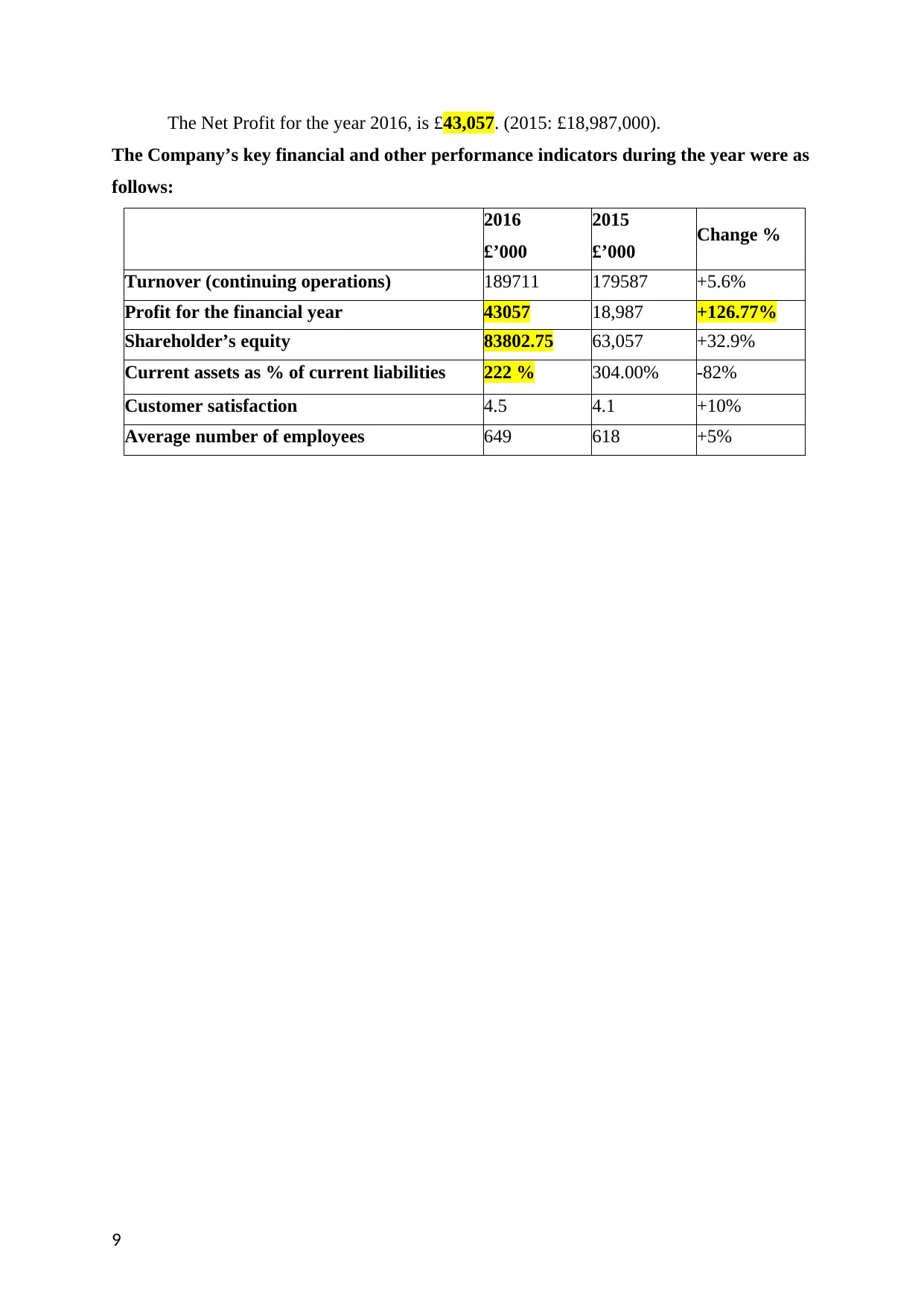

The Net Profit for the year 2016, is £43,057. (2015: £18,987,000).

The Company’s key financial and other performance indicators during the year were as

follows:

2016

£’000

2015

£’000 Change %

Turnover (continuing operations) 189711 179587 +5.6%

Profit for the financial year 43057 18,987 +126.77%

Shareholder’s equity 83802.75 63,057 +32.9%

Current assets as % of current liabilities 222 % 304.00% -82%

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

9

The Company’s key financial and other performance indicators during the year were as

follows:

2016

£’000

2015

£’000 Change %

Turnover (continuing operations) 189711 179587 +5.6%

Profit for the financial year 43057 18,987 +126.77%

Shareholder’s equity 83802.75 63,057 +32.9%

Current assets as % of current liabilities 222 % 304.00% -82%

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The turnover of the company increased by 5.6% due to operations.

Gross Profit = £81,125

Net Profit = £43057

Increase in net profits in the year 2016 was of 126.77%.

Increase in Shareholders equity was of 32.9% by £20,745.75.

The Quick ratio is 1.47:1

Current ratio is 2.22: 1.

(The appendix represents the respective calculation)

vi. Using Excel producing an Income Statement for the Sample

Organisation (see Case Study

(The appendix represents the respective calculation)

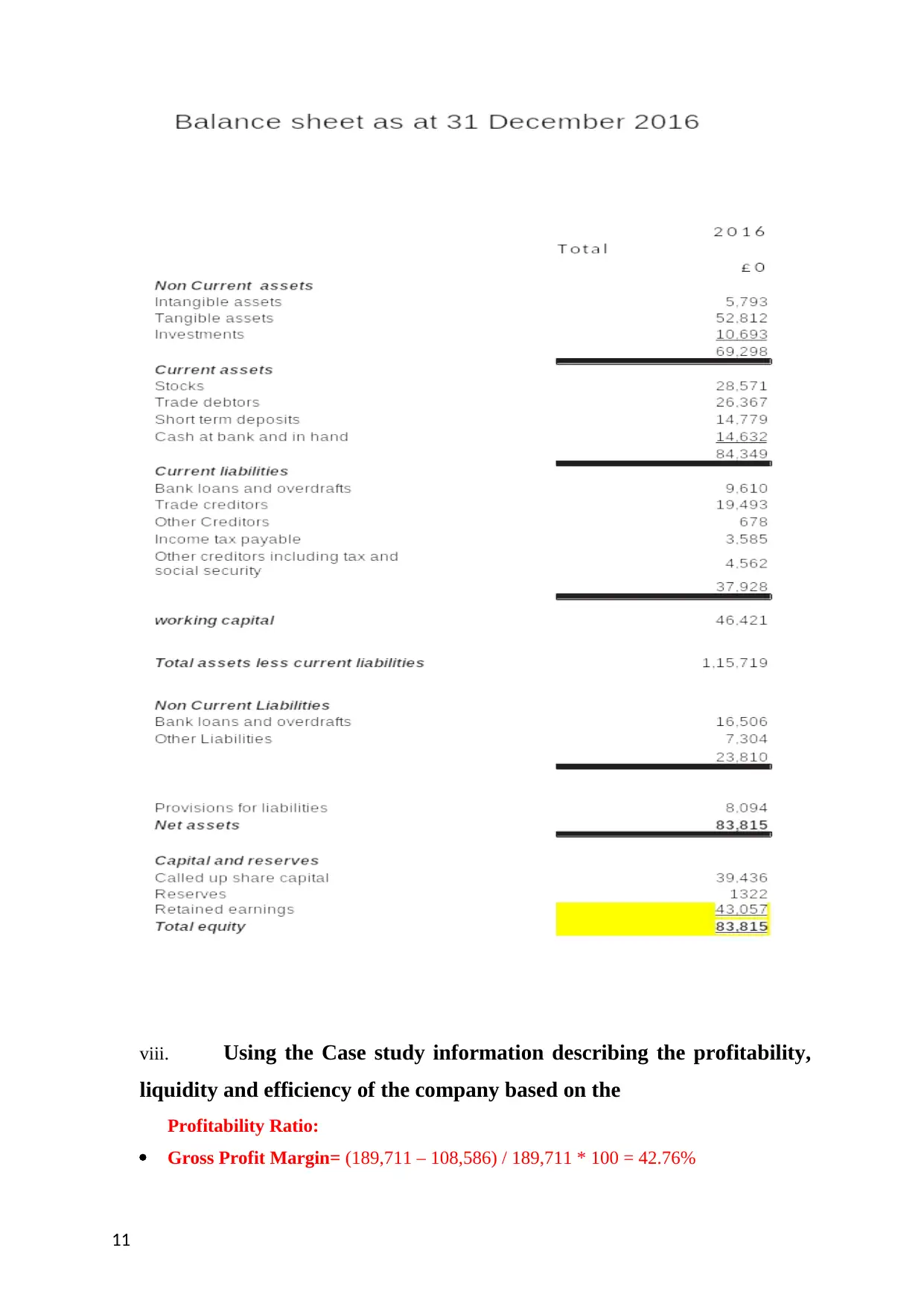

vii. Using Excel completing the Balance Sheet

10

Gross Profit = £81,125

Net Profit = £43057

Increase in net profits in the year 2016 was of 126.77%.

Increase in Shareholders equity was of 32.9% by £20,745.75.

The Quick ratio is 1.47:1

Current ratio is 2.22: 1.

(The appendix represents the respective calculation)

vi. Using Excel producing an Income Statement for the Sample

Organisation (see Case Study

(The appendix represents the respective calculation)

vii. Using Excel completing the Balance Sheet

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

viii. Using the Case study information describing the profitability,

liquidity and efficiency of the company based on the

Profitability Ratio:

Gross Profit Margin= (189,711 – 108,586) / 189,711 * 100 = 42.76%

11

liquidity and efficiency of the company based on the

Profitability Ratio:

Gross Profit Margin= (189,711 – 108,586) / 189,711 * 100 = 42.76%

11

Net Profit Margin = (43,057/189,711) * 100 = 22.70%

Interpretation: The above analysis determines profit percentage with reference to

revenue considering operating as well as non-operating expenses. Gross-profit has been

resulted at 42.76% whereas net gain is determined at 22.7. For instance, it shows that profit is

reducing by an approximate of 20%.

2. Efficiency Ratio:

Asset turnover Ratio= 189,711/153,647 = 1.23

Stock Turnover Ratio = (108,586/28,571) = 3.8

Accounts receivable Days = 365/ 7.19 = 50.77 days

Accounts Payable Days = 365/7.04 = 51.84 days

Interpretation: It determines that that average duration of debt paid by customers is

51 days and creditors are receiving payments in 52 days. Inventory turnover is resulted at 3.8

that means investment of stock flows 4 times in a financial year. Total assets turnover is

determined at 1.23.

3. Liquidity Ratio:

Current Ratio = 84,349/ 37,928 = 2.22:1

Quick Ratio = (84,349 - 28571)/ 37,928 = 1.47:1

Interpretation: The above calculation determines that current ratio being 2:1 whereas

quick ratio is 1:1. For instance, ratio of current assets to liability is 2.22, which shows that

company is solvent.

Section 4: Using examples from the case study describing and

discussing the processes this business might use to improve their

financial performance.

Financial Performance is meant by measure of how efficiently an business entity

uses assets in order to acquire revenue and profit out of it. From the calculations performed, it

has been evaluated that (Kaydos, 2020):

Current assets of the entity have reduced by 82% in comparison to the previous year.

Net profit has been observed to increase by 126.77% which was the impact of non

operating profits.

The increase in shareholders equity can result in influencing and growing selling rate

of shares which will rise in revenue generation and the operating expenses can be

reduced.

12

Interpretation: The above analysis determines profit percentage with reference to

revenue considering operating as well as non-operating expenses. Gross-profit has been

resulted at 42.76% whereas net gain is determined at 22.7. For instance, it shows that profit is

reducing by an approximate of 20%.

2. Efficiency Ratio:

Asset turnover Ratio= 189,711/153,647 = 1.23

Stock Turnover Ratio = (108,586/28,571) = 3.8

Accounts receivable Days = 365/ 7.19 = 50.77 days

Accounts Payable Days = 365/7.04 = 51.84 days

Interpretation: It determines that that average duration of debt paid by customers is

51 days and creditors are receiving payments in 52 days. Inventory turnover is resulted at 3.8

that means investment of stock flows 4 times in a financial year. Total assets turnover is

determined at 1.23.

3. Liquidity Ratio:

Current Ratio = 84,349/ 37,928 = 2.22:1

Quick Ratio = (84,349 - 28571)/ 37,928 = 1.47:1

Interpretation: The above calculation determines that current ratio being 2:1 whereas

quick ratio is 1:1. For instance, ratio of current assets to liability is 2.22, which shows that

company is solvent.

Section 4: Using examples from the case study describing and

discussing the processes this business might use to improve their

financial performance.

Financial Performance is meant by measure of how efficiently an business entity

uses assets in order to acquire revenue and profit out of it. From the calculations performed, it

has been evaluated that (Kaydos, 2020):

Current assets of the entity have reduced by 82% in comparison to the previous year.

Net profit has been observed to increase by 126.77% which was the impact of non

operating profits.

The increase in shareholders equity can result in influencing and growing selling rate

of shares which will rise in revenue generation and the operating expenses can be

reduced.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.